CBRE Research © 2017 CBRE, Inc. | 1

Summer 2017NORTH AMERICA SUBURBAN OFFICE TRENDS REPORT | LOCAL MARKET

St. Petersburg, Florida

• owntown St. Petersburg of s the cultural epicenter

. The submarket boasts seven arts districts was honored as the No. 1 artdestination in America for mid-sized cities.

• The is also known for its pier, a landmark that has been transformed multiple times since itsinception in 1889. The old structure was demolishedin 2015 and groundwork began on the new pier inJune 2017. The total project will cost $46 million andconstruction should be completed by the end of 2018.

• also h an innovation district,featuring research and medical tenants, life sciences and marine institutions, and a museum district.

• Flourishing development continues in the form ofcraft breweries, residential and mixed-use towers andhotels. Notable projects include:

• The Salvador, a green-certified condobuilding that will overlook the DaliMuseum and the Tampa Bay with street-level retail.

• ONE St. Petersburg, a pivotal mixed-usedevelopment that upon completion will bethe tallest building in Pinellas County. Thetower will feature 13 stories of hotel rooms, 41 stories of condo units and more than17,000 sq. ft. of retail.

• St. Pete is one of the most walkableneighborhoods in Pinellas County. Residents andtourists can find entertainment, dining and shoppingall in close proximity with a waterfront view.

Urban-Suburban Submarkets Trends

EmergingSt. Petersburg

Westshore

Source: CBRE Research, Q1 2017.

Urban-Suburban Submarkets

EstablishedN/AN/A

Source: CBRE Research, Q1 2017.

Q1 2017 Vacancy and RentSt.Pete CBD | Westshore | Total Suburban | Total Tampa

St.Pete CBD | Westshore | Total Suburban | Total Tampa

30

30

40

40

20

20

10

10

0Vacancy Rate

Source: CBRE Research, Q1 2017.

Three Year Rent Comparison

Rent

Q1 2017

6.4% $23.08

$23.08

9.0% $26.62

$26.62

11.0% $21.86

$21.86

11.2%

Q1 2014

$22.67

$22.670 $20.30 $24.11 $19.45 $19.90

CBRE Research © 2017 CBRE, Inc. | 1

Summer 2017NORTH AMERICA SUBURBAN OFFICE TRENDS REPORT | LOCAL MARKET

Westshore, Florida

• With its close proximity to Tampa’s urban core,

Westshore is the most sought-after suburban

submarket in Hillsborough County. This

submarket had the largest concentration of

insurance-related companies to occupy space during

the second quarter. Moreover, Amgen, a global

pharmaceutical company, will move into nearly

125,000 sq. ft. at the end of 2017.

• Aside from the Tampa CBD, the Westshore

submarket has the most development and planned

projects in Hillsborough. This submarket also boasts

the largest inventory of office properties (rentable

square feet) in the Tampa market. While there is no

multi-tenant office construction currently underway,

crews have been active with the development of

residential, hotel and retail properties.

• The Prisa Group plans to open an AC Hotel by

Marriott, the European chain of Marriott hotels, in

Westshore. The hotel is a concept that is expected to

attract millennials in addition to the usual business

travelers.

• The submarket is home to two large shopping malls,

as well as a bevy of restaurants and entertainment

attractions.

• To further strengthen this submarket as a true live-

work-play area, developers have built new and

revamped existing properties into attractive multi-

family housing options.

• Additional investment has been put into outdoor

space and improving walkability, such as widening

the sidewalks, adding canopies for shade and

creating bicycle lanes.

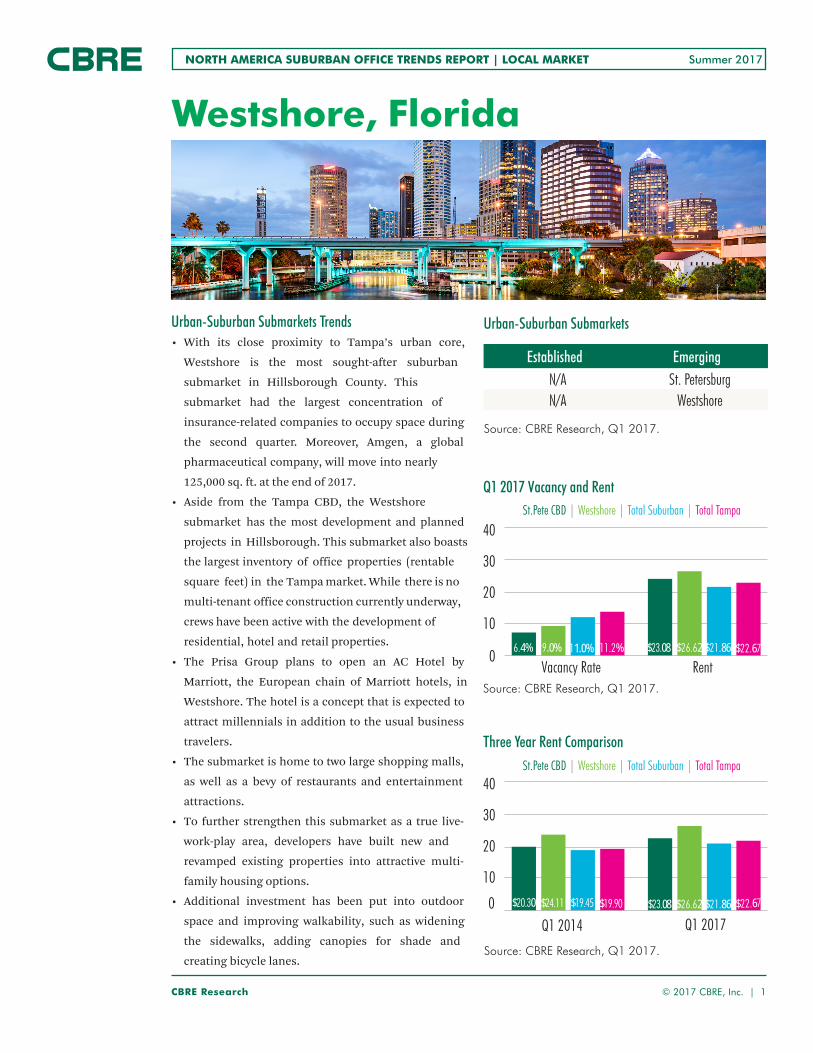

Urban-Suburban Submarkets Trends

EmergingSt. Petersburg

Westshore

Source: CBRE Research, Q1 2017.

Urban-Suburban Submarkets

EstablishedN/AN/A

Source: CBRE Research, Q1 2017.

Q1 2017 Vacancy and RentSt.Pete CBD | Westshore | Total Suburban | Total Tampa

St.Pete CBD | Westshore | Total Suburban | Total Tampa

30

30

40

40

20

20

10

10

0Vacancy Rate

Source: CBRE Research, Q1 2017.

Three Year Rent Comparison

Rent

Q1 2017Q1 2014

$20.30 $24.11 $19.45 $19.90 $23.08 $26.62 $21.86 $22.670

6.4% $23.089.0% $26.6211.0% $21.8611.2% $22.67

Disclaimer: Information contained herein, including projections, has been obtained from sources believed to be reliable. While we do not doubt its accuracy, we have not verified it and make no guarantee, warranty or representation about it. It is your responsibility to confirm independently its accuracy and completeness. This information is presented exclusively for use by CBRE clients and professionals and all rights to the material are reserved and cannot be reproduced without prior written permission of CBRE.

Summer 2017

Spencer G. Levy Americas Head of Research & Senior Economic Advisor +1 617 912 [email protected]@SpencerGLevy

Andrea Cross Americas Head of Off ce Research +1 415 772 [email protected]@AndreaBCross

Taylor Jacoby Senior Research Analyst +1 415 772 [email protected]

Max Saia Economist CBRE Econometric Advisors +1 213 613 [email protected]@MaxXSaia

Alex Krasikov Economist CBRE Econometric Advisors +1 617 912 [email protected]

James Portolese Senior EA Database Developer CBRE Econometric Advisors +1 617 912 [email protected]

To learn more about CBRE Research, or to access additional research reports, please visit the Global Research Gateway at www.cbre.com/researchgateway.

Additional U.S. Research from CBRE can be found here.

FOR MORE INFORMATION, PLEASE CONTACT:

Scott Marshall Executive Managing Director Advisory & Transaction Services | Investor Leasing +1 630 573 [email protected]@S_R_Marshall

Whitley Collins Global President Occupier Advisory and Transaction Services +1 310 363 [email protected]

LOCAL CONTACTS:

Scott Brien Research Operations Manager +1 813 273 [email protected]

NORTH AMERICA SUBURBAN OFFICE TRENDS REPORT | LOCAL MARKET