Download - Levitas presentation

Leaders in Volatility as an Asset Class | Managed Account & Advisory Services.

• Leading Managers of Volatility as an Asset Class.

• Quantitatively Driven Investment Process.

• Advanced Risk Management System.

• Proven Superior Risk Adjusted Returns.

• A Strong 3 Member Investment Management Team combining Market Experience with

Technical Knowledge.

• Based in Sydney and Established in 2013 by the Founder David O’Halloran.

• Servicing Clients in Australia, Singapore and Hong Kong.

ABOUT LEVITAS CAPITAL

Segregated Cash Account Segregated Securities Account

Legend

Cashflow

Investment Management

Capital (Investment)

Capital (Withdrawals)

IB audited Fees Trades

Profit & Loss

Client

Complete Segregation of Investment ownership and management

Securities Flow

IB audited Portfolio Reporting

Trade Execution, Custody & Portfolio Reporting

SECURITY OF CLIENT ASSETS

Clients Managed Account assets are held in the client’s name at Interactive Brokers. Clients have access to daily and monthly position statements for full transparency of their investment. There are no fees to open or close a managed account. There are no set time frames with managed accounts.

FINANCIAL & PERFORMANCE REPORTING

Monthly performance reports received by email and/or mail.

Online access to view live portfolio value and holdings.

Annual financial and performance reports received by email and/or mail.

HOW TO INVEST

Review the Fact Sheet, Information Memorandum & the Financial Services Guide. Available on our website.

Complete the Application and send to Levitas Capital along with required documents. Available on our website.

You will receive deposit instructions to fund your account. Take these to your bank to arrange the transfer. Funds are transferred in AUD into the Bank of America Sydney Branch for benefit of your account.

Your Account

CBOE 6

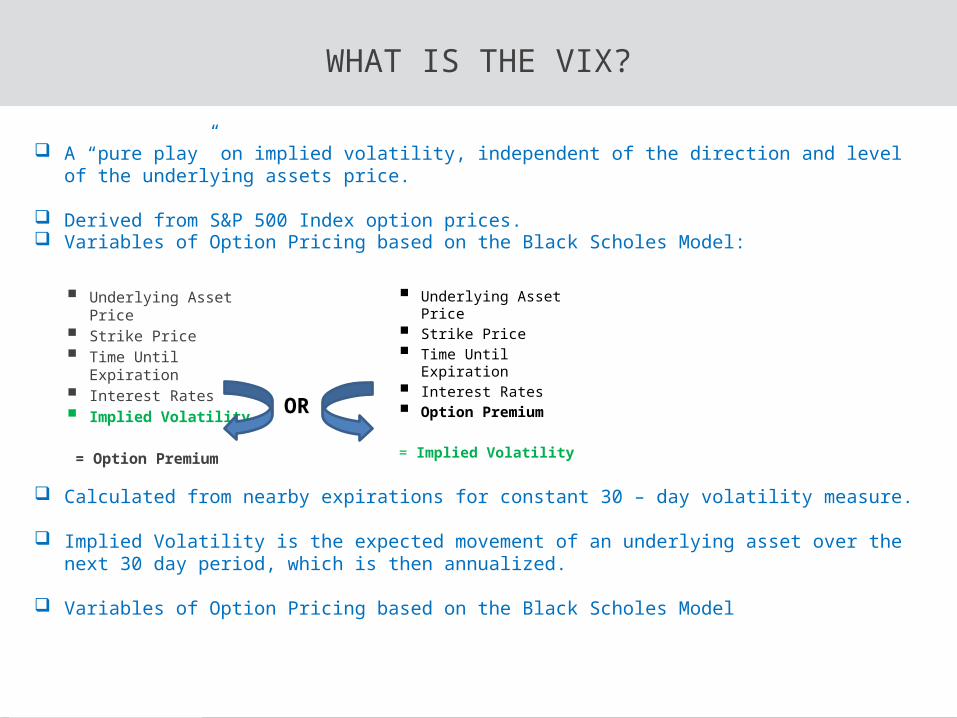

WHAT IS THE VIX?

A “pure play” on implied volatility, independent of the direction and level of the underlying assets price.

Derived from S&P 500 Index option prices.

Underlying Asset Price Strike Price Time Until Expiration Interest Rates Implied Volatility

= Option Premium

Calculated from nearby expirations for constant 30 – day volatility measure.

Implied Volatility is the expected movement of an underlying asset over the next 30 day period, which is then annualized.

Variables of Option Pricing based on the Black Scholes Model

OR

Underlying Asset Price Strike Price Time Until Expiration Interest Rates Option Premium

= Implied Volatility

Variables of Option Pricing based on the Black Scholes Model:

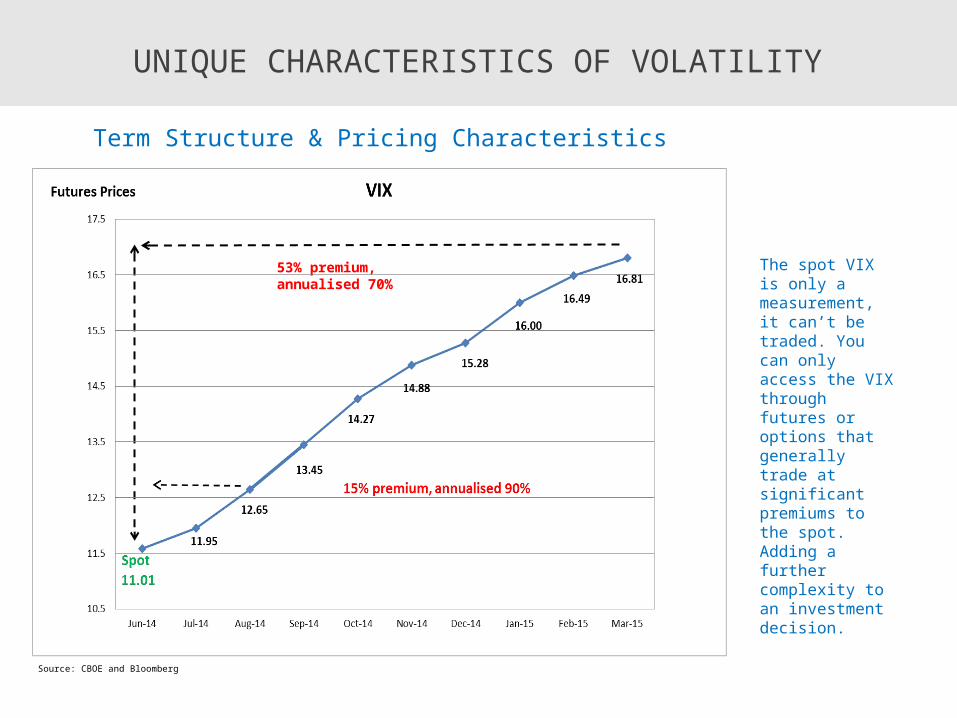

Term Structure & Pricing Characteristics

53% premium, annualised 70%

Source: CBOE and Bloomberg

UNIQUE CHARACTERISTICS OF VOLATILITY

Negatively correlated to equities

The VIX (Implied Volatility) trades at a premium to Realised Volatility, one sign of the “insurance premium” built into the pricing.

Volatility is Mean Reverting. Spikes are quickly followed by moves to the longer term base.

Source: Bloomberg & Levitas Capital

Term Structure & Pricing Characteristics

53% premium, annualised 70%

Source: CBOE and Bloomberg

UNIQUE CHARACTERISTICS OF VOLATILITY

The spot VIX is only a measurement, it can’t be traded. You can only access the VIX through futures or options that generally trade at significant premiums to the spot. Adding a further complexity to an investment decision.

![Computational Materials Science - BCAM · the advanced dynamic formulation developed by Levitas and Pres-ton [17]. All the above studies reviewed so far, have been limited to](https://cdn.vdocuments.us/doc/165x107/5caaa04888c993e6068bdeb2/computational-materials-science-the-advanced-dynamic-formulation-developed.jpg)