From Segments to Fragments Conflicting economic signals and their

implications for marketers

Presentation to CIM Spring Conference

Paul Flatters

The forces of fragmentation

ME

Presentation content

• Economic context: Multi-speed and polarised

• Demographic context: The peril of stereotypes

• Cultural context: The New Morality, mobile

connectivity and local activism

ECONOMIC CONTEXT: MULTI-

SPEED AND POLARISED

Living through economic history

-9.0%

-8.0%

-7.0%

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26

Total GDP, quarterly change after pre-recession peak

80s recession

90s recession

Great Depression

Current downturn

Source: ONS/Trajectory

Three narratives for the UK economy

“Boom time Britain”

Automotive industry

raises 2013 new car

forecast as July posts

17th consecutive

monthly rise

UK jobless claimant

count plunges,

unemployment

steady

“Cost of living crisis” “Austerity Britain”

Budget cuts could

make councils 'go

bust' says senior

councillor

2.8 3.0 2.6

-0.3

-4.3

1.9

1.6

0.7

2.6 2.6 2.8 2.7 2.7 2.4 2.3 2.4

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

UK GDP growth, % year on year

Real

Forecast

Source: Oxford Economics 2014

Recovery underway and

set to continue

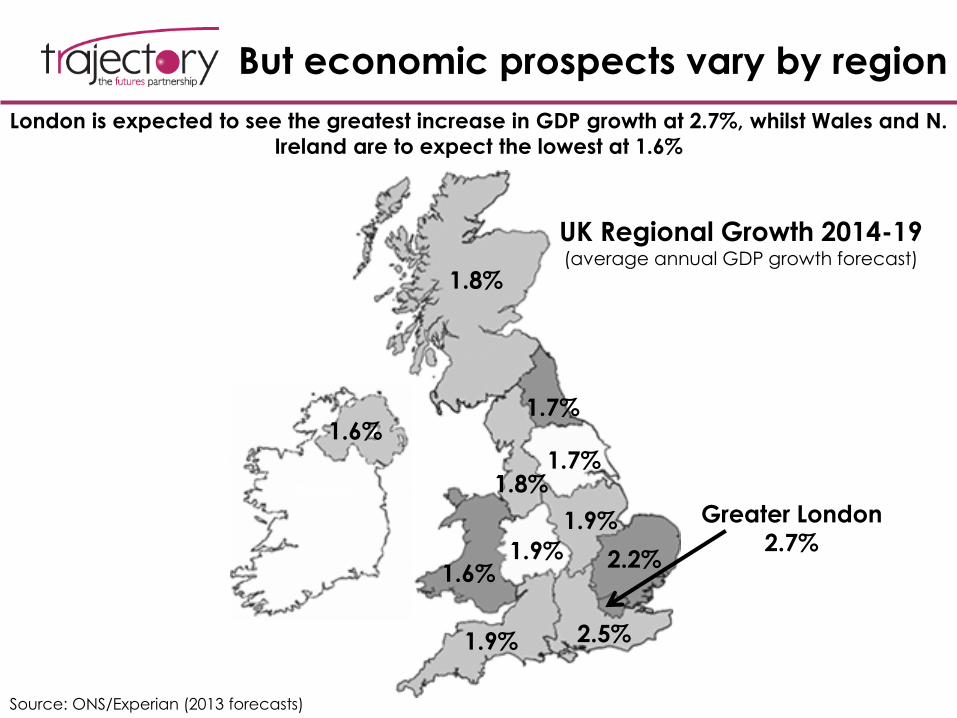

But economic prospects vary by region

Greater London

2.7%

1.8%

1.6%

1.6%

1.7%

1.8% 1.7%

1.9%

1.9%

2.2%

1.9% 2.5%

UK Regional Growth 2014-19 (average annual GDP growth forecast)

Source: ONS/Experian (2013 forecasts)

London is expected to see the greatest increase in GDP growth at 2.7%, whilst Wales and N.

Ireland are to expect the lowest at 1.6%

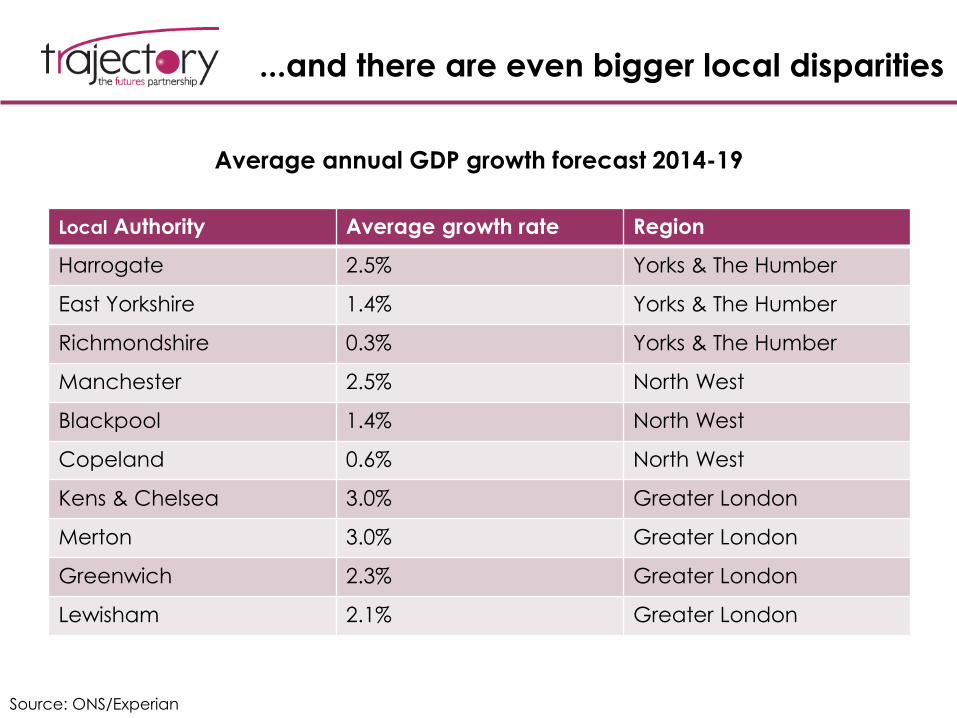

...and there are even bigger local disparities

Local Authority Average growth rate Region

Harrogate 2.5% Yorks & The Humber

East Yorkshire 1.4% Yorks & The Humber

Richmondshire 0.3% Yorks & The Humber

Manchester 2.5% North West

Blackpool 1.4% North West

Copeland 0.6% North West

Kens & Chelsea 3.0% Greater London

Merton 3.0% Greater London

Greenwich 2.3% Greater London

Lewisham 2.1% Greater London

Average annual GDP growth forecast 2014-19

Source: ONS/Experian

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

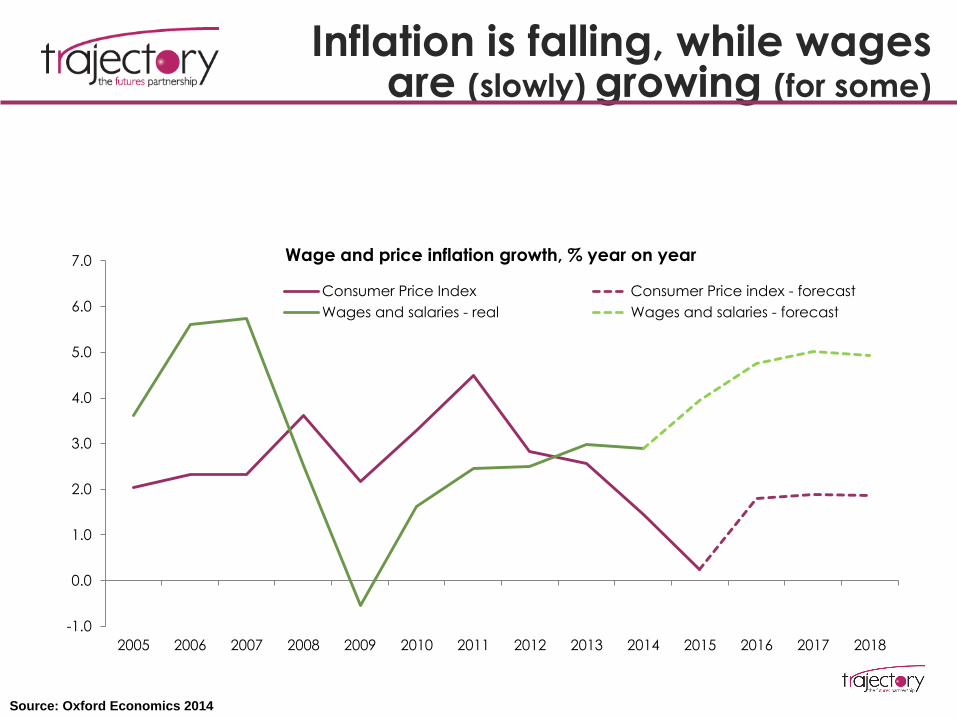

Wage and price inflation growth, % year on year

Consumer Price Index Consumer Price index - forecast

Wages and salaries - real Wages and salaries - forecast

Inflation is falling, while wages are (slowly) growing (for some)

Source: Oxford Economics 2014

Wages will not recover fully until 2017

(at the earliest)

60%

70%

80%

90%

100%

110%

120%

130%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Average wages (2007=100)

Source: Oxford Economics 2014

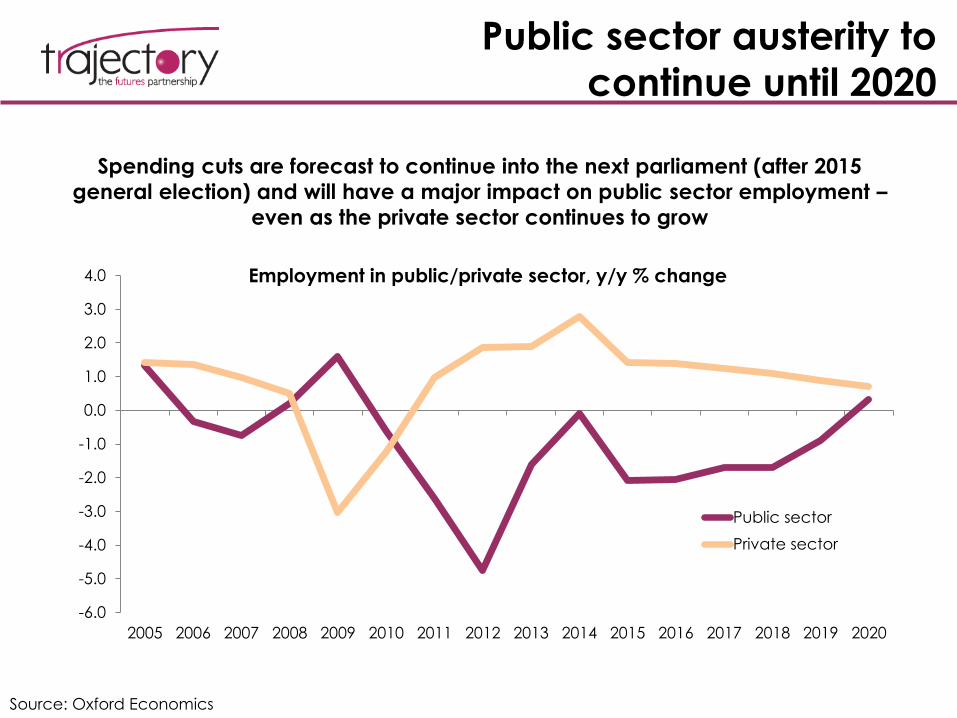

Public sector austerity to

continue until 2020

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Employment in public/private sector, y/y % change

Public sector

Private sector

Spending cuts are forecast to continue into the next parliament (after 2015

general election) and will have a major impact on public sector employment –

even as the private sector continues to grow

Source: Oxford Economics

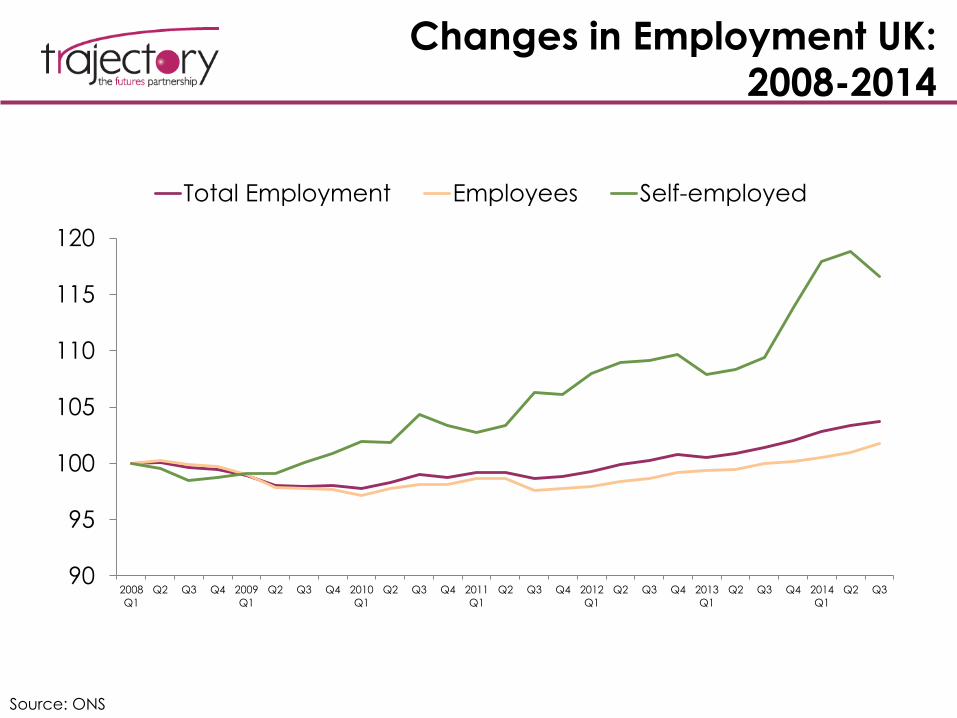

Changes in Employment UK:

2008-2014

90

95

100

105

110

115

120

2008

Q1

Q2 Q3 Q4 2009

Q1

Q2 Q3 Q4 2010

Q1

Q2 Q3 Q4 2011

Q1

Q2 Q3 Q4 2012

Q1

Q2 Q3 Q4 2013

Q1

Q2 Q3 Q4 2014

Q1

Q2 Q3

Total Employment Employees Self-employed

Source: ONS

The labour market in 2015: Fragility

Skills deficit & the ‘hour glass’

economy

58% 57%

54%

50% 49%

44%

46%

48%

50%

52%

54%

56%

58%

60%

Skills gaps caused by lack of each skill

Skills Commission 2013

DEMOGRAPHIC CONTEXT

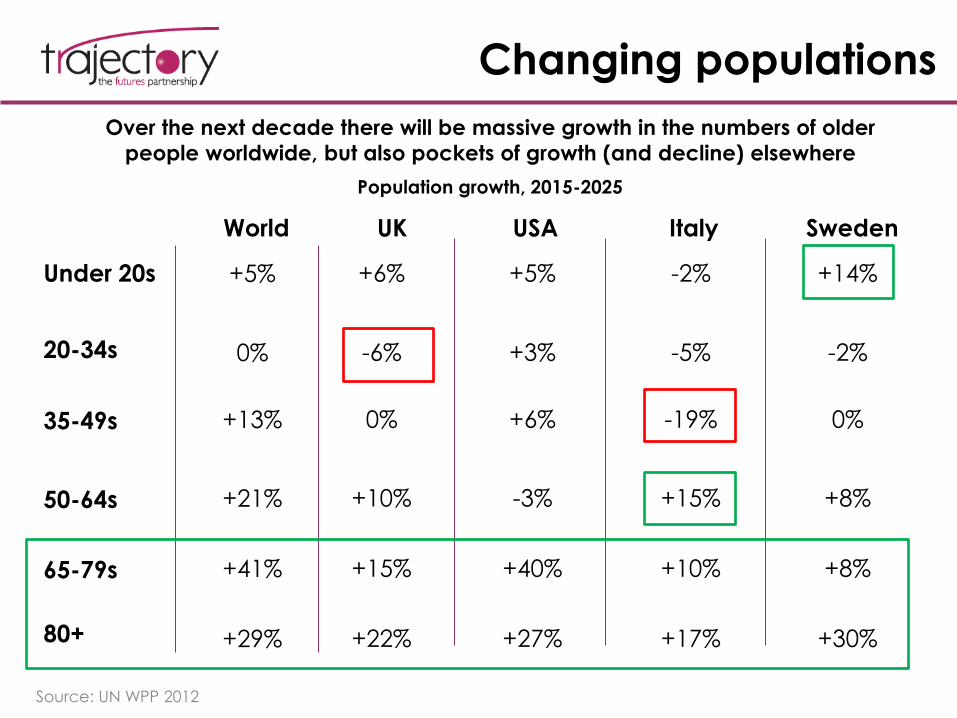

Changing populations

Over the next decade there will be massive growth in the numbers of older

people worldwide, but also pockets of growth (and decline) elsewhere

65-79s +41%

80+ +29%

Under 20s +5%

20-34s 0%

35-49s +13%

50-64s +21%

+15%

+22%

+6%

-6%

0%

+10%

+40%

+27%

+5%

+3%

+6%

-3%

+10%

+17%

-2%

-5%

-19%

+15%

+8%

+30%

+14%

-2%

0%

+8%

World UK USA Italy Sweden

Population growth, 2015-2025

Source: UN WPP 2012

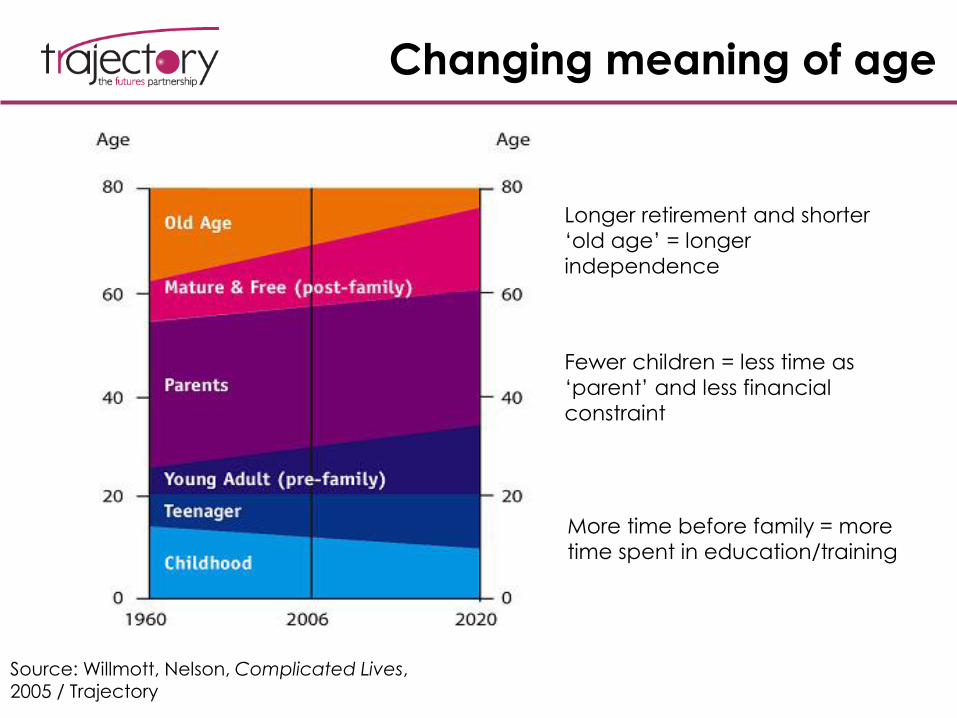

Changing meaning of age

Source: Willmott, Nelson, Complicated Lives, 2005 / Trajectory

More time before family = more

time spent in education/training

Fewer children = less time as

‘parent’ and less financial

constraint

Longer retirement and shorter

‘old age’ = longer

independence

UK population by

generational group

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

20

13

20

16

20

19

20

22

20

25

Gen Extra

Gen Y

Gen X

Baby Boomer

Pre War

Pre War

Baby Boomer

Gen X

Gen Y

% of UK adult (18+) population in each generational grouping, 1971–2020

Source: ONS/Trajectory

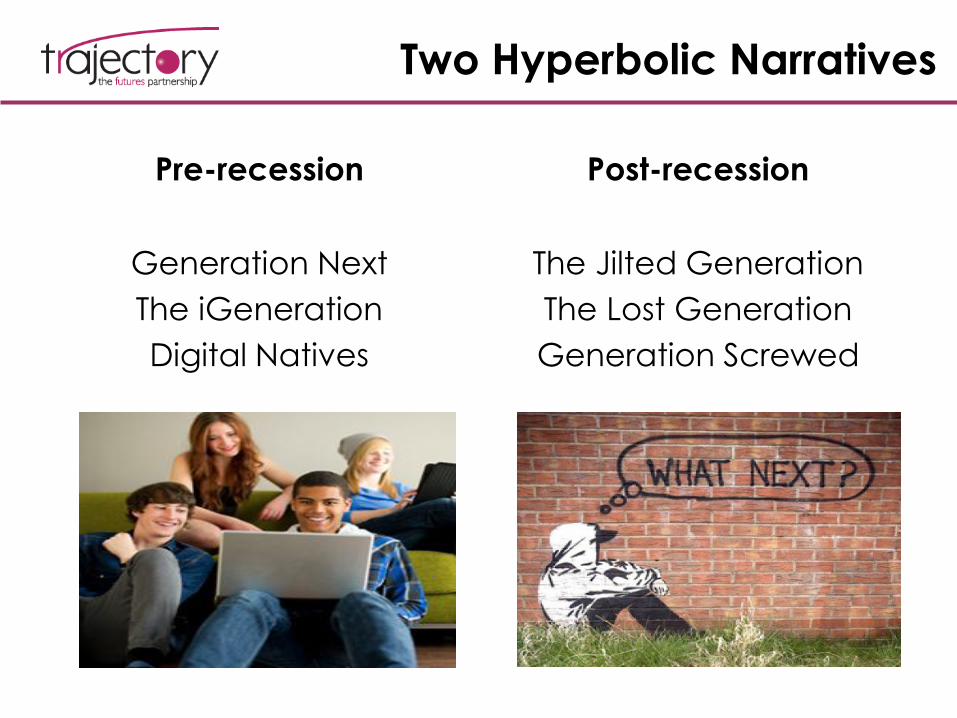

Two Hyperbolic Narratives

Pre-recession

Generation Next

The iGeneration

Digital Natives

Post-recession

The Jilted Generation

The Lost Generation

Generation Screwed

The many faces of Ageing

Diversity

DIVERSE PEOPLE-DIVERSE CULTURE-DIVERSE EXPECTATIONS

Complex Families

Separation. Divorce. Marriage. Remarriage. Step-Children.

No children. My Children. Grand Children. Mixed Ethnicity.

Same Sex. Education. Housing. Child-Care. Income. Leisure.

Privacy. Freedom. Great-Grand Children. Vertical Families.

Emigrants. Immigrants. Mixed-Faith. Single Parents.

CULTURAL CONTEXT

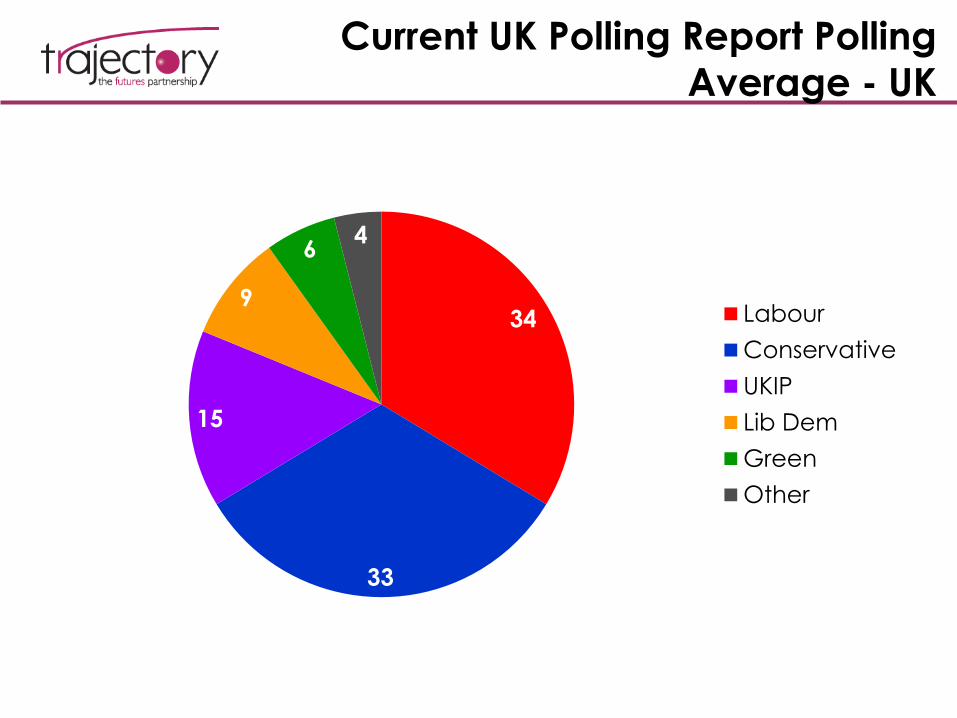

Political Fragmentation:

No Longer Two Tribes

97 90

87

75 81

77 74

68 65

83

61 65

0

20

40

60

80

100

120

1951 1966 1970 1974 1979 1997 2001 2005 2010

Labour & Conservative combined share of national vote at selected

General Elections

Two Party Share of UK GE Vote (%) Turn Out

Current UK Polling Report Polling

Average - UK

34

33

15

9

6 4

Labour

Conservative

UKIP

Lib Dem

Green

Other

Is it really happening? Does it

really matter?

The New Morality

Self-Preservation Society C-Suite Scrutiny Brands: Citizen to Personal

The Compromised Consumer

Value Hunting

Discretionary Thrift

Mercurial Consumption

Decline of Deference

Anxiety Society

Hyper-Connectivity

financial crisis, recession, austerity, stagnation, debt, youth, income, employment

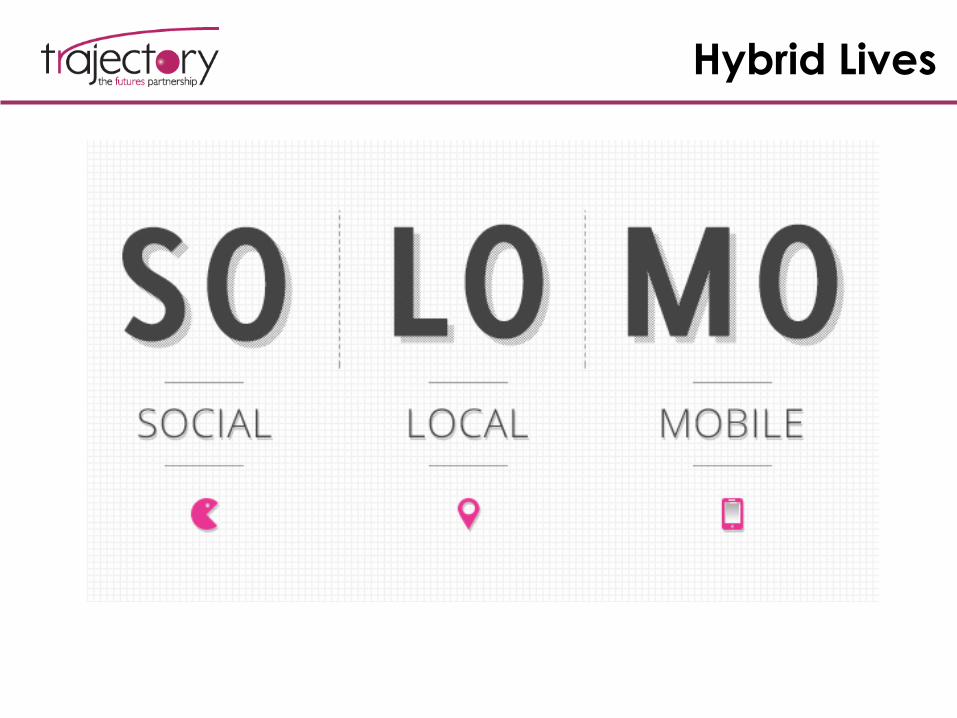

Mobile Everything

Hybrid Lives

Fast & Slow

Hybrid Portfolios

“To be a successful youth brand, you

must be able to do at least one of three

things: make young people’s life

easier, more fun or save them money”

Simon Eder, Voxburner

F&B responses to fragmentation

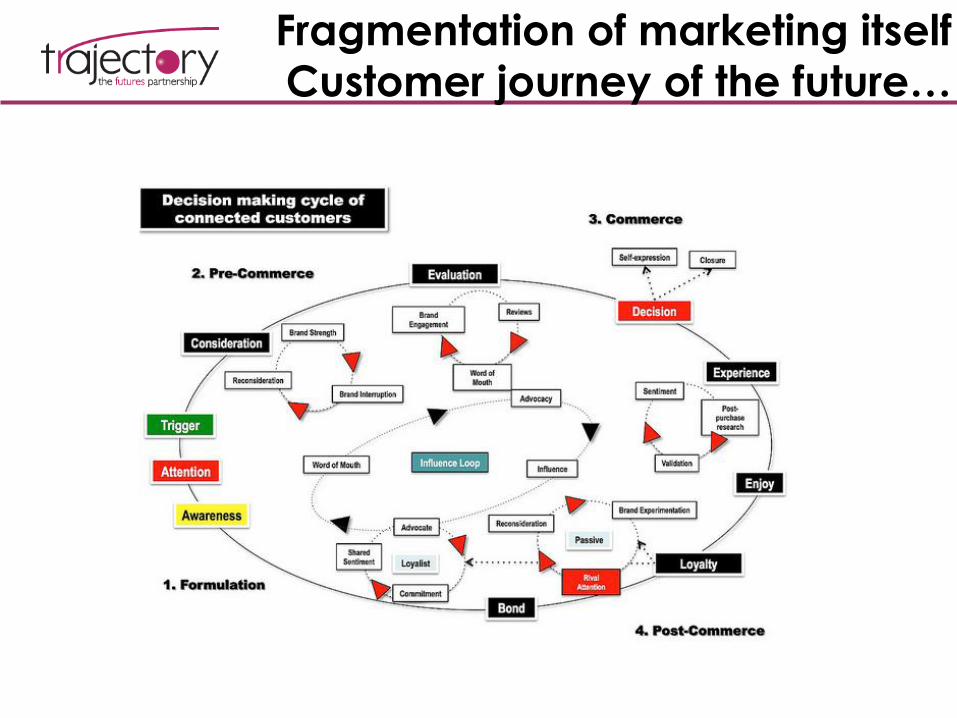

Fragmentation of marketing itself

Customer journey of the future…

Thank you

Trajectory Ltd Enterprise House

1-2 Hatfields

London SE1 9PG

T 020 3567 5801

#TrajectoryTweet

www.trajectorypartnership.com

Paul Flatters: Founder & CEO [email protected]