Monetary Integration in Europe

Jan Fidrmuc

Brunel University

Monetary Union

Monetary union implies a choice between exchange rate stability and monetary policy autonomy

The impossible trinity: only 2 of the following possible simultaneously: Full capital mobility Autonomous monetary policy Fixed exchange rates

Exchange-rate Regime Alternatives1. Free floating exchange rate

2. Managed float, target zone, crawling peg

3. Fixed exchange rate, currency board, dollarization

Exchange-rate Regime Choice Adjustment to adverse shocks (business

cycles) using monetary policy Can be misused inflation

Exchange-rate volatility and vulnerability to speculative attacks

Political pressure on exchange-rate policy

Two Corners

Only pure floats or hard pegs are robust: intermediate arrangements (soft pegs) invite

government manipulations, over or under valuations and speculative attacks

pure floats remove the exchange rate from the policy domain

hard pegs are robust to speculative attacks Soft pegs are half-hearted monetary policy

commitments, so they ultimately fail

Metallic Money

Before paper money, Europe was a de facto monetary union.

Under metallic money (gold and/or silver) the whole world was really an informal monetary union.

Formal unions only agreed on the metallic content of coins to simplify everyday trading.

Countries cannot issue currency and cannot use the exchange rate to adjust relative prices (e.g. to reverse a current-account deficit or to stimulate demand)

Adjustment occurs through prices and wages

The Interwar Period: The Worst of All Worlds

Paper money started circulating widely. The authorities attempted to resume the gold

standard but: no agreement on how to set exchange rates

between paper monies an unstable starting point due to war legacy

high inflation high public debts.

European Postwar Arrangements

An overriding desire for exchange rate stability: initially provided by the Bretton Woods system the US dollar as an anchor and the IMF as

conductor. Once Bretton Woods collapsed, the Europeans

were left on their own: the timid Snake arrangement the European Monetary System (EMS) the monetary union.

The Bretton Woods System Collapse Initial divergence (dollar exchange rates).

The Snake Arrangement Agreement on stabilizing intra-European bilateral

parities. No enforcement mechanism: too fragile to survive.

The EMS: Super Snake

EMS = European Monetary System A EU arrangement: all EU members are part of it

ERM = Exchange Rate Mechanism An agreement to fix the exchange rate

ERM jointly managed Changes in exchange rates agreed by all members Fluctuations between +/-2.25% and +/-15% Mutual support to prop up exchange rates when needed Allows prompt realignments Deutschemark gradually emerged as the anchor

EMS: Past and Present

EMS originally conceived as solution to the end of the Bretton Woods System

Gradually it became DM centered The speculative crisis of 1993 made the

monetary union option attractive Now ERM is the ante room for EMU entrants The UK and Denmark opted out from ERM

membership All the others are expected to enter the ERM

sooner or later (cf. Sweden)

Preview: The Four Incarnations of the ERM

1979-82: ERM-1 with narrow bands of fluctuation (2.25%) and symmetric.

1982-93: ERM-1 centered on the DM, shunning realignments.

1993-99: ERM-1 with wide bands (15%). From 1999: ERM-2, asymmetric, precondition to

full euro-area membership.

Four Incarnations of the EMS

The ERM: Key Features A parity grid:

bilateral central parities associated margins of fluctuations.

Mutual unlimited support: exchange market interventions short-term loans.

Realignments: tolerated, not encouraged require unanimous agreement.

The ECU: not a currency, just a unit of account took some life on private markets.

The ECUA basket of all EU currencies.

Evolution: From Symmetry to DM Zone

First a flexible arrangement: different inflation rates: long run monetary policy

independence frequent realignments.

Evolution: From Symmetry to DM Zone

Inflation

0

2

4

6

8

10

12

14

16

18

1950-1972 1973-1978 1979-1985 1986-1991 1992-1998

France

Germany

Italy

Netherlands

Italy 1980-1998

-3

-2

-1

0

1

2

3

4

1980 1983 1986 1989 1992 1995 1998

80

85

90

95

100

105

110

115

120

125

Current Account Real Exchange Rate (previous year)

Evolution: From Symmetry to DM Zone However: realignments:

barely compensated accumulated inflation differences

were easy to guess by markets speculative attacks

The symmetry was broken de facto. The Bundesbank became the example to follow.

The DM Zone

What shadowing the Bundesbank required: giving up of much what was left of

monetary policy independence aiming at a low German-style inflation rate avoiding realignments to gain credibility.

Breakdown of the DM zone Bad design:

full capital mobility established in 1990 as part of the Single Act

ERM in contradiction with impossible trinity unless all monetary independence relinquished.

Bad luck: German unification: a big shock that called for

very tight monetary policy the Danish referendum on the Maastricht Treaty.

A wave of speculative attacks in 1992-3: the Bundesbank sets limits to unlimited support.

Lessons From 1993

The two-corner view: even the cohesive ERM did not survive go to one of the two corners monetary union or floating exchange rate

Interventions cannot be unlimited: need more discipline and less support

Speculative attacks can hit even robust systems and properly valued currencies (i.e. self-fulfilling crises)

The Wide-Band ERM Way out of crisis:

wide band of fluctuation (15%) a soft ERM on the way to monetary union

ERM-2 ERM-1 ceased to exist on 1 January 1999 with

the launch of the Euro. ERM-2 was created to

Host currencies of old EU members who cannot or do not want to join euro area: Denmark and the UK have derogations Only Denmark has entered the ERM-2 Sweden has no derogation but has declined to

enter the ERM-2 Host currencies of new EU members before

they are admitted into euro area

ERM Members

Current ERM-2 Members

Country Date of ERM 2 membership

Band of fluctuation

Denmark 1 Jan. 1999 ±2.25%

Estonia 27 June 2004 ±15%

Lithuania 27 June 2004 ±15%

Latvia 2 May 2005 ±15%

ERM-2 vs ERM-1

ECB explicitly allowed to suspend intervention

Automatic unlimited interventions

‘Normal’ (±2.25%) and ‘standard’ (±15%) bands

Margin explicitly set

Asymmetric, all parities defined vis a vis euro

Symmetric, no anchor currency

ERM-2ERM-1

Optimum Currency Areas

Optimum Currency Areas?

What currency, or exchange-rate arrangement, is optimal? For individual countries, groups of countries or

regions within a country What economic criteria should be used?

E.g.: California in the early 1990s

Is it optimal for California to use the US dollar?

The Economic Toolkit There are benefits and costs involved in adopting a common currency. The solution has to involve trading off these benefits.

In a Nutshell Benefits:

No transaction costs, no exchange-rate uncertainty

Decreasing with size of currency area Costs:

Economic and political diversity Loss of monetary and exchange rate instruments Increasing with size of currency area

OCA Theory Focus on the costs of common currency Especially on asymmetric shocks

What are they? What problems do they cause in currency unions? How can their effects be mitigated?

Example: A demand shock Real exchange rate, EP/P*, must depreciate to restore competitiveness Either prices fall or nominal exchange rate depreciates. If not: overproduction and unemployment

Symmetric Shock Same demand shock in two similar countries that share the same currency and,

therefore, exchange rate: No problem. The same real XR adjustment as before.

Asymmetric Shock Only one country is affected; countries share common currency: Problem! Country A’s real exchange rate must depreciate both vis-à-vis ROW and Country B

Asymmetric Shock Country A wants a depreciation. Country B is unhappy: depreciation would lead to excess demand and inflationary pressure.

Asymmetric Shock Country B wants no change. Country A is unhappy because of excess supply and unemployment.

Asymmetric Shock Common central bank considers preferences of both countries and allows partial depreciation Nobody is happy.

In the long, the problem is solved. How?

Asymmetric Shock

Prices decline in country A and rise in country B. Real exchange rate adjusts because of price adjustment. Equilibrium is restored in both countries through disinflation and recession in A and inflation and expansion in B.

Asymmetric Shock

Implications of Asymmetric Shocks Both countries affected adversely when they share

the same currency. Also the case when a symmetric shock creates

asymmetric effects (e.g. oil price effects on oil exporting and oil importing countries).

This is an unavoidable cost. Next questions:

what reduces the incidence of asymmetric shocks?

what makes it easier to cope with shocks when they occur?

Answer: six OCA criteria.

Six OCA criteria

Three economic criteria Labor Mobility (Mundell) Diversification (Kenen) Openness (McKinnon)

Three political criteria Fiscal risk-sharing Homogeneity of preferences Solidarity

Criterion 1 (Mundell): Labour Mobility

An OCA is an area within which labour moves easily (including across national borders).

Criterion 1 (Mundell): Labour Mobility

Labour moves from A to B The two supply curves shift Equilibrium is restored without disinflation/inflation.

Criterion 1 (Mundell): Labour Mobility In an OCA labour (and capital) moves easily, within

and across national borders. Caveats:

labour mobility is easy within national borders but difficult across borders (culture, language, legislation, welfare benefits, etc.)

capital mobility: difference between financial and physical capital; physical capital is less mobile than financial capital

with specialization of labor, skills may also matter; migrants may need retraining.

Criterion 2 (Kenen): Production Diversification OCA: countries whose production and

exports are widely diversified and of similar structure.

If production and exports are diversified and similar, there are few asymmetric shocks and each of them is likely to be of small concern.

Criterion 3 (McKinnon): Openness OCA: Countries which are very open to trade and

trade heavily with each other. Traded vs non-traded goods:

traded good: prices are set worldwide a small economy is price-taker, so the exchange

rate does not affect competitiveness. If all goods are traded, domestic goods prices must

be flexible and exchange rate does not matter for competitiveness.

Criterion 3 (McKinnon): Openness Depreciation makes exports less expensive and

imports more expensive If countries are very open to trade, they tend to use

a lot of imported goods in the production process Then, depreciation is ineffective:

Depreciation imports more expensive domestic prices rise.

Criterion 4: Fiscal Transfers

Countries that agree to compensate each other for adverse shocks form an OCA.

Transfers can act as an insurance that mitigates the costs of an asymmetric shock.

Transfers stimulate demand demand curve shifts back.

Transfers exist within national borders: implicitly through the welfare system (e.g.

unemployment benefits) explicitly in some federations.

Criterion 5: Homogeneity of Preferences Countries that share a wide consensus on

the way to deal with shocks form an OCA. Matters primarily for symmetric shocks:

prevalent when the Kenen criterion is satisfied. May also help for asymmetric shocks:

better understanding of partners’ actions encourages transfers.

Different interest groups enjoy political power in different countries.

Criterion 6: Solidarity

Countries that view themselves as sharing a common destiny better accept the costs of operating an OCA.

A common currency will always face occasional asymmetric shocks that result in temporary conflicts of interests

This calls for accepting such economic costs in the name of a higher purpose.

Very Product

Open differentiation (McKinon) (Kenen)

Low likelihood of asymmetric shocks

YES: NO: OCA Need adjusment

Labour

mobility (Mundell)

YES: NO: OCA need adjustnent

Flexible wages and prices

YES: NO: OCA need political

support

Homogeneity Transfers of Solidarity

preferences

A summary

Is Europe An OCA?Correlation of demand and supply shocks with Euro area

GER

FRA

ITA

BEL

NLD

HUN

PRTAUTFIN

EST

S

DKESP

POL

IRLROM

GRSVK

UKSVNCZE

LVALTU

-0,6

-0,4

-0,2

0

0,2

0,4

0,6

0,8

-0,2 0 0,2 0,4 0,6 0,8

supply shocks

dem

and

sh

ock

s

•Each point represents correlation between demand and supply shocks of particular country with the euro-zone average.•Source: Korhonen and Fidrmuc (2001)

Is Europe An OCA?

Is Europe An OCA?

Is Europe An OCA?

Is Europe An OCA?

Is Europe An OCA?

Little labor mobility within countries and intra-EU (cf. USA) EU countries generally open and diversified EU budget low (1% of GDP) and used for administration,

CAP, regional and structural funds, not to counter asymmetric shocks US: 1$ fall in state GDP compensated by 0.10-0.40$ increase in net

transfers

Glass half full or half empty

Is Europe An OCA?

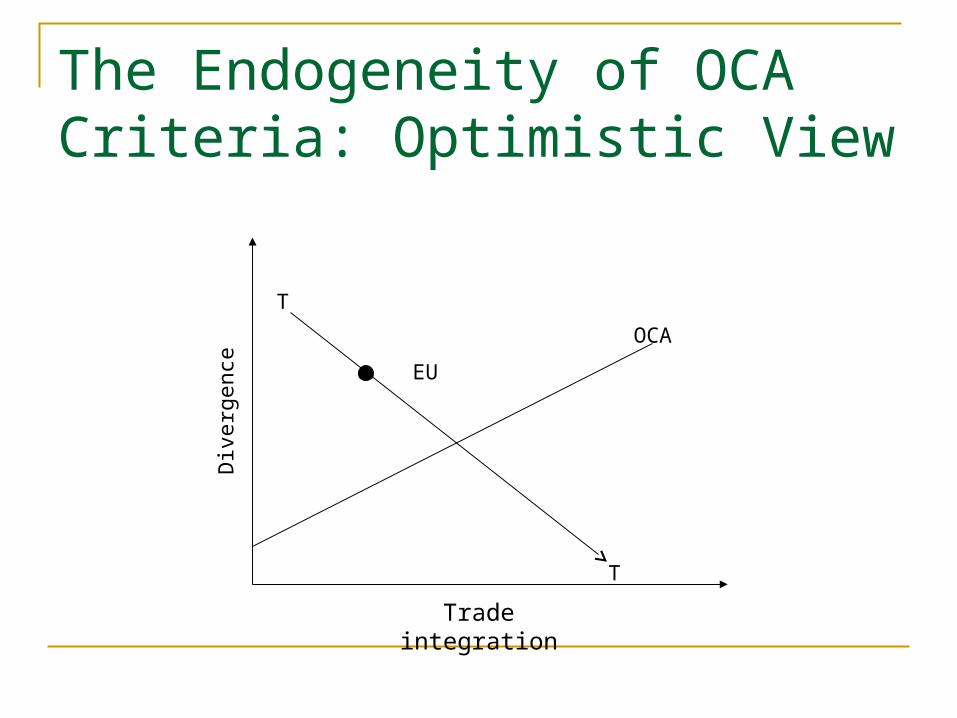

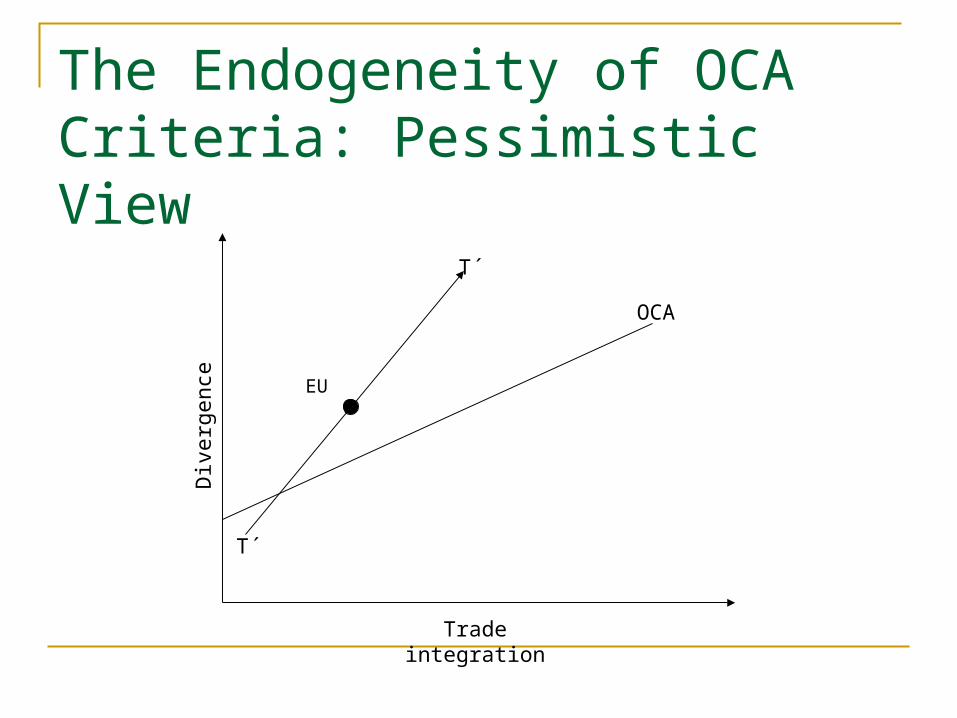

The Endogeneity of OCA Criteria

Living in a monetary union may help fulfil the OCA criteria over time.

Would the US be an OCA without a single common currency?

Will the existence of the euro area change matters too?

The Endogeneity of OCA Criteria: Two views Optimistic view (Frankel and Rose, European

Comission): Deepening trade integration intra-industry trade

and spillovers effects greater symmetry of shocks OCA criteria more likely fulfilled once common currency introduced

Pessimistic view (Krugman): Deepening trade integration greater

specialization greater vulnerability to country-specific shocks

No firm conclusion so far

The Endogeneity of OCA Criteria: Optimistic View

OCA

T

T

Div

erge

nce

Trade integration

EU

The Endogeneity of OCA Criteria: Pessimistic View

EU

T´

T´

OCA

Div

erge

nce

Trade integration

Trade

Eliminating exchange rate volatility by adopting a common currency raises trade: Estimates: +50-100% ‘border effect’ literature provides similar estimates.

EMU: preliminary evidence (Baldwin et al., 2008) Trade among EMU countries has increased by

approx. 5% compared to other countries.

Labour Markets

Mobility may not change much, but wages could become less sticky.

Two views: the virtuous circle: labour markets respond to

enhanced competition by becoming more flexible the hardening view: labour markets respond to

enhanced competition by increasing protective measures that raise stickiness.

The jury is still out.

Are the Other Criteria Endogenous? Transfers:

currently no support for more taxes to finance transfers.

Homogeneity of preferences: no expectation that it will change soon.

Solidarity: no expectation that it will change soon.

UK and EMU membership UK negotiated a formal opt-out from the obligation

to pursue EMU membership UK policy set out in 1997 UK committed in principle to join the EMU But would only join if there is a clear and

unambiguous economic case for joining To assess whether there is such a case, the

Treasury devised 5 economic tests If all 5 tests are passed, the final decision is to be

made by the British people in a referendum

UK Treasury’s Five Economic Tests1. Convergence in business cycles and economic

structures: There has been convergence but not yet enough, and important differences remain, especially in the housing market euro-area interest rates unlikely to be optimal for the UK.

2. Flexibility if problems emerge: UK labor market is more flexible than others, but still not sufficiently so.

3. Investment: UK membership in the euro-zone would boost FDI inflows to the UK.

UK Treasury’s Five Economic Test4. Financial Service and the City: Euro-zone

membership would strengthen the competitive position of the City.

5. Growth, stability and employment: Joining the EMU would allow the UK to benefit through increased trade, investment, competition ( lower prices) and productivity growth.

Treasury’s proposal: Joining now would not be in the national economic interest.

Source: HM Treasury, UK membership of the single currency: An assessment of the five economic tests, June 2003.

In the End

Monetary union is not only about economics. EU is not a perfect OCA a monetary union may function, at a cost.

The OCA criteria tell us where the costs will arise: labour markets and unemployment political tensions in presence of deep

asymmetric shocks.

European Monetary Union

The Long Road to Maastricht and to the Euro

The Maastricht Treaty

A firm commitment to launch the single currency by January 1999 at the latest.

Five convergence criteria for admission to the monetary union.

Formalization of central banking institutions.

Additional conditions mentioned (e.g. the excessive deficit procedure).

The Maastricht Convergence Criteria

Inflation: not to exceed by more than 1.5 per cent the average of

the three lowest rates among EU countries. Long-term interest rate:

not to exceed by more than 2 per cent the average interest rate in the three lowest-inflation countries.

ERM membership: at least two years in ERM without being forced to

devalue.

The Maastricht Convergence Criteria Budget deficit:

deficit less than 3 per cent of GDP. Public debt:

debt less than 60 per cent of GDP (or diminishing and approaching 60% at satisfactory pace)

Note: Fulfilment of criteria was observed on 1997 performance for decision in 1998.

The convergence criteria give little regard to standard OCA arguments

Interpretation of the Convergence Criteria: Inflation

Fear of allowing in unrepentant inflation-prone countries. Result: convergence in inflation rates before EMU entry

0.00

5.00

10.00

1991 1992 1993 1994 1995 1996 1997 1998

France Italy

Spain Germany

Belgium PortugalGreece average of three lowest + 1.5%

Interpretation of the Convergence Criteria: Long-Term Interest Rate It may be easy to bring inflation down in 1997

and then let go again. Long-term interest rates incorporate bond

markets’ expectations of future inflation. Requires convincing markets that inflation will

remain low also in the long term.

Interpretation of the Convergence Criteria: ERM Membership

Same logic as with the long-term interest rate: need to convince the markets.

Furthermore, maintaining a fixed XR for two years demonstrates commitment to strict monetary discipline

Interpretation of the Convergence Criteria: Budget Deficit and Debt (1) Historically, all big inflation episodes born out of runaway public deficits and debts.

Hence requirement that house is put in order before admission.

How were the ceilings chosen?: deficit: the German golden rule

Deficits should only finance infrastructure expenditure approx. 3% of GDP

debt: the 1991 EU average. Average many countries had more than 60% Several countries’ debt increased further after 1991

Interpretation of the Convergence Criteria: Budget Deficit and Debt (2) Problem No. 1: a few years of budgetary discipline do not

guarantee long-term discipline

excessive deficit procedure once in euro area.

Problem No. 2: deficit and debt ceilings are arbitrary.

The Debt and Deficit Criteria in 1997

Architecture of the monetary union

A Tour of the Acronyms

National Central Banks (NCBs) continue operating but with no monetary policy function.

A new central bank at the centre: the European Central Bank (ECB).

The European System of Central Banks (ESCB): the ECB and all EU NCBs (N=27).

The Eurosystem: the ECB and the NCBs of euro area member countries (N=16).

The System

How Does the Eurosystem Operate? Objectives:

what is it trying to achieve? Instruments:

what are the means available? Strategy:

how is the system formulating its actions?

Objectives (1)

The Maastricht Treaty’s Art. 105.1:‘The primary objective of the ESCB shall be to maintain price stability. Without prejudice to the objective of price stability, the ESCB shall support the general economic policies in the Community with a view to contributing to the achievement of the objectives of the Community as laid down in Article 2.’

Article 2: The objectives of European Union are a high level of employment and sustainable and non-inflationary growth.

In summary: fighting inflation is the absolute priority supporting growth and employment comes next.

Objectives (2)

Making the inflation objective operational: does the Eurosystem have a target?

It has a definition of price stability:“In the pursuit of price stability, the ECB aims at maintaining inflation rates below, but close to, 2% over the medium term.”

Leaves room for interpretation: how far below 2 per cent? what is the medium term?

Instruments (1)

Channels of monetary policy: longer run interest rates credit asset prices exchange rate.

These are all beyond central bank control. Instead it can control the very short-term interest

rate: European Over Night Index Average (EONIA). EONIA affects the channels through market

expectations.

Instruments (2)

The Eurosystem controls EONIA by establishing a ceiling, a floor and steering the market in-between.

The floor: the rate at which the Eurosystem accepts deposits (deposit facility).

The ceiling: the rate at which the Eurosystem stands ready to lend to banks (marginal lending facility).

In-between: weekly auctions (main refinancing facility).

EONIA & Co.

0

1

2

3

4

5

6

7

Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06

EONIA Deposit rate Marginal lending Main refinancing

Comparison With Other Strategies

The US Fed: legally required to achieve both price stability and

a high level of employment does not articulate an explicit strategy.

Inflation-targeting central banks (Czech Republic, Poland, Sweden, UK, etc.): announce a target (e.g. 2 per cent in the UK), a

margin (e.g. ±1%) and a horizon (2–3 years) compare inflation forecasts and target, and act

accordingly.

Independence and Accountability

Central banks should be independent: governments may be tempted to use the ‘printing

press’ to finance expenditure Misbehaving governments are eventually

punished by voters. What about central banks? Independence

removes them from such pressure. A democratic deficit?

Redressing the Democratic Deficit In return for their independence, central

banks should be accountable: to the public to elected representatives.

Examples: The Bank of England is given an inflation target by

the Chancellor. It is free to decide how to meet the target, but must explain its failures (the ‘letter’)

The US Fed must explain its policy to the Congress, which can vote to reduce the Fed’s independence.

The Eurosystem Weak Accountability The Eurosystem must report to the EU

Parliament. The Eurosystem’s President must appear

before the EU Parliament when requested, and does so every quarter.

But the EU Parliament cannot change the Eurosystem’s independence.

Inflation: Record so far

A difficult period:•oil shock in 2000•worldwide slowdown•September 11•stock market crash in 2002•Afghanistan, Iraq•Financial crisis since 2007

Euro Area Inflation

0

0.5

1

1.5

2

2.5

3

3.5

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

The Euro: Too Weak First, Then Too Strong?

Effective echange rate (1999Q1=100)

80

90

100

110

Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06

Growth record

Inflation Convergence and No Major Asymmetric Shocks

Fiscal Policy and the Stability and Growth Pact

The Fiscal Policy Instrument Fiscal policy: the only macroeconomic policy

instrument left at the national level in monetary union

Borrowing is a substitute for fiscal transfers: inter-temporal smoothing of shocks.

Yet, its effectiveness is questionable. Expectations (Ricardian equivalence):

deficit today higher tax tomorrow tax cut today may not be permanent

Slow implementation: agreement within government, approved by parliament, carried out by bureaucracy, taxes not retroactive.

Result: countercyclical actions can have procyclical effects.

Automatic vs Discretionary

Automatic stabilizers: tax receipts decline when the economy slows

down, and vice versa welfare spending rises when the economy slows

down, and vice versa no decision needed, so no lag: countercyclical

with immediate effect rule of thumb: deficit worsens by 0.5 per cent of

GDP when GDP growth declines by 1 per cent.

Automatic Stabilizers

Automatic vs Discretionary

Discretionary actions: a voluntary decision to change tax rates or spending.

Should Fiscal Policy be Subject to Collective Control? Yes, if national fiscal policies cause externalities. Income externalities via trade:

national business cycles spill-over to other countries via their impact on imports/exports

trade intensity increased by monetary union Borrowing cost externalities:

one common interest rate heavy borrowing capital inflows appreciation

of the euro

The Deficit Bias The track record of EU countries is not good.

EU public debt (% of GDP)

20

30

40

50

60

70

80

1970 1974 1978 1982 1986 1990 1994 1998 2002 2006

What is the Problem with the Deficit Bias?

Lack of fiscal discipline in parts of the euro area might concern financial markets and: raise borrowing costs: unlikely, markets can

distinguish among countries. More serious is the risk of default in one member

country: capital outflows and a weak euro pressure on other governments to help out pressure on the eurosystem to help out.

Answer to Default Risk: The No Bailout Clause The no-bailout clause:

Overdraft facilities or any other type of credit facility with the ECB or with the central banks of the Member States (hereinafter referred to as ‘national central banks’) in favour of Community institutions or bodies, central governments, regional, local or other public authorities, other bodies governed by public law, or public undertakings of Member States shall be prohibited, as shall the purchase directly from them by the ECB or national central banks of debt instruments. (Art. 101)

Summary: Should Fiscal Policy Independence be Limited? The arguments in favor of restrictions: serious externalities a bad track record.

The arguments against: Fiscal policy is the only remaining macroeconomic

instrument national governments know better economic

conditions at home. EU solution: Stability and growth pact

The Answer to Default Risk: Stability and Growth Pact

SGP: formal implementation of the Excessive Deficit Procedure (EDP) mandated by the Maastricht Treaty.

The EDP aims at preventing a relapse into fiscal indiscipline following entry in euro area.

The EDP makes permanent the 3 per cent deficit and 60 per cent debt ceilings and foresees fines.

Evolution of SGP: Original Pact: 1999 – November 2003 Limbo: November 2003 – March 2005 Adapted Pact: March 2005, in increase flexibility

How the Pact Works A limit on acceptable deficits: 3% of GDP A preventive arm

Aims at avoiding reaching the limit in bad years Calls for surpluses in good years

A corrective arm Aims at encouraging prompt action when deficit is above

limit Sanctions applied if limit repeatedly breached

Exceptional Circumstances

Negative growth or accumulated loss of output over a period of low growth exceptional

Taking account of ‘all relevant factors’ No specific definitions

The Procedure When the 3% is not respected:

the Commission submits a report to ECOFIN ECOFIN decides whether the deficit is excessive if so, ECOFIN issues recommendations with an

associated deadline the country must then take corrective action failing to do so and maintaining deficit below 3 per

cent triggers a recommendation by the Commission

ECOFIN decides whether to impose a fine the whole procedure takes about two years.

The Fine Schedule

The fine starts at 0.2 per cent of GDP and rises by 0.1 per cent for each 1 per cent of excess deficit.

How is the Fine Levied

The sum is withheld from payments from the EU to the country (CAP, Structural and Cohesion Funds).

The fine is imposed every year when the deficit exceeds 3 per cent.

The fine is initially considered as a deposit: if the deficit is corrected within two years, the

deposit is returned if it is not corrected within two years, the deposit

turns into a fine.

Issues Raised by the Pact Does the Pact impose procyclical fiscal policies?:

budgets deteriorate during economic slowdowns reducing the deficit in a slowdown may further

depress growth a fine both worsens the deficit and has a

procyclical effect. The solution: a budget close to balance or in surplus

in normal years.

The Early Years (Before Slowdown)

-6 -4 -2 0 2 4 6 8

Spain

Portugal

Netherlands

Luxembourg

Italy

Ireland

Greece

Germany

France

Finland

Belgium

Austria

2001 1998

The November 2003 decision

France

-4

-3

-2

-1

0

1

2

1999 2000 2001 2002 2003 2004 2005 2006

Germany

-4

-3

-2

-1

0

1

2

1999 2000 2001 2002 2003 2004 2005 2006

The November 2003 decision

ECOFIN decides to suspend the Pact The European Court of Justice:

recognizes the right of ECOFIN to interpret the pact

rules that the suspension decision is illegal The governments commit to re-examine the

pact

The March 2005 decision

Principles of the pact of upheld 3 % deficit limit fines, to be decided by ECOFIN

Flexibility introduced Will take into account debt level Will take into account growth over recent years

And now?