Download - Sbi Project on Deposits

JADAVPUR UNIVERSITY

“A STUDY ON SAVINGS PROPOSITIONS AMONGST THE EMPLOYEES /

PROFESSIONALS AND SELF EMPLOYEDS AND THEIR PREFERRED

INVESTMENT OPTIONS”

Internship Report submitted to SBI in completion of the requirement of Summer

Internship at State Bank of India

NAME OF THE STUDENT: PROJECT MENTOR AT THE

BANK:

SANJANA GOSWAMI RAHUL SHUKLA

BRANCH MANAGER AT SBI,

CHITTARANJAN

MAY 06,2013 TO JUNE 30,2013

ACKNOWLEDGEMENT

It is really a matter of pleasure for me on being selected for internship with SBI, with the

project topic , “A study on savings propositions amongst the employees / professionals and

Self Employeds and their preferred investment options ’’.

In preparing this project, I have gathered immense knowledge regarding savings and

investment and the deposit products of SBI, which would benefit me tremendously in my

career in the future. So, I would like to thank all the persons who contributed directly or

indirectly for the successful completion of my project report , “A study on savings

propositions amongst the employees / professionals and Self Employeds and their preferred

investment options ’’.

First of all,I would like to thank my project mentor, Mr. Rahul Shukla, Branch

Manager of SBI,Chittaranjan, for helping me in preparing and presenting this project. I am

highly thankful and grateful to him for his careful guidance without which I could not have

made progress with my project. I woud take this opportunity to thank the staff members of

SBI, Chittaranjan, who had also helped me a lot in my project.

Last but not the least, I am highly grateful to my university, Jadavpur University, for

giving me this opportunity to experience the banking life.

TABLE OF CONTENTS

Sl. No. Topic Name Page No.

1. INTRODUCTION 1

1.1 Brief profile of student

1.2 Brief profile of project mentor at the bank

1.3 Brief profile of organization

1.4 Nature of the project

1.5 Brief objectives/responsibilities assigned by the project mentor

2. FRAMEWORK OF STUDY

2.1 Theoretical framework

2.2 Specific objectives of the project

2.3 Scope of study

2.4 Limitations of study

2.5 Period of study

3. METHOLOGY AND ANALYSIS

3.1 Methodology

3.2 Observations

3.3 Analysis

3.4 Conclusions

3.5 Recommendations

4. BIBLIOGRAPHY

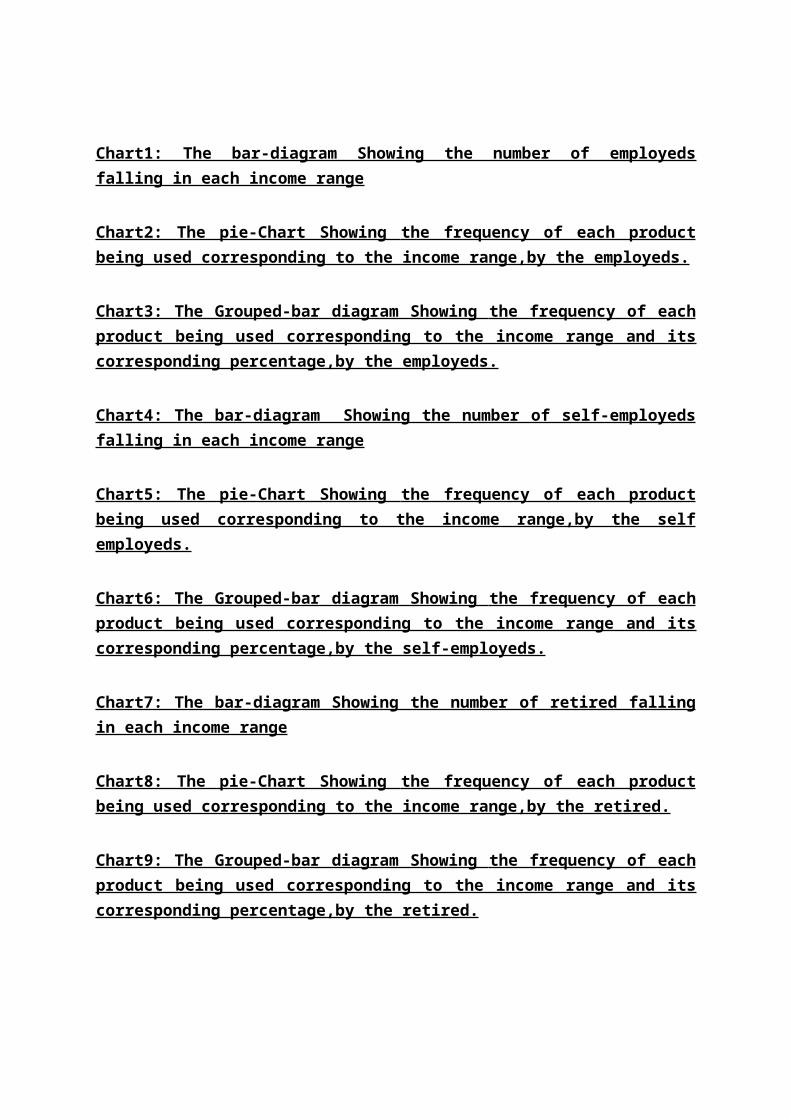

LIST OF CHARTS:

Chart1: The bar-diagram Showing the number of employeds falling in each income range

Chart2: The pie-Chart Showing the frequency of each product being used corresponding to the income range,by the employeds.

Chart3: The Grouped-bar diagram Showing the frequency of each product being used corresponding to the income range and its corresponding percentage,by the employeds.

Chart4: The bar-diagram Showing the number of self-employeds falling in each income range

Chart5: The pie-Chart Showing the frequency of each product being used corresponding to the income range,by the self employeds.

Chart6: The Grouped-bar diagram Showing the frequency of each product being used corresponding to the income range and its corresponding percentage,by the self-employeds.

Chart7: The bar-diagram Showing the number of retired falling in each income range

Chart8: The pie-Chart Showing the frequency of each product being used corresponding to the income range,by the retired.

Chart9: The Grouped-bar diagram Showing the frequency of each product being used corresponding to the income range and its corresponding percentage,by the retired.

LIST OF TABLES

Table1: Showing the interest rates offered by SBI for deposits less than Rs.1crore

Table2: Showing the interest rates offered by SBI for deposits above Rs.1crore

Table3: Showing the different products available under SBI Life

Table 4: Showing savings and investment options of the employed category

Table 5: Showing savings and investment options of the self-employed category

Table 6: Showing savings and investment options of the retired category

INTRODUCTION:

Brief Profile of Student:

NAME: SANJANA GOSWAMI

ADDRESS: STREET NO. : 11

QUARTERS NO. :11 A

P. O. CHITTARANJAN

DIST. BURDWAN

PIN 713331

EDUCATIONAL QUALIFICATION:

Passed CLASS X in 2007 from St. Joseph’s Convent High School,Chittaranjan.

Passed CLASS XII in 2009 from Deshbandhu Girls, Chittaranjan.

Graduated from MAHARAJDHIRAJ UDAY CHAND WOMEMS’ COLLEGE,

BURDWAN in 2012 under BURDWAN UNIVERSITY.

Presently pursuing Masters in Economics from Jadavpur University.

Brief profile of project mentor at the bank :

NAME: RAHUL SHUKLA

DESIGNATION: BRANCH MANAGER

SBI, CHITTARANJAN

Brief profile of organization

The State Bank of India(SBI) is the largest bank in India with presence in more than

50countries. It is a government-owned corporation with its headquarters in Mumbai,

Maharashtra. As of December 2012, it had assets of US$501 billion and 15,003 branches,

including 157 foreign offices making it the largest and financial services company in India by

assets.

In 2008, the government took over the stake held by the Reserve Bank of India. SBI

was ranked 285th in the Fortune Global 500rankings of the world’s biggest corporations for

the year 2012.

SBI provides a range of banking products through its network of branches in India and

overseas, including products aimed at non-resident Indians(NRIs). SBI has 14 LHO and 57

Zonal Offices that are strategically located located at important cities throughout the country.

SBI is a banking behemoth and has 20% market shares in deposits.

Deposits of the Bank increased from Rs. 10,43,647 crores in Mar 12 to Rs. 12,02,740

crores in Mar13, a growth of 15.24%.

Savings Bank Deposits increased from Rs. 3,59,847 crores in Mar 12 to Rs. 4,14,907

crores in Mar 13 ( 15.30% YOY growth).

Now coming to my branch i.e. the SBI Branch based at Chittaranjan , where I have been

sent for internship, it is a currency-chest branch having 4 link branchesand 5 ATMs.

Brief profile of SBI Chittaranjan branch are as follows:-

Branch Code : 241

Region : 6

Circle : Bengal

Network : GM-2

Module : Burdwan

Population : Semi-Urban

Office-type : Regular Branch

Opened on : 01-08-1966

Tier : 3

Number of NRI Account : 15

Number of pension account holder : 3536

Total Demand Deposit : 112crores

Total Time Deposit : 192crores

Total advances : 23crores

Net-banking :

Mobile-Banking :

Nature of the project

The project report was on “A study on savings propositions amongst the employees

/professionals and Self Employeds and their preferred investment options” .

The nature of this project report was that it dealt with the savings habit and the

investment options and preferences of the individual customers and how these savings habit

vary with their vocation in life viz. employed/self-employed/retired.

Brief objectives/ responsibilities assigned by the project mentor

The objectives / responsibilities assigned by the project mentor were:-

a) Firstly, to understand the concepts of savings and investment and then to explore

how this investment pattern varies person to person depending whether they are

employeds / self employeds / retired.

b) Secondly, to explore the deposit products and services offered by the State Bank of

India, to its customers.

c) Thirdly, to understand the perception of the customers ( i.e. employees / self

employeds / retired), by studying their savings propositions and their preferred

investment patterns, with respect to the products and services offered by SBI.

d) Fourthly, to understand the objectives of SBI, with respect to the products and

services offered by them.

e) Fifthly, to try and find out the level of awareness about the old existing products

and the new products being launched by SBI, amog the individuals.

f) Sixthly, to try and find out the reason of why people are investing in banks, why

are they depending solely on banks for investing their hard-earned money.

Keeping these above objectives assigned by the project mentor , in mind, I made progess

with my project report.Thus, these were the main guidelines which helped me in preparing

and presenting this project.

FRAMEWORK OF STUDY

Theoretical framework

The State Bank of India(SBI) was incorporated under the SBI Act 1955 and is the largest bank in India in terms of assets and deposit base and its areas of operation span all areas related to banking and finance viz.

The products offered by the State Bank of India are:-

Products:

Personal Banking

NRI Services

International

SME

Domestic Treasury

Interests

Savings Account

Debit and Credit cards

Now let us define concepts of savings and investment as related to my project topic : -

Savings: The portion of disposable income not spent on immediate consumption but

accumulated or invested through various investment avenues viz. Bank FD, Corporate

Debentures, Stock Market, Bond Market, Commodity Market, Real Estate, Bullion etc. in

anticipation of returns and consequent capital growth is called Savings.

Investment: Money deployed or asset created to generate cash flows and/or to augment capital or to meet requirements in case of emergencies is called Investment.

Two main classes of investment are:

Fixed Income Investment such as bonds, Fixed Deposit, preference shares.

Variable Income Investment such as business ownership (equities), or property

ownership. In economics, investment means creation of capital or goods capable of

producing other goods or services.

Expenditure on education and health is recognized as an investment in human capital and

research and development in intellectual capital. Return on investment (ROI) is a key

measure of an organization’s performance.

Now let us focus on the DEPOSIT PRODUCTS OF STATE BANK OF INDIA.

The DEPOSIT PRODUCTS OF STATE BANK OF INDIA can be summarized with

the help of the following structure:-

FIXED DEPOSIT:-

Fixed Deposit Scheme is one of the important saving schemes offered by the State Bank

of India.

This scheme is popular among both the employed group and retired group of

people.

This scheme is a boon for people who have large amount of savings and thus can

fix it as a deposit in banks.

Under this scheme ,the customer deposits a lumpsum money at the time of opening

a Fixed Deposit in the bank and fixes it for a specified time period, say 1 year or 2

year.The interest on deposit thus made is either payable at monthly/quarterly

intervals or cumulative interest along with principal amount is paid at the time of

maturity as per desire of the deposit holder. At the end of the period i.e. on

maturity date, the customer is paid the maturity value i.e. principal deposited and

the interest payable.

Features and benefits with SBI Fixed Deposits:-

Safety

SBI understands the value of your hard earned money and continue to deliver on their

promise of safety and security for over 200 years.

Liquidity Loan /overdraft facility

You can avail a loan/overdraft against your Fixed deposit.SBI provides you loan /

overdraft upto 90% of your Fixed deposit amount at nominal cost. So you continue to

earn interest in your fixed deposit and still can meet your urgent financial

requirements.

Premature Withdrawal

Interest to be charged on premature withdrawal of term deposits or fixed deposits at

1.00% below the rate applicable for the period deposit has remained with the Bank.

Transferability

Transfer of Term Deposits or Fixed Deposits between SBI wide networks of branches

without any charge.

Compounding / Flexible / Timely Payment of Interest

Under SBI Special Term Deposit Scheme, interest accrues in your account and gets

compounded quarterly. Besides, SBI assures timely delivery of the proceeds of your

deposit with interest, on maturity. Flexibility of payment on maturity through Cash

(subject to prevalent Income Tax Act), Banker's Cheque, Credit in Savings /Current

account.

Tax Implications

Tax Deductible at Source as per Income Tax Act.

Automatic Renewals

There is no need for you to keep track of the maturity of your fixed deposits. Your

fixed deposits with SBI will be renewed automatically, post maturity, and you

continue to earn interest for same period as that of your matured deposit, at the

interest rate prevailing at the time of maturity. Automatic renewals take place where

there are no standing instructions for renewal.

Fixed Deposits Rates of Interest:-

For deposit products less than Rs. 1crore

MATURITY PERIOD DEPOSIT AMOUNT INTEREST RATE

GENERAL

PUBLIC

SENIOR

CITIZEN

7 days to 90 days Less than Rs. 1 crore 6.75 NIL

91 days to 179 days Less than Rs. 1 crore 6.75 NIL

180 days Less than Rs. 1 crore 6.75 NIL

181 days to 240 days Less than Rs. 1 crore 6.75 NIL

241 days to less than 1 year Less than Rs. 1 crore 6.75 NIL

1 year to less than 2 years Less than Rs. 1 crore 8.75 9.00

2 years to less than 3 years Less than Rs. 1 crore 8.75 9.00

3 years to less than 5 years Less than Rs. 1 crore 8.75 9.00

5 years to upto 10 years Less than Rs. 1 crore 8.75 9.00

Table1: Showing the interest rates offered by SBI for deposits less than Rs.1crore

For deposit products above Rs. 1crore

MATURITY PERIOD DEPOSIT AMOUNT INTEREST RATE

GENERAL

PUBLIC

SENIOR

CITIZEN

7 days to 180 days More than Rs. 1 crore 7.50 NIL

181 days to 270 days More than Rs. 1 crore 7.50 NIL

271 days to less than 1 year More than Rs. 1 crore 7.50 NIL

1 year to less than 2 years More than Rs. 1 crore 8.75 NIL

2 years to less than 5years More than Rs. 1 crore 8.75 NIL

5 years to less than 10years More than Rs. 1 crore 8.75 NIL

For general public, interest rates are ranging from 6.75 % to 8.75 %.

For senior citizens, for different tenures are offered additional benefit of 0.25% above

the card rate for general public.

The SBI broadly categories its term(or fixed) deposits into two products types:-

a) Special Term Deposits Receipt(STDR)

b) Term Deposits Receipt(TDR)

And a sub-category Flexi-Fixed Deposit.

Special Term Deposits Receipt(STDR)

The STDR pays out the principal amount deposited by us, along with the interest

earned by us , on that principal amount deposited, after along time period, say it be 1

year or 2years, etc., as chosen by us at the time of opening the account.

In case of STDR, the interest earned by us is reinvested instead of getting paid out.

If we don’t need a regular source of income in the form of interest payouts, it makes

sense to go for STDR as it allows us to reap the dividends of compounding. The

interest accruing on our deposit with the bank gets reinvested ( or compounded)

quarterly giving us superior returns from the first year itself.

Minimum amount that can be accepted as Special Term Deposit is Rs. 5000.

Minimum and maximum tenure for STDR is 6 months and 120 months(10 years)

respectively.

Term Deposits Receipt(TDR)

The TDR pays out the interest earned by us at a periodicity (monthly , quarterly,half-

yearly or yearly) chosen by us at the time of opening of the account. Thus TDR gives

us a regular income in the form of interest payouts.

Minimum amount that can be accepted as Special Term Deposit is Rs. 5000.

Minimum and maximum tenure for STDR is 7 days and 120 months(10 years)

respectively.

Maximum amount of loan that can be granted against Term Deposits is 90% of

principal amount + accrued interest.

Maximum amount that can be held in the name of the Minor (above 10years of age)

for Term Deposit is Rs. 2,00,000/-, for a maximum period of 10years.

Interest rates on STDR/TDR are:-

For general public, interest rates are ranging from 6.75 % to 8.75 %.

For senior citizens, for different tenures are offered additional benefit of 0.25% above

the card rate for general public.

TDS on Term Deposit Interest:-

As per Section 194A of the Income Tax Act, Tax is deducted at source whenever

interest on time deposits credited or paid or likely to be credited or paid to the account

of a customer, exceeds Rs 10000/- per person, per branch in a financial year. In such

caes, 15G/15H forms are to be submitted by the person.

TDS is applicable on all time deposits except Recurring Deposit.

Form 15H is submitted by Depositors with age of 60 years & above.

Form 15G is submitted by Individuals below age of 60 years.

Form 15G & 15 H are valid only if It contains PAN.

If PAN is not submitted, applicable rate of TDS for Resident Individuals,20%

Plus 3% Cess.

Thus, it may be concluded that :-

a) STDR is mainly chosen by the employed persons. As the employed persons do not

need aregular source of income in the form of interest payouts, and they are able to

meet their monthly expenditures, through their monthly salary, so they prefer to

choose STDR.

b) TDR is mainly chosen by the retired persons,as they need a regular source of income

in the form of interest payouts,to meet their daily expenditures.

Flexi-Fixed Deposit

It is a sub category of Fixed Deposit.

It offers high rate of interest.

Minimum amount of deposit is Rs.

There is no penalty for premature withdrawl within 6 months.

RECURRING DEPOSIT(RD):-

Recurring Deposit Scheme is one of the important saving schemes offered by the State

Bank of India.

Recurring Deposit is very popular among the salaried class, specially who can

afford to save only few thousand rupees per month.

This scheme is a boon for people who do not have a large amount of savings and

thus cannot use the Fixed Deposit scheme of the banks.

Under this scheme,the customer deposits a minimum amount (normally fixed)

every month, and bank pays the interest at the pre-determined rates(which is

usually the same as applicable to Fixed Deposits).

At the end of the period i.e. on maturity date, the customer is paid the maturity

value i.e. principal deposited and the interest payable.

TDS is not deductable on the interests earned on RD’s.

Minimum monthly installment is Rs. 100/- for general public and Rs. 50/- for

senior citizens.

Minimum and Maximum tenure is 12months and 120 months(10years)

respectively.

If opened in the name of the minor(below 18 years of age): Monthly installments

should be so adjusted that the total amount payable on maturity does not exceed

Rs. 2,00,000/-.

Recurring Deposit Calculator :

Investment Amount

Period(in months)

Rate of interest

Maturity Value

This RD calculator calculates the maturity value (i.e. principal amount + interest earned)

of the deposits made under recurring deposit schemes of SBI.

SAVINGS ACCOUNT:-

A Savings Account may be opened by

a. Any individual in his sole name

b. By two or more individuals jointly with survivorship benefits.

If at any time any one of the account holders issue stop payment of operation by the

other joint account holders then account can be operated in future only Jointly by all

the account holders.

Minimum Cash Deposit permitted : Rs 10/-.

Maximum Cash Deposit permitted : No restriction.

Minimum cash withdrawal permitted:Rs 50/-.

Maximum cash withdrawal permitted :No restriction.

Number of Credits permitted:No restriction.

Maximum number of debit entries permitted without any charge 30 per half year

excluding SBI alternate channel transactions.Transactions through other bank’s ATM

will be included.

Service charge payable if debits exceeds the limit Rs 5/- per entry.

No Can third party cheques endorsed in favour of account holder be deposited.

In non cheque operated A/c,withdrawal form should be invariably accompanied by

Passbook.

Payment through withdrawal form can

be made to :Self only.

A savings account can be opened in the name of a minor, either

a) Singly or jointly with his her guardian

b) By guardian alone on behalf of his/her minor ward.

And the maximum balance in the account can be Rs. 2,00,000/- only.

A savings account is the initial criteria , which every indidual should have in the

banks, without which he cannot use any other products of the banks, So, every

individual has a savings account.

For General Public, the savings account is categorized into two types:-

a) Savings Plus

b) Savings Premium

Savings Plus:

Minimum Balance to be maintained in Savings A/c :Rs 5000/-

Service charge as applicable to SB account will be charged.

Minimum permissible ‘Threshold Amount’ above which sweep will take place:Rs

5,000/.

Minimum Amount of sweep to MOD Rs 10000/- and thereafter in multiple of 1000/-

Option for Auto Sweep Periodicity Once a week on any chosen day or once a month

on any chosen date subject to availability of fund in SB A/c.

Period of Deposit for MOD Component.: 1 year to 5 years.

Under the reverse sweep facility,customer can specify the principle for breaking of

MOD :Either LIFO or FIFO.

In absence of any such option the Bank would follow the principle of LIFO.

Loan against deposits held under Saving Plus Scheme is not granted.

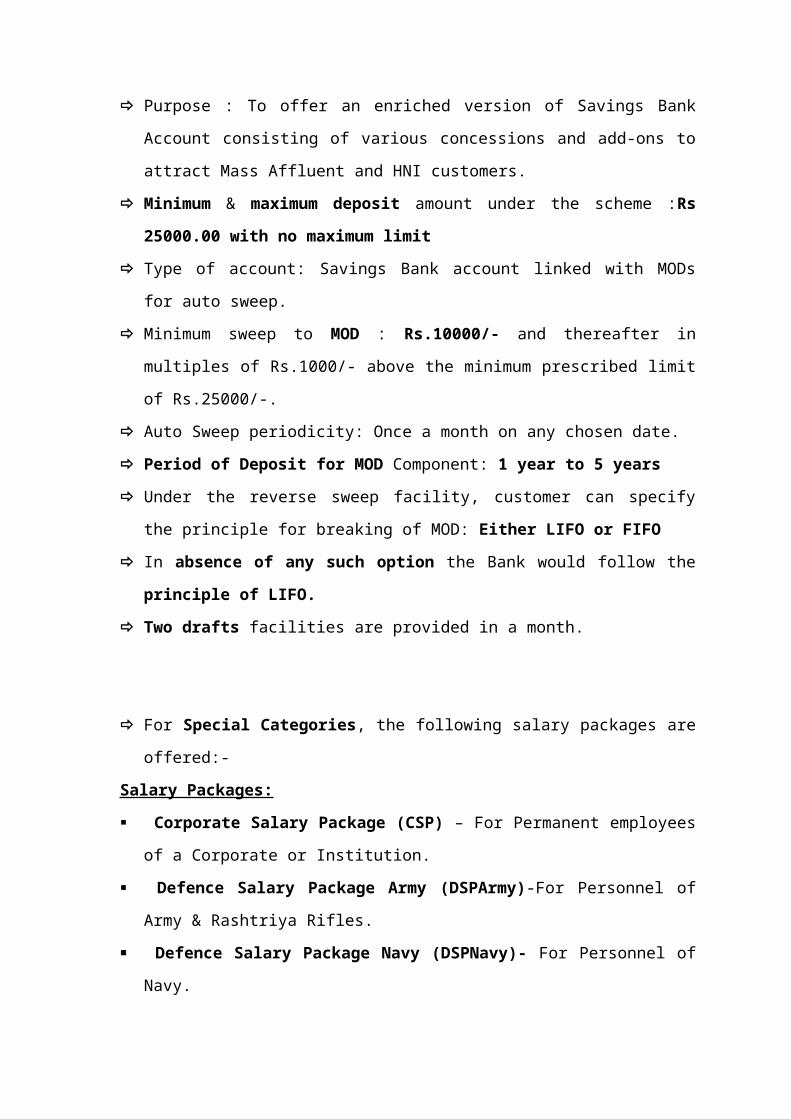

Savings Premium:

Eligibility criteria for residents above 18 years of age is:-

It can be opened singly, jointly with or without survivorship benefits.

Premium Savings Account was earlier called Rich Savings Account.

Purpose : To offer an enriched version of Savings Bank Account consisting of various

concessions and add-ons to attract Mass Affluent and HNI customers.

Minimum & maximum deposit amount under the scheme :Rs 25000.00 with no

maximum limit

Type of account: Savings Bank account linked with MODs for auto sweep.

Minimum sweep to MOD : Rs.10000/- and thereafter in multiples of Rs.1000/- above

the minimum prescribed limit of Rs.25000/-.

Auto Sweep periodicity: Once a month on any chosen date.

Period of Deposit for MOD Component: 1 year to 5 years

Under the reverse sweep facility, customer can specify the principle for breaking of

MOD: Either LIFO or FIFO

In absence of any such option the Bank would follow the principle of LIFO.

Two drafts facilities are provided in a month.

For Special Categories, the following salary packages are offered:-

Salary Packages:

Corporate Salary Package (CSP) – For Permanent employees of a Corporate or

Institution.

Defence Salary Package Army (DSPArmy)-For Personnel of Army & Rashtriya

Rifles.

Defence Salary Package Navy (DSPNavy)- For Personnel of Navy.

Defence Salary Package Air Force(DSP-Airforce)- For Personnel of Air force.

Defence Salary Package Assam Rifles(DSP-AR)- For Personnel of Assam Rifles.

Defence Salary Package GREF (DSPGREF)-For Personnel of General Reserve

Engineer Force.

Para Military Salary Package (PMSP)-For Personnel of Central ReservePolice

Force (CRPF); Commando Battalion for Resolute Action (COBRA), under

Command & Control of CRPF; Sashastra Seema Bal (SSB); Border Security Force

(BSF); National Security Guards (NSG); Indo Tibetan Border Police (ITBP) &

Central IndustrialSecurity Force (CISF).

Railway Salary Package (RSP)- For Personnel of Indian Railways.

Police Salary Package (PSP)- For permanent employees of Central Police

Organisations and Police Forces of States and Union Territories.

Indian Coast Guard Salary Package- A new salary package scheme is launched.

State Govt Salary Package (SGSP)- Concession will be available to those

employees who maintain their salary account with SBI only.

Central Govt Salary Package (CGSP)-Permanent employees of all ministries and

department of Central Govt including defence civilians are covered by the scheme

already. Now employees of RBI and NABARD are also included.

Variants of Salary A/cs in all theses

Salary PackagesFour (Silver, Gold, Diamond &Platinum).

§ Any Exception to the above Platinum Variant not available in DSPAR (Since

officers qualifying for Platinum Variant are on deputation from Army & they are

already covered under DSP-Army).

TAX SAVINGS SCHEME OF THE STATE BANK OF INDIA:-

The Tax savings scheme of SBI is one of the deposit products of SBI.

Individuals in single name or joint name.

Cater the need of Income Tax assesses.

PAN is mandatory.

It provides Tax Benefit under Sec 80C of IT Act 1961.

Minimum Deposit :Rs 1000/-

Maximum Deposit :Rs 100000/- in a year

Period of Deposit :Minimum 5 Years and Maximum 10 Years.

There is a lock in period of 5 years.

No loan facility. It can also be not held as collateral for securing any loan.

In case of Joint A/c, the First Account holder (u/s 80c of IT Act 1961) will get the

tax benefit.

ON-LINE PRODUCT:-

Products that are accessible to the customers 24*7 (365 days a year) at the comfort of

the house is called ON-LINE PRODUCT.

OTHER PRODUCTS OF SBI:

SBI Life:-

Every policy has single and regular premium.

Single:- can be deposited only once and can be withdrawn at the time of maturity

only.

Regular:- After every regular time period say 6months.

Every policy has locking period.

Customer Insurance Facilitator(CIF):-an agent has to pass this exam, conducted by

IRDA(Insurance Regulator Development Authority).

An agent can remain attached to only one company at a time.

SBI Life has merger with BNB Parivar( 90 SBI Life + 10% BNB).

Products of SBI Life:-

Traditional:-

SBI Cap:-

SBI Mutual Fund:-

SBI Mutual Fund is India’s largest bank sponsored mutual fund and has an enviable

track record in judicious investments and consistent wealth creation.

The fund traces its lineage to SBI - India’s largest banking enterprise. The institution

has grown immensely since its inception and today it is India's largest bank,

patronised by over 80% of the top corporate houses of the country.

SBI Mutual Fund is a joint venture between the State Bank of India and Société

Générale Asset Management, one of the world’s leading fund management companies

that manages over US$ 500 Billion worldwide.

In twenty years of operation, the fund has launched 38 schemes and successfully

redeemed fifteen of them. In the process it has rewarded it's investors handsomely

with consistent returns.

A total of over 5.8 million investors have reposed their faith in the wealth generation

expertise of the Mutual Fund.

Schemes of the Mutual fund have consistently outperformed benchmark indices and

have emerged as the preferred investment for millions of investors and HNI’s.

Today, the fund manages over Rs. 42,100 crores of assets and has a diverse profile of

investors actively parking their investments across 38 active schemes.

The fund serves this vast family of investors by reaching out to them through network

of over 130 points of acceptance, 29 investor service centers, 59 investor service

desks and 6 Investor Service Points.

SBI Mutual is the first bank-sponsored fund to launch an offshore fund – Resurgent

India Opportunities Fund.

SBI Gold:- It provides a platform for purchasing gold, not physically hand-in-hand,

but through machines.

SBI Bond: -

It is a type of buying certificates.

The rate of interest is fixed.

There is a locking period of 10-15 years.

It is mainly opted by those who try to get rid of tax through Section 80C.

PUBLIC PROVIDENT FUND(PPF):-

It is Government Sponsored Scheme.

Minimum amount to be deposited: Rs. 500

Maximum Deposit: Rs. 1,00,000/-.

Rate of interest is given every year on 31st March.

Time period: 15 years, it is to be extended at a block of 5years. After 5years,it can be

broken or loan can be taken.

Only 1nominee,two nominee is not possible.

SENIOR CITIZEN SAVING SCHEME:-

It is also a Government Sponsored scheme.

Minimum age of the depositor should be 60 years or above on the date ofdeposit

Period of deposit :Minimum 1 year maximum 10 years.

Minimum amount of deposit is Rs. 10000.00 and thereafter in multiple of Rs 1000.00

(For RD, maturity value should be Min. Rs.10,000/-).

Differential rate of interest under Senior Citizen Deposit Scheme is 0.25% above the

normal rates.

Nomination: i) Signature of nominee duly attested by Senior Citizen to be obtained.

ii) Option to write name of nominee on receipt apart from ‘nomination

registration no’ (if Senior Citizen not agreed for above provision,

consent letter to be kept on record).

Specific Objectives of the project:

Our endeavor was to:-

a) Explore the deposit products and services offered by the State Bank of India to

individual customers.

b) Understand the perception of the customers, (i.e. employed, self-employed, retired),

by studying their savings propositions and their preferred investment patterns,

with respect to the products and services offered by SBI.

c) Understand the objectives of Banks with respect to the products and services offered

by them.

d) To ascertain variances among individuals based on their income, age, number of

dependent family members.

e) Find out the level of awareness about the old existing products and the new products

being launched in by SBI, among individuals.

f) Lastly, to understand how individuals’ preferred investment options vary with their

vocation in life viz. employed/self employed/retired.

Scope of Study:

a) Scope of the study is to understand the various services and deposit products

offered by SBI to the individual customers.

b) An effort was made to study the savings propositions amongst the employeds, self-

employeds , and retired and their preferred investment options.

c) The study was undertaken at the SBI Branch based at Chittaranjan. Hence, the

survey was restricted to the bank customers of Chittaranjan only.

Limitations of study:

The Limitations of study in my project topic were:-

a) Since the study was done taking the SBI Branch based at Chittaranjan ,so the survey

was restricted to the bank customers of this branch only. Thus, the sample size was

restricted within the area Chittaranjan only.Hence,the conclusions may not be

generalized for the bank as a whole.

b) There were time constraints as this project was supposed to be completed within 8-10

weeks.

c) The SBI Branch at Chittaranjan is one of the prominent branches with significant

deposit base.

This project has been done purely for academic purpose and as a part of my internship under

SBI.

Period of Study:

The period of study in preparing this project report was 8-10 weeks, as allotted by SBI,

HR Department, LHO.

METHODOLOGY AND ANALYSIS

Methodology:

The project report on “A study on savings propositions amongst the employees /

professionals and Self Employeds and their preferred investment options”, aims to

collect data about the savings and investment patterns chosen by different individuals

depending on their age, category(employed / self-employed / retired), monthly salary and

number of dependent family members on them.

The methodology used by me in collecting data was by means of a survey.It was

carried out in the following ways:-

a) The survey was carried out by me, by remaining in the bank itself.

b) Questionnaires were prepared and each and every individual visiting the bank for their

own purposes, were approached through these questionnaires and were asked to fill

them up.

c) The questionnaires included a set of total 12 questions, which reflect the age, salary

(monthly), number of dependent family members , monthly investment(savings) and

its related investment patterns.

d) The filled up information was later analyzed to obtain the required interpretation and

the findings.

In this way, the data was collected for my project report.

Observations:

From among 50,000 account holders in the SBI Branch based at Chittaranjan, I have tried to

include about 150-200 customers of the bank in my survey.

But inspite of surveying about 150-200 customers, my project report contains data of about

125 customers only. This is because of the :-

Indifference shown by some people towards participating in this survey as they might

be least bothered in it and considered it as time wastage.

Many respondents were apprehensive about divulging their income and savings

related information. This was done mainly by the high-income group people and so

my entire survey includes only 8.0% of them.

Throughout my entire survey, I have covered three categories of people, namely, Employeds,

Self-Employeds and Retired.

Now we shall focus on each category, part-by-part, and study their savings propositions and

their preferred investment options.

EMPLOYEDS:-

The Employeds are those group of people who are still working and thus have a regular

source of income in the form of their monthly salary. These group invests that amount of

their salary which is left after their monthly expenditures, keeping in mind that they get tax-

benefits. Among the 50000 account holders of the SBI Branch based at Chittaranjan, my

survey includes 56% of Employeds. From the above table I came to the conclusion that

among all the employeds whom I have surveyed, 50% of them invests completely in SBI and

the remaining 50% of them only has the savings account in the form of salary account in SBI.

These two groups can be explained in the following manner:-

One group of Employeds which depends on SBI completely for their entire

investment, invests in the following products such as Savings account ,Fixed Deposit,

Recurring Deposit, SBI Life. These group of people fear to invest anywhere else

outside bank due to risk involved. So, inspite of getting relatively lower rate of

return/interest from SBI, they still invest in SBI due to safety.

The other group of Employeds which has only Savings account in SBI, implies that

they visit bank for the purpose of withdrawing money from their salary account only,

in order to meet their monthly expenditures. This may be due to lesser amount of

investible funds available with them or may be because of their different investment

preferences.

Some points to be noted about the Employeds are:-

Employed People of any income range are more concerned about tax savings. As all

of them are tax-conscious, although they invest in Fixed Deposit, Recurring Deposit,

Savings Account in SBI, but for tax benefits, they invest in Provident Funds(PF) and

Voluntary Provident Funds(VPF), and also in Public Provident Fund(PPF) Accounts

provided by banks. Many invest in LIC also. But one thing to be noted is that these

people do not prefer to invest in the Tax Savings Scheme of SBI, the reason for

which may vary from ignorance to individual preference.

Many High-Income group were apprehensive about divulging their income and

savings related information. This is why, my survey includes only 8.0 percentage of

high-income category.

SELF-EMPLOYEDS:-

My survey includes 20% of Self-Employeds. From the above table I came to the conclusion

that among all the Self-Employeds whom I have surveyed, all of them mainly invest in the

following FOUR categories :-

Fixed Deposit Schemes of the SBI (STDR)

Current Account

SBI Life

SBI Mutual Fund.

These type of investment pattern is opted by the Self-Employeds may be due to the

following reasons:-

These Self-Employeds do not have any any regular source of income with certainty,

as the employeds have. So this factor prevents them from investing in Recurring

Deposit Schemes. So, whenever they earn any heavy profit from their business, they

invest it in the Fixed Deposit.

SBI MF and SBI Life are mostly used by these Self-Employeds only, as they do so in

order to get higher returns.

RETIRED GROUP OF PEOPLE:-

The Retired groups of people are those who had crossed their 60 years of age and are thus

retired from their job life. They have no regular source of income. So with the amount of

money which they get after their retirement, they try to invest in such deposit products so that

they can earn a regular source of income in the form of interests and also keep some amount

fixed for sudden urgent needs such for medical purposes.

My survey includes 24% of Retired group of people.. From the above table I come to the

conclusion that among all the Retired group of people whom I have surveyed, all of them

mainly invest in the following TWO categories :-

Savings account

Fixed Deposit ( both STDR and TDR)

Such an investment pattern is chosen by the Retired group of people due to the following

reasons:-

Ignorance of the people towards learning something new.

Resistance to change: Old/ retired people do not easily adjust themselves with any

kind of changes surrounding them. So they keep on investing in their old investment

patterns.

Lack of awareness about the products: Retired people are less aware of the new

products being launched in by the banks. They actually don’t bother to know about

the new products . They are fully satisfied with the products they are using and with

the returns they are getting from it.

For example: SBI Mutual Fund is one of the products which could yield higher

returns if invested for longer time period. But very few people know about it and they

don’t try to enquire about it also. Thus, the retired group are mainly inclined towards

Savings account and Fixed Deposit.

Penetration level is low among the retired group.

Old/retired people are also found to be technology aversed: They are not so easily

equipped with the newer technology based facilities,being introduced in the bank such

as Internet banking.

But almost many of them hesitate to use these facilities because of:-

1. Fear of getting hacked

2. Lack of proper computer knowledge and use of internet.

Indecision to goals: Many a time they have no present financial goals/targets to be

met but they have a heavy amount in cash. So in such situations, when there is

indecision to goals, they prefer to go for Fixed Deposit (TDR).

Uptil now I have discussed about what I have observed from each category.

Now, we shall focus on over-all observations:-

From the survey, which I have carried out among the bank customers of the SBI,

Chittaranjan, the following conclusions can be drawn from the survey:-

a) People of any income range in this area are more concerned about tax savings.

b) TDS charged on Fixed Deposit should be stopped, as it does not earn any profit for

the bank. Rather, it causes harashment as suggested by the customers.

c) During my survey, I have realized that many people are not willing to reveal their

personal data regarding their salary and investment patterns. Some of them have also

misguided me by giving me wrong data.

d) Many High-Income group people have denied completely to reveal their salary and

investment patterns in fear of getting caught by Income Tax. This is why, my survey

includes only 8.0 percentage of high-income category.

e) Another conclusion that can be drawn from my survey is that Savings account, STDR,

SBI Life are the three most common products which are used by all categories of

customers of the bank.

f) SBI Mutual Fund is the least used product in SBI, as SBI Mutual Fund is based on the

share market transactions and is surrounded by risk and uncertainty.

But very few people know that SBI Mutual Fund can yield higher returns for long

term period. Due to lack of such knowledge among the customers, they are least

bothered to invest in SBI Mutual Fund and thus neglect it fully.

g) SBI Life is the common investment pattern among the self-employeds, although some

employeds have also invested in SBI Life.

Inspite of SBI Life being used in plenty but it is surrounded by complaints of

customers. Almost all users of SBI Life are complaining about getting lesser returns

compared to what they have invested.

h) The retired group invests only in TDR and no other products. They do so, in order

to get a regular source of income in the form of interests. Also, these retired category

is least interested to know about other existing old products and the new products

being launched in, by SBI.

i) The entire employed group which I have covered in my survey, are all Railway

Employees of Chittaranjan Locomotive Works (CLW) situated in Chittaranjan. As

all of them are tax-conscious , although they invest in Fixed Deposit, Recurring

Deposit, Savings Account in SBI, but for tax benefits, they invest in Provident

Funds(PF) and Voluntary Provident Funds(VPF), provided by CLW to their

employees and also in Public Provident Fund(PPF) Accounts provided by banks.

Many invest in LIC also. These people do not invest in the Tax Savings Scheme of

SBI.

ANALYSIS:-

In this section we shall show the results of my survey with the help of graph:-

EMPLOYEDS:-

SELF-EMPLOYEDS:-

RETIRED:-

Conclusions:-

Throughout my project report on “A study on savings propositions amongst the employees

/professionals and Self Employeds and their preferred investment options” ,within the

limited time frame available I have tried to gain a brief knowledge regarding the deposit

products offered by SBI and also tried to cover each and every aspect of the savings

propositions among different individuals.

My study was mainly focused on to find out how the savings propositions and

investment pattern of every individual, varies according to their monthly income,

age ,dependent family members and their future aspirations and needs etc. This study was

undertaken at the SBI Branch based at Chittaranjan and so the survey was restricted to the

bank customers of Chittaranjan only. I could not reach all of the customers in my allotted

time period, and so ,I could include only 125 respondents in my survey.

The area of my survey i.e. Chittaranjan, is a semi-urban area, where the only factory

located is Chittaranjan Locomotive works(CLW). Among these 125 respondents, majority of

them were government employees of CLW. The rest were the Self- employeds and the retired

group of people.

The important points to be noticed are:-

People save maximum portion of their income in Bank FDs, Post Offices. Their

savings is consolidated to Fixed Deposits only. They go for no other options.

Secondly, due to the “Sharda” case also, people have become more aware of the risks

involved with the promise of high returns. This is why, most of the people prefers to

save in banks due to safety.

Presently, the economic growth rate has slowed down to 5%. So people’s expectations

are not getting fulfilled and so very few of them are investing in share markets.

Government is trying to accelerate this growth rate, so that general public make use of

their deposits, in investment.

Due to fluctuations and consequent uncertainty in gold prices, people have reduced

their investment in gold (i.e.by buying gold coins from banks and by purchasing gold

items) and started investing in banks Fixed Deposits.

Thus we can conclude saying that the savings propositions and the investment

options of each and every individual, not only depends on their monthly income, age, number

of dependent family members and their respective monthly/daily expenditures but it is also

affected by other external factors such as inflationary trends,financial market upheavals,

fluctuations in gold prices, fear of the risks involved,lack of awareness or knowledge gap and

so on. So, there are several other factors,which influences a person to choose his investment

option.

Recommendations:

After completing my survey on the project report , “ A study on savings propositions

amongst the employees / professionals and Self Employeds and their preferred

investment options”, I came to some of the conclusions(as mentioned above) and

correspondingly my recommendations towards the bank are as follows:-

a) There should be more alternative technology platform for product delivery and

software deployed by the bank (CBS) should be more users friendly to enhance

productivity and save time.

b) Technology-savy products should be introduced, such as people should be able to do

STDR , TDR, RD through mobile banking. In present situation, mobile banking

allows only mobile recharge, checking of balance etc.

c) Products launched should be customer-savy i.e. the products launched should be such

that they are easily understandable by the customers by their own. Customers need not

approach other bank staff’s to get to know about the products.

d) Products should be beneficial to the customers so that more customers are attracted

towards SBI.

e) There is lack of staff in the SBI Branch based at Chittaranjan, so more staff should be

taken for purposes such as advertising the other associated products of SBI such as

SBI Life, SBI Mutual Fund etc. This might increase the sales of SBI Mutual fund.

f) Changes should be made in the schemes of SBI Life products as the returns till date

from them have been leave a lot to be desired.

BIBLIOGRAPHY

Websites:-

http://www.google.com

http://www.sbi.co.in

http://www.sbimf.com

http://www.sbilife.co.in

http://www.en.wikipedia.org

ANNEXURE 1:

The Savings propositions and the preferred investment options of the Employeds are shown

below in the following table:-

Sl.No. Age(in

years)

Income

(monthly)

Dependent Savings Savings options

STDR TDR RD SB/

CA

SBI Life/

SBI MF/

PPF

1. 59 50000 2 20000 STDR Nil RD SB SBI Life

2. 49 40000 1 10000 STDR Nil RD SB SBI Life

3. 55 40000 1 10000 STDR Nil RD SB SBI Life,

SBI MF

4. 44 55000 3 20000 STDR TDR RD SB Nil

5. 32 60000 2 22000 STDR Nil RD SB SBI Life

6. 27 35000 2 15000 Nil Nil RD SB Nil

7. 46 48000 2 20000 Nil Nil RD SB SBI Life

8. 50 50000 2 14000 Nil Nil Nil SB Nil

9. 55 30000 1 15000 STDR Nil Nil SB Nil

10. 54 45000 2 10000 STDR Nil RD SB Nil

11. 51 60000 2 40000 STDR Nil RD SB Nil

12. 49 55000 2 35000 STDR Nil Nil SB Nil

13. 54 30000 2 15000 STDR Nil Nil SB Nil

14. 45 35000 1 10000 Nil Nil Nil SB SBI Life

15. 49 40000 2 10000 Nil Nil Nil SB Nil

16. 50 40000 1 10000 Nil TDR RD SB Nil

17. 34 36000 1 10000 Nil TDR RD SB Nil

18. 36 15000 1 4000 STDR TDR RD SB Nil

19. 51 42000 2 27000 STDR Nil Nil SB SBI Life

20. 59 45000 2 20000 STDR Nil Nil SB SBI Life

21. 44 25000 3 10000 STDR Nil RD SB Nil

22. 46 30000 5 6000 STDR Nil RD SB Nil

23. 51 28000 2 12000 STDR Nil Nil SB Nil

24. 50 30000 2 16000 STDR TDR RD SB Nil

25. 52 40000 3 25000 Nil Nil Nil SB Nil

26. 49 20000 7 Nil Nil Nil Nil SB Nil

27. 43 25000 3 5000 Nil Nil Nil SB Nil

28. 47 30000 2 11000 Nil Nil Nil SB SBI Life

29. 50 35000 2 14000 Nil TDR Nil SB Nil

30. 50 29000 2 14000 Nil Nil Nil SB Nil

31. 42 19000 3 13000 Nil Nil Nil SB PPF

32. 51 30000 5 4000 Nil Nil Nil SB Nil

33. 50 7000 2 2000 STDR Nil Nil SB Nil

34. 45 45000 4 15000 STDR Nil Nil SB SBI Life

35. 46 32000 3 9000 STDR Nil Nil SB SBI Life

36. 43 30000 2 13000 STDR Nil Nil SB SBI Life

37. 58 60000 2 29000 STDR Nil RD SB SBI Life

38. 48 40000 3 20000 Nil Nil Nil SB Nil

39. 50 40000 4 12000 Nil Nil Nil SB SBI Life

40. 50 44000 2 12000 STDR Nil Nil SB SBI Life

41. 57 56000 2 30000 STDR TDR RD SB Nil

42. 58 80000 3 45000 STDR Nil RD SB SBI Life

43. 55 30000 3 10000 Nil Nil RD SB SBI Life

44. 21 27000 3 3000 STDR Nil RD SB PPF

45. 53 38000 3 13000 STDR Nil Nil SB PPF

46. 52 25000 2 9000 STDR Nil Nil SB Nil

47. 52 50000 2 20000 STDR Nil Nil SB Nil

48. 49 30000 3 12500 STDR Nil Nil SB Nil

49. 35 38000 2 11000 STDR Nil RD SB SBI Life

50. 45 40000 3 20000 Nil Nil RD SB SBI Life

51. 55 15000 2 5000 STDR Nil Nil SB SBI Life

52. 50 35000 3 20000 STDR Nil Nil SB Nil

53. 48 17000 3 7000 STDR Nil Nil SB Nil

54. 49 22000 2 9000 Nil Nil Nil SB Nil

55. 51 35000 4 12000 Nil TDR Nil SB Nil

56. 58 35000 3 8000 STDR Nil Nil SB Nil

57. 53 20000 2 8500 STDR Nil RD SB Nil

58. 38 30000 3 15000 STDR Nil Nil SB Nil

59. 47 24000 2 12000 STDR Nil RD SB Nil

60. 52 19000 2 6000 STDR Nil Nil SB SBI Life

HIGH INCOME GROUP PEOPLE

61. 58 100000 3 30000 Nil Nil Nil SB SBI Life,

SBI MF

62. 42 100000 1 20000 Nil Nil Nil SB SBI Life, SBI MF

63. 59 110000 4 25000 STDR Nil RD SB SBI Life, SBI MF

64. 32 100000 2 22000 Nil TDR RD SB SBI Life, SBI MF

65. 47 130000 3 35000 Nil TDR RD SB SBI Life, SBI MF

66. 52 105000 4 23000 Nil Nil RD SB SBI Life, SBI MF

67. 35 100000 3 20000 STDR Nil Nil SB SBI Life

68. 55 120000 5 25000 STDR Nil RD SB SBI Life

69. 45 110000 4 36000 STDR Nil RD SB SBI Life

70. 59 180000 5 40000 STDR TDR RD SB SBI Life

Table 4: Showing savings and investment options of the employed category

ANNEXURE2:-

The Savings propositions and the preferred investment options of the Self-Employeds are

shown below in the following table:-

Sl.No. Age(in

years)

Income

(monthly)

Dependent Savings Savings options

STDR TDR RD SB/

CA

SBI Life/

SBI MF

1. 29 35000 3 10000 STDR Nil Nil SB SBI Life

2. 48 25000 2 15000 Nil Nil RD SB Nil

3. 33 40000 2 20000 Nil Nil RD CA SBI Life

4. 40 70000 1 15000 STDR TDR Nil SB SBI Life

5. 54 50000 3 10000 Nil TDR Nil SB SBI Life

6. 35 8000 4 5000 Nil Nil Nil SB Savings

plus

7. 31 45000 2 13000 STDR Nil Nil SB SBI Life

8. 40 3000 2 500 Nil Nil Nil SB SBI Life

9. 47 30000 2 3000 STDR Nil RD SB SBI Life

10. 45 60000 5 15000 STDR Nil Nil SB Nil

11. 52 35000 2 17000 STDR Nil Nil SB SBI Life,

SBI MF

12. 53 40000 3 9000 STDR Nil Nil SB SBI Life

13. 30 35000 2 10000 STDR Nil Nil CA SBI Life

14. 35 50000 2 15000 STDR TDR Nil SB SBI Life

15. 44 40000 3 8000 STDR Nil Nil CA SBI Life

16. 58 60000 2 20000 STDR TDR Nil SB SBI Life

17. 25 55000 1 20000 Nil RD SB SBI Life

18. 30 30000 2 10000 STDR Nil Nil SB SBI Life

19. 32 35000 2 15000 STDR Nil Nil SB SBI Life

20. 57 40000 3 10000 Nil RD SB SBI Life

21. 60 30000 2 9000 STDR Nil Nil SB SBI Life,

SBI MF

22. 65 70000 4 20000 STDR Nil RD SB SBI Life,

SBI MF

23. 41 50000 5 9000 STDR Nil Nil CA SBI Life

24. 30 40000 1 10000 Nil TDR RD SB SBI Life,

SBI MF

25. 28 36000 3 16000 STDR Nil RD SB SBI Life

Table 5: Showing savings and investment options of the self-employed category

ANNEXURE3:-

The Savings propositions and the preferred investment options of the Retired group of

people are shown below in the following table:-

Sl.No. Age(in

years)

Pension

(monthly)

Dependent Savings Savings options

STDR TDR RD SB/

CA

SBI Life/

SBI MF

1. 70 13000 5 4000 STDR Nil Nil SB Nil

2. 59 17500 2 7000 STDR Nil Nil SB Nil

3. 50 12000 2 5000 STDR Nil Nil SB SBI Life

4. 60 15000 1 6500 STDR Nil Nil SB Nil

5. 73 13000 2 5000 STDR Nil Nil SB SBI Life

6. 62 10000 2 3000 STDR Nil Nil SB Nil

7. 55 15000 2 6000 STDR Nil Nil SB Nil

8. 60 18000 3 6000 STDR TDR Nil SB Nil

9. 75 12000 2 6000 Nil Nil RD SB Nil

10. 60 1600 2 Nil STDR Nil RD SB Nil

11. 60 10000 4 3000 STDR Nil Nil SB Nil

12. 61 13000 2 4000 STDR TDR Nil SB Nil

13. 73 20000 1 9000 STDR TDR Nil SB SBI Life

14. 58 18000 2 7000 STDR Nil Nil SB SBI Life

15. 62 18000 3 6000 Nil Nil Nil SB Nil

16. 74 12000 2 5500 STDR Nil RD SB Nil

17. 60 16000 2 5000 STDR Nil Nil SB SBI MF

18. 80 11000 1 Nil STDR Nil Nil SB Nil

19. 66 12500 1 2000 STDR Nil Nil SB SBI Life

20. 61 15000 2 6000 STDR Nil Nil SB Nil

21. 70 13000 1 4000 STDR Nil Nil SB Nil

22. 61 17500 1 7000 STDR Nil Nil SB Nil

23. 65 45000 2 20000 STDR TDR RD SB Nil

24. 60 25000 1 10000 STDR Nil Nil SB SBI Life

25. 67 14000 2 5000 STDR Nil Nil SB Nil

26. 78 4000 1 Nil STDR Nil Nil SB Nil

27. 61 19000 4 3000 STDR TDR RD SB SBI Life

28. 63 8000 2 2000 STDR Nil Nil SB Nil

29. 69 14500 2 3500 STDR Nil Nil SB Nil

30. 72 20000 1 8000 STDR Nil Nil SB Nil

Table 6: Showing savings and investment options of the retired category