1

2014 Bank Study Project Class of 2015

Managing Bank Performance Ernie Swift

Complete and mail by February 15, 2013 to:

Complete and mail by January 15, 2015

Graduate School of Banking at LSU 4273 Highland Road

Baton Rouge, LA 70808-4541 225-766-8595

NOTES: 1. Please use 8 l/2" x 11" paper (or paper folded to that size). 2. Please attach the standard YELLOW cover sheet provided to your solution. 3. Please staple your project or use a binder clip. DO NOT use paper clips or any kind of folder or binder.

2

Introduction:

This Bank Study Project is based on material covered in the course Managing Bank Performance

that was taught during the first week of the 2014 session of the Graduate School of Banking at

LSU. Unless indicated otherwise, the answers to the BSP questions are to be based on the

financial statements included within this problem.

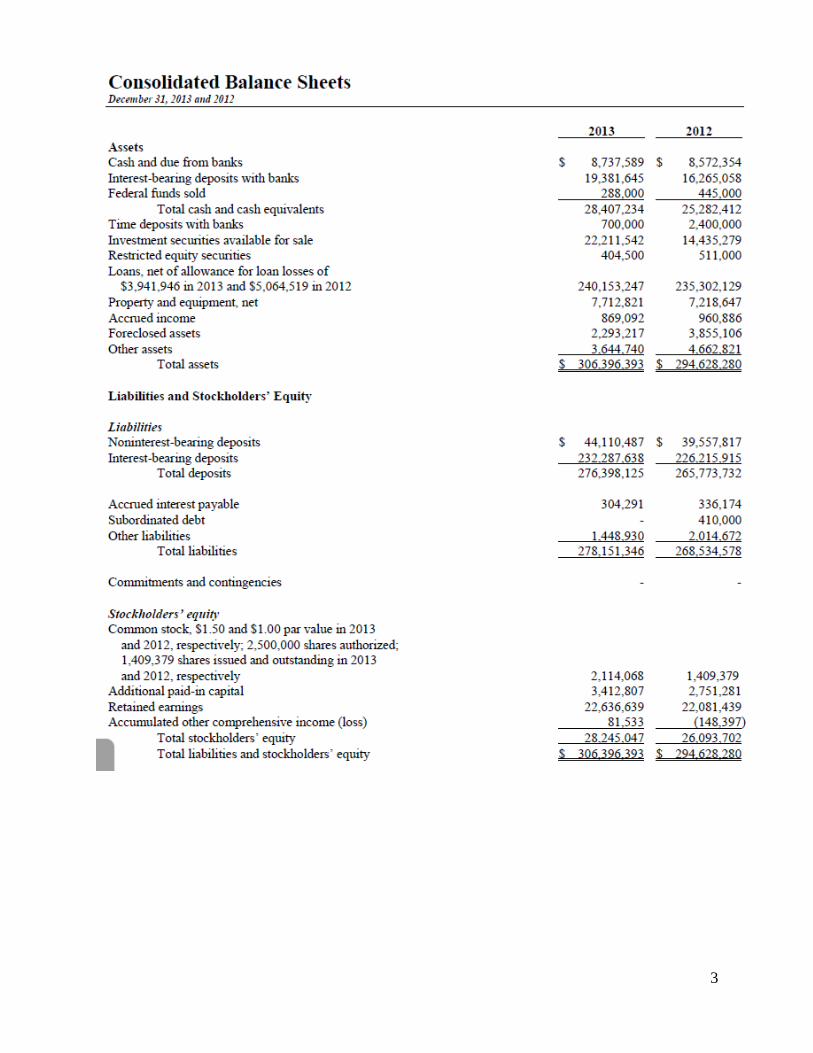

The name of the bank is KFCNTG Bank. The balance sheet and income statement for the years

2012 and 2013 are presented on pages 3 and 4. Other financial information will be presented

later in the problem. Use the data on pages 3 and 4 to answer the questions below and on page 5.

I. Calculate the following for each of the years 2012 and 2013:

2013 2012

1. The amount of Earning Assets

2. The amount of Interest Bearing Liabilities

3. The Yield on Earning Assets

4. The Cost Rate on Interest Bearing Liabilities

5. The Spread

6. The Net Interest Income

7. The Net Interest Margin

8. The Efficiency Ratio

9. The Return on Assets

10. The Return on Equity

Which of the first 8 items above has had the greatest impact on the change in ROA and ROE?

3

4

5

II. Calculate each of the following as a percent of total assets for each year using the data on

pages 3 and 4.

2013 2012

1. Interest Income

2. Interest Expense

3. Provision for Loan Losses

4. NonInterest Income

5. NonInterest Expense

6. Income Tax Expense

7. Net Income

8. Total Stockholders’ Equity

a. Divide your answers for #7 by your answers for #8. How do these values compare with

your answers to #10 on page 2?

b. If interest income to average assets increased 50 basis points in the next year, what would

be the change in ROA? Assume all of the other ratios remain the same.

c. What are the factors that could cause interest income to increase by 50 basis points?

d. What would likely be the effect on the other measures above that may cause your answer

to Q.b. above to be different?

6

e. In your judgment, is KFCNTG Bank performing well over the two years? Why?

f. Has KFCNTG’s performance improved or deteriorated? In which areas?

III. Some of you may have answered yes to the question e above, and some of you may have

answered no. Your answer may have depended upon how KFCNTG compares to your

hometown bank. A better analysis may be to compare the performance of KFCNTG against the

industry performance for banks in the same size category. Industry UBPR data is presented on

the next page for the years 2011, 2012, and 2013.

a. Transfer you answers for KFCNTG Bank to this page for ease of comparison, and then

calculate the same ratios for the industry average UBPR information on the following

page.

KFCNTG UBPR KFCNTG UBPR

2013 2013 2012 2012

9. Interest Income

10. Interest Expense

11. Provision for Loan Losses

12. NonInterest Income

13. NonInterest Expense

14. Income Tax Expense

15. Net Income

16. Total Stockholders’ Equity

b. How does KFCNTG compare with the industry peer group? Your answer should

evaluate every ratio.

7

8

c. What suggestions would you make to further improve the performance of KFCNTG as it

moves into 2014 and 2015?

IV. The interest rate risk position of the bank is best presented by a Beta Adjusted Gap

Report from the planning system used by the bank. A portion of this report is shown on below.

a. The date on this report is 90 days after the annual report date of 12/31/2013. However,

assuming that this makes little difference, what can you determine about the rate sensitivity

position of the bank?

9

b. Without knowing their exact values, what role do the beta values have in creating your

response to question (a) above? In what direction would these beta values on the liability

accounts need to change to cause the beta adjusted gap values to be more in line with the

unadjusted gap values?

c. In the management report of this analysis, a summary of the net interest margin shock

analysis is given and is replicated below. What does this analysis say about the bank’s interest

rate risk position? Does this correspond with your analysis of the Beta Adjusted Gap Report

discussed above in questions (a) and (b)? Why or why not?

d. Assume that the bank preformed a loan prepayment study and determined that loan

prepayments assumptions should be decreased for all scenarios. What effect would the slower

prepayment speeds in a rising rate environment have on the bank’s earnings at risk and why?

e. The bank assumes a 5% early withdrawal of time deposits based on a 200 and 300 basis

point rise in rates. If this doubles, what effect would it have on the bank’s earnings at risk and

why?

10

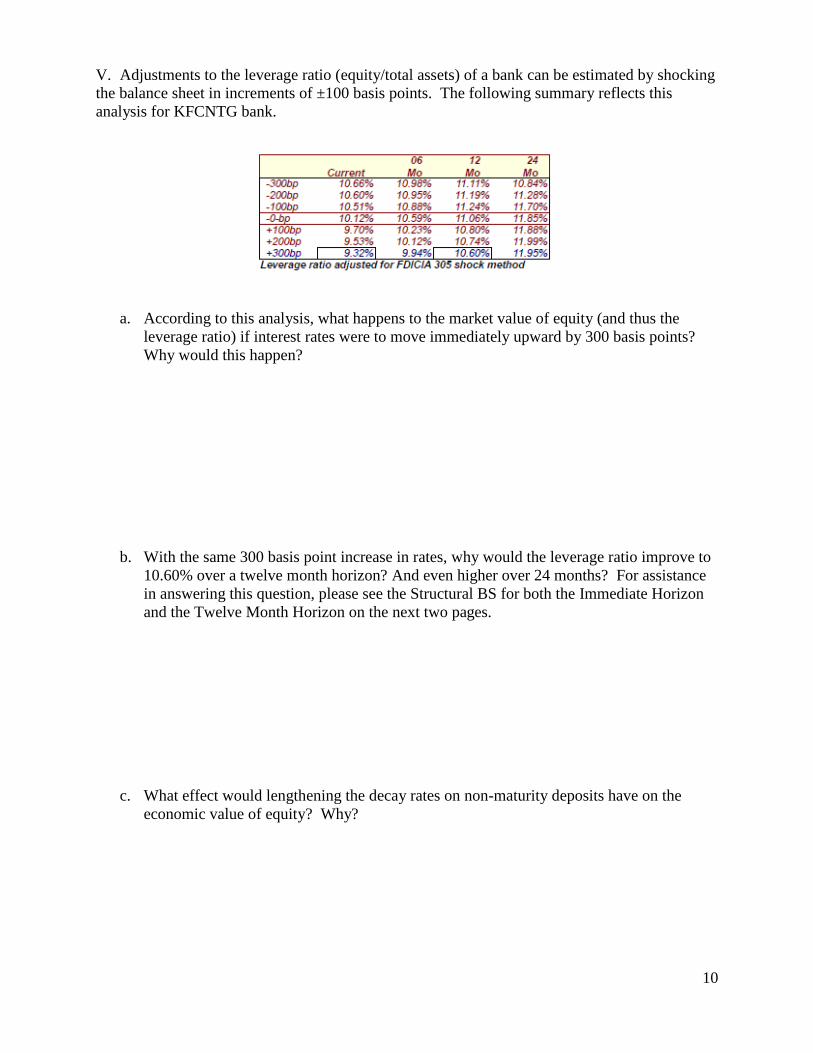

V. Adjustments to the leverage ratio (equity/total assets) of a bank can be estimated by shocking

the balance sheet in increments of ±100 basis points. The following summary reflects this

analysis for KFCNTG bank.

a. According to this analysis, what happens to the market value of equity (and thus the

leverage ratio) if interest rates were to move immediately upward by 300 basis points?

Why would this happen?

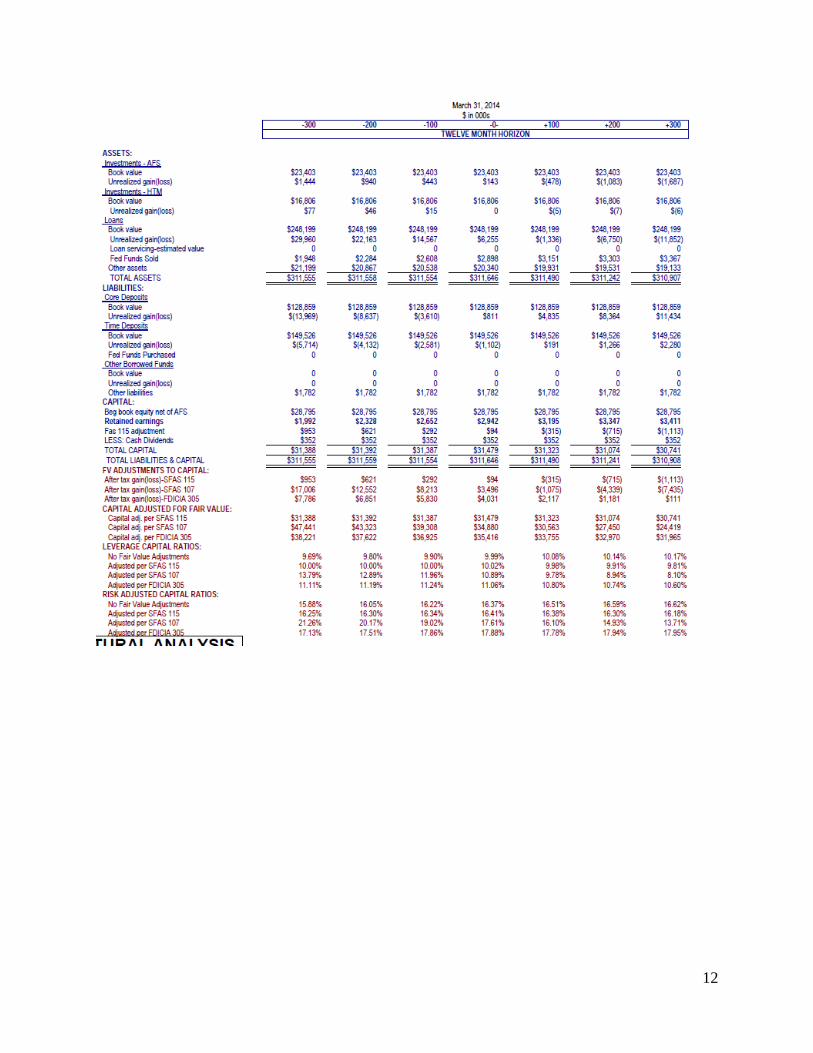

b. With the same 300 basis point increase in rates, why would the leverage ratio improve to

10.60% over a twelve month horizon? And even higher over 24 months? For assistance

in answering this question, please see the Structural BS for both the Immediate Horizon

and the Twelve Month Horizon on the next two pages.

c. What effect would lengthening the decay rates on non-maturity deposits have on the

economic value of equity? Why?

11

12