Fixed-Income and FX Weekly

Market outlook

Local assets extend losses. Local rates sold-off 3-4bps but real-rate Udibonos

rallied 6bps, while the peso lost 1.7% to 18.18 per dollar

Fed minutes and global growth concerns in the spotlight. China data during

the weekend was lower than expected, keeping markets doubting whether

financial risks (and overleverage) can be handled appropriately by authorities

without making a big dent on growth. Downside risks in other regions are also

present, with the BoE and BoJ maintaining a dovish bias. The G7 meeting in

Japan by the end of this week should be mostly concerned over the possible tools

that could be used to address this global scenario. In contrast and in the US, early

2Q16 data signal a rebound in GDP growth. In this context, investors are

questioning themselves how much is the fragile global backdrop likely to affect

the Fed in terms of their timing for rate hikes, with markets incorporating a

relatively low probability for a June (4%) or July (17.4%) move. The main event

this week will be the FOMC minutes to gauge the possibility of a sooner-than-

expected hike, with more hawkish comments by their members after the latest

decision. Also in the US, Empire and Philly surveys, housing data, and April CPI

and industrial production. In the Eurozone, ECB minutes, trade balance, April

CPI and March construction. In the UK, retail sales, and unemployment, while

Japan will release industrial production and 1Q16 GDP. Central bank meetings

include Colombia, South Africa, and Indonesia. In Mexico, Banxico’s minutes

after a neutral decision, final 1Q16 GDP, and March IGAE will be published

Fixed-Income

Supply – On Tuesday, the MoF will auction 1-, 3-, and 6-month zero-coupon

Cetes, the 5-year Mbono (Jun’21), and the 10-year real rate Udibono (Dec’25)

Demand – Foreigners’ holdings in Mbonos totaled MXN 1.632 trillion (US$ 91.7

billion), a market share equal to 59.5%, as of May 4th. Short positions in Mbono

Dec’24 located at MXN 5.5 billion from previous MXN 9.6 billion

Technicals – Mbono Dec’24 and 10-year UST kept a rising trend as market

participants where cautious over risk positions closing at 411bps from 401bps

Foreign exchange

Market positioning and flows – Net peso shorts were increased relatively

strongly, ending at US$ 1.2 billion. Mutual fund sold US$ 381 million in EM, its

first outflow in four weeks and explained by strong pressures in Asia

Technicals –The vol curve had a modest relief after the previous week strong

increase, with an average fall of 24bps up to the one-year tenor. USD/MXN

adjusted strongly upward during the past three weeks and is trading around 18.20,

not seen since the end of February

May 16, 2016 www.banorte.com www.ixe.com.mx

Gabriel Casillas Chief Economist and Head of Research [email protected]

Alejandro Padilla Head Strategist – Fixed-Income and FX [email protected]

Juan Carlos Alderete, CFA FX Strategist [email protected]

Santiago Leal Singer Fixed-Income and FX Analyst [email protected]

Banorte-Ixe FI/FX Strategy Mexico

Fixed-Income Market dynamics.…………………….pg. 2 Supply………………………………….pg. 3 Demand………………………………..pg. 4 Technicals……………………………..pg. 6 Recommendations…………………...pg. 8

Foreign exchange Market dynamics……………………..pg. 9 Market positioning and flows……....pg. 10 Technicals…………………………...pg. 11 Recommendations………………….pg. 13

Recommendations Fixed-Income We recommend waiting for better

entry levels for long positions in the belly of the Mbonos curve, as local rates are likely to trade sidelines with relevant factors ahead that could undermine risk premium

FX Maintain a short USD/MXN trading

bias (avoiding directional positions) on some signs of overshooting, such as lagging against oil

We expect higher USD selling interest above 18.00 pesos

Weekly estimated range between 17.90 to 18.40 per dollar

Document for distribution among the general public

2

Fixed-Income dynamics In line with our expectations, the Mexican market observed a profit taking

process along last week in tandem with higher risk premium in the global

spectrum. Local bonds registered a 3-4bps sell-off in the second week of May,

mainly in Mbonos and TIIE-IRS, but gains of 6bps in mid- and long-term linkers

(Udibonos). In this regard, Mbono Dec’24 finished at 5.81% (+2bps) and Mar’26 at

5.91% (+1bps)

Mbonos performance IRS (28-day TIIE) performance

Maturity date Yield to maturity

13/May/16 Weekly change

(bps) YTD (bps)

Jun'16 3.81 1 31

Dec'16 3.94 2 30

Jun'17 4.02 0 8

Dec'17 4.00 -5 -4

Jun’18 4.54 10 6

Dec'18 4.76 8 -2

Dec'19 5.10 7 -13

Jun'20 5.20 4 -22

Jun'21 5.41 5 -30

Jun'22 5.58 4 -32

Dec'23 5.75 2 -30

Dec'24 5.81 2 -29

Mar’26 5.91 1 -34

Jun'27 6.09 4 -33

May'29 6.25 2 -30

May'31 6.41 5 -25

Nov’34 6.52 3 -30

Nov'36 6.57 3 -32

Nov'38 6.61 1 -30

Nov'42 6.63 1 -31

Source: Valmer

Maturity date Yield to maturity

13/May/16 Weekly change

(bps) YTD (bps)

3-month (3x1) 4.14 3 55

6-month (6x1) 4.24 6 52

9-month (9x1) 4.36 7 50

1-year (13x1) 4.48 9 53

2-year (26x1) 4.72 8 29

3-year (39x1) 4.95 9 15

4-year (52x1) 5.16 6 -6

5-year (65x1) 5.37 7 -17

7-year (91x1) 5.73 3 -30

10-year (130x1) 6.09 2 -31

20-year (260x1) 6.75 1 -28

Source: Bloomberg

Mbonos curve at different closing dates %

Long-term reference Mbono Dec’24 %

Source: Bloomberg Source: Valmer

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

0 2 4 6 8

10

12

14

16

18

20

22

24

26

28

30

13-May-16 6-May-16 15-May-15

Years1Y 5Y 10Y 20Y 30Y

4.3

4.8

5.3

5.8

6.3

6.8

7.3

7.8

8.3

Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

3

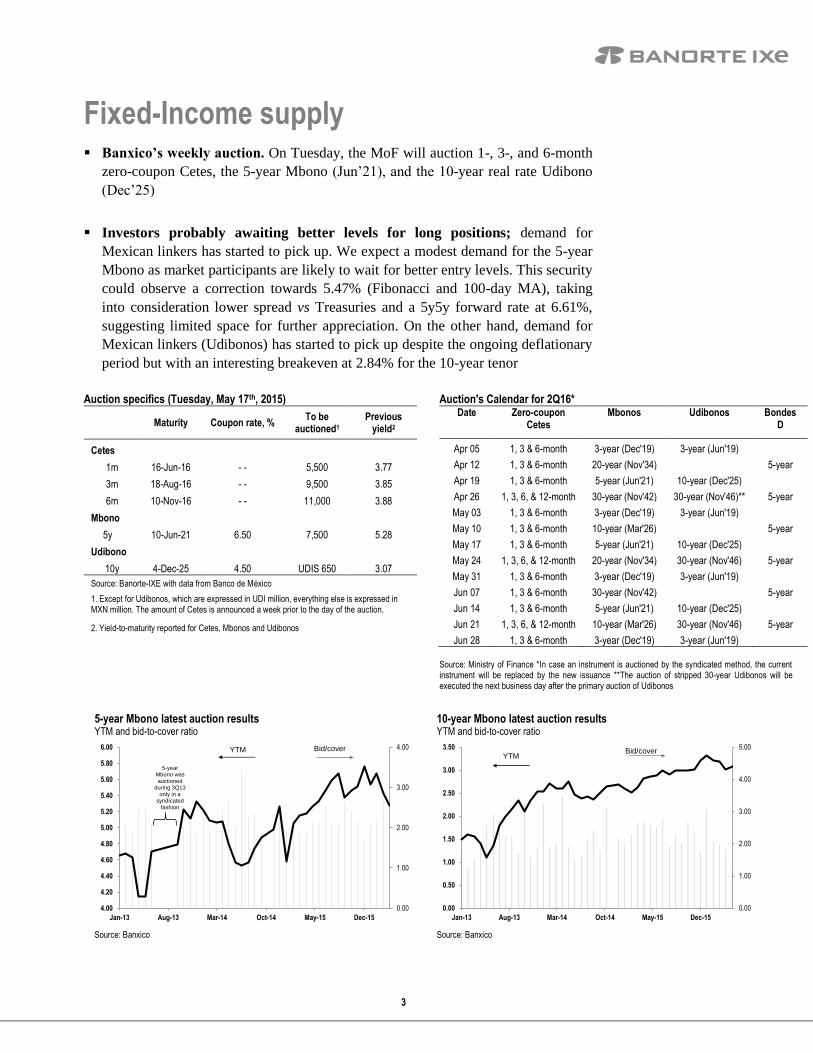

Fixed-Income supply Banxico’s weekly auction. On Tuesday, the MoF will auction 1-, 3-, and 6-month

zero-coupon Cetes, the 5-year Mbono (Jun’21), and the 10-year real rate Udibono

(Dec’25)

Investors probably awaiting better levels for long positions; demand for

Mexican linkers has started to pick up. We expect a modest demand for the 5-year

Mbono as market participants are likely to wait for better entry levels. This security

could observe a correction towards 5.47% (Fibonacci and 100-day MA), taking

into consideration lower spread vs Treasuries and a 5y5y forward rate at 6.61%,

suggesting limited space for further appreciation. On the other hand, demand for

Mexican linkers (Udibonos) has started to pick up despite the ongoing deflationary

period but with an interesting breakeven at 2.84% for the 10-year tenor

Auction specifics (Tuesday, May 17th, 2015) Auction's Calendar for 2Q16*

Maturity Coupon rate, %

To be auctioned1

Previous yield2

Cetes

1m 16-Jun-16 - - 5,500 3.77

3m 18-Aug-16 - - 9,500 3.85

6m 10-Nov-16 - - 11,000 3.88

Mbono

5y 10-Jun-21 6.50 7,500 5.28

Udibono

10y 4-Dec-25 4.50 UDIS 650 3.07

Source: Banorte-IXE with data from Banco de México

1. Except for Udibonos, which are expressed in UDI million, everything else is expressed in MXN million. The amount of Cetes is announced a week prior to the day of the auction.

2. Yield-to-maturity reported for Cetes, Mbonos and Udibonos

Date Zero-coupon Cetes

Mbonos Udibonos Bondes D

Apr 05 1, 3 & 6-month 3-year (Dec'19) 3-year (Jun'19)

Apr 12 1, 3 & 6-month 20-year (Nov'34)

5-year

Apr 19 1, 3 & 6-month 5-year (Jun'21) 10-year (Dec'25)

Apr 26 1, 3, 6, & 12-month 30-year (Nov'42) 30-year (Nov'46)** 5-year

May 03 1, 3 & 6-month 3-year (Dec'19) 3-year (Jun'19)

May 10 1, 3 & 6-month 10-year (Mar'26)

5-year

May 17 1, 3 & 6-month 5-year (Jun'21) 10-year (Dec'25)

May 24 1, 3, 6, & 12-month 20-year (Nov'34) 30-year (Nov'46) 5-year

May 31 1, 3 & 6-month 3-year (Dec'19) 3-year (Jun'19)

Jun 07 1, 3 & 6-month 30-year (Nov'42)

5-year

Jun 14 1, 3 & 6-month 5-year (Jun'21) 10-year (Dec'25)

Jun 21 1, 3, 6, & 12-month 10-year (Mar'26) 30-year (Nov'46) 5-year

Jun 28 1, 3 & 6-month 3-year (Dec'19) 3-year (Jun'19)

Source: Ministry of Finance *In case an instrument is auctioned by the syndicated method, the current instrument will be replaced by the new issuance **The auction of stripped 30-year Udibonos will be executed the next business day after the primary auction of Udibonos

5-year Mbono latest auction results YTM and bid-to-cover ratio

10-year Mbono latest auction results YTM and bid-to-cover ratio

Source: Banxico Source: Banxico

0.00

1.00

2.00

3.00

4.00

4.00

4.20

4.40

4.60

4.80

5.00

5.20

5.40

5.60

5.80

6.00

Jan-13 Aug-13 Mar-14 Oct-14 May-15 Dec-15

YTM Bid/cover

5-year Mbono was auctioned

during 3Q13 only in a

syndicated fashion

0.00

1.00

2.00

3.00

4.00

5.00

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Jan-13 Aug-13 Mar-14 Oct-14 May-15 Dec-15

YTMBid/cover

4

Fixed-Income demand Foreigners’ holdings on Cetes on a fresh multiyear low once again. Holdings in

these assets were at MXN 274 billion (39.8% of the total amount outstanding) as of

May 4th from MXN 314bn in the previous week. The figure reached MXN 272bn

(39.7%) on April 28th, a new low since Februray 2012. Its 2015-minimum was

MXN 375bn with a year-max at MXN 639bn (62.7%)

…and remain strongly exposed in Mbonos. These holdings totaled MXN 1.632

trillion (US$ 91.7 billion), a market share equal to 59.5%, from MXN 1,631 trillion

the previous week and MXN 1.571 trillion (60.5%) as 2015-high

Local institutional investors heavily invested in Udibonos. These type of

investors continue with strong holdings in inflation-linked Udibonos (around 67%

of total amount outstanding), and Bondes D (46%)

Government issuance by type of instrument Total amount of US$325 billion, % of total

Mbonos holdings by type of investor Total amount of US$154 billion, % of total

Source: Banxico Source: Banxico

Zero-coupon Cetes12%

Bondes D21%

Udibonos4%

Mbonos47%

IPAB bonds16%

Banks4%

Foreign investors59%

Institutional Investors

22%

Other locals15%

Government bond holdings by type of investor

US$ billion unless indicated, data as of 05/04/2016

Zero-coupon Cetes 39 40% 11% 16% 3% 8% 23%

Floating-rate Bondes D 68 0% 6% 38% 1% 11% 43%

Real-rate Udibonos 13 9% 46% 6% 15% 3% 21%

Fix ed-rate Mbonos 154 60% 15% 4% 2% 4% 15%

Source: Banorte-Ix e w ith data from Banx ico

% of total amount outstandingTotal

amount

outstanding

Foreign

investors

Pension

funds

Mutual

funds

Insurance

companiesBanks Other

Foreign investors holdings of government bonds

US$ billion

05/04/2016Previous

Week Difference 04/27/2016 Difference

Zero-coupon Cetes 15.4 17.6 -2.3 25.4 -10.0

Floating-rate Bondes D 0.1 0.1 0.0 0.1 0.0

Real-rate Udibonos 1.2 1.2 0.0 1.2 0.0

Fix ed-rate Mbonos 91.7 91.6 0.1 87.4 4.3

Source: Banorte-Ix e w ith data from Banx ico

Percentage of total amount outstanding

05/04/2016Previous

Week Difference 04/27/2016 Difference

Zero-coupon Cetes 39.8% 43.6% -3.8% 51.8% -12.0%

Floating-rate Bondes D 0.2% 0.2% 0.0% 0.2% 0.0%

Real-rate Udibonos 9.0% 9.0% 0.0% 9.6% -0.6%

Fix ed-rate Mbonos 59.5% 59.7% -0.2% 59.5% 0.0%

Source: Banorte-Ix e w ith data from Banx ico

DTMTotal amount

outstanding

Local

Banks

Foreign

investors

Pension and

Mutual fundsOther

Jun'16 5.7 17% 14% 27% 42%

Dec'16 6.8 3% 74% 5% 19%

Jun'17 6.2 6% 80% 2% 11%

Dec'17 9.5 3% 65% 8% 25%

Jun'18 11.5 18% 64% 8% 10%

Dec'18 14.9 1% 65% 6% 28%

Dec'19 8.5 7% 43% 19% 31%

Jun'20 6.9 0% 51% 9% 39%

Jun'21 13.1 6% 66% 4% 23%

Jun'22 6.2 1% 78% 16% 5%

Dec'23 5.3 1% 73% 23% 4%

Dec'24 14.1 1% 70% 18% 11%

Mar'26 3.6 0% 68% 24% 8%

Jun'27 5.0 1% 61% 30% 8%

May'29 5.5 0% 62% 29% 9%

May'31 7.9 1% 42% 49% 8%

Nov'34 4.5 3% 17% 73% 7%

Nov'36 3.6 1% 34% 56% 9%

Nov'38 5.9 1% 51% 42% 6%

Nov'42 8.9 1% 63% 32% 4%

Total 153.5 4% 59% 20% 17%

Source: Banxico

US$ billion and %, data as of May /5/16

Mbonos holdings by type of investor

5

Fixed-Income demand – Primary dealers Total short positions moderating levels after witnessing high ranges following

risk aversion over local assets. Short positions in Mbonos are located at MXN

72.7 bn. (US$ 4.0bn.) from MXN 79.4 bn. (US$ 4.4 bn.) the previous week

Likewise, position over Dec’24 falls from 1-month high. Figure for the 10-year

tenor set at MXN 5.5 bn. (US$ 301 mn.) from previous MXN 9.8 bn. (US$ 538

mn.). The 2015-average finished at MXN 5.9 bn. vs. MXN 4.6 bn. averaged

through 2014; during 2016 has averaged 5.3 bn.

Market makers' short positions on Mbono Dec'24 MXN billion

Market makers' short positions on Mbono Nov’42 MXN billion

Source: Banxico Source: Banxico

Market makers' short position on Mbonos US$ million

Maturity Date Total amount

outstanding as of 13-May-16

13-May-16 12-May-16 6-May-16 15-Apr-16 6-month MAX 6-month MIN

Jun'16 5,538 97 97 0 148 459 0

Dec'16 6,155 399 399 603 585 951 386

Jun'17 5,914 89 89 123 116 212 0

Dec'17 7,506 983 1,053 840 722 1,225 207

Jun'18 11,107 2 9 33 0 319 0

Dec'18 14,684 243 229 402 0 475 0

Dec'19 8,526 300 330 175 1 337 0

Jun'20 7,021 239 194 82 193 466 4

Jun'21 12,971 187 179 67 70 783 0

Jun'22 6,119 126 109 136 142 431 49

Dec'23 5,176 5 0 13 20 177 0

Dec'24 13,892 301 304 538 374 609 61

Mar’26 3,675 246 265 517 271 532 0

Jun'27 4,889 12 11 2 52 219 0

May'29 5,471 23 22 12 14 188 0

May'31 7,700 116 121 179 150 287 0

Nov'34 4,470 1 1 1 3 93 0

Nov'36 3,521 87 121 126 124 170 0

Nov'38 5,769 14 13 21 93 217 11

Nov'42 8,777 527 498 502 182 527 55

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Apr-10 Mar-11 Mar-12 Feb-13 Feb-14 Jan-15 Jan-16

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Apr-12 Sep-12 Feb-13 Jul-13 Dec-13 May-14 Oct-14 Mar-15 Aug-15 Jan-16

6

Fixed-Income technicals Foreign investors continue reducing exposure in Cetes following a negative

FX-adjusted carry. Spreads between Cetes and implied forward rates: 1-month -

27bps from -45bps last week, 3-month -30bp from -39bps, 6-month at -23bps from

-19bps, and the 1-year tenor at -8bps from -3bps

Market participants will pay attention to Banxico’s minutes this week,

together with Fed and ECB information. In our view, minutes from Banxico’s

last decision are likely to confirm the possibility of hiking at the same time or even

before the Federal Reserve if necessary during this 2016. This situation explains the

52bps of implied hikes that the Mexican yield curve prices in for year-end vs 13bps

in the U.S.

Cumulative implied moves in Banxico’s repo rate Basis points, using TIIE-MexDer futures

Source: Banorte-Ixe with data from MexDer

As investors remained cautious over risk positions the 10-year Mexico-U.S.

spread carry on through a rising path. The figure scored two weeks in a steady

increase, closing at 411bps from 401bps with a 12-month average at 390bps, a

mark close to the begging of the latter pick-up

Correlation increases but lingers in low levels. The 3-month reading increased to

+39% from +22% the previous week

Mbono Dec’24 and 10-year UST spread Basis points

Mexico and US 10-year bonds correlation 3-month moving correlation

Source: Bloomberg Source: Banorte-Ixe with data from Bloomberg

Spread between Cetes and Implied Forward Rates

Basis Points

Tenor Actual Prev ious Previous 6-month 6-month 6-month

16-May-16 Week Month Avg Max Min

1-month -27 -45 -54 10 93 -96

3 months -30 -39 -22 18 87 -45

6 months -23 -19 -8 23 71 -23

12 months -8 -1 0 18 38 -8

Source: Banorte-Ixe with data from Valmer and Bloomberg3

19

52

0

10

20

30

40

50

60

2Q16 3Q16 4Q16

250

300

350

400

450

500

Jan-12 Aug-12 Mar-13 Oct-13 May-14 Dec-14 Jul-15 Feb-16

-1.0

-0.8

-0.5

-0.3

0.0

0.3

0.5

0.8

1.0

Apr-10 Mar-11 Feb-12 Jan-13 Dec-13 Nov-14 Oct-15

Strong positive correlation

Strong negative correlation

Low correlation

7

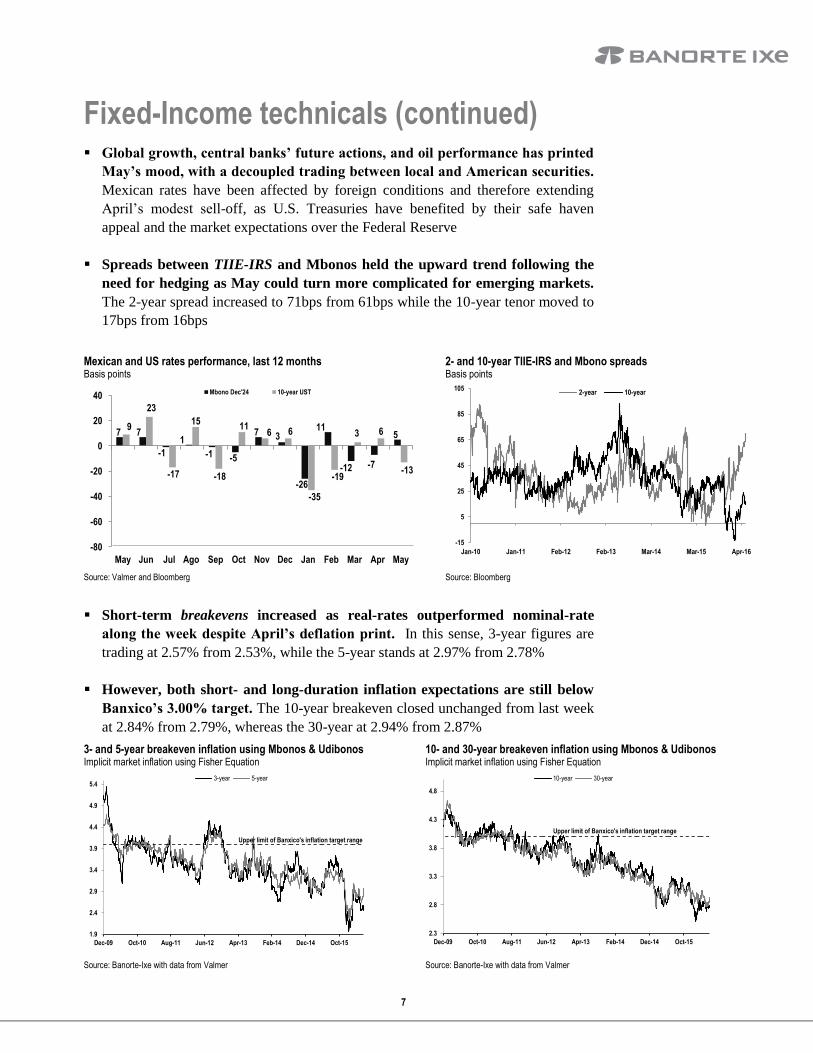

Fixed-Income technicals (continued) Global growth, central banks’ future actions, and oil performance has printed

May’s mood, with a decoupled trading between local and American securities.

Mexican rates have been affected by foreign conditions and therefore extending

April’s modest sell-off, as U.S. Treasuries have benefited by their safe haven

appeal and the market expectations over the Federal Reserve

Spreads between TIIE-IRS and Mbonos held the upward trend following the

need for hedging as May could turn more complicated for emerging markets.

The 2-year spread increased to 71bps from 61bps while the 10-year tenor moved to

17bps from 16bps

Mexican and US rates performance, last 12 months Basis points

2- and 10-year TIIE-IRS and Mbono spreads Basis points

Source: Valmer and Bloomberg Source: Bloomberg

Short-term breakevens increased as real-rates outperformed nominal-rate

along the week despite April’s deflation print. In this sense, 3-year figures are

trading at 2.57% from 2.53%, while the 5-year stands at 2.97% from 2.78%

However, both short- and long-duration inflation expectations are still below

Banxico’s 3.00% target. The 10-year breakeven closed unchanged from last week

at 2.84% from 2.79%, whereas the 30-year at 2.94% from 2.87%

3- and 5-year breakeven inflation using Mbonos & Udibonos Implicit market inflation using Fisher Equation

10- and 30-year breakeven inflation using Mbonos & Udibonos Implicit market inflation using Fisher Equation

Source: Banorte-Ixe with data from Valmer Source: Banorte-Ixe with data from Valmer

7 7

-1

1

-1 -5

7 3

-26

11

-12 -7

59

23

-17

15

-18

116 6

-35

-19

3 6

-13

-80

-60

-40

-20

0

20

40

May Jun Jul Ago Sep Oct Nov Dec Jan Feb Mar Apr May

Mbono Dec'24 10-year UST

-15

5

25

45

65

85

105

Jan-10 Jan-11 Feb-12 Feb-13 Mar-14 Mar-15 Apr-16

2-year 10-year

1.9

2.4

2.9

3.4

3.9

4.4

4.9

5.4

Dec-09 Oct-10 Aug-11 Jun-12 Apr-13 Feb-14 Dec-14 Oct-15

3-year 5-year

Upper limit of Banxico's inflation target range

2.3

2.8

3.3

3.8

4.3

4.8

Dec-09 Oct-10 Aug-11 Jun-12 Apr-13 Feb-14 Dec-14 Oct-15

10-year 30-year

Upper limit of Banxico's inflation target range

8

Fixed-Income trade recommendations Mexican curve attractive within the EM spectrum but we suggest as a tactical

strategy to underweight positions and wait for better entry levels for long

directional strategies in mid- and long-term Mbonos. The local yield curve

remains one of the most attractive alternatives in emerging markets, taking into

consideration a still steep slope (2/10 at 137bps), an appealing risk premia vis-à-vis

its fundamentals (10-year spread at 411bps vs 12-month mean at 390bps), and a

monetary normalization process already priced in (5y5y forward rate at 6.61%).

However, despite our expectation for a further flattening bias in the next 2 years

(positive for carry trade), we suggest appropriate waiting for better entry levels in

the long belly of the Mbonos curve. It is our take that the short-end will remain

pressured in tandem with deteriorated dynamics in the FX market since the end of

April. In our view, the 53bps of implied hikes priced in the curve for year-end are

attainable, with low probability of decreasing going forward. On the other hand, we

acknowledge the existence of an attractive valuation in mid- and long-term

securities, albeit with limited space for further appreciation, at least in coming

weeks. In this regard, we recommend as a tactical strategy holding an underweight

stance and waiting for better entry levels for long positions in the belly of the

Mbonos curve. For further details about our views on the market and forecasts

please refer to our research note: “Fixed-Income, FX and Commodities Quarterly –

2Q16 Outlook” <pdf>, published on April 19, 2016

9

FX dynamics

Mexican peso weak despite increase in oil. The MXN was the third worst among

EM despite a pick-up in oil prices, losing 1.7% to 18.18 per dollar

Dollar extends gains. Weak data in several regions but positive surprises in the US

gave the currency a lift against G10, with all lower except NOK and led by JPY

and SEK (-1.4% each)

Foreign Exchange market levels and historical returns

FX performance Against USD

Close at 13/05/16

Daily Change

(%)1

Weekly change

(%)1

Monthly change

(%)1

YTD1

(%)

Emerging Markets Brazil USD/BRL 3.53 -1.2 -0.7 -0.8 12.3

Chile USD/CLP 690.69 -0.8 -3.8 -2.9 2.6

Colombia USD/COP 2,992.48 -1.5 -1.2 0.5 6.1

Peru USD/PEN 3.34 -0.3 -0.7 -2.0 2.3

Hungary USD/HUF 278.99 -0.7 -1.2 -1.2 4.1

Malaysia USD/MYR 4.03 -0.1 -0.7 -3.9 6.5

Mexico USD/MXN 18.18 -1.2 -1.7 -4.1 -5.4

Poland USD/PLN 3.90 -0.6 -0.4 -2.5 0.5

Russia USD/RUB 65.45 -0.8 1.1 1.3 11.9

South Africa USD/ZAR 15.39 -2.5 -3.3 -5.5 0.5

Developed Markets

Canada USD/CAD 1.29 -0.7 -0.2 -1.0 6.9

Great Britain GBP/USD 1.44 -0.6 -0.4 1.1 -2.5

Japan USD/JPY 108.67 0.3 -1.4 0.6 10.6

Eurozone EUR/USD 1.13 -0.6 -0.9 0.3 4.1

Norway USD/NOK 8.20 -0.8 0.1 0.4 7.9

Denmark USD/DKK 6.58 -0.6 -0.8 0.3 4.4

Switzerland USD/CHF 0.98 -0.5 -0.3 -0.8 2.8

New Zealand NZD/USD 0.68 -0.7 -0.9 -2.2 -0.9

Sweden USD/SEK 8.25 -0.8 -1.4 -1.4 2.3

Australia AUD/USD 0.73 -0.8 -1.4 -5.1 -0.3

1. Positive (negative) changes mean appreciation (depreciation) of the corresponding currency against the USD.

%

Source: Bloomberg Source: Bloomberg

USD/MXN Last 12 months

USD/MXN – intraday Last 30 trading days

Source: Bloomberg Source: Bloomberg, Banorte-Ixe

YTDWeekly

-0.4

-0.9

-1.4

-1.4

-0.3

-0.9

-0.8

-0.2

0.1

-1.4

-2.5

-0.9

-0.3

2.3

2.8

4.1

4.4

6.9

7.9

10.6

-25 -20 -15 -10 -5 0 5 10 15 20 25

GBP

NZD

AUD

SEK

CHF

EUR

DKK

CAD

NOK

JPY

-1.7

-3.3

-0.4

-0.7

-3.8

-1.2

-1.2

-0.7

1.1

-0.7

-5.4

0.5

0.5

2.3

2.6

4.1

6.1

6.5

11.9

12.3

MXN

ZAR

PLN

PEN

CLP

HUF

COP

MYR

RUB

BRL

14.2

14.7

15.2

15.7

16.2

16.7

17.2

17.7

18.2

18.7

19.2

May-15 Aug-15 Nov-15 Feb-16 May-1616.9

17.1

17.3

17.5

17.7

17.9

18.1

18.3

18.5

10-Apr-2016 15-Apr-2016 21-Apr-2016 28-Apr-2016 4-May-2016 11-May-2016

30D Min / Psychological= 17.05 / 17.00

Fibonacci = 17.74

Fibonacci / Last year's close = 17.22 / 17.21

100D MA= 17.87

Fibonacci= 18.39

200D MA= 17.31

Psychological= 18.00

150D MA and Psychological= 17.50

Support= 17.62

30D Max= 18.20

Psychological= 18.50

10

FX positioning and flows MXN shorts surge higher. The net short was increased by US$ 901 million after

reaching its lowest level since October 2015 last week, the latest moment when the

position tried to flip to net long, ending at US$ 1.2 billion

First increase in USD positions in nine weeks. Global USD net shorts were

reduced by US$ 368 million to end at a still relatively high level of US$ 5.5 billion.

This was mainly explained by a hefty reduction in AUD longs of US$ 1 billion and

higher MXN shorts, as explained above. All other currencies were purchased, led

by GBP (+US$ 688 million) and CAD (+US$ 438 million)

Asian outflows impact overall EM performance. Mutual funds sold US$ 381

million in EM, the first outflow in four weeks amid an increase in market volatility.

Both fixed-income and equities were lower, with sales in the latter at US$ 248

million given a decrease of US$ 325 million in Asia. Bonds registered their first

outflow since the week ended March 2. In Mexico, fixed-income inflows were

barely positive at US$ 1.7 million, while equities picked up modestly to US$ 24

million

IMM positioning in USD/MXN futures Negative = net long in MXN

IMM positioning by currency* Billion dollars

Source: CME, Banorte-Ixe * Positive: Net long in the corresponding currency Source: CME, Banorte-Ixe

Foreign portfolio flows into Mexico Accumulated during the last 12M, million dollars

Net foreign portfolio flows by region* Weekly, million dollars

* Including only mutual funds’ investments Source: EPFR Global, Banorte-Ixe Source: EPFR Global, Banorte-Ixe

13.0

14.0

15.0

16.0

17.0

18.0

19.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

Feb-15 Jun-15 Oct-15 Feb-16

USD/MXN

Net positions (USD bn)

-3.1 -3.0

-1.3

0.6 0.81.8

2.8

6.8

-15

-10

-5

0

5

10

15

EUR GBP MXN NZD CHF CAD AUD JPY

3-May-16 10-May-16

-2,500

-2,100

-1,700

-1,300

-900

-500

-100

300

700

1,100

1,500

1,900

2,300

-4,500

-3,700

-2,900

-2,100

-1,300

-500

300

1,100

1,900

2,700

3,500

4,300

may-15 jul-15 sep-15 nov-15 ene-16 mar-16 may-16

Equities

Fixed Income232

297

146

48

76

-477

2

17

-600 -500 -400 -300 -200 -100 0 100 200 300 400

Latam

EM Asia

EM Europe

ME and Africa

May-11-16 May-04-16

11

FX technicals USD/MXN testing February-end highs. The upward correction continued, with

the peso reaching up to 18.20 on an intraday basis, a level not seen since the end of

February after consolidating since then with a strong resistance at 18.00 per dollar

MXN correlation with commodities strengthens. Despite a slight reduction in

MXN correlations with other currencies, the most important move was the increase

with the GSCI and gold, with not only oil but broad metals on the spotlight and

observing significant moves. Our base-case remains that correlations should remain

broadly high. Intraday volatility has picked up in the past two weeks and although

a more stable external environment could reduce correlations somewhat, we still

see a plethora of factors of a global nature as the main drivers of market trends

Slight reversal in implied volatilities. After last week’s strong increase, the vol.

curve moderated as it decreased 24bps on average up to the one-year tenor. The 1M

measure outperformed as it fell by 43bps to 13.4%, while the two- and three-

month measures decreased around 30bps. The spread against historicals tightened,

with the former at 8bps and the latter at 14bps, with the strongest catch-up in

market measures signaling an adjustment towards fair values

USD/MXN – Moving averages Last 120 trading days

USD/MXN – Fibonacci retracement Last 12 months

Source: Bloomberg Source: Bloomberg

USD/MXN – 1-month correlation with other currencies* Based on daily percentage changes

USD/MXN – 1-month correlation with other assets* Based on daily percentage changes

* Positive: appreciation of MXN and corresponding currency Source: Bloomberg, Banorte-Ixe

* Positive: appreciation of MXN and corresponding asset except VIX Source: Bloomberg, Banorte-Ixe

14.8

15.3

15.8

16.3

16.8

17.3

17.8

18.3

18.8

19.3

Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16

. . . . .

USD/MXN= 18.1839 MA (50)= 17.5886 MA (100)= 17.8691 MA (150)= 17.5027 MA (200)= 17.3081

14.0

15.0

16.0

17.0

18.0

19.0

May-15 Jul-15 Sep-15 Nov-15 Jan-16 Mar-16

19.4448

18.3924

17.7413

17.2150

16.6888

16.0377

14.9853

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

4-Feb-16 19-Feb-16 5-Mar-16 20-Mar-16 4-Apr-16 19-Apr-16 4-May-16

EUR CAD ZAR BRL HUF RUB

-0.5

-0.3

-0.1

0.1

0.3

0.5

0.7

0.9

Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16

VIX SPX Gold GSCI

12

FX technicals (continued) Short-term risk reversals once again signaling risks for the peso. The skew in

favor of short-term OTM USD/MXN calls over puts plunged again after last

week’s upward adjustment, with the 1M measure ending at 0.98 (-0.67vols) and the

3-month maturity at 1.74 (-0.46vols). When adjusted for volatility, the former went

again to undervalued territory, plunging from 0.12 to 0.07, or to -2.2σ over its 1Y

average, signaling once again an elevated risk of further pressures in the currency

USD/MXN – ATM options volatility curve %

USD/MXN – 1M implied and historical volatility %

Source: Bloomberg Source: Bloomberg

USD/MXN – Spread between implicit and historical volatility Bps

Emerging markets 1-month ATM options volatility Against USD, in standard deviations relative to last year’s average

Source: Bloomberg Source: Bloomberg, Banorte-Ixe

USD/MXN – 1-month and 3-month 25D risk reversals Last 24 months, difference between USD calls and puts, in vols

USD/MXN – 1-month 25D volatility-adjusted risk reversal Last 12 months, ratio adjusted against one month implied volatility

Source: Bloomberg Source: Bloomberg, Banorte-Ixe

11.0

11.5

12.0

12.5

13.0

13.5

14.0

14.5

15.0

1M 2M 3M 6M 9M 1Y

Today 2 weeks1 week 3 weeks

6

8

10

12

14

16

18

Feb-15 Jun-15 Oct-15 Feb-16

Historical

Implied

-400

-300

-200

-100

0

100

200

300

400

500

Feb-15 Apr-15 Jun-15 Aug-15 Oct-15 Dec-15 Feb-16 Apr-16

1M

3M

-1.54

-1.11

-1.04

-1.03

-0.93

-0.42

-0.11

-0.10

-0.03

0.74

1.06

-6.0 -5.0 -4.0 -3.0 -2.0 -1.0 0.0 1.0 2.0 3.0 4.0 5.0 6.0

HUF

RUB

BRL

PLN

TRY

COP

KRW

CLP

MYR

MXN

ZAR

CaroBarato

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

May-14 Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16

1M

3M

0.05

0.07

0.09

0.11

0.13

0.15

0.17

0.19

May-15 Aug-15 Nov-15 Feb-16 May-16

Risk Reversal 1Y average +1 st. dev. -1 st. dev.

USDMXN call > USDMXN put

13

FX trade recommendations We reiterate our short USD/MXN bias for trading purposes. We forecast a

weekly range between 17.90-18.40 pesos per USD. The MXN remained weak

throughout the week despite moderating the strength of the moves above 18.00 per

dollar. In our view, the cross has overshot somewhat. Therefore, we reiterate our

recommendation of maintaining a short USD/MXN bias for trading purposes, but

avoiding directional positions. Among the reasons, we highlight: (1) The peso

depreciated despite its high correlation with oil prices, and WTI gaining 3.7%; (2)

central banks such as the BoE and BoJ showed a more dovish tilt, which could

support risky assets, although the same bias has not been present in recent

commentary by FOMC members; (3) if the peso maintains a relatively weak

behavior when compared to other EM, we do not discard the possibility of

discretionary USD sales by the Foreign Exchange Commission, which could

provide some relief to the currency; and (4) local economic data has been stronger,

but the peso has not reacted meaningfully. Even after accounting for these factors,

we warn that it is likely that the peso’s appreciation potential will remain limited.

As a result, we suggest to keep avoiding strong directional positions, more so

considering the increase in intraday volatility during the past two weeks

USD/MXN - Forecasts Pesos per dollar

USD/MXN 30-day correlation with oil and 10Y UST Based on daily changes

Source: Banorte-Ixe Source: Banorte-Ixe with data from Bloomberg 3M Carry/Vol* and USD/MXN

Economic surprise indexes by region

% and pesos per dollar, respectively Pts

* 3M Mexico – US interest rate (in local currency) divided by 3M implied volatility Source: Bloomberg, Banorte-Ixe

Source: Citi, Bloomberg, Banorte-Ixe

16.3

16.5

16.7

16.9

17.1

17.3

17.5

17.7

17.9

18.1

18.3

18.5

18.7

Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16

Forecast

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16

10Y UST WTI

13.5

14.5

15.5

16.5

17.5

18.5

19.50.17

0.19

0.21

0.23

0.25

0.27

0.29

0.31

0.33

0.35

Jan-15 Mar-15 May-15 Jul-15 Sep-15 Nov-15 Jan-16 Mar-16

Carry/Vol (LHS) USD/MXN (RHS, inverted)

-120

-70

-20

30

80

May-14 Aug-14 Nov-14 Feb-15 May-15 Aug-15 Nov-15 Feb-16

US

Eurozone

Asia Pacific

14

Weekly economic calendar For the week ending May 20, 2016

Time (EDT)

Event Period Unit Banorte-Ixe Survey Previous

Sat

14

01:30 CH Industrial production Apr % y/y -- 6.5 6.8

01:30 CH Gross fixed investment (YTD) Apr % y/y -- 11.0 10.7

01:30 CH Retail sales Apr % y/y -- 10.6 10.5

Mon

16 08:30 US Empire manufacturing May index 5.0 6.5 9.6

19:00 US Fed's Kashkari Holds Town Hall on TBTF in Minneapolis

Tue

17

04:30 UK Consumer prices Apr % y/y 0.5 0.5 0.5

07:30 EZ Trade Balance* Mar billions -- 22.0 20.2

08:30 US Housing starts Apr thousands -- 1,125 1,089

08:30 US Building permits Apr thousands -- 1,134 1,076

08:30 US Consumer prices Apr % m/m 0.3 0.4 0.1

08:30 US Ex. food & enery Apr % m/m 0.2 0.2 0.1

08:30 US Consumer prices Apr %y/y 1.0 1.1 0.9

08:30 US Ex. food & energy Apr % y/y 2.1 2.1 2.2

09:15 US Industrial production Apr % m/m 0.2 0.3 -0.6

09:15 US Manufacturing Apr % m/m 0.3 0.3 -0.3

10:00 MX International reserves May 13 US$bn -- -- 177.7

12:00 US Fed's Williams and Lockhart Discuss Economy at Politico Event

12:30 MX Government bond auction -1M, 3M and 6M Cetes, 5-year Mbono and 10-year Udibono

13:15 US Fed's Kaplan in Moderated Q&A at Petroleum Club of Midland

17:00 CL Monetary policy decision (BCCh) May 17 % 3.50 3.50 3.50

Wed

18

03:30 EZ Consumer prices Apr (F) % y/y -0.2 -0.2 -0.2

03:30 EZ Core Apr (F) % y/y 0.7 0.7 0.7

10:00 UK Unemployment rate Mar % 5.1 5.1 5.1

14:00 US FOMC minutes

Thu

19

07:30 EZ ECB minutes

08:30 US Philadelphia Fed May index 2.0 3.0 -1.6

08:30 US Initial jobless claims May 14 thousands 275 275 294

10:00 MX Banxico's minutes

10:30 US Fed's Dudley speaks on Macroeconomic Trends in New York

SA Monetary policy decision (South African Reserve Bank) May 19 % 7.00 7.00 7.00

Fri

20

08:00 BZ Consumer prices May % m/m -- 0.74 0.51

08:00 BZ Consumer prices May % y/y -- 9.50 9.34

09:00 MX Gross domestic product 1Q16 % y/y 2.6 2.6 2.7

09:00 MX Gross domestic product* 1Q16 % q/q 0.7 0.7 0.8

09:00 MX Nominal gross domestic product 1Q16 % y/y 5.3 5.0 4.9

09:00 MX Global economic activity indicator (IGAE) Mar % y/y 1.5 1.4 4.1

10:00 US Existing home sales Apr millions -- 5.4 5.3

16:30 MX Survey of expectations (Banamex)

Source: Bloomberg and Banorte-Ixe. (P) preliminary data; (R) revised data; (F) final data; * Seasonally adjusted.

15

For the week ending May 13, 2016

Time (EDT)

Event Period Unit Actual Survey Previous

Sat

7 21:00 CH Trade balance Apr USDbn 45.6 40.0 29.9

21:00 CH Exports Apr % y/y -1.8 0.0 11.5

21:00 CH Imports Apr % y/y -10.9 -4.0 -7.6

Mon

9

05:10 US Chicago Fed's Evans Speaks on Economy and Policy on Panel in London

09:00 MX Consumer prices Apr % m/m -0.32 -0.26 0.15

09:00 MX Core Apr % m/m 0.22 0.19 0.36

09:00 MX Consumer prices Apr % y/y 2.48 2.60 2.60

13:00 US Minneapolis Fed's Kashkari Speaks in Minneapolis

21:30 CH Consumer prices Apr % y/y 2.3 2.3 2.3

Tue

10

MX Wage negotiations Apr % y/y 4.9 -- 4.5

02:00 GER Industrial production Mar % m/m -1.3 -0.2 -0.5

10:00 MX International reserves May 6 US$bn 177.7 -- 178.0

12:30 MX Government bond auction -1M, 3M and 6M Cetes, 10-year Mbono and Bondes D

13:00 US 3-year Treasury Bond auction

Wed

11 05:30 UK Industrial production* Mar % m/m 0.3 0.5 -0.3

07:00 BZ Retail sales Mar % y/y -5.7 -5.7 -4.2

13:00 US 10-year Treasury Bond auction

Thu

12

05:00 EZ Industrial production Mar % m/m -0.8 0.0 -0.8

07:00 UK Monetary policy decision (BoE) May 12 % 0.50 0.50 0.50

07:00 UK Quarterly inflation report

08:30 US Initial jobless claims May 7 thousands 294 270 274

09:00 MX Industrial production Mar % y/y -2.0 -0.9 2.6

09:00 MX Industrial production* Mar % m/m -0.2 0.1 -0.1

09:00 MX Manufacturing output Mar % y/y -1.5 0.1 3.9

11:00 US Cleveland Fed's Mester Speaks About Inflation Dynamics

13:00 US 30-year Treasury Bond auction

13:30 US Kansas City Fed's George Speaks on Economy in Albuquerque

17:00 PE Monetary policy decision (BCRP) May 12 % 4.25 4.25 4.25

20:00 SK Monetary policy decision (Central bank of South Korea)

May 13 % 1.50 1.50 1.50

BZ Economic activity* Mar % y/y -6.3 -6.0 -4.5

Fri1

3

02:00 GER Gross domestic product* 1Q16 (P) % q/q 0.7 0.6 0.3

05:00 EZ Gross domestic product* 1Q16 (F) % q/q 0.6 0.5 0.6

08:30 US Advance retail sales Apr % m/m 1.3 0.8 -0.4

08:30 US Retail sales ex autos Apr % m/m 0.8 0.3 0.1

08:30 US Producer prices Apr % m/m 0.2 0.3 -0.1

08:30 US Ex. food & energy prod Apr % m/m 0.1 0.1 0.0

10:00 US Business inventories Mar % m/m 0.4 0.2 -0.1

10:00 US U. of Michigan Confidence May (P) index 95.8 89.9 89.0

18:25 US San Francisco Fed's Williams Speaks in Sacramento

16

Disclaimer

The information contained in this document is illustrative and informative so it should not be considered as an

advice and/or recommendation of any kind. BANORTE is not part of any party or political trend.

Track of the latest fixed-income trade recommendations

Trade idea Entry Target Stop-loss Closed Status P/L Initial date End date

Receive 1-year TIIE-IRS (13x1) 3.92% 3.67% 4.10% 3.87%1

Closed Profit 12-Nov-15 8-Feb-16

Long spread 10-year TIIE-IRS vs US Libor 436bps 410bps 456bps 410bps Closed Profit 30-Sep-15 23-Oct-15

Receive 9-month TIIE-IRS (9x1) 3.85% 3.65% 4.00% 3.65% Closed Profit 3-Sep-15 18-Sep-15

Spread TIIE 2/ 10 yrs (flattening) 230pb 200pb 250pb 200pb Closed Profit 26-Jun-15 29-Jul-15

Long Mbono Dec'24 6.12% 5.89% 6.27% 5.83% Closed Profit 13-mar-15 19-mar-15

Relative-value trade, long 10-year Mbono (Dec'24) / flattening of the curve Closed Profit 22-Dec-14 6-Feb-15

Pay 3-month TIIE-IRS (3x1) 3.24% 3.32% 3.20% 3.30% Closed Profit 29-Jan-15 29-Jan-15

Pay 9-month TIIE-IRS (9x1) 3.28% 3.38% 3.20% 3.38% Closed Profit 29-Jan-15 29-Jan-15

Pay 5-year TIIE-IRS (65x1) 5.25% 5.39% 5.14% 5.14% Closed Loss 4-Nov-14 14-Nov-14

Long Udibono Dec'17 0.66% 0.45% 0.82% 0.82% Closed Loss 4-Jul-14 26-Sep-14

Relative-value trade, long Mbonos 5-to-10-year Closed Profit 5-May-14 26-Sep-14

Receive 2-year TIIE-IRS (26x1) 3.75% 3.55% 3.90% 3.90% Closed Loss 11-Jul-14 10-Sep-14

Receive 1-year TIIE-IRS (13x1) 4.04% 3.85% 4.20% 3.85% Closed Profit 6-Feb-14 10-Apr-14

Long Udibono Jun'16 0.70% 0.45% 0.90% 0.90% Closed Loss 6-Jan-14 4-Feb-14

Long Mbono Jun'16 4.47% 3.90% 4.67% 4.06% Closed Profit 7-Jun-13 21-Nov-13

Receive 6-month TIIE-IRS (6x1) 3.83% 3.65% 4.00% 3.81% Closed Profit 10-Oct-13 25-Oct-13

Receive 1-year TIIE-IRS (13x1) 3.85% 3.55% 4.00% 3.85% Closed Flat 10-Oct-13 25-Oct-13

Long Udibono Dec'17 1.13% 0.95% 1.28% 1.35% Closed Loss 9-Aug-13 10-Sep-13

Receive 9-month TIIE-IRS (9x1) 4.50% 4.32% 4.65% 4.31% Closed Profit 21-Jun-13 12-Jul-13

Spread TIIE-Libor (10-year) 390bps 365bps 410bps 412bps Closed Loss 7-Jun-13 11-Jun-13

Receive 1-year TIIE-IRS (13x1) 4.22% 4.00% 4.30% 4.30% Closed Loss 19-Apr-13 31-May-13

Long Udibono Jun'22 1.40% 1.20% 1.55% 0.97% Closed Profit 15-Mar-13 3-May-13

Receive 1-year TIIE-IRS (13x1) 4.60% 4.45% 4.70% 4.45% Closed Profit 1-Feb-13 7-Mar-13

Long Mbono Nov'42 6.22% 5.97% 6.40% 5.89% Closed Profit 1-Feb-13 7-Mar-13

Long Udibono Dec'13 1.21% 0.80% 1.40% 1.40% Closed Loss 1-Feb-13 15-Apr-13

Receive 1-year TIIE-IRS (13x1) 4.87% 4.70% 5.00% 4.69% Closed Profit 11-Jan-13 24-Jan-13

Receive TIIE Pay Mbono (10-year) 46bps 35bps 54bps 54bps Closed Loss 19-Oct-12 8-Mar-13

Spread TIIE-Libor (10-year) 410bps 385bps 430bps 342bps Closed Profit 21-Sep-13 8-Mar-13

Long Udibono Dec'12 +0.97% -1.50% +1.20% -6.50% Closed Profit 1-May-12 27-Nov-12

Long Udibono Dec'13 +1.06% 0.90% +1.35% 0.90% Closed Profit 1-May-12 14-Dec-12

1. Carry + ro ll-down gains of 17bps

Track of the latest FX trade recommendations*

Trade Idea Entry Target Stop-loss Closed Status P/L* Initial Date End date

Long USD/MXN 14.98 15.50 14.60 15.43 Closed Profit 20-Mar-15 20-Apr-15

Short EUR/MXN 17.70 n.a. n.a. 16.90 Closed Profit 5-Jan-15 15-Jan-15

Tactical trade: Long USD/MXN 14.40 n.a. n.a. 14.85 Closed Profit 15-Dec-14 5-Jan-15

Tactical trade: Long USD/MXN 13.62 n.a. n.a. 14.11 Closed Profit 21-Nov-14 3-Dec-14

Short USD/MXN 13.21 n.a. n.a. 13.64 Closed Loss 10-Sep-14 26-Sep-14

Tactical trade: Short EUR/MXN 17.20 n.a. n.a. 17.03 Closed Profit 27-Aug-14 4-Sep-14

USD/MXN call spread** 12.99 13.30 n.a. 13.02 Closed Loss 6-May-14 13-Jun-14

Directional short USD/MXN 13.00 12.70 13.25 13.28 Closed Loss 31-Oct-13 8-Nov-13

Limit short USD/MXN 13.25 12.90 13.46 -- Cancelled -- 11-Oct-13 17-Oct-13

Speculative short USD/MXN 12.70 12.50 13.00 13.00 Closed Loss 26-Jul-13 21-Aug-13

Short EUR/MXN 16.05 15.70 16.40 15.69 Closed Profit 29-Apr-13 9-May-13

Long USD/MXN 12.60 12.90 12.40 12.40 Closed Loss 11-Mar-13 13-Mar-13

Long USD/MXN 12.60 12.90 12.40 12.85 Closed Profit 11-Jan-13 27-Feb-13

Tactical limit short USD/MXN 12.90 12.75 13.05 -- Cancelled -- 10-Dec-12 17-Dec-12

* Total return does not consider carry gain/losses

** Low strike (long call) at 13.00, high strike (short call) at 13.30 for a premium of 0.718% of notional amount

Source: Banorte-Ixe

17

GRUPO FINANCIERO BANORTE S.A.B. de C.V.

Gabriel Casillas Olvera Chief Economist and Head of Research [email protected] (55) 4433 - 4695

Raquel Vázquez Godinez Assistant [email protected] (55) 1670 - 2967

Delia María Paredes Mier Executive Director of Economic Analysis [email protected] (55) 5268 - 1694

Alejandro Cervantes Llamas Senior Economist, Mexico [email protected] (55) 1670 - 2972

Katia Celina Goya Ostos Senior Global Economist [email protected] (55) 1670 - 1821

Miguel Alejandro Calvo Domínguez

Economist, Regional & Sectorial [email protected] (55) 1670 - 2220

Juan Carlos García Viejo Economist, International [email protected] (55) 1670 - 2252

Rey Saúl Torres Olivares Analyst [email protected] (55) 1670 - 2957

Lourdes Calvo Fernández Analyst (Edition) [email protected] (55) 1103 - 4000 x 2611

Alejandro Padilla Santana Head Strategist – Fixed income and FX [email protected] (55) 1103 - 4043

Juan Carlos Alderete Macal, CFA FX Strategist [email protected] (55) 1103 - 4046

Santiago Leal Singer Analyst Fixed income and FX [email protected] (55) 1670 - 2144

Manuel Jiménez Zaldivar Director Equity Research —Telecommunications / Media

[email protected] (55) 5268 - 1671

Victor Hugo Cortes Castro Equity Research Analyst [email protected] (55) 1670 - 1800

Marissa Garza Ostos Senior Equity Research Analyst – Conglomerates/Financials/ Mining/ Chemistry

[email protected] (55) 1670 - 1719

Marisol Huerta Mondragón Equity Research Analyst – Food/Beverages [email protected] (55) 1670 - 1746

José Itzamna Espitia Hernández Equity Research Analyst – Airports / Cement / Infrastructure / Fibras

[email protected] (55) 1670 - 2249

Valentín III Mendoza Balderas Equity Research Analyst – Auto parts [email protected] (55) 1670 - 2250

Corporate Debt

Tania Abdul Massih Jacobo Director Corporate Debt [email protected] (55) 5268 - 1672

Hugo Armando Gómez Solís Analyst, Corporate Debt [email protected] (55) 1670 - 2247

Idalia Yanira Céspedes Jaén Analyst, Corporate Debt [email protected] (55) 1670 - 2248

Armando Rodal Espinosa Head of Wholesale Banking [email protected] (55) 1670 - 1889

Alejandro Eric Faesi Puente Head of Global Markets and Institutional Sales [email protected] (55) 5268 - 1640

Alejandro Aguilar Ceballos Head of Asset Management [email protected] (55) 5268 - 9996

Arturo Monroy Ballesteros Head of Investment Banking and Structured Finance

[email protected] (55) 5004 - 1002

Gerardo Zamora Nanez Head of Transactional Banking, Leasing and Factoring

[email protected] (81) 8318 - 5071

Jorge de la Vega Grajales Head of Government Banking [email protected] (55) 5004 - 5121

Luis Pietrini Sheridan Head of Private Banking [email protected] (55) 5004 - 1453

René Gerardo Pimentel Ibarrola Head of Asset Management [email protected] (55) 5268 - 9004

Ricardo Velázquez Rodríguez Head of International Banking [email protected] (55) 5004 - 5279

Víctor Antonio Roldan Ferrer Head of Corporate Banking [email protected] (55) 5004 - 1454

Research and Strategy

Economic Analysis

Fixed income and FX Strategy

Equity Strategy

Wholesale Banking