Ghana Data Launch

Hosted by

MFTransparency

December 21st , 2011

Promoting Transparent Pricing in the Microfinance Industry

enabling APR & EIR Program

enabling Africa to Price Responsibly and Educate on Interest Rates

Sponsored by the MasterCard Foundation

Eight countries in 20 months: Malawi, Uganda,

Rwanda, Ghana, South Africa*, Tanzania, Zambia, Mozambique

*Data collection efforts in SA were suspended and other activities are being implemented

Ghana is the fourth country in the enabling APR & EIR Program

Transparency workshops in Accra on February 25th and Tamale on February 28th, 2011 to launch the Ghana Initiative.

This initiative includes the collection and publication of pricing data *

*Due to the severe delays in collecting data in Ghana, the training components are suspended until further

notice. We are exploring options to make sure the training is offered by other organization but nothing has been finalized

Transparent Pricing Initiative in Ghana

Transparent Pricing Initiative in Ghana

The enabling APR & EIR Program is sponsored by:

Thank you to our local partner in Ghana:

Participating Institutions

Transparent Pricing Initiative in Ghana Participating MFIs

Calvary Enterprise Development Foundation

CashPhase Ghana Limited

Cedi Finance Foundation

Christian Rural Aid Network (CRAN) Community Aid for Sustainable Development(CASUD)

Daasgift Quality Foundation

East Mamprusi Community Bank

E-LIFE Development Agency (ELDA)

EMPRETEC Ghana Foundation

Grameen Ghana

Participating MFIs

African Gate Financial Support

Ahantaman Rural Bank Limited

AIDEZ Small Project International (ASPI)

ASA Initiative

ASA-Ghana Association of Progressive Entrepreneurs in Development (APED)

Atwima Kwanwoma Rural Bank

Baobab Financial Services Limited

BestFUND

Bonzali Rural Bank

Transparent Pricing Initiative in Ghana Participating MFIs

Nwabiagya Rural Bank Limited Opportunity International Savings & Loans Ltd.

ProCredit Savings & Loans Company Ltd.

Rich Step Investment

Sekam Trust International

Simli Pong

Sinapi Aba Trust

Tamale Community Credit Union

The Bridge Financial Services Limited

Union Rural Bank Limited

Participating MFIs

Initiative Development-Ghana

Innovative Finance

Kraban Support Foundation

Kumanwuman Rural Bank Limited

Lower Pra Rural Bank Limited

Maata-N-Tudu Association

Mail Finance

Markaz Al Bishara Markaz Community Cooperative Credit Union

MicrofinPlus Ghana

Type of Institution (40 Institutions)

7.50%

25.00%

7.50%

52.50%

7.50%

Type of Institution

Coop

Privately-owned for-profit

Publicly-trade for-profit

NGO

Other

Regulated vs. Unregulated

• Twenty three of the forty participating institutions are regulated

57.50%

42.50%

Regulated vs Unregulated

Regulated

Unregulated

Product Pricing Analysis

Loan Purpose (114 products)

17%

6% 6%

13%

51%

7%

0%

10%

20%

30%

40%

50%

60%

Housing Emergency Consumer Education Business AnyPurpose

Pe

rce

nta

ge o

f P

urp

ose

s

Purpose as a Percentage of Purposes

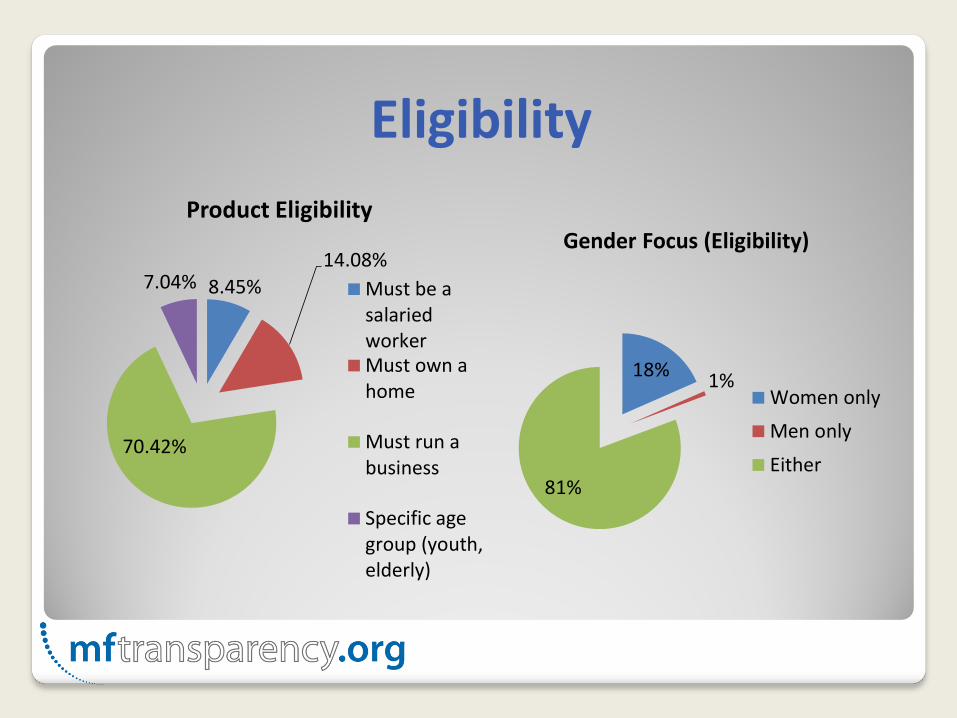

Eligibility

18% 1%

81%

Gender Focus (Eligibility)

Women only

Men only

Either

8.45%

14.08%

70.42%

7.04%

Product Eligibility

Must be asalariedworkerMust own ahome

Must run abusiness

Specific agegroup (youth,elderly)

Lending Methodology

44.59%

44.59%

10.81%

Lending Methdology

Individual

Solidarity

Village Banking

Other Services Offered

22.51%

24.08%

23.04%

10.99%

11.52%

7.85%

0% 5% 10% 15% 20% 25% 30%

Credit Education

Credit Insurance

Group Meetings

Business Training

TA Visits to Workplace

Other Training

Percentage of services offered

Other Services Offered with Loan Product

Repayment Frequency

2%

44%

3%

18%

25%

7%

1% 0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Daily Monthly Quarterly Every 2weeks

Weekly Single endpayment

Irregularpayments

Percentage of frequencies

Repayment Frequency

Reasons for Variations in Price

46 products have a range of interest rates

4.35%

13.04%

10.87%

30.43% 13.04%

8.70%

19.57%

Interest Difference Reasons

Branch office location

Client profile/Client risk

Length of time as client

Loan size

Purpose of loan

Collateral

Other

Interest Calculation Method

15.79%

84.21%

Interest Rate Calculation Method

Declining Balance

Flat

Fees & Insurance

103 products (90%) have a fee

16% of all fees are for the purpose of insurance

90%

10%

Products with a Fee

Fee

No Fee 84%

16%

Fee & Insurance

OtherType ofFees

Insurance

Fees & Insurance

93%

7%

Does the product have a fee or insurance charge?

Disbursement

Ongoing

20.87%

79.13%

Fees/Insurance Disclosed on Repayment Schedule

Disclosed

Notdisclosed

Compulsory Savings 73 products out of 114 require compulsory savings

Of the 73 products that require savings, 10 disclosed the amount of compulsory savings on the repayment schedule

For 9 products, borrowers control savings internally

60%

4%

36%

Compulsory Savings

Required forall loans

Required forsome loans

Neverrequired

5.48%

49.32% 24.66%

10.96%

9.59%

Compulsory Savings by Type of Institution

Coop

NGO

Privately-ownedfor profitOther

Publicly-tradedfor profit

Pricing Calculations

Interest Rate Calculations

Interest Fees Insurance Taxes Security

Deposit

APR (Interest + Fees + Insurance) X X X

APR (Including Taxes & Security

Deposit) X X X X X

EIR (Interest + Fees + Insurance) X X X

EIR (Including Taxes & Security

Deposit) X X X X X

APR Ranges by Institution Type APR (Int + Fees + Ins)

224.08%

82.13% 79.72% 67.46%

85.54%

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

300.00%

Co-op NGO Privately-ownedFor-Profit

Publically-tradedfor-Profit

Other

APR by Institution Type (Weighted Average, Minimum and Maximum)

APR Ranges by Product Purpose APR (Int + Fees + Ins)

Business Housing Emergency Consumer EducationAny

Purpose

Minimum APR 0.0% 33.1% 43.0% 33.1% 29.2% 33.1%

Maximum APR 268.2% 207.8% 164.5% 207.8% 207.8% 276.5%

Weighted Average APR 88.7% 74.2% 66.8% 72.5% 92.0% 71.8%

0.0%

50.0%

100.0%

150.0%

200.0%

250.0%

300.0%

AP

R (

Int

+ Fe

es +

Insu

ran

ce)

APR by Product Purpose

APR Ranges by Geographic Focus APR (Int + Fees + Ins)

Rural Urban Both

Minimum 18.6% 0.0% 50.1%

Maximum 174.1% 276.5% 207.8%

Weighted Average APR 86.1% 103.3% 71.7%

86.1% 103.3%

71.7%

0.0%

50.0%

100.0%

150.0%

200.0%

250.0%

300.0%

AP

R (

Int

+ F

ees

+ In

sura

nce

)

APR by Geographic Focus

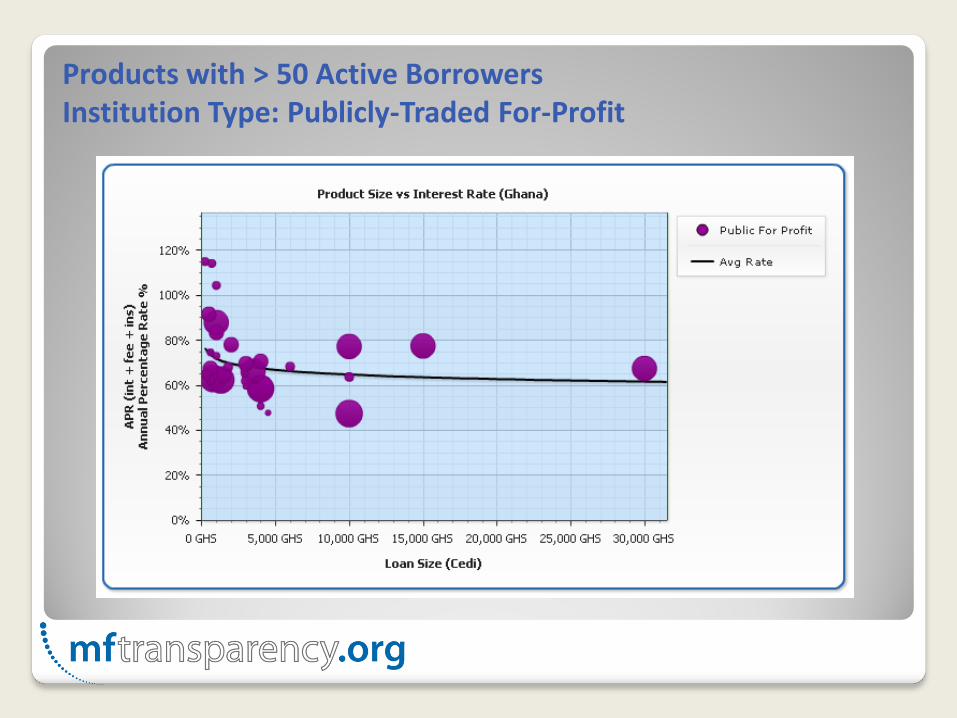

MFTransparency Interactive Price Graphs

Price Graphs APR (Int + Fees + Insurance)

Products with > 50 Active Borrowers

Products with > 50 Active Borrowers Loan Amount < 2,500 GHS

Products with > 50 Active Borrowers Institution Type: Cooperatives

Products with > 50 Active Borrowers Institution Type: NGO

Products with > 50 Active Borrowers Institution Type: Privately-owned for-profit

Products with > 50 Active Borrowers Institution Type: Publicly-Traded For-Profit

Products with > 50 Active Borrowers Institution Type: Other

Products with > 50 Active Borrowers Purpose: Business

Products with > 50 Active Borrowers Purpose: Education

Products with > 50 Active Borrowers Purpose: Consumption

Products with > 50 Active Borrowers Purpose: Housing

Products with > 50 Active Borrowers Purpose: Emergency

Products with > 50 Active Borrowers Purpose: Any purpose

Products with > 50 Active Borrowers Interest Calculation Method: Flat

Products with > 50 Active Borrowers Interest Calculation Method: Declining Balance

Summary Institution cost structure: Every institution has a unique cost

structure which requires a unique pricing strategy.

Product cost structure: Different loan products can have significantly different cost structures. It is therefore necessary to look at each loan product individually when assigning loan prices.

Limitations of portfolio yield: If we do not analyze costs and prices on a product-by-product basis, our overall portfolio yield may be positive, but some individual products not profitable. This can cause sustainability problems in the future.

Remember: Each product is unique and requires a distinct pricing strategy.

Recommendations

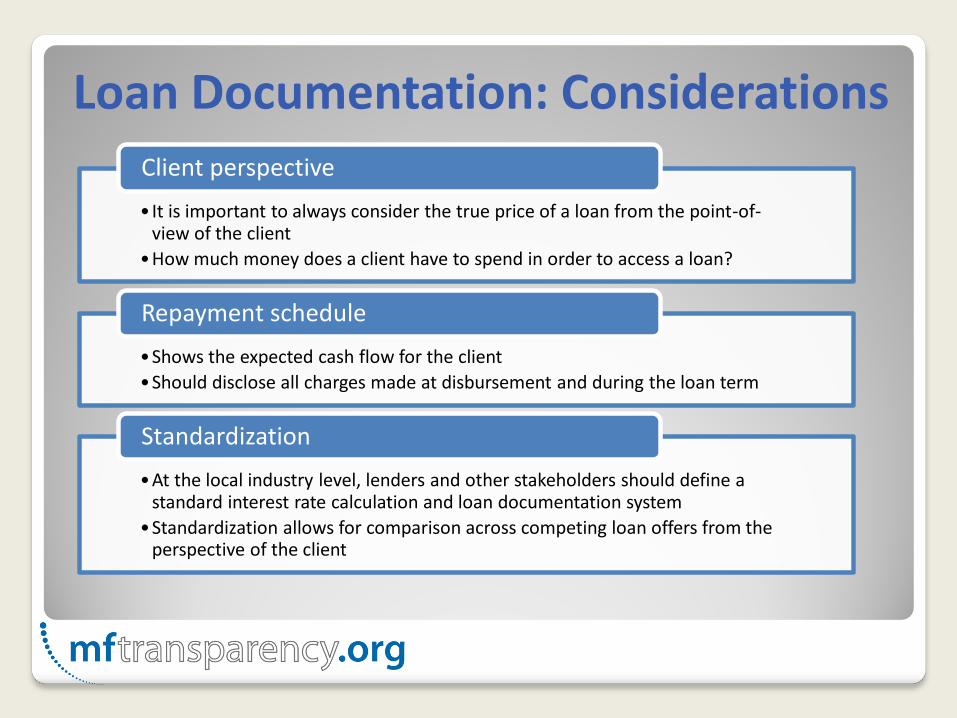

Loan Documentation: Considerations

• It is important to always consider the true price of a loan from the point-of-view of the client

•How much money does a client have to spend in order to access a loan?

Client perspective

•Shows the expected cash flow for the client

•Should disclose all charges made at disbursement and during the loan term

Repayment schedule

•At the local industry level, lenders and other stakeholders should define a standard interest rate calculation and loan documentation system

•Standardization allows for comparison across competing loan offers from the perspective of the client

Standardization

Resources: Recommended Repayment Schedule Template

Example from the ground..

•A scenario where an MFI had quoted a flat interest rate of x% on all loans

• In practice , as seen on the actual repayment schedule for some loans, the MFI was charging the client only half of what was quoted in the loan contract

•50% loss in revenue for the MFI

• Impacts future sustainability of the MFI

•Differential treatment of clients : some are charged lower than others for the same product

Miscalculation of interest rates

• Investment in sound Management Information Systems (MIS)

• Investment in staff training to ensure that the correct amounts are reflected on repayment schedules

Recommendations

General Recommendations Loan documentation

• Communicate as much information on both repayment schedule and contract

Interest rate calculation method

• Switch from flat to declining balance to enhance transparency

Client Protection Principles

• Implement principles of the Smart Campaign to improve transparency and strengthen social mission

MFTransparency is currently piloting

a in and

The educational resources we will develop for Malawi and Rwanda will also be adapted to the unique context of other countries

We collaborate with our local partners to adapt these materials to the local context and implement them successfully.

Ways to Get Involved Endorse MFTransparency. More than 870 individuals and

organizations have signified their support in principle of MFTransparency's mission by becoming an endorser. Add your name to the list: http://www.mftransparency.org/endorsements/form/

Educate about transparent pricing. MFTransparency develops and disseminates educational resources covering a range of topics related to transparent pricing. These materials are all available free of charge through the Resources Library on our website.

Participate in country projects. We work with government agencies, networks, associations, donors, investors, academics and other stakeholders in every project country and always welcome new partnerships. MFIs can also actively participate by submitting their data when MFTransparency launches the Transparent Pricing Initiative in their country.

Promoting Transparent Pricing in the Microfinance Industry