Download - Lic Profile

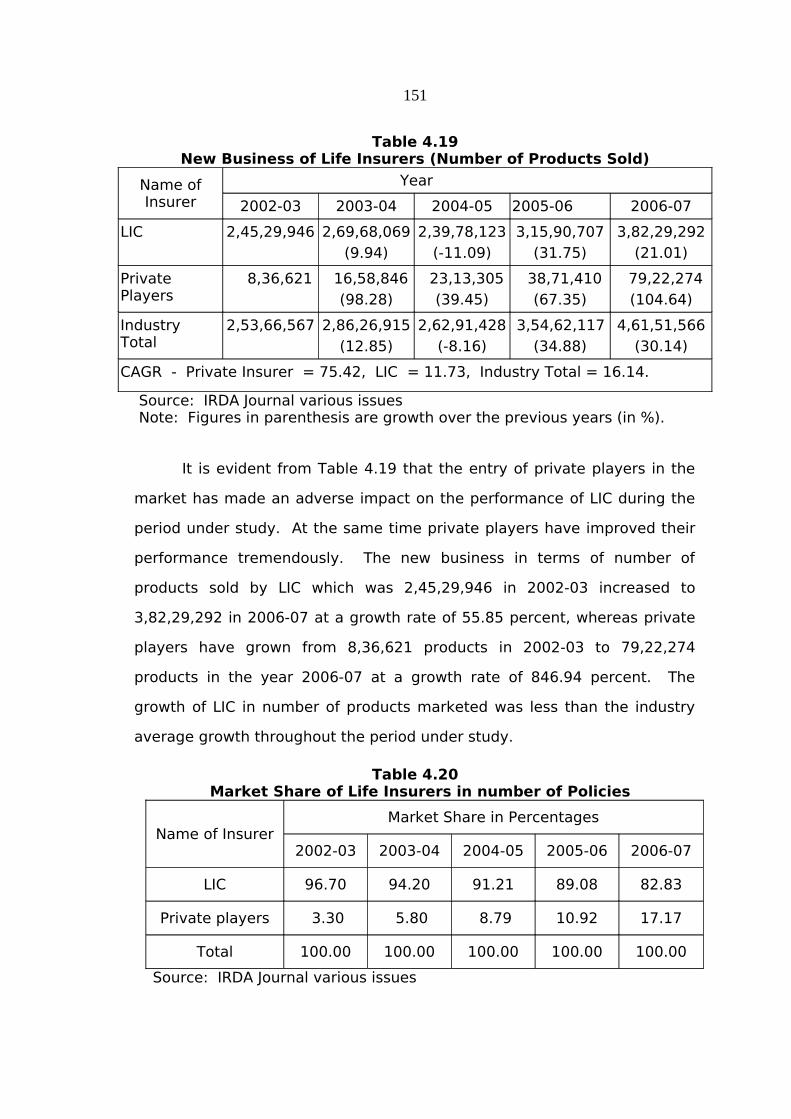

PROFILE OF LIFE INSURANCE CORPORATION OF

INDIA

INTRODUCTION

The present chapter portrays the marketing activities of LIC of India

and discusses briefly the business performance of the Corporation during

the period before and after liberalization of the insurance sector. An

attempt is made to compare the business performance of LIC with that of

the private players and the impact of privatization on LIC.

Life insurance business in India was being transacted by private

companies until 1956. As a result of the long felt need and in the interest

of insuring public, the life insurance business was nationalized in 1956. The

nationalization resulted in the establishment of Life Insurance Corporation

of India (LIC) by an act of the Parliament. The Corporation was formed and

began to function on September1, 1956 by taking over 170 companies and

75 provident societies. The entire initial capital of Rs.5crore was contributed

by the government of India. The objective of nationalization was described

by the then finance minister, Dr. Deshmukh as “to see that the gospel of

insurance is spread as far and wide as possible so that we reach beyond the

more advanced urban areas well into the hither to neglected rural areas” 1.

Headquartered in Mumbai, which is considered the financial capital of

India, Life Insurance Corporation of India currently has 8 Zonal Offices,

101Divisional Offices, 2048 Branch Offices located in different cities and

towns in India. The Corporation has a network of above one million agents

for soliciting life insurance business from the public 2. It is the largest life

insurance agency in the world. The LIC also transacts business abroad and

has offices in Fiji, Mauritius and United Kingdom. The Corporation is

associated with joint ventures abroad in the field of insurance, namely, Ken-

India Assurance Company Limited, Nairobi, United Oriental Assurance

Company Limited, Kuala Lumpur and Life Insurance Corporation

(International) E.C. Bahrain.

As a result of the insurance sector reforms process initiated in India,

the monopoly of the Corporation came to an end in 2000. The long 44

years of monopoly shows many ups and downs in the business of LIC. The

Corporation has been rated as No.1 Company in net worth and net profits

and No. 2 in total income in India.

Objectives of the Life Insurance Corporation of India

The Life Insurance Corporation of India (LIC) was set-up by the

Government of India to achieve the following objectives: 3

Spread Life Insurance widely and in particular to the rural areas and to

the socially and economically backward classes with a view to reaching

all insurable persons in the country and providing them adequate

financial cover against death at a reasonable cost.

Maximize mobilization of people’s savings by making insurance linked

savings adequately attractive.

Deploy the funds to the best advantage of the investors as well as the

community as a whole, keeping in view national priorities and

obligations of attractive return.

Conduct business with utmost economy and with the full realization that

the moneys belong to the policy holders.

Act as trustees of the insured public in their individual and collective

capacities.

Meet the various life insurance needs of the community that would arise

in the changing social and economic environment.

101

Involve all people working in the corporation to the best of their

capabilities in furthering the interests of the insured public by providing

efficient service with courtesy.

Promote amongst all agents and employees of the Corporation a sense

of participation, pride and job satisfaction through discharge of their

duties with dedication towards achievement of corporate objectives.

Organizational Structure of LIC of India

The Life Insurance Corporation Act, 1956 gives broadly the pattern of

its organization which is given in Figure 4.1.

CHAIRMAN

MANAGING DIRECTORS

Central Office (Mumbai)

Zonal Offices -8

Hyderabad Delhi Bhopal PatnaMumbai Kolkatta Chennai

Kanpur

102

LIFE INSURANCE CORPORATION OF INDIA

BOARD OF DIRECTORS

Divisional Offices - 101

Branch Offices - 2048

Figure 4.1. Organizational set up of Life Insurance Corporation of

India

The Corporation consists of members not exceeding 15 in number

appointed by the Central Government. The Chairman is the chief executive

of the Corporation. Various committees of the Corporation are constituted

under the Life Insurance Corporation Act and the regulations framed there

under. General superintendence and direction of the affairs of business of

LIC is entrusted to the Executive Committee which would be formed from

among its own members not exceeding five. The Chairman of the

Corporation is the Chairman of all these committees. The organizational

structure envisaged by the Act consists of a four-tier structure. The central

office at the top is primarily concerned with the formulation of policies.

Below the central office there are zonal offices to assist the central office in

the matter of development, planning and review of business and

supervision of divisional offices within their jurisdiction. Divisional office is

akin to a head office of an erstwhile insurer and is concerned with all

activities of the insurer from procurement of new business to settlement of

claims. Under each divisional office there are branch offices and sub-

offices.

At the time of nationalization, LIC had 5 Zonal Offices, 33 Divisional

Offices and 240 Branch Offices. As on 31st March 2007, the Corporation has

8 Zonal Offices, 101 Divisional Offices, 2048 Branch Offices and 132

Satellite Offices (SOs) 4. One Divisional Office at Mumbai is functioning

exclusively for business under Salary Savings Scheme.

MARKETING ACTIVITIES OF LIFE INSURANCE CORPORATION OF

INDIA

103

A life insurance company’s success reflects the consolidated effort of

all of its activities. These activities may be arranged into three major

functional classifications – marketing, investments, and administration. Of

these three areas, marketing is the largest in terms of both personnel

requirements and costs and is critical to success5.

Insurance marketing is an effort to transform the prospects into

actual policyholders6. The twofold goal of marketing is to attract new

customers by promising superior value and to keep current customers

satisfied by delivering value added services 7. Ensuring life security to an

individual and his family calls for the concerted efforts at four levels,

namely; (i) Insurer (LIC of India), (ii) Branch Manager, (iii) Development

officer, and (iv) Agent (Intermediary). The duties and responsibilities of

different functionaries of LIC of India are briefly described in the following

pages.

Central Office

The Central Office located at Mumbai has mainly a policy making and

co-ordinating role. In general, at the Central Office broad policy decisions

are taken on the recommendations of the Departmental Heads by the

Chairman or the appropriate committee of the Corporation or the

Corporation itself. Marketing department of the Central Office deals with

the planning of the development of new business, opening up of new

offices. All matters relating to development officers and agents are

processed by the marketing department of the Central Office, in assistance

with the various operating Divisional Offices. The foreign operations cell of

the marketing department handles all foreign business of the Corporation.

The Corporation mobilizes peoples’ savings and invests the same according

to the investment priorities prescribed by the IRDA Regulations and the LIC

104

of India Act, 1956. It acts as trustees of the policyholders. It is the duty

and responsibility of the Corporation to conduct business with care.

Product development and pricing are the important functions of the

Corporation. It is the function of the Development Department to develop

training programme for branch officials, development officers and agents.

Publicity and public relations are also looked after by this department.

Zonal Office

The Zonal Offices of the Corporation are at Mumbai, Hyderabad, New

Delhi, Bhopal, Kanpur, Patna, Kolkatta, and Chennai. Southern Zone

comprises of the States of Tamil Nadu, Kerala, Union Territories of

Pondicherry and Lakshadweep. A Zonal Office has under its jurisdiction a

number of Divisional Offices as well as Branch Offices for effective and

better services to the policyholders. The marketing department at the

Zonal Office prepares marketing strategy for development of new business.

Proposals on sub-standard risk and proposals beyond the limits of the

divisional offices are underwritten by the Zonal Offices. It reviews the

Divisional Office’s budget for various departments, aids and advises

Divisional Offices for better services to policyholders, conducts product

research, and organizes the training programme for the Development

Officers.

Divisional Office

A divisional office is akin to a head office of an erstwhile insurer and

is concerned with all activities of the insurer from procurement of new

business to settlement of claims. There are 12 Divisions in the Southern

Zone; 8 in Tamil Nadu and 4 in Kerala. The Divisional Offices in Kerala are:

(1) Thiruvananthapuram, (2) Kottayam, (3) Ernakulam and (4) Kozhikode.

The branches in Kasargod and Kannur districts fall under the jurisdiction of

Kozhikode Division.

105

The marketing department at Divisional Office supervises the quality

of work done in various branches through its various sections. The sales

section is entrusted with the functions of product research vis-à-vis the

markets, review of branch plans to develop agency force, recruitment of

agents, appointment of development officers, opening of branches,

allocation of territories between branches, analysis and review of monthly

performance of branches, conducting of training programme for Assistant

Branch Managers (sales), Development Officers and Agents, deciding cases

beyond the branch authority, processing of ‘early claims’, etc. As on March

31, 2007, there were 101 divisional offices in India including one salary

savings scheme (SSS) division at Mumbai.

Branch Office

The Branch Office of the Corporation is the main operating office in

the sense that this is the only office where sales of insurance products are

made and services given. At the time of nationalization LIC had 240 branch

offices; the number increased to 2,048 by 1998 8. During the period

between 1998 and 2007 no single branch office was opened. But with a

vision of providing easy access to its policyholders, LIC has launched as

many as 132 Satellite Offices (SOs) during the period from 2005 to 2007.

These satellite offices, which are attached to the respective parent

branches, are basically an extension of the large parent branches for

services to policyholders. Processing of new proposals and collection of

renewal premium are the main functions of these offices.

Each branch is given a specific area of operation and is expected to

strictly adhere to the territorial limits for procuring business. New business

is brought in by licensed agents, banks under the bancassurance and

corporate agents. Issue or renewal of license to agents is made according

106

to the provisions contained in the Insurance Regulatory and Development

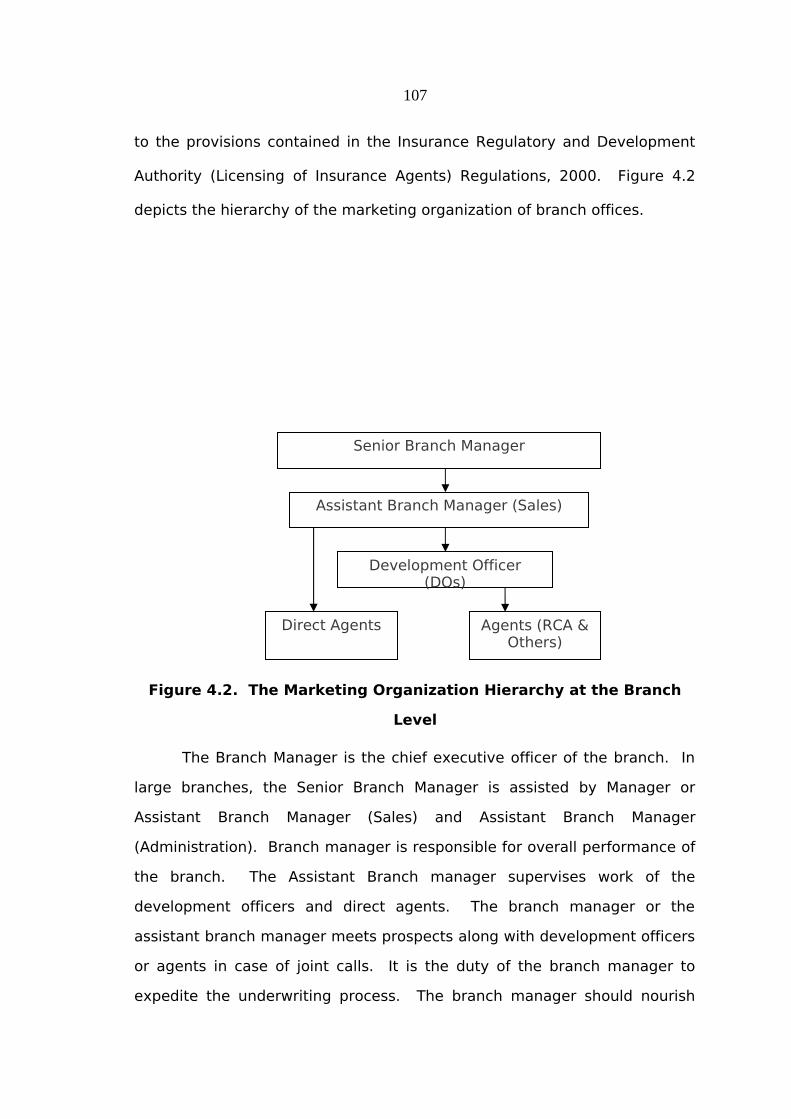

Authority (Licensing of Insurance Agents) Regulations, 2000. Figure 4.2

depicts the hierarchy of the marketing organization of branch offices.

Figure 4.2. The Marketing Organization Hierarchy at the Branch

Level

The Branch Manager is the chief executive officer of the branch. In

large branches, the Senior Branch Manager is assisted by Manager or

Assistant Branch Manager (Sales) and Assistant Branch Manager

(Administration). Branch manager is responsible for overall performance of

the branch. The Assistant Branch manager supervises work of the

development officers and direct agents. The branch manager or the

assistant branch manager meets prospects along with development officers

or agents in case of joint calls. It is the duty of the branch manager to

expedite the underwriting process. The branch manager should nourish

Senior Branch Manager

Assistant Branch Manager (Sales)

Development Officer (DOs)

Agents (RCA & Others)

Direct Agents

107

enthusiasm in employees and agents. Preparing performance budgets at

the branch level, timely reporting of performance of the branch to Divisional

Office, and prompt and unfailing service to the customers are the duties of

the branch manager.

Development Officers

Development officers are the field personnel in the distribution of life

insurance products. They create time, place and possession utility to

insurance products. They can appoint agents and give the initial training

for selling life insurance products. The duties and responsibilities of a

development officer shall be:

To develop and increase the production of life insurance business in a

planned way as far as may be practicable in the area allotted by the

Corporation.

To guide, supervise and direct the activities of the agents placed

under their supervision by the Corporation.

To introduce suitable persons to the Corporation for appointment as

new agents.

To act generally in such a way as to activate existing agents and

motivate new agents, so as to develop a stable agency force.

To render all such services to policyholders conducive to better policy

servicing.

To carry out the investigation of claims, revival of lapsed policies and

liaison work in connection with the Salary Savings Scheme business.

It is the obligation of development officers to ensure that the agents

under them conduct their work and / or business strictly in accordance with

the provisions of the Insurance Act, 1938 and Rules framed there under, LIC

of India (Agents) rules 1972 read with IRDA (licensing of Insurance Agents)

108

Regulations, 2000 as amended from time to time and in the best interest of

the Corporation.

Individual Agents

Individual agents are the most important distribution channels in life

insurance marketing. The success of an insurance company is highly

dependent on the army of agents and brokers 9. The Insurance Act, 1938

defines “Insurance Agent” as agent licensed under section 42 being an

individual who receives or agrees to receive payment by way of commission

or other remuneration in consideration of his soliciting or procuring

insurance business including business relating to the continuance, renewal

or revival of policies of insurance. Individual agents are classified into

Direct Agents and Career Agents. The Corporation has a scheme of career

agents to promote the cause of professionalising the agency force. There

are two types of Career Agents: (i) Urban Career Agents (UCAs), and (ii)

Rural Career Agents (UCAs). UCAs are recruited for the Career Branch at

the Divisional Office. To carry out the field operations, the Divisional

Marketing Manager appoints career agents and ordinary (direct) agents on

the recommendation of the Branch Manager. Direct agent’s job is

supervised by the Branch Manager or Assistant Branch Manager (Sales) and

career agent’s job is supervised by the development officer. Career agents

are paid stipend for three years and they are given training at the branch

office.

The regulation regarding appointment, licensing and remuneration of

agents are laid in the Insurance Agents’ Regulations, 2000 of the IRDA Act.

As per the Regulation, each person aspiring to be an agent has to undergo

practical training of 100 hours in life or general insurance, as the case may

be. In case of composite agent, he/she should have completed at least 150

hours of practical training in life and general insurance business combined.

109

The training has to be conducted by an institute approved and notified by

the IRDA.

An agent is required to do a Minimum Business Guarantee (MBG) of

12 policies (12 lives) in a year. If he/ she can’t achieve the minimum

guaranteed business, agency is terminated. There is no limit regarding the

number of career agents that a development officer can recruit and

supervise. Similar is the case of direct agents. The functions of agents laid

down in Rule 8 of the Life Insurance Corporation of India (Agents) Rules

1972 are as under 10.

Every agent shall solicit and procure new life insurance business which

shall not be less than the minimum prescribed in these rules and shall

endeavour to conserve the business already secured.

In procuring new business, an agent shall take into consideration the

needs of the prospect and his premium paying capacity.

The agent should make all reasonable enquiries in regard to the lives to

be insured before recommending proposals for acceptance. He should

bring to the notice of the Corporation any circumstances which may

adversely affect the risk to be underwritten. For this purpose, Agent’s

Confidential Report and in all cases of large sum proposed, a Moral

Hazard Report (MHR) is obtained from agents.

An agent shall not interfere with any proposal introduced by any other

agent.

Every agent shall maintain contact with all persons who have become

policyholders of the Corporation through him and shall advice every

policyholder to effect nomination or assignment in respect of their policy

and offer necessary assistance in this behalf.

110

The agent shall endeavour to ensure that the policyholder remits

premium within the days of grace, and prevent lapsing of a policy or its

conversion into a paid-up policy.

Render all reasonable assistance to the claimants in filling claim forms.

As per the Rules, agents are strictly prohibited:

• From advancing premium on behalf of proposers or policyholders.

• From printing, publishing or circulating any leaflets, handbills or

advertisements, etc. relating in any way to the Corporation even

at their own cost.

• From allowing or offering to allow directly or indirectly commission

or rebate to a proposer or life assured.

• From collecting any moneys from proponents or policyholders.

They may however collect deposits towards the first premium and

renewal premium, and remit the same to the Corporation

immediately.

The total number of agents on roll of the Corporation was 11,03,047

as at 31st March, 2007 against 10,52,283 as at 31st March 2006. Agents get

commission at the prescribed rate in respect of policies canvassed by them.

The rate of commission is 2 percent for single premium and on regular

premium policies it varies between 5 to 25 percent and depends on type of

policies11. Life insurance salesmen, unlike other salesmen, receive renewal

commission on their past business. Renewal commission is paid for

continued service the agent is expected to render to the policyholders.

Unlike the case of other commodities, insurance customers do not

normally go in search of agent or the product. The agent has to find out

people, meet them, discuss with them, and convert the prospect in to

customer. Different steps followed in insurance selling process are given in

111

figure 4.3. A sale results when the salesman takes the prospect along with

him through well defined steps. These steps are not separate and clear-cut

but blend into one integrated process if it can be so called.

Figure 4.3. Life Insurance Selling Process

Source: Yogakshema, Vol. IX, Issue 1, January 2001.

Over the years on account of the trust and the huge network of

agents that has been built, LIC has come to occupy a special place in the

hearts of its policy holders. The impact that the agent will make on his

prospect on the basis of his personality, knowledge and presentation skills

will be crucial and may finally help him to close the sale. The agent will

also have to work from the point of view of the best interest of the

customer; his own interest will have to get relegated to secondary place 12.

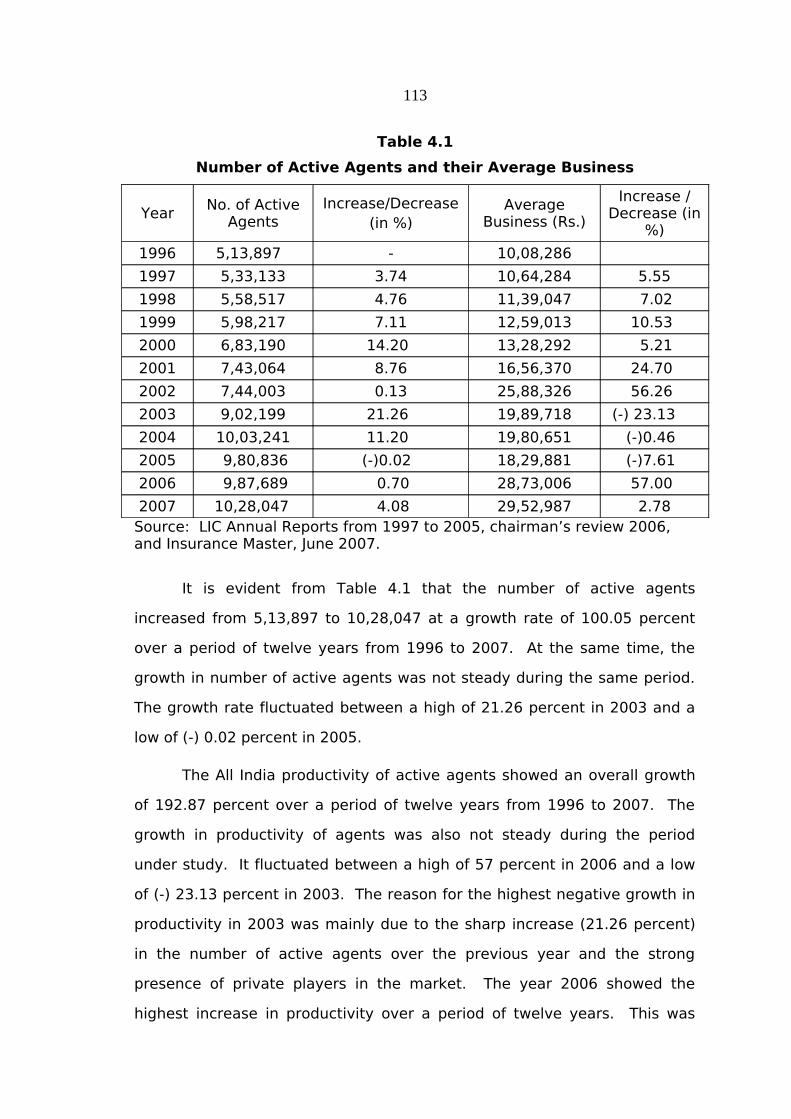

Table 4.1 shows the growth in the number of active agents and their

average business during the last twelve years from 1996 to 2007. The

total number of agents on the roll of LIC was 11,03,047 as at 31.03.2007 as

against 10,52,283 as at 31.03.2006. Whereas the number of active agents

was 10,28,047 as at 31.03.2007 as compared to 9,87,689 as at

31.03.2006.

112

Prospecting Pre-approach and Approach

Interview Solicitation

Policy Preparation

Underwritting Acceptance Offer-Proposal

Table 4.1

Number of Active Agents and their Average Business

YearNo. of Active

AgentsIncrease/Decrease

(in %)Average

Business (Rs.)

Increase / Decrease (in

%)

1996 5,13,897 - 10,08,286

1997 5,33,133 3.74 10,64,284 5.55

1998 5,58,517 4.76 11,39,047 7.02

1999 5,98,217 7.11 12,59,013 10.53

2000 6,83,190 14.20 13,28,292 5.21

2001 7,43,064 8.76 16,56,370 24.70

2002 7,44,003 0.13 25,88,326 56.26

2003 9,02,199 21.26 19,89,718 (-) 23.13

2004 10,03,241 11.20 19,80,651 (-)0.46

2005 9,80,836 (-)0.02 18,29,881 (-)7.61

2006 9,87,689 0.70 28,73,006 57.00

2007 10,28,047 4.08 29,52,987 2.78Source: LIC Annual Reports from 1997 to 2005, chairman’s review 2006, and Insurance Master, June 2007.

It is evident from Table 4.1 that the number of active agents

increased from 5,13,897 to 10,28,047 at a growth rate of 100.05 percent

over a period of twelve years from 1996 to 2007. At the same time, the

growth in number of active agents was not steady during the same period.

The growth rate fluctuated between a high of 21.26 percent in 2003 and a

low of (-) 0.02 percent in 2005.

The All India productivity of active agents showed an overall growth

of 192.87 percent over a period of twelve years from 1996 to 2007. The

growth in productivity of agents was also not steady during the period

under study. It fluctuated between a high of 57 percent in 2006 and a low

of (-) 23.13 percent in 2003. The reason for the highest negative growth in

productivity in 2003 was mainly due to the sharp increase (21.26 percent)

in the number of active agents over the previous year and the strong

presence of private players in the market. The year 2006 showed the

highest increase in productivity over a period of twelve years. This was

113

because of the aggressive marketing strategy followed for LIC’s golden

jubilee product ‘Bima Gold’ and active participation of many agents in the

campaign. Up on analysis of Table 4.1, one could find that the increase in

number of active agents was not followed by proportionate increase in

productivity.

Alternative Channels

Any sales process which does not involve the tied channels will be

called an alternative channel13. Channels play a pivotal role in marketing ;

they perform a number of vital distribution functions. Firms rely on the

marketing channels for generating customer satisfaction and for achieving

differentiation over competitors. Channels are thus a vital source of

competitive advantage. Agents were the only mode of distribution of life

insurance products in India till 2003. Today a number of innovative

alternative channels are being offered to consumers. The alternative

channels became popular in India with the emergence of private players

with foreign collaboration14. Some of them are Bancassurance, Brokers,

Corporate Agents, Internet Marketing, Tele Marketing, etc. The figure 4.4

gives a clear picture of the marketing channels of LIC.

Figure 4.4. Marketing Channels of LIC

114

Individual Agents

Alternative Channels

Bancassurance Broker

s

Corporate Agents

Marketing Channels of LIC

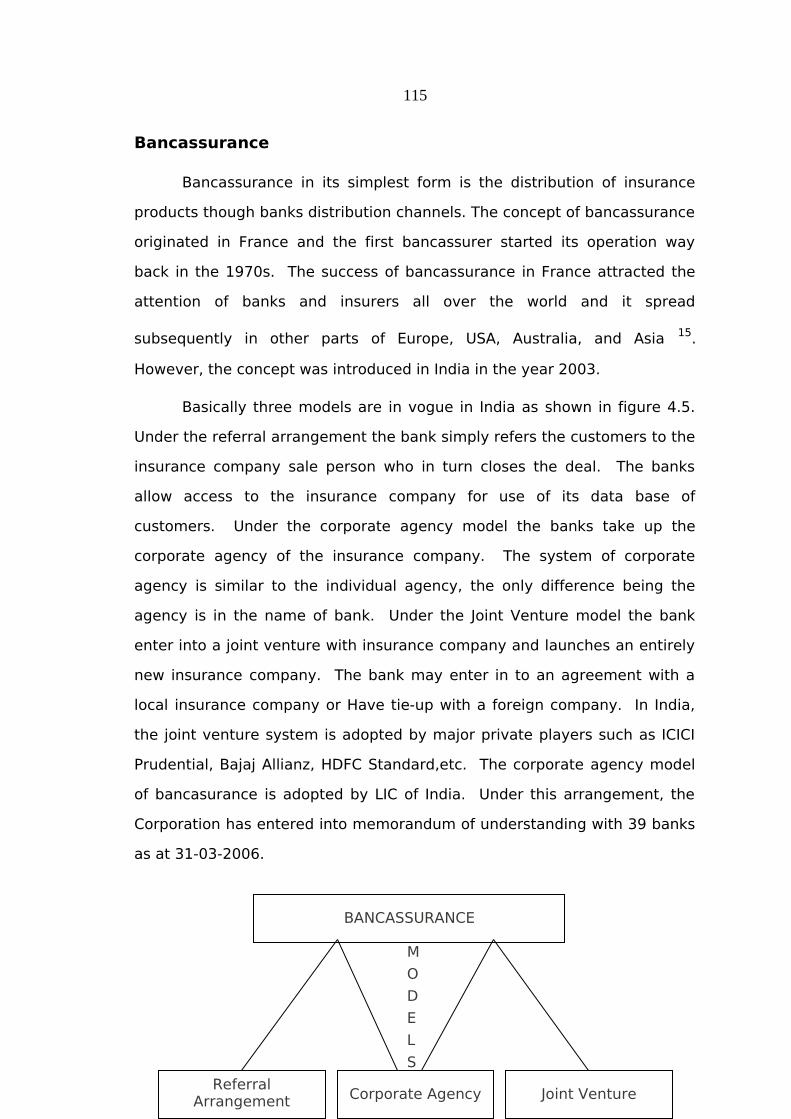

Bancassurance

Bancassurance in its simplest form is the distribution of insurance

products though banks distribution channels. The concept of bancassurance

originated in France and the first bancassurer started its operation way

back in the 1970s. The success of bancassurance in France attracted the

attention of banks and insurers all over the world and it spread

subsequently in other parts of Europe, USA, Australia, and Asia 15.

However, the concept was introduced in India in the year 2003.

Basically three models are in vogue in India as shown in figure 4.5.

Under the referral arrangement the bank simply refers the customers to the

insurance company sale person who in turn closes the deal. The banks

allow access to the insurance company for use of its data base of

customers. Under the corporate agency model the banks take up the

corporate agency of the insurance company. The system of corporate

agency is similar to the individual agency, the only difference being the

agency is in the name of bank. Under the Joint Venture model the bank

enter into a joint venture with insurance company and launches an entirely

new insurance company. The bank may enter in to an agreement with a

local insurance company or Have tie-up with a foreign company. In India,

the joint venture system is adopted by major private players such as ICICI

Prudential, Bajaj Allianz, HDFC Standard,etc. The corporate agency model

of bancasurance is adopted by LIC of India. Under this arrangement, the

Corporation has entered into memorandum of understanding with 39 banks

as at 31-03-2006.

115

Referral Arrangement Corporate Agency Joint Venture

M

O

D

E

L

S

BANCASSURANCE

Figure 4.5. Bancassurance Models in India

Source: The Insurance Times, October 2004.

Corporate Agents

Many companies, firms, non-banking finance companies, co-

operative societies, etc., are also taking corporate agencies to market

insurance products. As on 31st March 2007, LIC had tie up with 628

corporate agents across the country. The Kerala State Financial Enterprises

Limited and District Co-operative Banks function as the corporate agents of

LIC in Kannur and Kasargod districts to sell life insurance products.

Brokers

The institution of brokers in India is in a nascent stage. But brokers,

who are professionals in the area of insurance, will be acting on behalf of

the customers, rendering quality advice to them not only on the products

but also on the life insurance company through which they can take such

products. There were 103 brokers in the marketing network of LIC as on

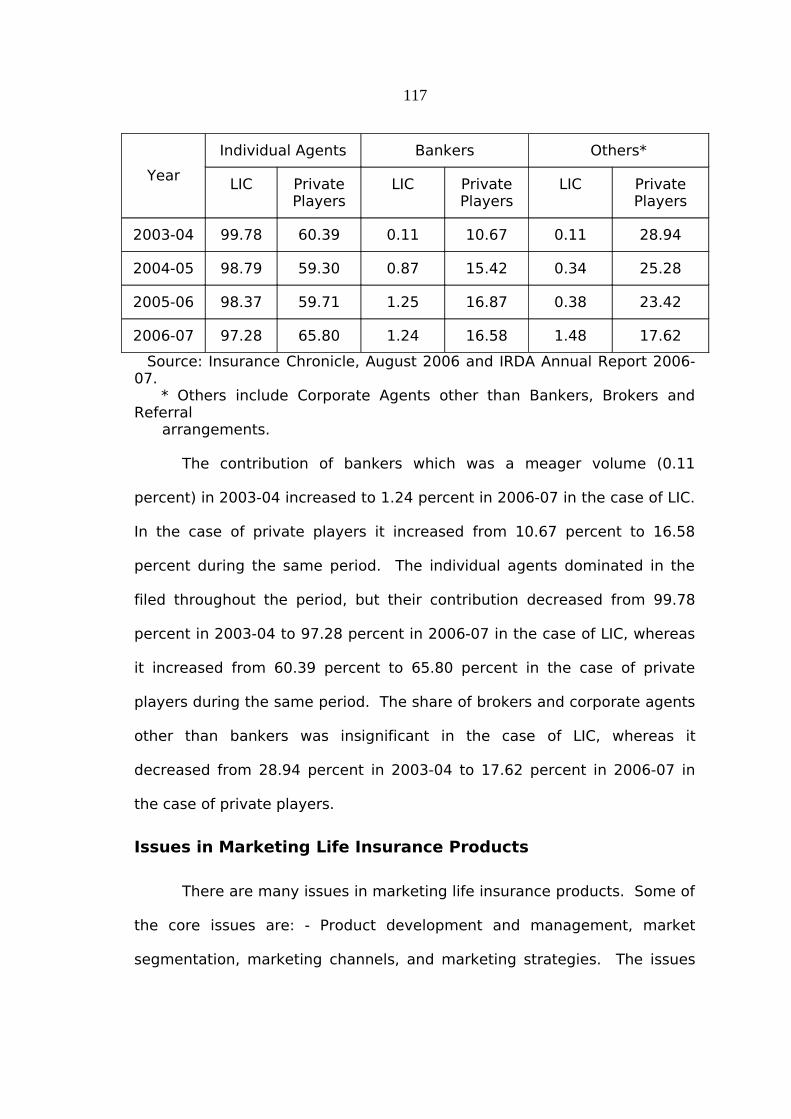

31st March, 2006 16. Table 4.2 reveals the percentage of new business

premium underwritten by the intermediaries of LIC and private players

during the four year period immediately following the year of introduction of

bancassurance in India.

Table 4.2

New Business Premium Underwritten through Various

Intermediaries

(In percent)

116

Year

Individual Agents Bankers Others*

LIC Private Players

LIC Private Players

LIC Private Players

2003-04 99.78 60.39 0.11 10.67 0.11 28.94

2004-05 98.79 59.30 0.87 15.42 0.34 25.28

2005-06 98.37 59.71 1.25 16.87 0.38 23.42

2006-07 97.28 65.80 1.24 16.58 1.48 17.62

Source: Insurance Chronicle, August 2006 and IRDA Annual Report 2006-07. * Others include Corporate Agents other than Bankers, Brokers and Referral arrangements.

The contribution of bankers which was a meager volume (0.11

percent) in 2003-04 increased to 1.24 percent in 2006-07 in the case of LIC.

In the case of private players it increased from 10.67 percent to 16.58

percent during the same period. The individual agents dominated in the

filed throughout the period, but their contribution decreased from 99.78

percent in 2003-04 to 97.28 percent in 2006-07 in the case of LIC, whereas

it increased from 60.39 percent to 65.80 percent in the case of private

players during the same period. The share of brokers and corporate agents

other than bankers was insignificant in the case of LIC, whereas it

decreased from 28.94 percent in 2003-04 to 17.62 percent in 2006-07 in

the case of private players.

Issues in Marketing Life Insurance Products

There are many issues in marketing life insurance products. Some of

the core issues are: - Product development and management, market

segmentation, marketing channels, and marketing strategies. The issues

117

regarding marketing channels were discussed in the preceding pages. The

other core issues are elaborated in the following pages.

Product Development and Management

In marketing, a product is anything that can be offered to a market

that might satisfy a want or need. When used as a business term, a

‘product’ can be either a physical, tangible good or service. A product is

both what a seller has to sell and what a buyer has to buy17. The policy is

termed as product in life insurance business. Since, in insurance business

the companies are engaged in selling services, and therefore, services are

their products18. Product management involves developing strategies and

tactics that will increase product demand over the products life cycle.

When an individual or an organization buys a policy from insurance

companies, not only policies are bought but agent’s assistance, advice and

prestige of insurance companies and the facilities of claim are also

bought19.

New product development starts with idea generation – the

systematic search for new-product ideas. Major sources of new-product

ideas include internal sources, and external sources such as customers,

competitors, agents and others. Using internal sources, the LIC find new

ideas through formal research survey and development. Meetings at

branch office and divisional office level with development officers, agents,

and customers, etc. will be helpful in understanding their needs and

requirements which will lead to development of new product ideas.

Practices developed by the marketing wing will encourage generation of

118

new ideas which can be screened and brought up to the Zonal Office (Z.O.)

and Central Office (C.O.). Procedures would also be evolved which would

facilitate interaction between marketing and actuarial wing so that

thorough consideration is given to feasibility of proposals vis-a-vis customer

needs and pricing.

Life Insurance Corporation offers a basket of schemes to meet the

various needs of an individual and his family. Only individual plans are

available for sale from branch offices through the intermediaries. The

group schemes and social security schemes are sold through Divisional

office. Under group scheme, LIC offers life insurance protection to various

groups such as employer-employee, professionals, co-operatives, weaker

sections of the society, etc.

119

Fig 4.6. LIC’s products

1. Basic Life Insurance Plansa) Whole Life Schemeb) Endowment Scheme

1. Group Term Assurance Schemes

1 Janasree Bima Yojana (JBY)

2. Term Assurance Plans Anmol Jeevan-I, New Bima Kiran. 3. Plans for Children Jeevan Anurag, KomalJeevan, Jeevan kishore, Jeevan Chhaya, Marriage/Education, Deferred Endowment.

4. Pension Plans – JeevanNidhi, Jeevan Akshay, New Jeevan Dhara, New Jeevan Suraksha, Future Plus.

5. Plans for HandicappedDependents – Jeevan Adar, Jeevan Viswas.

6. Joint Life PlanJeevan Sathy.

8. Unit Linked Plans - Bima Plus, Future Plus, Market Plus, Money Plus.

2. Group Term Insurance in lieu of EDLI

3. Group Gratuity Scheme

4. Group Super Annuation Scheme

5. Group Savings Linked Insurance

6. Group Leave Encash- ment Scheme

7. Group Mortgage Redemption Insurance

8. Scheme for Deposit Holders of Banks

2 Shiksha Sahayog Yojana (SSY)

7. Periodic Money Back PlanJeevan Rekha, Jeevan Surabhi, Jeevan Bharathi

9. Other Plans.

II GROUP SCHEMESI INDIVIDUAL PLANS III SOCIAL SECURITY SCHEMES

120

L I C’S P R O D U C T S

Figure 4.6 depicts popular plans developed by LIC. The object of

Social Security Scheme is to provide insurance protection to the rural and

urban poor below the poverty line or marginally above it. Under the

Janashree Bima Yojana, 50 percent of the premium is subsidized from the

Social Security Fund maintained by LIC and the remaining 50 percent is

contributed by members / Nodal agency / State Government. Products

launched by LIC before IRDA set up were 127. Products cleared by IRDA up

to 2007-08 are 46 plus 8 rider benefit products.

Unit-Linked Products of LIC

Unit-Linked policy is a new generation product which became popular

in Indian market after the entry of private players. Internationally, till

1960s, life insurance policies were sold as traditional or non-linked policies.

A unit-linked plan provides an opportunity for the discerning investor to

benefit from the returns available in the capital market without going for

direct investment in the capital market. In ULIPs, the investment element,

expenses and benefits are to the account of the policyholder20.

During the period from 2000 to 2007, LIC introduced five unit linked

policies such as Bima Plus, Future Plus, Jeevan Plus, Market Plus, and Money

Plus. Future Plus is a ULIP pension plan. The Bima Plus and Future Plus

ULIPs were closed for sale in the year 2006.

The Corporation grew at a rate of 23 percent in FPI during the pre-

liberalisation period (i.e., from 1994-95 to 1999-2000), whereas during the

competition period from 2000-01 to 2005-06, the average growth rate was

41 percent. The private sector has also performed well, growing at a rate of

105 percent 21. The analysis of the market performance indicates two

specific reasons for this growth. One, the market has shifted from

conventional products to ULIPS. Two, introduction of pure protection

121

products and riders and add-ons have changed the market. About 80 per

cent of the premium income of private players was from ULIPs, whereas it

was about 20 percent in the case of LIC in the year 2004-05. From 2005-06

onwards, LIC also has shifted from conventional products to ULIPs and

about 45 percent of the premium income was from this segment.

Life insurance companies give much importance to ULIPs because

these products impose very little liability on companies compared to

conventional products. As per the IRDA rules, an insurance company need

to keep 1.5 times of its insurance liability as solvency margin. In the case

of conventional products the entire premium amount is used for insurance

coverage, whereas only 20 percent of ULIPs premium amount is used for

insurance coverage. Therefore, companies are in a better position to make

available insurance products with low capital. But, focusing exclusively on

these could impair growth and long-term profitability for India’s life insurers

22.

Market Segmentation for LIC

The market for life insurance business is found vast, the potential

policyholders are large in number and their needs and requirements are not

identical. If the market segmentation is done in a right fashion, the

marketers find it convenient to identify the level of expectations of users.

The main purpose of market segmentation is to know the market. Unless

the Corporation knows the needs and requirements and identifies the level

of expectations of the policyholders, it is difficult to formulate a sound

marketing strategy.

122

Figure 4.7. Market Segmentation for LIC

The segmentation would help insurance professionals in making the

promotional measures creative which would be very much instrumental in

sensitizing the prospects. The advertisement appeals, messages,

campaigns can be made proactive to the receiving capacity of the target

audience. The sales promotion measures can also be innovated to get a

positive response. The segmentation would help insurance companies for

better product designing, identifying the agents for various segments and

preparing those agents to cater to their needs. Segment wise collected

SEGMENTS Sub-segments

REGION WISE

Central ZoneNorthern “ “Eastern “ “Southern “ “Western “ “

AREA WISE Urban AreaRural Area

INDUSTRIAL SECTORPublic sectorPrivate sector

Co-operative sector

INSTITUTIONAL SECTOR Universities, Colleges,Schools, Institutes

TRADE SECTOR Small businessBig business

GENDER WISE Men, Women

AGE WISE Kids, Teens, Youth, Grey

HOUEHOLD SECTORSalaried classSelf employed

Retired employeesWage earners

123

data simplifies the task of branch manager, especially while identifying a

profitable segment23.

Marketing Strategies of LIC

Just like manufacturing businesses, good service firm use marketing

to position them strongly in chosen target markets. Since services differ

from tangible products, they often require additional marketing approaches.

Successful service companies focus their attention on both their customers

and their employees. This suggests that services marketing also require

internal and interactive marketing24. The Corporation effectively train and

motivate its customer-contact employees and all the supporting service

people to work as a team to provide customer satisfaction. The Corporation

provides in house training facilities and external training opportunities to its

employees. Officers in the executive cadre were trained at MDC, Mumbai,

Insurance Institute of India located at 25 centres throughout India, and NIA,

Pune. Depending on the training needs, LIC also expose their agents and

development officers to different External Training Institutes (ETIs) for

specialized training.

During the year 2005-06, MDC conducted a total of 87 programmes

and training was imparted to 2,230 officials. Development officers and

agents were trained at 8 Zonal Training Centres, 25 Sales Training Centres,

101 Divisional Training Centres, and 520 agents’ Training Centres. In

addition to the above, meeting of managers at different levels,

development officers and agents were used to be conducted frequently, at

branch offices and divisional offices to evaluate the business performance

and services provided to customers.

One of the hottest strategies in marketing today is Customer

Relationship Marketing (CRM). CRM in life insurance is about understanding

the policyholders’ needs and encouraging this knowledge to increase sales

124

and improve service quality. CRM requires a team approach to serve the

policyholders, which makes it easier to take care of the needs and

expectations of the policyholders. At the branch offices of the Corporation,

there is one Customer Relations Executive to understand the policyholders’

needs and behaviours. This officer is required to hold at least two meeting

of customers; one before 31st January and second before 30th September of

every year. At the divisional office, the Manager Planning is given the

additional charge of Customer Relations Manager.

The Manager (Planning) at the divisional office has to prepare the

business budget for the branches under the control of the division, after

conducting market survey. But in actual practice, the budget is prepared

by adding a certain percentage (20% to 25%) to the previous year’s actual

performance. Designing and development of products take place at the

Central Office of the Corporation. The marketing strategies for the products

identified to market are also developed at the Central Office. But selection

of banks and other corporate agents, signing Memorandum of

Understanding (MoU) with them, etc. is done at the divisional office.

Advertising and other promotional activities, excepting erection of banners

and boards are done at the Zonal office level.

The marketing strategies of LIC are influenced by various factors.

Changes in the external and internal environment such as the Government

policies, financial markets, competitors’ policies, customer expectations,

regulatory mechanisms, technological developments, global scenario of

insurance market, etc. influence the marketing strategy of the Corporation.

BUSINESS PERFORMANCE OF LIC

With the opening of the insurance sector in 1999, more than a score

players entered into the insurance market. These new players have grown

steadily over a period of time and captured more than 20 percent of the

125

market by the end of March 2007 25. LIC during the last 52 years of its

existence has undergone several trials and tribulations, faced ups and

downs in business growth but managed to grow and metamorphose into a

giant in the industry. In the light of the above, the business performance of

LIC viewed from different dimensions like new business in terms of number

of products, sum assured, first premium income of products marketed,

growth of rural new business, etc. is presented in the following sections.

New Business – Number of Products (Individual Insurance)

Marketed

To spread life insurance at a reasonable cost is the first and foremost

objective of the Corporation. New business is a pointer towards the spread

of message of insurance among those people who have never availed of the

benefits of life insurance as well as the existing policyholders. LIC has its

insurance business in India as well as outside India. The business outside

India is negligible compared to the business in India. The new business

performance of LIC in terms of number of products marketed both in and

outside India for a period of twelve years from 1995-96 to 2006-07 is

depicted in Table 4.3.

The number of products marketed in India rose from 110.20 lakhs in

1995-96, which account for 99.87 percent, to 381.92 lakhs in 2006-07,

which constitute 99.96 percent of total products marketed. Number of

products marketed under new business – individual insurance has grown at

a rate of 246.28 percent over a period of 12 years from 1995-96 to 2006-

07. But the annual growth rate of products marketed fluctuated between a

low of (-) 17.53 percent in 2004-05 and a high of 44.65 percent in 2005-06.

The number of products marketed out of India was a meager 13,345

products in 1995-96, which constitute 0.12 percent only, and it rose to

15,792 in 2006-07, which constitute 0.04 per cent of total products

marketed by LIC. The annual growth rate of business outside India also

126

fluctuated between a low of (-) 37.45 percent in 2000-01 and a high of

19.42 per cent in 2004-05.

Table 4.3

Number of Products Marketed under New Business-Individual

Insurance

YearNo. of Products Marketed

Trend (%)

Annual Growth (in %)

In IndiaOutside India

Total In IndiaOutside

India1995-96 1,10,20,825

(99.87 %)13,345(0.12 %)

1,10,34,170 100 - -

1996-971,22,68,476

(99.89 %)12,296(0.11 %)

1,22,80,772 111.30 11.32 (-)7.86

1997-981,33,11,294

(99.89 13,904

(0.11 %)1,33,25,198 120.76 8.50 13.07

1998-991,48,43,687(99.90 %)

13,356(0.10 %)

1,48,57,043 134.64 11.51 (-)3.94

1999-001,69,76,782(99.93 %)

12,648(6.07 %)

1,69,89,430 153.97 14.37 (-)5.30

2000-011,96,56,663(99.95 %)

7,911(0.05 %)

1,96,64,574 178.21 15.78 (-)37.45

2001-022,24,91,304(99.95 %)

8,695(0.05 %)

2,24,99,999 203.91 14.42 9.91

2002-032,42,68,416((99.94 %)

10,359(0.06 %)

2,42,78,775 220.03 7.90 19.14

2003-042,64,56,320(99.56 %)

11,562(0.04 %)

2,64,67,882 239.87 9.01 11.61

2004-052,18,17,967(99.94 %)

13,807(0.06 %)

2,18,31,774 197.85 (-)17.53 19.42

2005-063,15,59,177(99.96 %)

13,370(0.04 %)

3,15,72,547 286.13 44.65 (-)3.16

2006-073,81,92,783(99.96 %)

15,792(0.04 %)

3,82,08,575 346.27 21.02 18.11

Source: Annual Reports of LIC of India (1995-96 to 2004-05) and Insurance Master, June 2007.Note: Figures in parenthesis shows percentage to total.

The relatively low annual growth rate of products marketed in India

in 2002-03 and the negative growth in 2004-05 could be attributed to

various factors like the withdrawal of tax benefits on single premium bonds

in 2002-03, the imposition of 5 percent service tax on premium payments

made which was subsequently withdrawn, the fall of interest rates and the

127

resultant withdrawal of guaranteed return products. The drought situation

during 2002-03 also had adversely affected the business of LIC.

The introduction of more and more Unit Linked Products by private

players, decline in number of agents, severe competition from new players

and strike by development officers as a result of withdrawal of certain

benefits enjoyed by them previously, resulted into negative growth of

business in the year 2004-05 26. The spurt growth of 44.65 percent in

2005-06 can be attributed to: (i) aggressive marketing strategy adopted by

the Corporation for marketing its golden jubilee product – ‘Bima Gold’, (ii)

concentration on unit linked products, and (iii) recovery of agriculture

sector.

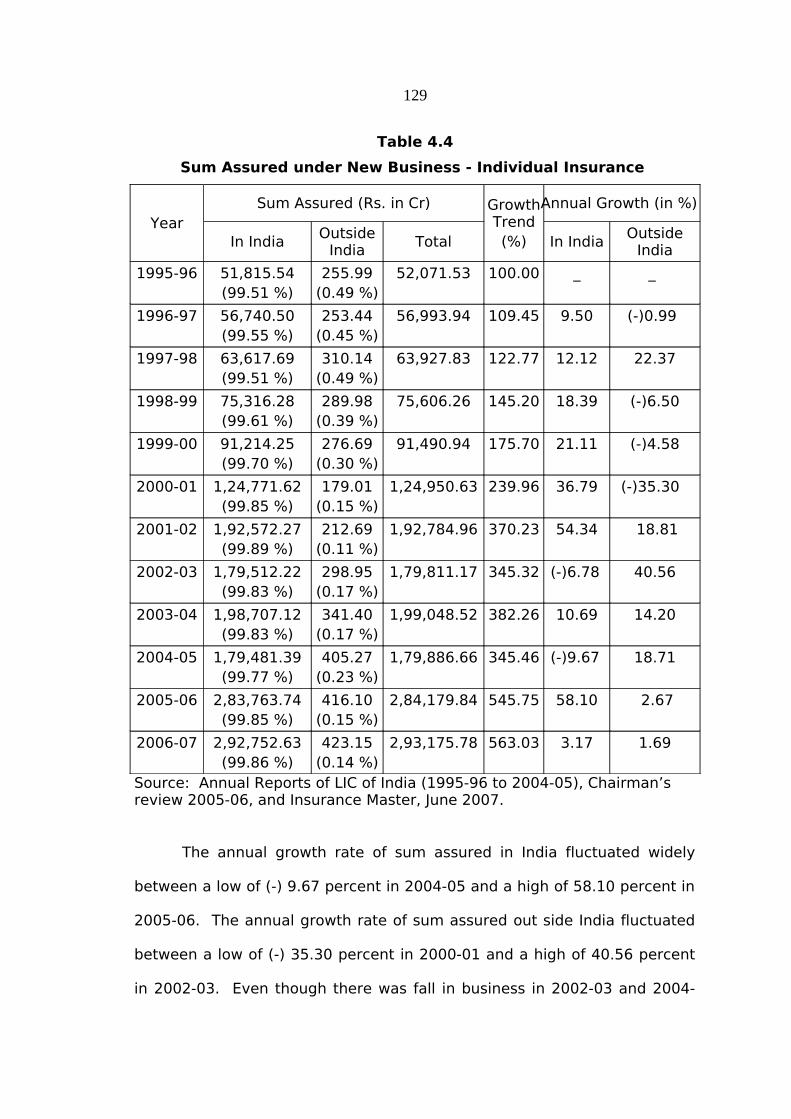

Sum Assured of products Marketed

Up to the year 2004-05, LIC gave much emphasis for both sum

assured and premium income of products marketed. But from the year

2005-06 onwards greater emphasis was being given for premium income

and number of policies marketed. The sum assured under new business for

the period from 1995-96 to 2006-07 is depicted in Table 4.4.

During 1995-96, the sum assured under new business in India was

Rs.51,815.54 crores, which accounts 99.51 percent while it was Rs.255.99

crores outside India, which constitutes 0.49 percent only. Sum assured of

business in India rose to Rs.2,92,752.63 crores (99.86 percent) in 2006-07,

while it was Rs.423.15 crores (0.14 percent) outside India. In case of sum

assured of products marketed in India, the performance of the Corporation

has been quite satisfactory during the period under study except for two

years, i.e., 2002-03 and 2004-05 when there was a fall in the amount of

sum assured.

128

Table 4.4

Sum Assured under New Business - Individual Insurance

YearSum Assured (Rs. in Cr) Growth

Trend(%)

Annual Growth (in %)

In IndiaOutside

IndiaTotal In India

Outside India

1995-96 51,815.54(99.51 %)

255.99(0.49 %)

52,071.53 100.00 _ _

1996-97 56,740.50(99.55 %)

253.44(0.45 %)

56,993.94 109.45 9.50 (-)0.99

1997-98 63,617.69(99.51 %)

310.14(0.49 %)

63,927.83 122.77 12.12 22.37

1998-99 75,316.28(99.61 %)

289.98(0.39 %)

75,606.26 145.20 18.39 (-)6.50

1999-00 91,214.25(99.70 %)

276.69(0.30 %)

91,490.94 175.70 21.11 (-)4.58

2000-01 1,24,771.62(99.85 %)

179.01(0.15 %)

1,24,950.63 239.96 36.79 (-)35.30

2001-02 1,92,572.27(99.89 %)

212.69(0.11 %)

1,92,784.96 370.23 54.34 18.81

2002-03 1,79,512.22(99.83 %)

298.95(0.17 %)

1,79,811.17 345.32 (-)6.78 40.56

2003-04 1,98,707.12(99.83 %)

341.40(0.17 %)

1,99,048.52 382.26 10.69 14.20

2004-05 1,79,481.39(99.77 %)

405.27(0.23 %)

1,79,886.66 345.46 (-)9.67 18.71

2005-06 2,83,763.74(99.85 %)

416.10(0.15 %)

2,84,179.84 545.75 58.10 2.67

2006-07 2,92,752.63(99.86 %)

423.15(0.14 %)

2,93,175.78 563.03 3.17 1.69

Source: Annual Reports of LIC of India (1995-96 to 2004-05), Chairman’s review 2005-06, and Insurance Master, June 2007.

The annual growth rate of sum assured in India fluctuated widely

between a low of (-) 9.67 percent in 2004-05 and a high of 58.10 percent in

2005-06. The annual growth rate of sum assured out side India fluctuated

between a low of (-) 35.30 percent in 2000-01 and a high of 40.56 percent

in 2002-03. Even though there was fall in business in 2002-03 and 2004-

129

05, the Corporation improved its performance in 2005-06 as is evident from

the fact that the annual growth rate showed 58.10 percent increase over

the previous year. This can be attributed to the massive sale of LIC’s

golden jubilee policy – ‘Bima Gold’ and concentration on unit linked

products.

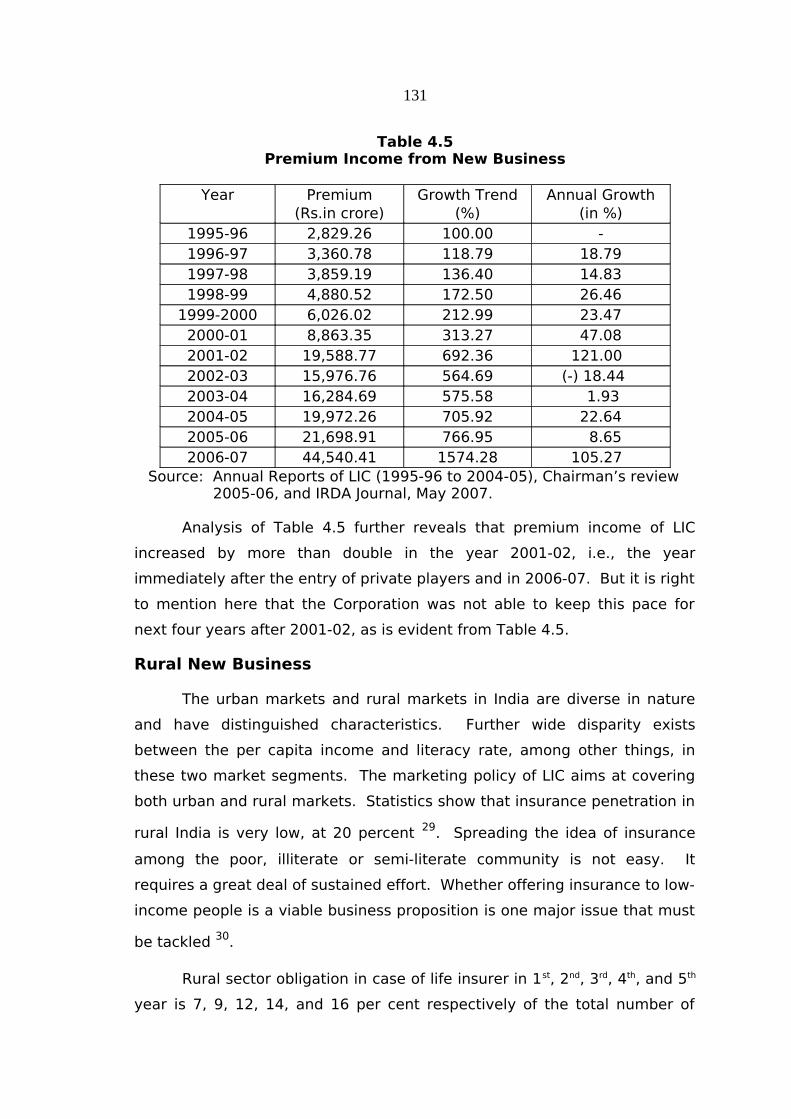

Premium Income from New Business

Premium is the fragmented value of the sum assured payable

continuously at regular intervals to the insurance company until maturity of

the policy. The quantum of premium income collected is the most

important indicator to assess the working results of an insurance company

27. Premium income can be classified into two: (i) first year premium, and

(ii) renewal premium. Premium collected on the new business is called first

year premium and premium collected on business in force is called renewal

premium. First Year Premium Income (FYPI) collected is taken to assess the

growth of a life insurance company 28. Premium income of LIC from new

business for the year 1995-96 to 2005-06 is depicted in Table 4.5.

Premium income of the Corporation has shown tremendous growth

during the period under study. The first year premium income which was

Rs.2,829.26 crores in 1995-96 increased to Rs. 44,540.41 in 2006-07 at a

growth rate of 1474 percent. But the annual growth in first year premium

income was not consistent throughout the period under study. FYPI growth

fluctuated between a high of 121 percent in 2001-02 and a low of (-) 18.44

percent in 2002-03. FYPI showed an increasing trend through out the

period under study except the year 2002-03.

130

Table 4.5 Premium Income from New Business

Year Premium(Rs.in crore)

Growth Trend(%)

Annual Growth(in %)

1995-96 2,829.26 100.00 -1996-97 3,360.78 118.79 18.791997-98 3,859.19 136.40 14.831998-99 4,880.52 172.50 26.46

1999-2000 6,026.02 212.99 23.472000-01 8,863.35 313.27 47.082001-02 19,588.77 692.36 121.002002-03 15,976.76 564.69 (-) 18.442003-04 16,284.69 575.58 1.932004-05 19,972.26 705.92 22.642005-06 21,698.91 766.95 8.652006-07 44,540.41 1574.28 105.27

Source: Annual Reports of LIC (1995-96 to 2004-05), Chairman’s review 2005-06, and IRDA Journal, May 2007.

Analysis of Table 4.5 further reveals that premium income of LIC

increased by more than double in the year 2001-02, i.e., the year

immediately after the entry of private players and in 2006-07. But it is right

to mention here that the Corporation was not able to keep this pace for

next four years after 2001-02, as is evident from Table 4.5.

Rural New Business

The urban markets and rural markets in India are diverse in nature

and have distinguished characteristics. Further wide disparity exists

between the per capita income and literacy rate, among other things, in

these two market segments. The marketing policy of LIC aims at covering

both urban and rural markets. Statistics show that insurance penetration in

rural India is very low, at 20 percent 29. Spreading the idea of insurance

among the poor, illiterate or semi-literate community is not easy. It

requires a great deal of sustained effort. Whether offering insurance to low-

income people is a viable business proposition is one major issue that must

be tackled 30.

Rural sector obligation in case of life insurer in 1st, 2nd, 3rd, 4th, and 5th

year is 7, 9, 12, 14, and 16 per cent respectively of the total number of

131

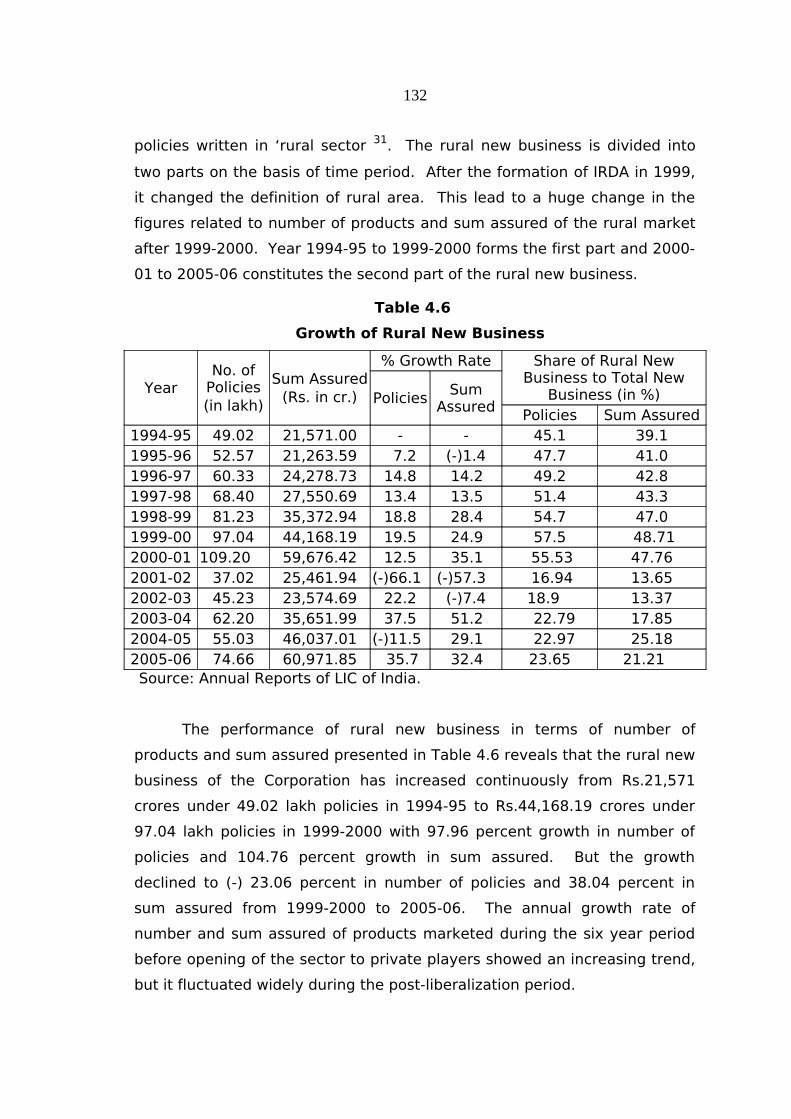

policies written in ‘rural sector 31. The rural new business is divided into

two parts on the basis of time period. After the formation of IRDA in 1999,

it changed the definition of rural area. This lead to a huge change in the

figures related to number of products and sum assured of the rural market

after 1999-2000. Year 1994-95 to 1999-2000 forms the first part and 2000-

01 to 2005-06 constitutes the second part of the rural new business.

Table 4.6

Growth of Rural New Business

YearNo. of

Policies(in lakh)

Sum Assured(Rs. in cr.)

% Growth Rate Share of Rural New Business to Total New

Business (in %)PoliciesSum

AssuredPolicies Sum Assured

1994-95 49.02 21,571.00 - - 45.1 39.11995-96 52.57 21,263.59 7.2 (-)1.4 47.7 41.01996-97 60.33 24,278.73 14.8 14.2 49.2 42.81997-98 68.40 27,550.69 13.4 13.5 51.4 43.31998-99 81.23 35,372.94 18.8 28.4 54.7 47.01999-00 97.04 44,168.19 19.5 24.9 57.5 48.712000-01 109.20 59,676.42 12.5 35.1 55.53 47.762001-02 37.02 25,461.94 (-)66.1 (-)57.3 16.94 13.652002-03 45.23 23,574.69 22.2 (-)7.4 18.9 13.372003-04 62.20 35,651.99 37.5 51.2 22.79 17.852004-05 55.03 46,037.01 (-)11.5 29.1 22.97 25.182005-06 74.66 60,971.85 35.7 32.4 23.65 21.21 Source: Annual Reports of LIC of India.

The performance of rural new business in terms of number of

products and sum assured presented in Table 4.6 reveals that the rural new

business of the Corporation has increased continuously from Rs.21,571

crores under 49.02 lakh policies in 1994-95 to Rs.44,168.19 crores under

97.04 lakh policies in 1999-2000 with 97.96 percent growth in number of

policies and 104.76 percent growth in sum assured. But the growth

declined to (-) 23.06 percent in number of policies and 38.04 percent in

sum assured from 1999-2000 to 2005-06. The annual growth rate of

number and sum assured of products marketed during the six year period

before opening of the sector to private players showed an increasing trend,

but it fluctuated widely during the post-liberalization period.

132

Figure 4.8Rural new business (number of policies) in India

0

20

40

60

80

100

120

1994-95 1995-96 1996-97 1997-98 1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06

Year

Num

ber

(Lak

hs)

Figure 4.9Growth in Rural New Business (Sum Assured)

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1994-95 1995-96 1996-97 1997-98 1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06

Year

Am

ount

(C

rore

s)

133

The share of products marketed in rural area to total new products

marketed has steadily increased from 45.1 percent in 1994-95 to 57.5

percent in 1999-2000. Similarly, the sum assured has steadily increased

from 39.1 percent to 48.71 percent during the same period. But the share

of rural products marketed and sum assured which was 55.53 percent and

47.76 percent respectively in 2000-01 declined to 23.65 percent and 21.21

percent respectively in 2005-06. From the above analysis it is evident that

LIC concentrated in urban areas and lost business in rural areas after

liberalization of the sector, as private players established their presence in

rural areas also by opening more and more branches. Figure 4.8 and 4.9

portrays the growth in number and sum assured of products marketed by

LIC in rural area during the pre-libralisation and post-liberalisation period.

LIFE INSURANCE MARKETING IN KASARGOD AND KANNUR

The Kasargod and Kannur districts which are situated in the northern

part of Kerala come under the Kozhikode Division of the LIC. Kozhikode

division is one of the prominent divisions under the Southern Zone. The

performance of marketing individual life insurance products of LIC in

Kasargod and Kannur districts vis-a vis the performance at national level is

evaluated from different dimensions like number of products marketed,

sum assured of products marketed, premium income on products

marketed, during the post liberalization period from 2001-02 to 2006-07.

Since the first private insurer after opening of the sector was established in

October 2000, the year 2001-02 has been taken as the first full year of

operations for assessing the business performance of LIC in the areas of

study.

Number of Products Marketed

Sustained and conscious efforts are required to carry the message of

life insurance into the rural areas, especially backward and remote areas.

The LIC agents play a vital role in persuading the rural folks to purchase life

134

insurance products of their choice by giving required information about

various insurance products. From 2004-05 onwards, LIC lay greater

emphasis for number of products sold as well as premium income for

measuring the growth of business. Table 4.7 exhibits the number as well as

growth of products marketed in Kannur and Kasargod districts and at All

India level during the period from 2001-2002 to 2006-2007.

Table 4.7Growth of Products Marketed (2001-02 to 2006-07)

YearNo. of Products Marketed in Growth (in %)

KANNUR KASAR-GOD

ALL INDIA KANNUR KASAR-GOD

ALL INDIA

2001-02 97,912 33,308 2,24,91,304 - - -

2002-03 1,12,615 39,095 2,42,68,416 15.02 17.37 7.90

2003-04 1,10,605 41,284 2,64,56,320 (-)1.78 5.60 9.01

2004-05 97,495 33,625 2,18,17,967 (-)11.85 (-)18.55

(-) 7.53

2005-06 1,41,327 52,433 3,15,72,547 44.96 55.93 44.71

2006-07 1,31,433 54,035 3,82,08,575 (-) 7.00 3.05 21.02

CAGR 6.07 10.16 11.18Source: Compiled from Divisional Office, Annual Reports of LIC (2002 to 2005), and IRDA Journal various issues.

Analysis of the Table 4.7 reveals that number of products marketed

showed a growth rate of 134.24 percent in Kannur and 162.23 percent in

Kasargod district, whereas it was 169.88 percent at all India level during the

post-liberalisation period from 2001-02 to 2006-07,. The annual growth

rate of products marketed fluctuated between a high of 44.96 percent in

2005-06 and a low of (-) 11.85 percent in 2004-05 in Kannur district,

whereas it fluctuated between a high of 55.93 percent in 2005-06 and a low

of (-) 18.55 percent in 2004-05 in Kasargod district. The Compound Annual

Growth Rate (CAGR) of 6.07 in Kannur and 10.16 in Kasargod reveals that

there is significant difference between the two districts regarding the

growth in number of products sold. Kasargod district was ahead of Kannur

district regarding growth in number of products sold, throughout the period,

135

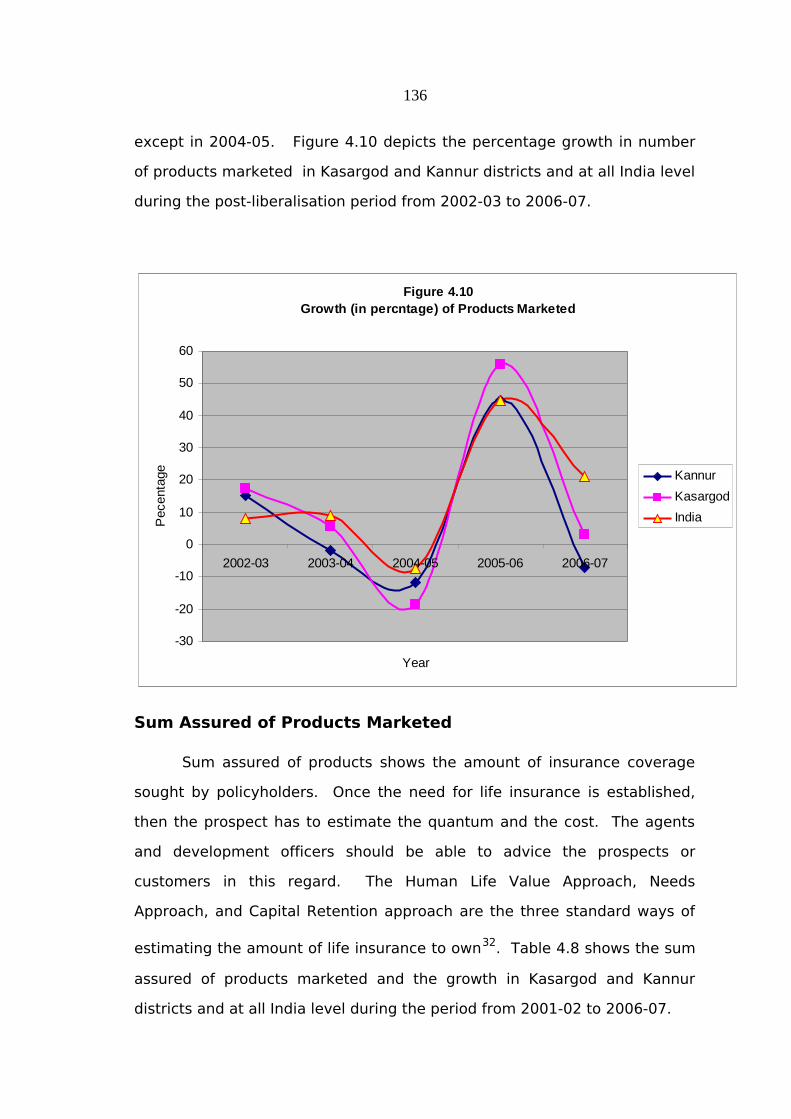

except in 2004-05. Figure 4.10 depicts the percentage growth in number

of products marketed in Kasargod and Kannur districts and at all India level

during the post-liberalisation period from 2002-03 to 2006-07.

Figure 4.10Growth (in percntage) of Products Marketed

-30

-20

-10

0

10

20

30

40

50

60

2002-03 2003-04 2004-05 2005-06 2006-07

Year

Pec

enta

ge Kannur

Kasargod

India

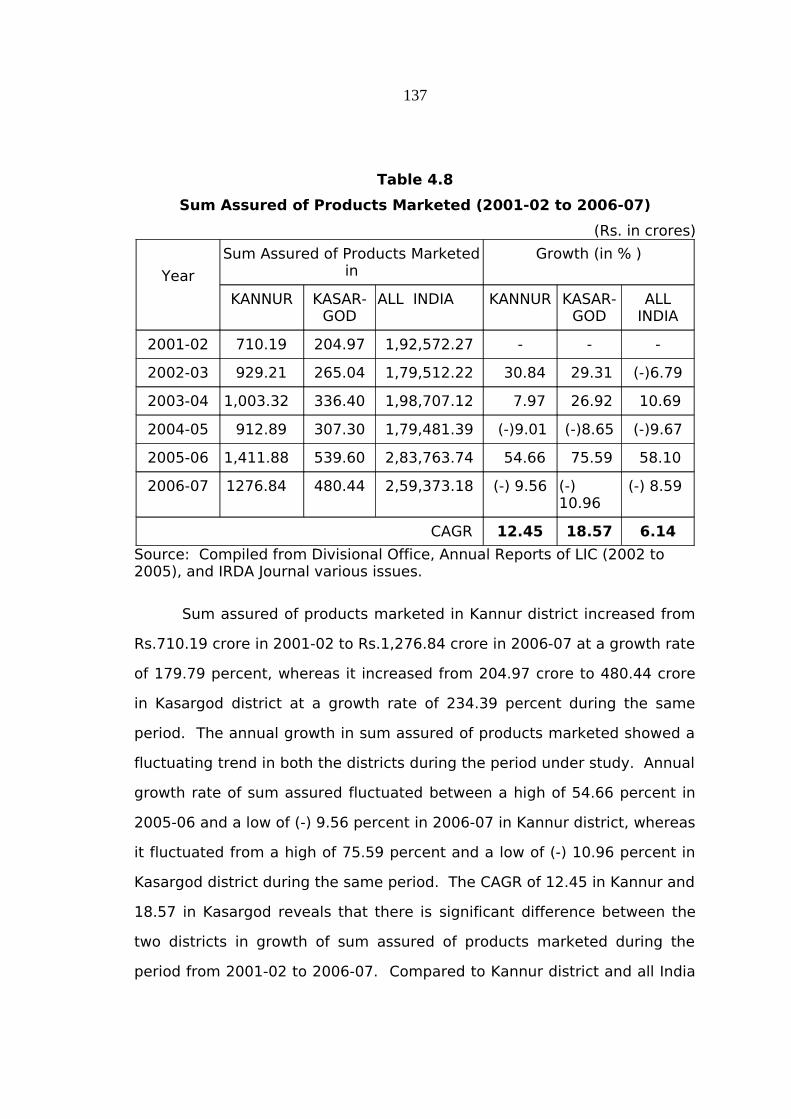

Sum Assured of Products Marketed

Sum assured of products shows the amount of insurance coverage

sought by policyholders. Once the need for life insurance is established,

then the prospect has to estimate the quantum and the cost. The agents

and development officers should be able to advice the prospects or

customers in this regard. The Human Life Value Approach, Needs

Approach, and Capital Retention approach are the three standard ways of

estimating the amount of life insurance to own32. Table 4.8 shows the sum

assured of products marketed and the growth in Kasargod and Kannur

districts and at all India level during the period from 2001-02 to 2006-07.

136

Table 4.8

Sum Assured of Products Marketed (2001-02 to 2006-07)

(Rs. in crores)

Year

Sum Assured of Products Marketed in

Growth (in % )

KANNUR KASAR-GOD

ALL INDIA KANNUR KASAR-GOD

ALL INDIA

2001-02 710.19 204.97 1,92,572.27 - - -

2002-03 929.21 265.04 1,79,512.22 30.84 29.31 (-)6.79

2003-04 1,003.32 336.40 1,98,707.12 7.97 26.92 10.69

2004-05 912.89 307.30 1,79,481.39 (-)9.01 (-)8.65 (-)9.67

2005-06 1,411.88 539.60 2,83,763.74 54.66 75.59 58.10

2006-07 1276.84 480.44 2,59,373.18 (-) 9.56 (-) 10.96

(-) 8.59

CAGR 12.45 18.57 6.14

Source: Compiled from Divisional Office, Annual Reports of LIC (2002 to 2005), and IRDA Journal various issues.

Sum assured of products marketed in Kannur district increased from

Rs.710.19 crore in 2001-02 to Rs.1,276.84 crore in 2006-07 at a growth rate

of 179.79 percent, whereas it increased from 204.97 crore to 480.44 crore

in Kasargod district at a growth rate of 234.39 percent during the same

period. The annual growth in sum assured of products marketed showed a

fluctuating trend in both the districts during the period under study. Annual

growth rate of sum assured fluctuated between a high of 54.66 percent in

2005-06 and a low of (-) 9.56 percent in 2006-07 in Kannur district, whereas

it fluctuated from a high of 75.59 percent and a low of (-) 10.96 percent in

Kasargod district during the same period. The CAGR of 12.45 in Kannur and

18.57 in Kasargod reveals that there is significant difference between the

two districts in growth of sum assured of products marketed during the

period from 2001-02 to 2006-07. Compared to Kannur district and all India

137

level, the sum assured of products marketed had grown significantly in

Kasargod district during the years 2003-04 and 2005-06.

Analysis of table 4.7 and 4.8 further reveals that there was fall in the

number as well as sum assured of products marketed in both the districts

and at all India level during the year 2004-05. The performance of the

division also showed a negative growth in the same year. The main

reasons for this can be attributed to: (i) concentration on Unit Linked

Products in 2004-05, and (ii) laxity on the part of Development Officers and

Agents as part of their All India strike in 2004-05 and competition from

private players.

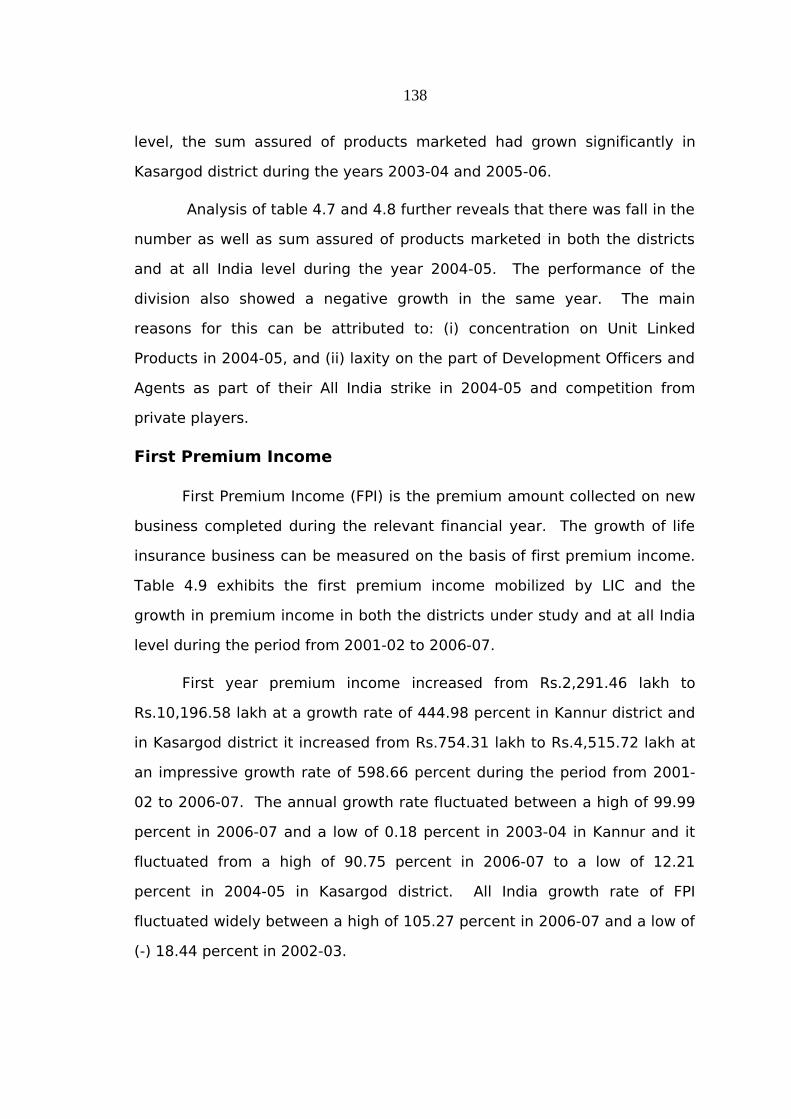

First Premium Income

First Premium Income (FPI) is the premium amount collected on new

business completed during the relevant financial year. The growth of life

insurance business can be measured on the basis of first premium income.

Table 4.9 exhibits the first premium income mobilized by LIC and the

growth in premium income in both the districts under study and at all India

level during the period from 2001-02 to 2006-07.

First year premium income increased from Rs.2,291.46 lakh to

Rs.10,196.58 lakh at a growth rate of 444.98 percent in Kannur district and

in Kasargod district it increased from Rs.754.31 lakh to Rs.4,515.72 lakh at

an impressive growth rate of 598.66 percent during the period from 2001-

02 to 2006-07. The annual growth rate fluctuated between a high of 99.99

percent in 2006-07 and a low of 0.18 percent in 2003-04 in Kannur and it

fluctuated from a high of 90.75 percent in 2006-07 to a low of 12.21

percent in 2004-05 in Kasargod district. All India growth rate of FPI

fluctuated widely between a high of 105.27 percent in 2006-07 and a low of

(-) 18.44 percent in 2002-03.

138

Table 4.9

First Premium Income Collected (2001-02 to 2006-07)

(Rs. in Lakhs)

Year

First Premium Income Collected in Growth (in %)

KANNUR KASAR-GOD

ALL INDIA KANNUR KASAR-GOD

ALL INDIA

2001-02 2,291. 46 754. 31 19,58,877.25 - - -

2002-03 3,232. 04 1,180. 90 15,97,676.15 41. 05 56. 55 (-)18.44

2003-04 3,237. 88 1,414. 63 16,28,468.67 0.18 19.79 1.93

2004-05 3,725. 45 1,587. 40 19,97,225.52 15.06 12.21 22.64

2005-06 5,098. 32 2,367. 35 21,69,891.21 36.85 49.13 8.65

2006-07 10,196.58 4,515.72 44,54,041.01 99.99 90.75 105.27

CAGR 34.79 43.03 22.69

Source: Compiled from Divisional Office, Annual Reports of LIC (2002 to 2005), and IRDA Journal various issues.

The CAGR reveals that there is significant difference between

Kasargod and Kannur districts regarding FPI collected during the period

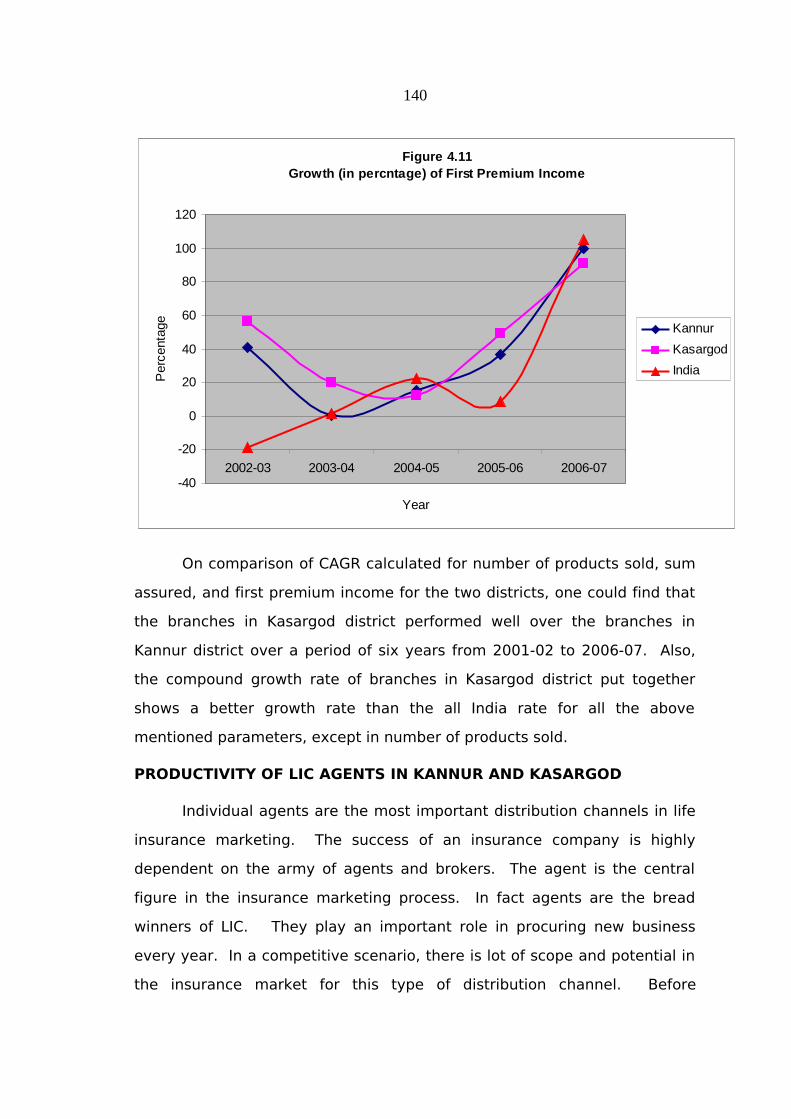

under study. Figure 4.11 depicts percentage growth in first premium

income in Kasargod and Kannur districts and at all India level during the

period from 2002-03 to 2006-07. The heavy growth in the first premium

income in the last two years of study can be attributed to: (i) concentration

on Unit Linked Policies, and (ii) aggressive marketing campaign adopted by

LIC for its Golden Jubilee product ‘Bima Gold’.

139

Figure 4.11Growth (in percntage) of First Premium Income

-40

-20

0

20

40

60

80

100

120

2002-03 2003-04 2004-05 2005-06 2006-07

Year

Per

cent

age

Kannur

Kasargod

India

On comparison of CAGR calculated for number of products sold, sum

assured, and first premium income for the two districts, one could find that

the branches in Kasargod district performed well over the branches in

Kannur district over a period of six years from 2001-02 to 2006-07. Also,

the compound growth rate of branches in Kasargod district put together

shows a better growth rate than the all India rate for all the above

mentioned parameters, except in number of products sold.

PRODUCTIVITY OF LIC AGENTS IN KANNUR AND KASARGOD

Individual agents are the most important distribution channels in life

insurance marketing. The success of an insurance company is highly

dependent on the army of agents and brokers. The agent is the central

figure in the insurance marketing process. In fact agents are the bread

winners of LIC. They play an important role in procuring new business

every year. In a competitive scenario, there is lot of scope and potential in

the insurance market for this type of distribution channel. Before

140

measuring productivity of agents, growth of individual agents in the two

districts and at all India level is assessed.

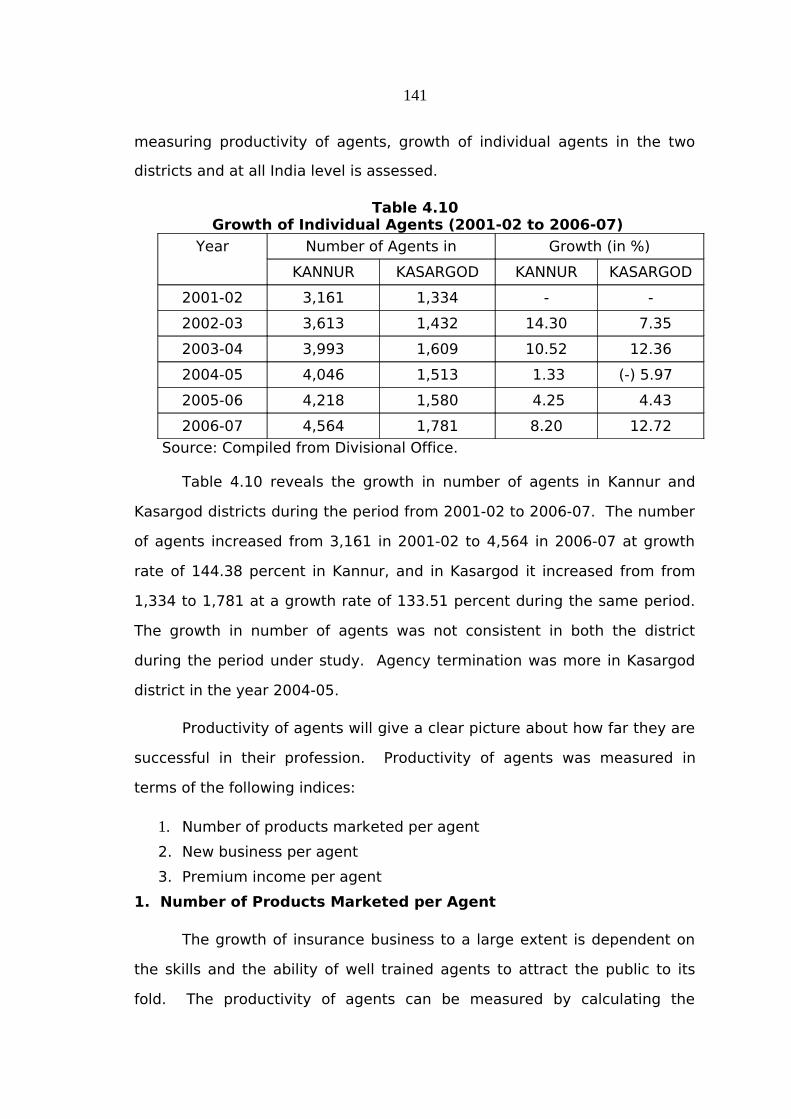

Table 4.10 Growth of Individual Agents (2001-02 to 2006-07)

Year Number of Agents in Growth (in %)

KANNUR KASARGOD KANNUR KASARGOD

2001-02 3,161 1,334 - -

2002-03 3,613 1,432 14.30 7.35

2003-04 3,993 1,609 10.52 12.36

2004-05 4,046 1,513 1.33 (-) 5.97

2005-06 4,218 1,580 4.25 4.43

2006-07 4,564 1,781 8.20 12.72

Source: Compiled from Divisional Office.

Table 4.10 reveals the growth in number of agents in Kannur and

Kasargod districts during the period from 2001-02 to 2006-07. The number

of agents increased from 3,161 in 2001-02 to 4,564 in 2006-07 at growth

rate of 144.38 percent in Kannur, and in Kasargod it increased from from

1,334 to 1,781 at a growth rate of 133.51 percent during the same period.

The growth in number of agents was not consistent in both the district

during the period under study. Agency termination was more in Kasargod

district in the year 2004-05.

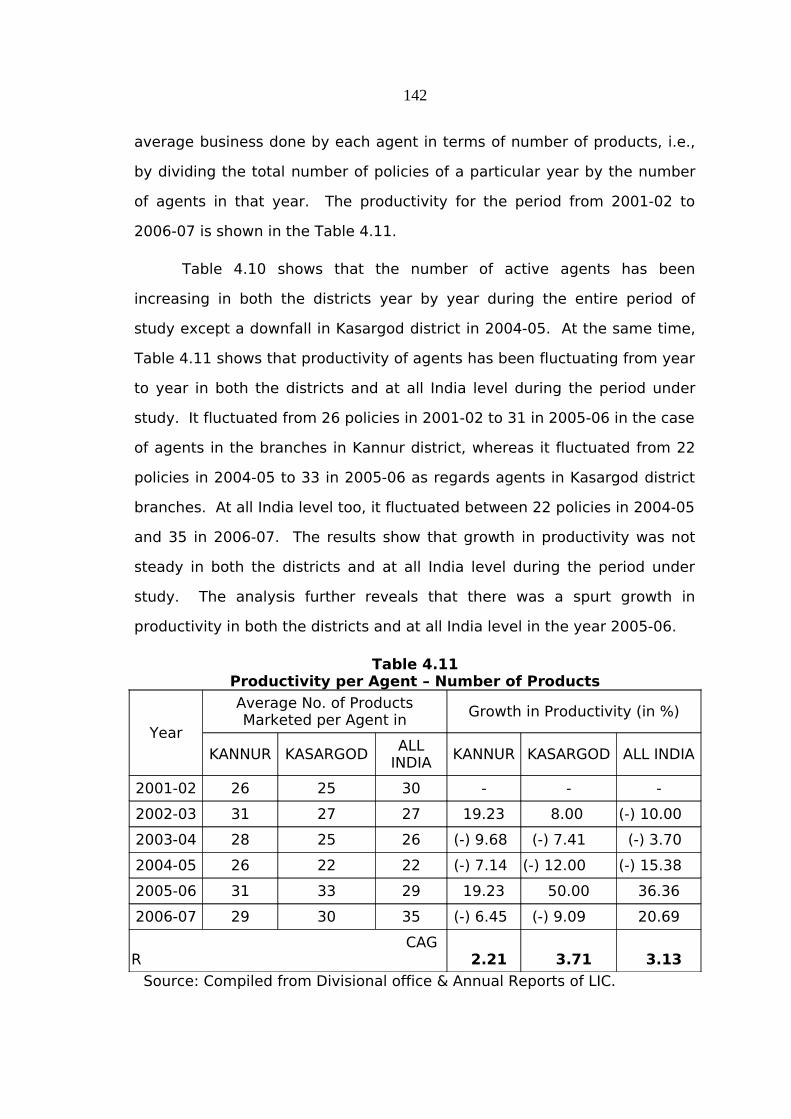

Productivity of agents will give a clear picture about how far they are

successful in their profession. Productivity of agents was measured in

terms of the following indices:

1. Number of products marketed per agent

2. New business per agent

3. Premium income per agent

1. Number of Products Marketed per Agent

The growth of insurance business to a large extent is dependent on

the skills and the ability of well trained agents to attract the public to its

fold. The productivity of agents can be measured by calculating the

141

average business done by each agent in terms of number of products, i.e.,

by dividing the total number of policies of a particular year by the number

of agents in that year. The productivity for the period from 2001-02 to

2006-07 is shown in the Table 4.11.

Table 4.10 shows that the number of active agents has been

increasing in both the districts year by year during the entire period of

study except a downfall in Kasargod district in 2004-05. At the same time,

Table 4.11 shows that productivity of agents has been fluctuating from year

to year in both the districts and at all India level during the period under

study. It fluctuated from 26 policies in 2001-02 to 31 in 2005-06 in the case

of agents in the branches in Kannur district, whereas it fluctuated from 22

policies in 2004-05 to 33 in 2005-06 as regards agents in Kasargod district

branches. At all India level too, it fluctuated between 22 policies in 2004-05

and 35 in 2006-07. The results show that growth in productivity was not

steady in both the districts and at all India level during the period under

study. The analysis further reveals that there was a spurt growth in

productivity in both the districts and at all India level in the year 2005-06.

Table 4.11Productivity per Agent – Number of Products

Year

Average No. of Products Marketed per Agent in

Growth in Productivity (in %)

KANNUR KASARGODALL

INDIAKANNUR KASARGOD ALL INDIA

2001-02 26 25 30 - - -

2002-03 31 27 27 19.23 8.00 (-) 10.00

2003-04 28 25 26 (-) 9.68 (-) 7.41 (-) 3.70

2004-05 26 22 22 (-) 7.14 (-) 12.00 (-) 15.38

2005-06 31 33 29 19.23 50.00 36.36

2006-07 29 30 35 (-) 6.45 (-) 9.09 20.69

CAGR 2.21 3.71 3.13

Source: Compiled from Divisional office & Annual Reports of LIC.

142

The CAGR of productivity for the entire study period was 2.21 in

Kannur, 3.71 in Kasargod, and 3.13 at all India level. On the basis of CAGR,

it can be concluded that growth in productivity of agents in the branches in

Kasargod district was better than the agents in the branches in Kannur

district and at all India level over a period of six years.

Table 4.12Analysis of Variance of Products Marketed per Agent

District Mean S D F ‘p’ value Significance

Kannur 28 2.26

0.652174

0.438124

Not SignificantKasargod 27 3.95

Total 27 3.17

The mean number of products marketed per agent was 28 (S.D. 2.26)

in Kannur and 27 (S.D. 3.95) in Kasargod. The analysis further reveals that

there is no significant difference in productivity in terms of number of

products marketed, between the agents in Kasargod and Kannur district

branches.

2. New Business per Active Agent

Agents play an important role in procuring new business every year.

In a competitive scenario, there is lot of scope and potential in the

insurance market for this type of distribution channel. Productivity in terms

of new business per LIC agent can be measured by dividing the total sum

assured in a year by the total number of active agents in that year. It gives

the average business per active agents.

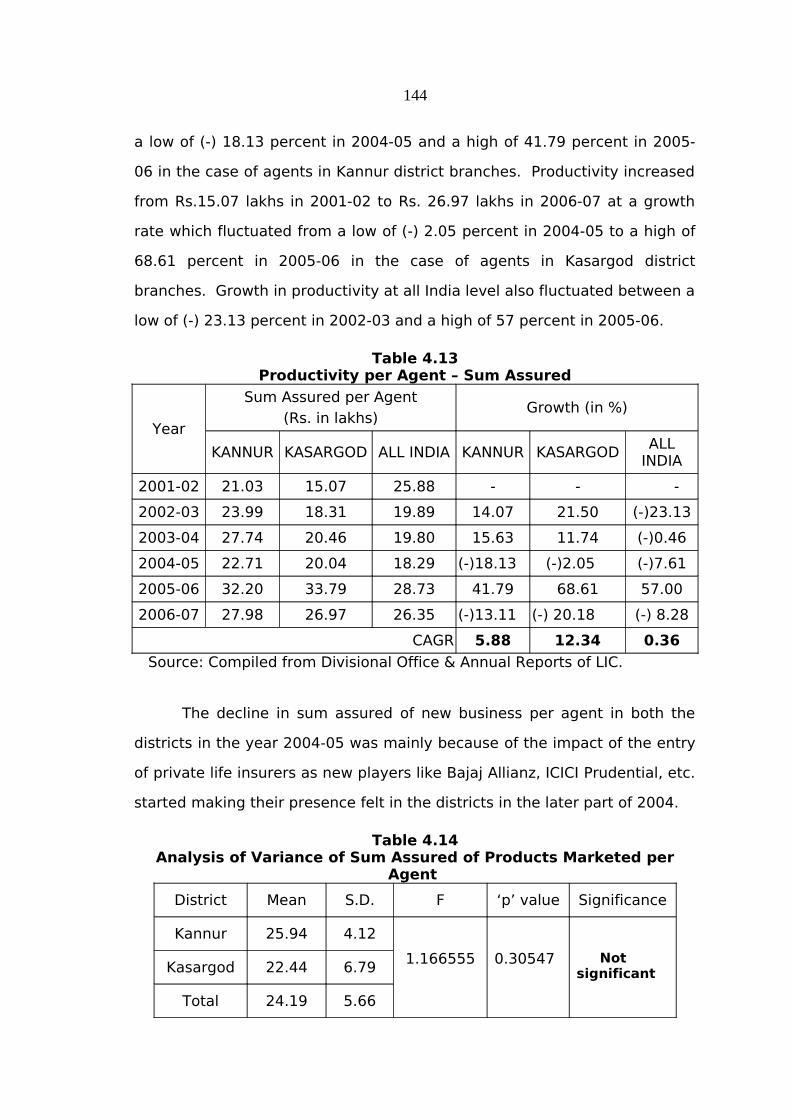

Table 4.13 reveals that productivity per agent in terms of sum

assured of new business has been fluctuating in both the districts under

study from 2001-02 to 2006-07. It increased from Rs. 21.03 lakhs in 2001-

02 to Rs. 27.98 lakhs in 2006-07 at a growth rate which fluctuated between

143

a low of (-) 18.13 percent in 2004-05 and a high of 41.79 percent in 2005-

06 in the case of agents in Kannur district branches. Productivity increased

from Rs.15.07 lakhs in 2001-02 to Rs. 26.97 lakhs in 2006-07 at a growth

rate which fluctuated from a low of (-) 2.05 percent in 2004-05 to a high of

68.61 percent in 2005-06 in the case of agents in Kasargod district

branches. Growth in productivity at all India level also fluctuated between a

low of (-) 23.13 percent in 2002-03 and a high of 57 percent in 2005-06.

Table 4.13Productivity per Agent – Sum Assured

Year

Sum Assured per Agent(Rs. in lakhs)

Growth (in %)

KANNUR KASARGOD ALL INDIA KANNUR KASARGODALL

INDIA

2001-02 21.03 15.07 25.88 - - -

2002-03 23.99 18.31 19.89 14.07 21.50 (-)23.13

2003-04 27.74 20.46 19.80 15.63 11.74 (-)0.46

2004-05 22.71 20.04 18.29 (-)18.13 (-)2.05 (-)7.61

2005-06 32.20 33.79 28.73 41.79 68.61 57.00

2006-07 27.98 26.97 26.35 (-)13.11 (-) 20.18 (-) 8.28

CAGR 5.88 12.34 0.36

Source: Compiled from Divisional Office & Annual Reports of LIC.

The decline in sum assured of new business per agent in both the

districts in the year 2004-05 was mainly because of the impact of the entry

of private life insurers as new players like Bajaj Allianz, ICICI Prudential, etc.

started making their presence felt in the districts in the later part of 2004.

Table 4.14Analysis of Variance of Sum Assured of Products Marketed per

Agent

District Mean S.D. F ‘p’ value Significance

Kannur 25.94 4.12

1.166555 0.30547 Not significantKasargod 22.44 6.79

Total 24.19 5.66

144

Analysis of variance in Table 4.14 reveals no significant difference in

mean sum assured of products marketed per agent in Kasargod and Kannur

districts during the period under study. Even though there is no significant

difference in mean sum assured of products marketed per agent in the two

districts, the CAGR of productivity of agents in Kasargod district branches

shows a heavy growth of 12.34 percent over a period of six years from

2001-02 to 2006-07.

3. First Premium Income per Agent

Agents are motivated and trained to pursue more and more people

to purchase life insurance policies. The performance of agents is highly

linked with the premium they collect as they are paid commission on the

basis of premium collected in a particular year. The first premium income

collected is used to assess the growth in business of insurance companies.

The productivity of agents in terms of FPI is calculated by dividing first

premium collected in a particular year by the number of agents in that year.

Table 4.15First Premium Income per Agent

Year

Premium income per Agent (in Rs.)

Growth (in %)

KANNUR KASARGOD ALL INDIA KANNUR KASARGOD ALL INDIA

2001-02 72,492 55,046 2,15,344 - - -

2002-03 89,456 82,465 1,38,805 23.40 49.81 (-)35.54

2003-04 81,089 87,920 1,25,235 (-) 9.35 6.61 (-)9.78

2004-05 92,077 1,04,917 1,14,705 13.55 19.33 (-)8.41

2005-06 1,20,871 1,49,832 1,53,722 31.27 42.81 34.02

2006-07 2,53,549 2,23,413 4,03,794 109.76 49.11 162.68

CAGR 28.46 32.34 13.40

Source: Compiled from Divisional Office & Annual Reports of LIC.

145

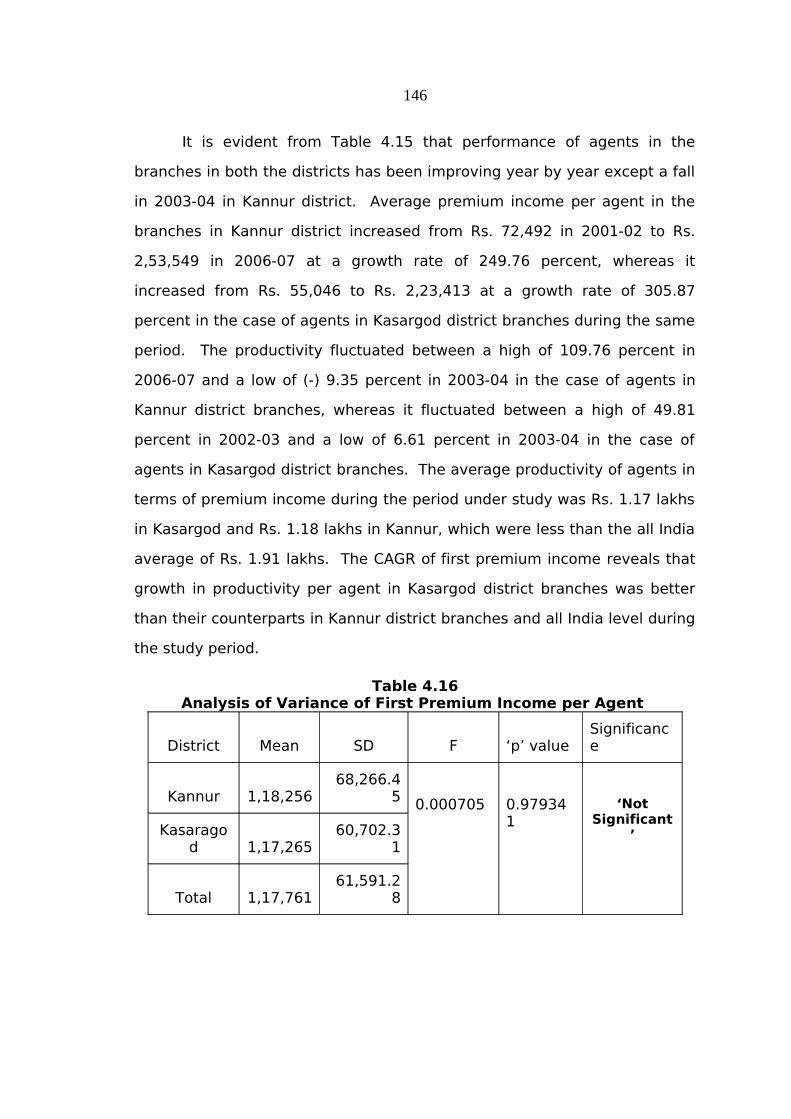

It is evident from Table 4.15 that performance of agents in the

branches in both the districts has been improving year by year except a fall

in 2003-04 in Kannur district. Average premium income per agent in the

branches in Kannur district increased from Rs. 72,492 in 2001-02 to Rs.

2,53,549 in 2006-07 at a growth rate of 249.76 percent, whereas it

increased from Rs. 55,046 to Rs. 2,23,413 at a growth rate of 305.87

percent in the case of agents in Kasargod district branches during the same

period. The productivity fluctuated between a high of 109.76 percent in

2006-07 and a low of (-) 9.35 percent in 2003-04 in the case of agents in

Kannur district branches, whereas it fluctuated between a high of 49.81

percent in 2002-03 and a low of 6.61 percent in 2003-04 in the case of

agents in Kasargod district branches. The average productivity of agents in

terms of premium income during the period under study was Rs. 1.17 lakhs

in Kasargod and Rs. 1.18 lakhs in Kannur, which were less than the all India

average of Rs. 1.91 lakhs. The CAGR of first premium income reveals that

growth in productivity per agent in Kasargod district branches was better

than their counterparts in Kannur district branches and all India level during

the study period.