i

Recommendations for Reorganizing

the World Bank Safeguard Function:

Priorities for Consultation on a

Safeguard Implementation Plan

Vince McElhinny

Bank Information Center

October 6, 2014

As the World Bank moves forward on plans to define a Global Practice safeguards model, any options

that the Bank is considering for reorganizing the safeguard function should be discussed openly and

assessed on the basis of agreed upon criteria before reaching final decisions on the new organizational

structure. Based on internal Bank evaluations and management proposals, this paper identifies some of

those criteria. Effective implementation of the World Bank safeguards requires a robust, independent

critical mass of environmental and social safeguard expertise with adequate budget, skill mix, clear and

appropriate reporting line, proper incentives and adequate support for strengthening borrower

implementation capacity. Three core reforms are proposed: a 100% increase in safeguard staffing to

correct a long-standing capacity deficit, a commensurate increase in overall annual safeguard budget to

$80 million, and the reinforcement of the independent review responsibility of the Regional Safeguard

Advisors. The paper identifies and makes reform recommendations for seven areas that should be reform

priorities in any Bank proposal to reorganize the safeguard function and broader enabling environment.

ii

Executive Summary: Effective implementation of any future World Bank Safeguard policy framework

that covers all Bank instruments, does not dilute core Bank responsibility and matches the highest

standards, also depends on the proper enabling environment. IEG, among others, has signaled that the

optimal organizational arrangements for effective safeguard implementation are not in place at the World

Bank. A leaked assessment of the Bank's safeguard system by the Bank's internal audit department (IAD)

describes an alarming state of disarray.1 The report validates long standing Independent Evaluation

Group (IEG) and civil society concerns that World Bank's commitment to "do no harm" to people or the

environment has become increasingly compromised by an obscure and underfunded system that allows

safeguards to be routinely shoved to the margin of decision making. With proposed reforms to World

Bank Safeguard policies likely to shift investment to instruments with fewer clear protections, an even

greater burden will be placed on beleaguered and demoralized World Bank safeguard staff.

The IAD report describes a safeguard structure at the World Bank that may be unprepared to assume

these responsibilities due to lack of adequate budget, independence, incentives and line management

protection to do their job effectively. The ongoing corporate strategy implementation process has already

taken decisions and introduced changes to the budget process that could help or hinder the reform to the

incentives, structure and budget for safeguards essential to the effective implementation of a new policy

framework.

By not presenting any content related to a safeguard implementation plan to CODE on July 30th as part of

the plans for Phase II consultations on the proposed safeguard framework, Bank management missed an

important opportunity. Going forward, the World Bank must clarify how the proposed Environmental

and Social Framework and implementation plan must be consulted simultaneously. This paper first

discusses the key features of the World Bank's safeguard organizational structure before and after the July

1, 2014 launch of the Global Practices. In the second section, I discuss priorities for consideration as the

Bank continues to think about how best to reorganize the safeguard function and the enabling

environment to be most effective.

Overall Recommendation: The World Bank's proposal for strengthening the safeguards must explain

the key elements of a Safeguard implementation plan that includes an indicative annual or multi-year

budget, staffing baseline capacity, targets and gap filling actions for relevant skill sets, reforms to the

safeguard organizational structure, including roles and responsibilities of key safeguard actors that

ensure adequate support and independent checks and balance, requirements for the independent

monitoring and reporting of environmental and social outcomes, and incentives for achieving consistent,

reliable good practice.

Specific recommendations for any reorganized Safeguard Implementation Plan at the World Bank

include:

1. Increased staff capacity: Based on estimates of gaps in current baseline Bank capacity and

projected shifts in portfolio risk and safeguard coverage, increased World Bank Group

safeguard staffing capacity (by at least 100%) and skill mix are needed to enhance safeguard

support and effective policy compliance during project planning, preparation, supervision, and

evaluation.

2. Budget size and control: The World Bank should allocate to the appropriate safeguard Director

or Manager level independent control over adequate, off-the-top resources approved on an annual

1 World Bank Internal Audit Department (IAD) - Advisory Review of the Bank's Safeguard Risk Management, June 16, 2014.

The report is based on surveys and interviews with 148 social and environmental Bank specialists, project leaders and

management, a review of the investment project portfolio, including and in-depth review of 21 projects.

iii

basis to ensure effective implementation of the safeguard policies. Based on World Bank and

other MDB safeguard systems, a minimum safeguard annual budget should be between $60 -

$80 million, depending on several factors.

3. Independence: The safeguard organizational structure must ensure independence and

accountability at all phases of the project cycle, at a minimum, by strengthening the Regional

Safeguard Advisor project clearance authority at concept and appraisal stages.

4. Clear line management: The World Bank requires a Vice-President level champion for

safeguards and a single, clear line management of authority and guidance to ensure that senior,

more experienced safeguard staff are assigned to higher risk projects.

5. Incentives: Revise rewards and recognition for safeguards work in World Bank Performance

Evaluations. Performance evaluations should transparently reward the higher quality of operation

outcomes or impacts (including positive safeguards implementation outcomes) in addition to

contribution to volume of lending approvals, among other factors.

6. Increased resources for safeguard capacity strengthening: Provide dedicated resources for

greater safeguard implementation training for Bank and Borrower specialists, managers and

executives.

7. Reporting safeguard outcomes: Strengthen accountability for better planning, tracking,

reporting and learning about portfolio environmental and social risk, safeguard costs and

development benefits, including expanded use of independent and community monitoring of

higher risk projects, input from independent experts, and the publication of an annual Global

Reporting Initiative (GRI) format Sustainability report that discloses disaggregated portfolio risk

and Bank capacity to manage that risk.

iv

Table of Contents

I. World Bank Safeguards Organization before July 1, 2014 .................................................. 2

II. Management proposal for reorganizing the World Bank Safeguards .............................. 4

a. Single, Centralized Safeguard Unit - the path not taken. ............................................ 4

b. Proposal for locating the safeguard staff within Global Practice Vice-Presidency ... 8

III. Seven Recommendations for Greater World Bank Safeguard Effectiveness ................ 11

1. Capacity and skills aligned with development challenges ........................................... 11

a. Estimating Supply of Safeguard Risk in the World Bank Portfolio ......................... 14

b. Estimating Demand for Safeguard Work with Cost Coefficients ............................. 14

2. Independent Control of Safeguard Budget by Safeguard Line Management.............. 19

3. Independent clearance responsibility/accountability...................................................... 22

4. Clear Senior Management structure and reporting line ................................................ 25

5. Safeguard Incentives .......................................................................................................... 26

6. Increase resources for safeguard capacity strengthening .............................................. 27

7. Strengthen Accountability for better tracking, reporting and learning

about Portfolio E&S risk, Safeguard costs and development benefits .............................. 28

Annex A: Explanation of Calculations for Safeguard Budget ................................................ 31

A. Fixed Costs: Staff Salary and Budget ............................................................................ 31

B. Variable Costs: Consultants, Travel and Training ........................................................ 36

C. Total Safeguard Budget .................................................................................................... 38

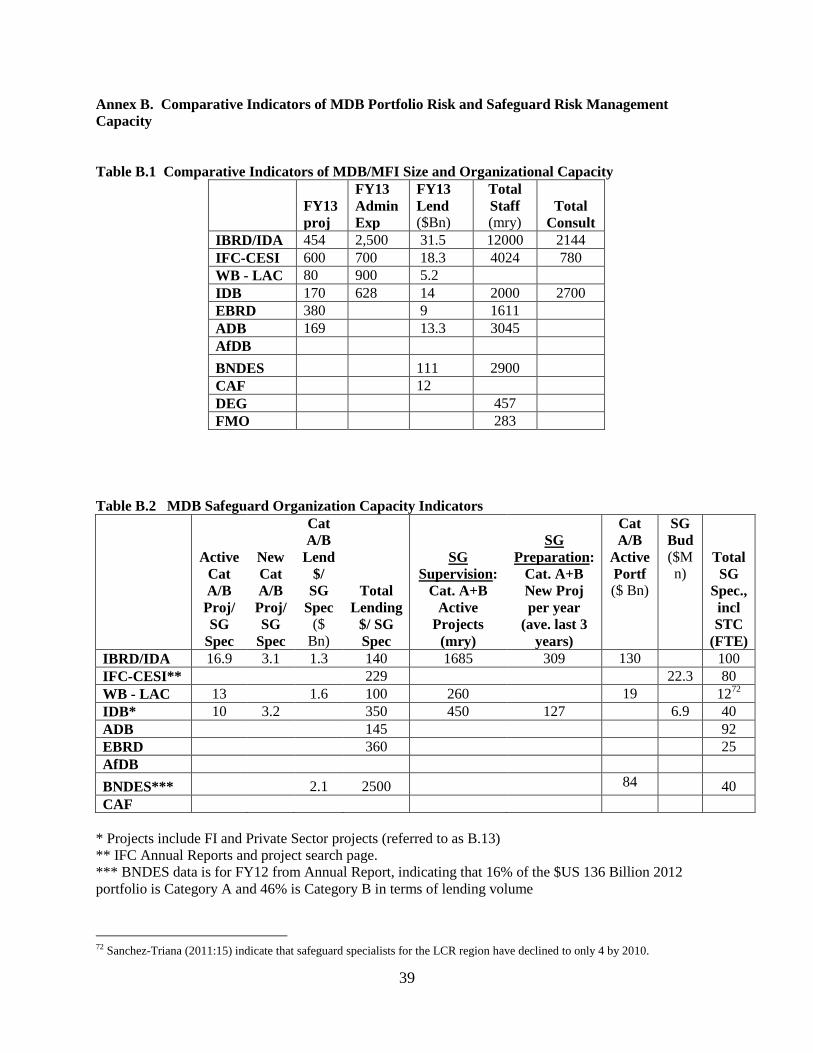

Annex B. Comparative Indicators of MDB Portfolio Risk and Safeguard Risk

Management Capacity ................................................................................................................ 39

List of Figures

Figure 1. World Bank Existing Safeguard Organizational Structure (IEG, 2011) ........................ 5

Figure 2. Safeguard Organization Option 1-Structured SG Cluster within Global Practices VP.. 9

Figure 3. Distribution of IBRD and IDA Lending Volume by Environmental Categorization

(FY90-FY14) ................................................................................................................................ 12

Figure 4. Distribution of World Bank FY10-FY14 Lending by Environmental Categorization . 12

Figure 5. Number of World Bank Projects per Safeguard Specialist by Region (2010) ............. 13

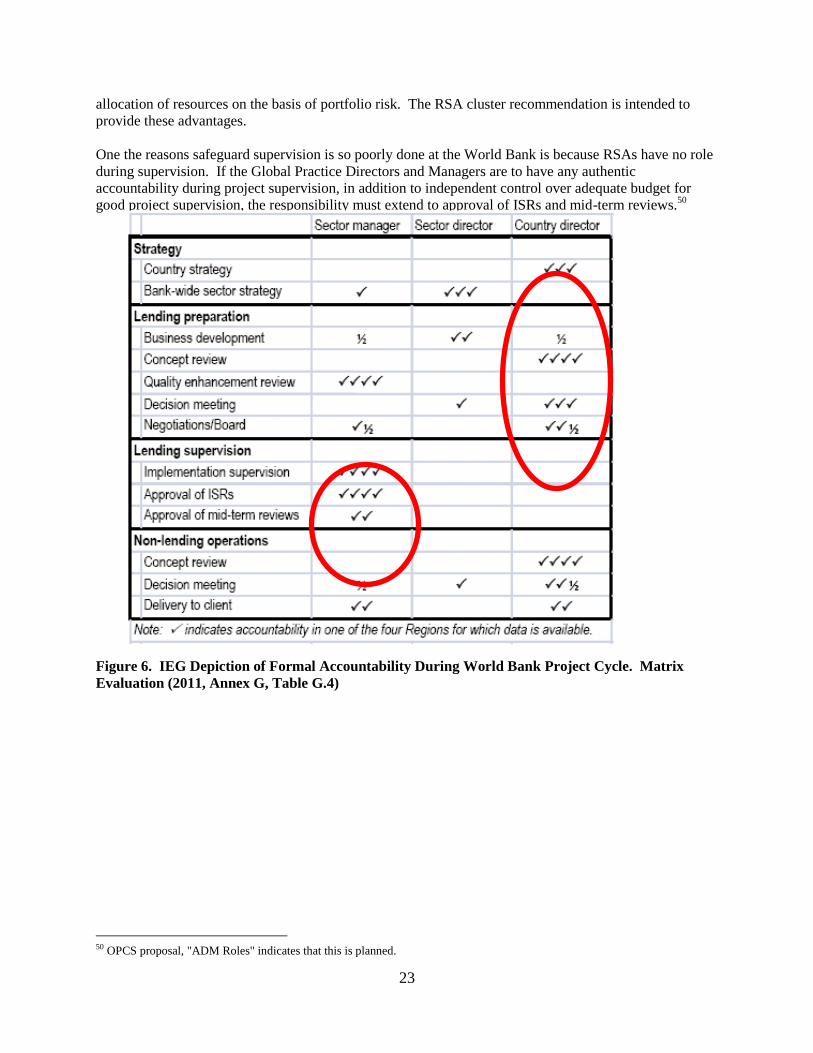

Figure 6. IEG Depiction of Formal Accountability During World Bank Project Cycle. Matrix

Evaluation (2011, Annex G, Table G.4) ....................................................................................... 23

Figure 7. Proposed Accountability in the Investment Lending Project Cycle, OPCS Jan. 30,

2014............................................................................................................................................... 24

List of Tables

Table 1. Current World Bank Regional Safeguard Advisors, and E&S Practice Managers ......... 7

Table A.1. World Bank Staff Salary Structure 2013 ................................................................... 31

Table A.2 OPCS 2013 Estimate of World Bank Environmental Safeguard Capacity ............... 32

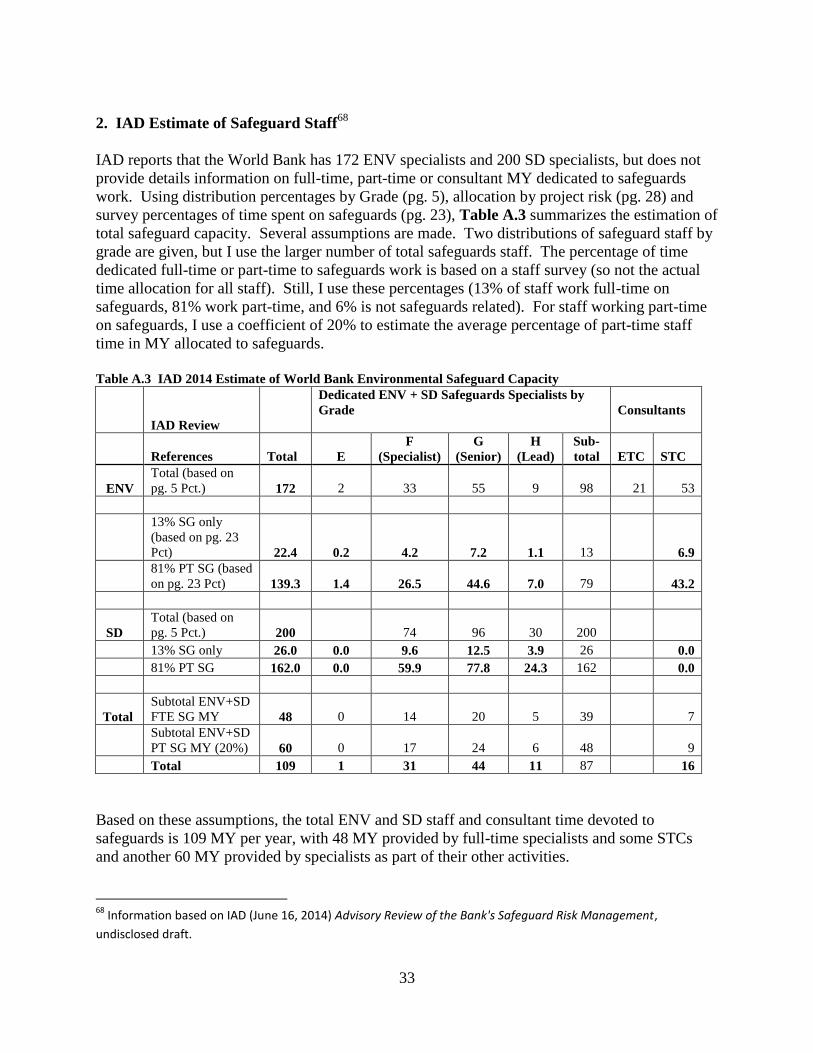

Table A.3. IAD 2014 Estimate of World Bank Environmental Safeguard Capacity .................. 33

Table A.4. Environmental Safeguard Fixed Costs (Staff Salary and Benefits) ........................... 35

Table A.5. Summary of World Bank Safeguard Fixed Cost Estimates for three scenarios ........ 35

v

Table A.6. World Bank FY14 RSA Budget ................................................................................ 36

Table A.7. Estimate of World Bank Safeguard Travel Expenses ............................................... 37

Table A.8. Summary of Estimated World Bank Safeguard Budget (Baseline Scenario,

OPCS and BIC proposals) ............................................................................................................ 38

Table B.1 Comparative Indicators of MDB/MFI Size and Organizational Capacity.................. 39

Table B.2 MDB Safeguard Organization Capacity Indicators................................................... 39

1

Acknowledgements

This report was made possible by the generous support of the Gordon and Betty Moore Foundation. I am

grateful as well for the contribution of time and thoughtful analysis by many people currently and

formerly employed at the World Bank Group, as well many others working in shareholder governments

of the Bank. The nature of the material on which the report is based, including documents and

information that is not officially made available to the public by the Bank, underscore the challenge of

full public acknowledgement. My knowledge of how safeguards have worked and could work better at

the Bank has also benefited from continuous exchange with colleagues at the Bank Information Center,

and partners. The author takes responsibility for all errors, but is hopeful that those found will not

discourage further opportunity for increasingly open and informed debate about the shared goal of

building the optimal enabling environment for effective safeguards in the future.

2

I. World Bank Safeguards Organization before July 1, 2014

The World Bank Safeguard Policy Review is premised on the recognition of systemic problems with the

World Bank's implementation of its existing policies. The 2010 Independent Evaluation Group (IEG)

evaluation of WBG safeguard performance pointed to several areas of priority for reform, also echoed in

phase I consultations: inconsistent risk categorization, gaps in risk coverage, the lack of project safeguard

supervision or outcome reporting, inconsistent safeguard application for lending through frameworks and

borrower systems, and poor leverage of the full range of safeguard benefits, including contributions to

sustainability and economic development.2

Concerns have been expressed both inside and outside the Bank about the perceived limitations of the

existing organization and management of World Bank safeguards staff. IEG argues that without

appropriate organizational reforms, the expected improvements in safeguard policy performance will not

happen. Three groups currently carry out complementary Safeguard functions at the WB, but their

organization is confusing, they lack independence (in terms of budget control), adequate capacity, proper

incentives, and clear line management. These internal challenges will limit the effectiveness the World

Bank safeguard organization model.

The implementation of the Corporate Strategy at the World Bank and the simultaneous revision of the

Bank’s safeguard policies both present the opportunity to assess and consider proposals for organizing the

Bank’s safeguard function. However, World Bank management has yet to provide a space to make

safeguard organization and implementation reforms a more integral part of the ongoing consultation

process.3 Instead, substantive reforms to the organization of safeguard function within the World Bank

are underway without a public discussion. An options analysis for safeguard re-organization was done in

October 2013 and those options have either been decided or are now under review by Bank management

in the context of the definition of the Global Practices and the implementation of the new Corporate

Strategy.

This paper is based on the safeguards organizational model proposed by the Bank as of July 1, 2014. This

note proposes how such an approach should be guided by seven vital principles for strengthening the

Bank’s overall safeguard capacity: 1) Ensuring adequate capacity and skills aligned with development

challenges; 2) Safeguard budget control; 3) Independent project clearance responsibility/accountability;

4) Clear Senior Management structure and reporting line; 5) Incentives; 6) Increased resources for

safeguard capacity strengthening and 7) Accountability for reporting safeguard results.

Understanding the options for change hinge on understanding how safeguards have been organized at the

World Bank before the current reorganization. The short summary of the Bank's safeguard function that

follows is limited by the absence of any clear description of this topic outside the Bank.4 The Bank's

safeguard function, including staff incentives and accountability that existed prior to the Global Practices

and new Corporate Structure were officially launched on July 1, 2014 has evolved over several recent

organizational reforms. Several complementary and interacting units carry out the Bank's safeguard

duties.

Safeguard Support and Quality Assurance: The World Bank has between 300 and 350 staff with

environmental and social safeguard expertise that devote some percentage of their time to support of

2 A. Dani, A. Freeman, and V. Thomas, Evaluative Directions for the World Bank Group's Safeguards and Sustainability

Policies, Evaluation Brief 15, 2011, The World Bank Independent Evaluation Group. 3 In addition to the lack of management response to prior drafts of the current proposal, see FPP, BIC, Urgewald (April, 2013)

submission on Safeguard Implementation to Safeguard Review, Phase I 4 This section is based on interviews with over 50 Bank staff since 2009 as well as a review of numerous project and policy

documents.

3

project preparation or supervision support.5 Safeguard work is substantially understaffed given the 2400

active investment finance projects and a lending portfolio of $170 Billion.6 These safeguard quality

assurance functions were mapped until recently to one of the six regions, while a small number of staff

were mapped to the Environment or Social Development Network Anchors, and reported to Sector

Managers and Directors. Most of these environmental and social specialists combined two types of work:

the provision of safeguard cross-support to projects and the direct management of climate change, carbon

financing, technical analysis, and other lending projects in their sector, both independently and as part of

teams in other sectors. The Country Management Units and specific Task Team Leaders within each

Regional Vice-Presidency have exercised control over a large share of the Bank's annual administrative

budget to contract the services of safeguard specialist services through work program agreements. The

demand for safeguard support and supervision is determined by the project manager.

The creation of the Quality Assurance and Compliance Unit (QACU) and the Environmental and

International Law Unit (LEGEN) of the Legal Department, ensured more centralized guidance for

safeguard application during project preparation. Since 2004, QACU (which included six Regional

Safeguard Advisors, RSAs) and LEGEN have provided guidance for the most complex safeguard

operational challenges, and retained safeguard monitoring responsibility for the Bank's highest risk

projects. Despite the title Advisor, the RSAs exercise project clearance authority at concept and appraisal

stages of project preparation for the highest risk projects. The responsibility is delegated to Sector

Manager for some Category B and C projects at appraisal.

A significant restructuring of safeguard functions was introduced in 2006. Before then, both the

safeguard support and clearance functions were located in the same network (Environmentally and

Socially Sustainable Development (ESSD). In response to concern over a perceived conflict of interest

resulting from both support functions (that have vested interests in the approval of the project) and

compliance functions reporting to the same Director and VP, the compliance function led by the Regional

Safeguard Advisors was relocated from ESSD to Operational Services group within OPCS. As IEG

observes, "the World Bank consolidated the Environmentally and Socially Sustainable Development

Network (ESSD) and the Infrastructure Network—into the Sustainable Development Network (SDN)

under one vice president, bringing the environmental and social staff and their internal clients from the

infrastructure and agricultural sectors under one umbrella." 7 Under this arrangement, QACU continued

to rely largely on the technical staff in the regional environmental and social units to conduct due

diligence and appraisal.

While some viewed safeguards and other operations activities as too close under ESSD, the reform has

also fueled a perception that the division of labor between OPCS and SDN may have moved safeguards

into an untenable position that is often too far removed from fundamental project cycle decisions.

As IEG explains, understanding how the administrative budget has been allocated helps illustrate the

concerns about the effectiveness of the current safeguard model, particularly for project supervision. The

budget for safeguard staff to support project preparation and supervision is controlled by the project task

team leader. The intensity and range of safeguard appraisal and supervision is determined not by a

Safeguard Manager or Director, but rather by the TTL judgment in what some view as an excessively

subjective and unpredictable resource allocation model. The RSAs receive a small off-the-top budget

from OPCS for review and clearance work and there are some measures for adjusting project budgets to

5 A recent internal audit identified 172 Environmental specialists and 200 Social Development specialists at the Bank, who

presumably had some level of safeguard expertise. See IAD, Advisory Review of the Bank's Safeguard Risk Management, (June

16, 2014) undisclosed summary draft. 6 Based on Bank reported data on Sep. 8, 2014, does not include 115 DPOs, 20 PforR and over 100 unclassified projects. IAD

(2014) reports 2,355 IPF projects active as of Feb. 2014. 7 IEG 2011, pg. 15

4

add Safeguard capacity. Once a project enters the Bank pipeline (within the total budget allocation to a

VPU) and is allocated by each managing sector, the budget for Safeguard work for higher risk or lower

performing projects can be topped up by the RVPs.

Due in part to safeguard budget control residing within the six Regional Vice-Presidencies, safeguard

staff lack a predictable work plan and a single, clear line management. Technical support staff report to

regionally specific sector managers. Regional safeguard advisors report to a Quality Director within

Operational Services for a specific region.8 QACU (recently renamed as OPSOR) reports to another

Director within OPCS. The specific relationships between CMUs/TTLs, QACU, and Safeguard cross-

support varies for each of the Bank's six regions - there is no single Safeguard system.9 This fragmented

and overlapping management structure leads to confusion and perverse strategies for safeguard

application and oversight. that few outside the Bank understand. IEG argues that reliance on this

"market" approach to contracting safeguard services results in "considerable inefficiencies in resource

allocation for safeguards oversight."10

II. Management proposal for reorganizing the World Bank Safeguards

Efforts to retool and reorganize the Bank safeguard organizational structure are intended to ensure

compatibility with the newly reorganized World Bank Group. On July 1, the Bank formally launched the

Global Practices and taken strides to integrate some World Bank Group functions, such as Human

Resources and External Communications. Other organizational reforms are under discussion and are far

less clear or visible.

Some reorganization decisions not taken are equally noteworthy - the decision not to create a single

Safeguards Global Practice or Cross-Cutting Solution Area, for example. A proposal to merge

Environment and Social Practices was resisted, reportedly by Social Directors, and Social was then

merged with a Global Practice on Urban and Rural Development. Splitting Environment and Social

technical staff into separate GPs may have the benefit of balancing the attention given to social risk

assessment given a perception of a bias toward environmental issues. However, lumping social into a

multi-sector GP and beyond arms length coordination with environmental staff also creates the first

coordination transaction cost and may dilute the authority of both GPs.11

a. Single, Centralized Safeguard Unit - the path not taken.

In considering all options for reforming the World Bank Safeguards structure, a proposal to pool the

safeguard specialists into a single, self-standing and independently managed group was also rejected, as

was the complementary option of merging the World Bank Safeguard groups with the IFC's Environment

and Social Development Department (CES).

Similar to IFC, EBRD, and IDB, which have adopted a centralized safeguard model, such an approach

would have mapped all safeguard support and compliance staff to a single unit that most likely would

have reported to the Vice-President of OPCS. At IFC CES, the social and environmental safeguard

8 Regional Quality Directors assumed the responsibilities for the Quality Assurance Group (QAG), which was dissolved in 2010.

These Directors have dual reporting lines to VP OPCS and RVP. Not clear what happens to Quality Directors under the new

structure (in RVPs)? 9 IAD (2014) 10 IEG 2011, pg 16 11 The debate over where the social development focus would fit within the 14 Global Practices was apparently taken quite late in

the design process.

5

specialists are grouped into respective clusters under 1 or 2 safeguard managers, and report primarily to

the Director for E&S Risk, but provide support to Investment Officers. Social and environmental

safeguard managers coordinate cross-support between groups.

As illustrated in Figure 1, IEG underscores two fundamental differences that distinguish the current

World Bank safeguard model from the IFC. At the IFC, all safeguard staff are housed in a central,

independent unit, which controls its own budget and can therefore assert greater autonomy in allocating

staff resources based on risk.

Secondly, the IFC combines compliance, including the clearing most projects at concept and appraisal

and the handling of the highest risk projects, and support within a single reporting line to Senior Director

and a Vice-President (Advisory Services). The IFC provides a firewall of budget independence between

safeguard staff and project managers as well as a much clearer reporting line for safeguard staff. IEG

asserts that IFC has budget authority, which helps resolve the internal conflict of interest presumed to

result from integrating support and compliance functions.12

Figure 1. World Bank Existing Safeguard Organizational Structure (IEG, 2011)

A single CES Director controls the $22 million annual budget for all IFC safeguard function activities.13

The E&S Director prepares an annual project preparation and supervision plan and independently

allocates supervision staff resources based on risk.

The E&S Risk Director is responsible for knowing the risk spread across the actual and projected IFC

portfolio as well as alignment with current CES safeguard staff capacity. The E&S Director and

Managers are responsible for training and certification of CES staff, which includes maintaining and

12 Procurement support and oversight also sit within the newly created Governance Global Practice. Despite sharing many of the

same sensitivities associated with Safeguards, there is much less concern with co-location of both procurements quality assurance

and control under the same line management and budget. 13 The IFC budget figure does not reflect the full cost of safeguards work in that IFC, more so than the Bank, can charge project

preparation costs to the client.

6

reporting annually on the roster or IFC and consultant staff capacity for the safeguard function. IFC's

E&S Director is responsible for reporting on safeguards outcomes for producing knowledge products that

ensure systemic learning from safeguard performance.

Some of the primary differences and possible advantages of a centralized safeguard unit favored by IFC

and others compared to current decentralized safeguard model preferred by the World Bank include:

CES has independent budget control of all safeguard quality assurance/support and quality

control activities, which facilitates annual planning and provides incentives for a more rational

approach to supervision

Compliance and Technical Support are co-located within the same unit, which preserves

independence but enhances consistency and optimizes resource allocation of SG staff

All safeguard staff are mapped full time to same Vice-Presidency with clear reporting line to a

single VP, which allows for a more coherent career path and incentive structure

A robust, critical mass of safeguard staff devote all time to safeguard support or oversight, which

enhances the ability to defend the safeguard value proposition.

The primary risks of the IFC model for the Bank include:

The centralized models hinges on having the right person and adequate budget to effectively lead it.

Safeguard specialist incentives may be effected by perception of a more limited set of career path

options, induced by the lack of operational management options. The result could be a less talented

pool of specialists.

Compliance and support functions located within the same reporting line could present a conflict of

interest.14

Without strong links to the regional operational structures, a central pooled staff may not be well

coordinated with safeguards challenges when they first arise or be close enough to the client to

adequately strengthen and use borrower safeguards systems.

The decision not go farther in integrating the IFC and World Bank safeguard structures may reflect the

limited progress in achieving greater World Bank - IFC integration in general. This has been

accompanied by the migration of some IFC safeguard staff, including a CES senior manager, to the Bank

Environment and Social, Urban, Rural and Resilience Global Practices.

Embedding safeguards within the Global Practices: Instead, Bank management has decided to locate

the majority of environmental and social specialists in the Global Practices. A gradual implementation of

the Global Practices began on July 1, 2014 without full clarity about the pending decisions related to any

reorganization of the safeguard function. A memo from the Directors in the ENRM (GP4) and Social,

Urban, Rural, Resilience (GP13) Global Practices described the interim arrangements for managing

safeguards after July 1.15

Referring to the new Accountability and Decision Making framework, the

memo assures that there will be few immediate changes to the safeguard procedures of the past. The

decision was taken early in 2014 to map all Regional Safeguard Advisors and their team to OPCS, which

would now provide the RSA budget.16

RSAs will continue to review and clear investment concepts

(PCN) and appraisal packages (PAD). RSAs may transfer projects for further review to Sector/Practice

Managers - who have final clearance authority.

14 Worth noting is that procurement and financial management both belong to Governance GP without apparently triggering the

same concerns of a conflict of interest. 15 Maninder Gill and Bilal Rahill, Arrangements for Managing Safeguards Beginning July 1, 2014. 16 The decision was taken in April, 2014. Until FY15, RSA budget was paid by the Regional Vice-Presidencies. Other Regional

Operation Services previously mapped to the Regions with joint reported to OPCS, will be reportedly mapped to the Global

Practices.

7

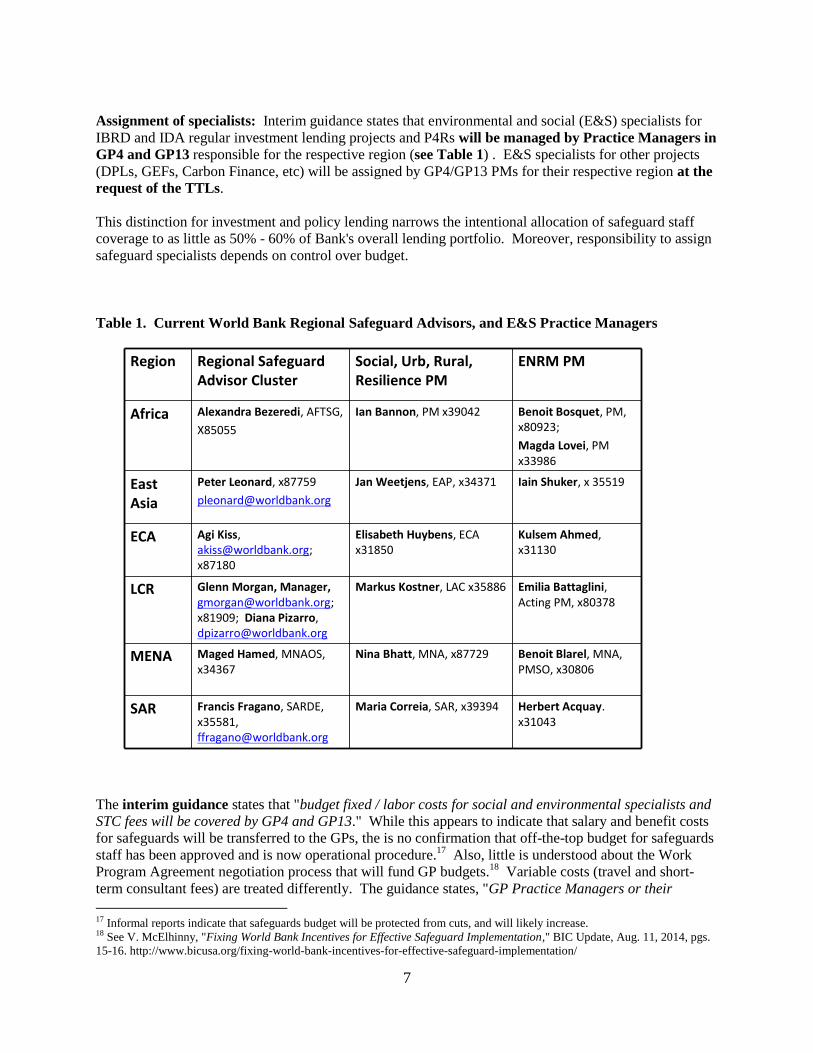

Assignment of specialists: Interim guidance states that environmental and social (E&S) specialists for

IBRD and IDA regular investment lending projects and P4Rs will be managed by Practice Managers in

GP4 and GP13 responsible for the respective region (see Table 1) . E&S specialists for other projects

(DPLs, GEFs, Carbon Finance, etc) will be assigned by GP4/GP13 PMs for their respective region at the

request of the TTLs.

This distinction for investment and policy lending narrows the intentional allocation of safeguard staff

coverage to as little as 50% - 60% of Bank's overall lending portfolio. Moreover, responsibility to assign

safeguard specialists depends on control over budget.

Table 1. Current World Bank Regional Safeguard Advisors, and E&S Practice Managers

Region Regional Safeguard Advisor Cluster

Social, Urb, Rural, Resilience PM

ENRM PM

Africa Alexandra Bezeredi, AFTSG,

X85055

Ian Bannon, PM x39042 Benoit Bosquet, PM, x80923;

Magda Lovei, PM x33986

East Asia

Peter Leonard, x87759

Jan Weetjens, EAP, x34371 Iain Shuker, x 35519

ECA Agi Kiss, [email protected]; x87180

Elisabeth Huybens, ECA x31850

Kulsem Ahmed, x31130

LCR Glenn Morgan, Manager,[email protected]; x81909; Diana Pizarro, [email protected]

Markus Kostner, LAC x35886 Emilia Battaglini, Acting PM, x80378

MENA Maged Hamed, MNAOS, x34367

Nina Bhatt, MNA, x87729 Benoit Blarel, MNA, PMSO, x30806

SAR Francis Fragano, SARDE, x35581, [email protected]

Maria Correia, SAR, x39394 Herbert Acquay. x31043

The interim guidance states that "budget fixed / labor costs for social and environmental specialists and

STC fees will be covered by GP4 and GP13." While this appears to indicate that salary and benefit costs

for safeguards will be transferred to the GPs, the is no confirmation that off-the-top budget for safeguards

staff has been approved and is now operational procedure.17

Also, little is understood about the Work

Program Agreement negotiation process that will fund GP budgets.18

Variable costs (travel and short-

term consultant fees) are treated differently. The guidance states, "GP Practice Managers or their

17 Informal reports indicate that safeguards budget will be protected from cuts, and will likely increase. 18 See V. McElhinny, "Fixing World Bank Incentives for Effective Safeguard Implementation," BIC Update, Aug. 11, 2014, pgs.

15-16. http://www.bicusa.org/fixing-world-bank-incentives-for-effective-safeguard-implementation/

8

designees will hire the necessary STCs, as required and agreed through the budget allocation exercise

managed by GP4 and GP13. All travel costs will be covered by the budget of the respective projects to

ensure coordinated preparation of the missions. For DPLs, GEFs, and Carbon Finance, the fixed and

variable costs will continue to be covered by the respective projects." Left unclear is how the budget

allocation exercise to determine variable costs will work.

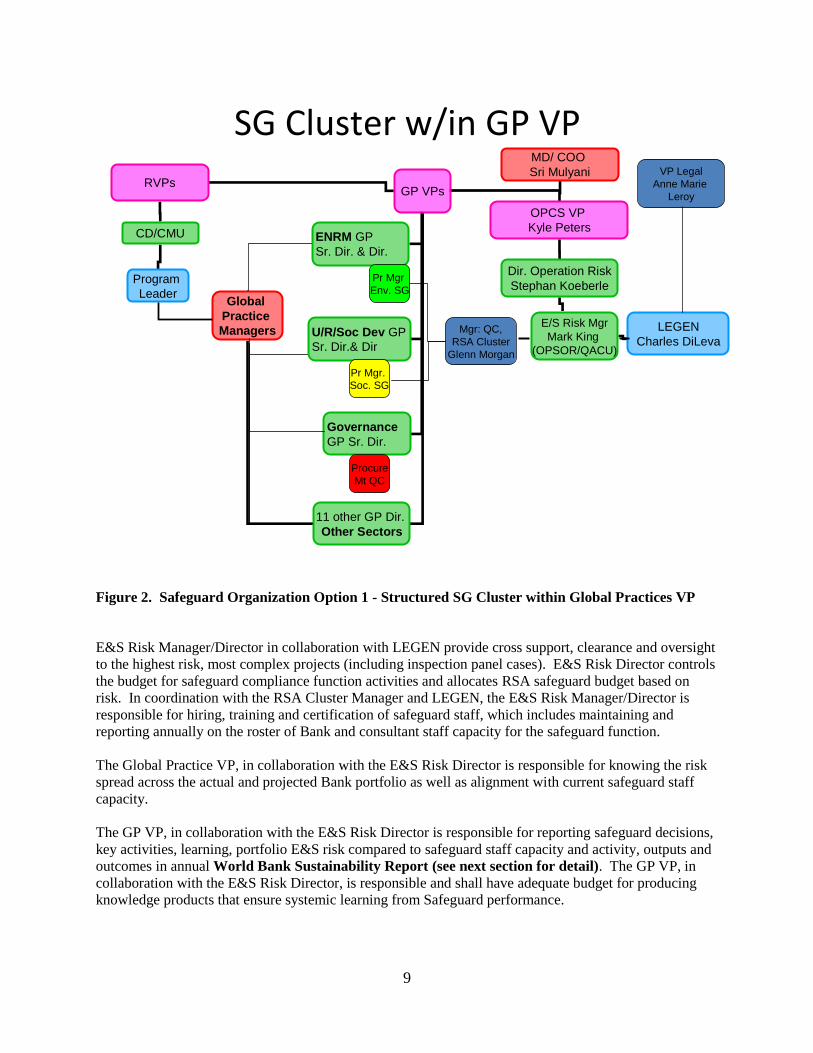

b. Proposal for locating the safeguard staff within Global Practice Vice-Presidency

Building on the interim guidance and the alternative model for organizing the safeguard function within

the Global Practices, for which the Bank has opted, strengthening the safeguard function in this model

would involve several critical reforms. Under such a model (see Figure 2), all safeguard technical cross-

support specialists would be mapped to the ENRM-GP4 and SURR-GP13 Global Practices and should be

grouped as an autonomous unit within those GPs.

An adequate budget for safeguard support (both preparation and supervision) should be controlled by a

safeguard Unit Manager for each of the environmental and social safeguard units. Allocation of

safeguard staff for support and supervision of projects is decided by safeguard Unit Managers in

coordination with GP Managers and each other. As early as possible in the project cycle, RSAs help

trouble-shoot and mediate potential disagreements between safeguard and GP managers regarding

appropriate level of safeguard staff time on the project and other safeguard policy interpretation issues

(related to RSA project clearance authority). GP Director, in coordination with environmental and social

safeguard Unit Managers, prepares annual project preparation and supervision plans (based on CPF

Safeguard business plans - see Recommendation 7 below) and allocates supervision staff resources based

on risk.

The environmental and social (E&S) Risk Director and RSA Cluster Manager (now both part of OPSOR),

in collaboration with LEGEN are accountable for safeguard compliance. As noted in the interim

guidance, all six RSAs will be grouped in a single cluster under a single Director/ Manager with expanded

capacity and budget autonomy. The RSA Manager reports to the E&S Risk Manager/Director. RSA

Manager and in some cases, E&S Risk Manager/Director advise GP VP on resolution of all safeguard

related disagreements between GP Managers or Directors. RSAs clear all projects at concept and

appraisal, exercising authority to transfer some projects to Practice Managers for approval.

9

SG Cluster w/in GP VPMD/ COO

Sri Mulyani

GP VPs

OPCS VP

Kyle Peters

RVPs

E/S Risk Mgr

Mark King

(OPSOR/QACU)

CD/CMU

Program

Leader

ENRM GP

Sr. Dir. & Dir.

U/R/Soc Dev GP

Sr. Dir.& Dir

Governance

GP Sr. Dir.

Mgr: QC,

RSA Cluster

Glenn Morgan

Pr Mgr

Env. SG

Pr Mgr.

Soc. SG

Procure

Mt QC

11 other GP Dir.

Other Sectors

Global

Practice

Managers

Dir. Operation Risk

Stephan Koeberle

LEGEN

Charles DiLeva

VP Legal

Anne Marie

Leroy

Figure 2. Safeguard Organization Option 1 - Structured SG Cluster within Global Practices VP

E&S Risk Manager/Director in collaboration with LEGEN provide cross support, clearance and oversight

to the highest risk, most complex projects (including inspection panel cases). E&S Risk Director controls

the budget for safeguard compliance function activities and allocates RSA safeguard budget based on

risk. In coordination with the RSA Cluster Manager and LEGEN, the E&S Risk Manager/Director is

responsible for hiring, training and certification of safeguard staff, which includes maintaining and

reporting annually on the roster of Bank and consultant staff capacity for the safeguard function.

The Global Practice VP, in collaboration with the E&S Risk Director is responsible for knowing the risk

spread across the actual and projected Bank portfolio as well as alignment with current safeguard staff

capacity.

The GP VP, in collaboration with the E&S Risk Director is responsible for reporting safeguard decisions,

key activities, learning, portfolio E&S risk compared to safeguard staff capacity and activity, outputs and

outcomes in annual World Bank Sustainability Report (see next section for detail). The GP VP, in

collaboration with the E&S Risk Director, is responsible and shall have adequate budget for producing

knowledge products that ensure systemic learning from Safeguard performance.

10

Primary differences and advantages of this proposal compared to current World Bank safeguard model:

Global Practices have independent safeguard budget control for most fixed and variable costs related

to core safeguard function activities

Safeguard compliance and technical support are separated between GP and OPCS to avoid any

possible or perceived conflict of interest.

All safeguard cross-support staff are mapped full time to VP GP with clear reporting line to a single

VP.

All safeguard cross-support staff devote all/most time to SG support or oversight.

RSA Cluster capacity is fully integrated, expanded and coordinated by a single Manager.

Safeguard staff have somewhat more coherent and positive career path and incentive structure (still

some incentive tension in the GPs between Operations and Support technical staff)

Increased reporting requirements on corporate safeguard performance, including knowledge products.

Some of the primary risks that remain with this approach include:

This model is less appealing to safeguard staff that also want to act as project task managers or help

deliver projects. Balancing safeguards with operations management could strike the right balance in

the incentives for safeguard specialists. However, the risk of mixing safeguards and project delivery

actions could be to dilute the safeguard focus into a generalist environmental or social approach. In

other words, a single environmental safeguards expert should not be expected to manage risk

assessment for hydrological flows, deforestation, urban air and water contamination and carbon

taxing policy reforms. Providing high level safeguard advice and support requires both an advanced

level of knowledge of specific complex technical issues that are unique to each sector, as well as

ability to identify inter-sectoral linkages and externalities. This trade-off risk between safeguards and

more career enhancing project delivery duties is evident in the current Bank structure.

Tendency toward fragmentation of safeguard support into many GPs as transport, energy, agriculture

and water directors under pressure to achieve greater efficiency gains recruit trusted safeguard experts

to remain within their GP, diminishing further the critical mass authority needed for effective

safeguards implementation and increasing coordination transaction costs.

Without clear protection or enhanced incentives from a dedicated and independent safeguard

management, embedded safeguard specialists in the GP VP reporting line that has little expertise in

this field may leave the perception that they are less well positioned for career progression or more

susceptible to reprisals for the discharge of their safeguard functions.

As the World Bank moves forward on plans to define a Global Practice safeguards model, any options

that the Bank is considering, including the ones outlined above, should be discussed openly and assessed

on the basis of these criteria before reaching final decisions on the new organizational structure.

Effective implementation of the World Bank safeguards requires a robust, independent critical

mass of environmental and social safeguard expertise with adequate budget, skill mix, clear and

appropriate reporting line, proper incentives and adequate support for strengthening borrower

implementation capacity. In the following section, these safeguard organizational principles are

explained.

11

III. Seven Recommendations for Greater World Bank Safeguard Effectiveness

1. Capacity and skills aligned with development challenges

Recommendation 1: Based on estimates of gaps in current baseline Bank capacity and projected

shifts in portfolio risk and safeguard coverage, increased World Bank safeguard staffing capacity

(by at least 100%), and skill mix are needed to enhance safeguard support and effective policy

compliance during project planning, preparation, supervision, and evaluation.

By many standards and internal accounts, the World Bank lacks the capacity to assure safeguard

management in project preparation and supervision commensurate with risk and environmental impact.19

A gap exists between current capacity and actual or projected risk in the portfolio or the transformational

development challenges that the Bank is attempting. This gap is leaving the Bank vulnerable to an

unacceptable level of risk of non-compliance with current safeguard policies and compromising the

quality and integrity of a number of Bank financed projects. The staffing shortage is also hindering the

ability of Bank Safeguard specialists to adequately undertake other aspects of their mandate, including

addressing emerging issues.

IAD confirms that he Bank lacks an updated, accurate understanding of the spread of safeguard risk

across its portfolio and can not report the total amount or allocation of resources spent on safeguard

implementation. Lack of updated or complete portfolio safeguard risk data make any precise assessment

of this gap difficult to impossible. The Bank lacks an updated baseline of current social and

environmental safeguard staff capacity based on areas of skill and extent of certified expertise. As a

result, IAD reports that "over half of active projects, including some high risk projects do not have

assigned safeguard specialists,... high grade specialists are not necessarily assigned to high risk

projects." 20

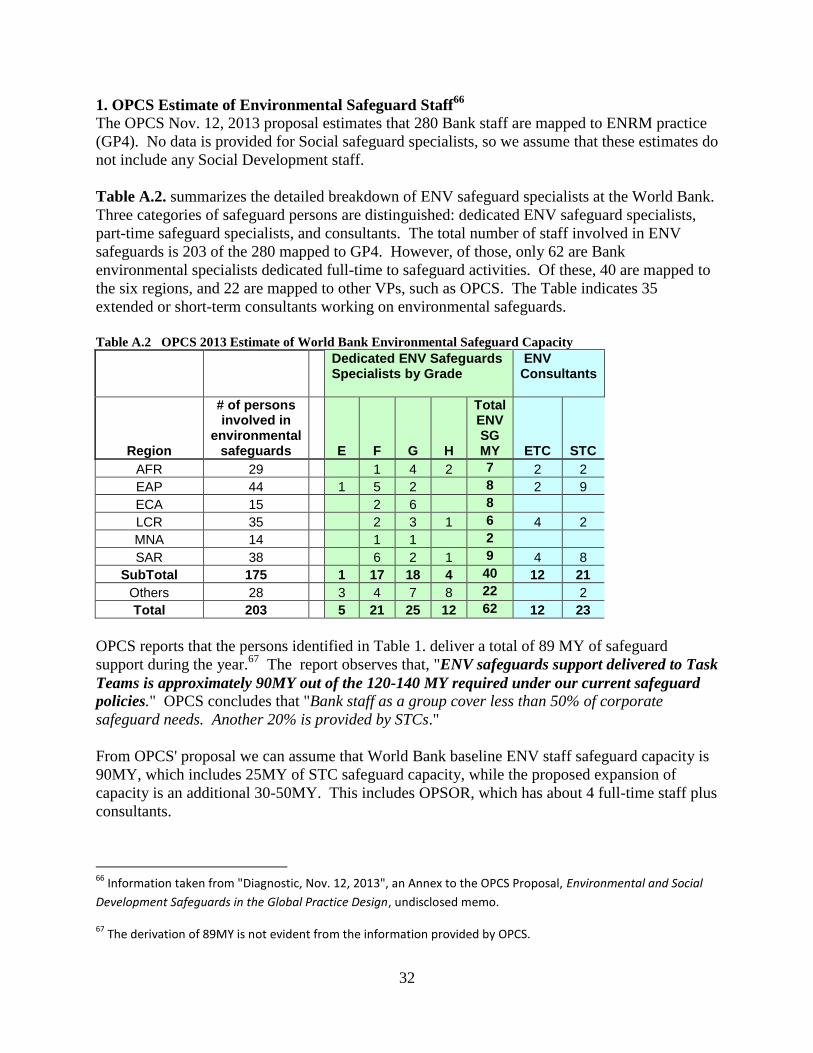

The number of staff for IBRD and IDA mapped to ENRM Global Practice is 280 and another 525 to

Rural, Urban and Social Development Global Practice. IAD reports that Environment and Social

Development Sectors identified 172 and 200 specialists, respectively (perhaps only a third of which work

on safeguards full-time). Of the 372 ENV or SD specialists identified by IAD, only 50% were full-time

grade GG or higher.21

When discounting for part-time and staff less specialized in safeguards, a lower

estimate of safeguard specialists at the Bank is approximately 100.22

The Bank has approximately $55 Billion in Category A investment lending in the active portfolio (285

projects, or 12% of all investment projects) and another $92 Billion in Category B investment lending

(1,400 projects, or 58% of all investment projects) out of 2,730 projects valued at approximately $197

Billion on the books. In FY14, the distribution of newly approved IBRD and IDA investment projects is:

19 See IEG (2010) Safeguards and Sustainability Policy in a Changing World, particularly summaries of focus group interviews;

see also, E.Sanchez-Triana, L. Ortolano, G. Ruta, G. Desfuli, and R. Kanakia (March 2011) Implementation of Environmental

Policies, unpublished Environmental Strategy Analytical Background Paper, pgs. 15-30;, more recently, see IAD (2014)

Advisory Review of the Bank's Safeguard Risk Management. 20 IAD (2014: 26-30) 21 IAD (2014: 5) 22 Based on interviews with Bank staff, IAD 2014 Safeguard Review and OPCS Safeguard Diagnostic, "Environment and Social

Development Safeguards in the Global Practice Design," unpublished memo, November, 2013. The Bank refers only to persons

involved in Environmental Safeguards, which may not include social safeguard specialists. However, Sanchez-Triana et al

(2011) argue that of the 229 regular/term staff mapped to environment, only a third of these staff tend to spend a majority of their

time working on safeguards.

12

Category A (41), Category B (269), Category C (144), Category FI (7), and 8 Guarantees.23

Figures 3 &

4 show the distribution of environmental categorization for IBRD and IDA lending over a 25 year history

and for FY14, respectively.

The two charts indicate that Category A projects are about one-fifth of the total Bank portfolio by lending

volume. Category B project volume are about two-fifths, increasing at the expense of Category C

projects over time. About 25% - 35% of the Bank's long-term portfolio is not properly categorized for

environmental risk.24

Distribution of Env. Categorization of

IBRD/IDA Lending Volume (1990-2013) $US

DPL

21%

A

17%

C

23%

B

35%

Other

4%

Figure 3. Distribution of IBRD and IDA Lending Volume by Environmental Categorization (FY90-

FY14)

World Bank FY09-FY14 Ave. Lending by Env. Categorization (%)

7%

47%

29%

13%

4%

19%

37%

8%

31%

5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

A B C DPL Other

No. of Projects Volume of Lending

Figure 4. Distribution of World Bank FY10-FY14 Lending by Environmental Categorization

23 Based on World Bank data, in addition to 63 DPLs, 11 PforR, 4 Carbon Offset, and 1 uncategorized project. 24 IAD (2014:7) puts the share of projects not categorized for safeguard risk at 50%. For a detailed explanation of the evolution

of Bank lending and environmental risk categorization, see V. McElhinny," Trends in World Bank lending forecast further

decline in safeguard coverage and signs of a return to higher risk and higher reward lending," BIC Info Update. Oct. 7, 2013

13

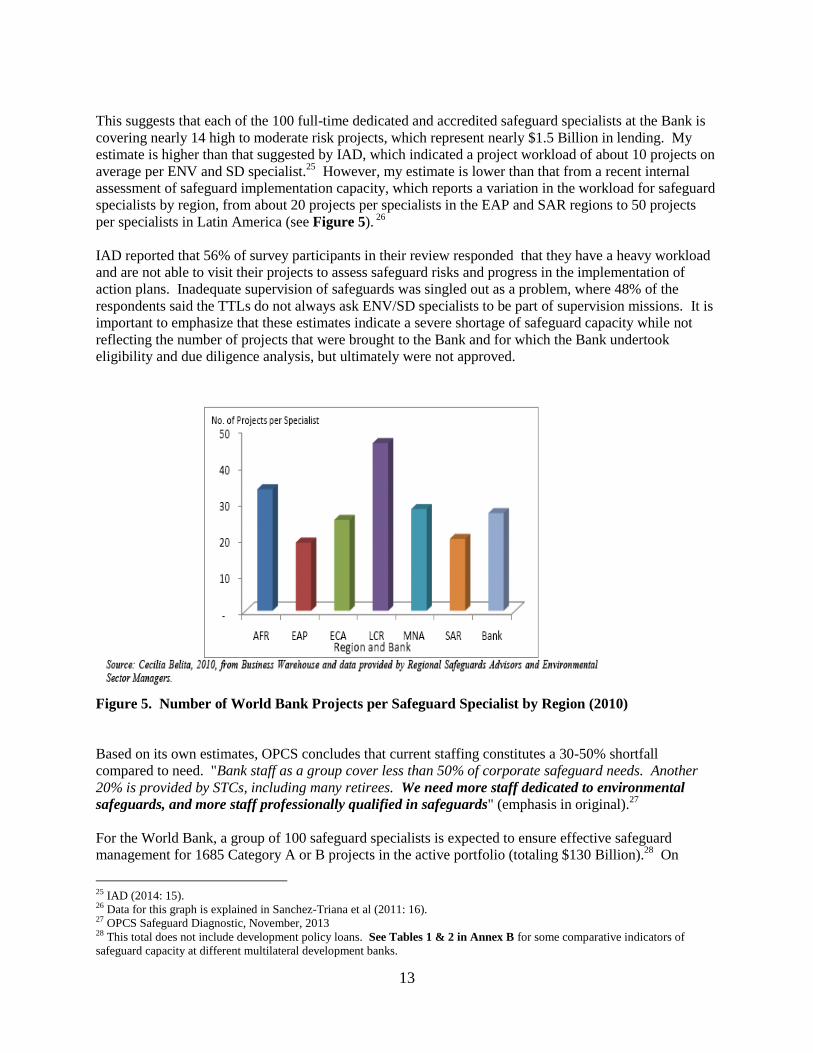

This suggests that each of the 100 full-time dedicated and accredited safeguard specialists at the Bank is

covering nearly 14 high to moderate risk projects, which represent nearly $1.5 Billion in lending. My

estimate is higher than that suggested by IAD, which indicated a project workload of about 10 projects on

average per ENV and SD specialist.25

However, my estimate is lower than that from a recent internal

assessment of safeguard implementation capacity, which reports a variation in the workload for safeguard

specialists by region, from about 20 projects per specialists in the EAP and SAR regions to 50 projects

per specialists in Latin America (see Figure 5). 26

IAD reported that 56% of survey participants in their review responded that they have a heavy workload

and are not able to visit their projects to assess safeguard risks and progress in the implementation of

action plans. Inadequate supervision of safeguards was singled out as a problem, where 48% of the

respondents said the TTLs do not always ask ENV/SD specialists to be part of supervision missions. It is

important to emphasize that these estimates indicate a severe shortage of safeguard capacity while not

reflecting the number of projects that were brought to the Bank and for which the Bank undertook

eligibility and due diligence analysis, but ultimately were not approved.

Figure 5. Number of World Bank Projects per Safeguard Specialist by Region (2010)

Based on its own estimates, OPCS concludes that current staffing constitutes a 30-50% shortfall

compared to need. "Bank staff as a group cover less than 50% of corporate safeguard needs. Another

20% is provided by STCs, including many retirees. We need more staff dedicated to environmental

safeguards, and more staff professionally qualified in safeguards" (emphasis in original).27

For the World Bank, a group of 100 safeguard specialists is expected to ensure effective safeguard

management for 1685 Category A or B projects in the active portfolio (totaling $130 Billion).28

On

25 IAD (2014: 15). 26 Data for this graph is explained in Sanchez-Triana et al (2011: 16). 27 OPCS Safeguard Diagnostic, November, 2013 28 This total does not include development policy loans. See Tables 1 & 2 in Annex B for some comparative indicators of

safeguard capacity at different multilateral development banks.

14

average, each Bank specialist has safeguard responsibility for 3.1 new projects with high or moderate

social and environmental risks, and supervision responsibility for nearly 17 active high or moderate risk

projects.

a. Estimating Supply of Safeguard Risk in the World Bank Portfolio

Demand for safeguard expertise is primarily a function of the changing level of environmental and social

risk in the project portfolio as well as the Bank's appetite for tolerating risk with respect to compliance

with its policies and the environment and social integrity of its projects. The most reliable baseline

indication of Bank safeguard capacity would be the actual time allocation of current safeguard specialists.

For several reasons, timesheet data for how safeguard specialists allocate their time is either not reliable

or not available. The Bank timesheet coding system leaves room for considerable inaccuracy due to the

lack of punctuality in completing the form, shifting of cost codes by managers, and the unsupervised use

of contingency funds. It is common as well that some project preparation costs, including safeguards, are

charged to a prior project that is ending - resulting in challenges for the correct project assignment of staff

hours or costs.

In the absence of this information, a second way to estimate demand is to estimate active and projected

portfolio risk, separated into safeguard preparation and supervision activities. Cost coefficients can then

be used to translate the supply of portfolio risk into demand for safeguard support and compliance

oversight during project preparation and supervision. These cost coefficients may vary to reflect the

Bank's risk tolerance level, but for this paper I assume a low risk tolerance.

The World Bank approves about 40 Category A investment loans and about 270 Category B investment

loans each (10 year average) The average number of Category A and B projects approved between

FY10-FY14 is 309. Current FY14 data indicate that the World Bank has 284 Category A projects and an

additional 1,411 Category B projects in the active portfolio, for a total of $130 billion in high to moderate

risk projects. Adding a share of Category C, FI and Guarantee projects brings the total to 1940 high or

moderate risk projects in the active portfolio as of Sep. 1, 2014.29

Given the President's mandate for

IBRD to increase overall lending by $100 Billion over the coming decade and the Bank to take on greater

risk, we would expect the number of Category A and B projects to grow steadily from the current

baseline. Based on these assumptions, Table 2 provides a breakdown of recent and future World Bank

project approvals by risk Categorization.30

Similarly, the level of risk reflected in the change in Category A and B projects to be supervised in the

active portfolio of the Bank is projected for the next two years. Projected Supervision portfolio is

estimated by adding to the previous year (2013) the total number of approved projects for that year. To

adjust for projects reaching completion and exiting the Bank portfolio, I subtract 15% of the that year's

portfolio. For Category C projects, 50% of prior year portfolio is subtracted due to faster completion

rates. The projected increase in Category A & B projects offset somewhat by the overall decline in

overall lending after unprecedented spike in response to the 2008-2011 financial crisis.

b. Estimating Demand for Safeguard Work with Cost Coefficients

29 In addition to Category A and B projects, a modest amount of safeguard preparation is required for an estimated 50% of

Category C projects (accounting for projects in which safeguard policies are not triggered and additional funding projects) and

supervision resources are required for an estimated 25% of active Category C projects, as well as a small number of public

financial intermediary projects and guarantees. Including these additional safeguard related projects brings the active portfolio to

1917 for FY14. 30 Investment project distribution by environmental and social risk is drawn from data provided in the World Bank's project

database.

15

Safeguard staff cross-support for Category A projects can vary, from as little as 4-8 staff weeks per year

during typical preparation but reaching as high as 1-2 FTE working full time on a project the entire year.

I estimate an average of 43 safeguard staff weeks per year for the 5-10 highest risk Category A project

preparation and 18 staff weeks for the Safeguard preparation of all other Category A projects. I estimate

7 staff weeks for the preparation of higher risk Category B projects, and 3.5 weeks for all other Category

Bs. I estimate 2.4 weeks the preparation of the 15% of Category C projects that require more than initial

screening, and 5 weeks for both FI and Guarantee project preparation.31

Using these cost coefficients for

project preparation summarized in Table 3, an estimated demand for safeguard supervision is 56.2 FTE

Safeguard staff per year in FY2014, increasing by 2016 to 59.6 FTE. 32

Table 2. World Bank Safeguard FTE Demand for Operational Support and Oversight

Preparation 2010 2011 2012 2013 2014 2015 2016

Actual***** Projected

Cat. High A (25%) 9.6 10.5 8.25 7.5 10.25 11.25 12

Cat. A (75%) 38.4 31.5 24.75 22.5 30.75 33.75 36

Cat. High B (33%) 139 143 149.5 108.5 134.5 135 135

Cat. Low B (67%) 139 143 149.5 108.5 134.5 135 135

Cat. C 96 100.5 75.5 59.5 72 75 75

FI 16 11 9 11 7 10 10

Guarantee 3 1 5 3 8 5 5

Project Total 441 440.5 421.5 320.5 397 405 408

SG Preparation

FTE req.** 60.7 59.7 55.2 43.4 56.2 57.7 59.6

Supervision Actual Projected****

Cat. High A (25%) 73.5 71 71 71

Cat. A (75%) 220.5 213 212 214

Cat. High B (33%) 694.5 706 734 759

Cat. Low B (67%) 694.5 706 734 759

Cat. C* 181 150 147 148

FI 79 66 60 58

Guarantee 5 6 12 15

Project Total 1938 1917 1970 2025

SG Supervision 163.7 157.7 159.3 162.4

31 A conservative estimate of 3 staff weeks for the 200+ Category B projects considers the variation for safeguard demands

between "high" and "low" Bs. 32 Although my cost coefficients are higher than those proposed by OPCS, they are conservative for two reasons. I am not

including 20-25 projects per year on average that are brought to the Bank, involve some preparation or due diligence investment

but are then dropped. I am also not accounting for staff weeks needed to offset the accumulated deficit in safeguards activity

that was not properly staffed over that past five year period of above average lending. Finally, I estimate that 48 staff weeks is

equal to 1 FTE person year (MY), which is likely to be higher than the actual rate.

16

FTE req.***

SG Total

FTE req.***

207.2 213.8 217.0 221.9

* Assume only 25% of Category C projects require safeguard preparation or supervision support

** Safeguard Preparation FTE estimated using 10 SW /yr for Cat. A; 3 SW/yr for Cat. B, and 0.25 SW/yr for Cat. A,

and 5 SW /per year for FI and Guarantees. Staff Years (MY) are estimated by dividing SW by 48 weeks/year.

*** Safeguard Preparation FTE estimated using 10 SW /yr for Cat. A; 3 SW/yr for Cat. B, and 0.25 SW/yr for Cat.

A, and 5 SW /per year for FI and Guarantees. Staff Years (MY) are estimated by dividing SW by 48 weeks/year.

**** Projected Supervision portfolio is estimated by adding to the total number of projects in the active portfolio for

the previous year the total number of approved projects for that year, then subtracting 15% of the prior year's

portfolio. For Category C projects, 50% of prior year portfolio is subtracted due to faster completion rates.

***** Actual portfolio and new projects do not include Development Policy Operations or other projects

uncategorized for risk.

Similarly for safeguard supervision, my estimates of safeguard staff demand are based on the required

supervision for the active portfolio, as opposed to the actual inadequate level of supervision that is now

done. For the 1,875 active projects, a supervision report is produced semi-annually and site visits are

conducted on a periodic basis.33

However, the additional attention that is required to trouble-shoot

problems, consider course corrections, staff more frequent site visits, and analysis for the higher risk and

problem projects implies considerable additional time commitment. For supervision, an estimate of 25

staff weeks of supervision is required for the small share of highest risk Category A project, compared to

9 weeks for other Category As. For the high risk Category B projects, 2 weeks is required, while 1

weeks is required for low risk Cat. B and C. I estimate that 5 weeks for FI and Guarantee projects.

Combined, these coefficients produce a demand for 157.7 FTE staff of safeguard supervision support for

FY2014 with a projected demand of 162.4 FTE by FY16.

Table 3. Cost Coefficients for Low Corporate Risk Tolerance for Safeguard Cross-Support

(average over all projects, includes RSA and OPSOR time)

Category Preparation Supervision

High A 43 weeks (1 FTE) 25 weeks

A 18 weeks 9 weeks

High B 7 weeks 2 weeks

Moderate B 3.5 week 1 week

C 2.5 weeks 1 week

FI 5 weeks 5 weeks

G 5 weeks 5 weeks

Combined, the current and projected social and environmental risk in the World Bank investment lending

portfolio suggests a demand for approximately 214 - 222 FTE for safeguard support.

This estimate is double the existing Bank capacity.34

Even before accounting for other duties assigned

to WB Safeguard staff and the risk management activities associated with 25-35% of non-

investment lending, the severe existing under-capacity is evident.

33 The frequency or intensity of project site visits is difficult to estimate precisely, so I assume 2 visits per year for 2 day mission

on average. 34 The equivalent estimate here of approximately 9,000 staff weeks is three times higher than the 3,150 staff weeks that were

estimated in 2010 to be devoted to environmental safeguard activities.

17

However, operational support duties are only part of Safeguard staff responsibilities. Because of the

overwhelming focus for Bank Safeguard specialists to keep up with the demand for project safeguard

services, safeguard staff have not been able to properly attend to other mandates. An estimated 35-40

additional full-time safeguard staff plus an equivalent support capacity of 60 MY of short-term

consultants would be required to assume responsibilities for additional tasks, including:

policy development and interpretation,

support for corporate initiatives

assess and manage portfolio risk

identifying and helping the Bank respond to emerging issues,

upstream environmental and social risk management in the context of regional and country

programming,

training and accreditation of safeguard staff and consultants;

developing, sharing and disseminating knowledge products;

undertaking the full range of social impact assessment options;

analyzing institutional capacity, strengthening the capacity of borrower risk management and

using country systems;

analyzing the proper inclusion of economic cost-benefit assessments of project's environmental

impact; and

improving the reporting of project safeguard and sustainability outcomes.

In practice, the undersupply of qualified, dedicated safeguard staff, exacerbated by perverse budgeting

incentives, leads to performance breakdowns in implementation. OPCS argues, "Because of the shortage,

most safeguard resources are allocated to project preparation, to get projects on our books, and less on

supervision to improve results."35

IAD adds that the Bank lacks an updated, accurate understanding of the

spread of safeguard risk across its portfolio and can not report the total amount or allocation of resources

spent on safeguard implementation. Over half of active projects, including some high risk projects do not

have assigned safeguard specialists.36

In other words, under the current safeguard system, human and

budget resources for proper safeguard supervision are often not available.

Problems caused by the undersupply of environmental safeguards specialists are compounded by

deficiencies in the mix of skills possessed by safeguards specialists. The Bank will need to factor in the

many areas of expanded safeguard coverage under consideration but not reflected in the current range of

skills available among safeguard staff. Some of the emerging issue areas identified in the safeguard

review would imply acquiring additional staff capacity in a number of areas of social risk (community

health and safety, disability, labor, gender and sexual orientation, child and human rights) as well as

environmental risk (climate, SESA, cumulative impact, biodiversity, ecological flows) and knowledge of

borrower risk management systems.37

A recent internal report highlighted other factors complicating the undersupply of safeguard expertise:

"Safeguard specialists often operate in areas outside the specialties they possess. Often,

one safeguards specialist is expected to provide operational support on projects in a

variety of sectors, ranging from hydropower to roads. Supervising preparation of

35 OPCS (2013) Diagnostic, pg. 1. 36 IAD (2014: 30). 37 In the 2009 revision of ADB Safeguard Policy Statement, an explicit commitment to increase staff resources over a three year

period was spelled out. "The estimates suggest that incremental staff resources ranging from 1253-1749 person-weeks per year

will be required for safeguard review work in the immediate to medium term (2010–2012)." See ADB SPS, 2010, pg. 27-29).

18

environmental documentation for even a single project type, such as a dam for

hydroelectric power, requires a number of technical specialties, such as environmental

flows, limnology, ionic equilibrium at low temperatures, land and aquatic biodiversity,

dam safety, occupational health and safety, geomorphology and sediment transport, and

watershed management. A single safeguards specialist, no matter how well trained,

cannot provide all the necessary support for twenty or thirty projects in different sectors,

much less in all of the subject areas required by the Bank‘s safeguards policies” 38

Not ensuring adequate safeguard staff capacity also constrains efforts to recruit and retain a senior

safeguard team, while continuing to train younger staff. Similarly, without a clear or updated baseline for

how environmental and social risk is spread across the Bank's active and projected portfolio, planning for

a risk based approach to safeguarding projects is difficult. An efficient risk based allocation of safeguard

resources requires precise, regularly updated assessment of portfolio risk to properly align with available

supply of expertise.

Greater reliance on short-term or long-term consultants can only be a temporary solution to the safeguard

capacity problem. Several factors limit the use of consultants:

The prospects of finding qualified consultants available for a temporary period of time are limited

given the nature of specialized expertise required. High demand for the expertise sought often

exceeds supply.

The limited duration of consecutive days that consultants are allowed to work means that after the

maximum is reached the Bank must find new people with the necessary skills and experience.

There will be a high investment cost on Bank safeguard staff in terms of orientation and

supervision.

The transaction costs associated with finding consultants, and processing and managing the

contracts will be significant.

If demand for operational support already exceeds the total Bank Safeguard capacity even before

accounting for other responsibilities that could consume a substantial share of staff resources, the result is

that an alarming part of the Bank's existing portfolio is not receiving adequate or any safeguard support.

Clearly, the Bank reorganization must correct the current undersupply of safeguard staff to ensure

adequate risk management.

The lack of adequate safeguard capacity at the Bank leads indirectly to other inefficiencies and ineffective

uses of existing resources.

IEG argues that “the artificial separation of environmental and social staff between those who work on

safeguards and those who work on social or environmental sustainability is a cause for concern….

forcing an unnecessary division of labor among the social and environmental staff. The increasing

divide between most of the Bank staff who work on safeguards and those who work on environmental and

social sustainability has diminished the Bank’s ability to deliver on its sustainability agenda. To expand

further its focus on issues such as biodiversity, climate change, and benefit-sharing to enhance social

impacts on the poor,” IEG recommends that the Bank move beyond the “do-no-harm” approach—to

encourage greater attention to how safeguards are doing good, in terms of enhancing environmental and

social results. 39

38 Sanchez-Triana, Ernesto, Leonard Ortolano. Giovanni Ruta, Ghazal Dezfuli, Rahul Kanakia, (March 2011) “Implementation of

Environmental Policies,” World Bank 2010 Environment Strategy Background paper (unpublished manuscript); 39 IEG (2011: 22)

19

2. Independent Control of Adequate Safeguard Budget by Safeguard Line Management

Recommendation 2. The World Bank should allocate to the appropriate Safeguard Director or

Manager level independent control over adequate, off-the-top resources approved on an annual

basis to ensure effective implementation of the safeguard policies. Based on World Bank and other

MDB safeguard systems, a minimum safeguard annual budget should be between $60 - $80 million,

depending on several factors.

The prevailing “internal labor market” approach to supplying safeguard specialists for Bank projects is

not working, particularly for project supervision. IEG reported that more than a third of World Bank

projects had inadequate environmental and social supervision, manifested mainly in unrealistic safeguards

rating and poor or absent monitoring and evaluation.40

This failure to supervise many Bank projects is

attributed by IEG to lack of off-the-top budget control by safeguard managers. “The budget for

safeguards supervision in the World Bank is controlled by the task team leaders for each project, who

determine the intensity of supervision and choose the team members or consultants for safeguards

supervision. The concern for technical capacity of the task team leader to make this judgment, or the

conflict of interest, is not deemed relevant during the supervision phase.” “The reliance on an internal

market for safeguards supervision," according to IEG, "has resulted in considerable inefficiencies in

resource allocation for safeguards oversight at the World Bank, compared to IFC.” 41

The Environmental Department background study underscores the same concerns:

Putting safeguard budget control in the hands of country directors, forces environmental

(and social) specialists to sell their services in an internal competitive market that naturally

removes incentives for task managers to hire specialists who, in the minds of some TTLs,

call for lengthy and expensive environmental assessments.” 42

“Staff members interviewed consistently said that safeguards experts were generally

selected on the basis of availability. When asked to clarify this point, interviewees

explained that due to the perpetual shortage of environmental specialists, they drew on

specialists in environmental units primarily for high-risk projects. If no environmental

specialists were available, they would draw supplemental staff from a roster of consultants

who would be mentored or backed up by a Bank staff member while performing safeguards

tasks. Interviewees noted the absence of a structured approach for selecting relevant

safeguard specialists (either Bank staff or consultants) when shortages existed in a region.

As one interviewee put it, staff selection was done on an ad hoc basis.”

These organizational tensions are further compounded by existing budgetary arrangements

that lead to low levels of staffing during project supervision. Funding for safeguard-

related activities is drawn primarily from resources earmarked to ensure safeguards

compliance during project preparation but not during supervision. Budgets for supervision

are not sufficient to adequately meet safeguards support needs, which in turn inhibits the

ability of the Bank to effectively target resources toward projects with relatively high

environmental and social risk.43

The Bank‘s projects’ budget does not include adequate

40 IEG 2010, xii. 41 IEG (2011: 21) 42 Weaver, C. and R. Leiteritz. 2005. “Our Poverty Is a World Full of Dreams: Reforming the World Bank.” Global Governance

(July, 2005). 43 Whitford, P. and K. Mathur. 2008. The Effectiveness of World Bank Support for Community-Based and -Driven Development.

Safeguard Policy Review. IEG Background Paper. Washington DC: IEG.

20

funding for regular supervision of category B projects by environmental safeguards

specialists.44

TTLs may opt not to spend budgetary allowances on safeguards issues and, in

fact, they have incentives to cut costs during supervision because of budget constraints.

As if the proliferation of evidence was not enough, IAD was commissioned to look yet again at the

funding of safeguard activities as part of a 2014 audit. The results, while not surprising or divergent from

long held concerns, also serve to underscore the foot-dragging by management to finally address this

structural impediment to effective safeguard implementation. IAD findings are incomplete due to the

lack of systematized safeguard expenditure data. With the exception of RSA budgets and the LCR

region, no safeguard expenditure data was available for safeguard fixed or variable expenses. On

safeguard budgets, IAD finds:

"In most regions, the project specific safeguard budget is included in the project supervision budget held

by the TTL. ENV and SD specialists claim that they are not always funded adequately for safeguard risk

management due to the prioritizations made by the TTLs. In 5 of the 6 regions, there is no safeguards

budget allocation to ENV and SD sectors, although these sectors allocate ENV and SD specialists to

projects to undertake safeguard work." 45

IAD juxtaposes the reality of this chronic absence of safeguard supervision with the fact that "the TTL has

budget authority for safeguard supervision, [and that] 34% of survey participants responded that the TTL

decides on the level of safeguards support for his/her project."46

For a Bank poised to introduce sweeping safeguard reforms the success of which is premised on a more

accountable provision of implementation support, fixing the existing budgetary roadblocks to effective

safeguard supervision can be seen as nothing less than a litmus test for delivering on this promise.

There are expectations among some in the Bank that the reorganization focus on pivoting the Bank to be

more efficient, agile and reliant on use of borrower systems may actually result in a significant

transformation of the project portfolio and a lowered demand for safeguard resources. Such a scenario

could involve a cost savings in safeguard staffing expenses. In fact, the new strategic budgeting process

places strategic factors above other budget determinants such as portfolio risk. Just as ex ante safeguard

requirements are under pressure to be streamlined and eliminated, ex ante budget estimates may be less

appropriate in the new budget model than, say, an emergency fund to permit rapid response to emergent

safeguard needs during a period of transitional uncertainty.

Without predicting what the long-term changes may be for the Bank's portfolio - in part because they rest

on a number of highly debatable assumptions, the current portfolio will not change much in the short-

term. OPCS reports that the World Bank has a "young portfolio," with an average project having been in

the active portfolio about 3.6 of a typical 6.6 year project disbursement cycle.47

Any change in portfolio

risk or risk management resource allocation will be gradual at best. Unless the new approach is simply to

concede that a significant amount of risk will not be managed going forward (which appears to be the

default approach now), then the Bank would be required to take proactive steps to reduce the backlog of

mismanaged safeguard risk that has accumulated in the active and foreseeable portfolio.

44 World Bank LCR. 2006. Lessons from the Field. A Thematic Review of Safeguard Policy Implementation in Rural and Urban

Water Supply and Sanitation, Community Driven Development, Biodiversity Conservation, Land Administration, Roads, and

Health Sector Projects in Latin America and the Caribbean. Unpublished Report. Washington, DC: World Bank. 45 IAD (2014: 37) 46 Op cit, pg. 38 47 OPCS, "Review of the World Bank FY13 Portfolio and Update on Actions to Assure Quality," April 15, 2014., pgs. 11-12. The

average lag in years for investment projects between approval to exit is 6.6 years.

21

Relevant safeguard unit managers or directors must have independent control over budget for staff salary

and travel expenses, in addition to resources for appropriate training, corporate support, and knowledge