1

Making Social Protection Work for the Informal Sector: The Case of PhilHealth and ALKANSSSYA Program for the Self-Employed

AKI-CBMS Proposal on Social Protection

By: Mitzie Irene P. Conchada and Marites M. Tiongco

April 2015

Abstract: In the DLSU-AKI annual report of Monitoring the Philippine Economy, the Philippines

maintained its growth momentum in 2014, besting other Asian economies. Given this, it is

interesting to find out whether various sectors have benefited from this growth, particularly the

informal sector which includes bulk of the poor who are self-employed and are mostly engaged in

the services sector. The intention of this study aimed to determine the effect of social protection,

particularly PhilHealth and the ALKANSSSYA on informal sector especially those who are poor

and self-employed. By the end of 2014, total benefit payment for all sectors amounted to PhP 78.2

billion (PhP 19.2 billion for the informal sector). Since the government spends so much on the

PhilHealth, especially with its expansion of the indigent program, there is a need to investigate the

effectiveness of the program especially on the poor. Utilizing data from the Community Based

Monitoring Survey (CBMS) collected in2015 from selected provinces in the Philippines, the

propensity score matching method showed that those who availed of PhilHealth(both individual

paying and sponsored member) have a higher total income and income in cash compared to those

who did not avail (PhP288 and PhP595 respectively). PhilHealth beneficiaries are also more likely to

have higher total sales from entrepreneurial activities in the informal sector (PhP69) than non-

beneficiaries. On the other hand, ALKANSSSYA beneficiaries also had higher annual income,

higher total sales from entrepreneurial activities and higher expenditure than non-beneficiaries

(PhP986, PhP18, and PhP304 respectively). The results support the claim that social protection is

indeed effective in improving the income of the poor, especially those who are dependent on the

2

informal sector. Expanding the coverage of the programs for the informal sector, thus, will aid in

increasing social inclusion and in reducing poverty levels.

3

I. INTRODUCTION

In the DLSU-AKI annual report of Monitoring the Philippine Economy, the Philippines

maintained its growth momentum in 2014, besting other Asian economies. Despite doubts over

growth prospects and challenges in the external market, the Philippine economy attained a solid 6.1

percent growth in 2014. Favorable demand and supply side factors combined with improvements in

the global market, particularly a recovering US economy and intensifying demand in Asia, led to the

6.1 percent growth in the country’s Gross Domestic Product (GDP). This brings the year-end

forecast to a higher estimate (Monitoring the Philippine Economy, January 2014). Given this, it is

interesting to find out whether various sectors have benefited from this growth, particularly the

informal sector, which includes bulk of the poor who are self-employed and are mostly engaged in

the services sector.1

Despite the performance of the economy, unemployment still remains one of the major

concerns. By the end of 2014, unemployment rate was recorded at 6.8 percent which implies that

there is still a large number of Filipinos who are unemployed given our population. Moreover, the

Philippine Statistics Authority (PSA)reported that most of the unemployed were males, high school

graduates and belonged to the age group 15 to 24 years old (Philippine Statistics Authority, 2014).

Given fewer stable job opportunities in the country, Filipinos are seeing entrepreneurship as an

alternative to earn income.

1The authors adapt the operational definiton of the informal sector by the Philippine Statistics Authority (PSA),

which shall refer to “household unincorporated enterprises which consist of both informal own-account enterprises and enterprises of informal employers. Informal own-account enterprises are household unincorporated enterprises owned and operated by own-account workers, either alone or in partnership with member/s of the same or other households which may employ unpaid family workers as well asoccasionally /seasonally hired workers but do not employ employees on continuing basis. Enterprises of informalemployers are household unincorporated enterprises owned and operated by own-account workers, either alone or in partnership with members of the same or other household which employ one or more employees on a continuing basis…”

4

As of 2012, there were 940,886 registered micro, small and medium enterprises (MSMEs) in

the Philippines (99.6 percent of the total establishments), majority of which are in the retail and

wholesale industry.Despite this impressive number, there is a huge number of businesses, mostly

belonging to self-employed Filipinos, that are not registered and are part of what is called the

informal sector. There are many barriers as to why many of them are not registered and one of the

reasons is the high opportunity cost of having to register their business especially for micro

establishments such as sari-sari stores, food stalls and other small scale businesses.

More often than not, these businesses belonging to the informal sector are exposed to

different types of shocks, both internal and external such as sickness in the family and natural

disasters. Their vulnerability to shocks hinders the business from realizing its full potential and thus

resources are wasted. To protect the informal sector from shocks, the government invested in social

protection. The definition of social protection in the Philippines was formalized in 2007 and covers

four components namely: social insurance, social welfare, social safety nets, and labor market

interventions (International Labor Organization, 2014). On the other hand, the National Economic

Development Authority (NEDA) is a set of policies and programs that seek to reduce proverty and

vulnerability to risks and to enhance social status and rights of the marginalized. One of the

initiatives on social protection was the passage of the National Health Insurance Act in 1995 which

aims to provide equitable access to quality health care to everyone (International Labor

Organization, 2014). Through the Act, the National Health Insurance System or PhilHealth was

established to implement universal health care by the year 2016. As of the December 2014, there

were a total of 2,023,696 members in the informal sector, which is only 9 percent of the informal

sector (PhilHealth, 2014). Membership has increased by 62,586 by the end of December 2015, but in

terms of proportion, growth has remained at 9 percent of the informal sector (Philhealth, 2015a). It

5

is thus important to increase the coverage of the informal sector since they are more vulnerable to

shocks.

According to the International Labor Organization (2014), social protection is crucial as the

country faces socio-economic factors that affect the population. For one, the Philippines has most

unequal income distribution among East Asian middle-income countries. Second, general and youth

unemployment are high (7.1% and 16.6% respectively). Furthermore, the rapid population growth

at the rate of 1.9% places pressure on the labor market. Third, aside from unemployment, a high

percentage of the employed are considered vulnerable (38.4%). Fourth, a strong service sector is

prevalent which requires more man power. Lastly, the exposure of the country to natural disasters

such as typhoons makes it more vulnerable (International Labor Organization, 2014).

It is the intention of this study to determine the effect of social protection, particularly

PhilHealth and the ALKANSSSYA2 on informal sector especially those who are poor and self-

employed.3By the end of 2014, total benefit payment for all sectors amounted to PhP 78.2 billion

(PhP 19.2 billion for the informal sector).Since the government spends so much on the PhilHealth,

especially with its expansion of the indigent program, there is a need to investigate the effectiveness

of the program especially on the poor.There are many programs aimed towards the informal sector

but there are a few studies on this. This study will focus on answering the research question: ―Are

people in the informal sector better-off availing PhilHealth and the ALKANSSSYAprogram?‖

Specifically, the research aims to address the following objectives:

1. Provide an overview of the coverage of the Philhealthand the ALKANSSSYA program

in the informal sector

2 The AlkanSSSya is an innovative saving mechanism which allows people to pay premiums whenever they can. It

was introduced by Social Security System to address expansion coverage of PhilHealth to include the informal sector.

6

2. Identify barriers to access Philhealth and the ALKANSSSYA program in the informal

employment

3. Determine whether PhilHealth and ALKANSSSYA members experienced an

improvement in the income of the poor who are part of informal sector.

7

II. REVIEW OF RELATED LITERATURE

a. Poverty in the Philippines

In an effort to address poverty through the MDGs on human capital development through

education, health and women empowerment, various programs have been implemented. However,

progress has been slow in reducing poverty. Table 2.1 shows that poverty incidence in the

Philippines has not improved that much since the year 2003. Moreover, the magnitude of poor

families has increased from 3.8 million families in 2006 to 4.2 million in 2012 (NSCB, 2012). The

poverty incidence among Filipino families in 2012 was the highest in the regions ARMM, Eastern

Visayas (region 8), and Soccsksargen (region 12) with 48.7 percent, 37.4 percent, and 37.1 percent

respectively. In the region ARMM, Lanao del Sur had the most severe incidence of poverty among

families with 67.3 percent. This was followed by Maguindanao with 54.5 percent families of the

total number of families who are considered poor.

Table 2.1First Semester Poverty Incidence Among Families (%)

Major Island Group

1991

First Semester Poverty Incidence among Families (%)

2003 2006 2009 2012 2015 Increase/Decrease

06-09 09-12 12-15

PHILIPPINES 29.7 22.9 23.4 22.9 22.3 21.1 (0.5) (0.5) (1.3)

Luzon

14.73 15.4 15.0 14.5 13.4 (0.4) (0.5) (1.0)

NCR

2.8 3.7 3.8 4.5 0.9 0.1 0.7

Without NCR

19.3 18.4 17.6 16.1 (0.9) (0.8) (1.5)

Visayas

32.44 31.6 30.7 29.1 28.7 (0.9) (1.6) (0.4)

Mindanao

35.17 36.2 35.6 36.0 33.8 (0.6) 0.4 (2.1)

8

Source: Philippine Statistical Authority. 2016. Data downloaded on April 10, 2015 from http://psa.gov.ph/poverty-press-releases2/data

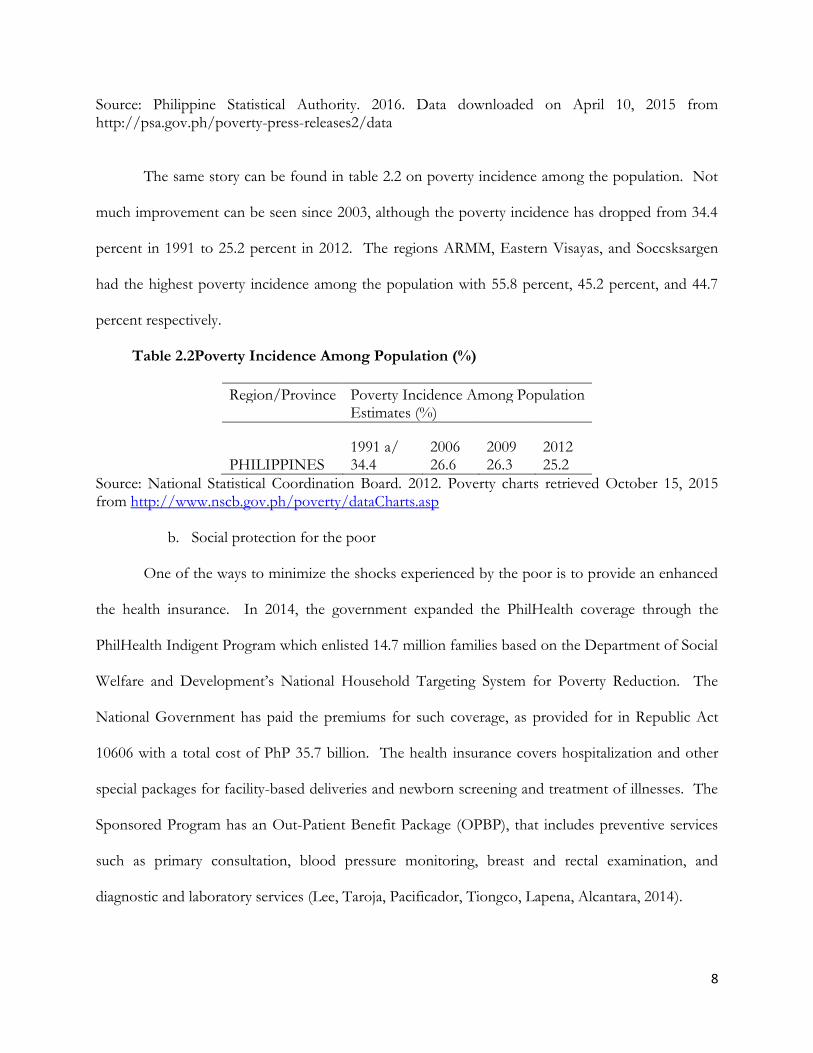

The same story can be found in table 2.2 on poverty incidence among the population. Not

much improvement can be seen since 2003, although the poverty incidence has dropped from 34.4

percent in 1991 to 25.2 percent in 2012. The regions ARMM, Eastern Visayas, and Soccsksargen

had the highest poverty incidence among the population with 55.8 percent, 45.2 percent, and 44.7

percent respectively.

Table 2.2Poverty Incidence Among Population (%)

Region/Province Poverty Incidence Among Population

Estimates (%)

1991 a/ 2006 2009 2012

PHILIPPINES 34.4 26.6 26.3 25.2

Source: National Statistical Coordination Board. 2012. Poverty charts retrieved October 15, 2015 from http://www.nscb.gov.ph/poverty/dataCharts.asp

b. Social protection for the poor

One of the ways to minimize the shocks experienced by the poor is to provide an enhanced

the health insurance. In 2014, the government expanded the PhilHealth coverage through the

PhilHealth Indigent Program which enlisted 14.7 million families based on the Department of Social

Welfare and Development’s National Household Targeting System for Poverty Reduction. The

National Government has paid the premiums for such coverage, as provided for in Republic Act

10606 with a total cost of PhP 35.7 billion. The health insurance covers hospitalization and other

special packages for facility-based deliveries and newborn screening and treatment of illnesses. The

Sponsored Program has an Out-Patient Benefit Package (OPBP), that includes preventive services

such as primary consultation, blood pressure monitoring, breast and rectal examination, and

diagnostic and laboratory services (Lee, Taroja, Pacificador, Tiongco, Lapena, Alcantara, 2014).

9

Aside from the Indigent Program, PhilHealth also has a specific program for those who are

part of the informal sector. This includes street hawkers, market vendors, pedicab and taxi drivers,

small-time construction workers, and home-based industries and services. They also cover

dependents such as the legitimate spouse, child or children below 21 years old and are still

unmarried, children above 21 years old but are suffering from physical or mental disability, and

parents who are 60 year old and above (Philhealth, 2015b).

Another social protection program from the government is Social Security System’s (SSS)

program for self-employed people. The program includes self-employed professionals, owners of

business, farmers and fisherfolk, and workers in the informal sector such as market and ambulant

vendors, public utility transport drivers, tourism industry-related workers, and others in a similar

situation (https://www.sss.gov.ph/sss/appmanager/pages.jsp?page=selfemployedcoverage).

Launched in 2011, AlkanSSSya is a micro-savings program intended for self-employed members in

the informal sector, particularly those who have irregular income such as tricycle drivers and market

vendors. It is designed to fit the way of life of informal sector workers and to make saving for

monthly SSS premiums as affordable as only P11.00 per day for a minimum SSS monthly

contribution of Php330. The informal sector groups are organized and are registered as SSS Self-

employed members that must meet the monthly salary of Php3,000. Those who have a higher

month salary can contribute a higher monthly contribution.

Prior to AlkanSSSya, there were already several affordable saving schemes through commercial

banks introduced by SSS. However, there was very low participation from the informal sector

because saving was difficult to do for those who had highly irregular incomes in addition to being

risk averse to formal banking transactions.

TheAlkanSSSya derived its concept from a piggy bank, and makes use of large metal safety box with

secure individual compartments in which members can put their savings to pay for their monthly

10

contribution. The money saved will be picked up by SSS authorized collectors by the end of the

month and will be credited to their monthly contribution. This does away with the hassle of having

to go to a bank or the SSS office to remit their money, which is often of the hindrances that

members experience. The program was initially conceptualized for tricycle drivers in Las Pinas but

has spread nationwide because of its effectivity and popularity. This has deemed to be successful

because of the benefits of the micro-savings program

(http://www.philstar.com/business/2013/06/09/951731/sss-expands-alkansssya-program-inmates-

drivers. The program has more than 80 partners across the country that service the self-employed

and the informal sector workers.

These social security programs are aimed at minimizing the negative impact of internal and

external shocks that may affect families who are dependent on self-employment and informal sector

activities. Very few studies have shown theeffectivity of social security programs for the informal

sector thus this study aims to look deeper into how the program works and what benefits do the

beneficiaries receive compared to non-members.

11

III. EMPIRICAL MODEL AND METHODOLOGY

In assessing whether the social security programs of PhilHealth and SSS are effective, the

study will employ and impact evaluation. Usui (2011) discussed the various approaches to

conducting an impact evaluation study. The basic idea behind an impact evaluation study is to

compare the indicators before and after the implementation of the program. Setting up time-bound

and measurable performance indicators is very important because this will allow proper monitoring

and evaluation. Usui (2011) identifies the first step as setting up an ex-ante target for each

performance indicator with a specific time frame. To determine the impact of the program, the

actual value of the indicator is measured at a certain stage after completion of the project (Usui,

2011). The baseline value is usually used as a point of comparison. This baseline could be the initial

characteristics of the household before implementation of the program.

The study will evaluate the impact of the programs on the informal sector using propensity

score matching. Propensity score matching, as developed by Rosenbaum and Rubin (1983), is a

statistical technique that tries to estimate the effect of an intervention or treatment given certain

covariates that predict receiving the treatment. The PSM technique is used for observational data to

estimate the impact of an intervention and helps answer the question ―what is the treatment effect

on the treated.‖ In the case of this study, we answer the question what is the impact of PhilHealth

and Social Security System’s AlkanSSSyaon income and health expenditures of the beneficiaries.

Moreover, the PSM technique establishes the counterfactual, that is what would have happened to

the beneficiaries had they not received the social protection program. Through the PSM a proper

counterfactual can be found by matching a beneficiary to a non-beneficiary with similar pre-

intervention characteristics (also called covariates). For the households with matched characteristics,

each has an equal chance of becoming a beneficiary or non-beneficiary (Capuno, 2013).

12

For observational studies such as this, the assignment of treatments to subjects is not

randomized and the PSM thus mimics an experiment by creating a sample of units that received the

treatment that is comparable on all observed covariates to a sample of units that did not receive the

treatment. The propensity scores that will be generated will be used to match a beneficiary to a non-

beneficiary, which is better than using covariates to match the two groups because the latter has too

many dimensions which may result in the failure of common support (Capuno, 2013).

In carrying out the PSM in this study, the following steps will be implemented. First,

covariates (independent variables) that simultaneously influence participation into the program as

well as the outcome will be selected. The covariates and outcome will then used in the probit model

that would help estimate the propensity score.

In the absence of pre-treatment data, we will use time invariant observable variables in the

study. We will use household characteristics such as gender of the household head (1 if male, 0

otherwise), highest educational attainment of the household, age of the household head, and family

size. The treatment variable shall be whether the household is a beneficiary or not of the two social

security programs. The model will be regressed against several outcome variables such as income

and health expenditures.

The model is described as:

Pr 𝑆𝑆 = 1 = 𝐹(𝛽1 + 𝛽2𝑖𝑛𝑑𝑖𝑣𝑖𝑑𝑢𝑎𝑙 𝑐ℎ𝑎𝑟𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑖 + 𝛽3ℎ𝑜𝑢𝑠𝑒ℎ𝑜𝑙𝑑 𝑐ℎ𝑎𝑟𝑎𝑐𝑡𝑒𝑟𝑖𝑠𝑡𝑖𝑐𝑠𝑖 +

𝛽4𝑤𝑒𝑎𝑙𝑡ℎ 𝑖𝑛𝑑𝑒𝑥𝑖 + 𝜀𝑖)

The equation was used for both the PhilHealth and Social Security System’s AlkanSSSya.

The equation above describes the relationship of the independent variables which are the

characteristics of the household, characteristics of the individual and wealth index to whether they

are beneficiaries or non-beneficiaries of PhilHealth and AlkanSSSya programs using the latest

13

Community Based Monitoring System which includes questions on unemployment, social protection

and entrepreneurship.

The outcomesincluded in the study were total income, total income in cash, wage in cash,

total sales from entrepreneurial activities, and total expenditure in cash.

14

IV. RESULTS AND ANALYSIS

Making PhilHealth and SSS accessible to the informal sector might be a challenge in itself as

contribution is not mandatory and accessibility might post a cost to the contributor. Despite the

long term benefits that could be drawn from the program, the short-sightedness and lack of

foresight of some individuals can hinder them from availing of the program (SOURCE?).

PhilHealth

According to Sifverberg (2016), Philhealth coverage rates were at 56-58%, indicating that

over 40% of people who did not qualify as dependents and are unemployed did not have healthcare.

The study also noted that Bicol and Eastern Visayas Regions had some of the lowest rates at 23.85%

and 28.95% respectively, although Sulu and Tawi-tawi posted even worse rates of 3% (Silfverberg,

2016).

Sifverberg (2016) mentioned in that the availability of health care resources in the area

seemed to be an essential factor in the ensuing level of coverage in the province, with more private

hospitals making it more likely for a province to have higher coverage rates. Moreover, Sifverberg

(2016)stated that the problem may have to do with informal sector workers sometimes classifying

themselves as members of the formal sector. Sifverberg (2016) therefore recommended that the

government channel funds into the health insurance system instead of public providers and examine

the depth of Philhealth coverage, especially the Individually Paying Program, since some people may

perceive that coverage will end up accounting for only a minute part of their medical expenses.

AlkanSSSya

According to SSS’ 2014 Annual Report, the AlkanSSSya Program was conceived by the SSS

as a service to informal sector workers like public utility vehicle drivers, market vendors, farmers,

fishermen, and prison detainees, who face demands to focus on basic needs in addition to 12-14

15

hour work days, and thus do not have the time to learn about and exercise financial planning. It

allows for members to save as little as P12 day or around P330 a month; it serves just like a literal

piggy bank for savings for the future (SSS, 2014).

Since the implementation of the AlkanSSSya Program in 2011 until December 2014, it has

covered 122,387 members of 1,236 informal sector groups (ISGs), collecting P167m in

contributions. The program experienced an improvement in 2014, achieving a coverage of 63,758

members from 673 ISGs, more than half of all cumulative members and reached ISGs since 2011;

total contributions also reached P66.2m in 2014, accounting for 40% of the cumulative

contributions since 2011

https://www.sss.gov.ph/sss/DownloadContent?fileName=SSS2014_Annual_Report.pdf).

Barriers to Social Security

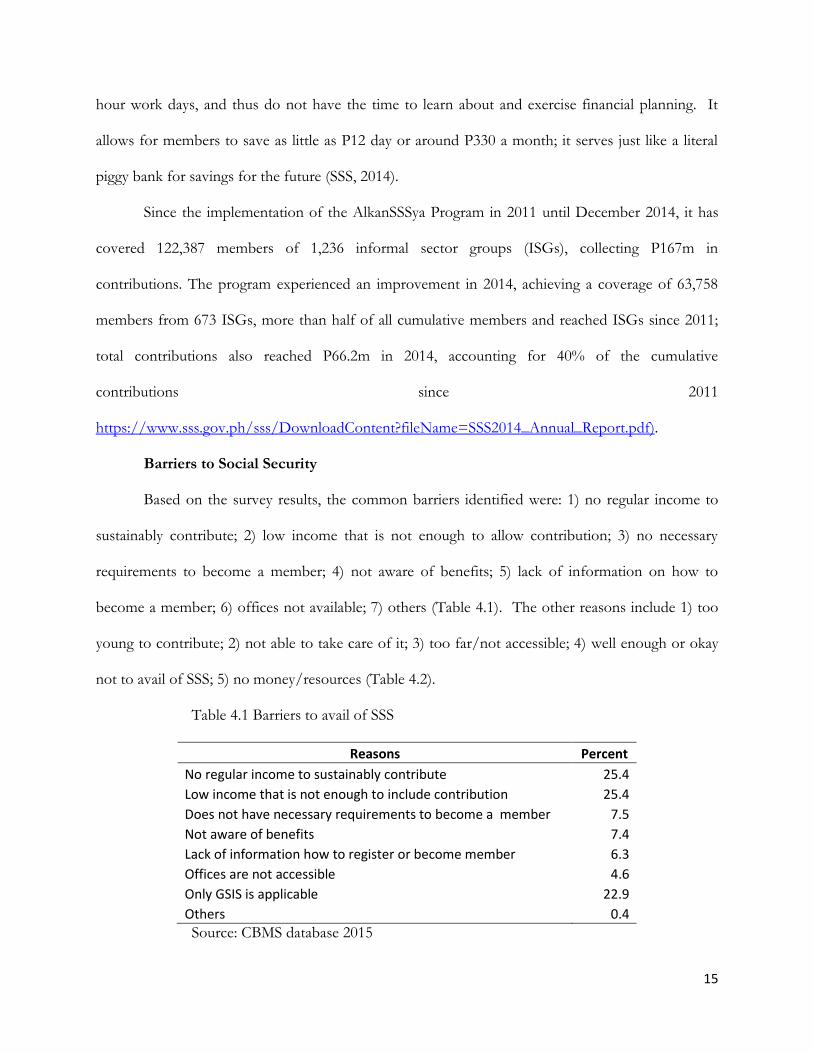

Based on the survey results, the common barriers identified were: 1) no regular income to

sustainably contribute; 2) low income that is not enough to allow contribution; 3) no necessary

requirements to become a member; 4) not aware of benefits; 5) lack of information on how to

become a member; 6) offices not available; 7) others (Table 4.1). The other reasons include 1) too

young to contribute; 2) not able to take care of it; 3) too far/not accessible; 4) well enough or okay

not to avail of SSS; 5) no money/resources (Table 4.2).

Table 4.1 Barriers to avail of SSS

Reasons Percent

No regular income to sustainably contribute 25.4

Low income that is not enough to include contribution 25.4

Does not have necessary requirements to become a member 7.5

Not aware of benefits 7.4

Lack of information how to register or become member 6.3

Offices are not accessible 4.6

Only GSIS is applicable 22.9

Others 0.4

Source: CBMS database 2015

16

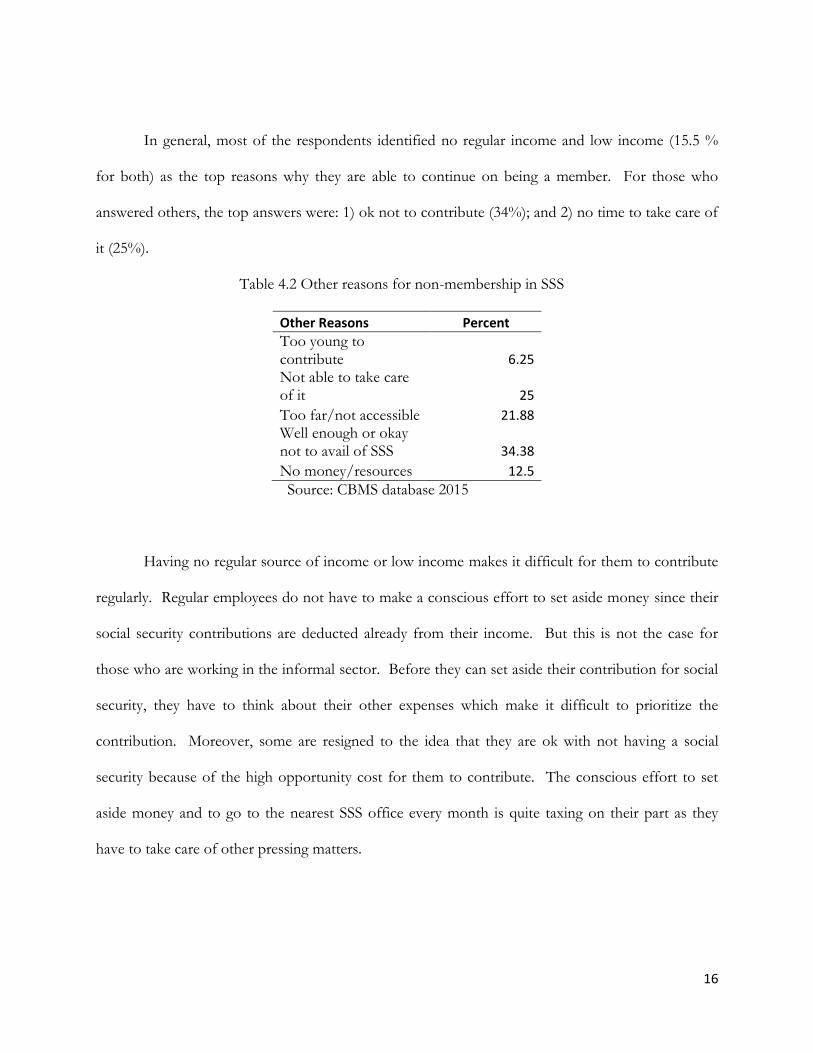

In general, most of the respondents identified no regular income and low income (15.5 %

for both) as the top reasons why they are able to continue on being a member. For those who

answered others, the top answers were: 1) ok not to contribute (34%); and 2) no time to take care of

it (25%).

Table 4.2 Other reasons for non-membership in SSS

Other Reasons Percent

Too young to contribute 6.25 Not able to take care of it 25

Too far/not accessible 21.88 Well enough or okay not to avail of SSS 34.38

No money/resources 12.5

Source: CBMS database 2015

Having no regular source of income or low income makes it difficult for them to contribute

regularly. Regular employees do not have to make a conscious effort to set aside money since their

social security contributions are deducted already from their income. But this is not the case for

those who are working in the informal sector. Before they can set aside their contribution for social

security, they have to think about their other expenses which make it difficult to prioritize the

contribution. Moreover, some are resigned to the idea that they are ok with not having a social

security because of the high opportunity cost for them to contribute. The conscious effort to set

aside money and to go to the nearest SSS office every month is quite taxing on their part as they

have to take care of other pressing matters.

17

Descriptive Statistics

The next section discusses variables that were used in the study based on the propensity

score model. There were a total of 283 respondents for the AlkanSSSya program, 138 were

beneficiaries and 145 non-beneficiaries. For the PhilHealth individual paying and sponsored

programs, there were a total of 10,483 individuals: 5,233 were beneficiaries and 5,250 were non-

beneficiaries.

Table 4.3 Descriptive statistics for PHILHEALTH

Variable Definition Mean Std. dev Min Max

Dependent variable Availprog Availed of PHILHEALTH 0.4992 0.5000 0 1

Independent variables wi_simple Wealth index 1 (simple) 0.2318 0.1571 0 0.9565

educal1 Grade school 0.3269 0.4691 0 1

educal2 College 0.0551 0.2283 0 1

educal3 Technical vocation 0.0096 0.0977 0 1

sex Male or female 0.5038 0.5000 0 1

internet Access to internet 0.0315 0.1746 0 1

unemp Unemployed 0.0198 0.1395 0 1

Outcomes totin Total income 76,482 46,819 0 401,000

totincsh Total income in cash 61,012 44,062 0 365,000

wagcsh Wage in cash 41,597 43,773 0 365,000

totexp Total expenditures 138 3,221 0 190,000

Number of observations 10,438 Income and expenditure are in current prices (Philippine pesos) and represent annual figures.

Table 4.3 provides some information about the characteristics of individuals who are

beneficiaries and non-beneficiaries of PhilHealth in the CBMS 2015. The beneficiaries and non-

beneficiaries were from NCR: Manila and Marikina, Batangas, Cavite, Negros Occidental, and

Misamis Occidental. Almost half of the individuals who are part of the informal sector are females.

18

Most of them are married, have high school as their highest educational attainment, and belong to a

family with an average size of 6 members. When it comes to the economic profile of the

individuals, the average annual total income (in cash) is PhP61,012 while the average wage is

PhP41,597.Only a few of them are unemployed as most are self-employed in different kinds of

economic activities, especially those related to the services sector. Since all of the respondents are

poor, access to household appliances, land, and a vehicle is very low: only less than ¼ or 23% have

access to such wealth variables. Moreover,access to internet which measures social connectedness is

also very low: only 3% of the respondents have access. The next table describes the profile of the

respondents who availed of the ALKANSSSYA program.

The profile of those who availed of ALKANSSSYA is almost similar to the PhilHealth

beneficiaries except that all the respondents are from Marikina. Most of the respondents are females

(54%) and are married, and have high school as their highest educational attainment. Only 9 percent

have finished college and 3 percent have finished a technical/vocational course. Most of them

belong to a family of 6 and rely on self-employment activities. The individuals who are engaged in

activities in the informal sector are mostly in the retail business (44%): sari-sari store, food vendors;

and are engaged in the services sector (25%) - either drivers, carpenters, work in the parlor as a

stylist, manicurist, etc.

19

Table 4.4 Descriptive statistics for ALKANSSSYA

Variable Definition Obs Mean Std. dev Min Max

Dependent variable

availprog Availed of ALKANSSSYAprogram 283 0.4876 0.5007 0 1

Independent variables wi_factora~s Wealth index 2 (factor analysis) 283 0.0000 4.2115 -11.12 8.54

phsize Family size 283 6.4558 2.7068 1 15

educal1 Grade school 283 0.2898 0.4545 0 1

educal2 College 283 0.0919 0.2894 0 1

educal3 Technical vocation 283 0.0353 0.1850 0 1

sex Male or female 283 0.4629 0.4995 0 1

civstat1 Widow 283 0.0530 0.2244 0 1

civstat4 Married 283 0.3604 0.4810 0 1

internet Access to internet 283 0.0777 0.2682 0 1

unemp Unemployed 283 0.0742 0.2626 0 1

Outcomes

totin Total income 283

78,227

62,549 0

240,000

totincsh Total income in cash 283

49,009

54,961 0

240,000

Wagcsh Wage in cash 283

40,235

52,715 0

194,000

totsales Total sales from entrep activities (cash) 65

77

620 0

5,000

Totexp Total expenditures 65

1,969

14,886 0

120,000

Number of individuals 146 Income and expenditure are in current prices (Philippine pesos) and represent annual figures.

The indicator for social connectivity or access to internetis very low, only 7% have a access.

Moreover, access to the other household appliances, land and a vehicle is very low. In fact, on the

average, the individuals belong to households that do not have any of the appliances which is an

indicator of how poor the households are. The average total income (annual) is PhP78,227 or

P6,519 monthly; average wage (annual, in cash) is PhP40,235 or PhP3,353. Total sales from their

entrepreneurial activity is only PhP77 and average expenditure is PhP1,969.

20

Both beneficiaries and non-beneficiaries of the PhilHealth and AlkanSSSya programs are

poor and almost have no ownership to property such as land and other assets. Their main source of

income is from self-employment activities that yields a very low income and may not be enough to

meet the needs of the family. Given their economic status, being a member of the PhilHealth and

Alkansssya programs would help augment their expenses especially in health care.

Propensity score matching results

To determine the impact of the PhilHealth and Alkansssya programs, the study compared

the impact on beneficiaries and non-beneficiaries. The study made sure that the characteristics of

the two groups were the same in order to find out the counterfactual: what have happened if the

program was not implemented?Controlling for the characteristics of the two groups would really

point out the impact of the programs. For the PhilHealth program, there were a total of 10,438

individuals: 5,233 were beneficiaries and 5,250 were non-beneficiaries. For the AlkanSSSya

program, there were a total of 283 respondents: 138 were beneficiaries and 145 non-beneficiaries.

The non-beneficiaries were randomly chosen from a pool of non-beneficiaries who had the same

characteristics as those with the beneficiaries.

The following results are based on the Community Based Monitoring System 2015 database.

The study used the Propensity Score Method (PSM) which is an impact evaluation tool used when

no baseline survey has been conducted and the only data available are the characteristics of the

beneficiaries. The aforementioned method is a quasi-experiment that tries to determine what would

have happened if the program was not implemented. The model used in the study is described as:

𝑃𝑟𝑆𝑆 = 𝐹(𝛽1 + 𝛽2𝑤𝑒𝑎𝑙𝑡ℎ 𝑖𝑛𝑑𝑒𝑥𝑖 + 𝛽3ℎ𝑜𝑢𝑠𝑒ℎ𝑜𝑙𝑑 𝑠𝑖𝑧𝑒𝑖 + 𝛽4𝑠𝑒𝑥𝑖 + 𝛽5𝑒𝑑𝑢𝑐𝑖 + 𝛽6𝑖𝑛𝑡𝑒𝑟𝑛𝑒𝑡𝑖

+ 𝛽7𝑢𝑛𝑒𝑚𝑝𝑖 + 𝛽8𝑐𝑖𝑣𝑠𝑡𝑎𝑡𝑖 + 𝜀𝑖

where: Wealth index – index durable assets such as land, housing, etc to capture personal

21

security and privacy

Household size – number of family members

Sex – whether male or female (with value equal to 1 if male, 0 if female)

Educal – highest educational attainment as proxy for living standards — the higher the

education the more likely to raise living standards

Internet – internet connection; proxy for social connectedness as dimensions for well-

being/welfare

Unemp – dummy variable for whether the individual is unemployed or not (1 if

unemployed, 0 if employed)

Civstat – dummy variables for various civil status (with value equal to 1 if married, 0 if

not married 0; widowed, 1, not widowed, 0; live-in, 1, not live-in, 0; and

separated, 1, not separated 0)

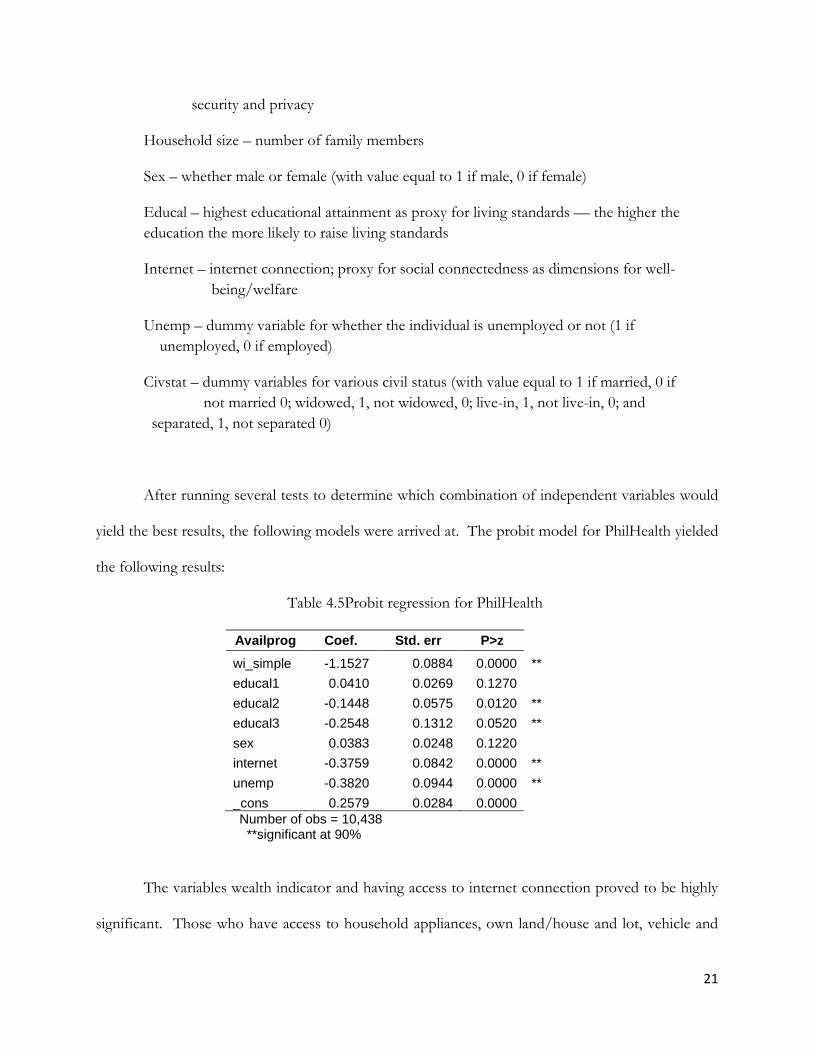

After running several tests to determine which combination of independent variables would

yield the best results, the following models were arrived at. The probit model for PhilHealth yielded

the following results:

Table 4.5Probit regression for PhilHealth

Availprog Coef. Std. err P>z

wi_simple -1.1527 0.0884 0.0000 **

educal1 0.0410 0.0269 0.1270 educal2 -0.1448 0.0575 0.0120 **

educal3 -0.2548 0.1312 0.0520 **

sex 0.0383 0.0248 0.1220 internet -0.3759 0.0842 0.0000 **

unemp -0.3820 0.0944 0.0000 **

_cons 0.2579 0.0284 0.0000 Number of obs = 10,438

**significant at 90%

The variables wealth indicator and having access to internet connection proved to be highly

significant. Those who have access to household appliances, own land/house and lot, vehicle and

22

internet connection are not likely to be poor thus will not enroll in the individual paying or

sponsored program. The poor who are usually not employed and rely only on economic activities in

the informal sector are less likely to avail of the PhilHealth program due to several reasons. One of

them is not having extra income/profit to pay for the monthly premium. This goes to say that

individuals who are unemployed are not likely to avail of PhilHealthindividual paying or sponsored

program. The barriers which is mainly lack of income, especially when they are unemployed,

prevents them from being a member. The educational attainment of the individual was also

significant, particularly those who were college and technical/vocational graduates. Those who have

finished college and technical/vocational courses are (14% and 25% respectively) not likely to avail

of the PhilHealth individual paying program. These individuals are more likely to have a full time

job, thus wouldn’t require availing of PhilHealth’s individual paying program.

The next table describes the probit regression results for the AlkanSSSya program.

Table 4.6Probit regression for AlkanSSSya

availprog Coef. Std. err P>z

wi_factora~s 0.0224 0.0209 0.2830

phsize 0.0107 0.0286 0.7070

educal1 0.0360 0.1760 0.8380

educal2 0.1465 0.2790 0.5990

educal3 0.0910 0.4227 0.8290

sex 0.0789 0.1573 0.6160

civstat1 0.3163 0.3526 0.3700

civstat4 0.1899 0.1717 0.2690

internet -0.8213 0.3348 0.0140 **

unemp 0.0403 0.3001 0.8930

_cons -0.1511 0.2393 0.5280

Number of obs = 283 **significant at 90%

The probit regression results reveal that there is only one variable that turned out to be

significant: access to internet. Access to internet, which measures social connectivity, decreases the

probability (82%) of availing the AlkanSSSya program. An individual who has access to internet is

23

more likely to be non-poor and would more likely to have a regular job where his SSS contributions

are automatically deducted.

After performing balancing tests and robustness of the PSM, the last step performed was to

estimate the average treatment effect (ATT) using the beneficiaries (poor individuals who are part of

the informal sector who availed of PhilHealth and ALKANSSSYA) versus the non-beneficiaries.

The results are summarized in the table below:

Table 4.7PSM results: For PhilHealth beneficiaries and non-beneficiaries

Treated Control ATT Std. Err. t-value

Total income per capita 5233 5031 607.58 104.57 5.81 **

Total income in cash per capita 5233 5031 992.96 102.45 9.69 **

Wage in cash per capita 5233 5031 146.33 114.09 1.28 *

Total expen cash per capita 5233 5031 4155.98 509.51 8.15 **

*statistically significant at p<0.10 **statistically significant at p<0.05

To check the robustness of the ATT results, the study used Nearest Neighbor Matching

(NNM). If any of these tests appeared significant (based on the bootstrapped standard errors), then

it means that the results are robust.

The results for PhilHealth reveal that those who availed of the program have a higher annual

income than those who did not avail – by PhP608. Furthermore, annual income in cash is PhP993

higher than those who did not avail. Wage is also higher for beneficiaries as they get to enjoy

PhP146 compared to non-beneficiaries. Lastly, individuals who are PhilHealth members have

higher annual expenditures: PhP4,155. The results are consistent with the a-priori expectations that

individuals who have access to social security insurance such as PhilHealthgives them more savings

which they can use for more important expenses such as education and food.

24

The next table shows the results the ALKANSSSYA program. All of the outcome variables

turned out to be significant. This implies that the impact of the program is effective in improving

the welfare of the beneficiaries, especially in terms of their income, wage, total sales from

entrepreneurial activities and total expenses.

Table 4.8PSM results: For AlkanSSSya beneficiaries and non-beneficiaries

Treated Control ATT Std. Err. t-value

Total income per capita

138 78 1,890.65 1145.58 1.65 *

Total income in cash per capita 138 78 1,472.31 1096.41 1.34 *

Wage in cash per capita 138 78 1,349.66 1094.97 1.23 *

Total sales from entrep per capita 138 18 18.38 18.471 0.99

Total expen cash per capita 138 78 317.23 237.86 1.33 *

*statistically significant at p<0.10

Those who availed of the AlkanSSSya program in Marikina enjoy higher total income of

(PhP1,890) and higher wage (PhP1,349) than non-members. Moreover, those individuals who are

engaged in a small business enjoy higher sales of PhP18. Though this is a small amount, if this is

summed up through a longer period of time, it would create a bigger difference. In addition to that,

members are able to have extra to spend more on other essential goods (PhP317) such as food and

other basic goods.

Given the benefits of being a member of PhilHealth and AlkanSSSya programs, there is

more than enough reason to believe that the money paid for the premium (PhP2,400/year for

PhilHealth, and PhP330/month for AlkanSSSya) will go a long way. It helps the individual augment

its expenses for health and other investment generating activities through the benefits that they get

from being a member. Being part of the informal sector makes them vulnerable to shocks such as

25

sudden changes in prices and one of the ways to minimize the negative economic impact of this is

there is access to social security such as in this case, the PhilHealth individual paying and sponsored

program and the AlkanSSSya program.

26

V. CONCLUSION AND POLICY RECOMMENDATIONS

This study has shown some initial evidence on the effectiveness of some social protection

programs such as the PhilHealth and ALKANSSSYA program for those who are involved in the

informal sector. Being part of the informal sector implies that the individual has no permanent

source of income, thus there is no financial security. The PhilHealth and ALKANSSSYA programs

aim to provide health and insurance security.

The results show that both programs are effective for poor individuals involved in the

informal sector in terms of gaining more income. The programs help augment the financial needs

by allowing them to use their income for expanding their business instead of using it for emergency

purposes such as hospitalization or other health needs.

Given the results of this exercise, it is recommended to increasethe low coverage in terms of

membership among the informal sector. This can be done by promoting enrollmentthat can be

initiated by the local chief executives andlocal government units in partnership with civil society and

non-government organizations. However, there isinadequate dataon the number of people in the

informal sector so theproblem lies on how toidentify individuals and households that are poor,

vulnerable and marginalized within the informal sector.It is expected that the informal sector will be

more visible and will be identified efficiently as potential beneficiaries of social protection

programsin the new database from DSWD’s National Household Targeting System for Poverty

Reduction or ―Listahanan‖. The Listahanan is an information management system that assesses and

identifies who the poor are and where they are located in order to maximize the social proteciton

programs.

The use of CBMS data can also help provide baseline information with its rider

questionnaire on social protection by expanding its coverage to all provinces and municipalities.

27

With CBMS data, the informal sector will no longer be invisible and thus better profiling of this

sector will be achieved.

Promoting enrolment and increasing the coverage would also mean increasing the budget for

health at the local government level. One sources of funds would be revenues from the sin tax, in

which 85% of the total revenue is earmarked to fund universal health care, which could also be used

to cover the poor informal sector who can not afford heatlh care.

Another possible policy implication is to improve the accessibility of a payment facility. The

local chief executives and local government units can facilitate in information campaigns on what

services are offerred by Philhealth and ALKANSSSYA. Another one is identifying partners that can

assist in the payment of contributions, for example, in partnership with a telecom networkthrough

the use of an e-load facility or mobile phones in remitting one’s contribution. An individual would

simply purchase a load and have a choice to remit part of it or all of it to his PhilHealth and SSS

contributions. Another possible way of making payment more accessible is through retail

pawnshops (Cebuana or Palawan Express etc.) that are very prevalent in provinces. Exploring more

avenues in partnership with the private sector can make payment facilities more accessible and less

costly on the part of the contributor, especially in geographically isolated areas.

Though it is difficult to reach individuals in the informal sector since most are

undocumented, it is best to involve the participation of the local chief executives and local

government units in identifying, monitoring and providing support for the informal

sector.Community support such as providing assistance in filling out registration forms or creating

opportunities for livelihood and job-creating enterprises that will sustain their incomes. A

sustainable employment will help encourage the poor to set aside a few pesos daily as they can now

afford to save and seek for better health care.

28

REFERENCES

Angelo King Institute. (2014). Monitoring the Philippine Economy Annual Report. BusinessWorld. Retrieved February 19, 2016, from

http://www.bworldonline.com/content.php?section=Economy&title=health-insurance-coverage-rates-56%-58%-for-informal-sector----pids&id=122149

Capuno, J. (2012). Household decisions and child health : Estimating the links between water

treatment and the incidence of diarrhea using non-recursive two-equation causal models. UPSE Discussion Paper No. 2012-02

International Labor Organization. (2014). www.ilo.org Lee, R., Tarroja, C., Pacificador, A., Tiongco, M., Lapena, M., and Alcantara, M. (2014). ―How the

Department of Health and Other Interventions Close the Gap in Health Outcome Disparities among Local Government Units.‖ Inception Report prepared for the Department of Health and the European Union.

National Statistical Coordination Board. 2012. Poverty charts retrieved October 15, 2015 from

http://www.nscb.gov.ph/poverty/dataCharts.asp National Statistics Office. (2014). Census on Population and Housing 2010. Retrieved from

http://census.gov.ph/content/statistical-tables-sample-variables-results-2010-census-population-and-housing-%E2%80%93-bataan on March 3, 2015.

PhilHealth. (2014). www.philhealth.gov.ph Philhealth. (2015a). Philhealth Stats & Charts. http://www.philhealth.gov.ph/about_us/statsncharts/snc2015_2nd.pdf . Downloaded on April 12, 2015. PhilHealth. (2015b). http://www.philhealth.gov.ph/members/informal/dependent.html Rosenbaum, P.R. & D.B. Rubin. (1983). The central role of the propensity score in observational

studies for causal Silfverberg, D.V. (2016). PhilHealth coverage in the informal sector: Identifying determinants of

enrollment. PIDS Policy Notes. No. 2016-02 (January 2016). Philippine Institute of Development Studies.

Social Security System.(2014) SSS Annual Report (Rep.) Retrieved February 19, 2016, from SSS

website: https://www.sss.gov.ph/sss/DownloadContent?fileName=SSS2014_Annual_Report.pdf

Social Security System. (2015). https://www.sss.gov.ph/sss/appmanager/pages.jsp?page=selfemployedcoverage

29

Tubadeza, K. P. (2016, January 26). Health insurance coverage rates 56%-58% for informal sector --

PIDS. Usui, N. (2011). Searching for effective poverty interventions: Conditional cash transfers in the

Philippines. Asia Development Bank.