Download - Pharma, Biotech & Medtech 2020 in Review

Pharma, Biotech & Medtech 2020 in ReviewEvaluate Vantage staff report – February 2021

Evaluate Vantage Pharma, Biotech and Medtech 2020 in review Copyright © 2021 Evaluate Ltd. All rights reserved.

Evaluate Vantage Pharma, Biotech and Medtech 2020 in review

The pandemic ensured that 2020 was unlike any other year for biopharma and medtech companies. But, while these

sectors turned their collective attentions to vanquishing the novel coronavirus, the usual business of drug and device

development continued alongside.

This report is a round-up of Evaluate Vantage’s analyses of 2020 – from M&A, venture financing and IPO markets,

to the progress of the Covid-19 pipeline, all based on Evaluate data.

In many ways Covid-19 turbocharged an industry that was already riding fairly high. The financing climate had been

strong for a few years, but 2020 saw records broken in the venture and IPO worlds. With the spotlight on biopharma,

which made remarkably swift progress on a pipeline of pandemic therapies, investors rushed to inject money into

the sector.

This also resulted in ballooning stock market valuations, with many companies ending the year worth substantially

more than at the beginning. Those developing Covid-19 vaccines and treatments drove those gains, with several

small developers transformed into multi-billion-dollar enterprises. The vaccine developers Moderna, Biontech and

Novavax especially stand out.

Similar dynamics were seen in the medtech arena, with diagnostics companies benefiting in particular – both those

developing tests for Covid-19 and those working on liquid biopsy cancer tests. Such work appealed hugely to

investors in publicly traded companies and to venture backers alike.

M&A also held up remarkably well across the board, considering that for much of the year global travel was not

possible. But the world quickly adapted to virtual meetings, and a number of big transactions emerged, culminating

in Astrazeneca’s $39bn move on Alexion in December. The pandemic also provided the impetus for the biggest

deal in medtech last year – the $18.5bn merger of the telehealth groups Teladoc and Livongo.

Heady valuations have not noticeably curtailed deal-making, although this remains a concern heading into 2021.

When preclinical companies can easily achieve the sort of market cap more typically associated with later-stage

developers, some big and expensive disappointments seem inevitable.

When it comes to medtech M&A, however, 2021 has kicked off in spectacular fashion with deals worth more than

$10bn already arranged. Liquid biopsy and remote patient monitoring have already emerged as major trends to

watch in the coming year.

The main Covid-19 focus this year is set to switch from tests for the disease to the progress of vaccines and

therapeutics against the pandemic. And this is a fast-changing environment: in the days after this report was put

together, vaccines from Johnson & Johnson and Novavax generated encouraging phase III data. 2021 is shaping

up to be another wild ride.

Evaluate Vantage staff report – February 2021

2

Unless stated, all data are sourced to Evaluate and were accessed in January 2021

Contents

Introduction 2

Covid-19: Biopharma and medtech’s ongoing response 4

Pharma and Biotech 2020 in review 12

One victory for biopharma over the coronavirus in 2020 12

A big year for biotech flotations 16

Covid or not, venture financing breaks records 19

Astrazeneca shows megamergers were still possible in 2020 21

2020 drug approvals rise despite Covid-19 24

MedTech 2020 in review 26

A tale of two Covids for device makers 26

Medtech deal-making stands firm in difficult times 29

Medtechs rake in the venture cash 31

Astounding success greets newly public device makers 34

Focus on Covid-19 does not distract the FDA 36

3 Evaluate Vantage Pharma, Biotech and Medtech 2020 in review Copyright © 2021 Evaluate Ltd. All rights reserved.

4 Copyright © 2021 Evaluate Ltd. All rights reserved.Covid-19: Biopharma and medtech’s ongoing response

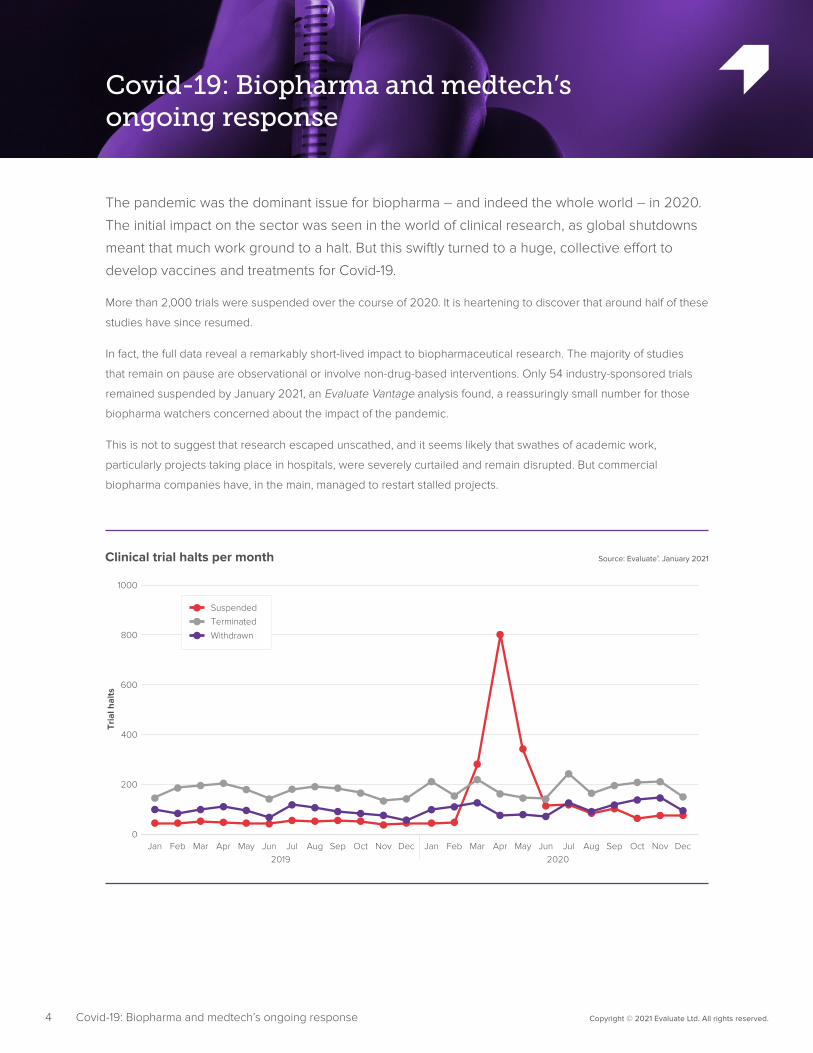

The pandemic was the dominant issue for biopharma – and indeed the whole world – in 2020.

The initial impact on the sector was seen in the world of clinical research, as global shutdowns

meant that much work ground to a halt. But this swiftly turned to a huge, collective effort to

develop vaccines and treatments for Covid-19.

More than 2,000 trials were suspended over the course of 2020. It is heartening to discover that around half of these

studies have since resumed.

In fact, the full data reveal a remarkably short-lived impact to biopharmaceutical research. The majority of studies

that remain on pause are observational or involve non-drug-based interventions. Only 54 industry-sponsored trials

remained suspended by January 2021, an Evaluate Vantage analysis found, a reassuringly small number for those

biopharma watchers concerned about the impact of the pandemic.

This is not to suggest that research escaped unscathed, and it seems likely that swathes of academic work,

particularly projects taking place in hospitals, were severely curtailed and remain disrupted. But commercial

biopharma companies have, in the main, managed to restart stalled projects.

Covid-19: Biopharma and medtech’s ongoing response

Source: Evaluate®. January 2021Clinical trial halts per month

Tria

l hal

ts

600

800

400

200

1000

0

Terminated

Suspended

Withdrawn

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2019 2020

This analysis uses clinicaltrials.gov data, focusing on changes made to trial entries that concern the recruitment status

of a study. Those that were changed to suspended, terminated or withdrawn between January 2019 and December

2020 were identified.

A more detailed look at this data can be found here:

Clinical development

Vaccines offer the world an exit from the pandemic, and thus much of the focus has fallen on

these development efforts. As it stands in early 2021, mRNA-based projects from Biontech/

Pfizer and Moderna are being rolled out in many countries, while Astrazeneca is waiting to hear

whether it can add EU authorisation to its green light in the UK. Locally developed vaccines are

also available in Russia and China.

But other options are needed, and the table below highlights the most closely watched contenders. The progress

or otherwise of vaccines from J&J and Novavax will make a big difference to how the world looks 12 months from

now. These two groups are next in the queue to report data and seek approval, after which they could supply huge

quantities of shots in 2021.

Setbacks cannot be ruled out, unfortunately, and January 2021 saw Merck & Co scrap two early-stage candidates,

and a month earlier CSL had canned its project in phase I. Merck said efficacy could not match existing options,

while safety concerns caused the Australian biotech to pull the plug.

Development delays have also hit partners Sanofi and Glaxo, two of the world’s leading vaccine developers which

between them have the manufacturing capacity to help feed the huge global demand. Necessary reformulation

pushed back the potential launch of their project by six months to late 2021, the pharma giants said in December, an

estimate that feels like a best-case scenario.

All eyes will be on these projects waiting in the wings this year, in the hope that vaccine output can be massively

upscaled in 2021.

5 Copyright © 2021 Evaluate Ltd. All rights reserved.Covid-19: Biopharma and medtech’s ongoing response

Project Description Company Update

Comirnaty (BNT162b2) mRNA (2 dose) Pfizer/Biontech Global rollout underway.

mRNA-1273 mRNA (2 dose) Moderna Rollout in US underway, green light in Europe.

Sputnik V Adenovirus (2 dose) Gamaleya Research Institute/Russia

Rolling out in Russia

AZD1222 Chimp adenovirus (2 dose) Astrazeneca Rolling out in UK; under review in Europe; US trial due to report 2021

Ad26.COV2-S Adeno type 26 (1 & 2 dose) J&J Ph3 Ensemble (single dose) data due Jan 2021; Ensemble 2 (2-dose) recruiting, data due 2021.

NVX-CoV2373 Recombinant nanoparticle (2 dose) Novavax Data from UK ph3 and S Africa ph2b due Q1'21; US/Mexico ph3 data due Q2'21.

CVnCoV mRNA (2 dose) Curevac Herald, Europe ph2/3 data due Q1'21; Europe ph3 due 2021.

COVID-19 S-Trimer Trimerised fusion protein (2 dose) Clover/Glaxo Ph1 ongoing; ph2/3 due to start.

Covid-19 vaccine project Recombinant protein (1 or 2 dose tbc) Sanofi/Glaxo Ph3 due to start 2021, pending development of new formulation.

Next steps for selected clinical-stage Covid-19 vaccines Source: Evaluate®, company statements. January 2021

In terms of gauging what sales of vaccines might look like, analysts covering big pharma companies have tended

to wait until proof of efficacy emerged before forecasting demand. Biotech analysts covering Novavax have put in

numbers ahead of data, illustrating the high expectations here.

As such, a reliable consensus is only available for the three products below. Lack of numbers for AZD1222 can

probably be explained by Astra’s pledge not to make a profit while a pandemic is declared, although it is still

uncertain whether this particular vaccine will get much use in the US.

6 Copyright © 2021 Evaluate Ltd. All rights reserved.Covid-19: Biopharma and medtech’s ongoing response

Source: Evaluate®. January 2021Vaccine demand: a sellside view

Ann

ual s

ales

WW

($bn

)

3

4

5

6

7

1

2

NVX-CoV2373 (Novavax)

mRNA-1273 (Moderna)

Comirnaty (Pfizer)

2020 2021 2022 2023 2024 2025 20260

7 Copyright © 2021 Evaluate Ltd. All rights reserved.Covid-19: Biopharma and medtech’s ongoing response

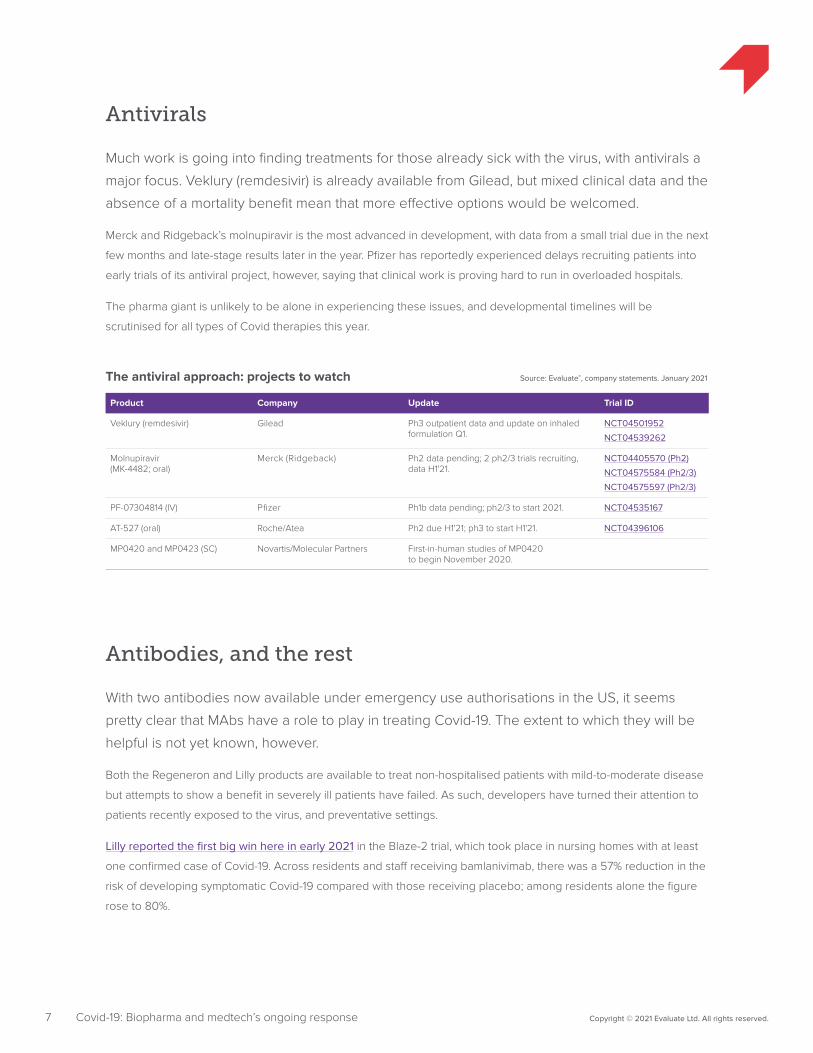

Antivirals

Much work is going into finding treatments for those already sick with the virus, with antivirals a

major focus. Veklury (remdesivir) is already available from Gilead, but mixed clinical data and the

absence of a mortality benefit mean that more effective options would be welcomed.

Merck and Ridgeback’s molnupiravir is the most advanced in development, with data from a small trial due in the next

few months and late-stage results later in the year. Pfizer has reportedly experienced delays recruiting patients into

early trials of its antiviral project, however, saying that clinical work is proving hard to run in overloaded hospitals.

The pharma giant is unlikely to be alone in experiencing these issues, and developmental timelines will be

scrutinised for all types of Covid therapies this year.

Product Company Update Trial ID

Veklury (remdesivir) Gilead Ph3 outpatient data and update on inhaled formulation Q1.

NCT04501952

NCT04539262

Molnupiravir (MK-4482; oral)

Merck (Ridgeback) Ph2 data pending; 2 ph2/3 trials recruiting, data H1'21.

NCT04405570 (Ph2)

NCT04575584 (Ph2/3)

NCT04575597 (Ph2/3)

PF-07304814 (IV) Pfizer Ph1b data pending; ph2/3 to start 2021. NCT04535167

AT-527 (oral) Roche/Atea Ph2 due H1'21; ph3 to start H1'21. NCT04396106

MP0420 and MP0423 (SC) Novartis/Molecular Partners First-in-human studies of MP0420 to begin November 2020.

The antiviral approach: projects to watch Source: Evaluate®, company statements. January 2021

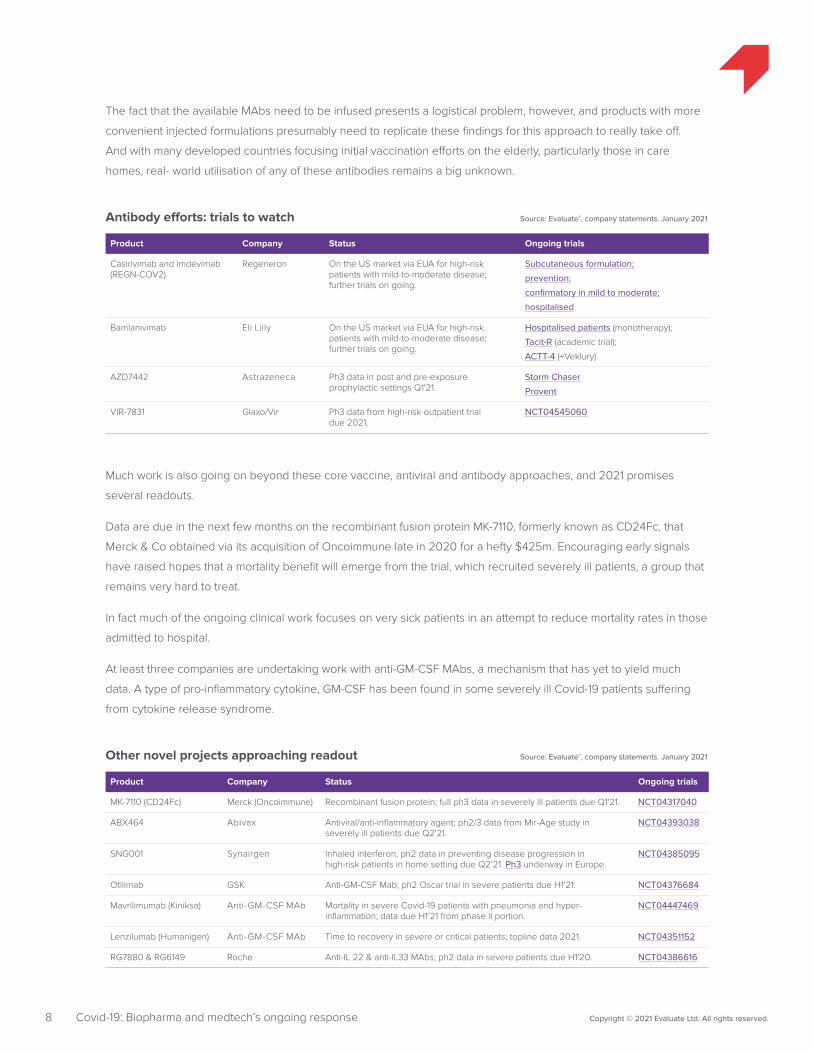

Antibodies, and the rest

With two antibodies now available under emergency use authorisations in the US, it seems

pretty clear that MAbs have a role to play in treating Covid-19. The extent to which they will be

helpful is not yet known, however.

Both the Regeneron and Lilly products are available to treat non-hospitalised patients with mild-to-moderate disease

but attempts to show a benefit in severely ill patients have failed. As such, developers have turned their attention to

patients recently exposed to the virus, and preventative settings.

Lilly reported the first big win here in early 2021 in the Blaze-2 trial, which took place in nursing homes with at least

one confirmed case of Covid-19. Across residents and staff receiving bamlanivimab, there was a 57% reduction in the

risk of developing symptomatic Covid-19 compared with those receiving placebo; among residents alone the figure

rose to 80%.

8 Copyright © 2021 Evaluate Ltd. All rights reserved.Covid-19: Biopharma and medtech’s ongoing response

The fact that the available MAbs need to be infused presents a logistical problem, however, and products with more

convenient injected formulations presumably need to replicate these findings for this approach to really take off.

And with many developed countries focusing initial vaccination efforts on the elderly, particularly those in care

homes, real- world utilisation of any of these antibodies remains a big unknown.

Product Company Status Ongoing trials

Casirivimab and imdevimab (REGN-COV2)

Regeneron On the US market via EUA for high-risk patients with mild-to-moderate disease; further trials on going.

Subcutaneous formulation;

prevention;

confirmatory in mild to moderate;

hospitalised

Bamlanivimab Eli Lilly On the US market via EUA for high-risk patients with mild-to-moderate disease; further trials on going.

Hospitalised patients (monotherapy);

Tacit-R (academic trial);

ACTT-4 (+Veklury)

AZD7442 Astrazeneca Ph3 data in post and pre-exposure prophylactic settings Q1'21.

Storm Chaser

Provent

VIR-7831 Glaxo/Vir Ph3 data from high-risk outpatient trial due 2021.

NCT04545060

Product Company Status Ongoing trials

MK-7110 (CD24Fc) Merck (Oncoimmune) Recombinant fusion protein; full ph3 data in severely ill patients due Q1'21. NCT04317040

ABX464 Abivax Antiviral/anti-inflammatory agent; ph2/3 data from Mir-Age study in severely ill patients due Q2'21.

NCT04393038

SNG001 Synairgen Inhaled interferon; ph2 data in preventing disease progression in high-risk patients in home setting due Q2’21. Ph3 underway in Europe.

NCT04385095

Otilimab GSK Anti-GM-CSF Mab; ph2 Oscar trial in severe patients due H1'21. NCT04376684

Mavrilimumab (Kiniksa) Anti-GM-CSF MAb Mortality in severe Covid-19 patients with pneumonia and hyper- inflammation; data due H1’21 from phase II portion.

NCT04447469

Lenzilumab (Humanigen) Anti-GM-CSF MAb Time to recovery in severe or critical patients; topline data 2021. NCT04351152

RG7880 & RG6149 Roche Anti-IL 22 & anti-IL33 MAbs; ph2 data in severe patients due H1'20. NCT04386616

Antibody efforts: trials to watch Source: Evaluate®, company statements. January 2021

Other novel projects approaching readout Source: Evaluate®, company statements. January 2021

Much work is also going on beyond these core vaccine, antiviral and antibody approaches, and 2021 promises

several readouts.

Data are due in the next few months on the recombinant fusion protein MK-7110, formerly known as CD24Fc, that

Merck & Co obtained via its acquisition of Oncoimmune late in 2020 for a hefty $425m. Encouraging early signals

have raised hopes that a mortality benefit will emerge from the trial, which recruited severely ill patients, a group that

remains very hard to treat.

In fact much of the ongoing clinical work focuses on very sick patients in an attempt to reduce mortality rates in those

admitted to hospital.

At least three companies are undertaking work with anti-GM-CSF MAbs, a mechanism that has yet to yield much

data. A type of pro-inflammatory cytokine, GM-CSF has been found in some severely ill Covid-19 patients suffering

from cytokine release syndrome.

9 Copyright © 2021 Evaluate Ltd. All rights reserved.Covid-19: Biopharma and medtech’s ongoing response

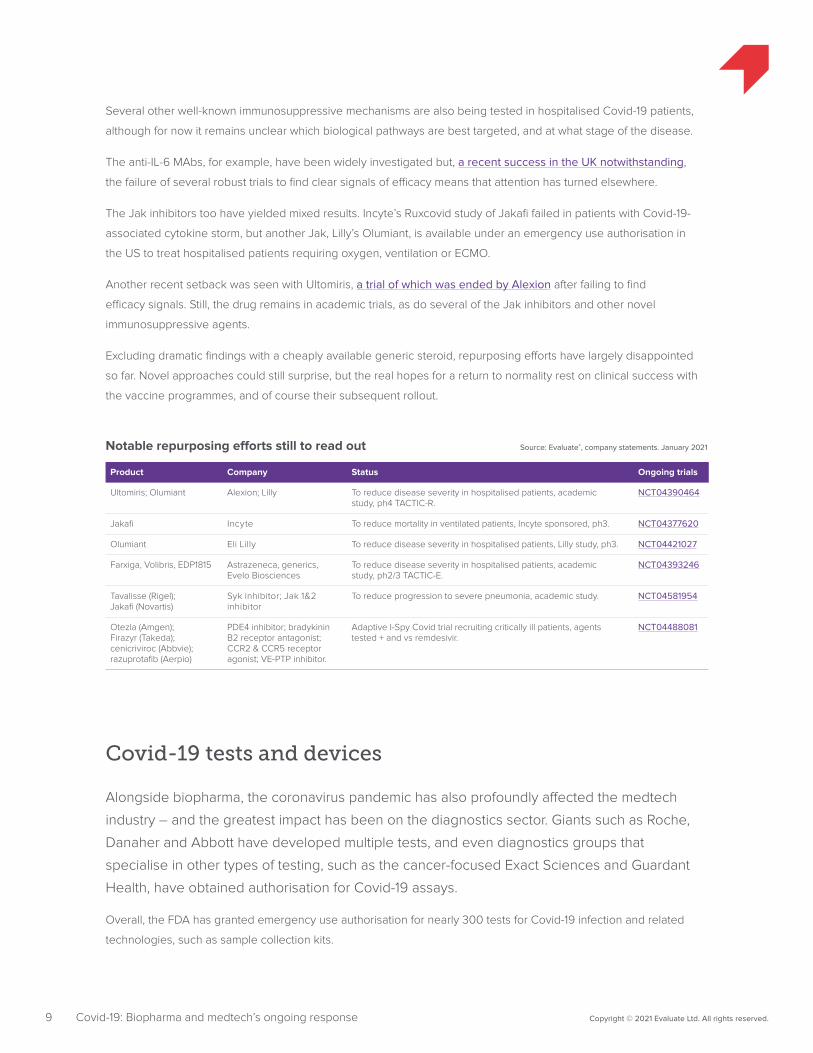

Several other well-known immunosuppressive mechanisms are also being tested in hospitalised Covid-19 patients,

although for now it remains unclear which biological pathways are best targeted, and at what stage of the disease.

The anti-IL-6 MAbs, for example, have been widely investigated but, a recent success in the UK notwithstanding,

the failure of several robust trials to find clear signals of efficacy means that attention has turned elsewhere.

The Jak inhibitors too have yielded mixed results. Incyte’s Ruxcovid study of Jakafi failed in patients with Covid-19-

associated cytokine storm, but another Jak, Lilly’s Olumiant, is available under an emergency use authorisation in

the US to treat hospitalised patients requiring oxygen, ventilation or ECMO.

Another recent setback was seen with Ultomiris, a trial of which was ended by Alexion after failing to find

efficacy signals. Still, the drug remains in academic trials, as do several of the Jak inhibitors and other novel

immunosuppressive agents.

Excluding dramatic findings with a cheaply available generic steroid, repurposing efforts have largely disappointed

so far. Novel approaches could still surprise, but the real hopes for a return to normality rest on clinical success with

the vaccine programmes, and of course their subsequent rollout.

Covid-19 tests and devices

Alongside biopharma, the coronavirus pandemic has also profoundly affected the medtech

industry – and the greatest impact has been on the diagnostics sector. Giants such as Roche,

Danaher and Abbott have developed multiple tests, and even diagnostics groups that

specialise in other types of testing, such as the cancer-focused Exact Sciences and Guardant

Health, have obtained authorisation for Covid-19 assays.

Overall, the FDA has granted emergency use authorisation for nearly 300 tests for Covid-19 infection and related

technologies, such as sample collection kits.

Product Company Status Ongoing trials

Ultomiris; Olumiant Alexion; Lilly To reduce disease severity in hospitalised patients, academic study, ph4 TACTIC-R.

NCT04390464

Jakafi Incyte To reduce mortality in ventilated patients, Incyte sponsored, ph3. NCT04377620

Olumiant Eli Lilly To reduce disease severity in hospitalised patients, Lilly study, ph3. NCT04421027

Farxiga, Volibris, EDP1815 Astrazeneca, generics, Evelo Biosciences

To reduce disease severity in hospitalised patients, academic study, ph2/3 TACTIC-E.

NCT04393246

Tavalisse (Rigel); Jakafi (Novartis)

Syk inhibitor; Jak 1&2 inhibitor

To reduce progression to severe pneumonia, academic study. NCT04581954

Otezla (Amgen); Firazyr (Takeda); cenicriviroc (Abbvie); razuprotafib (Aerpio)

PDE4 inhibitor; bradykinin B2 receptor antagonist; CCR2 & CCR5 receptor agonist; VE-PTP inhibitor.

Adaptive I-Spy Covid trial recruiting critically ill patients, agents tested + and vs remdesivir.

NCT04488081

Notable repurposing efforts still to read out Source: Evaluate®, company statements. January 2021

10 Copyright © 2021 Evaluate Ltd. All rights reserved.Covid-19: Biopharma and medtech’s ongoing response

With treatments arriving, the emphasis at the agency has quite rightly switched to evaluating and approving vaccines.

But new tests were still reaching the market right up to the end of 2020, with Nirmidas Biotech’s MidaSpot Covid-19

antibody test winning authorisation on New Year’s Eve.

While the first half of 2020 was all about RNA and antibody tests, for current and previous infections respectively, the

latter half of the year saw growing emphasis on new testing modalities.

Lateral flow antigen testing holds great promise for testing large numbers of people quickly and cheaply, but since

these tests are less sensitive than molecular assays they must be used repeatedly within a stable population if they

are to keep infections under control. The cost of repeated testing mounts up quickly, and the logistical challenges,

including of the subsequent contact tracing, are considerable.

T-cell-mediated immunity is, alongside antibody testing, a potentially highly useful technique for assessing immunity

to the coronavirus, both in people previously infected and those who have received a vaccine. Data backing this

approach are early but encouraging, and T-cell testing could yet become a part of efforts to assess the effectiveness

of vaccination regimens, and identify patients who need a booster.

50

250

0

100

150

200

Cum

ulat

ive

tria

l cou

nt

EUAs granted to Covid-19 tests Source: Evaluate®, FDA. January 2021

Antibody tests

Viral RNA tests

Other

Mar 2020 May 2020 Jul 2020 Sep 2020 Nov 2020 Jan 2021

The pace of test authorisations undeniably slackened during the autumn, however. As the vaccine rollout continues,

and hopefully accelerates under the new administration, demand for Covid-19 assays ought to shrink.

EUA = emergency use authorisation. Commercial tests only; cumulative figures.Note: “Other” includes 11 antigen tests, six home sampling kits, three saliva collection devices and three IL-6 tests.

11 Copyright © 2021 Evaluate Ltd. All rights reserved.Covid-19: Biopharma and medtech’s ongoing response

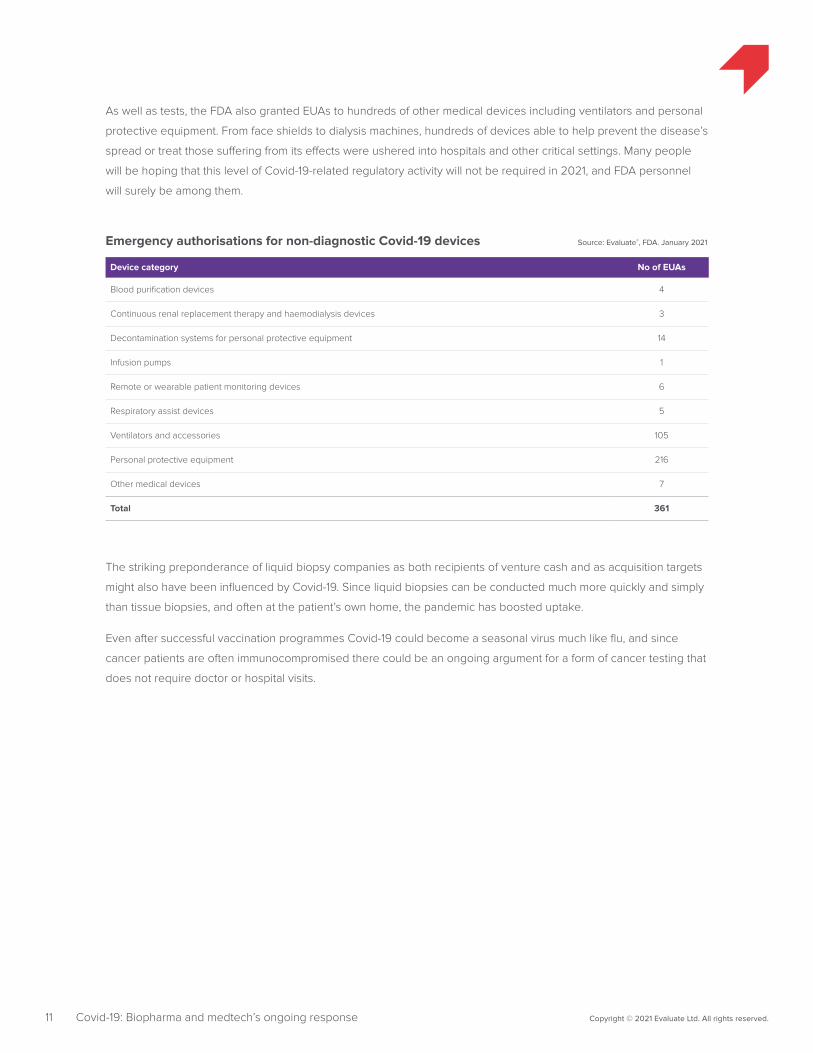

Device category No of EUAs

Blood purification devices 4

Continuous renal replacement therapy and haemodialysis devices 3

Decontamination systems for personal protective equipment 14

Infusion pumps 1

Remote or wearable patient monitoring devices 6

Respiratory assist devices 5

Ventilators and accessories 105

Personal protective equipment 216

Other medical devices 7

Total 361

Emergency authorisations for non-diagnostic Covid-19 devices Source: Evaluate®, FDA. January 2021

The striking preponderance of liquid biopsy companies as both recipients of venture cash and as acquisition targets

might also have been influenced by Covid-19. Since liquid biopsies can be conducted much more quickly and simply

than tissue biopsies, and often at the patient’s own home, the pandemic has boosted uptake.

Even after successful vaccination programmes Covid-19 could become a seasonal virus much like flu, and since

cancer patients are often immunocompromised there could be an ongoing argument for a form of cancer testing that

does not require doctor or hospital visits.

As well as tests, the FDA also granted EUAs to hundreds of other medical devices including ventilators and personal

protective equipment. From face shields to dialysis machines, hundreds of devices able to help prevent the disease’s

spread or treat those suffering from its effects were ushered into hospitals and other critical settings. Many people

will be hoping that this level of Covid-19-related regulatory activity will not be required in 2021, and FDA personnel

will surely be among them.

Pharma and Biotech 2020 in review

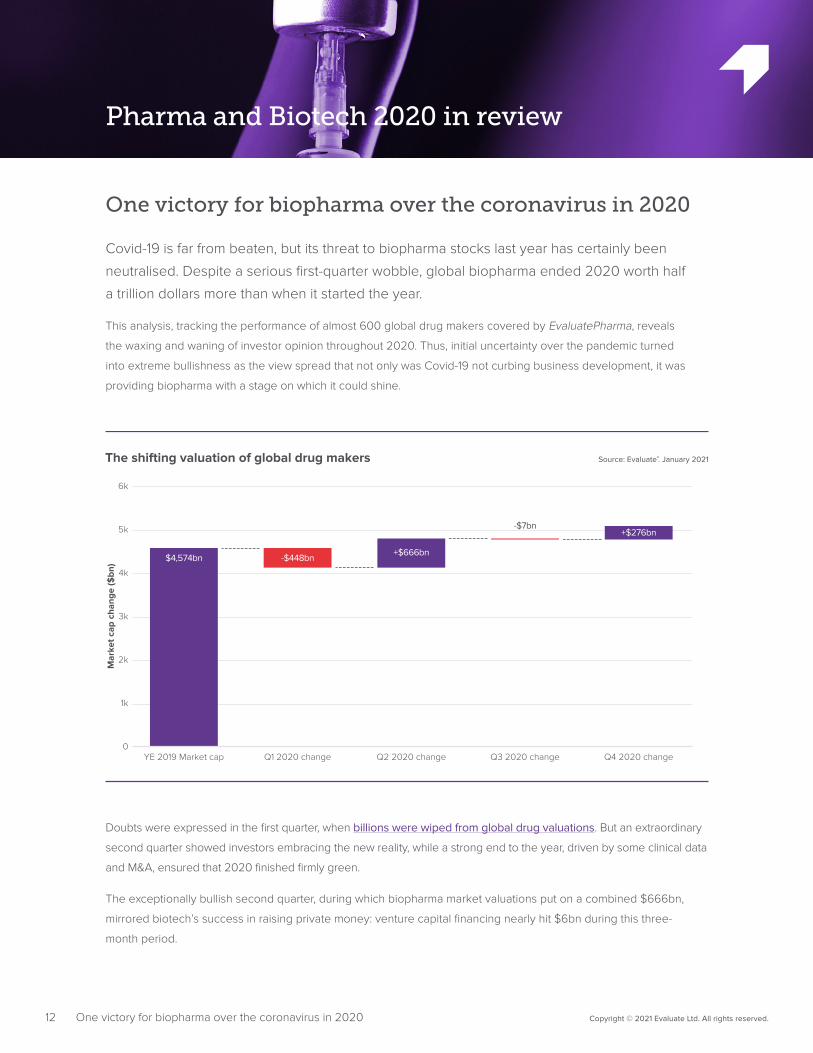

12 Copyright © 2021 Evaluate Ltd. All rights reserved.One victory for biopharma over the coronavirus in 2020

One victory for biopharma over the coronavirus in 2020

Covid-19 is far from beaten, but its threat to biopharma stocks last year has certainly been

neutralised. Despite a serious first-quarter wobble, global biopharma ended 2020 worth half

a trillion dollars more than when it started the year.

This analysis, tracking the performance of almost 600 global drug makers covered by EvaluatePharma, reveals

the waxing and waning of investor opinion throughout 2020. Thus, initial uncertainty over the pandemic turned

into extreme bullishness as the view spread that not only was Covid-19 not curbing business development, it was

providing biopharma with a stage on which it could shine.

Source: Evaluate®. January 2021The shifting valuation of global drug makers

Mar

ket c

ap c

hang

e ($

bn)

1k

2k

3k

4k

5k

6k

YE 2019 Market cap

$4,574bn

Q1 2020 change

-$448bn

Q2 2020 change

+$666bn

Q3 2020 change

-$7bn

Q4 2020 change

+$276bn

0

Doubts were expressed in the first quarter, when billions were wiped from global drug valuations. But an extraordinary

second quarter showed investors embracing the new reality, while a strong end to the year, driven by some clinical data

and M&A, ensured that 2020 finished firmly green.

The exceptionally bullish second quarter, during which biopharma market valuations put on a combined $666bn,

mirrored biotech’s success in raising private money: venture capital financing nearly hit $6bn during this three-

month period.

13 Copyright © 2021 Evaluate Ltd. All rights reserved.One victory for biopharma over the coronavirus in 2020

Source: Evaluate®. January 2021Absolute market cap gains and losses, by size bracket

Mar

ket c

ap m

ovem

ent (

$bn

)

-200

-100

100

200

300

Q1 2020 Q2 2020 Q3 2020 Q4 2020-300

0

25bn+

Bigpharma

250m-5bn

5bn-25bn

Source: Evaluate®. January 2021Percentage market cap gains and losses, by size bracket

% o

f mar

ket c

ap to

tal

-10%

10%

20%

30%

40%

-20%

0%

25bn+

Bigpharma

250m-5bn

5bn-25bn

Q1 2020 Q2 2020 Q3 2020 Q4 2020

True enough, there was another small wobble in the third quarter, but a more granular analysis reveals this to have been

down to quarterly collapses in the share prices of Bayer, over the continuing Monsanto acquisition fallout, and Gilead.

Gilead is an interesting case in point. Its stock had initially surged on hopes that the antiviral Veklury could treat

Covid-19. The reality turned out to be rather different, and the shares sold off, as two major acquisitions failed to

dispel investor concerns about future growth.

14 Copyright © 2021 Evaluate Ltd. All rights reserved.One victory for biopharma over the coronavirus in 2020

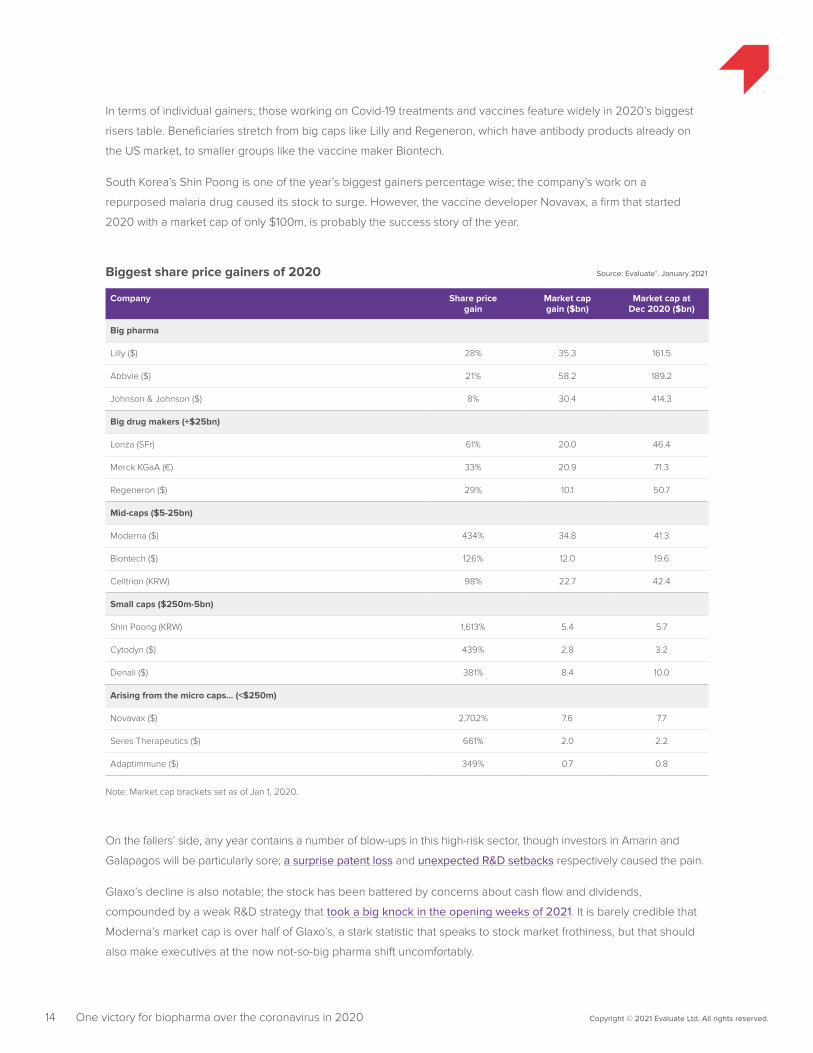

In terms of individual gainers, those working on Covid-19 treatments and vaccines feature widely in 2020’s biggest

risers table. Beneficiaries stretch from big caps like Lilly and Regeneron, which have antibody products already on

the US market, to smaller groups like the vaccine maker Biontech.

South Korea’s Shin Poong is one of the year’s biggest gainers percentage wise; the company’s work on a

repurposed malaria drug caused its stock to surge. However, the vaccine developer Novavax, a firm that started

2020 with a market cap of only $100m, is probably the success story of the year.

Company Share price gain

Market cap gain ($bn)

Market cap at Dec 2020 ($bn)

Big pharma

Lilly ($) 28% 35.3 161.5

Abbvie ($) 21% 58.2 189.2

Johnson & Johnson ($) 8% 30.4 414.3

Big drug makers (+$25bn)

Lonza (SFr) 61% 20.0 46.4

Merck KGaA (€) 33% 20.9 71.3

Regeneron ($) 29% 10.1 50.7

Mid-caps ($5-25bn)

Moderna ($) 434% 34.8 41.3

Biontech ($) 126% 12.0 19.6

Celltrion (KRW) 98% 22.7 42.4

Small caps ($250m-5bn)

Shin Poong (KRW) 1,613% 5.4 5.7

Cytodyn ($) 439% 2.8 3.2

Denali ($) 381% 8.4 10.0

Arising from the micro caps… (<$250m)

Novavax ($) 2,702% 7.6 7.7

Seres Therapeutics ($) 661% 2.0 2.2

Adaptimmune ($) 349% 0.7 0.8

Biggest share price gainers of 2020 Source: Evaluate®. January 2021

On the fallers’ side, any year contains a number of blow-ups in this high-risk sector, though investors in Amarin and

Galapagos will be particularly sore; a surprise patent loss and unexpected R&D setbacks respectively caused the pain.

Glaxo’s decline is also notable; the stock has been battered by concerns about cash flow and dividends,

compounded by a weak R&D strategy that took a big knock in the opening weeks of 2021. It is barely credible that

Moderna’s market cap is over half of Glaxo’s, a stark statistic that speaks to stock market frothiness, but that should

also make executives at the now not-so-big pharma shift uncomfortably.

Note: Market cap brackets set as of Jan 1, 2020.

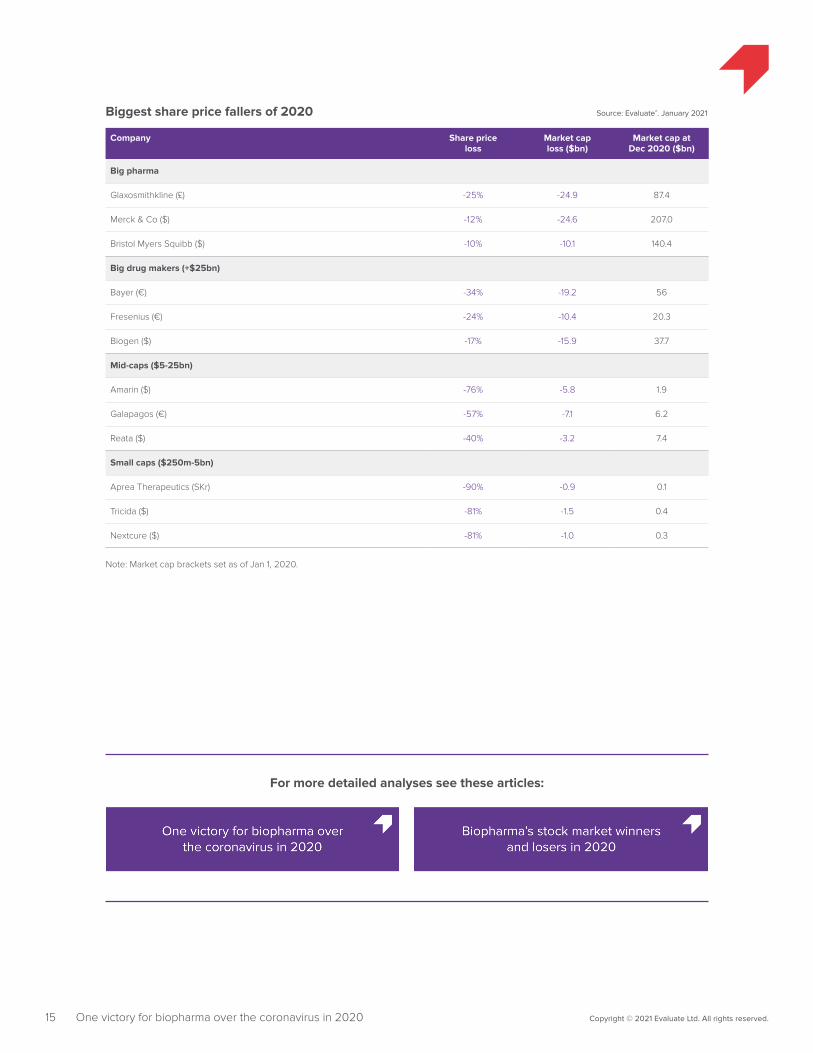

15 Copyright © 2021 Evaluate Ltd. All rights reserved.One victory for biopharma over the coronavirus in 2020

Company Share price loss

Market cap loss ($bn)

Market cap at Dec 2020 ($bn)

Big pharma

Glaxosmithkline (£) -25% -24.9 87.4

Merck & Co ($) -12% -24.6 207.0

Bristol Myers Squibb ($) -10% -10.1 140.4

Big drug makers (+$25bn)

Bayer (€) -34% -19.2 56

Fresenius (€) -24% -10.4 20.3

Biogen ($) -17% -15.9 37.7

Mid-caps ($5-25bn)

Amarin ($) -76% -5.8 1.9

Galapagos (€) -57% -7.1 6.2

Reata ($) -40% -3.2 7.4

Small caps ($250m-5bn)

Aprea Therapeutics (SKr) -90% -0.9 0.1

Tricida ($) -81% -1.5 0.4

Nextcure ($) -81% -1.0 0.3

Biggest share price fallers of 2020 Source: Evaluate®. January 2021

Note: Market cap brackets set as of Jan 1, 2020.

For more detailed analyses see these articles:

16 Copyright © 2021 Evaluate Ltd. All rights reserved.A big year for biotech flotations

10%

-20%

-10%

0%

Source: Evaluate®. January 2021Tracking demand for IPOs

Ave

rage

pre

miu

m/d

isco

unt t

o flo

at r

ange

2016

Q1 Q2 Q3 Q4

2017

Q1 Q2 Q3 Q4

2018

Q1 Q2 Q3 Q4

2019

Q1 Q2 Q3 Q4

2020

Q1 Q2 Q3 Q4-30%

-11

-19

-10

0-1

-2 -2

-6

-2

2

-1

-18

-5

-3

0

-8

4

8

6

Year

4

Average premium/discount to float range

A big year for biotech flotations

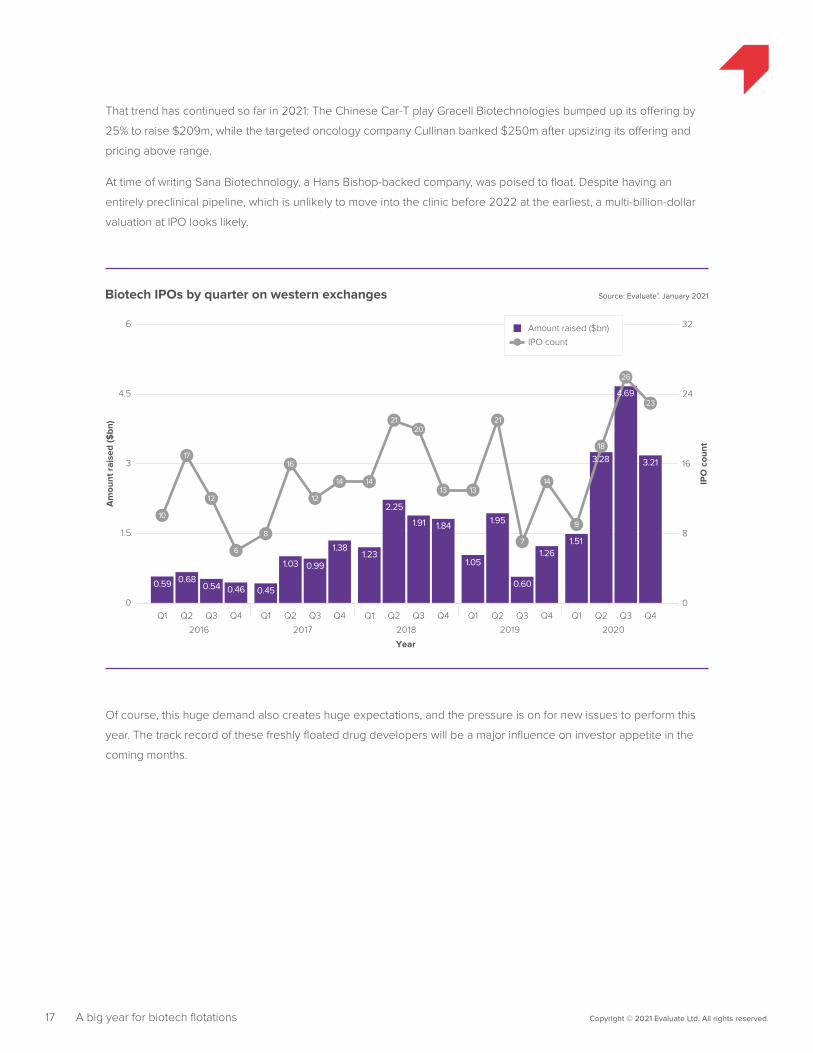

With the final numbers in, the excesses of 2020 are laid bare. An astonishing $12.7bn was

raised last year by young drug developers via IPOs, a figure that outstrips previous records

by a long way.

The number of companies that went public is also high, although not remarkably so. But those that did float managed

to amass huge sums, taking full advantage of the cash flowing readily into the sector.

Whether this largesse continues in 2021 is the burning question for IPO investors, and for now there are few signs of

diminishing appetites.

These analyses concern pure-play drug developers only.

The chart above illustrates how investor interest in biotech soared last year, with all listing companies managing to

float at or above the initial prices proposed by bankers. Many pulled off upsized offerings, selling substantially more

shares than planned at valuations inflated by huge demand.

17 Copyright © 2021 Evaluate Ltd. All rights reserved.A big year for biotech flotations

6

1.5

3

4.5

Am

ount

rai

sed

($bn

)

IPO

cou

nt

32

24

8

16

0

Amount raised ($bn)

IPO count

2016

Q1

0.59

Q2

0.68

Q3

0.54

Q4

2017

Q1

0.45

Q2 Q3

0.99

Q4

1.38

0.46

2018

Q1 Q2

2.25

1.03

Q3

1.91

Q4

1.84

2019

Q1

1.23

Q2 Q3 Q4

2020

Q1

1.51

Q2 Q3 Q4

3.21

1.05

1.95

0.60

0

10

17

12

6

8

16

12

14 14

2120

13 13

21

7

14

9

18

26

Year

23

1.26

3.28

4.69

Source: Evaluate®. January 2021Biotech IPOs by quarter on western exchanges

That trend has continued so far in 2021: The Chinese Car-T play Gracell Biotechnologies bumped up its offering by

25% to raise $209m, while the targeted oncology company Cullinan banked $250m after upsizing its offering and

pricing above range.

At time of writing Sana Biotechnology, a Hans Bishop-backed company, was poised to float. Despite having an

entirely preclinical pipeline, which is unlikely to move into the clinic before 2022 at the earliest, a multi-billion-dollar

valuation at IPO looks likely.

Of course, this huge demand also creates huge expectations, and the pressure is on for new issues to perform this

year. The track record of these freshly floated drug developers will be a major influence on investor appetite in the

coming months.

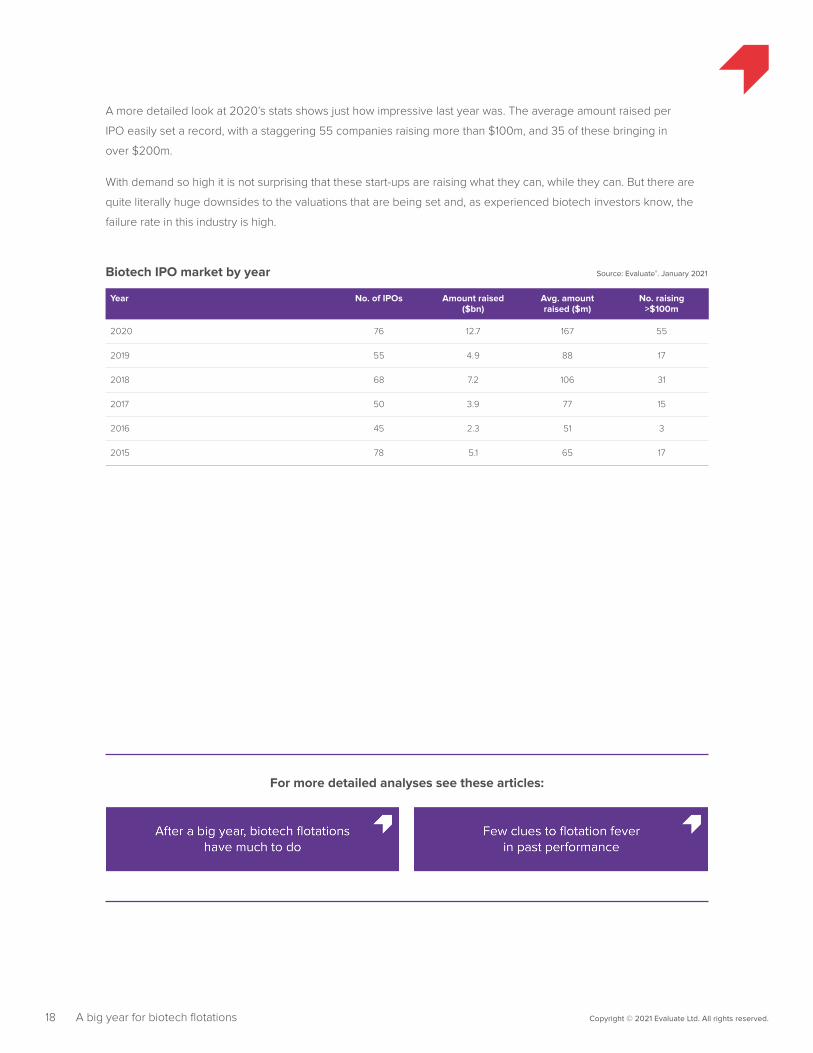

A more detailed look at 2020’s stats shows just how impressive last year was. The average amount raised per

IPO easily set a record, with a staggering 55 companies raising more than $100m, and 35 of these bringing in

over $200m.

With demand so high it is not surprising that these start-ups are raising what they can, while they can. But there are

quite literally huge downsides to the valuations that are being set and, as experienced biotech investors know, the

failure rate in this industry is high.

18 Copyright © 2021 Evaluate Ltd. All rights reserved.A big year for biotech flotations

Year No. of IPOs Amount raised ($bn)

Avg. amount raised ($m)

No. raising >$100m

2020 76 12.7 167 55

2019 55 4.9 88 17

2018 68 7.2 106 31

2017 50 3.9 77 15

2016 45 2.3 51 3

2015 78 5.1 65 17

Biotech IPO market by year Source: Evaluate®. January 2021

For more detailed analyses see these articles:

19 Copyright © 2021 Evaluate Ltd. All rights reserved.Covid or not, venture financing breaks records

8

2

3

1

4

6

7

5

Source: Evaluate®. January 2021Quarterly biopharma VC rounds

Com

bine

d in

vest

men

t ($

bn)

Num

ber

of r

ound

s2016

Q1

2.782.43 2.39

2.84 2.97

Q2 Q3 Q4

2017

Q1 Q2 Q3 Q4

2018

Q1 Q2 Q3 Q4

2019

Q1 Q2 Q3 Q4

2020

Q1 Q2 Q3 Q4

Year

2.17

4.10

4.304.34

3.773.42

4.75

5.73

4.884.78124

137

128

108

120

155

140

106

127

117

137

115 112

121

111

98105

118

108

0

200

50

75

25

100

150

175

125

0

3.843.60

97

3.964.73

5.01

$50m - $100m

$100m+ Other rounds

Count

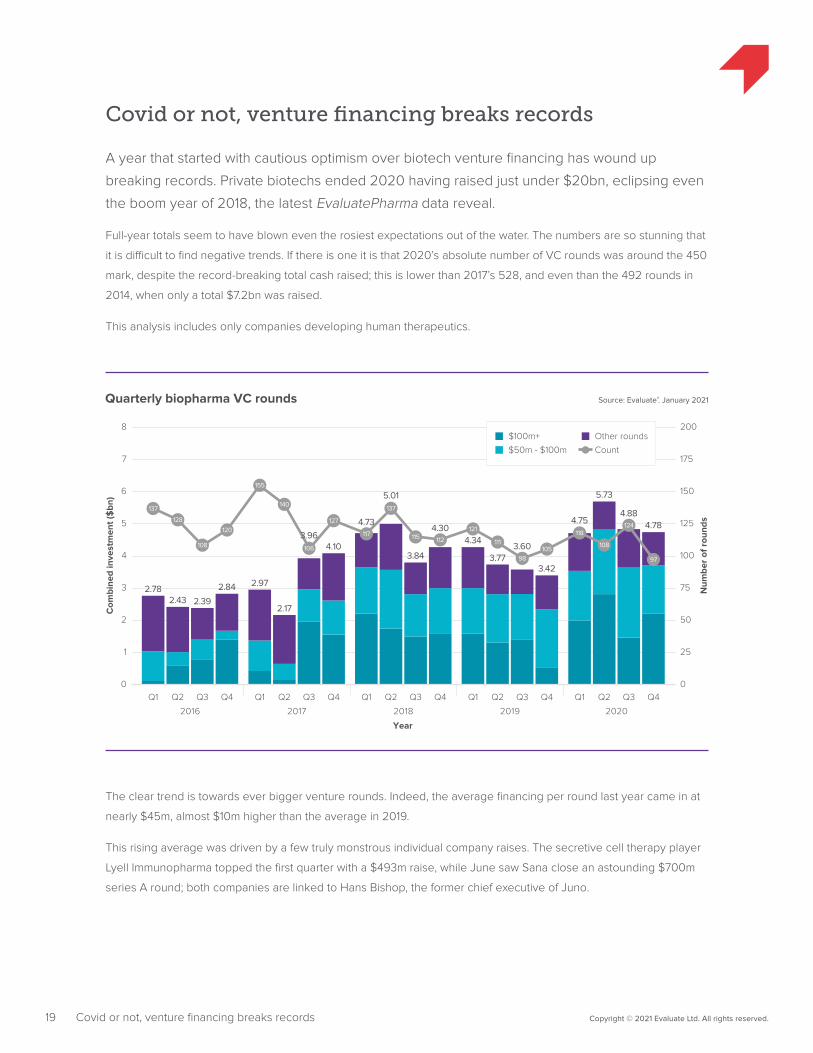

Covid or not, venture financing breaks records

A year that started with cautious optimism over biotech venture financing has wound up

breaking records. Private biotechs ended 2020 having raised just under $20bn, eclipsing even

the boom year of 2018, the latest EvaluatePharma data reveal.

Full-year totals seem to have blown even the rosiest expectations out of the water. The numbers are so stunning that

it is difficult to find negative trends. If there is one it is that 2020’s absolute number of VC rounds was around the 450

mark, despite the record-breaking total cash raised; this is lower than 2017’s 528, and even than the 492 rounds in

2014, when only a total $7.2bn was raised.

This analysis includes only companies developing human therapeutics.

The clear trend is towards ever bigger venture rounds. Indeed, the average financing per round last year came in at

nearly $45m, almost $10m higher than the average in 2019.

This rising average was driven by a few truly monstrous individual company raises. The secretive cell therapy player

Lyell Immunopharma topped the first quarter with a $493m raise, while June saw Sana close an astounding $700m

series A round; both companies are linked to Hans Bishop, the former chief executive of Juno.

20 Copyright © 2021 Evaluate Ltd. All rights reserved.Covid or not, venture financing breaks records

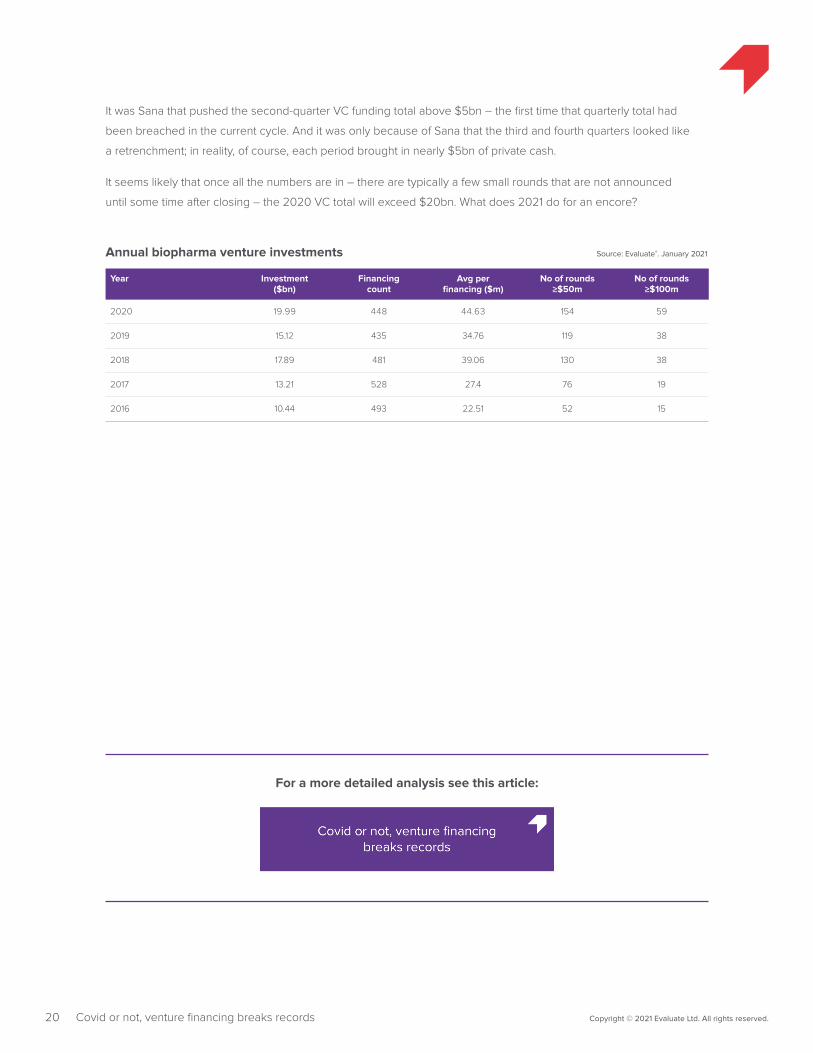

Year Investment ($bn)

Financing count

Avg per financing ($m)

No of rounds ≥$50m

No of rounds ≥$100m

2020 19.99 448 44.63 154 59

2019 15.12 435 34.76 119 38

2018 17.89 481 39.06 130 38

2017 13.21 528 27.4 76 19

2016 10.44 493 22.51 52 15

Annual biopharma venture investments Source: Evaluate®. January 2021

It was Sana that pushed the second-quarter VC funding total above $5bn – the first time that quarterly total had

been breached in the current cycle. And it was only because of Sana that the third and fourth quarters looked like

a retrenchment; in reality, of course, each period brought in nearly $5bn of private cash.

It seems likely that once all the numbers are in – there are typically a few small rounds that are not announced

until some time after closing – the 2020 VC total will exceed $20bn. What does 2021 do for an encore?

For a more detailed analysis see this article:

21 Copyright © 2021 Evaluate Ltd. All rights reserved.Astrazeneca shows megamergers were still possible in 2020

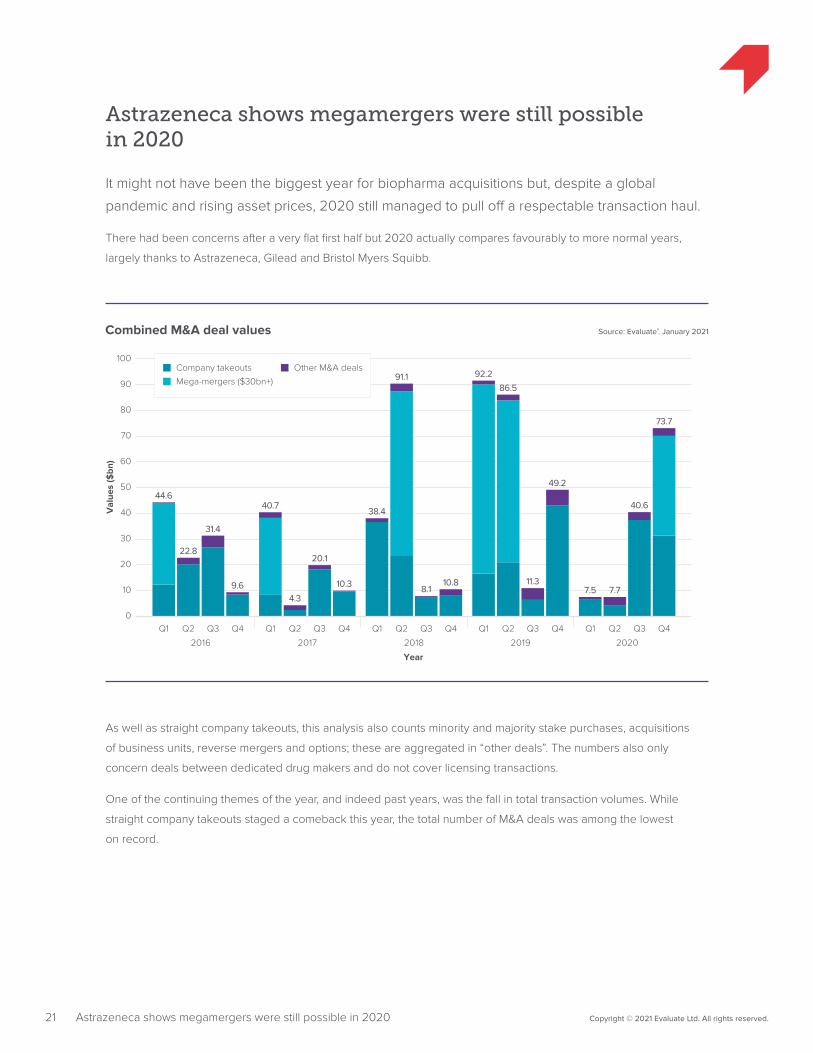

Astrazeneca shows megamergers were still possible in 2020

It might not have been the biggest year for biopharma acquisitions but, despite a global

pandemic and rising asset prices, 2020 still managed to pull off a respectable transaction haul.

There had been concerns after a very flat first half but 2020 actually compares favourably to more normal years,

largely thanks to Astrazeneca, Gilead and Bristol Myers Squibb.

100

20

30

10

40

60

80

90

70

50

Source: Evaluate®. January 2021Combined M&A deal values

Val

ues

($bn

)

2016

Q1

44.6

22.8

31.4

9.6

40.7

Q2 Q3 Q4

2017

Q1 Q2 Q3 Q4

2018

Q1 Q2 Q3 Q4

2019

Q1 Q2 Q3 Q4

2020

Q1 Q2 Q3 Q4

Year

4.3

10.3 10.8

92.2

86.5

49.2

7.5 7.7

40.6

73.7

0

8.111.3

20.1

38.4

91.1Mega-mergers ($30bn+)

Company takeouts Other M&A deals

As well as straight company takeouts, this analysis also counts minority and majority stake purchases, acquisitions

of business units, reverse mergers and options; these are aggregated in “other deals”. The numbers also only

concern deals between dedicated drug makers and do not cover licensing transactions.

One of the continuing themes of the year, and indeed past years, was the fall in total transaction volumes. While

straight company takeouts staged a comeback this year, the total number of M&A deals was among the lowest

on record.

80

20

30

10

40

60

70

50

Source: Evaluate®. January 2021Quarterly M&A deal counts

Dea

l cou

nt

2016

Q1

56

46

53

48

72

Q2 Q3 Q4

2017

Q1 Q2 Q3 Q4

2018

Q1 Q2 Q3 Q4

2019

Q1 Q2 Q3 Q4

2020

Q1 Q2 Q3 Q4

Year

31

51

45 46

35

51

3335

4341

0

464444

46 46

Mega-mergers ($30bn+)

Company takeouts Other M&A deals

After disappointing activity in the first two quarters, as the world got to grips with new ways of working, deal volumes

and values alike picked up in the second half. Indeed, the final quarter saw the year’s biggest deal, Alexion’s $39bn

takeover by Astrazeneca.

The transaction was not only 2020’s sole mega-merger, it also went a long way to saving the year from being

distinctly pedestrian in terms of deal size. The other big spender in 2020 was Gilead, which was one of the few

multiple purchasers, having pulled out its chequebook for Immunomedics and Forty Seven, for a combined $26bn.

The Gilead deals also stand out because of the premiums paid to win those targets, at 110% and 111% respectively,

unusually large for transactions of that size. But asset prices have been high for the past couple of years, the graph

over the page shows.

With smaller developers flush with cash there is little expectation that asset prices will dip in 2021.

22 Copyright © 2021 Evaluate Ltd. All rights reserved.Astrazeneca shows megamergers were still possible in 2020

Source: Evaluate®. January 2021Paying a premium for biopharma buyouts

Ave

rage

pre

miu

m (%

)

100%

125%

75%

50%

150%

25%2016 2017 2018 2019 2020

R&D-stage

All companies

Commercial-stage

For more detailed analyses see these articles:

23 Copyright © 2021 Evaluate Ltd. All rights reserved.Astrazeneca shows megamergers were still possible in 2020

24 Copyright © 2021 Evaluate Ltd. All rights reserved.2020 drug approvals rise despite Covid-19

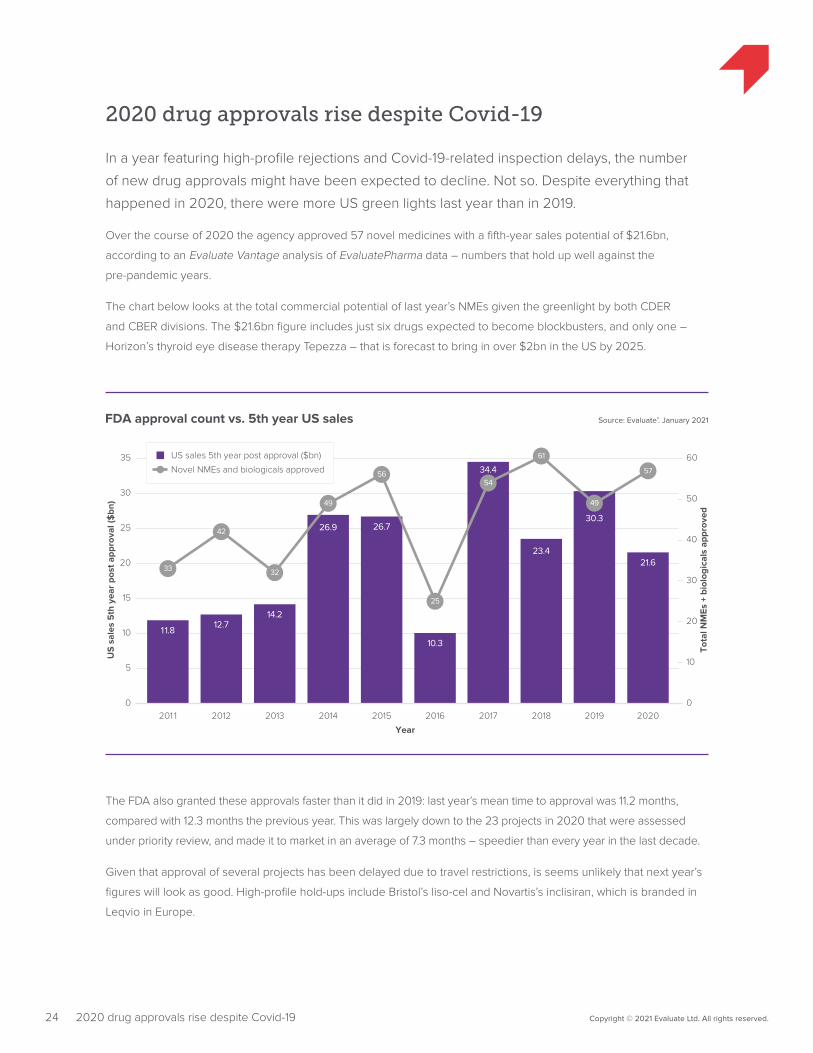

2020 drug approvals rise despite Covid-19

In a year featuring high-profile rejections and Covid-19-related inspection delays, the number

of new drug approvals might have been expected to decline. Not so. Despite everything that

happened in 2020, there were more US green lights last year than in 2019.

Over the course of 2020 the agency approved 57 novel medicines with a fifth-year sales potential of $21.6bn,

according to an Evaluate Vantage analysis of EvaluatePharma data – numbers that hold up well against the

pre-pandemic years.

The chart below looks at the total commercial potential of last year’s NMEs given the greenlight by both CDER

and CBER divisions. The $21.6bn figure includes just six drugs expected to become blockbusters, and only one –

Horizon’s thyroid eye disease therapy Tepezza – that is forecast to bring in over $2bn in the US by 2025.

Source: Evaluate®. January 2021FDA approval count vs. 5th year US sales

US

sal

es 5

th y

ear

post

app

rova

l ($

bn)

Tota

l NM

Es +

bio

logi

cals

app

rove

d

5

10

15

20

25

35

30

60

50

40

30

20

10

0

US sales 5th year post approval ($bn)

Novel NMEs and biologicals approved

Year

2019

30.3

201 1

11.8

2012

12.7

2013

14.2

2014

26.9

2015

26.7

2016

10.3

2017

33

42

32

49

56

2018

23.4

25

54

34.4

61

2020

21.6

0

49

57

The FDA also granted these approvals faster than it did in 2019: last year’s mean time to approval was 11.2 months,

compared with 12.3 months the previous year. This was largely down to the 23 projects in 2020 that were assessed

under priority review, and made it to market in an average of 7.3 months – speedier than every year in the last decade.

Given that approval of several projects has been delayed due to travel restrictions, is seems unlikely that next year’s

figures will look as good. High-profile hold-ups include Bristol’s liso-cel and Novartis’s inclisiran, which is branded in

Leqvio in Europe.

Source: Evaluate®. January 2021CDER+CBER average approval times

Ave

rage

rev

iew

tim

e (m

onth

s)

5

10

15

20

25

0

Standard reviews

Breakthrough therapy reviews

Priority reviews

PDUFA IV PDUFA VIPDUFA V

2011(n=33)

2012(n=42)

2013(n=32)

2014(n=49)

2015(n=56)

2016(n=25)

2017(n=54)

2018(n=61)

2019(n=49)

2020(n=57)

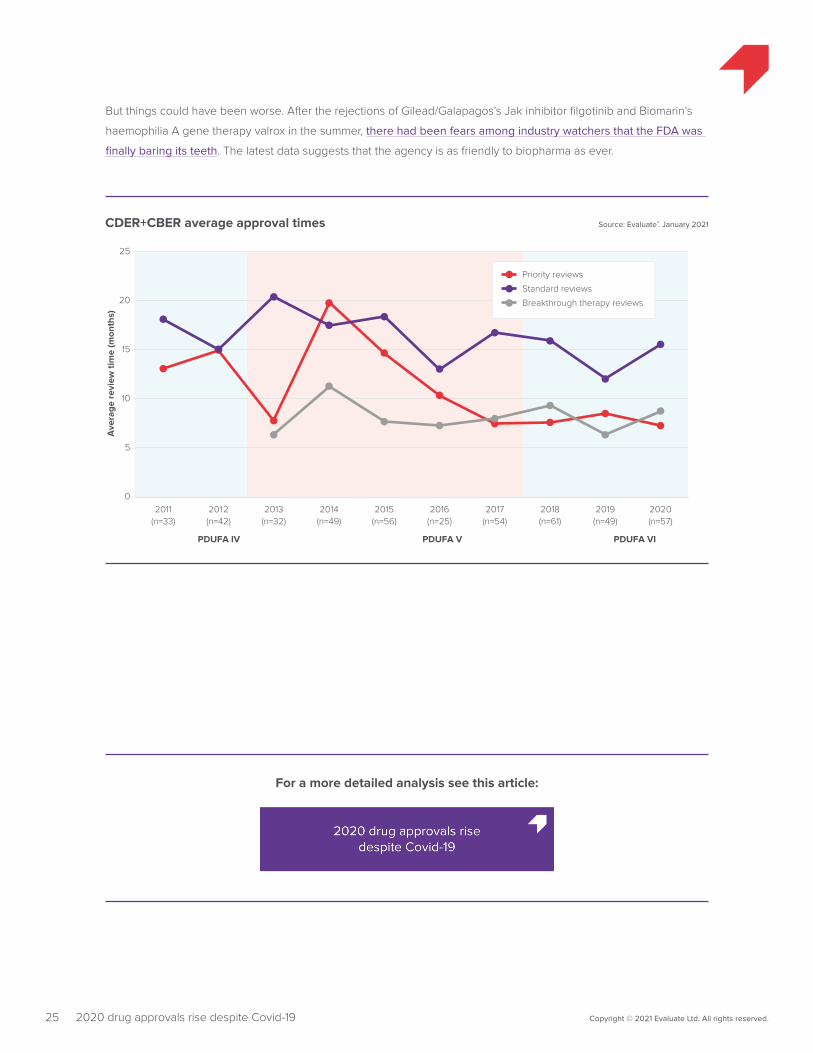

But things could have been worse. After the rejections of Gilead/Galapagos’s Jak inhibitor filgotinib and Biomarin’s

haemophilia A gene therapy valrox in the summer, there had been fears among industry watchers that the FDA was

finally baring its teeth. The latest data suggests that the agency is as friendly to biopharma as ever.

For a more detailed analysis see this article:

25 Copyright © 2021 Evaluate Ltd. All rights reserved.2020 drug approvals rise despite Covid-19

Medtech 2020 in review

26 Copyright © 2021 Evaluate Ltd. All rights reserved.A tale of two Covids for device makers

Stock index % change in 2020

Thomson Reuters Europe Healthcare (EU) 6%

Dow Jones U.S. Medical Equipment Index 22%

S&P Composite 1500 HealthCare Equipment & Supplies 17%

Indices

A tale of two Covids for device makers

A look at medtech stocks’ performance at the half-year point revealed a stark delineation

between those companies whose devices were of use in treating or diagnosing Covid-19 and

those whose businesses had suffered from the pandemic and its associated lockdowns.

Six months on and the picture is blurrier, though Covid-19 was still a huge influence on device makers. Overall, the

more established end of the sector is in a better position than it was in the summer, with the most successful big-cap

companies seeing their share prices more than double. Even greater gains were seen among smaller companies –

but so were greater losses.

Indices of medical device stocks point to the broader recoveries occurring across stock markets. They do not show

the sorts of gains medtech companies saw in pre-pandemic 2019, but the second half of 2020 allowed a palpable

improvement from the first.

Of all the big-cap companies, Teladoc saw its share price increase the most – indeed, it was not even in the big cap

cohort at the start of 2020. The various quarantine measures put in place starting from the spring of 2020 ensured

that demand soared for the remote health consultation services that Teladoc provides .

The acquisition of Livongo in August – at $18.5bn, last year’s largest medtech deal – prompted Teladoc’s stock to

fall slightly. But the group soon recovered as investors digested the possibilities of adding a company whose

business model signs up entire companies at a swoop. Livongo’s own share price had grown by 200% across the

first half of 2020.

Align Technology’s stock jumped 35% when its third-quarter earnings came in more than four times higher than

analysts had been expecting.

The Covid-19 angle here, Align’s chief executive Joseph Hogan explained, was the “Zoom effect”. People working

remotely, staring at their own image in videoconference software, took more notice of their dental imperfections

– and, because these white-collar workers had hung on to their jobs but spent less on holidays, commuting and

socialising, they had the cash to do something about it.

27 Copyright © 2021 Evaluate Ltd. All rights reserved.A tale of two Covids for device makers

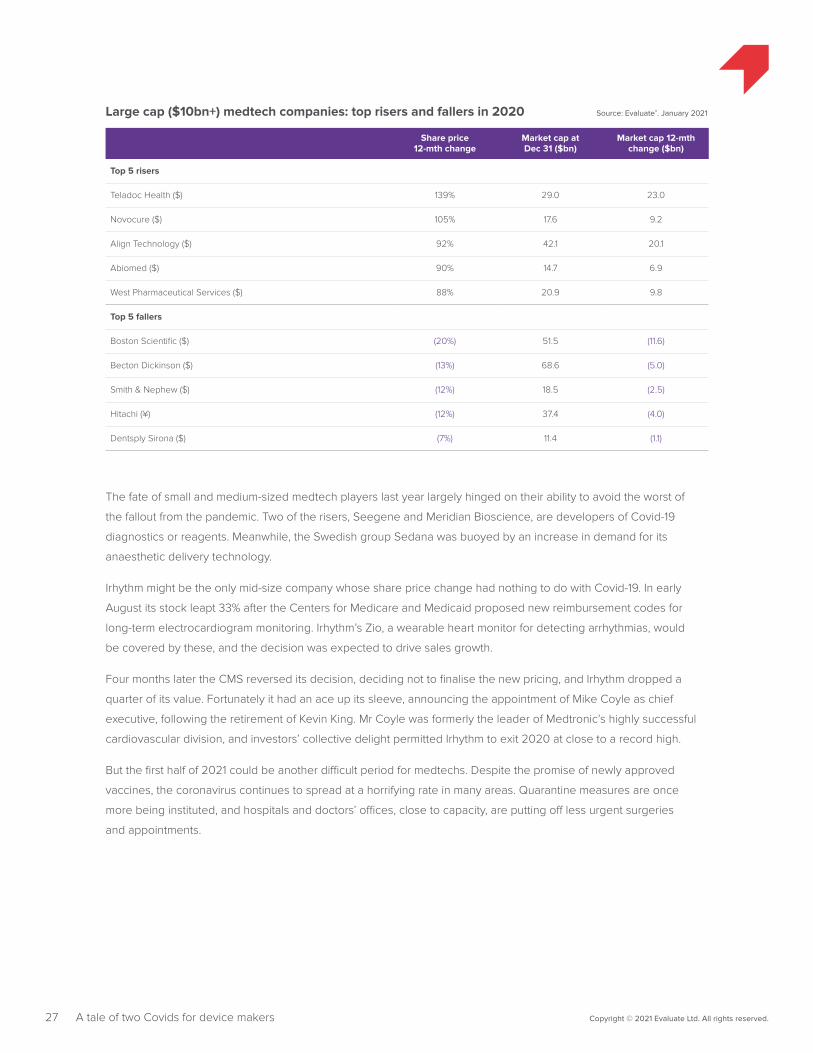

Share price 12-mth change

Market cap at Dec 31 ($bn)

Market cap 12-mth change ($bn)

Top 5 risers

Teladoc Health ($) 139% 29.0 23.0

Novocure ($) 105% 17.6 9.2

Align Technology ($) 92% 42.1 20.1

Abiomed ($) 90% 14.7 6.9

West Pharmaceutical Services ($) 88% 20.9 9.8

Top 5 fallers

Boston Scientific ($) (20%) 51.5 (11.6)

Becton Dickinson ($) (13%) 68.6 (5.0)

Smith & Nephew ($) (12%) 18.5 (2.5)

Hitachi (¥) (12%) 37.4 (4.0)

Dentsply Sirona ($) (7%) 11.4 (1.1)

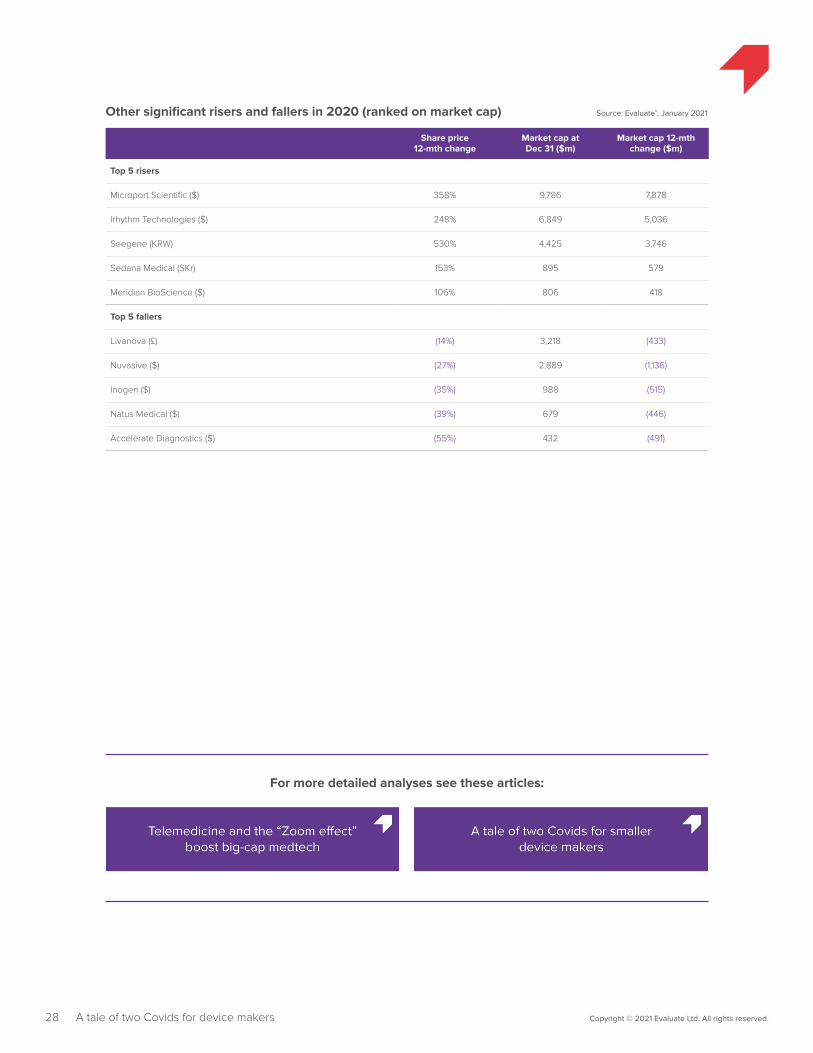

Large cap ($10bn+) medtech companies: top risers and fallers in 2020 Source: Evaluate®. January 2021

The fate of small and medium-sized medtech players last year largely hinged on their ability to avoid the worst of

the fallout from the pandemic. Two of the risers, Seegene and Meridian Bioscience, are developers of Covid-19

diagnostics or reagents. Meanwhile, the Swedish group Sedana was buoyed by an increase in demand for its

anaesthetic delivery technology.

Irhythm might be the only mid-size company whose share price change had nothing to do with Covid-19. In early

August its stock leapt 33% after the Centers for Medicare and Medicaid proposed new reimbursement codes for

long-term electrocardiogram monitoring. Irhythm’s Zio, a wearable heart monitor for detecting arrhythmias, would

be covered by these, and the decision was expected to drive sales growth.

Four months later the CMS reversed its decision, deciding not to finalise the new pricing, and Irhythm dropped a

quarter of its value. Fortunately it had an ace up its sleeve, announcing the appointment of Mike Coyle as chief

executive, following the retirement of Kevin King. Mr Coyle was formerly the leader of Medtronic’s highly successful

cardiovascular division, and investors’ collective delight permitted Irhythm to exit 2020 at close to a record high.

But the first half of 2021 could be another difficult period for medtechs. Despite the promise of newly approved

vaccines, the coronavirus continues to spread at a horrifying rate in many areas. Quarantine measures are once

more being instituted, and hospitals and doctors’ offices, close to capacity, are putting off less urgent surgeries

and appointments.

Share price 12-mth change

Market cap at Dec 31 ($m)

Market cap 12-mth change ($m)

Top 5 risers

Microport Scientific ($) 358% 9,786 7,878

Irhythm Technologies ($) 248% 6,849 5,036

Seegene (KRW) 530% 4,425 3,746

Sedana Medical (SKr) 153% 895 579

Meridian BioScience ($) 106% 806 418

Top 5 fallers

Livanova (£) (14%) 3,218 (433)

Nuvasive ($) (27%) 2,889 (1,136)

Inogen ($) (35%) 988 (515)

Natus Medical ($) (39%) 679 (446)

Accelerate Diagnostics ($) (55%) 432 (491)

Other significant risers and fallers in 2020 (ranked on market cap) Source: Evaluate®. January 2021

28 Copyright © 2021 Evaluate Ltd. All rights reserved.A tale of two Covids for device makers

For more detailed analyses see these articles:

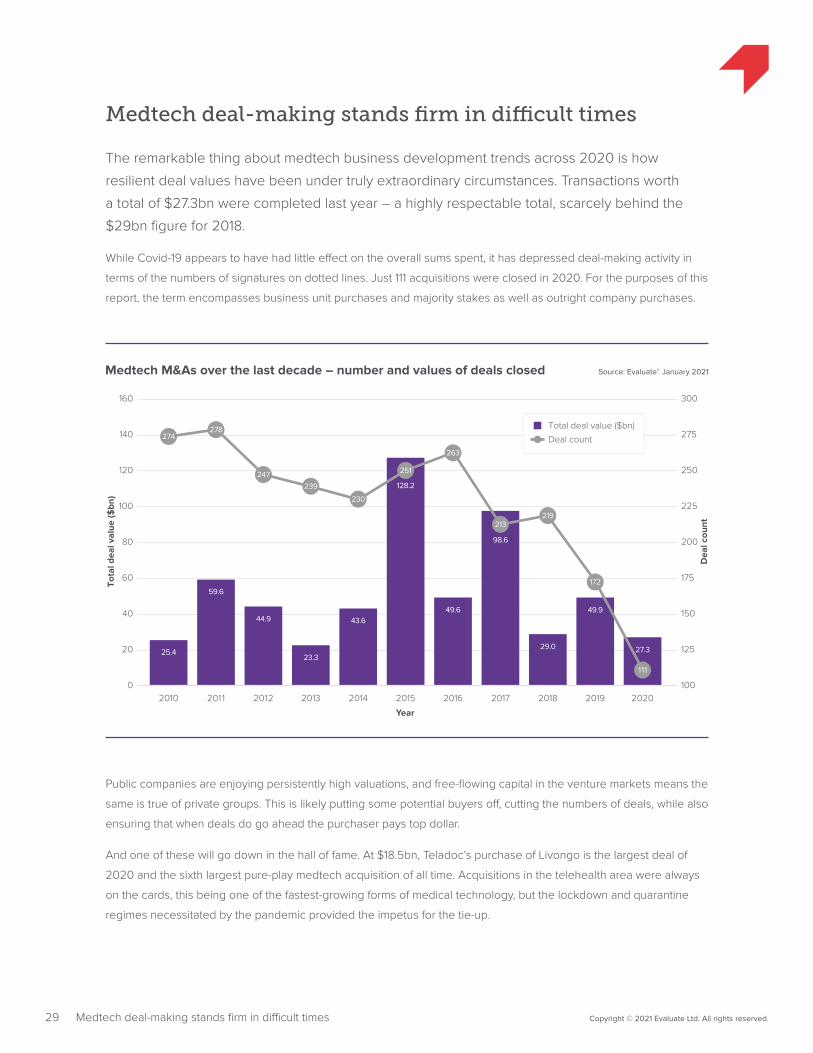

Source: Evaluate®. January 2021Medtech M&As over the last decade – number and values of deals closed

Tota

l dea

l val

ue ($

bn)

Dea

l cou

nt

20

40

60

80

120

100

140

160

275

300

175

200

225

250

150

125

100

Total deal value ($bn)

Deal count

Year

2010

25.4

2011

59.6

2012

44.9

2013

23.3

2014

43.6

2015

128.2

2016

49.6

2017

98.6

2019

49.9

2018

29.0

274278

247239

230

251

263

213

2020

27.3

219

0

111

172

29 Copyright © 2021 Evaluate Ltd. All rights reserved.Medtech deal-making stands firm in difficult times

Medtech deal-making stands firm in difficult times

The remarkable thing about medtech business development trends across 2020 is how

resilient deal values have been under truly extraordinary circumstances. Transactions worth

a total of $27.3bn were completed last year – a highly respectable total, scarcely behind the

$29bn figure for 2018.

While Covid-19 appears to have had little effect on the overall sums spent, it has depressed deal-making activity in

terms of the numbers of signatures on dotted lines. Just 111 acquisitions were closed in 2020. For the purposes of this

report, the term encompasses business unit purchases and majority stakes as well as outright company purchases.

Public companies are enjoying persistently high valuations, and free-flowing capital in the venture markets means the

same is true of private groups. This is likely putting some potential buyers off, cutting the numbers of deals, while also

ensuring that when deals do go ahead the purchaser pays top dollar.

And one of these will go down in the hall of fame. At $18.5bn, Teladoc’s purchase of Livongo is the largest deal of

2020 and the sixth largest pure-play medtech acquisition of all time. Acquisitions in the telehealth area were always

on the cards, this being one of the fastest-growing forms of medical technology, but the lockdown and quarantine

regimes necessitated by the pandemic provided the impetus for the tie-up.

Source: Evaluate®. January 2021Medtech M&As by size – number of deals closed over the last decadeN

umbe

r of

dea

ls

10

20

30

40

50

60

70

80

110

90

100

120

130

140

Year

2010

5

38

91

2011

11

46

77

2012

6

40

76

2013

4

35

66

2014

8

47

60

2015

18

32

70

2016

12

33

67

2017

19

31

51

2018

8

42

43

2019

13

31

42

2020

4

15

21

0

$0-100m

$100m-$1bn

$1bn+

30 Copyright © 2021 Evaluate Ltd. All rights reserved.Medtech deal-making stands firm in difficult times

Note: Only includes deals with known value.

The coming year ought to see a return to more M&A deal-making, should vaccine rollouts go as hoped. There will

certainly be appetite for deals: the groups negatively affected by hospitals prioritising Covid-19 patients, such as

those active in the orthopaedics and cardiology arenas, will be keen to catch up by buying high-growth businesses.

Completion date

Acquirer Target Value ($bn) M&A focus Evaluate Vantage coverage

Oct 30 Teladoc Health Livongo 18,500 Diabetic care, healthcare IT and patient monitoring

Teladoc bets $18.5bn that Covid-19 will change the world for good

Nov 11 Stryker Wright Medical Group 5,400 Orthopaedics Wright and Stryker embark on a joints venture

Oct 2 Invitae Archer DX 1,400 In vitro diagnostics Invitae ends medtech merger drought with ArcherDX deal

Dec 31 Dentsply Sirona Byte 1,040 Dental Dentsply sees clear advantages to $1bn Byte deal

Nov 18 Steris Key Surgical 850 General hospital & healthcare supply

Steris turns the Key on 2020’s fifth biggest buy

Top 5 deals closed in 2020 Source: Evaluate®. January 2021

31 Copyright © 2021 Evaluate Ltd. All rights reserved.Medtechs rake in the venture cash

For a more detailed analysis see this article:

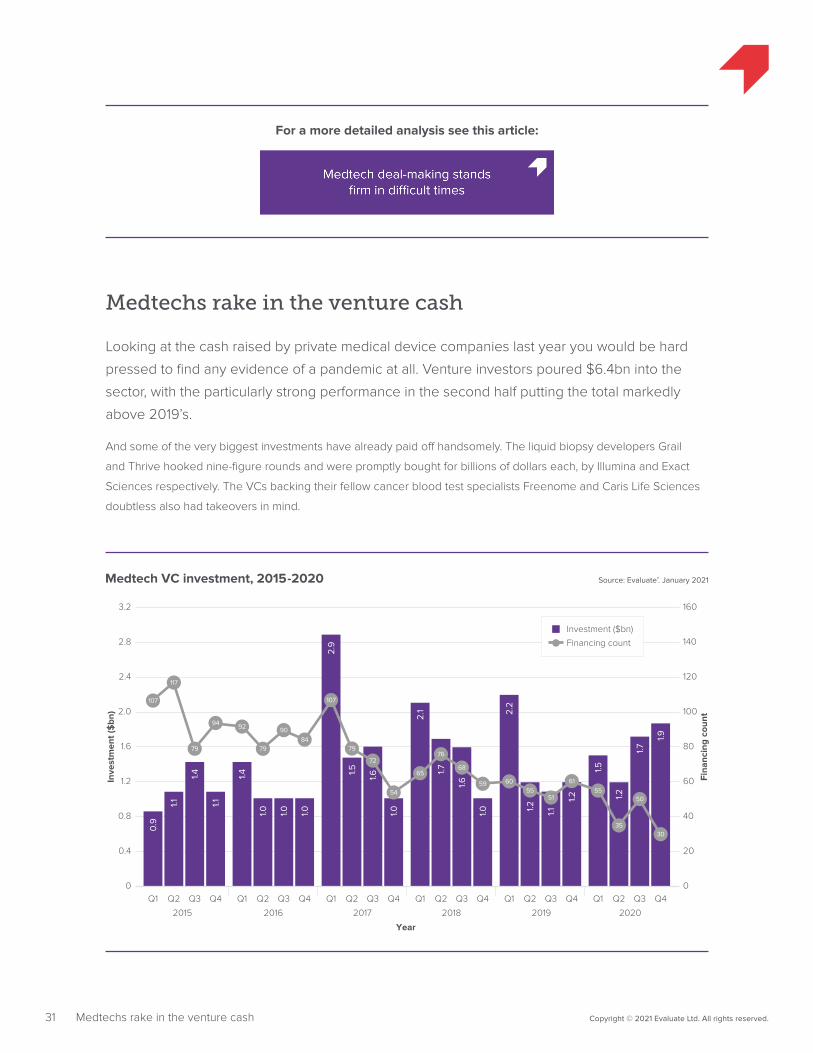

Medtechs rake in the venture cash

Looking at the cash raised by private medical device companies last year you would be hard

pressed to find any evidence of a pandemic at all. Venture investors poured $6.4bn into the

sector, with the particularly strong performance in the second half putting the total markedly

above 2019’s.

And some of the very biggest investments have already paid off handsomely. The liquid biopsy developers Grail

and Thrive hooked nine-figure rounds and were promptly bought for billions of dollars each, by Illumina and Exact

Sciences respectively. The VCs backing their fellow cancer blood test specialists Freenome and Caris Life Sciences

doubtless also had takeovers in mind.

Source: Evaluate®. January 2021Medtech VC investment, 2015-2020

Inve

stm

ent (

$bn

)

Fina

ncin

g co

unt

2.4

2.0

1.6

1.2

0.8

0.4

2.8

3.2

Investment ($bn)

Financing count

Year

2015

Q1

0.9

Q2

1.1

Q3 Q4

2016

Q1

1.4

Q2 Q3

1.0

Q4

1.0

2017

Q1

2.9

Q2

1.5

Q3

1.6

Q4

2018

Q1

2.1

Q2

1.7

Q3 Q4

2019 2020

Q1 Q2 Q3 Q4

1.1

1.2

1.2

2.2

Q1 Q2 Q3 Q4

1.7

1.9

1.2

1.5

1.0

1.6

1.0

1.4

1.0

1.1

120

100

80

60

40

20

140

160

0

117

79

94 92

79

9084

107

79

72

54

65

76

68

59 6055

51

107

55

35

61

30

50

0

32 Copyright © 2021 Evaluate Ltd. All rights reserved.Medtechs rake in the venture cash

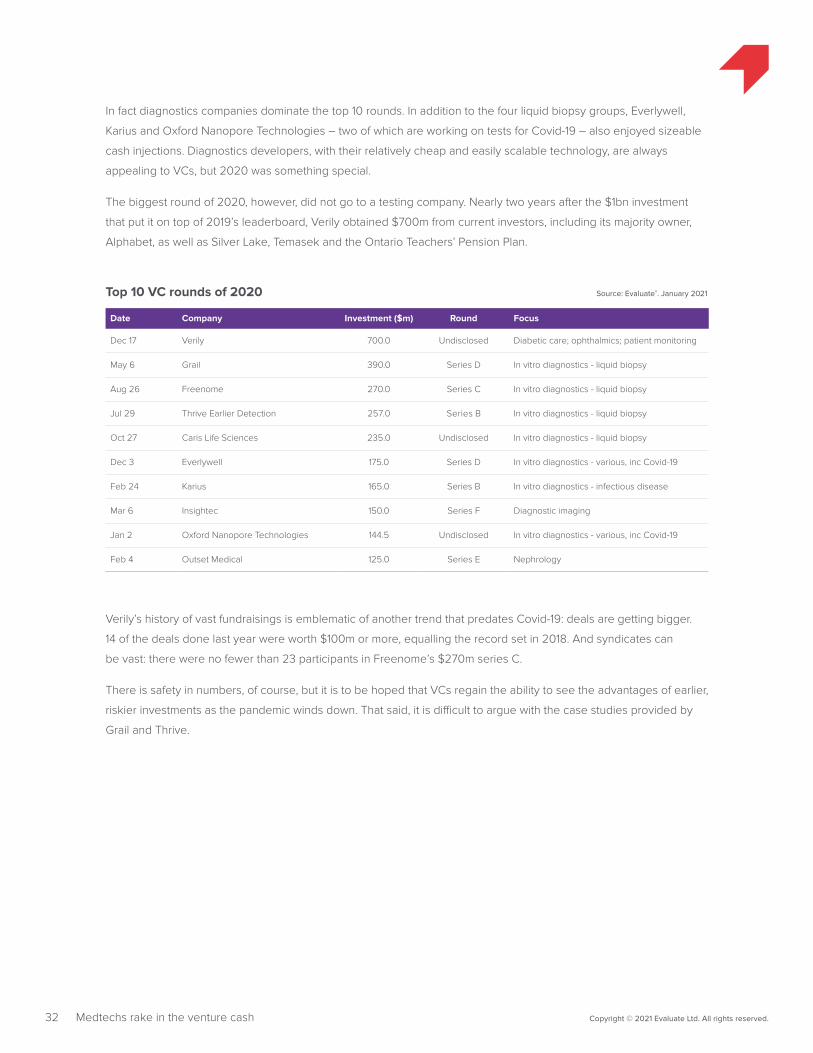

In fact diagnostics companies dominate the top 10 rounds. In addition to the four liquid biopsy groups, Everlywell,

Karius and Oxford Nanopore Technologies – two of which are working on tests for Covid-19 – also enjoyed sizeable

cash injections. Diagnostics developers, with their relatively cheap and easily scalable technology, are always

appealing to VCs, but 2020 was something special.

The biggest round of 2020, however, did not go to a testing company. Nearly two years after the $1bn investment

that put it on top of 2019’s leaderboard, Verily obtained $700m from current investors, including its majority owner,

Alphabet, as well as Silver Lake, Temasek and the Ontario Teachers’ Pension Plan.

Date Company Investment ($m) Round Focus

Dec 17 Verily 700.0 Undisclosed Diabetic care; ophthalmics; patient monitoring

May 6 Grail 390.0 Series D In vitro diagnostics - liquid biopsy

Aug 26 Freenome 270.0 Series C In vitro diagnostics - liquid biopsy

Jul 29 Thrive Earlier Detection 257.0 Series B In vitro diagnostics - liquid biopsy

Oct 27 Caris Life Sciences 235.0 Undisclosed In vitro diagnostics - liquid biopsy

Dec 3 Everlywell 175.0 Series D In vitro diagnostics - various, inc Covid-19

Feb 24 Karius 165.0 Series B In vitro diagnostics - infectious disease

Mar 6 Insightec 150.0 Series F Diagnostic imaging

Jan 2 Oxford Nanopore Technologies 144.5 Undisclosed In vitro diagnostics - various, inc Covid-19

Feb 4 Outset Medical 125.0 Series E Nephrology

Top 10 VC rounds of 2020 Source: Evaluate®. January 2021

Verily’s history of vast fundraisings is emblematic of another trend that predates Covid-19: deals are getting bigger.

14 of the deals done last year were worth $100m or more, equalling the record set in 2018. And syndicates can

be vast: there were no fewer than 23 participants in Freenome’s $270m series C.

There is safety in numbers, of course, but it is to be hoped that VCs regain the ability to see the advantages of earlier,

riskier investments as the pandemic winds down. That said, it is difficult to argue with the case studies provided by

Grail and Thrive.

33 Copyright © 2021 Evaluate Ltd. All rights reserved.Medtechs rake in the venture cash

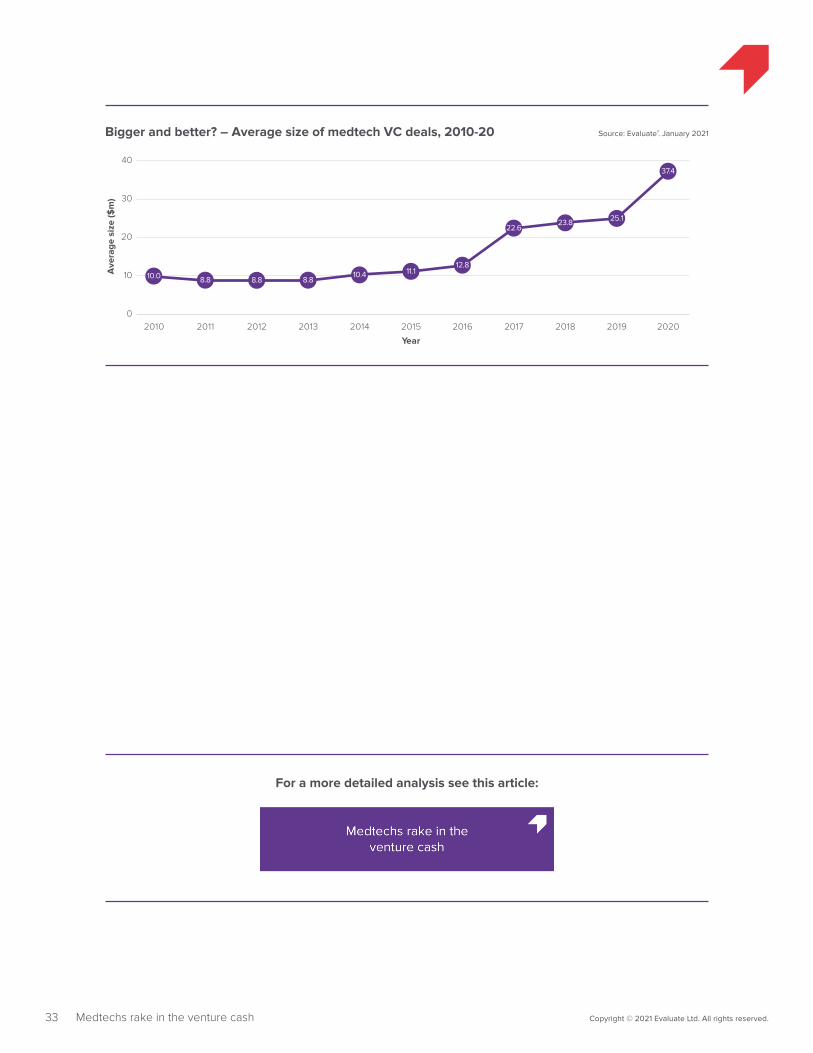

10

20

30

0

Source: Evaluate®. January 2021Bigger and better? – Average size of medtech VC deals, 2010-20

Ave

rage

siz

e ($

m)

40

Year

2010

10.0

2011

8.8

2012

8.8

2013

8.8

2014

10.4

2015

11.1

2016

12.8

2017

22.6

2018

23.8

2019 2020

37.4

25.1

For a more detailed analysis see this article:

34 Copyright © 2021 Evaluate Ltd. All rights reserved.Astounding success greets newly public device makers

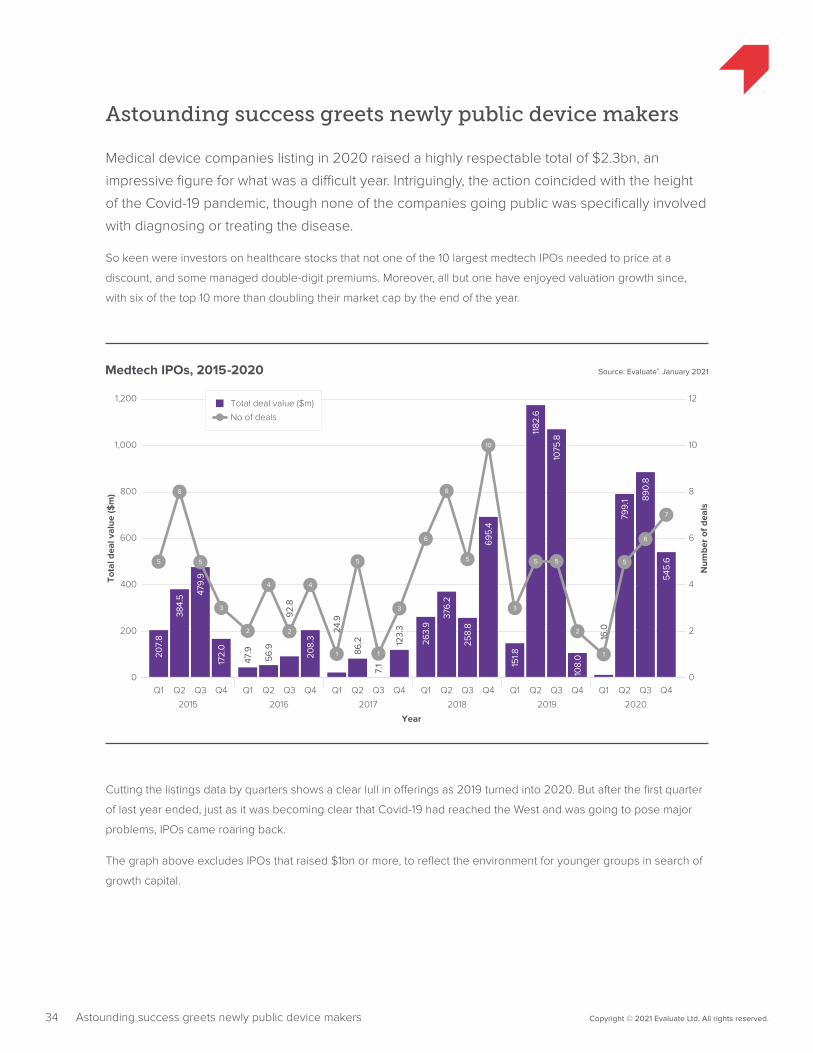

Astounding success greets newly public device makers

Medical device companies listing in 2020 raised a highly respectable total of $2.3bn, an

impressive figure for what was a difficult year. Intriguingly, the action coincided with the height

of the Covid-19 pandemic, though none of the companies going public was specifically involved

with diagnosing or treating the disease.

So keen were investors on healthcare stocks that not one of the 10 largest medtech IPOs needed to price at a

discount, and some managed double-digit premiums. Moreover, all but one have enjoyed valuation growth since,

with six of the top 10 more than doubling their market cap by the end of the year.

Source: Evaluate®. January 2021Medtech IPOs, 2015-2020

Tota

l dea

l val

ue ($

m)

Num

ber

of d

eals

1,000

800

600

400

200

1,200 Total deal value ($m)

No of deals

Year

2015

Q1

207.

8

Q2

384.

5

Q3 Q4

2016

Q1

47.9

Q2 Q3

92.8

Q4

208.

3

2017

Q1

24.9

Q2

86.2

Q3

7.1

Q4

2018

Q1

263.

9

Q2

376.

2

Q3 Q4

2019 2020

Q1 Q2 Q3 Q4

1075

.8

108.

0

1182

.6

151.8

Q1 Q2 Q3 Q4

890.

8

545.

6

799.

1

695.

4

258.

8

123.

3

479.

9

56.9

172.

0

10

8

6

4

2

12

0

8

5

3

2

4

2

4

1

5

1

3

6

8

5

10

3

5 55

1

5

2

7

6

0

16.0

Cutting the listings data by quarters shows a clear lull in offerings as 2019 turned into 2020. But after the first quarter

of last year ended, just as it was becoming clear that Covid-19 had reached the West and was going to pose major

problems, IPOs came roaring back.

The graph above excludes IPOs that raised $1bn or more, to reflect the environment for younger groups in search of

growth capital.

35 Copyright © 2021 Evaluate Ltd. All rights reserved.Astounding success greets newly public device makers

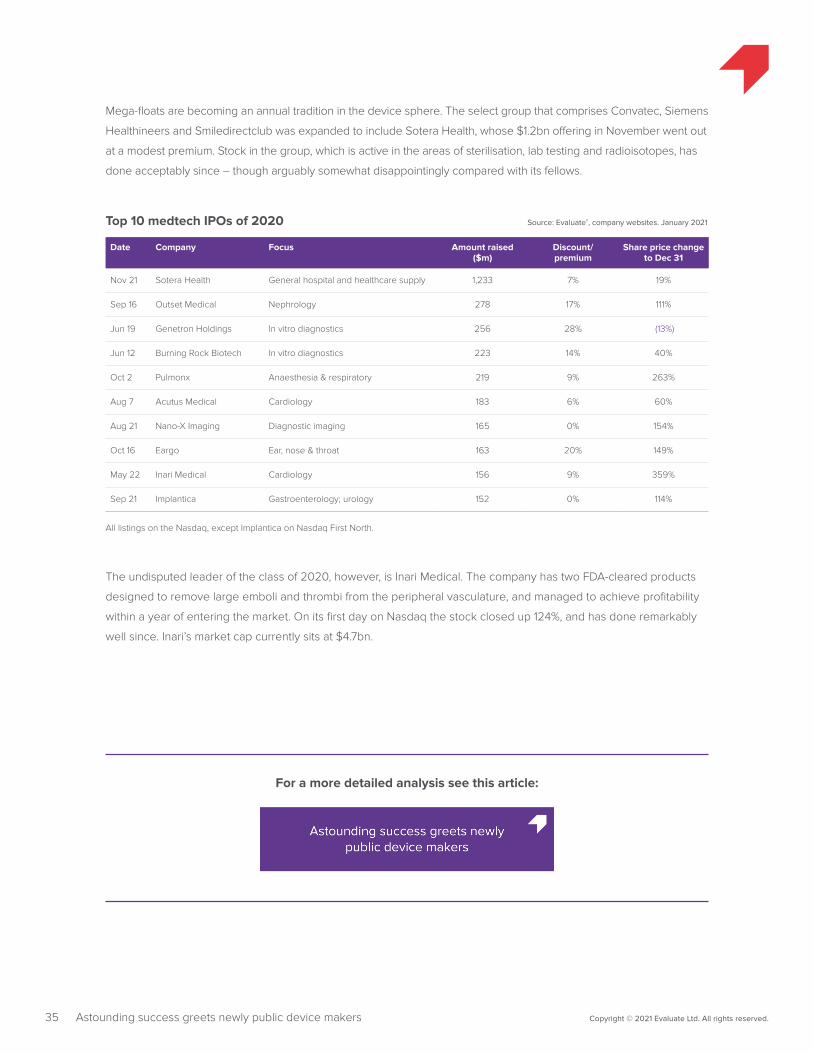

Mega-floats are becoming an annual tradition in the device sphere. The select group that comprises Convatec, Siemens

Healthineers and Smiledirectclub was expanded to include Sotera Health, whose $1.2bn offering in November went out

at a modest premium. Stock in the group, which is active in the areas of sterilisation, lab testing and radioisotopes, has

done acceptably since – though arguably somewhat disappointingly compared with its fellows.

Date Company Focus Amount raised ($m)

Discount/ premium

Share price change to Dec 31

Nov 21 Sotera Health General hospital and healthcare supply 1,233 7% 19%

Sep 16 Outset Medical Nephrology 278 17% 111%

Jun 19 Genetron Holdings In vitro diagnostics 256 28% (13%)

Jun 12 Burning Rock Biotech In vitro diagnostics 223 14% 40%

Oct 2 Pulmonx Anaesthesia & respiratory 219 9% 263%

Aug 7 Acutus Medical Cardiology 183 6% 60%

Aug 21 Nano-X Imaging Diagnostic imaging 165 0% 154%

Oct 16 Eargo Ear, nose & throat 163 20% 149%

May 22 Inari Medical Cardiology 156 9% 359%

Sep 21 Implantica Gastroenterology; urology 152 0% 114%

Top 10 medtech IPOs of 2020 Source: Evaluate®, company websites. January 2021

All listings on the Nasdaq, except Implantica on Nasdaq First North.

The undisputed leader of the class of 2020, however, is Inari Medical. The company has two FDA-cleared products

designed to remove large emboli and thrombi from the peripheral vasculature, and managed to achieve profitability

within a year of entering the market. On its first day on Nasdaq the stock closed up 124%, and has done remarkably

well since. Inari’s market cap currently sits at $4.7bn.

For a more detailed analysis see this article:

36 Copyright © 2021 Evaluate Ltd. All rights reserved.Focus on Covid-19 does not distract the FDA

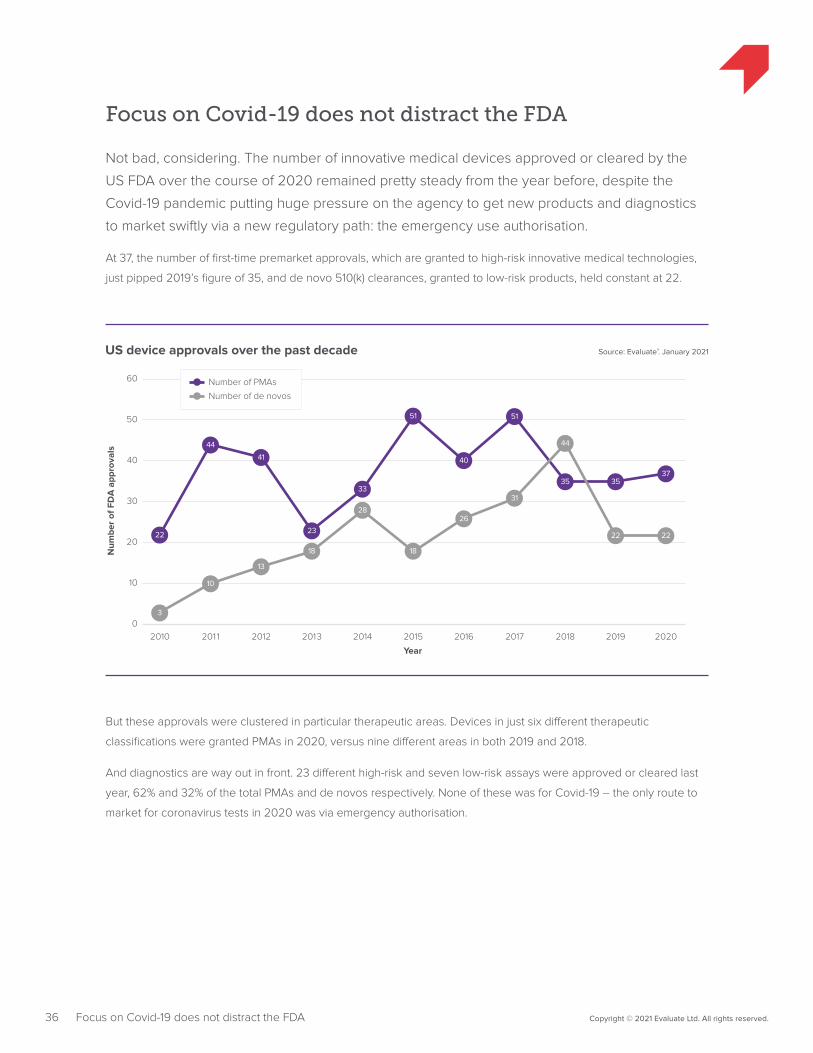

Focus on Covid-19 does not distract the FDA

Not bad, considering. The number of innovative medical devices approved or cleared by the

US FDA over the course of 2020 remained pretty steady from the year before, despite the

Covid-19 pandemic putting huge pressure on the agency to get new products and diagnostics

to market swiftly via a new regulatory path: the emergency use authorisation.

At 37, the number of first-time premarket approvals, which are granted to high-risk innovative medical technologies,

just pipped 2019’s figure of 35, and de novo 510(k) clearances, granted to low-risk products, held constant at 22.

Source: Evaluate®. January 2021US device approvals over the past decade

Num

ber

of F

DA

app

rova

ls

10

20

30

40

50

60

0

Year

Number of de novos

Number of PMAs

2010 2011 2012

3

22

10

44

13

41

2013

18

23

2014

28

33

2015

18

51

2016

26

40

2017

31

51

2019

22

35

2020

22

37

2018

44

35

But these approvals were clustered in particular therapeutic areas. Devices in just six different therapeutic

classifications were granted PMAs in 2020, versus nine different areas in both 2019 and 2018.

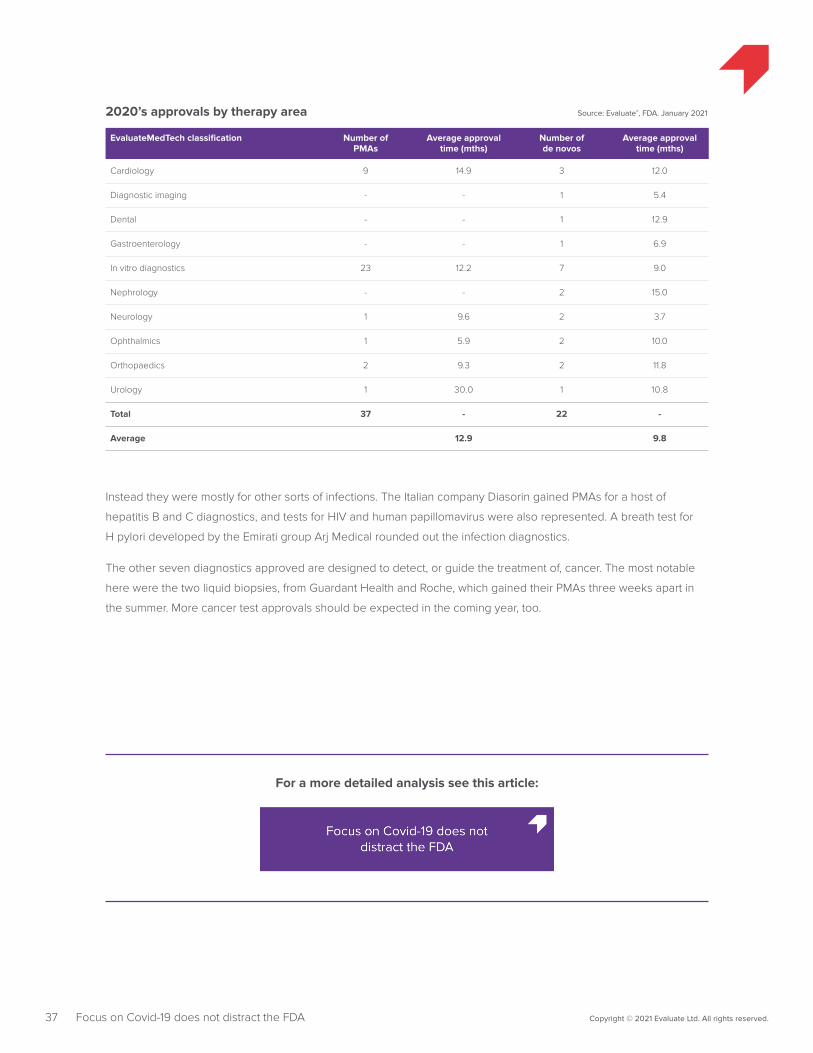

And diagnostics are way out in front. 23 different high-risk and seven low-risk assays were approved or cleared last

year, 62% and 32% of the total PMAs and de novos respectively. None of these was for Covid-19 – the only route to

market for coronavirus tests in 2020 was via emergency authorisation.

37 Copyright © 2021 Evaluate Ltd. All rights reserved.Focus on Covid-19 does not distract the FDA

EvaluateMedTech classification Number of PMAs

Average approval time (mths)

Number of de novos

Average approval time (mths)

Cardiology 9 14.9 3 12.0

Diagnostic imaging - - 1 5.4

Dental - - 1 12.9

Gastroenterology - - 1 6.9

In vitro diagnostics 23 12.2 7 9.0

Nephrology - - 2 15.0

Neurology 1 9.6 2 3.7

Ophthalmics 1 5.9 2 10.0

Orthopaedics 2 9.3 2 11.8

Urology 1 30.0 1 10.8

Total 37 - 22 -

Average 12.9 9.8

2020’s approvals by therapy area Source: Evaluate®, FDA. January 2021

Instead they were mostly for other sorts of infections. The Italian company Diasorin gained PMAs for a host of

hepatitis B and C diagnostics, and tests for HIV and human papillomavirus were also represented. A breath test for

H pylori developed by the Emirati group Arj Medical rounded out the infection diagnostics.

The other seven diagnostics approved are designed to detect, or guide the treatment of, cancer. The most notable

here were the two liquid biopsies, from Guardant Health and Roche, which gained their PMAs three weeks apart in

the summer. More cancer test approvals should be expected in the coming year, too.

For a more detailed analysis see this article:

Additional complimentary copies of this report can be downloaded at: www.evaluate.com/2020Review

Daily analysis of key industry developments, underpinned by Evaluate’s commercial intelligence.

We don’t just tell you what’s happened – we tell you what it means for you.

Evaluate provides trusted commercial intelligence for the pharmaceutical industry. We help our clients to refine and transform their understanding of the past, present and future of the global pharmaceutical market to drive better decisions. When you partner with Evaluate, our constantly expanding solutions and our transparent methodologies and datasets are instantly at your disposal, along with personalized, expert support.

Evaluate gives you the time and confidence to turn understanding into insight, and insight into action.

provides a complete, dynamic view of development risk and commercial return across the full clinical lifecycle, delivering game-changing insight into pharma asset potential.

offers a global view of the pharmaceutical market’s past, present and future performance with consensus forecasts to 2026, company financials, pipelines and deals.

tracks, benchmarks, and forecasts global performance for the medical device and diagnostic industry with consensus forecasts to 2026, company financials and more.

improves your strategic decision-making with customized solutions and deep insights that draw on our industry expertise and trusted commercial intelligence.

provides award-winning, thought-provoking news and insights into current and future developments in the industry, and is the only pharmaceutical news service underpinned by Evaluate’s commercial intelligence.

FEB 2021

Evaluate Headquarters Evaluate Ltd. 11-29 Fashion Street London E1 6PX United Kingdom

T +44 (0)20 7377 0800

Evaluate Americas EvaluatePharma USA Inc. 60 State Street, Suite 1910 Boston, MA 02109 USA

T +1 617 573 9450

Evaluate Asia Pacific Evaluate Japan KK Holland Hills Mori Tower 2F 5-11-2 Toranomon, Minato-ku Tokyo 105-0001, Japan

T +81 (0)80 1 164 4754

www.evaluate.com | @EvaluatePharma @EvaluateVantage