Download - Management of bank accounts

Management of bank accounts

DOTT. STEFANO BLANCO

DOTT. MASSIMILIANO FONTANA

1

2

Definition of a bank

The bank is a commercial company that carries outsystematically, institutionally and on its own risk afinancial intermediation activity

Definition of a bankAn increasingly important role is taking on the provision of:

•Monetary services

•Financial services

•Consulting services

3

Definition of a bankThe bank is an institution that also engages incurrency and financial transactions using their ownmoney and that of the customers. In particular, thebank accumulates its gains in three ways:

•through the difference between debtors andcreditors rate

•through commissions on the services banks offer

•by carrying out financial operations themselves

4

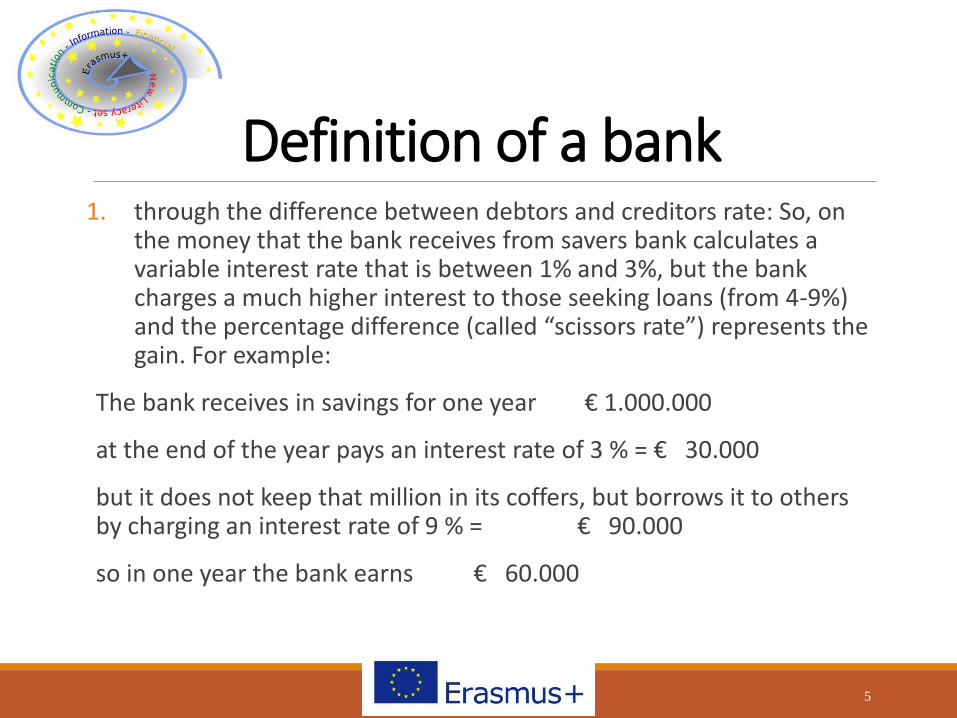

Definition of a bank1. through the difference between debtors and creditors rate: So, on

the money that the bank receives from savers bank calculates a variable interest rate that is between 1% and 3%, but the bank charges a much higher interest to those seeking loans (from 4-9%) and the percentage difference (called “scissors rate”) represents the gain. For example:

The bank receives in savings for one year € 1.000.000

at the end of the year pays an interest rate of 3 % = € 30.000

but it does not keep that million in its coffers, but borrows it to others by charging an interest rate of 9 % = € 90.000

so in one year the bank earns € 60.000

5

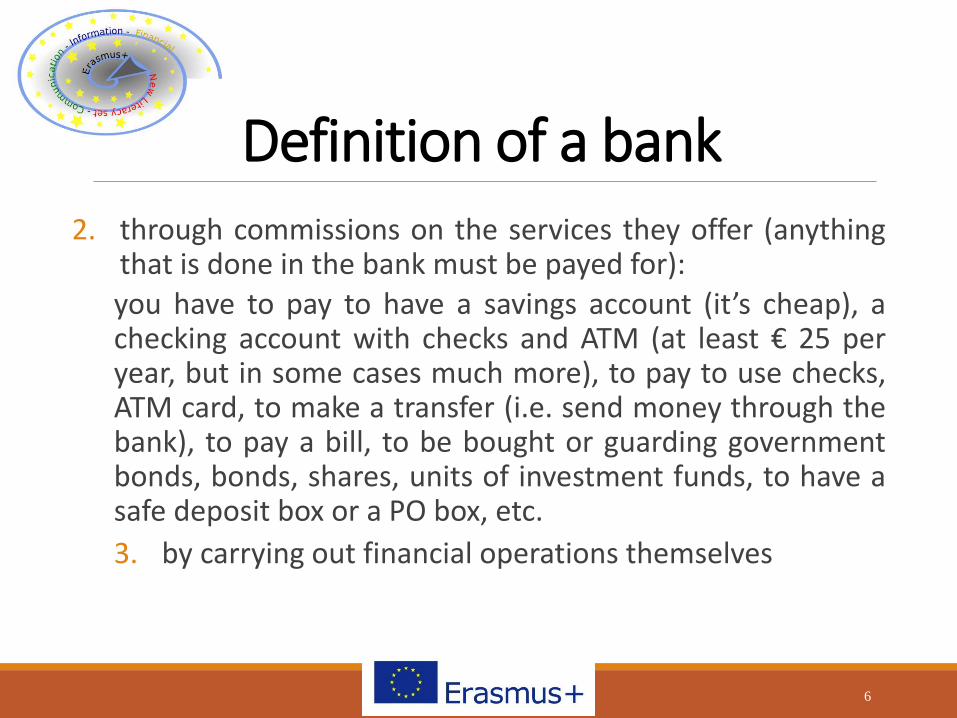

Definition of a bank2. through commissions on the services they offer (anything

that is done in the bank must be payed for):

you have to pay to have a savings account (it’s cheap), achecking account with checks and ATM (at least € 25 peryear, but in some cases much more), to pay to use checks,ATM card, to make a transfer (i.e. send money through thebank), to pay a bill, to be bought or guarding governmentbonds, bonds, shares, units of investment funds, to have asafe deposit box or a PO box, etc.

3. by carrying out financial operations themselves

6

The role of banks in the economyThe best-known financial intermediaries in oureconomic system are the BANKS.

They collect funds from individuals in surplus, givingthem a fee called INTEREST (Active for customers –Passive for the bank), and allowing individuals toborrow in financial deficit from which demand anINTEREST (Passive for customers – Active for banks ).

7

The role of banks in the economy

The bank's earnings is the JAWS RATIOwhich is determined by the differencebetween active interest rate (x bank)and borrowing interest rate (x bank).

8

The role of banks in the economyBanks have intermediary role:

No cash

No finding savers and borrowers personally

No costly lawyers fees for contracts

Bank absorbs loans that default

Banks borrow (i.e. hold customers’ deposits) short-term but lend long-term – this is called „termtransformation”

9

Bank account contract

10

The bank takes on the task

of making payments and

collections on behalf of the

client using the deposited

money

They are recorded:

• As a CREDIT - the deposits by

cash or checks.

• As a DEBT - the payment of

issued checks, bills, credit

transfers and periodic

expenses.

Types of bank accountsThe most important and most commonly used bank accounts are current account and giro account.

Bank accounts are open and run by a credit institution on demand andon behalf of one or more payment service users (clients) for executionof payment transactions.

Who can open an account in a credit institution?

11

What to consider beforedeciding to open an account

account opening costs,

monthly account management costs,

additional features offered with opening an account,

all types of benefits that are linked to the transaction account,

how much are these benefits, whether their amount varies and how,

daily limits for cash withdrawals at ATMs,

the number of ATMs available and their locations (spread of the ATM network and branches of credit institutions),

the interest rate on the positive balance in the account and

terms and conditions associated with closing the account.

12

Opening a bank accountA credit institution opens a current account or a giro account based on a framework contract concluded with a payment service user

When opening an account, a credit institution is obliged to:

confirm your identity,

conduct other procedures in accordance with the regulations in chargeof the prevention of money laundering and terrorist financing,

obtain all information that is required to be submitted for this accountin accordance with the law on a unique account register that regulatesthe contents of the unique account register in the country (ifapplicable).

13

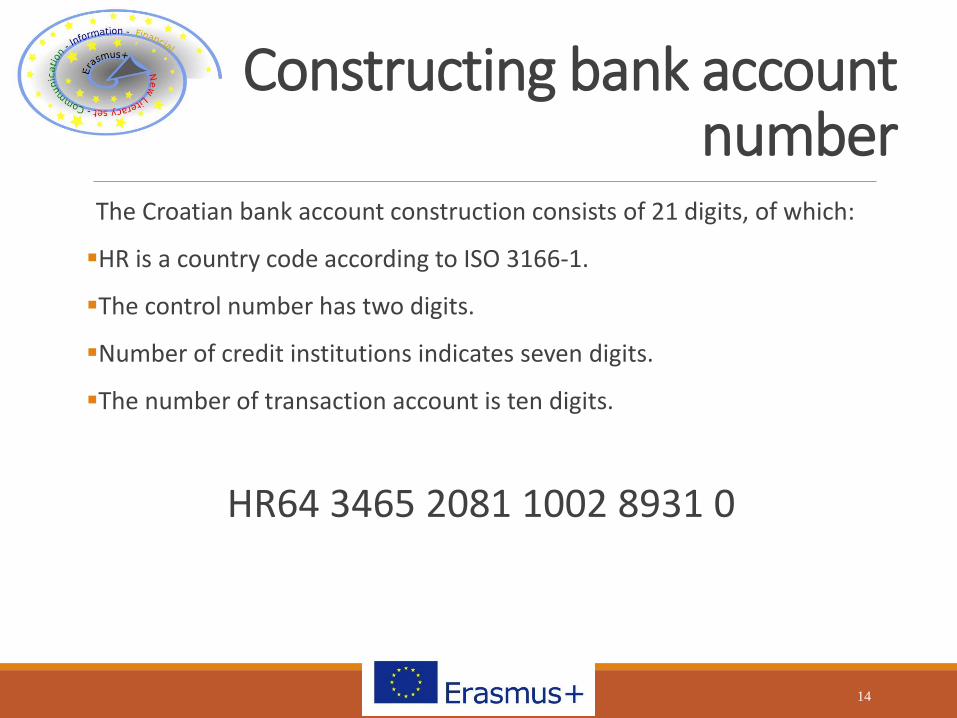

Constructing bank accountnumber

The Croatian bank account construction consists of 21 digits, of which:

HR is a country code according to ISO 3166-1.

The control number has two digits.

Number of credit institutions indicates seven digits.

The number of transaction account is ten digits.

HR64 3465 2081 1002 8931 0

14

Current accountA current account is a transaction account that a bank opens at therequest of consumers for the purpose of receiving regular or casualpayments and making payments within the limits of available funds inthe account

Permissible vs unauthorized overdraft

Related purchase - other banking products and services are usuallylinked to the current account

15

Giro accountThe giro account is a type of transaction account that is primarilyintended for occasional income of individuals

Traditionally, the giro account is used for payments of income such as rent, royalties and the like

16

Account balance

The account balance is thedocument that the bank sendsperiodically to the account holderand consists of three parts:

17

Account balance

-a list, in chronological order, of the movements of the account, that is the real account balance;

18

Account balance

-the progressive summary balance (or progressive account balance), which summarizes the daily balances of the account resulting in currency movements ordered by dates; it is useful for the calculation of interest;

19

Account balance

-the calculation of the compensations (counting costs and interest) that are credited or debited to the account at the end of the period.

20

Account balanceDate (monthly, quarterly, semi-annual)

Iban code (identifies c/c, bank, country)

Date and currency (the accounting transaction date)

“give” and “take” movements (operations credit and debit)

Transactions description (transaction details)

Beginning and ending balance

21

Banca delle Banche Sig. Mario Rossi

Agenzia Sede Indirizzo Via del Varco

C/C N° 14000 Città Viterbo

Estratto

conto

relativo al

4° trimestre dell'anno 2016

DATA VALUTA DARE AVERE DESCRIZIONE OPERAZIONE OPERAZ. NUM N°

1/10 30/9 12410,00 ripresa saldo a 12.410,00 1

2/10 30/9 15,20 Add.competenze III trim.2016 p 12.394,80 2

9/10 9/10 460,00 versamento in contanti a 12.854,80 4

12/10 14/10 1350,00 versamento a/b a 14.204,80 5

17/10 17/10 1555,50 pagato RID periodico p 12.649,30 3

31/10 31/10 59,30 pagata bolletta p 12.590,00 6

11/11 19/11 2668,50 versamento a/b a 15.258,50 7

26/11 26/11 215,00 Pagam.MAV (Pag.Med.Avviso) p 15.043,50 8

30/11 30/11 1808,00 pagamento acconto imposte p 13.235,50 9

2/12 2/12 7918,88 acquisto titoli p 5.316,62 10

10/12 18/12 1819,00 versamento a/b a 7.135,62 11

23/12 23/12 407,80 Rata Mutuo n.12545123 p 6.727,82 12

MOVIMENTI SALDO

22

Progressive summary balance

Currency and currency balances (with the dates when theamounts of the account with the same currency havechanged)

Days (specifies the number of days between that balanceand the next one)

“debtors and creditors numbers” (currency balancemultiplied by the days showed on the side)

Status change (increase or decrease in the interest rate)

The calculation of interest

23

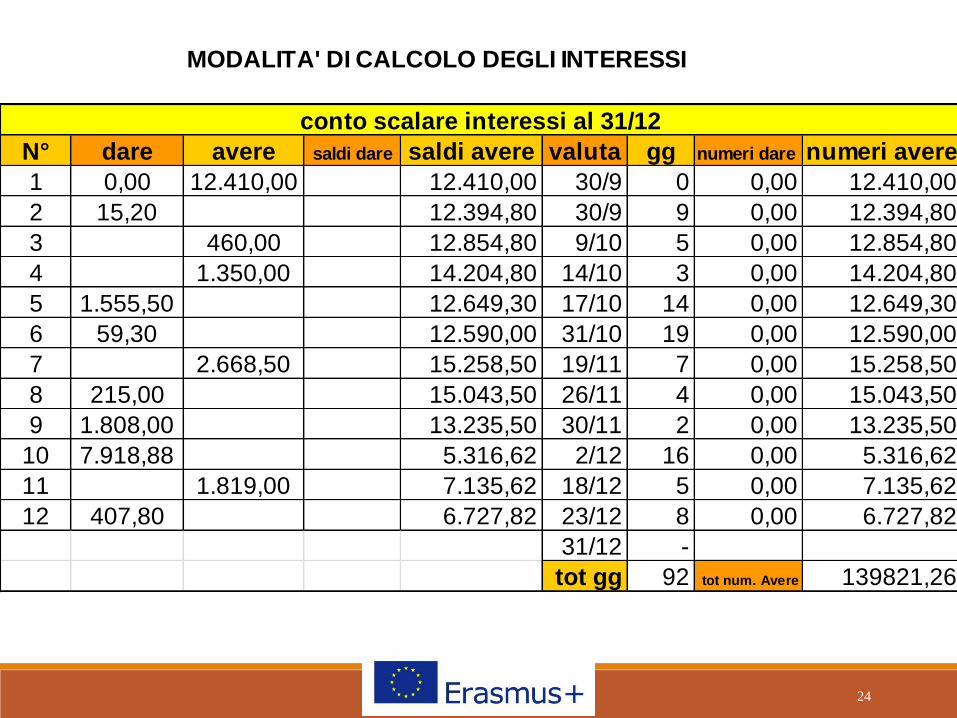

N° dare avere saldi dare saldi avere valuta gg numeri dare numeri avere

1 0,00 12.410,00 12.410,00 30/9 0 0,00 12.410,00

2 15,20 12.394,80 30/9 9 0,00 12.394,80

3 460,00 12.854,80 9/10 5 0,00 12.854,80

4 1.350,00 14.204,80 14/10 3 0,00 14.204,80

5 1.555,50 12.649,30 17/10 14 0,00 12.649,30

6 59,30 12.590,00 31/10 19 0,00 12.590,00

7 2.668,50 15.258,50 19/11 7 0,00 15.258,50

8 215,00 15.043,50 26/11 4 0,00 15.043,50

9 1.808,00 13.235,50 30/11 2 0,00 13.235,50

10 7.918,88 5.316,62 2/12 16 0,00 5.316,62

11 1.819,00 7.135,62 18/12 5 0,00 7.135,62

12 407,80 6.727,82 23/12 8 0,00 6.727,82

31/12 -

tot gg 92 tot num. Avere 139821,26

conto scalare interessi al 31/12

MODALITA' DI CALCOLO DEGLI INTERESSI

24

Interest rates and account fees/costs

Financial Institutions charge you different fees for different services. In addition, the bank may pay you interest for keeping your money at that bank.

25

Digital bankingThe 'digital revolution' is having strong impacts on configuring bankingoffers and service models targeted at retail customers.

Banks which offer their customers online banking are expected to havemore advantageous conditions when compared to traditional channels.

26

Digital bankingBank branches Contact Center ATM Digital

Selling face to face, and of

complex products and services

Parking Areas - advanced

service

specialized

Resources

Commercial

Initiatives commercial

combined network not-bank

distributive

Face 'Human' bank

Principals for outdoor

activities

New Role in contact chat with customers

Support / Integration of other channels

Integration / Synergy with remote

management consultant and chat

Cornerstone of customer retention

support

No phone bank.

Proactive outbound

Extension services available

'Less cash – Less transactions '

Support for “remote”

distribution

Dissemination “not urbanized”

areas

Support in complex operations

using

virtual assistant

'Digital' in the middle of

the bank

Role towards the

customer in the internal

transformation to the

bank

Mobile focus

Continuous

improvement customer

experience

Personalization of

customer services

27