PPP’s: Theory & Practice PPP’s: Theory & Practice

SANPSHOTS: Manila Water Company, Inc. (MWC)

Mainstreaming Mainstreaming Public-Private Public-Private

PartnershipsPartnerships

Anouj Mehta, Senior Infrastructure Finance Specialist (PPPs), Asian Development Bank

Bhopal, 26Bhopal, 26thth February 2009 February 2009

Backdrop: ManilaBackdrop: Manila Metro Manila:

Capital of the Philippines and made up of 17 municipalities

Population of over 14 million Intensely congested in parts – second most populous

in S.E. Asia

Backdrop: Water OperationsBackdrop: Water Operations

Prior to 1997, responsibility for water and sewrage services rested with:

Metropolitan Water and Sewerage Services (MWSS), a Government Corporation

Poor service performance parameters: Years of under-investment by MWSS MWSS was hugely indebted Grossly inefficient services Huge Non-Revenue Water as % of production Severe problem of illegal connections Low water pressure

• Coverage: Only 58% population• 63% Non Revenue Water

• 24*7 Water Coverage: 26% only• Poor Heavily Affected: poor piped coverage

Paying upto 13% of incomes, some Rs 1000 per mth

Government Response to Water Crisis :Government Response to Water Crisis :

Set out clear objectives: Improvement in quality and efficiency of

service. Expansion of service. Reduction in water tariff. End expensive government subsidies.

Promulgation of “National Water Crisis Act” 1995

National Water Crisis Act (1995)National Water Crisis Act (1995)

Granting of authority to the President to privatise water utilities, including MWSS CRUCIAL: Expression of political will and commitment

Create public awareness about benefits of “privatization” (reduction in water tariff!).

Criminalization of water theft. Re-organisation of MWSS

Split Manila service area into two zones (East and West zones)

Introduction of PSP and competition and Takeover policy between zones

Performance Benchmarking encouraged

Not “Privatisation” But PPP ApproachNot “Privatisation” But PPP Approach It was not privatisation

The government retained ownership of the assets of the MWSS,

but followed a “lease” model to the private companies to improve and operate assets for a fixed period,

and then to be returned to government Bid process

Aimed to bid out off the rights to operate and expand the water and sewage network system,

With a set of performance targets to achieve, And with the preferred bidder being the one offering the

lowest price of water, for the set performance targets. Private companies responsibilities were

Raising finance, debt servicing, improving the network and tariff billing and collection

Re-organisation MWSSRe-organisation MWSS

MWSSZone West(60% population)

Maynilad Water Services Inc

(MWSI)

Zone East(40% population)

Manila WaterCompany Inc

(MWCI)METRO MANILA

The East Zone Concession FrameworkThe East Zone Concession Framework

To rehabilitate, expand, & operate the east zone of Metro Manila’s water utility for 25 years,

Targets increase coverage of water and sanitation services for 5 million

people, Improve continuous water availability, Meet quality standards and service quality, Reduce NRW

User tariff set by competitive bidding - the lowest price of water Manila Water offered to charge just over one quarter (26.39%)

of the existing rates Tariff adjustments provisions. Regulation by contract (no legislative regulation) Subject to demand risks

Some Striking Features Some Striking Features

Staggered works: Major capital expenditures commenced after 5 years; Initial focus on softer and cheaper measures to

improve services such as replacement of meters and reducing water theft.

Increase in existing water tariff (August 1996) by 38%. Reportedly;

Overdue Would have been implemented regardless of

privatization

Establishment of a Regulatory Office to Monitor and enforce concessions Implement rate adjustments Deal with customer complaints

Ayala Group (33.5%) United Utilities

(11.7%) Mitsubishi Corporation

(7.8%) IFC (7.3%) Employees (2.7%) Public (37%)

The East Zone Concession Framework: Won By The East Zone Concession Framework: Won By Manila Water CompanyManila Water Company

Embarked on heavy Capex Program

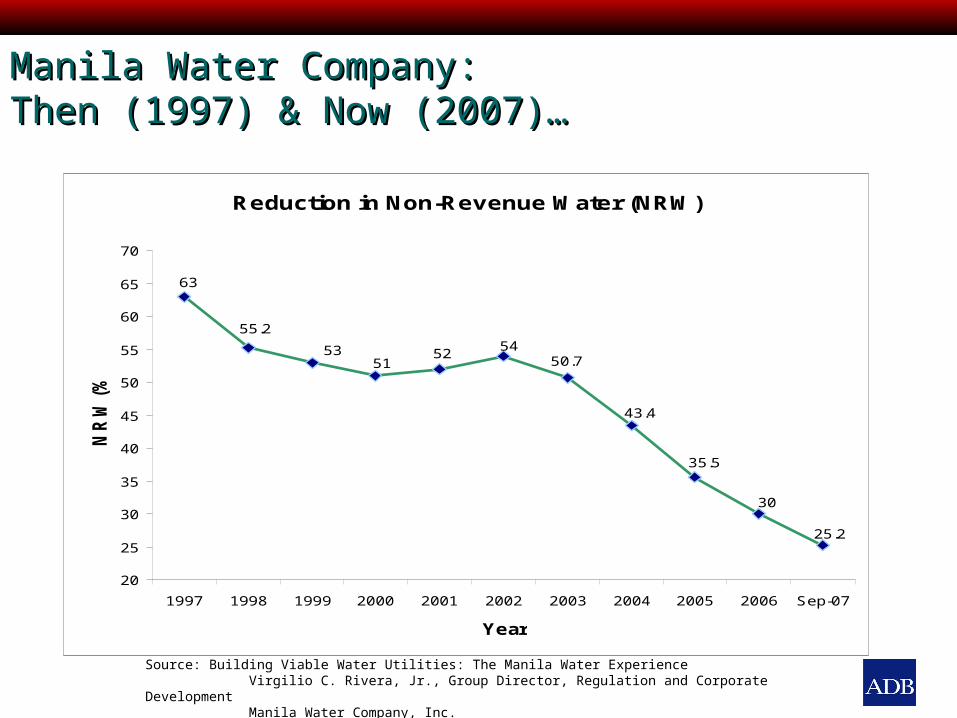

Manila Water Company: Manila Water Company: Then (1997) & Now (2007)…Then (1997) & Now (2007)…

Reduction in Non-Revenue Water (NRW)

25.2

30

35.5

43.4

50.754

5251

55.2

53

63

20

25

30

35

40

45

50

55

60

65

70

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 Sep-07

Year

NR

W(%

)

Source: Building Viable Water Utilities: The Manila Water Experience Virgilio C. Rivera, Jr., Group Director, Regulation and Corporate Development Manila Water Company, Inc.

3.1 million(58% of population)

5.6 million(99% of population)

Customer Base

19972007Water CoverageWater Coverage

Availability of WaterAvailability of Water

16 24Hours per Day

Manila Water Company: Manila Water Company: Then (1997) & Now (2007)…Then (1997) & Now (2007)…

Providing 24 by 7 Water SupplyProviding 24 by 7 Water Supply

Manila Water Company: Manila Water Company: Then (1997) & Now (2007)…Then (1997) & Now (2007)…

Doubled billed water from 440 MLD to 1000 MLDDoubled billed water from 440 MLD to 1000 MLD

Manila Water Tariff Rates

20.4819.7218.55

14.0213.88

9.37

4.02 4.37 4.55 4.77

0

5

10

15

20

25

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Year

Pes

o p

er c

u. m

eter

Source: Building Viable Water Utilities: The Manila Water Experience Virgilio C. Rivera, Jr., Group Director, Regulation and Corporate Development Manila Water Company, Inc.

Manila Water Company: Manila Water Company: Then (1997) & Now (2007)…Then (1997) & Now (2007)…

Costs of production might initially increase - modernisation and upgradation, risk capital with initial turn around phase; generally later should drop with productivity enhancements etc

Tariffs reflective of costs will likely increase for a period

Sustained tariff levels Pricing can incorporate

affordable levels for consumers (5% income)

Can incorporate poor focused schemes to allow affordability

Coverage of service, quality and sustained accessibility will benefit over time

Less pressure on government budgets freeing up space for other programmes

Tariff Comparison - Manila Water

0

5

10

15

20

Pes

o pe

r cu.

m

MWSS Projected Rate Manila Water Rate

Monthly water bill much less than 5% income of a low income household Monthly water bill much less than 5% income of a low income household (IFC) – affordable (1% of low income household’s income and 1.4% of (IFC) – affordable (1% of low income household’s income and 1.4% of

middle income houshold incomes)middle income houshold incomes)

MWC: Affordable?

Private Vended WaterPrivate Vended Water Was getting about 6 cu. m per month

from trucks

PricePrice1000 pesos per month

Specific Program for the Poor: WATER FOR THE POOR Programme:•Supplying 1.5 m legal connections to slums and cluster areas •Using the community including one metre for a cluster and sub meters which are Monitored by the community and bills collected by the community also and thenGiven to MWC•Prior to TPSB, poor were paying P1000 per cu.m. – almost 11-13% of incomes•Post TPSB, around P10 per cu.m.; less than 5% of the monthly incomes

Real cost of water under the pre PPP scenario - poor mostly using private low quality trucked Real cost of water under the pre PPP scenario - poor mostly using private low quality trucked water supplieswater supplies

MWC Piped WaterMWC Piped Water Now getting around 30 cu. M per

month from pipes

PricePrice300 Pesos per month

Average Household in East Zone:

MWC: Helping The Poor?

Tariff Adjustment ProvisionsTariff Adjustment Provisions Inflation. The regulator allowed for increases

according to annual rates of inflation. Unforeseen events. Companies could change

prices once a year due to drastic or other unpredictable events, such as the rapid devaluation of the peso.

Rate re-basing. At the start of each five year period, a review of tariffs could be made so they can be adjusted to reflect “fair returns” for the company agreed in the contract. (cost recovery based tariff)

Thank you.