Make the Most of Your Super

Presented by John Frogley, DFPManager – Employer Services, Catholic SuperFebruary – June 2010

Disclaimer

The information provided is about the Fund and is not intended as financial advice. It does not

take into account specific needs, so you should consider your personal position, objectives and

requirements before taking any action. The information is also subject to change.

Authorised by the Trustee of Catholic Super, CSF Pty Limited (ABN 50237986957) (AFSL

246664) (RSE L0000307) (RSE R1000597).

Agenda

• Catholic Super Overview & Returns

• Catholic Super Fund Merge

• Superannuation Rules

• Super Salary Sacrifice – How it works

• Transition to Retirement

• Government Super Co-Contribution

• Insurance Options Overview

History

• Established in 1971

• Over 70,000 members* (approx. 2,500 pension members)

• Over $3.7 Billion in assets*

• All profits to members

• Member Services 1300 655 002

Frank PeganChief Executive Officer

Peter BugdenChairman

* Approx. 02/2010

About Catholic Super

• Your choice of “Build Your Own” investment options

• Access to CSF Financial Planning Services

• Account based Pensions

• Member Online – access to account online facility

• Education Seminars

• Public Offer (Personal Plan)

• Information including newsletters and brochures

• Member Services 1300 655 002

• No Super Lump Sum Benefits Tax from age 60

• No Income Tax on Super Pensions from age 60

Summary – Super Rules …

• Employer contribution limit from $50,000 to $25,000 under age 50

effective 1st July 2009

- Employer contribution limit Age 50+ from $100,000 to $50,000 till

2011/12 then to $25,000 for all ages

• ‘Transition to Retirement’ Strategy

• After tax contribution limit of $150,000 per year**

• 1st July 2009, access to co-contribution via salary sacrifice changed

* Conditions apply ** $450,000 up front or limit can be averaged over 3 years.

Summary – Super Rules …

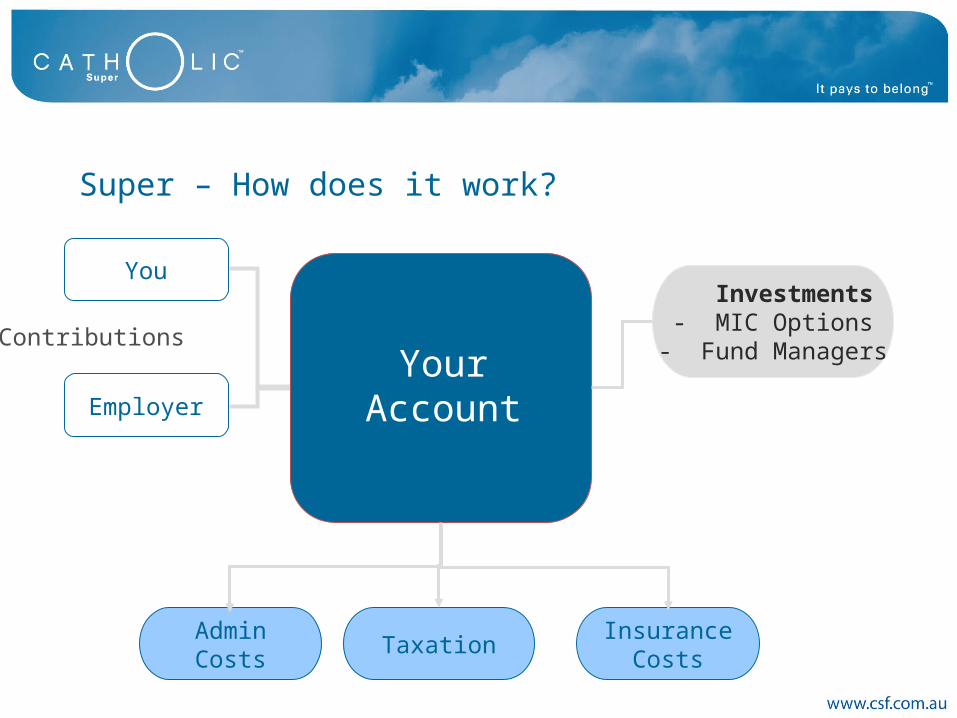

Taxation

Investments- MIC Options

- Fund Managers

You

Employer

AdminCosts

InsuranceCosts

Contributions

Super – How does it work?

YourAccount

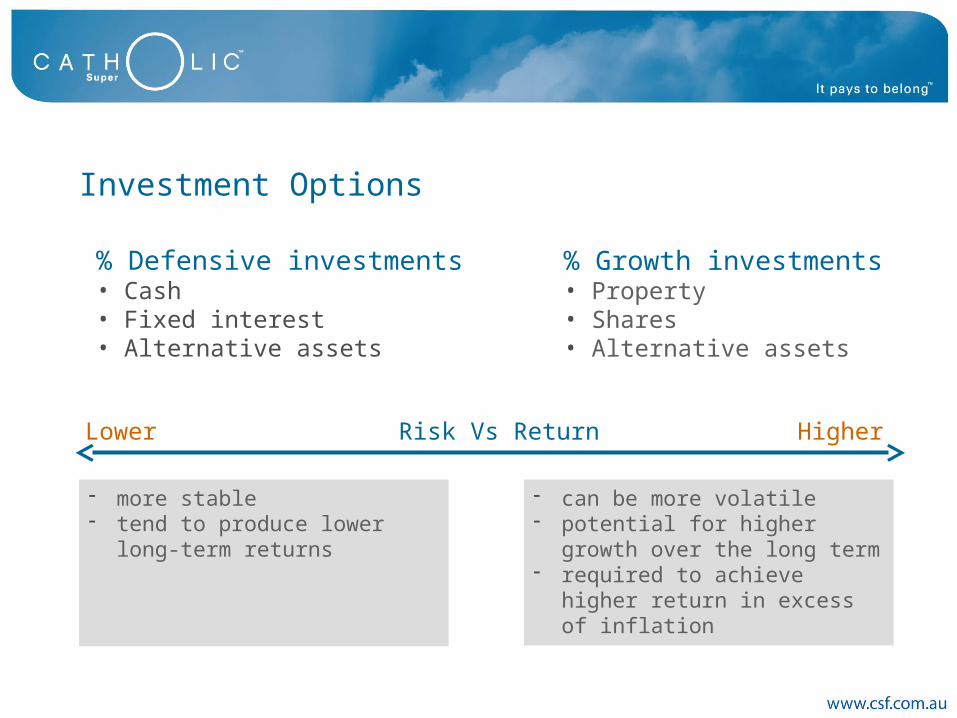

% Defensive investments• Cash• Fixed interest• Alternative assets

% Growth investments• Property• Shares• Alternative assets

can be more volatile potential for higher growth over

the long term required to achieve higher return

in excess of inflation

more stable tend to produce lower long-term

returns

Lower Risk Vs Return Higher

Investment Options

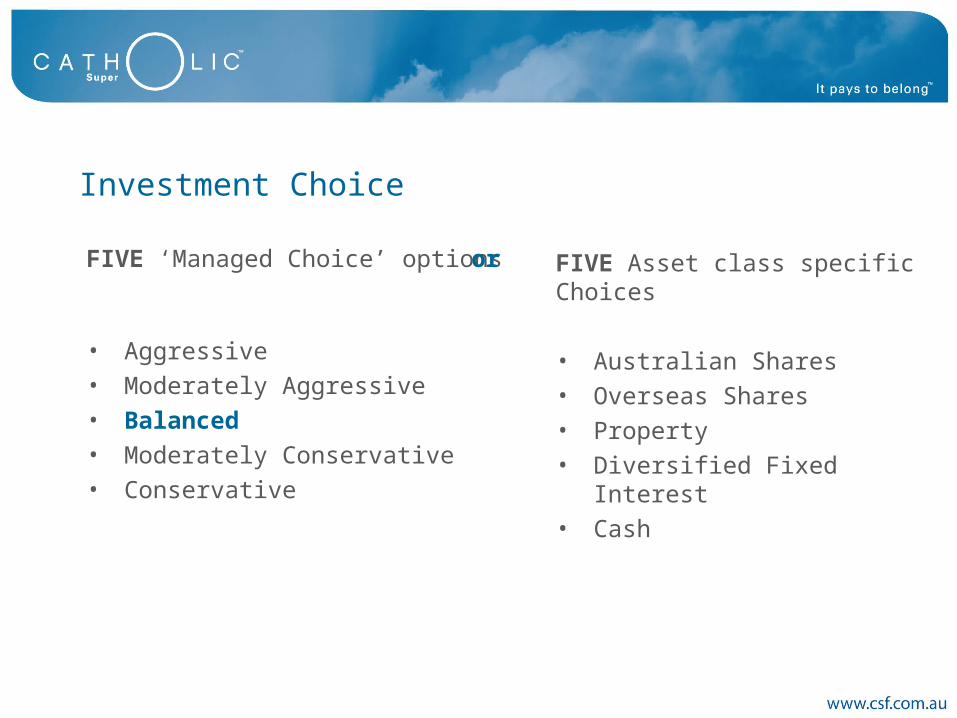

FIVE ‘Managed Choice’ options

• Aggressive

• Moderately Aggressive

• Balanced

• Moderately Conservative

• Conservative

FIVE Asset class specific Choices

• Australian Shares

• Overseas Shares

• Property

• Diversified Fixed Interest

• Cash

or

Investment Choice

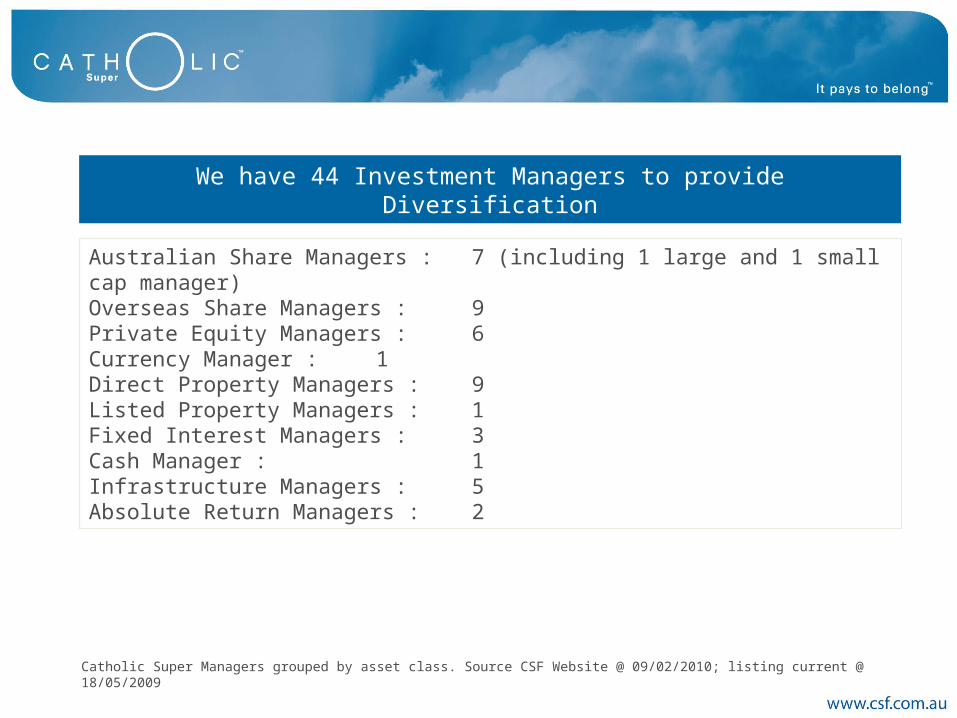

Australian Share Managers : 7 (including 1 large and 1 small cap manager)Overseas Share Managers : 9Private Equity Managers : 6Currency Manager : 1Direct Property Managers : 9Listed Property Managers : 1Fixed Interest Managers : 3Cash Manager : 1Infrastructure Managers : 5Absolute Return Managers : 2

We have 44 Investment Managers to provide Diversification

Catholic Super Managers grouped by asset class. Source CSF Website @ 09/02/2010; listing current @ 18/05/2009

Australian Shares: %BHP Billiton Limited 7.9National Australian Bank Ltd 5.3ANZ Banking Group 5.1Commonwealth Bank of Aust 4.5Westpac Banking Corporation 4.5

Rio Tinto Limited 3.2 Woolworths Limited 2.6CSL Limited 2.0Telstra Limited 1.6Coca Cola Amatil Limited 1.5Amcor Ltd 1.4QBE Insurance Group 1.3Insurance Australia Group 1.2Asciano Group 1.2Oil Search Limited 1.2Total weighting 44.5

What are the 15 Major Share Investments within the Fund, both in Australia and Overseas?

Source CSF Website @ 09/02/2010; listing current @ 30/09/2009 Guide Only

Overseas Shares: %Microsoft Corporation 1.1Nestle’ SA 1.0Samsung Electronics Limited 0.9Roche Holdings 0.7Johnson & Johnson 0.7Vodaphone Group 0.6Intel Corporation 0.6SBI Holdings 0.6Heineken 0.6Cisco Systems Inc. 0.6T & D Holdings 0.5Wellpoint Inc 0.5CVS Caremark Corporation 0.5Vivendi S.A 0.5Linde Ag 0.5Total weighting 9.9

Managed Choice *FYTD % 1 Year %3 Years (pa)

%5 Years (pa)

%

Aggressive 19.09 29.86 -0.67 6.85

Moderately Aggressive 16.19 24.00 -0.13 6.52

Balanced 12.51 16.97 0.10 6.34

Moderately Conservative 10.50 14.92 1.28 5.76

Conservative 7.05 8.98 2.92 5.72

Catholic Super Returns

Build Your Own *FYTD % 1 Year %3 Years (pa)

%5 Years (pa)

%

Australian Shares 27.59 47.44 1.52 10.08

Overseas Shares 13.91 23.67 -4.34 2.95

Property 9.33 7.27 2.18 6.65

Fixed Interest 3.77 5.50 3.62 4.07

Cash 2.25 3.00 4.76 4.92

*FYTD 31/03/2010 Catholic Super website

Managed Choice2008-2009

%2007-2008

%2006-2007

%2006-2005

%2004-2005

%2003-2004

%

Aggressive -12.1 -12.2 25.0 17.7 16.3 16.1

Moderately Aggressive -10.7 -9.4 22.6 15.9 15.0 13.8

Balanced -9.9 -6.4 21.0 15.3 14.3 11.8

Moderately Conservative -6.0 -3.9 16.4 11.3 11.0 10.2

Conservative -3.3 2.3 12.2 8.8 9.3 5.9

Catholic Super Returns - Financial Years

Build Your Own2008-2009

%2007-2008

%2006-2007

%2006-2005

%2004-2005

%2003-2004

%

Australian Shares -12.2 -13.0 30.7 22.6 26.3 22.0

Overseas Shares -10.0 -19.1 20.0 12.9 8.3 14.3

Property -12.1 7.0 16.2 12.4 13.4 10.8

Fixed Interest 6.2 0.3 4.4 3.0 7.7 3.3

Cash 4.9 5.9 5.4 4.7 5.2 5.9

As at 30 June 2009

Make extra contributions

• Either regular payments or lump sum

• Before tax (Salary Sacrifice) or after

• Member Investment Choice

• Consolidate super accounts

• Find your lost super

Maximise your returns

How do I increase my Super?

Income Tax Rates - 2009/10

Medicare Levy is also payable at the rate of 1.5 to 2.5 % of taxable income

Taxable Income Tax Payable Tax Rate on Excess

$ 6,000 NIL 15%

$ 35,000 $4,350 30%

$ 80,000 $17,850 38%

$ 180,000 $55,850 45%

Compare super to other investments

Outside Super Super (Salary Sacrifice)

Salary $ 10,000

Less tax $ 3,150 @ 31.5%

Net to invest @ 4% cash $ 6,850

After Tax $ 188 @ 31.5%

Value after Yr 1 $ 7,038

Compare super to other investments

Outside Super Super (Salary Sacrifice)

Salary $ 10,000 $ 10,000

Less tax $ 3,150 @ 31.5% $ 1,500 cont. tax @ 15%

Net to invest @ 4% cash $ 6,850 $ 8,500 @ 4% cash option

After Tax $ 188 @ 31.5% $ 289 earnings tax @15%

Value after Yr 1 $ 7,038 $ 8,789 24.8% +

Examples:

You could finish full-time work but continue part-time & use some of your super to supplement your income

or

Continue to work full-time & direct more salary into super while drawing a tax effective super account based Pension* to repay debt, improve lifestyle or enhance savings

Transition to Retirement Pension

*Also previously known as an Allocated Pension

• You must be minimum of 55* years of age

• You can continue to work either full time or part time

• A 10% maximum super income limit per year

• A 4%* minimum super income limit per year up to age 65

• Tax free income if over age 60

• New employer contribution limit of **$50,000 till 2011/12 then $25,000

• Tax concessions between age 55 – 59 e.g. 15% tax offset

• *Temporary halving of minimum drawdown percentage extended to 2009/10

Account Based Pension Rules

* Phase in to age 60.**2009/10

Minimum income as a %

of account balance

Minimum income as a %of account balance

(2009-2010 only)

Maximum income as a %

of account balanceAge

Under 65 4% 2.0% 100%

65 – 74 5% 2.5% 100%

75 – 79 6% 3.0% 100%

80 – 84 7% 3.5% 100%

85 – 89 9% 4.5% 100%

90 – 94 11% 5.5% 100%

95 + 14% 7.0% 100%

Pensions – Yearly Income Payments

9% Employer & Salary Sacrifice

Your Super Account

$$$$$$

$$$$$$

Pension Income

Account Based Pension

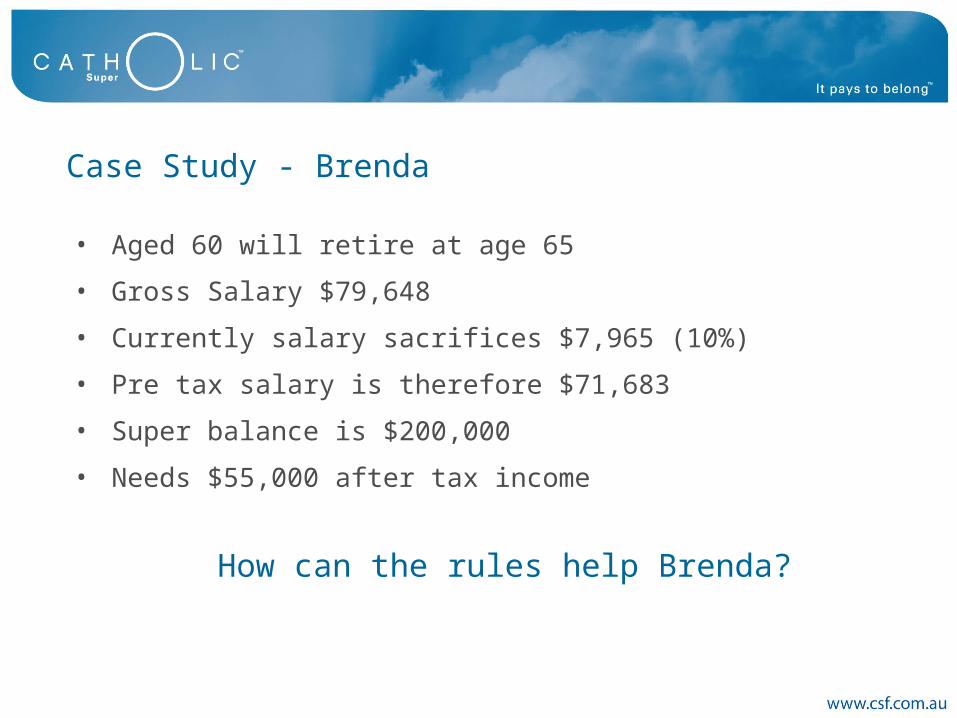

Overview – Transition to Retirement; How it Works

• Aged 60 will retire at age 65

• Gross Salary $79,648

• Currently salary sacrifices $7,965 (10%)

• Pre tax salary is therefore $71,683

• Super balance is $200,000

• Needs $55,000 after tax income

Case Study - Brenda

How can the rules help Brenda?

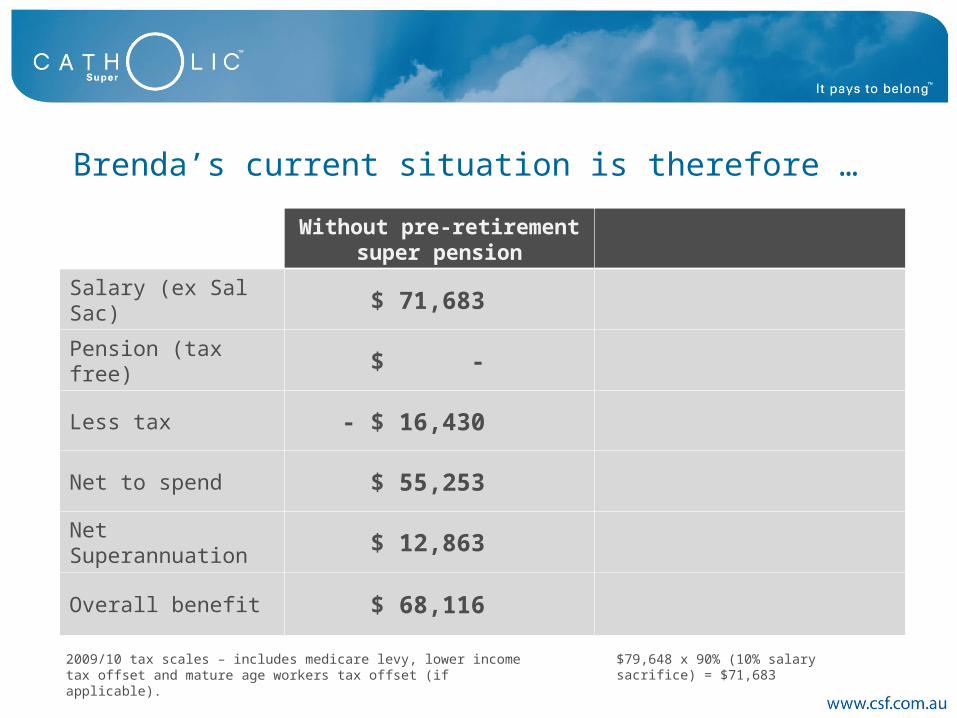

Without pre-retirement super pension

Salary (ex Sal Sac) $ 71,683

Pension (tax free) $ -

Less tax - $ 16,430

Net to spend $ 55,253

Net Superannuation $ 12,863

Overall benefit $ 68,116

Brenda’s current situation is therefore …

2009/10 tax scales – includes medicare levy, lower income tax offset and mature age workers tax offset (if applicable).

$79,648 x 90% (10% salary sacrifice) = $71,683

Post 01/07/2009 Transitional Concessional Cap of $50,000

Brenda must leave a minimum $2,000 in her superannuation account; therefore transfers $198,000 to TTR strategy

Under the super rules Brenda:

• Draws a $19,800 tax free pre–retirement super pension

• Salary sacrifices $38,946 to increase her super

• Reduces her pre tax salary to $36,816

• Pays only 15% tax on her super contributions compared

to 31.5%

• Is not entitled to the $1,000 Government Co - contribution

Without pre-retirement super pension

With pre-retirement super pension

Salary (ex Sal Sac) $ 71,683 $ 40,702

Pension (tax free) $ - $ 19,800

Less tax - $ 16,430 - $ 5,249

Net to spend $ 55,253 $ 55,253

Net Superannuation $ 12,863 $ 19,397

Overall benefit $ 68,116 $ 74,650

What does this mean for Brenda?

$6,534 extra

2009/10 tax scales – includes medicare levy, lower income tax offset and mature age workers tax offset (if applicable).

$50,000 Transitional Concessional Cap effective 01/07/09 (Brenda uses $46,114 of this cap)

SGC (9%) on $79,648 is $7,168 less 15% tax = $6,093

• Encourage super savings for lower income earners

• Additional contribution up to a maximum of $1,000 per year

• Must make after-tax contribution

• Reduces by 3.33 cents for every dollar over $31,920

• Gross income*

• Phases out completely at $61,920

• Part time or casual workers (e.g.. teenage children)

* Plus reportable fringe benefits and salary sacrifice * 10% + income from eligible employment.* Restored in full 2014/15

Government Super Co-Contribution Scheme

*Temporary Reduction to Scheme

Assessable Income Co-contribution

$ 31,920 or less $ 1,000

$ 35,000 $ 897

$ 45,000 $ 564

$ 55,000 $ 231

$ 61,920 or more $ 0

Government Co-contribution Scheme

Temporary Reduction to Scheme

* Member must be an eligible employee & make a personal after tax contribution. Assumes member contribution of $1,000. Changes apply for 2009/10 to 2011/12 then increasing back to $1500 by 2014/15

** Plus reportable fringe benefits. Beware salary sacrifice rule change - assessable income 1st July 2009.

• Managing Risk

• Protect your Assets

• Protect Yourself and your Family

• Life Insurance

• Income Protection Insurance

Insurance

• Death Only

• Death and Total and Permanent Disablement (TPD)

• Income Protection

3 Types of Insurance Cover

• Basic Cover – an automatic level of cover for all

employer-sponsored members

• Build Your Own Cover – allows you to increase your

cover to suit your own needs

2 Ways to Structure your Insurance Cover

* All employer sponsored members

Insurance *

• Automatic Basic Cover is 2 Units of Death Only Insurance

and 2 Units of Total & Permanent Disablement

• Automatic default is 5 Units of cover for Income

Protection - 60 day wait period & 5 year benefit period

• Can purchase additional Cover under Build Your Own

Cover options subject to limits and evidence of health

• Cover is 24 hours 7 days a week for members

Death & TPD Cover

• Basic cover of 2 units provided upon joining the Fund up to age 65

• Death cover only is provided to age 70; if required

Age Next Birthday

<35 36 - 40 41- 45 46 - 50 51 - 57 58 – 60 61 - 6364 - 65

66 - 70

Cover Amount (2 units)

$201,000 $172,200 $129,200 $86,200 $57,400 $43,000 $28,800 $14,400 $11,200

Aged Based Example:

Income Protection Insurance *

• Benefit payable is 85% (includes 10% Superannuation) of

your stated monthly income

• Optional waiting periods – 60 days or 30 days

• Optional benefit payment periods – to age 65 or 5 years

• Each Unit provides a gross monthly benefit of $585*

* Limits apply Indexed to Average Weekly Ordinary Times Earnings

Super - Accumulation Stage Taxation

15% MaxTax Rateon Earnings

AccumulationFund Balance $$$

Before Retirement

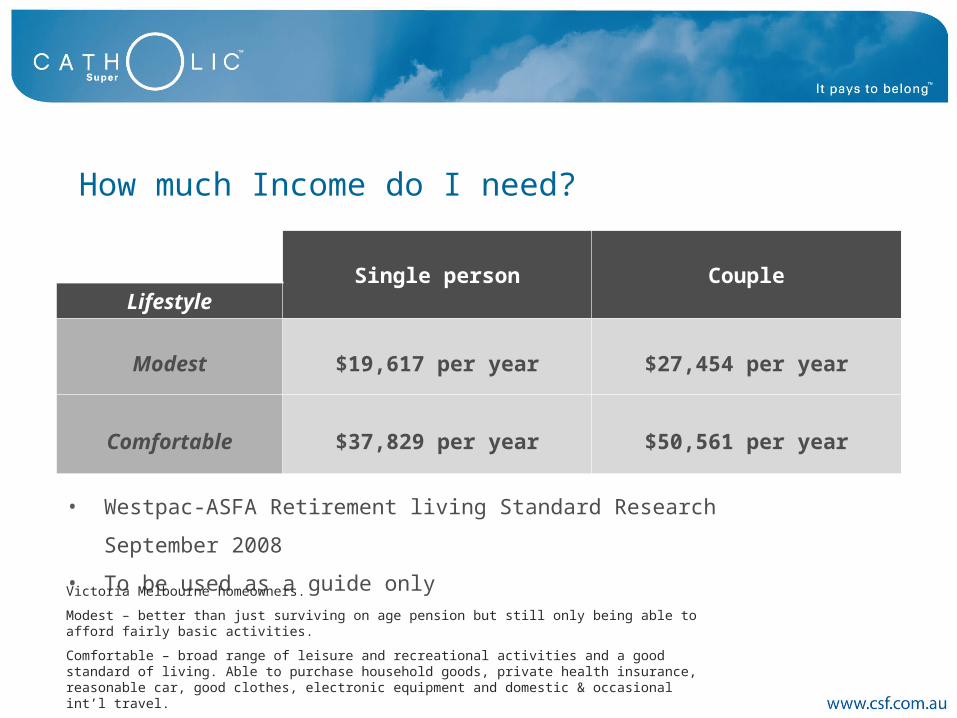

• Westpac-ASFA Retirement living Standard Research September 2008

• To be used as a guide only

How much Income do I need?

Single person CoupleLifestyle

Modest $19,617 per year $27,454 per year

Comfortable $37,829 per year $50,561 per year

Victoria Melbourne homeowners.

Modest – better than just surviving on age pension but still only being able to afford fairly basic activities.

Comfortable – broad range of leisure and recreational activities and a good standard of living. Able to purchase household goods, private health insurance, reasonable car, good clothes, electronic equipment and domestic & occasional int’l travel.

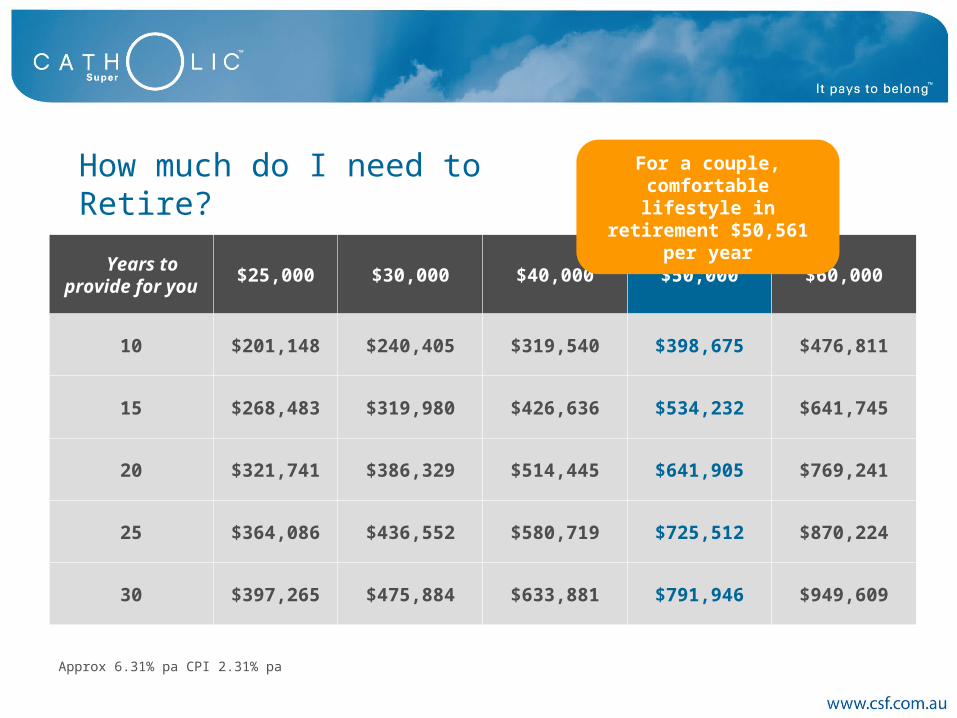

How much do I need to Retire?

Years to provide for you

$25,000 $30,000 $40,000 $50,000 $60,000

10 $201,148 $240,405 $319,540 $398,675 $476,811

15 $268,483 $319,980 $426,636 $534,232 $641,745

20 $321,741 $386,329 $514,445 $641,905 $769,241

25 $364,086 $436,552 $580,719 $725,512 $870,224

30 $397,265 $475,884 $633,881 $791,946 $949,609

For a couple, comfortable lifestyle in retirement

$50,561 per year

Approx 6.31% pa CPI 2.31% pa

• Wholly owned by Catholic Super

• Salaried employees - no commissions

• No fee to discuss your situation

• Your personal Financial Plan in writing - Fee $1,210*

• Contact us on 1300 655 002

CSF Financial Services

*$958 Net fee - after fund tax credit if deducted from your Super account

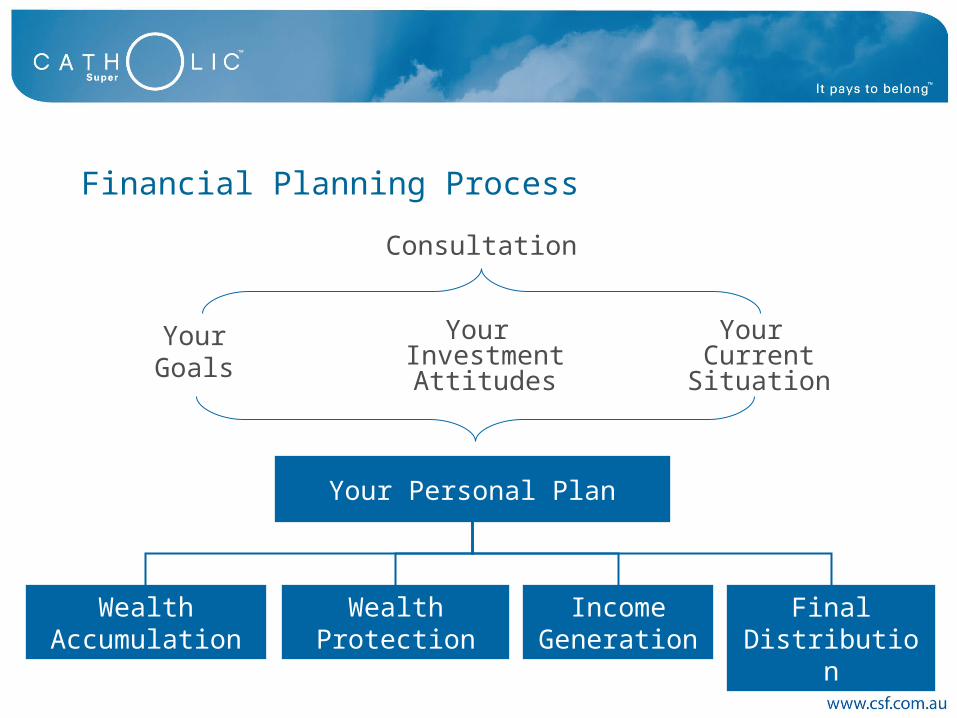

Financial Planning Process

Your Personal Plan

IncomeGeneration

YourGoals

Your InvestmentAttitudes

Your CurrentSituation

Consultation

Wealth Accumulation

Wealth Protection

Final Distribution

MemberAccess

• Manage your account in our secure online facility,

MemberAccess: Change your details such as email, address, phone number. View your balance, transactions, investment options Switch your investment options. (No fee for switching) Receive your statements electronically Link your accounts for a single login (if you have a super and pension

account).

• Register for access online: You’ll need your member number, name, postcode and birthday to

register (The same as we have them recorded)

• Call 1300 655 002 if you have any questions

Online Statements

• Helps us reduce our use of natural resources

• Enables you to store your statements electronically and keep

track of past statements

• Available through MemberAccess, our secure online facility

• An Industry Fund - all profits returned to members

• SuperRatings Platinum Rating

• SuperRatings Fund of the Year Finalist in 2009 & 2010

• Low fees

• Investment Performance

• Seminars and school visits

• Access to CSF Financial Services

Why Catholic Super?