MENA IPO EyeH1 2015

Inside H1 2015 2

Key trends impacting MENA IPOs 5

H2 2015 outlook 8

Summary of IPOs 9

Key events to look out for 13

Contacts 13

2 | MENA IPO Eye — H1 2015

The MENA IPO Eye is a quarterly publication covering the MENA IPO markets.

Through the publication, we intend to highlight the latest developments, market trends and outlook of IPO activity in the region, providing valuable insights for companies looking to float in the future.

For feedback, please email [email protected].

Mayur Pau MENA IPO Leader

H1 2015 highlightsIncreasing IPO activity in Q2 2015, with IPOs in Egypt and Saudi Arabia leading the way

H1 2015 saw 11 IPOs in the Middle East and North Africa (MENA) region, raising capital of over US$2.4b. Deal volume decreased by 31% and proceeds raised decreased by 1% in H1 2015, compared with H1 2014. Egypt and Saudi Arabia witnessed the highest number of IPOs with five and three IPOs respectively.

Q2 2015 saw an uptick in IPO activity, with nine IPOs in the MENA region raising over US$2.1b. Capital raised through MENA firms increased by 92%, while the number of IPOs decreased by two in Q2 2015, compared with Q2 2014.

The IPO of Saudi Ground Services Company on the Saudi Stock Exchange (SE) (Tadawul) was the largest IPO in H1 2015, raising US$751.9m, and was over twice the size of the next largest IPO during the period.

Nine IPOs in Q2 2015

Company (oversubscription rate)

Domicile Sector Amount raised (US$m)

Listing date Listing Exchange*

Saudi Ground Services Company (3.39x)

KSA** Transport 751.9 25 June 2015 Saudi SE

Emaar Misr (institutional tranche — 11x; and retail tranche — 36x)

Egypt Real estate 298.8 5 July 2015*** Egypt SE

Integrated Diagnostics Holdings PLC (11.2x)

Egypt Health care 290.2 11 May 2015 London SE

Edita Food Industries (4.5x)

Egypt Food and beverages

263.0 2 April 2015 Egypt SE and London SE (GDRs)****

Phoenix Power Company SAOG (15x)

Oman Power and utilities

146.3 22 June 2015 Muscat SM

Saudi Company for Hardware (6.2x)

KSA Industrial manufacturing

134.4 12 May 2015 Saudi SE

Middle East Paper Company (0.01x)

KSA Industrial manufacturing

119.9 3 May 2015 Saudi SE

Other IPOs***** 116.0Total 2,120.5

Source: Zawya. * Exchange SE: stock exchange, SM: stock market. ** KSA: Kingdom of Saudi Arabia. *** IPO is considered closed with finalized subscription and share value. **** GDRs: Global depository receipts. ***** Other IPOs include Universal Automobile Distributors Holding (US$42m, Tunisia) and Total Maroc (US$73.9, Morocco).

Reduced volatility and stabilizing oil prices leading to increased IPO activity

Following a decline in Brent crude oil prices during H2 2014 and Q1 2015, oil prices appear to have stabilized, with Brent crude (OPEC basket price) hovering around US$60 per barrel. As a result, several companies that had deferred IPO plans due to volatility in the markets driven by oil price movements have executed their IPO plans, particularly in Saudi Arabia and Egypt.

3MENA IPO Eye — H1 2015 |

Egypt and Saudi Arabia continue to be strong IPO performers

IPOs on the Egyptian and Saudi Arabian exchanges were the primary drivers of IPO activity in MENA in H1 2015. Egypt continues to benefit from increasing political stability, improved economic conditions and various reforms, which are driving confidence in the Egyptian capital markets, attracting both companies and investors.

Egyptian IPOs were among the largest in the MENA region. This included Integrated Diagnostics Holdings PLC, Edita Food Industries, Orascom Construction Limited and Emar Misr.

Saudi Arabia saw the listing of three companies, including the long-awaited IPO of Saudi Ground Services Company, which is part of the continued privatization of Saudi Arabian Airlines business units.

IPOs on the Tadawul and the Egyptian Exchange continue to attract strong demand, with offerings up to 11 times oversubscribed, highlighting positive investor sentiment in these markets in particular.

Return of outbound London IPOs

Q2 2015 also saw the first MENA outbound IPOs since the listing of Gulf Marine Services on the London Stock Exchange (LSE) in Q1 2014. Integrated Diagnostics Holdings (health care diagnostic services) and Edita Foods Industries (packaged food distributor) opted for listings on the LSE, through a main market listing and listing of GDRs, respectively.

Integrated Diagnostics Holdings listed 43.5% of its shares on 11 May 2015 (UK election day). Shares were offered at US$4.45 per share on 6 May 2015 (conditional trading date) and are currently traded at US$5.75 per share.

Integrated Diagnostics Holdings is the third MENA health care company to list on the LSE, following the successful IPOs of NMC Health (2012) and Al Noor Hospital (2013). This sector continues to be one of the most attractive sectors in the MENA region for IPOs.

Opening of the largest market in MENA to foreign investors

On 15 June 2015, Tadawul, the largest capital market in MENA with a market capitalization of US$580m, opened its stock market to foreign direct investment (FDI). Qualified foreign investors (QFIs) including banks, insurance companies and asset managers were allowed to invest in companies listed on Tadawul. Previously, only companies from the Gulf Cooperation Council (GCC) countries had access to this exchange.

New regulations relating to foreign investors on Tadawul

• QFIs must have minimum assets worth SAR18.75b (US$5b).

• QFIs must have a five-year track record.

• A single investor may not own more than 5% of a company by stock market value and a group of foreign investors cannot own more than 10%.

• The maximum proportion of shares of any issuer that may be owned by QFIs is 20%.

• Overall foreign ownership of a company cannot be more than 49%.

• There is a tax of 5% on dividends for foreign investors.

Source: Rules for Qualified Foreign Financial Institutions Investments in Listed Shares, Capital Market Authority, Saudi Arabia.

Many commentators have stated this as an important reform that will help transform Tadawul’s global reputation and reduce volatility by attracting more institutional investors. However, the current ownership rules may limit the potential impact of this reform.

“ Markets with a big tranche of institutional investors are characterized by low volatility and high efficiency. Increasing institutional investors’ strategic ownership in listed companies supports governance practices and increases transparency, a target that is hard to achieve amid the dominance of retail investors in the market.” CMA (Source: Arabnews.com)

4 | MENA IPO Eye — H1 2015

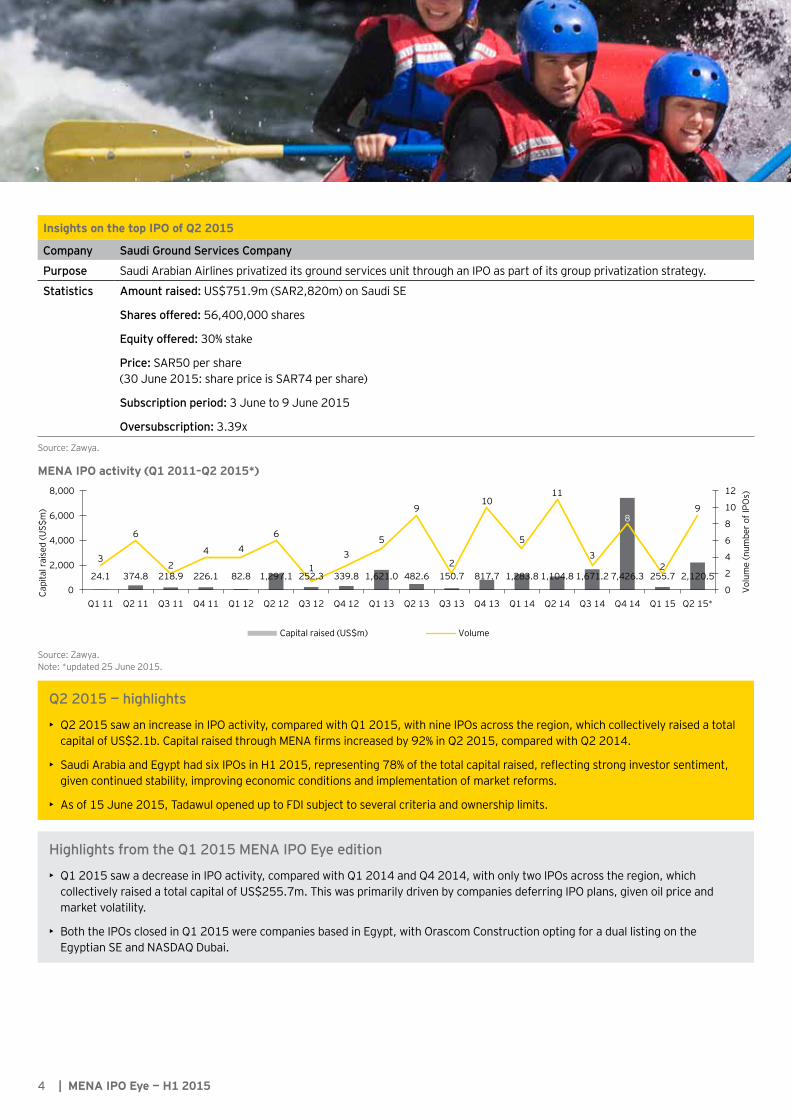

Insights on the top IPO of Q2 2015

Company Saudi Ground Services Company

Purpose Saudi Arabian Airlines privatized its ground services unit through an IPO as part of its group privatization strategy.

Statistics Amount raised: US$751.9m (SAR2,820m) on Saudi SE

Shares offered: 56,400,000 shares

Equity offered: 30% stake

Price: SAR50 per share (30 June 2015: share price is SAR74 per share)

Subscription period: 3 June to 9 June 2015

Oversubscription: 3.39x

Source: Zawya.

MENA IPO activity (Q1 2011–Q2 2015*)

Capital raised (US$m) Volume

24.1 374.8 218.9 226.1 82.8 1,297.1 252.3 339.8 1,621.0 482.6 150.7 817.7 1,283.8 1,104.8 1,671.2 7,426.3

3

6

24 4

6

13

5

9 9

2

10

5

11

3

8

0

2

4

6

8

10

12

0

2,000

4,000

6,000

8,000

Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14

255.7 2,120.52

Q1 15 Q2 15*Q4 14

Volu

me

(num

ber o

f IPO

s)

Capi

tal r

aise

d (U

S$m

)

Source: Zawya. Note: *updated 25 June 2015.

Q2 2015 — highlights

• Q2 2015 saw an increase in IPO activity, compared with Q1 2015, with nine IPOs across the region, which collectively raised a total capital of US$2.1b. Capital raised through MENA firms increased by 92% in Q2 2015, compared with Q2 2014.

• Saudi Arabia and Egypt had six IPOs in H1 2015, representing 78% of the total capital raised, reflecting strong investor sentiment, given continued stability, improving economic conditions and implementation of market reforms.

• As of 15 June 2015, Tadawul opened up to FDI subject to several criteria and ownership limits.

Highlights from the Q1 2015 MENA IPO Eye edition

• Q1 2015 saw a decrease in IPO activity, compared with Q1 2014 and Q4 2014, with only two IPOs across the region, which collectively raised a total capital of US$255.7m. This was primarily driven by companies deferring IPO plans, given oil price and market volatility.

• Both the IPOs closed in Q1 2015 were companies based in Egypt, with Orascom Construction opting for a dual listing on the Egyptian SE and NASDAQ Dubai.

5MENA IPO Eye — H1 2015 |

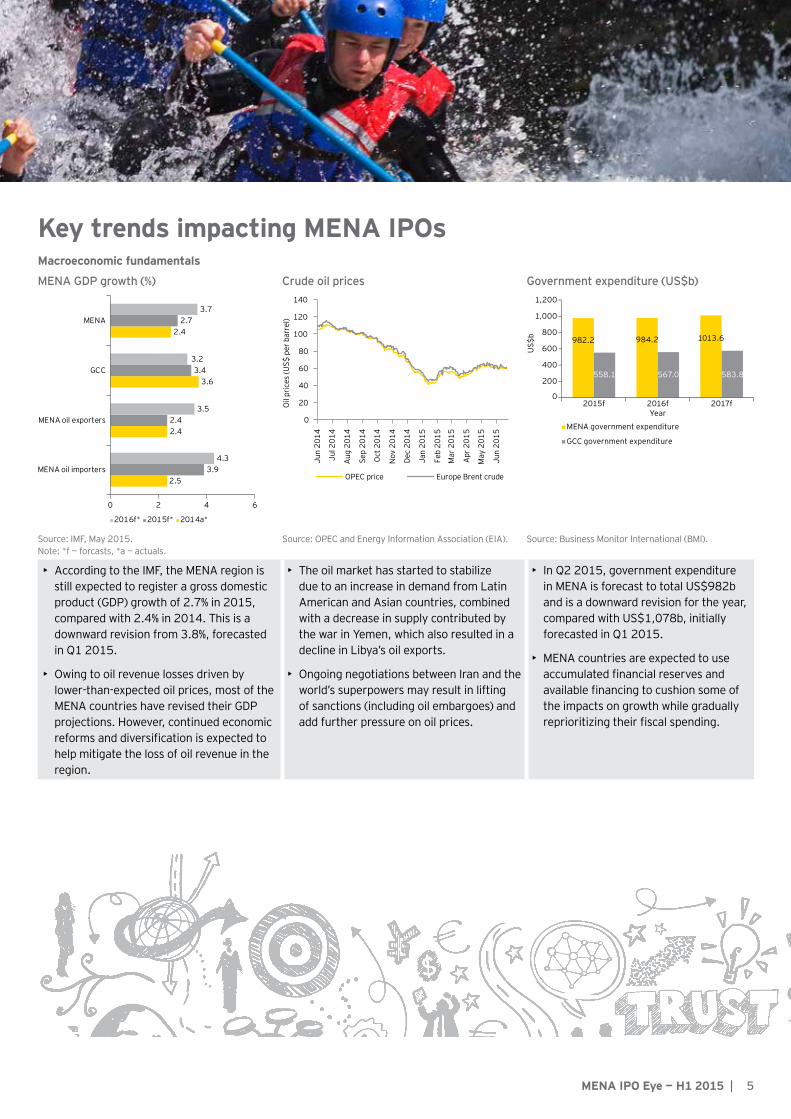

Key trends impacting MENA IPOsMacroeconomic fundamentals

MENA GDP growth (%) Crude oil prices Government expenditure (US$b)

2.5

2.4

3.6

2.4

3.9

2.4

3.4

2.7

4.3

3.5

3.2

3.7

0 2 4 6

MENA oil importers

MENA oil exporters

GCC

MENA

2016f* 2015f* 2014a*

0

20

40

60

80

100

120

140

Oil

pric

es (U

S$ p

er b

arre

l)

OPEC price

Jun

2014

Jul 2

014

Aug

201

4

Sep

2014

Oct

201

4

Nov

201

4

Dec

2014

Jan

2015

Feb

2015

Mar

201

5

Apr

201

5

May

201

5

Jun

2015

Europe Brent crude

982.2 984.2 1013.6

558.1 567.0 583.8

0

200

400

600

800

1,000

1,200

2015f 2016f 2017f

US$

b

Year

MENA government expenditure

GCC government expenditure

Source: IMF, May 2015. Note: *f — forcasts, *a — actuals.

Source: OPEC and Energy Information Association (EIA). Source: Business Monitor International (BMI).

• According to the IMF, the MENA region is still expected to register a gross domestic product (GDP) growth of 2.7% in 2015, compared with 2.4% in 2014. This is a downward revision from 3.8%, forecasted in Q1 2015.

• Owing to oil revenue losses driven by lower-than-expected oil prices, most of the MENA countries have revised their GDP projections. However, continued economic reforms and diversification is expected to help mitigate the loss of oil revenue in the region.

• The oil market has started to stabilize due to an increase in demand from Latin American and Asian countries, combined with a decrease in supply contributed by the war in Yemen, which also resulted in a decline in Libya’s oil exports.

• Ongoing negotiations between Iran and the world’s superpowers may result in lifting of sanctions (including oil embargoes) and add further pressure on oil prices.

• In Q2 2015, government expenditure in MENA is forecast to total US$982b and is a downward revision for the year, compared with US$1,078b, initially forecasted in Q1 2015.

• MENA countries are expected to use accumulated financial reserves and available financing to cushion some of the impacts on growth while gradually reprioritizing their fiscal spending.

6 | MENA IPO Eye — H1 2015

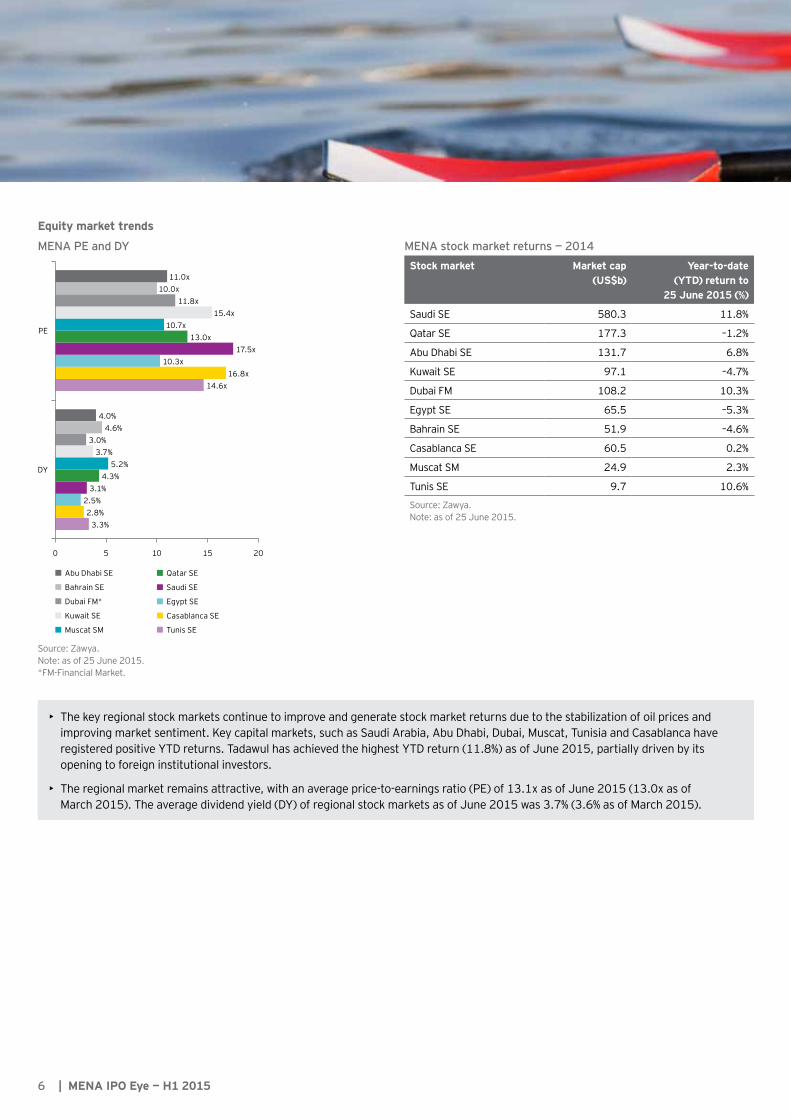

Equity market trends

MENA PE and DY

3.3%

14.6x

2.8%

16.8x

2.5%

10.3x

3.1%

17.5x

4.3%

13.0x

5.2%

10.7x

3.7%

15.4x

3.0%

11.8x

4.6%

10.0x

4.0%

11.0x

0 5 10 15 20

DY

PE

Abu Dhabi SE

Bahrain SE

Dubai FM*

Kuwait SE

Muscat SM

Qatar SE

Saudi SE

Egypt SE

Casablanca SE

Tunis SE

Source: Zawya. Note: as of 25 June 2015. *FM-Financial Market.

Stock market Market cap (US$b)

Year-to-date (YTD) return to

25 June 2015 (%)

Saudi SE 580.3 11.8%

Qatar SE 177.3 –1.2%

Abu Dhabi SE 131.7 6.8%

Kuwait SE 97.1 –4.7%

Dubai FM 108.2 10.3%

Egypt SE 65.5 –5.3%

Bahrain SE 51.9 –4.6%

Casablanca SE 60.5 0.2%

Muscat SM 24.9 2.3%

Tunis SE 9.7 10.6%

Source: Zawya. Note: as of 25 June 2015.

• The key regional stock markets continue to improve and generate stock market returns due to the stabilization of oil prices and improving market sentiment. Key capital markets, such as Saudi Arabia, Abu Dhabi, Dubai, Muscat, Tunisia and Casablanca have registered positive YTD returns. Tadawul has achieved the highest YTD return (11.8%) as of June 2015, partially driven by its opening to foreign institutional investors.

• The regional market remains attractive, with an average price-to-earnings ratio (PE) of 13.1x as of June 2015 (13.0x as of March 2015). The average dividend yield (DY) of regional stock markets as of June 2015 was 3.7% (3.6% as of March 2015).

MENA stock market returns — 2014

7MENA IPO Eye — H1 2015 |

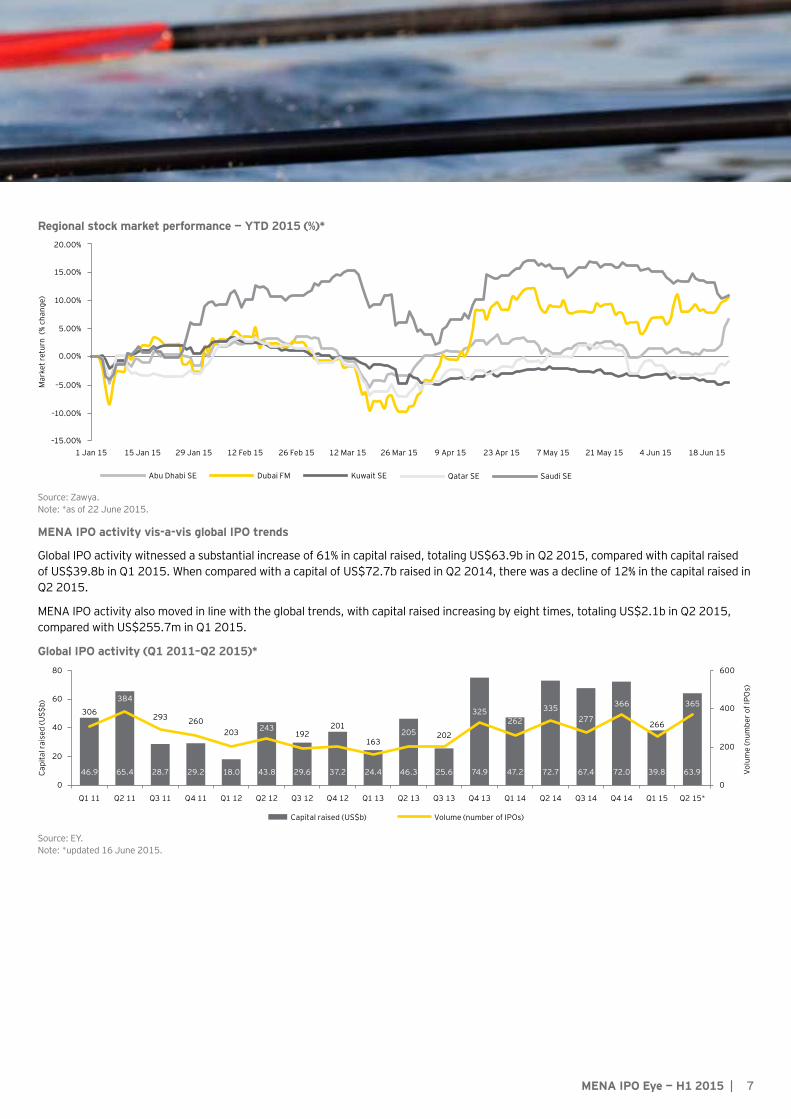

Regional stock market performance — YTD 2015 (%)*

–15.00%

–10.00%

–5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

1 Jan 15 15 Jan 15 29 Jan 15 12 Feb 15 26 Feb 15 12 Mar 15 26 Mar 15 9 Apr 15 23 Apr 15 7 May 15 21 May 15 4 Jun 15 18 Jun 15

Mar

ket r

etur

n (%

cha

nge)

Abu Dhabi SE Dubai FM Kuwait SE Qatar SE Saudi SE

Source: Zawya. Note: *as of 22 June 2015.

MENA IPO activity vis-a-vis global IPO trends

Global IPO activity witnessed a substantial increase of 61% in capital raised, totaling US$63.9b in Q2 2015, compared with capital raised of US$39.8b in Q1 2015. When compared with a capital of US$72.7b raised in Q2 2014, there was a decline of 12% in the capital raised in Q2 2015.

MENA IPO activity also moved in line with the global trends, with capital raised increasing by eight times, totaling US$2.1b in Q2 2015, compared with US$255.7m in Q1 2015.

Global IPO activity (Q1 2011–Q2 2015)*

46.9 65.4 28.7 29.2 18.0 43.8 29.6 37.2 24.4 46.3 25.6 74.9 47.2 72.7 67.4 72.0 39.8

306

384

293 260203 243

192201

163205 202

325262

335277

366

266

63.9

365

0

200

400

600

0

20

40

60

80

Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Q2 15*Q1 15

Volu

me

(num

ber o

f IPO

s)

Capi

tal r

aise

d (U

S$b)

Capital raised (US$b) Volume (number of IPOs)

Source: EY. Note: *updated 16 June 2015.

8 | MENA IPO Eye — H1 2015

H2 2015 outlookStabilizing oil prices, but uncertainty from the potential lifting of sanctions on Iran

Brent crude oil prices appear to have stabilized over Q2 2015, resulting in less volatility and improved returns on the key MENA stock exchanges. This is expected to continue going forward, resulting in improved confidence for companies looking to IPO.

The stability in oil prices is expected to boost the regional stock markets. However, the potential lifting of sanctions on Iran, based on ongoing negotiations with the world’s superpowers toward the end of the Q2 2015, is likely to add downward pressure on oil prices, going forward.

Regional reforms, paving the way for increased IPO activity

With Saudi Arabia opening Tadawul to direct foreign participation for the first time, both local and international investors are positioning themselves to trade in the largest MENA bourse (capitalization of US$580b). This is likely to drive increased activity and investment, going forward.

Foreign investors are also expected to be attracted by the recent introduction of pre-IPO funds, which provide growth capital to companies and do not require foreign investors to go through the licensing process.

In Kuwait, the authorities are planning to align the stock market with the global norms in order to encourage foreign investors.

In Egypt, the government is planning to introduce value-added tax (VAT) by the second half of 2015 to increase government revenues and spending.

These regional reforms are expected to drive capital market activity in the region in H2 2015.

New companies law in the UAE

The UAE IPO market has been subdued over the first half of 2015; however, Q2 2015 saw the new Commercial Companies Law come into effect.

The legislation allows companies to float a minimum of 30% of their shares (previously 55%) and underwriting has been given statutory recognition, allowing companies to use a book building process to price shares, rather than the price being allocated by the regulator.

The new law is likely to have a significant impact on the UAE IPO market, given companies often see outbound IPOs as more attractive due to the previous minimum float requirement.

With several companies waiting for the right time to launch or restart their IPO process, we expect several UAE companies to IPO in H2 2015.

The Greek effect

The ongoing Greek crisis in Europe, may have a delayed impact on the MENA exchanges.

Firms preparing for an IPO in 2015

According to the Zawya IPO Monitor, over 50 companies from the MENA region have plans to go public in 2015.

Some of the prominent names expected to be listed in the second half of 2015 are Zain Iraq (Iraq), Qalaa Holdings (Egypt), Kuwait Airways Corporation (Kuwait), Emaar Financial Services (UAE), Arab Paper Manufacturing Co. Ltd. (Saudi Arabia), Riyadh Cables Group of Companies (Saudi Arabia), Al-Watania Poultry, and Jindal Shadeed Iron & Steel Co. (Oman).

Broader outlook — highlights

• Oil prices appear to have stabilized in Q2 2015. However, ongoing negotiations between Iran and the world’s superpowers are likely to result in the end of sanctions, and may impact oil prices and the MENA capital markets going forward.

• The full effect of the change in regulation to allow FDI on the Tadawul is expected to pick up momentum in H2 2015, as stakeholders become familiar with the new rules.

• The UAE has issued a new commercial companies law with a revised minimum float requirement of only 30% (previously 55%). This change in minimum float requirement is likely to increase IPO activity in H2 2015. Additional reforms in Egypt and Kuwait are also expected to drive the capital market activity in the region.

9MENA IPO Eye — H1 2015 |

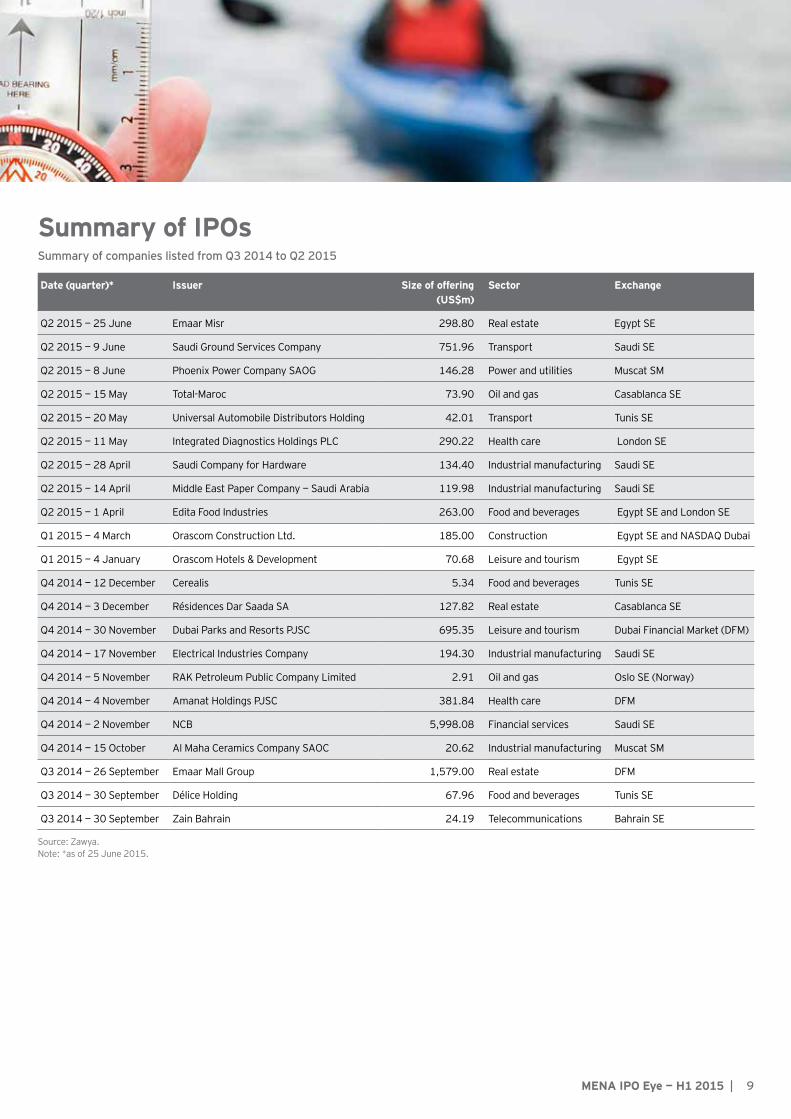

Summary of IPOsSummary of companies listed from Q3 2014 to Q2 2015

Date (quarter)* Issuer Size of offering (US$m)

Sector Exchange

Q2 2015 — 25 June Emaar Misr 298.80 Real estate Egypt SE

Q2 2015 — 9 June Saudi Ground Services Company 751.96 Transport Saudi SE

Q2 2015 — 8 June Phoenix Power Company SAOG 146.28 Power and utilities Muscat SM

Q2 2015 — 15 May Total-Maroc 73.90 Oil and gas Casablanca SE

Q2 2015 — 20 May Universal Automobile Distributors Holding 42.01 Transport Tunis SE

Q2 2015 — 11 May Integrated Diagnostics Holdings PLC 290.22 Health care London SE

Q2 2015 — 28 April Saudi Company for Hardware 134.40 Industrial manufacturing Saudi SE

Q2 2015 — 14 April Middle East Paper Company — Saudi Arabia 119.98 Industrial manufacturing Saudi SE

Q2 2015 — 1 April Edita Food Industries 263.00 Food and beverages Egypt SE and London SE

Q1 2015 — 4 March Orascom Construction Ltd. 185.00 Construction Egypt SE and NASDAQ Dubai

Q1 2015 — 4 January Orascom Hotels & Development 70.68 Leisure and tourism Egypt SE

Q4 2014 — 12 December Cerealis 5.34 Food and beverages Tunis SE

Q4 2014 — 3 December Résidences Dar Saada SA 127.82 Real estate Casablanca SE

Q4 2014 — 30 November Dubai Parks and Resorts PJSC 695.35 Leisure and tourism Dubai Financial Market (DFM)

Q4 2014 — 17 November Electrical Industries Company 194.30 Industrial manufacturing Saudi SE

Q4 2014 — 5 November RAK Petroleum Public Company Limited 2.91 Oil and gas Oslo SE (Norway)

Q4 2014 — 4 November Amanat Holdings PJSC 381.84 Health care DFM

Q4 2014 — 2 November NCB 5,998.08 Financial services Saudi SE

Q4 2014 — 15 October Al Maha Ceramics Company SAOC 20.62 Industrial manufacturing Muscat SM

Q3 2014 — 26 September Emaar Mall Group 1,579.00 Real estate DFM

Q3 2014 — 30 September Délice Holding 67.96 Food and beverages Tunis SE

Q3 2014 — 30 September Zain Bahrain 24.19 Telecommunications Bahrain SE

Source: Zawya. Note: *as of 25 June 2015.

10 | MENA IPO Eye — H1 2015

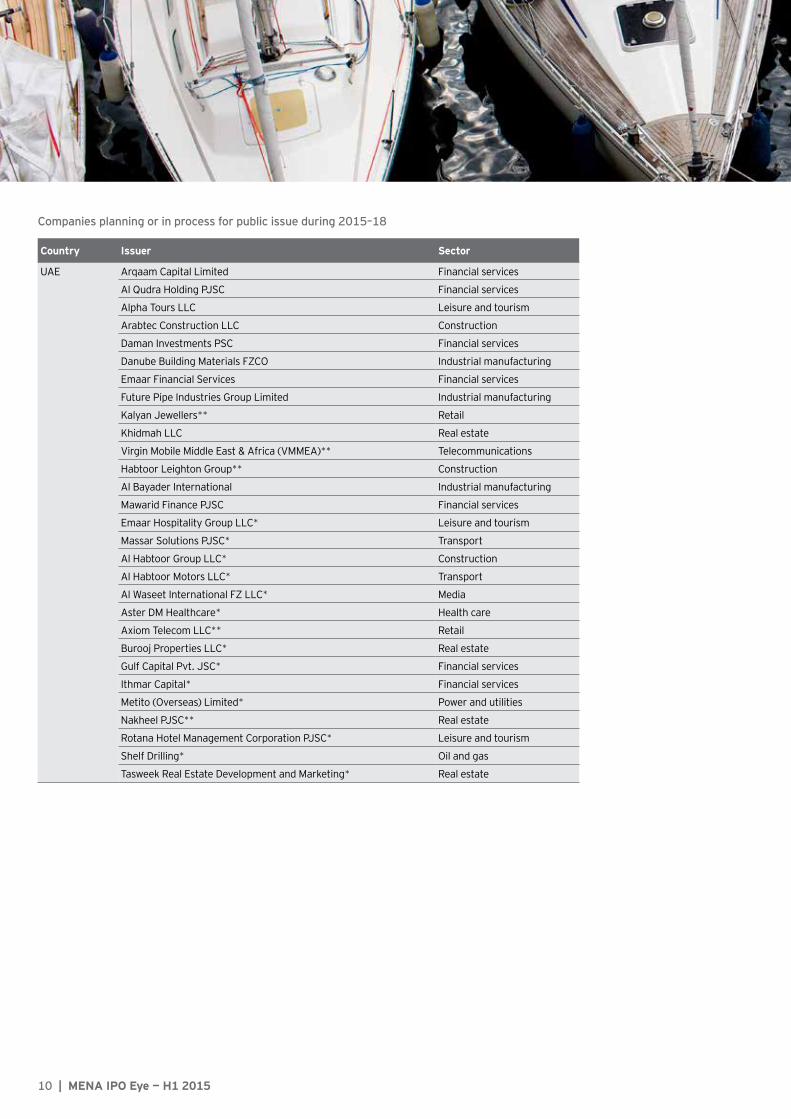

Companies planning or in process for public issue during 2015–18

Country Issuer Sector

UAE Arqaam Capital Limited Financial services

Al Qudra Holding PJSC Financial services

Alpha Tours LLC Leisure and tourism

Arabtec Construction LLC Construction

Daman Investments PSC Financial services

Danube Building Materials FZCO Industrial manufacturing

Emaar Financial Services Financial services

Future Pipe Industries Group Limited Industrial manufacturing

Kalyan Jewellers** Retail

Khidmah LLC Real estate

Virgin Mobile Middle East & Africa (VMMEA)** Telecommunications

Habtoor Leighton Group** Construction

Al Bayader International Industrial manufacturing

Mawarid Finance PJSC Financial services

Emaar Hospitality Group LLC* Leisure and tourism

Massar Solutions PJSC* Transport

Al Habtoor Group LLC* Construction

Al Habtoor Motors LLC* Transport

Al Waseet International FZ LLC* Media

Aster DM Healthcare* Health care

Axiom Telecom LLC** Retail

Burooj Properties LLC* Real estate

Gulf Capital Pvt. JSC* Financial services

Ithmar Capital* Financial services

Metito (Overseas) Limited* Power and utilities

Nakheel PJSC** Real estate

Rotana Hotel Management Corporation PJSC* Leisure and tourism

Shelf Drilling* Oil and gas

Tasweek Real Estate Development and Marketing* Real estate

11MENA IPO Eye — H1 2015 |

Country Issuer Sector

Saudi Arabia Al Aqeeq Real Estate Development Company Real estate

Al-Watania Poultry Agriculture

Arab Paper Manufacturing Co. Ltd. Industrial manufacturing

Riyadh Cables Group of Companies** Industrial manufacturing

Nas Holding Transport

Saudi Airlines Cargo Co. LLC Transport

Saudi Aramco Total Refining and Petrochemical Company Oil and gas

Petromin Corporation** Oil and gas

ACWA Power International* Power and utilities

Al Bassami International Group** Transport

Al Sawani Food and Industrial Supply Company* Retail

Al-Ittefaq Steel Products Co.* Industrial manufacturing

Almana General Hospital — Hofuf* Health care

Dr Sulaiman Al Habib Medical Center* Health care

Murabaha Company* Financial services

Tadawul* Financial services

Taajeer Co. For Machinery, Real Estate and Vehicles Trading* Financial services

Egypt Al Ahly Sporting Club** Education

Arabian Food Industries Company Food and beverages

Beta Egypt Real estate

Cairo for Development and Cars Manufacturing Transport

Food Industries Holding Company Food and beverages

Qalaa Holdings Egypt

Middle East Oil Refinery Oil and gas

Arabtec Egypt for Construction Construction

Raya Contact Center Services

Smart Villages Development And Management Company Real estate

Wadi Group Agriculture

Delta Cement* Construction

Etisalat Misr SAE* Telecommunications

Oman Al Khonji Real Estate & Development LLC (Aqar) Real estate

Falcon Insurance Company SAOC Financial services

Jindal Shadeed Iron & Steel Co. LLC Mining and metals

Kunooz Oman Holding Conglomerates

Oman Reinsurance Company SAOC Financial services

Connect Arabia Telecommunications

Sama Telecommunications Telecommunications

TruckOman LLC Transport

Alargan Towell Investment Company LLC Real Estate

Barr al Jissah Resort Company Real Estate

Muscat Electricity Distribution Company SAOC Power and Utilities

Oman Merchant Bank Financial Services

12 | MENA IPO Eye — H1 2015

Country Issuer Sector

Qatar Al-Sulaiman Holding Conglomerates

Elan Qatar** Services

Barwa Bank QSC Financial services

QIC International LLC Financial services

Qatar Airways Transport

Aljasr Takaful Insurance Company* Financial services

Damaan Islamic Insurance Company* Financial services

Hassad Food Company** Agriculture

Kuwait Kuwait Airways Corporation KSC Transport

Mezzan Holding Company Food and beverages

Housing Finance Company KSCP* Financial services

Bahrain Istikhlaf Bank* Unknown sector

Khalifa bin Salman Port* Transport

Lebanon Middle East Airlines Transport

Patchi* Food and beverages

Iraq Zain Iraq Telecommunications

Elaf Islamic Bank Financial services

Tunisia Modern Leasing Financial services

Morocco Maghrebail Financial services

Source: Zawya. Note: *delayed IPO, **rumored IPO.

13MENA IPO Eye — H1 2015 |

Key events to look out forName of the event Date Theme

Arab IPO Summit14–17 September 2015

The summit will connect capital markets, stock exchanges, investment banks and top private companies in the Arab world to discuss the latest developments in the Arabian capital markets, the future of capital markets in the region and regulations on listings for issuers.

MENA IPO Retreat, Dubai (by invitation only)

To be confirmed

Strategies for companies going public or raising capital through IPOs — discussions and guidance from a dedicated panel of industry experts and professionals

Mayur Pau MENA IPO Leader

[email protected] +971 4312 9446

Darrell Traynor Executive Director — Transaction Advisory Services

[email protected] +971 2417 4571

Shahzad Shaikh Manager — Transaction Advisory Services

[email protected] +971 4701 0858

Contacts

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

The MENA practice of EY has been operating in the region since 1923. For over 90 years, we have grown to over 5,000 people united across 20 offices and 15 countries, sharing the same values and an unwavering commitment to quality. As an organization, we continue to develop outstanding leaders who deliver exceptional services to our clients and who contribute to our communities. We are proud of our accomplishments over the years, reaffirming our position as the largest and most established professional services organization in the region.

© 2015 EYGM Limited. All Rights Reserved.

EYG no. CY1005 ED 0116

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com/mena