Macro Models Unit

20 August 20041

Models, Forecasting and the Transmission

Mechanism of Monetary Policy

Presentation to the Portfolio and Select Committee on Finance

Cape Town20 August 2004

Macro Models Unit

20 August 20042

Contents

• Why do central banks need forecasts• General remarks about models and

forecasting• Models used by the SARB• Communicating the forecast• The monetary policy transmission

mechanism• Concluding remarks

Macro Models Unit

20 August 20043

Why Are Policy Makers Concerned With the Future?

• Monetary policy works with a considerable time lag

• Long time lags from changes in interest rates to output and from output to inflation

• It differs across countries and over time

• Policy makers wish to know what will happen if they change the central bank’s interest rate

• Our knowledge about the MPTM is limited

Macro Models Unit

20 August 20044

Monetary policy and forecasts

• Regardless of the monetary policy framework, a policymaker must have a view of the future because of the existence of transmission lags

“Implicit in any monetary policy action or inaction is an expectation of how the future will unfold, that is, a forecast. There is no way to avoid making a forecast, explicitly or implicitly.” Alan Greenspan, 1994

Macro Models Unit

20 August 20045

General remarks on models

Macro Models Unit

20 August 20046

Central Banks & models

• When sufficient data are available, central banks should make use of econometric techniques and of models:– To understand and quantify how the

economy and monetary policy works (i.e. the transmission mechanism)

– Monitor where the economy stands and make short-term projections

– Make longer-term projections to determine impact of monetary policy

CCBS Handbook in Central Banking, #3

Macro Models Unit

20 August 20047

Benefits of Models

• Provide a simple framework with which to analyse and quantify short to medium-term macroeconomic developments

• Assists in the construction of forecasts in a systematic and consistent manner

• Useful for alternative policy simulations

Macro Models Unit

20 August 20048

Requirements for Models (1)

• To capture structural changes in the economy

• Not necessarily to supply precise forecasts, but at least a good indication of directional effects of policy options

• To correspond to linkages in the economy and to track the dynamics in the model easily

Macro Models Unit

20 August 20049

Requirements for Models (2)

• To follow a pluralistic approach: not one model for all occasions, but a suite of models

• To follow a pragmatic approach: supplement model output with surveys, value judgements, etc.

• To organise thoughts about policy and the economy, but their limitations must always be kept in mind.

Macro Models Unit

20 August 200410

Difficulties in modelling individual behaviour

• A market economy is steered by decisions of millions of consumers and workers, and hundreds of thousands of managers, investors and entrepreneurs

• A gigantic task to take account of the different circumstances in which each finds him/herself and the different choices and incentives they face

Macro Models Unit

20 August 200411

Modelling with and without theory

• Econometricians learn from observing past behaviour of the economy as a whole, rather than individual behaviour

• Econometrics is based on probability theory – used to test the validity of economic theory

and– also to look for relationships with no

underlying rationale in economic behaviour

Macro Models Unit

20 August 200412

Steps in model building

• Literature study• Gather data and estimate

individual equations• Model validation

– Tests for system dynamics & stability– Test forecasting ability and accuracy:

A lengthy process

Macro Models Unit

20 August 200413

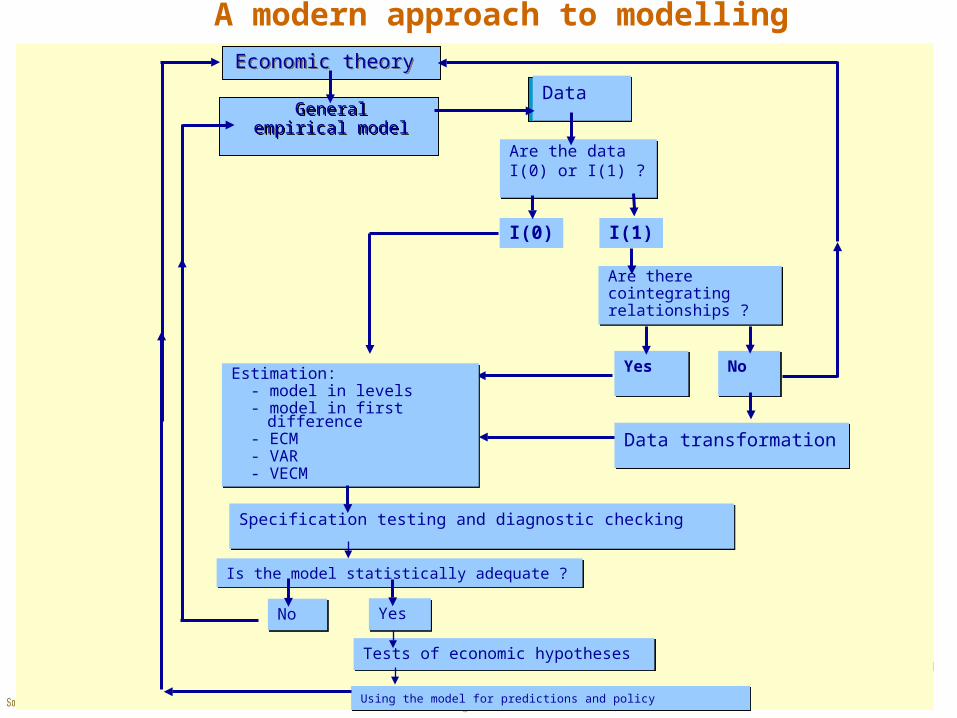

A modern approach to modellingEconomic theoryEconomic theory

Generalempirical model

Generalempirical model

DataData

Are the dataI(0) or I(1) ?Are the dataI(0) or I(1) ?

Are there cointegrating relationships ?

Are there cointegrating relationships ?

I(0) I(1)

YesYes NoNo

Data transformationData transformation

Estimation: - model in levels - model in first difference - ECM - VAR - VECM

Estimation: - model in levels - model in first difference - ECM - VAR - VECM

Specification testing and diagnostic checkingSpecification testing and diagnostic checking

Is the model statistically adequate ?Is the model statistically adequate ?

NoNo YesYes

Tests of economic hypothesesTests of economic hypotheses

Using the model for predictions and policyUsing the model for predictions and policy

Macro Models Unit

20 August 200414

Hold-out Periodor

Out-of-sampleex-post forecast

Hold-out Periodor

Out-of-sampleex-post forecast

Ex-ante forecastEx-ante forecastEstimation period

orIn-sample forecast

Estimation periodor

In-sample forecast

t1980t1980 t2000t2000 t2004t2004

Root mean square errors (RMSE’s)Root mean square errors (RMSE’s)

tt

YY

Model evaluation

Macro Models Unit

20 August 200415

Models used by the SARB

Macro Models Unit

20 August 200416

Structural and Atheoretical models developed and used by the SARB

• Core model• Small-scale model• Phillips-curve model • Vector auto-regressive (VAR) model• Auto-regressive integrated moving-average (ARIMA)

model• Indicator models• Disaggregated inflation model

Assist in thinking about a wide range of issues in a structured and quantified way and fosters debate around modelling, forecasting and monetary policy issues

Macro Models Unit

20 August 200417

Core model

• Keep relatively small: 63 equations of which 25 are structural equations

• Focus on inflation and other key economic variables impacting on inflation

• Economic theory determines long-run relationship between variables

• No long-run trade-off between inflation and output

• Short-run dynamics to explain short-term fluctuations in variables

Macro Models Unit

20 August 200418

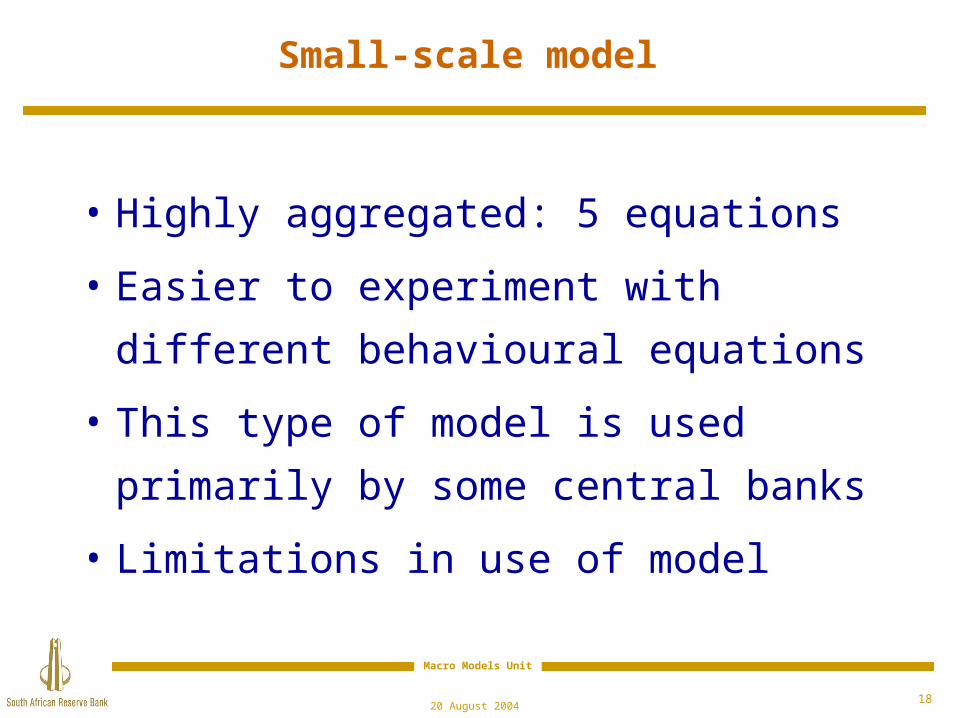

Small-scale model

• Highly aggregated: 5 equations

• Easier to experiment with different

behavioural equations

• This type of model is used

primarily by some central banks

• Limitations in use of model

Macro Models Unit

20 August 200419

Phillips-curve model

• Single equation model

• Useful to describe the determinants of inflation

and for inflation forecasting

• Original concept relates to wage inflation and

unemployment, but modern versions relate to

price inflation and output gap

• Cross-check forecasts derived from core model

Macro Models Unit

20 August 200420

Vector auto-regressive (VAR) model

• Dynamic interaction between a set of variables

• Do not require strong theoretical assumptions -

model is rather based on actual trends in data

• Useful over short time horizons

• Primarily used for short-term forecasting (up to 4

periods)

• Impulse responses describe reaction of variables on

exogenous shocks

Macro Models Unit

20 August 200421

Auto-regressive integrated moving-average (ARIMA) model

• Single equation model

• Models a single variable in terms of an auto-regressive component and a moving-average component

• Easy to estimate and solve the model

• No strong theoretical assumptions

• Useful over shorter time horizons

• Disadvantage : ARIMA models cannot predict turning points easily as they are based on historical figures (or trends of the past)

Macro Models Unit

20 August 200422

Indicator models

• Utilised to identify early indications of

sources of inflationary pressure

• Not used to forecast inflation

• Effectiveness decreases as forecast

period is prolonged

• Currently 19 univariate models - monitor

the monetary sector, foreign sector,

labour market and domestic demand

Macro Models Unit

20 August 200423

Disaggregated inflation model

• Model the components of CPIX

independently

• Uses monthly data

• Possible to identify sources of inflation

• Components are modelled mainly as a

function of unit labour costs, import

prices and the output gap

Macro Models Unit

20 August 200424

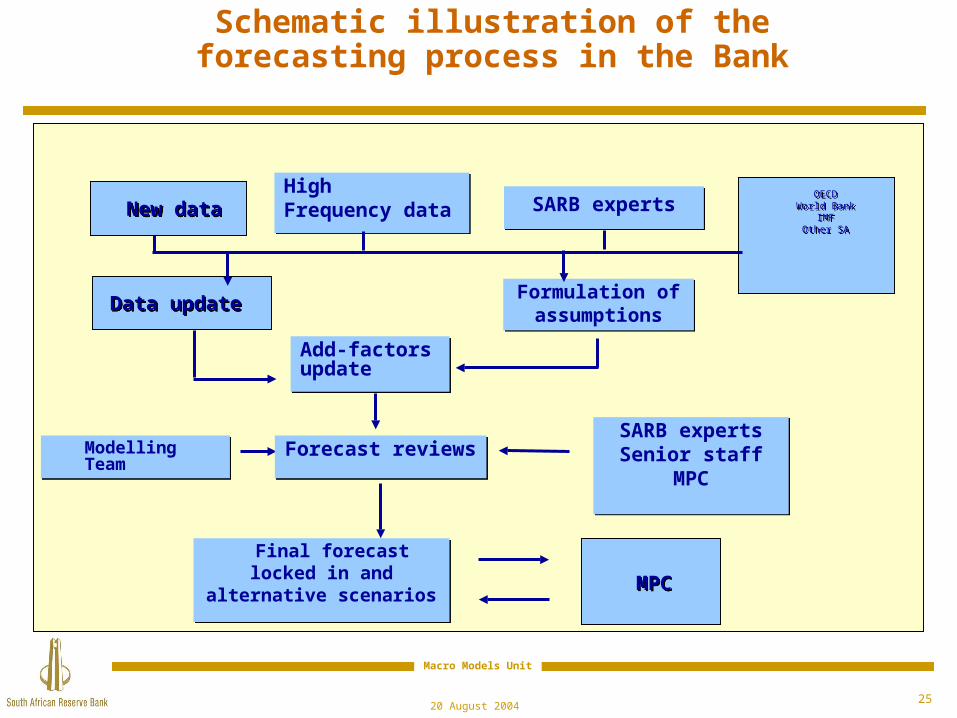

Forecasting process in the Bank

• Intensive process spanning 6 weeks, 6 times a year : from information collection and analysis to final discussion at the MPC meeting

• Collection and analysis of all relevant information on international and domestic economy

• Initial assumptions by technical staff

• Comments and suggestions by senior staff

• Final assumptions and specification of alternative scenarios by members of the MPC

• Preparation of forecasts with all the models and cross checking

• Preparation of final MPC document

• Discuss forecasts, risks and uncertainties at MPC meeting

• Publish the inflation forecast in the MPR twice a year

Macro Models Unit

20 August 200425

New dataNew dataHighFrequency dataHighFrequency data SARB expertsSARB experts

OECDWorld Bank

IMFOther SA

OECDWorld Bank

IMFOther SA

Data updateData update

Modelling TeamModelling Team

Final forecastlocked in and

alternative scenarios

Final forecastlocked in and

alternative scenarios

Formulation ofassumptions

Formulation ofassumptions

Add-factors updateAdd-factors update

Forecast reviewsForecast reviewsSARB expertsSenior staff

MPC

SARB expertsSenior staff

MPC

MPCMPC

Schematic illustration of the forecasting process in the Bank

Macro Models Unit

20 August 200426

Role of forecasts

“ In an ever-changing economy, no single model can possibly assimilate in a comprehensive way all the factors that matter for policy. Forming judgements about those factors, and their implications for policy, is the job of the Committee, not something that can be abdicated to models or even modellers. But economic models are

indispensable tools in that process.” - Bank of England

Macro Models Unit

20 August 200427

SARB models and forecasts only one consideration in policy formulation

Core model

Forecast

Policy

Assumptionsand judgements

Other models

Other issues andpolicy judgements

Macro Models Unit

20 August 200428

Communicating the forecast

Macro Models Unit

20 August 200429

Fan chart

• Many central banks use a fan chart in presenting the forecast for inflation

• A point forecast does not have much chance of matching actual outcome

• Used to convey a more accurate representation of the assessment of medium-term inflationary pressures

• Helps to focus the discussion on uncertainty & risks around the forecast

• Fan indicates probabilities, NOT upper & lower bounds for inflation

Macro Models Unit

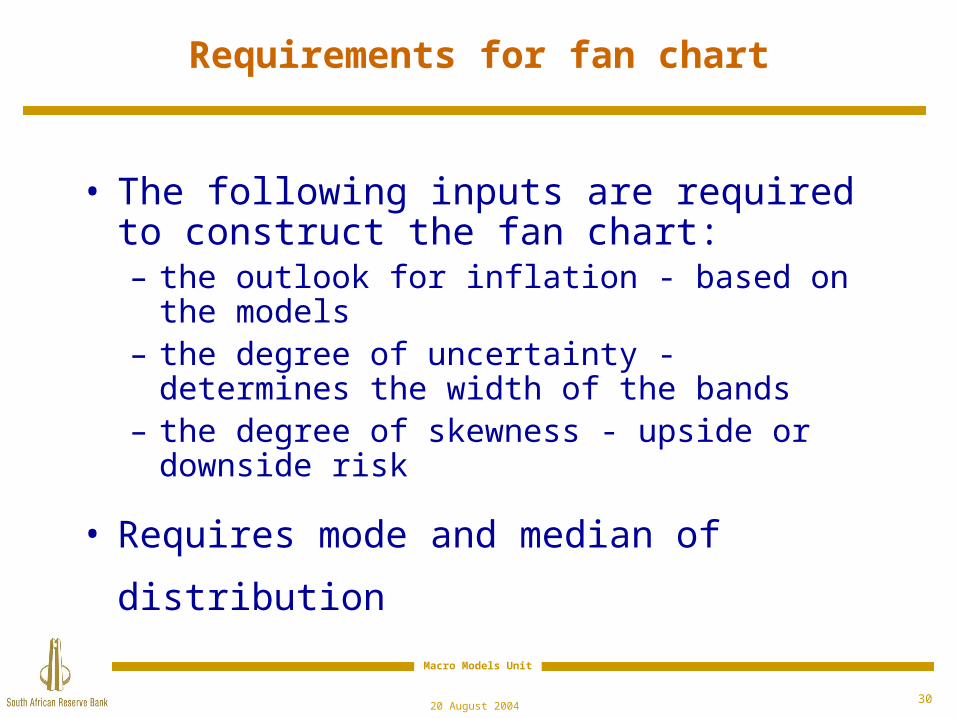

20 August 200430

Requirements for fan chart

• The following inputs are required to construct the fan chart:– the outlook for inflation - based on the

models– the degree of uncertainty - determines the

width of the bands– the degree of skewness - upside or

downside risk

• Requires mode and median of

distribution

Macro Models Unit

20 August 200431

Forecast

+50% Band

-50% Band

Distribution around the forecast

Macro Models Unit

20 August 200432

Fan chart

Macro Models Unit

20 August 200433

The monetary policy transmission

mechanism

Macro Models Unit

20 August 200434

“The tail wags the dog. By gently touching a tiny tail, Alan Greenspan wags the mammoth dog, the great American economy. Isn’t that remarkable? The federal funds rate is the shortest of all interest rates, remote from the rates on assets and debts by which businesses and households finance real investment and consumption expenditures counted in GDP. Why does monetary policy work? How? It’s a mystery, fully understood by neither central bankers nor economists.” James Tobin

The mystery of the MPTM

Macro Models Unit

20 August 200435

The transmission mechanism

• Describes how monetary policy affects output and inflation

• When the official interest rate is changed: • By how much is inflation affected, and when? • Is output affected in the short-run?• Through which channels does this happen?

• “To be successful in conducting monetary policy, the monetary authorities must have an accurate assessment of the timing and effect of their policies on the economy, thus requiring an understanding of the mechanisms through which monetary policy effects the economy” (Mishkin, 1995).

Macro Models Unit

20 August 200436

Difficult to estimate

• The lags with which monetary policy acts are long and variable (Friedman)

• Our knowledge of the transmission mechanism is imperfect.

• Estimating the transmission mechanism is difficult. (Mahadeva and Sinclair, 2001)– Lack of reliable data– Unforeseeable changes in the structure of

the economy– Separating cause from effect in the data

Macro Models Unit

20 August 200437

E

DEPTH AND BREADTH OF FINANCIAL MARKETS LOW HIGH

Impo

rtan

ce o

f in

tere

st r

ate

in tr

ansm

issi

on

mec

hani

smHIGH

Macro Models Unit

20 August 200438

Officialrate

Market rates

Asset prices

Exchange rate

Domestic demand

Net externaldemand

Totaldemand

Domesticinflationarypressure

Importedinflation

InflationExpectations/confidence

The transmission mechanism

Bank of England

Core model consistent with this view of the transmission mechanism

Macro Models Unit

20 August 200439

SARB diagram

• The SARB view is similar to other central banks’ view of the MPTM

• The starting point is again the official interest rate changes and then illustrate in more detail the key influences and channels running to the rest of the economy and ultimately to the rate of inflation.

• Can create wrongly the impression that one can isolate the impact through these channels

• Both diagrams essentially say the same thing• Main impact between 12 to 24 months, in line with

international experience

Macro Models Unit

20 August 200440

rates

Inflation rate

of goods and

&

of goods and

Net exports

Relativeprices

Nominalexchange

Import prices

Wages

Inflation

Other asset prices

Expenditure&

Investment

Net wealth

of goods and

Money

&

Demand & supplyof goods and

services

Repurchase rate

Other interest

rates

Inflation rate

Demand & supplyof goods and

services

Expenditure&

Investment

Demand & supplyof goods and

services

Net exports

Relativeprices

Nominalexchangerate

Import prices

Wages

Inflationexpectations

Other asset prices

(equity, land, property)

Expenditure&

Investment

Net wealth

Demand & supply of goods and

services

Money and credit

Expenditure&

Investment

Demand & supplyof goods and

services

Monetary Policy Transmission Mechanism

Current

Account

Capitalmovements

Change in

reserves

Wages

Inflation

expectations

Macro Models Unit

20 August 200441

SARB practice

• Baseline forecast with fixed repo rate• Alternative scenarios

– with “market expectations” repo rate– with Taylor-type policy reaction function– with alternative specifications by MPC– with alternative assumptions on ‘risk’

variables

Macro Models Unit

20 August 200442

Concluding remarks

Macro Models Unit

20 August 200443

Finally

• SARB follows inflation targeting framework with a Monetary Policy Committee setting official interest rates

• Model estimation procedures in line with modern approach to modelling

• Model development process in line with international practice• Core model reflects the monetary policy transmission

mechanism• Coefficients and impulse response functions are broadly in line

with research findings of SARB and others• Forecasting process covers the various conventions of setting

policy rates in models and the use of alternative scenarios• Forecast is a combination of staff and MPC inputs• Inflation forecast is published, using the fan chart to indicate

uncertainty inherent in forecasting

Macro Models Unit

20 August 200444

Thank you