SMART UNCONVENTIONAL MONETARY

(SUMO) POLICIES: GIVING IMPETUS TO

GREEN INVESTMENT

Romain Morel

Project manager, Investment and Climate CDC Climat Research

Our Common Future under Climate Change

UNDERSTANDING WHERE SUMO

POLICIES STAND

The real paradigm shift

Today We need the private

sector/financial markets to

move on climate to address

the 2°C

What could

really work

Climate change and

subsequent policies will

substantially modify our

business model/ability to

address our mandate

3

Our proposal: looking at institutions’ mandates, finding the impact

of climate change and climate policies on them and looking for how

they can address climate financing issues within their mandate.

Based on a report written with IDDRI “Mainstreaming climate change in the financial sector and its governance”

http://bit.ly/1SykWcA

3 dimensions make climate fighters’ and the

financial sector’s agendas mutually reinforcing

4

1. Expected impacts of climate change will substantially harm global

GDP growth in the short and long term

Besides the expected loss in global wealth, sovereign debt and the

whole financial sector may suffer from repeated crises.

2. Financial risks induced by climate policies will harm individual

institutions but may become systemic according to amounts at stake

As expected value loss are high in an “optimized” world, the financial

sector should advocate for a better anticipation of climate policies.

3. A 2°C-compatible financial sector is full of new opportunities and an

improved way to make business

More productive investment, better intermediation and better risk

assessment will be the result of a successful low-carbon transition.

Based on a report written with IDDRI “Mainstreaming climate change in the financial sector and its governance”

http://bit.ly/1SykWcA

Mainstreaming climate change at

each stage of the value chain

Supply of capital

• Incentive structure faced by capital providers, intermediaries and asset holders to allocate their assets

Matching instrument and tools

• Translating low-carbon and resilient project into financial assets that match investors’ needs

Demand of green capital

• Creating the environment to make emerge enough low-carbon and resilient, economically viable, projects.

5

The financial governance and regulatory

institutions can act at every stages

E.g.: IMF and

OECD works on

international

cooperation on

fiscal policies and

policy alignment

E.g.: IOSCO and central banks

could work on how developing

green securitization

Based on a report written with IDDRI “Mainstreaming climate change in the financial sector and its governance”

http://bit.ly/1SykWcA

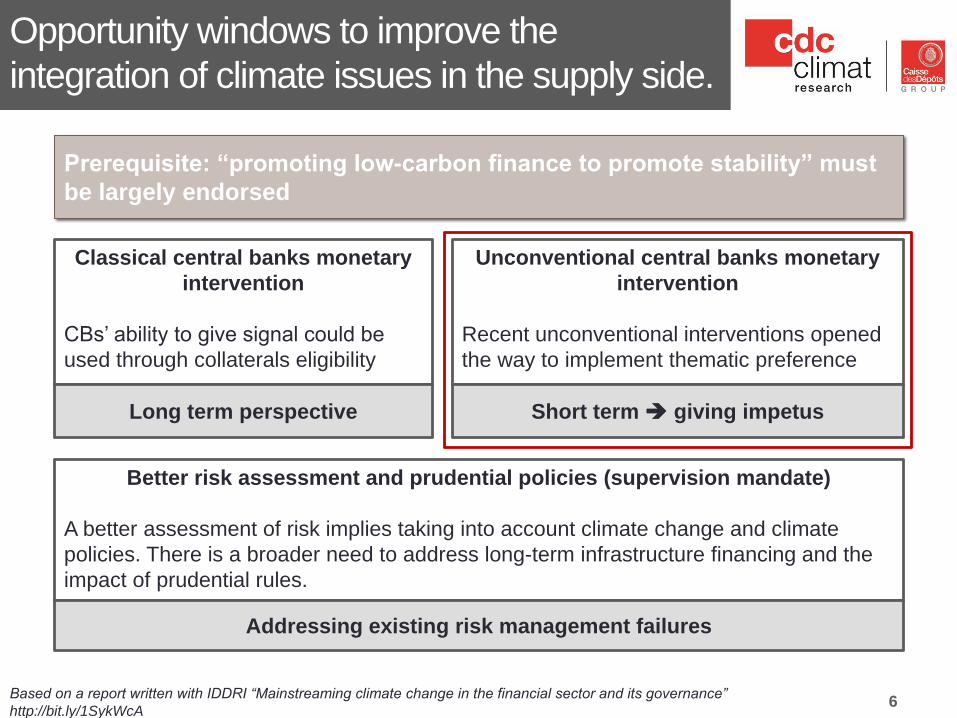

Opportunity windows to improve the

integration of climate issues in the supply side.

6

Prerequisite: “promoting low-carbon finance to promote stability” must

be largely endorsed

Classical central banks monetary

intervention

CBs’ ability to give signal could be

used through collaterals eligibility

Unconventional central banks monetary

intervention

Recent unconventional interventions opened

the way to implement thematic preference

Long term perspective Short term giving impetus

Better risk assessment and prudential policies (supervision mandate)

A better assessment of risk implies taking into account climate change and climate

policies. There is a broader need to address long-term infrastructure financing and the

impact of prudential rules.

Addressing existing risk management failures

Based on a report written with IDDRI “Mainstreaming climate change in the financial sector and its governance”

http://bit.ly/1SykWcA

UNDERSTANDING SUMO POLICIES

A REVIEW OF DIFFERENT PROPOSALS

Shifting trillions with low-recourse to

public budgets

• Unconventional Monetary Policies can be seen as a way

to “print money” to help finance the low-carbon transition

• They also can be perceived as a “coherence” test of the

alignment of monetary policies and climate change

objectives

• They usually appear in a context of low-inflation/deflation

and can inflate the risk of financial bubbles

8

Three mechanisms based on

unconventional monetary policies

SDRs

Green Quantitative

Easing

Carbon Certificates

9

Two mechanisms based on

existing elements and one

original mechanism

Different scales of

implementation

Possible co-benefits

Used to capitalize an international Green

Fund

Restricting the access to QE for specific

assets

Creation of a new asset setting a price on

emission reductions. Set a carbon price for

new infrastructure.

Some limits that can be tackled thanks

to an efficient MRV procedure

• Limits linked with the economic optimality • Windfall profit and rent-seeking

• Moral hazard

• Crowding-out of private investment

• Transaction costs

• Hence a need for an efficient Monitoring, Reviewing and Verification (MRV) procedure with limited costs of implementation

Tradeoff between a precise selection of projects and low transaction costs

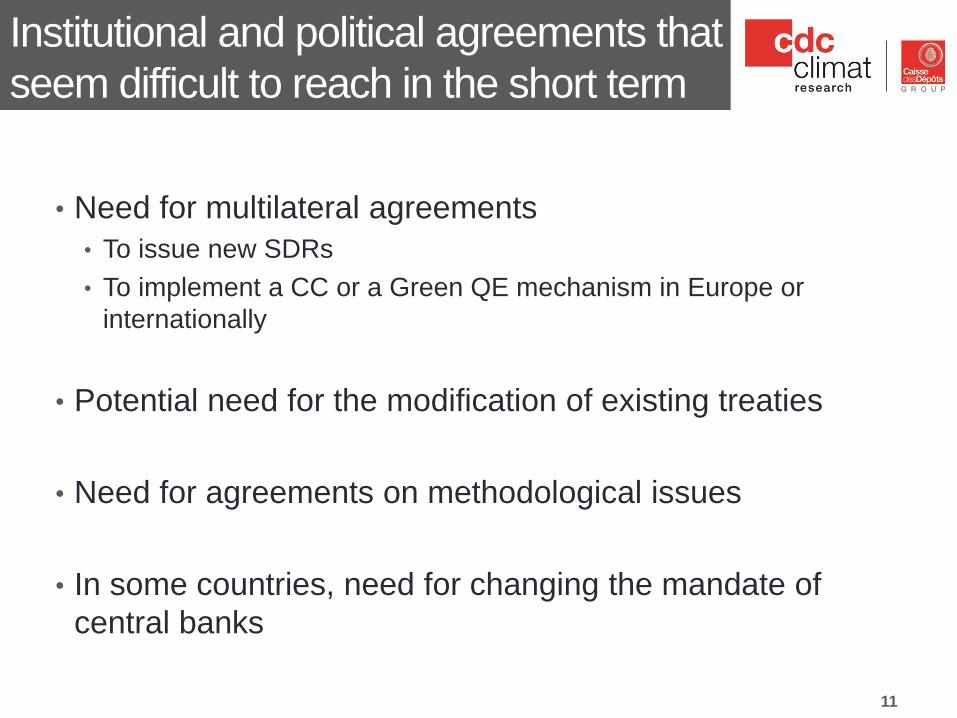

10

• Need for multilateral agreements

• To issue new SDRs

• To implement a CC or a Green QE mechanism in Europe or

internationally

• Potential need for the modification of existing treaties

• Need for agreements on methodological issues

• In some countries, need for changing the mandate of

central banks

Institutional and political agreements that

seem difficult to reach in the short term

11

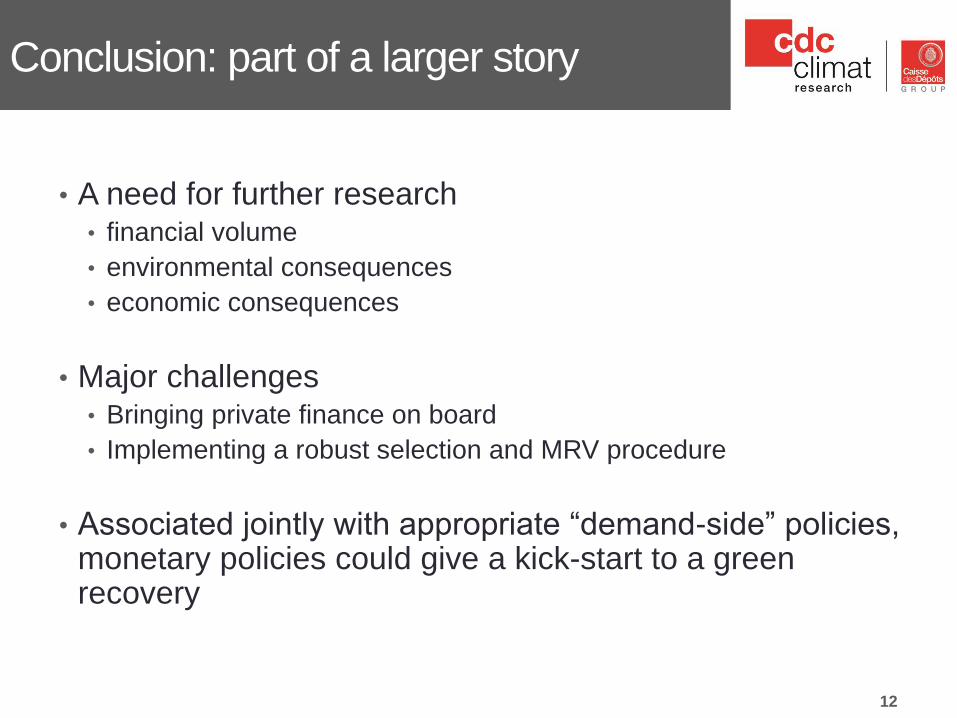

• A need for further research • financial volume

• environmental consequences

• economic consequences

• Major challenges • Bringing private finance on board

• Implementing a robust selection and MRV procedure

• Associated jointly with appropriate “demand-side” policies, monetary policies could give a kick-start to a green recovery

Conclusion: part of a larger story

12

Thank you for your attention

To read our publications:

http://www.cdcclimat.com