© SBM Offshore 2015. All rights reserved. www.sbmoffshore.com

SBM Brasil, 2016

© SBM Offshore 2014. All rights reserved. www.sbmoffshore.com

SBM Brasil Presentation

Oil & Gas day - FEIMEC

© SBM Offshore 2015. All rights reserved. www.sbmoffshore.com

5/25/2016

Oil & Gas Today

© SBM Offshore 2015. All rights reserved. www.sbmoffshore.com 45/25/2016

11th and 12 th

Rounds

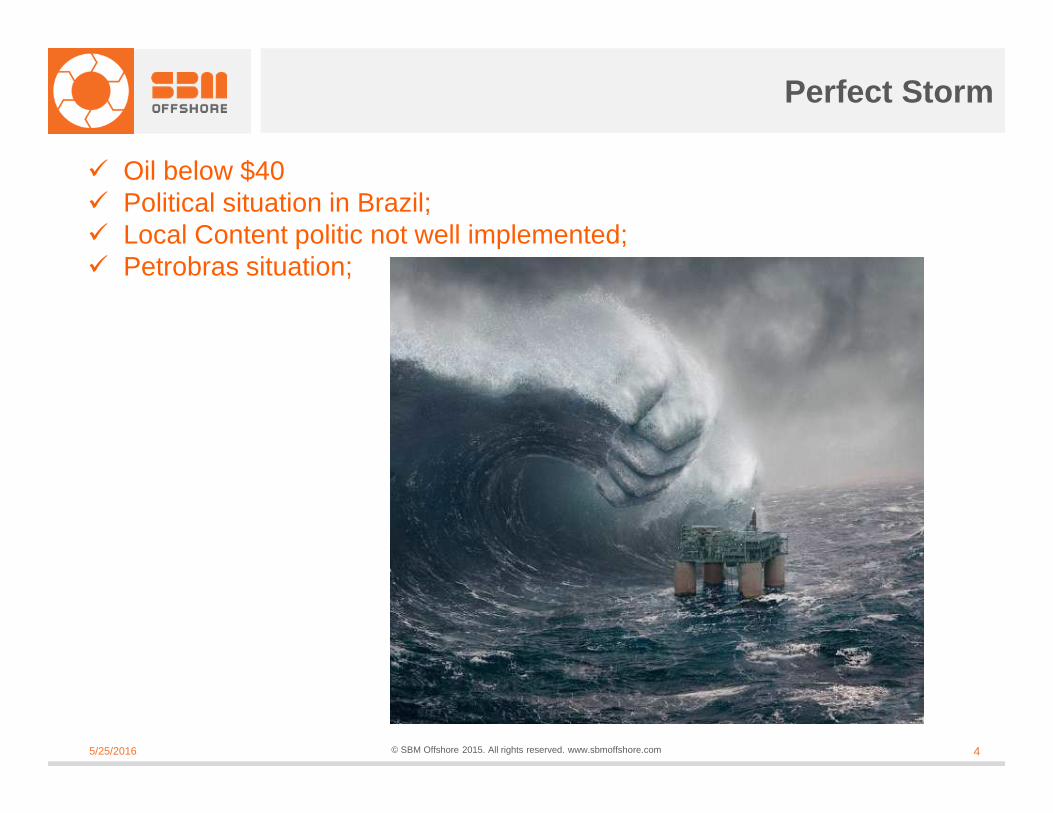

Perfect Storm

� Oil below $40� Political situation in Brazil;� Local Content politic not well implemented;� Petrobras situation;

© SBM Offshore 2015. All rights reserved. www.sbmoffshore.com 55/25/2016

11th and 12 th

Rounds

� Low oil prices reduces field feasibility

Oil price has seriously deteriorated

© SBM Offshore 2015. All rights reserved. www.sbmoffshore.com 65/25/2016

11th and 12 th

Rounds

Actual Scenario

� Upstream capex inflation has raise faster than oil making field development.

© SBM Offshore 2015. All rights reserved. www.sbmoffshore.com

5/25/2016

What if…

© SBM Offshore 2015. All rights reserved. www.sbmoffshore.com 85/25/2016

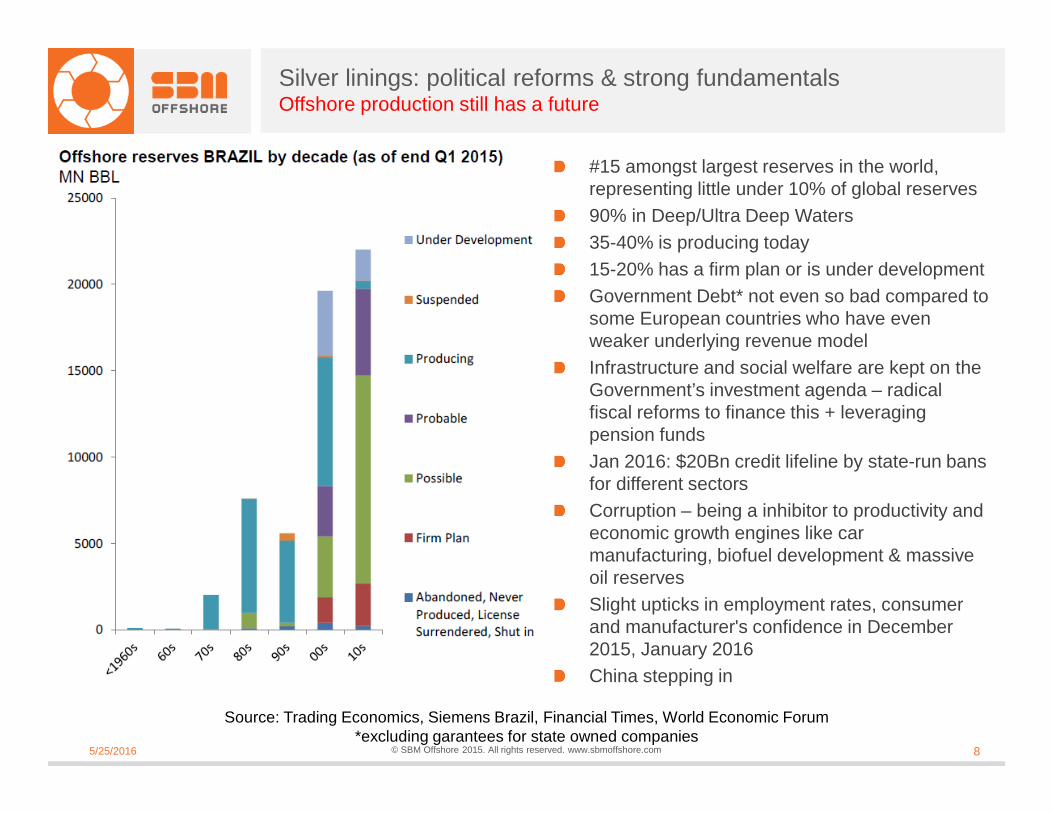

Silver linings: political reforms & strong fundamentalsOffshore production still has a future

#15 amongst largest reserves in the world, representing little under 10% of global reserves90% in Deep/Ultra Deep Waters35-40% is producing today15-20% has a firm plan or is under developmentGovernment Debt* not even so bad compared to some European countries who have even weaker underlying revenue modelInfrastructure and social welfare are kept on the Government’s investment agenda – radical fiscal reforms to finance this + leveraging pension fundsJan 2016: $20Bn credit lifeline by state-run bans for different sectorsCorruption – being a inhibitor to productivity and economic growth engines like car manufacturing, biofuel development & massive oil reservesSlight upticks in employment rates, consumer and manufacturer's confidence in December 2015, January 2016China stepping in

Source: Trading Economics, Siemens Brazil, Financial Times, World Economic Forum *excluding garantees for state owned companies

© SBM Offshore 2015. All rights reserved. www.sbmoffshore.com 95/25/2016

Liquids: a supply and demand rebalance expected in 2018

© SBM Offshore 2015. All rights reserved. www.sbmoffshore.com 105/25/2016

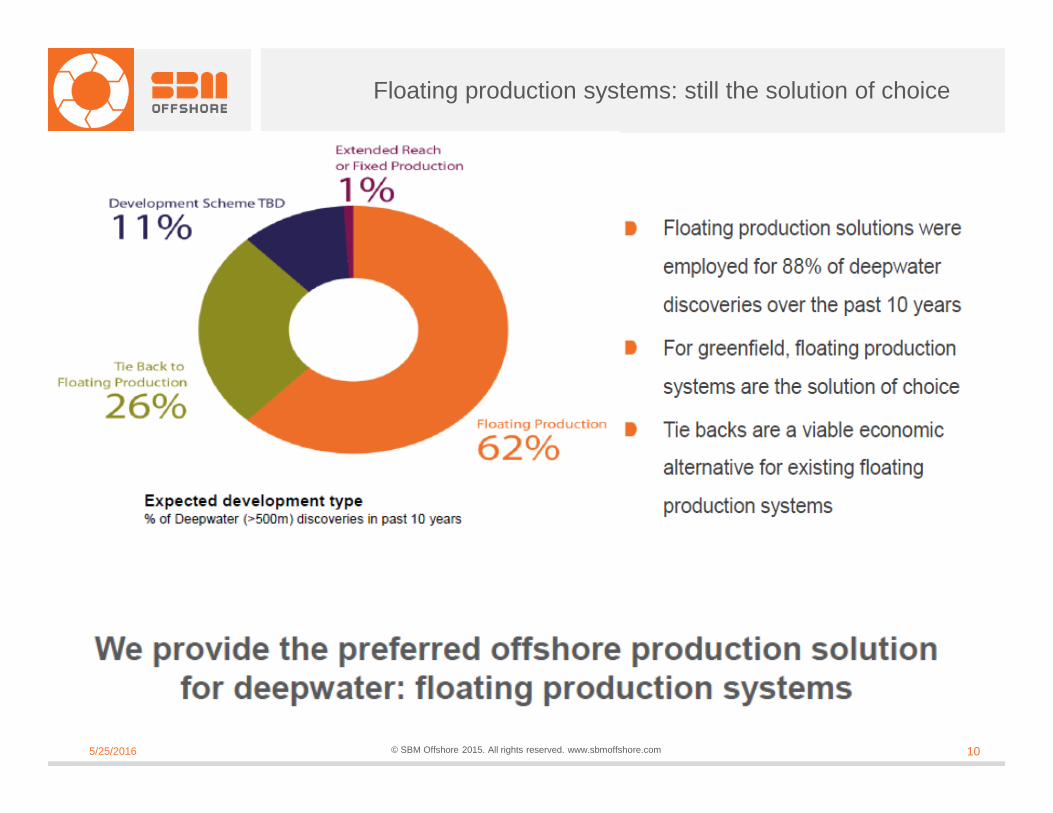

Floating production systems: still the solution of choice

© SBM Offshore 2015. All rights reserved. www.sbmoffshore.com 115/25/2016

Despite downturn, still main Worldwide FPSO MarketExpected FPSO Awards – Next 3 years

11

Non-Petrobras

at least 2 FPSO

awards within the

next 3 years

at least 2 FPSO Awards

within the next 3 years

+

FPSOPROJECTS TO BE AWARDED

***conservative view***

?

2014 – 2019 2015 – 2020

$220bi $98bi

Petrobras 5yr Business Plan – Total CAPEX

US$ 80biE&P

Libra P1Sépia

Marlim 1Búzios 5

Lula OesteSergipe

Esp. Santo

AtlantaKangaroo

Pão de AçúcarGato do Mato

XereleteWahoo

© SBM Offshore 2015. All rights reserved. www.sbmoffshore.com

5/25/2016

SBM Vision 2025

© SBM Offshore 2015. All rights reserved. www.sbmoffshore.com 135/25/2016

Building our future… through our Achievements!!

© SBM Offshore 2015. All rights reserved. www.sbmoffshore.com 145/25/2016

11th and 12 th

Rounds

Preparing today… for tomorrow… and beyond...

� Product life cycle� Retain talents

© SBM Offshore 2015. All rights reserved. www.sbmoffshore.com 155/25/2016

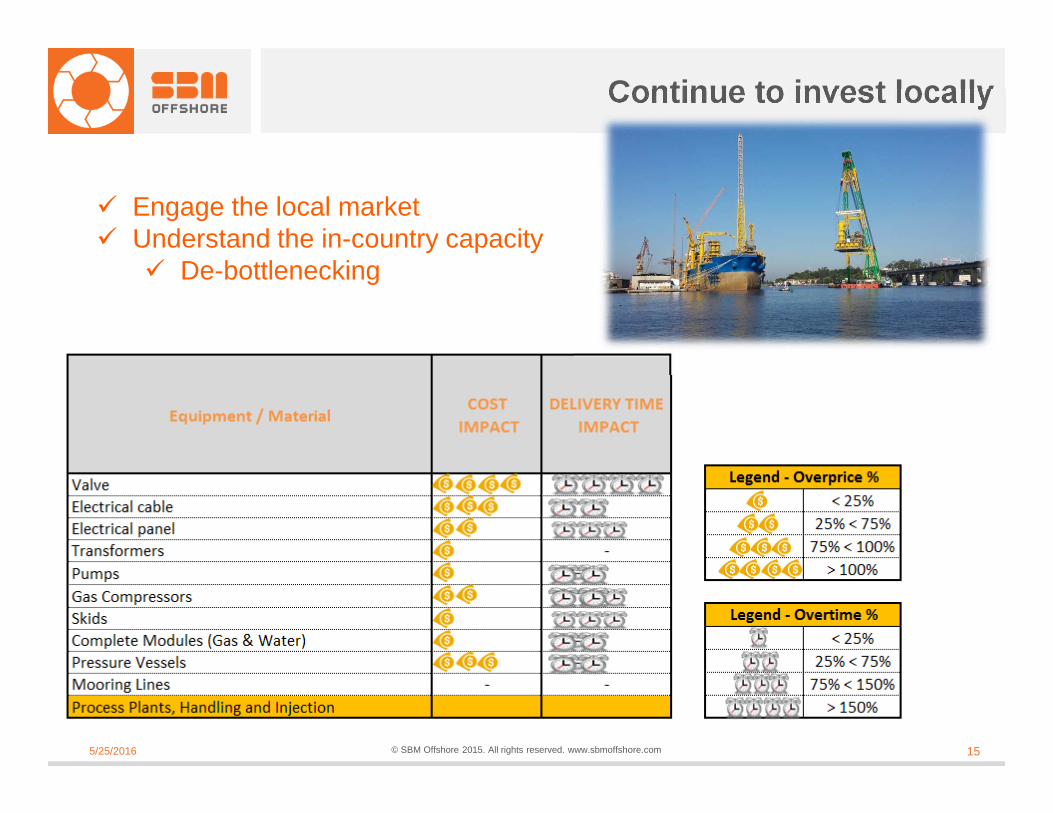

Continue to invest locally

� Engage the local market� Understand the in-country capacity

� De-bottlenecking

© SBM Offshore 2015. All rights reserved. www.sbmoffshore.com 165/25/2016

We Do Believe…

International competitiveness

International competitiveness

Long term investment

Support the country to develop the industry and people

Know-how/competitive advantage to attend LC requirements

Local suppliers frame work agreements

© SBM Offshore 2015. All rights reserved. www.sbmoffshore.com 185/25/2016

SBM Lease Fleet Portfolio

CANADA End date of LeaseExcluding extension options

MOPU – Deep Panuke Up to 2021

USA End date of LeaseExcluding extension options

Semi-Sub –Thunder Hawk Up to 2025

FPSO – Turritela Up to 2025

BRAZIL End date of LeaseExcluding extension options

FPSO – Marlim Sul (demob) Up to 2015

FPSO – Espírito Santo Up to 2024

FPSO – Capixaba Up to 2022

FPSO – Cidade de Anchieta Up to 2030

FPSO – Cidade de Paraty Up to 2033

FPSO – Cidade de Ilhabela Up to 2034

FPSO – Cidade de Maricá Up to 2035

FPSO – Cidade de Squarema Up to 2035

FPSO – Frade Turn-key

FPSO – P-57 Turn-key

FPSO – OSX-2 Turn-key

MYANMAR End date of LeaseExcluding extension options

FSO – Yetagun Up to 2018

MALAYSIA End date of LeaseExcluding extension options

FSO – Kikeh Up to 2022

EQUATORIAL GUINEA End date of LeaseExcluding extension options

FSO – Aseng Up to 2026

CONGO End date of LeaseExcluding extension options

LPG – Nkossa II Up to 2018

ANGOLA End date of LeaseExcluding extension options

FPSO – Mondo Up to 2022

FPSO – Saxi Batuque Up to 2023

FPSO – N’Goma Up tp 2026

Under Construction Lease in Operation Turn-Key (exclusively in Brazil

FPSO – Falcon

FPSO – Brasil

Turn-key projects specifically for Brazil

14 FPSOs, 2 FSOs, 1 Semi-Sub, 1 MOPU – 248 years of operations

Average remaining lease duration: 14.5 years

Laid Up

![121105 - Apresentação 3Q12 - eng [Somente leitura]static.telefonica.aatb.com.br/Arquivos/Download/779_Presentation_3Q12.pdf2 Investor Relations Telefônica Brasil S.A. Highlights](https://cdn.vdocuments.us/doc/165x107/6052ba2f6b381e324a19eaef/121105-apresentao-3q12-eng-somente-leitura-2-investor-relations-telefnica.jpg)