© 2010 Ncondezi Coal Company – All Rights Reserved July 2010

An Emerging Mozambican Coal Exploration and

Development Company

Graham Mascall – Chief Executive OfficerMozambique Coal Conference, Maputo - 20 July, 2010

Disclaimer – Important Notice

This document, which is personal to the recipient, has been issued by Ncondezi Coal Company Limited (the “Company”). This document does not

constitute or form part of any offer or invitation to sell or issue, or any solicitation of any offer to purchase or subscribe for, any securities of the

Company, nor shall any part of it nor the fact of its distribution form part of or be relied on in connection with any contract or investment decision

relating thereto, nor does it constitute a recommendation regarding the securities of the Company. In particular, this document and the information

contained herein does not constitute an offer of securities for sale in the United States.

This document is being supplied to you solely for your information. The information in this document has been provided by the Company or obtained from publicly

available sources. No reliance may be placed for any purposes whatsoever on the information or opinions contained in this document or on its completeness. No

representation or warranty, express or implied, is given by or on behalf of the Company or any of the Company’s directors, officers or employees or any other

person as to the accuracy or completeness of the information or opinions contained in this document and no liability whatsoever is accepted by the Company or

any of the Company’s members, directors, officers or employees nor any other person for any loss howsoever arising, directly or indirectly, from any use of such

information or opinions or otherwise arising in connection therewith.

Nothing in this document or in the documents referred to in it should be considered as a profit forecast. Past performance of the Company or its shares cannot be

relied on as a guide to future performance.

Certain statements, beliefs and opinions in this document are forward-looking, which reflect the Company’s or, as appropriate, the Company’s directors’ current

expectations and projections about future events. By their nature, forward-looking statements involve a number of risks, uncertainties and assumptions that could

cause actual results or events to differ materially from those expressed or implied by the forward-looking statements. These risks, uncertainties and assumptions

could adversely affect the outcome and financial effects of the plans and events described herein. Forward-looking statements contained in this document

regarding past trends or activities should not be taken as a representation that such trends or activities will continue in the future. The Company does not

undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. You should not

place undue reliance on forward-looking statements, which speak only as of the date of this document.

This document has been prepared in compliance with English law and English courts will have exclusive jurisdiction over any disputes arising from or connected

with this document.

2

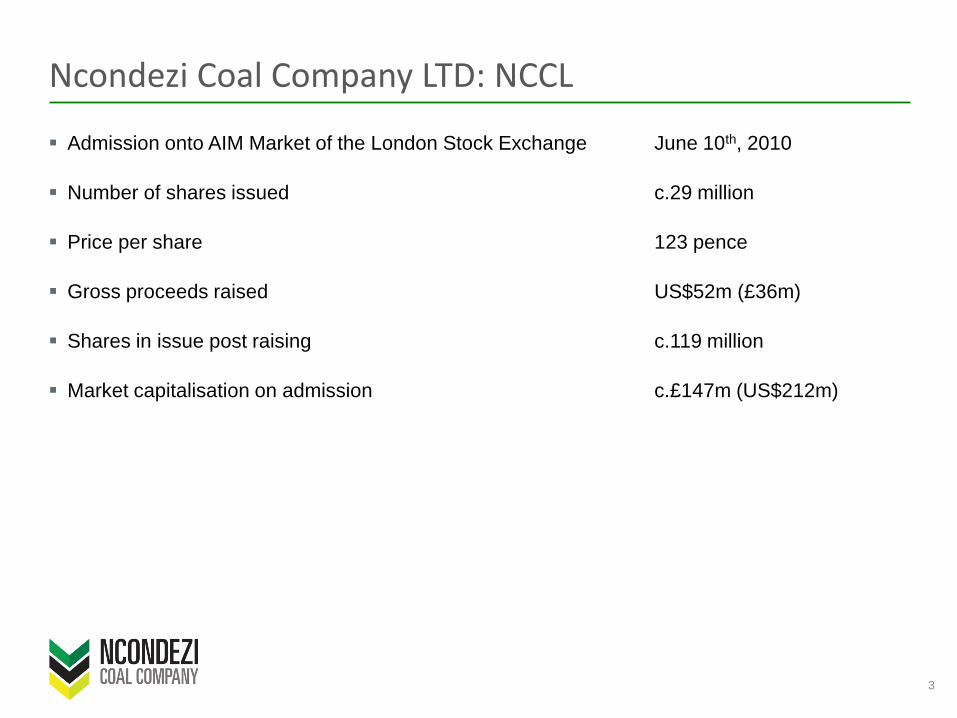

Ncondezi Coal Company LTD: NCCL

3

Admission onto AIM Market of the London Stock Exchange June 10th, 2010

Number of shares issued c.29 million

Price per share 123 pence

Gross proceeds raised US$52m (£36m)

Shares in issue post raising c.119 million

Market capitalisation on admission c.£147m (US$212m)

Shareholder structure

4

100%1

Additional Licences(Licences 1314L & 1315L)

Ncondezi Project(Licences 804L & 805L)

Dos Santos

Family

10%

1 Licences 100% held indirectly through 100% owned subsidiaries in Mozambique and Mauritius

MinoritiesManagement

EBTFree floatStrata Ltd

5%46% 15% 24%

100%1 100%

Introduction

5

Ncondezi Coal Company Limited (“Ncondezi” or the “Company”) is a AIM listed coal exploration and development company with 4 licences in the Tete province of Mozambique

The licences were first issued in December 2004

Strata Limited became a majority shareholder in the Group in 2007 and funded the two subsequent work programs between 2007 and 2009

Current management team, led by CEO Graham Mascall, joined the company in Q4 2009

Nigel Walls – Chief Operating Officer

Manish Kotecha – Chief Financial Officer

Exploration activities focused on licences 804L and 805L (“Ncondezi Project”)

122 boreholes or 16,737 m drilled to date

Scoping Study on licences 804L & 805L completed Q2 2010

Investment Summary

6

Strategic licences in one of the world’s largest undeveloped coking and thermal coal basins in Mozambique

Close proximity to coal projects being developed by Vale and Riversdale and existing rail infrastructure

Large scale resource with significant upside potential

Ncondezi Project is one of the largest contiguous licence areas in the region

JORC resource classification of 1.8Bt

Only 3 of 7 blocks drilled

Additional exploration target of 400-1,600Mt1 identified with further drilling

SRK Scoping Study confirms economically robust 10Mtpa thermal coal project

Coking coal potential to be further tested

Initial results from 3 holes show encouraging coking coal potential

Experienced management team

Over 70 years collective experience in the mining sector

Board includes Mozambique’s ex National Director of Mines

Current Work Program designed to complete fast track Bankable Feasibility Study (“BFS”) in H2 2012

1 Initial estimates are based on limited drilling and are scheduled to be explored further. Reported in accordance with clause 18.1 of the JORC code

Ncondezi Board

Richard Stuart - Chairman Chairman of Strata Limited

Former Joint Senior Partner of Fleming-Martin, one of South Africa's leading brokerage firms that was acquired by Flemings in 2000

Estevao Pale - Non Executive Director Current CEO of Companhia Moçambicana de Hidrocarbonetos (CMH), a Mozambican natural gas company

Former National Director of Mines in the Ministry of Mineral Resources and Energy between 1996 and 2005

Has sat on the board of numerous companies in the mining sector, and conducted several consultancies for international organizations

Graham Mascall - CEO Over 35 years of experience in mining and mining finance

Chairman of Gemfields, an AIM listed Emerald/Gemstone company, and on the Board of Directors of London Mining PLC

Previously CEO of International Molybdenum and Lubel Coal Company

Mark Trevan - Non Executive Director Currently Managing Director at Caledon Resources

Previously worked for Rio Tinto for 25 years as a senior executive in the coal division

Nigel Sutherland - Non Executive Director Over 34 years experience in the global resource sector

Previously worked with Anglo American for 17 years and Goldfields for 4 years

Colin Harris - Non Executive Director Currently Director General of the MPD Zanaga iron ore project in Congo Brazzaville

Over 40 years experience as an exploration geologist

Previously worked for Rio Tinto for 25 years, Anglo American for 5 years and Cominco for 14 years

7

Mozambique: An African Success Story

One of Africa’s fastest growing economies

Politically stable since the end of civil war in 1992

Considered successful example of post-conflict reconciliation

President re-elected in elections in October 2009

Key mining sector ministers reappointed for further 5 years

High inflows of Foreign Direct Investment

Strong commercial links with South Africa as its main trading partner

Political and economical stability

Strong resource development and investment track record

Vale – Moatize US$1.3 billion

Riversdale/Tata Steel – Benga US$260 million

BHP – Mozal US$2 billion

Kenmare – Moma US$500 million

Sasol Gas Pipeline US$1.2 billion

Other companies investing in Mozambique include ENRC, Coal of India,

JSW and Jindal

8

Tete: One of the Largest Undeveloped Coal Regions

9

Ncondezi Project

1.4bn resource

US$1.3bn project cost

First production in H2 2011

Capacity for 11Mtpa production, 8.5Mtpa coking, 2.5Mtpa thermal

Building one of the largest wash plants in the southern hemisphere – 26Mtpa

Zambeze Project

24,740 ha

150 boreholes drilled

JORC resource of 9.0Bt

6.1Bt at <500m depth

Coking and thermal coal potential

MoU signed with Wuhan Iron and Steel to acquire a 40% stake for US$800m in three tranches

Sena Railway

Moatize Town

Tete Town

Vale (Moatize Project)

ENRC licence 871L

JORC resource of 1.0Bt

Located south of Zambezi River

Others

Opening first box

cut at MoatizeBenga Project

4,560 ha

4Bt resource, reserves of 502Mt

Tata Steel acquired 35% stake in 2007 for A$100m

First production in H2 2011

Phase 1 to produce 1.7Mtpa coking and 0.3Mtpa thermal with capex of US$260m

Potential capacity of 10Mtpa

Riversdale Mining (US$1.6bn market cap.)

38,700 ha

JORC resource of 1.8Bt tonnes

100% of resource at c.200m

Scoping study confirms 10Mtpa thermal coal open cast mine

10kms to Sena Railway and c.40kms from provincial capital Tete

Source: SRK (May 2010), Golder Associates Africa maps, Company websites and publications

The Ncondezi Project – Licences 804L and 805L

10

c.35kms

c.11

kms

Source: SRK (May 2010)

c.35kms

North

122 boreholes totalling 16,737 metres have been drilled across 804L and 805L to date

Ncondezi Project Exploration History

11

1980-1981 Swede Coal Exploration (No resource classified)

8 core holes completed

Confirmed presence with initial indications of substantial coal resource

2004 Company awarded licences 804L and 805L

2006 Exploration Programme

2 twin core holes completed on 804L and 805L to confirm Swede Coal results

2007 Strata Limited investment in the Company

2007-2008 Exploration Programme

65 core holes totalling 5,522 meters completed

Drilling in Southern, Northern, and Western Blocks

Samples sent to ACT laboratories in Tete for wash tests

2009 Exploration Programme (1.8Bt JORC resource classified)

SRK review of project

New management team recruited

54 Percussion holes totalling 10,978m including 8,555m of geophysical logging completed

31 twinning holes and 23 new holes

3 cored holes drilled for coking tests

3D geological modelling completed

2010 Exploration Programme

1.8Bt JORC resource classified

Scoping Study produced by SRK

Core recovery from S18

Percussion chips from W05

1.8Bt JORC Resource Identified

12

Significant resources identified (JORC) on 804L & 805L

Geological loss factor of 30% applied to all blocks

Drilling limited to 200m depth

JORC classification and tonnages (South, North and West Blocks only)1

Block

Measured

Mt

Indicated

Mt

Measured &

Indicated

Mt

Inferred

Mt

Total

Mt

South 24 447 471 127 597

North 0 174 174 503 677

West 0 0 0 534 534

Total 24 620 644 1164 1,809

Resource (804L & 805L)

Characteristics (804L & 805L)

Five distinct coal zones identified in the North, South and

West blocks

Varying thickness but Zone 1 thickest at up to 83.5m

Average thickness of coal seams: 4.4-49.3m

Shallow nature of deposits conducive to open pitmining

General dip 5-30 degrees

Coal zones can be beneficiated at acceptable yields by

dense medium separation to produce export coal products Source: SRK (May 2010)

Source: SRK (May 2010)

Note: In situ resources tonnages have been adjusted for a 30% geological loss factor1 Numbers are rounded

South Block Cross Sections

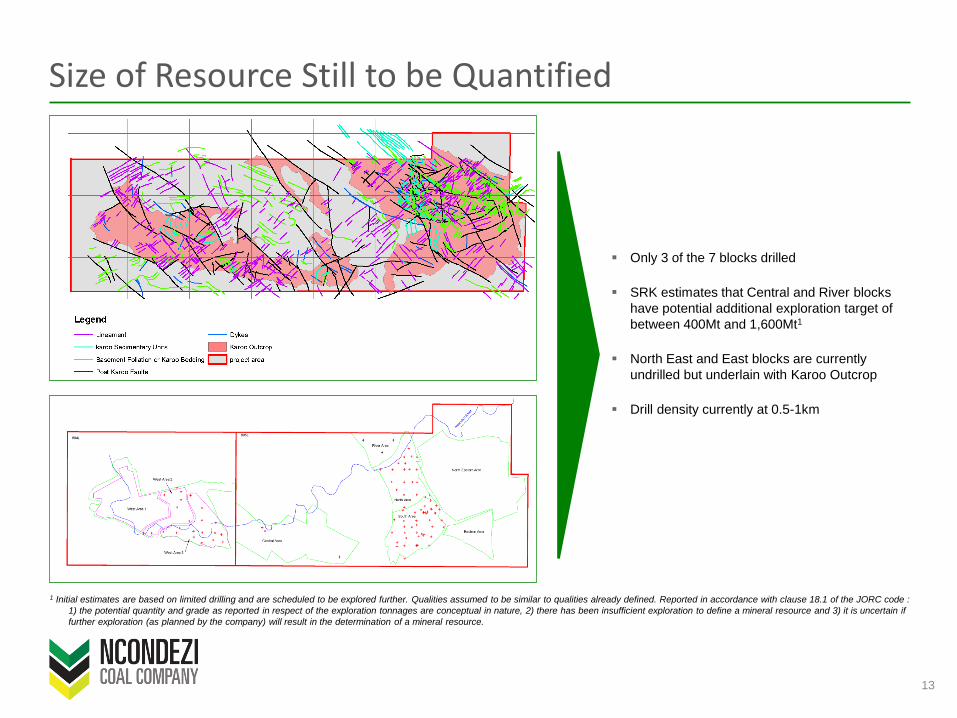

Size of Resource Still to be Quantified

Only 3 of the 7 blocks drilled

SRK estimates that Central and River blocks

have potential additional exploration target of

between 400Mt and 1,600Mt1

North East and East blocks are currently

undrilled but underlain with Karoo Outcrop

Drill density currently at 0.5-1km

13

1 Initial estimates are based on limited drilling and are scheduled to be explored further. Qualities assumed to be similar to qualities already defined. Reported in accordance with clause 18.1 of the JORC code :

1) the potential quantity and grade as reported in respect of the exploration tonnages are conceptual in nature, 2) there has been insufficient exploration to define a mineral resource and 3) it is uncertain if

further exploration (as planned by the company) will result in the determination of a mineral resource.

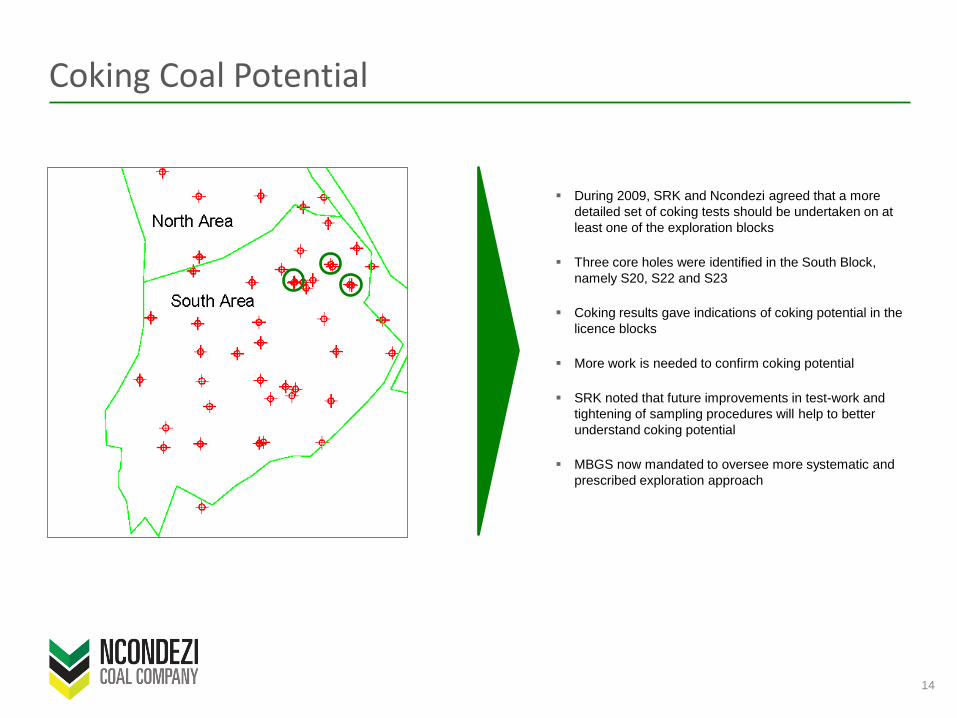

Coking Coal Potential

During 2009, SRK and Ncondezi agreed that a more

detailed set of coking tests should be undertaken on at

least one of the exploration blocks

Three core holes were identified in the South Block,

namely S20, S22 and S23

Coking results gave indications of coking potential in the

licence blocks

More work is needed to confirm coking potential

SRK noted that future improvements in test-work and

tightening of sampling procedures will help to better

understand coking potential

MBGS now mandated to oversee more systematic and

prescribed exploration approach

14

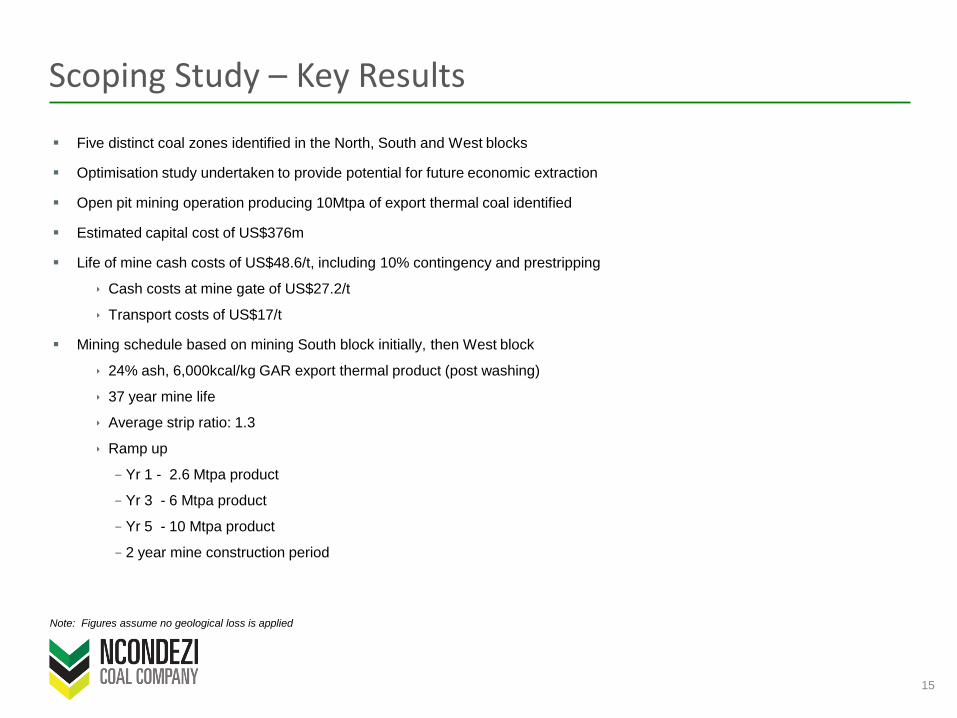

Scoping Study – Key Results

Five distinct coal zones identified in the North, South and West blocks

Optimisation study undertaken to provide potential for future economic extraction

Open pit mining operation producing 10Mtpa of export thermal coal identified

Estimated capital cost of US$376m

Life of mine cash costs of US$48.6/t, including 10% contingency and prestripping

Cash costs at mine gate of US$27.2/t

Transport costs of US$17/t

Mining schedule based on mining South block initially, then West block

24% ash, 6,000kcal/kg GAR export thermal product (post washing)

37 year mine life

Average strip ratio: 1.3

Ramp up

− Yr 1 - 2.6 Mtpa product

− Yr 3 - 6 Mtpa product

− Yr 5 - 10 Mtpa product

− 2 year mine construction period

15

Note: Figures assume no geological loss is applied

Production commencing 2014/15

Maximum depth of approximately 200m

200 Mt of 24% ash, 6,000 kcal/kg GAR coal export

product

22 year mine life

Total material movement 1,788 Mt

Raw coal production of 756 Mt

Stripping ratio of 1.4

Scoping Study Conceptual Pit – Configuration and phasing

Production commencing year 23

Maximum depth of approximately 200 m

15 year mine life

Average stripping ratio of 1.2

South Block

West Block

Optimised pit shells for the South and West Blocks

For a primary 24% ash, 6,000kcal/kg GAR coal export product

Overview

Source: SRK (May 2010)

16

Mozambique Strategically Positioned to Supply Growth Markets in the Seaborne Coal Markets

+3.5Bt tonnes of global coal demand growth forecast by 2030

90% of long term coal demand expected to come from Asia,

particularly India and China

Mozambique competitively positioned for exports into India,

China, Brazil and Europe

India and China to account for c.60% of growth in

seaborne demand between 2009 and 2015

Expected strong demand for Mozambique’s coal products

Mozambican coal expected to be competitive with those

of Australia, South Africa, Indonesia, Colombia

17

+150

+50

+690

+110

+380

+2,210

Global Coal Demand Growth Forecast 2007-2030 (Mt)

Source of Additional Seaborne Coal Demand 2009-2015 (Mtpa)

India

125

Japan

25

Taiwan

12.5

Other Pacific

40

Atlantic

45

Total additional seaborne coal demand 2015E = 378Mtpa

China

100

South Korea

30

Total growth in global coal demand 2007-2030 = 3.8Bt

Source: Peabody, JPMorgan Cazenove Equity Research

0

20

40

60

80

100

120

140

2009A 2010E 2011E 2013E 2015E 2017E 2019E

Investment case for thermal coal remains robust Global seaborne thermal coal demand traditionally robust with CAGR

of 10% over last 30 years

Ongoing demand growth will be driven by increased electrification of the planet

94 GW of new coal fired power generation to come on line in 2010

This represents an additional thermal coal requirement of 375Mtpa

Asia, particularly China and India, is already leading the growth in power generation demand

China and India account for 40% of the World’s population

US per capita electricity use is 5x higher than China and 25x higherthan India

India forecast to be the World’s fastest growing importer of coal

India currently has 78GW of new coal fired power generation underconstruction

Supply side problems developing for the seaborne market

China & India – Insufficient domestic production, both net importers ofthermal coal in 2009 and predicted to continue going forward

Australia – Mine tax on coal producers limits development of newprojects. Capacity constraints at port and rail

Indonesia – Coal quality decreasing. Regulation being developed tolimit coal exports as domestic coal fired industry ramps up

South Africa – Rail constraints already limiting exports

Columbia – Coal industry threatened by industrial action

Russia – Cash costs have risen 45% in last two years, largely drivenby increases in rail charges

USA – Appalachian exports only viable at thermal coal prices of$105/t and above

18

Indian Seaborne Thermal Coal Demand

Millions of Tonnes

Source: Peabody, McCloskey, JPMorgan Cazenove Equity Research

New Coal Fired Power Generation 2010 (GW)

China

55

India

19

Other Asia

8

USA

7

Others

5

Total new power generation 2010E = 94GW

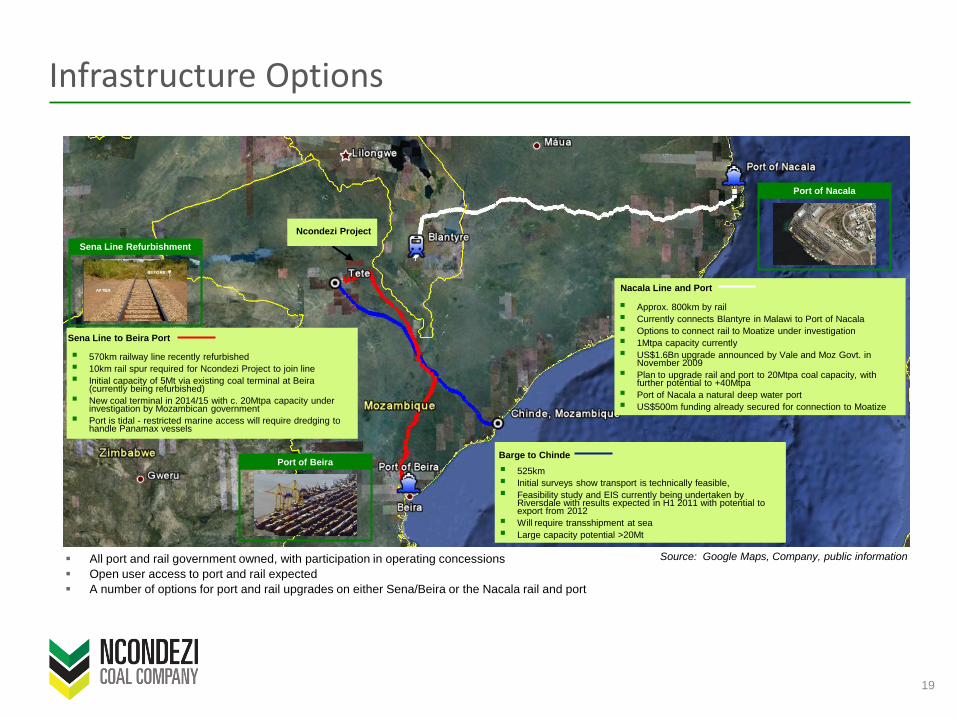

Infrastructure Options

19

570km railway line recently refurbished

10km rail spur required for Ncondezi Project to join line

Initial capacity of 5Mt via existing coal terminal at Beira (currently being refurbished)

New coal terminal in 2014/15 with c. 20Mtpa capacity under investigation by Mozambican government

Port is tidal - restricted marine access will require dredging to handle Panamax vessels

Sena Line to Beira Port

525km

Initial surveys show transport is technically feasible,

Feasibility study and EIS currently being undertaken by Riversdale with results expected in H1 2011 with potential to export from 2012

Will require transshipment at sea

Large capacity potential >20Mt

Barge to Chinde

Approx. 800km by rail

Currently connects Blantyre in Malawi to Port of Nacala

Options to connect rail to Moatize under investigation

1Mtpa capacity currently

US$1.6Bn upgrade announced by Vale and Moz Govt. in November 2009

Plan to upgrade rail and port to 20Mtpa coal capacity, with further potential to +40Mtpa

Port of Nacala a natural deep water port

US$500m funding already secured for connection to Moatize

Nacala Line and Port

Ncondezi Project

All port and rail government owned, with participation in operating concessions

Open user access to port and rail expected

A number of options for port and rail upgrades on either Sena/Beira or the Nacala rail and port

Sena Line Refurbishment

Port of Beira

Port of Nacala

Source: Google Maps, Company, public information

Additional Licences 1314L and 1315L

20

Licence 1314L

Located 130km south west of Tete on the border

with Zimbabwe

Total area of 17,380 hectares

Licence 1315L

Located 320km North West of Tete on north shore of

Cahora Basa Lake.

Total area of 17,080 hectares

Licence 1314LLicence 1315L

Source: SRK (May 2010)

Environmental and Social Responsibility

Environment and Social Policy in place

Full time Community Liaison Officer appointed in Tete

Commence Environmental Social Economic baseline study in Q3 2010

Environmental and Social Impact Assessments (“ESIA”) to completed in 2012

Important part of the BFS and standalone requirement for mining licence application

ESIA work to be carried out by independent local and international consultants

Work will begin in Q3 2010

21

“Environment, Social, Health and Safety responsibilities are integral to the way we do business”

Work Program Overview Work Program fully funded from proceeds of June 2010 AIM placing

Work Program budget of US$47.2m over two years

+US$40m dedicated to exploration work

Resource drilling on the Ncondezi Project to identify coal potential on all blocks

Total drilling on 804L & 805L of 64,000m budgeted

Focus on coal quality data

MBGS to provide consulting input and overview on exploration management, procedures and data

management activities

Will target yield increases and coking coal potential

Additional coking coal test work on cored holes that display coking characteristics

SRK has reviewed and given its support of the Work Program, and considers it to be achievable

22

Professionals already mandated for Work Program to date

Strategy

Target completion of BFS and ESIA by H2 2012

2 year construction phase - target first production in late 2014

Upgrade and increase resource at Ncondezi Project

Maximise transition of resources from Inferred to Measured & Indicated

Yield optimisation on saleable product

Assess and maximise coking coal potential

Assess other value creating options

Offtake agreement

Corporate opportunities

Infrastructure participation

Target to be next coal exporter after Vale and Riversdale

23

Summary

Largest undeveloped coal region in the world

Access to key growth markets

Infrastructure revitalisation underway

Supportive government with track record of world-class projects

Well

Positioned

to Serve

Growth

Market

Ncondezi Project

JORC compliant resource of 1.8Bnt

Fast track to BFS and project development

SRK Scoping Study supports 10Mtpa export thermal coal project with coking coal

potential

Attractive

Resource

Base with

Significant

Upside

Potential

24

Questions?

25