OECD-BSP Asian Seminar for Financial Education and Financial Inclusion: Addressing the Upcoming Challenges

September 12th, 2012

The Child and Youth Finance Movement: Promoting Financial Inclusion for Children and Youth Cases Studies for a school-based approach.

Daniele Scauso Financial Authorities Relationship Manager

• Financial Authorities and Governmental Sector Representatives

• Financial Institutions and Networks

• NGOs and Social Enterprises

• Financial Education Service Providers

• Foundations

• Leading researchers in the fields of financial inclusion and financial literacy

• Media

• Technology & TelCo.

• Multilateral and Bilateral

Agencies

• Youth

• And more….!

CYFI: a collaborative Partnership Network

Percentage of the Population Below the Age of 18

Source: World Bank /UN Stat 2012

Percentage of 15-25 Year Olds Banked

Source: World Bank /UN Stat 2012

53. We recognize the need for women and youth to gain access to financial services and financial education, ask the GPFI, the OECD/INFE, and the World Bank to identify barriers they may face and call for a progress report to be delivered by the next Summit.

Source: G20 Leaders Declaration - 18-19 June 2012, Los Cabos - Mexico.

Child and youth finance on the International Agenda

CYFI Movement: Vision and Mission

Cognitive Skills Personal Skills Interpersonal Skills

Level 1: 0- 5 years

Identify emotions, understands consequences

Care for precious items, basic health and safety

Express feelings, understands compassion

Level 2: 6 to 9 years

Basic children’s rights, respects diversity

Can follow a daily plan, accepts responsibilities

Respect for rules/guidelines, listening skills

Level 3: 10-14 years

Seeks information for independant thought

Appreciation for lifelong learning, anger management

Express opinions, planning and teamwork

Level 4: 15+ years

Articulate rights, social justice, community outlook

Initiative in the pursuit of goals, time management

Relationship building, leadership, negotiation

CYFI Social/Lifeskills Education (UNICEF, UNESCO)

CYFI Education Framework

Resources and Use

Planning and Budgeting

Risk and Reward Financial Landscape

Level 1: 0- 5 years

Value of money, saving and sharing

Prices and purchases of things they want

Consequences of carelessness, saving special items

Money in the community, understand belongings

Level 2: 6 to 9 years

Recognize monetary symbols

Needs and wants, savings plan

The necessity of saving, rewards of sharing

Choices on banks and financial services

Level 3: 10-14 years

Differant denominations, be an informed consumer

Budget for expenses, short vs. long term planning

Risks and rewards of various financial products

Where to seek financial info, effects of advertising

Level 4: 15+ years

Financial negotiations, purchasing power

Calculate spending capacity, financial goals

Risk of default, impact of interest rates, illicit activity

Aware of financial crimes, evaluate FSPs, mobile banking

CYFI Financial Education (OECD)*

* CYFI has based the Financial Education component of the CYFI Learning Framework on OECD’s PISA 2012 Financial Literacy Assessment Framework. (http://www.oecd.org/dataoecd/8/43/46962580.pdf)

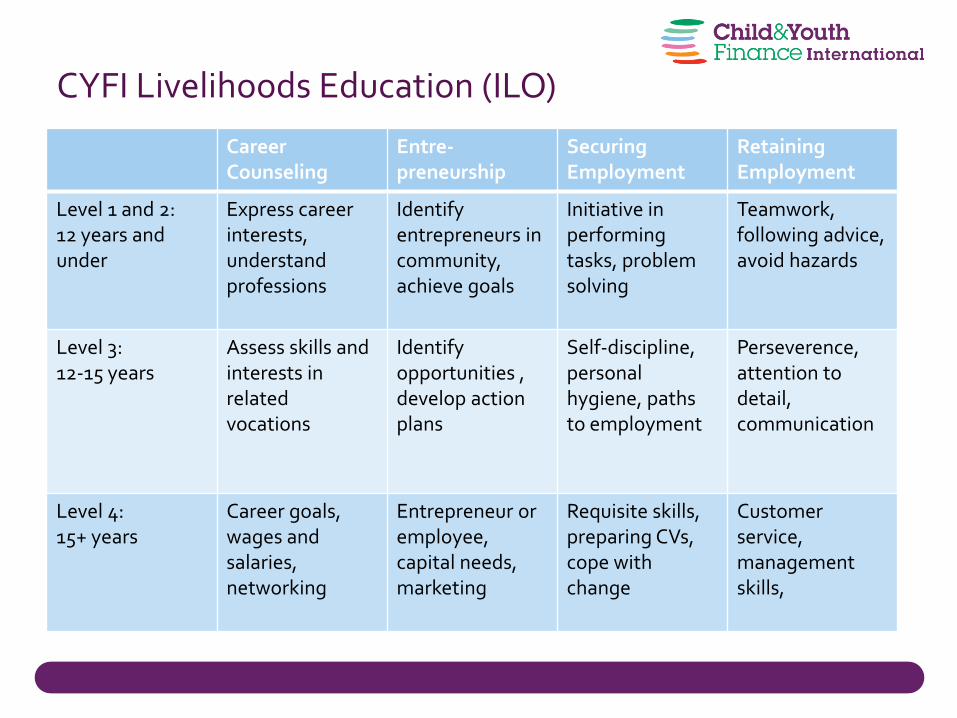

Career Counseling

Entre-preneurship

Securing Employment

Retaining Employment

Level 1 and 2: 12 years and under

Express career interests, understand professions

Identify entrepreneurs in community, achieve goals

Initiative in performing tasks, problem solving

Teamwork, following advice, avoid hazards

Level 3: 12-15 years

Assess skills and interests in related vocations

Identify opportunities , develop action plans

Self-discipline, personal hygiene, paths to employment

Perseverence, attention to detail, communication

Level 4: 15+ years

Career goals, wages and salaries, networking

Entrepreneur or employee, capital needs, marketing

Requisite skills, preparing CVs, cope with change

Customer service, management skills,

CYFI Livelihoods Education (ILO)

Promoting Access to Youth Financial Services (YFS)

• Youth do have money to save

• Research shows significant impact in beginning

savings habits at young age

• Complement to Financial Education

• Informal vs formal savings

• The role of Financial Regulation

• The role of Technology

• Products Barriers

12

ChildFriendly and YouthFriendly Banking Product Certificate

Minimum Institutional Requirements

• The financial institution is licensed under appropriate national laws and regulations

• The institution is in good standing with its national regulatory authority

• The institution is covered by a deposit guarantee scheme, if applicable, in the country

• The institution has a code of conduct with respect to children including staff training and development programs on how to interact with children

12

Minimum Product Requirements

• Non-discriminatory access to products

• Maximum control by the child within the national legal and regulatory framework

• Net positive financial return received by the child • No penalty in case of withdrawals • No or minimal requirements with respect to initial

opening deposits

• No credit facilities (including overdrafts) related to product

• Child-friendly (simple and transparent)communication

surrounding the product • Financial education component to the product (different

levels ranging from educational brochures to “Bank in School programs”)

Case study: Aflatoun – NATCCO Partnerships for Formal Child Savings at school

Source: “Partnerships for Formal Child Savings: The Aflatoun-NATCCO Philippines Case”, Aflatoun Social & Financial Education, 2012

Highlights 2006: NATCCO introduced Aflatoun Program to the network 12 Cooperatives 2008: DepEd National Memo No. 228 Series of 2008 approved for the nationwide implementation of the program – Launch of Child Savings program 2011: Over 12.800 children savings ( age 5-12) More than 10.000 accounts collectively hold Youth Savings Volume: 44.000 USD

Integration in the School Curriculum • Teachers’ training

• Tailoring Education Material

Development of a Child-friendly savings products • Voluntary enrolment in the savings scheme by the student

• Parents need not be signatories to accounts

• The classroom savings process is operated by an Executive Committee

• Accounts are registered in both personal passbooks and a separate ledger

• Deposits can be made on a weekly basis with a minimum deposit of PHP5

• Deposits and withdrawals exceeding a certain amount must be explained

with valid reason presented

• Parents can encourage their children to save but cannot participate

directly in the savings scheme

Implementation

Carla Sánchez - Winner of the CYFI Youth Champion Award at the 1st CYFI Annual Summit & Awards Ceremony, April 3rd-4th, 2012 – Amsterdam, The Netherlands

Children International & Banco de Guayaquill Ecuador

School bank Concept

Who: CYFI Technology and Innovation WG

Keywords: Schools, community centers, non-formal education institutions

Financial inclusion aided by technology Childfriendly – Youthfriendly savings products

Global Connections

GOAL: to reach the maximum number of unbanked children and youth through financial access at schools combined with child and youth financial education

Moving Forward

• Addressing Regulatory Barriers: collaborating with the World Bank on a global survey on childfriendly/youthfriendly regulatory frameworks

• Join The CYFI Week on March 15th -22nd , 2013!

• Join the Movement! Become a Partner of the CYFI Network

Looking forward to meeting you

• CYFI Regional Meeting for Asia & Pacific

December 4th, 2012 - Manila

• 2nd CYFI Annual Summit

April 8th – 10th , 2013 - Istanbul

Supporting CYFI

ChildFinance ChildFinance

www.childfinanceinternational.org

Daniele Scauso

Financial Authorities Relationship Manager

Tel. +31 (0) 20 52 03 812