Perfect Storm for Commodities05 December 2013

War Room

HiddenLevers War Room

Open Q + A

Macro Coaching

Archived webinars

CE Credit

Idea Generation

Presentation deck

Product UpdatesScenario Updates

I. Market Update

II. Perfect Storm for Commodities

III. Scenarios

IV. Winners + Losers

War Room

HiddenLevers

MARKET UPDATE

Market Update

QE Taper Tantrums

Q3 US GDP = 3.6%Iran Détente

Nasdaq 4k

Macro Snapshot

Employment, manufacturing, equities, and bond spreads trending in the right direction – why won’t CPI get with the program?

PERFECT STORM FOR COMMODITIESHiddenLevers

Commodities Past

Real commodities prices flat since 1870’s – 0% real growth

Commodities markets appear highly cyclical over 200 years, and we look to be at a top

source: Business Insider

Commodities Present: Oil & Energy

sources: EIA, DOT

US oil production has recovered rapidly, while total vehicle miles are well below 2007 peak.

But global demand and risk premium have kept oil up 4.6% YTD.

Supply is up… And demand is flat.

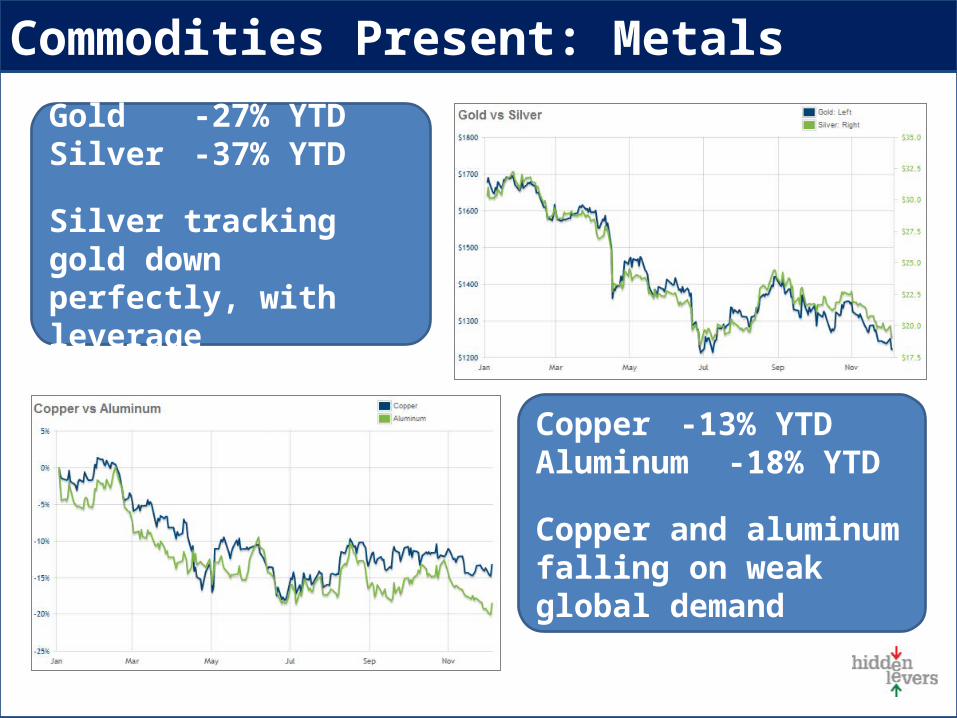

Commodities Present: Metals

Gold -27% YTD Silver -37% YTD

Silver tracking gold down perfectly, with leverage

Copper -13% YTD Aluminum -18% YTD

Copper and aluminum falling on weak global demand

Commodities Present: Agriculture

source: HiddenLevers, UN, Financial Times

-16% YTD-27% since July 2012

Long term trend

Agriculture commodities down since mid 1990s

Double digit declines in 2014 + 2015 expected

triple topReasons for continuing drop

- Favorable weather- Falling input costs- Larger harvests- Bumper crop in corn

Commodities Future: Deflation?

CPI has generallyfollowedS&P 500 –divergencestarted mid-2012

US CPI had a lagged correlation with S&P 500 until breakdown in mid-2012, despite Fed efforts. Are commodities and CPI predicting deflation?

precious metals out of favor Food prices deflating into 2015

US oil demand declining

Perfect Storm for Commodities – Recap

Top of Commodities Super Cycle

HiddenLevers

COMMODITIES DEFLATION – SCENARIOS

Scenario: Commodities bounce back

EM/BRICS recovery is key

Signals rising world wide

inflation

source: HiddenLevers

Equities now a leading indicator economy

USD weakness helps spur

commodities

Will this trend pick up?

Scenario: Equities decoupling continues

US economy pickup doesn’t increase

commodity demand

QE continuing means decoupling story in

tact

source: HiddenLevers

QE meltup + deflation in other risk assets

Tech growth in US is not like manufacturing

growth in EM

Decoupling is the current dynamic

1996-1999

S&P + 125%

Oil - 55%

Copper - 55%

Scenario: Equities follow Commodities down

Industrial metals and S&P have long

history

source: HiddenLevers

Deflation spiral on all risk assets

Fed taper will kick this off

2008 Crisis

S&P - 52%

Oil - 76%

Copper - 64%

GoodCommodities Bounce Back

BadDecoupling

continues

UglyEquities

follow Commodities

Scenarios: Perfect Storm for Commodities

EM recovery would lead to rising inflation and a commodities bounce.

Commodities could decouple from equities if tech-led growth continues

Fed has failed to raise CPI – could be prelude to stronger deflation, with commodities and equities down together

HiddenLevers

WINNERS + LOSERS

Winners – Middlemen

Food Makers Car Makers Utilities

Oil Refiners Plane Makers

Winners – Lower input costs

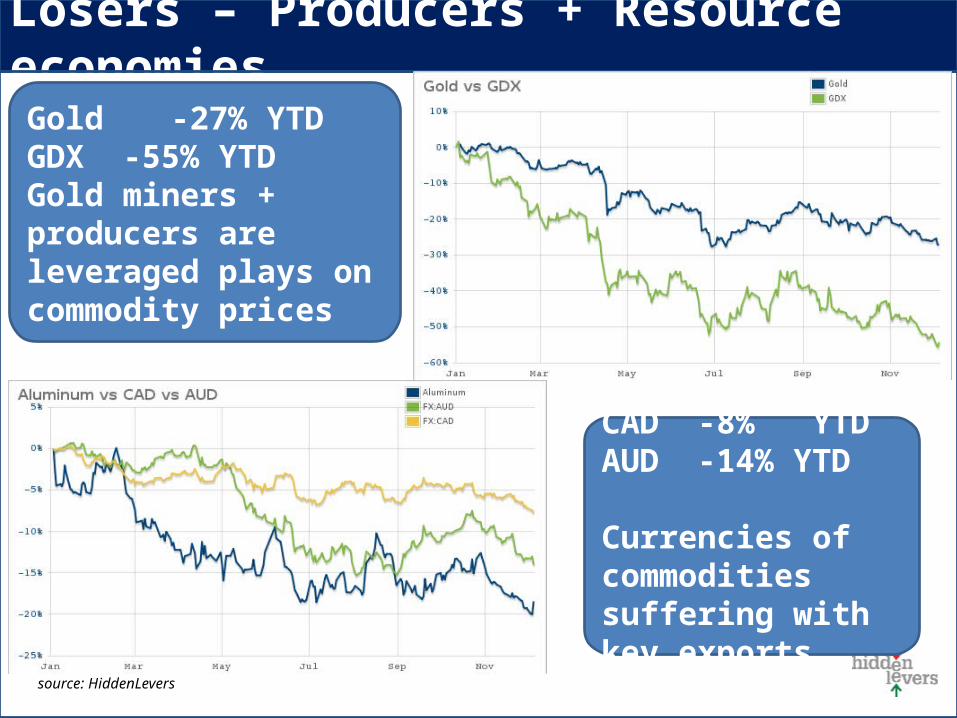

Losers – Producers + Resource economies

source: HiddenLevers

Gold -27% YTDGDX -55% YTDGold miners + producers are leveraged plays on commodity prices

CAD -8% YTD AUD -14% YTD

Currencies of commodities suffering with key exports

Find it on HiddenLevers

Scenario Library

Risk Profiles for

securities

Macro Themes

Economic Data

Center

source: Burtynski

War RoomGold Crash

Commodities

Industry groupings

War RoomBRICS

• Scenario email alerts

• Scenario progress visualization

• Mobile site improvements

Coming soon:

- Dashboard page

- Product development survey

Product Update