Lean LaunchpadClass 4: Distribution Channels

Aaron EdenCreated by Steve Blank

Weekly Topics

» 5/12 – What to Expect» 5/19 – First Pitches» 5/26 – Experiment Day» 6/2 –Value Propositions» 6/9 – Customers, Users, Payers» 6/16 – Distribution Channels (Justin)» 6/23 – Customer Relationships » 6/30 – Revenue Models» 7/7 – Partners» 7/14 – Key Resources & Costs» 7/21 – Lessons Learned Presentations

Agenda

» Team Presentations» Distribution Channels» Mentoring

Presentations

» What were your hypotheses about users and customers? Did you learn anything different?

» Did anything change about Value Proposition? » What do customers say their problems are? How do

they solve this problem(s) today? Does your value proposition solve it? How?

» What was it about your product that made customers interested? excited?

» If B-B, who’s: decision maker, size of budget, what are they spending it on today, how will this buying decision be made?

City Recess

Appstore Analytics

WionTV

Forward Intelligence

Verb Club

How does each customer segment want to be reached?

Through which interaction points?

Channels

10

Test Hypotheses: Channels

11

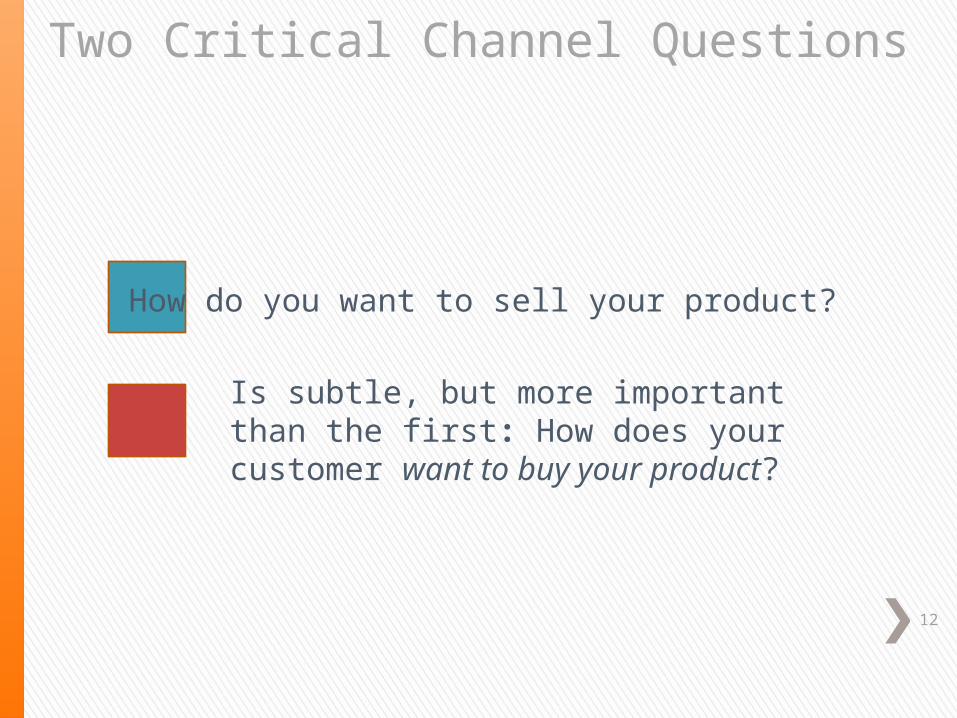

Two Critical Channel Questions

How do you want to sell your product?

Is subtle, but more important than the first: How does your customer want to buy your product?

12

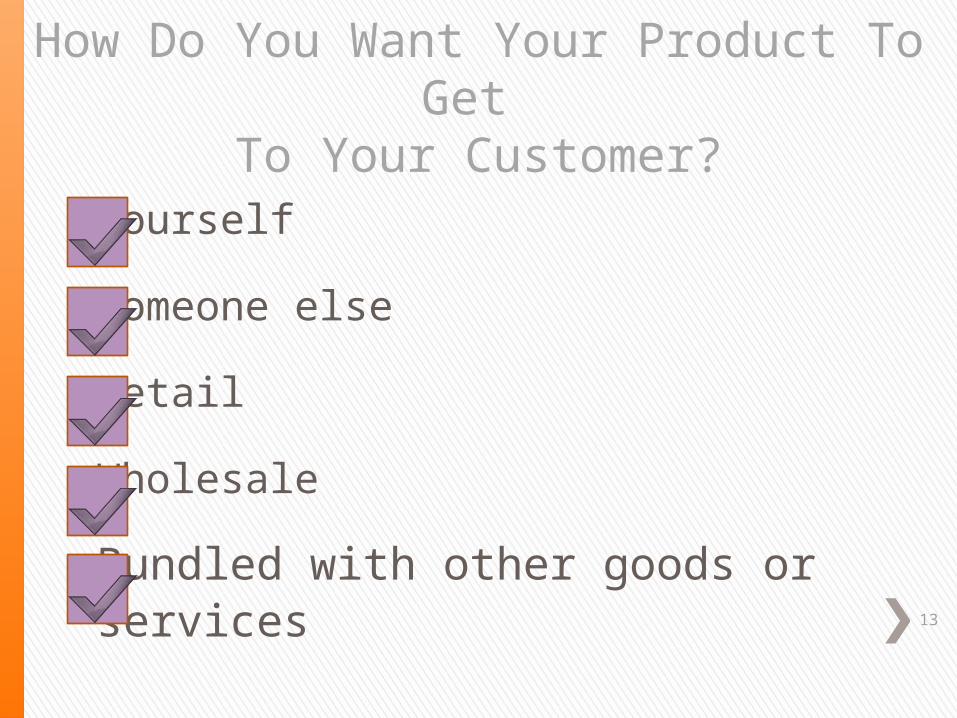

Yourself

Someone else

Retail

Wholesale

Bundled with other goods or services

How Do You Want Your Product To Get To Your Customer?

13

How Does Your Customer Want to Buy Your Product From Your Channel?

Same Day

Delivered and installed

Downloaded

Bundled with other products

As a service

…14

Web Channels

15

Physical Channels

16

Types of Channels

IndirectDirect Licensing

• OEM• VAR• Reseller• Distributor

17

» Some products are embedded in others (OEM)

» Some products are resold by others (VARs)

» Some products are distributed by others» Who’s the customer?

The Channel as a Customer

18

Distribution ComplexityM

ark

eti

ng

Co

mp

lexi

ty

Solution Complexity

Evangelists

Higher

Volu

me

Higher V

alue A

dded

ServiceTechnicians

Global SystemsSystems Integrators

WANsMainframes

TonerWeb, Telesales

Keyboards

Printers

Retail

Desktop PCs

PC Servers

VARs

LANs

Minis

Direct Sales

19

» Commission» Percentage of sales price» Discounted pre-purchase

How Are Channels Compensated?

20

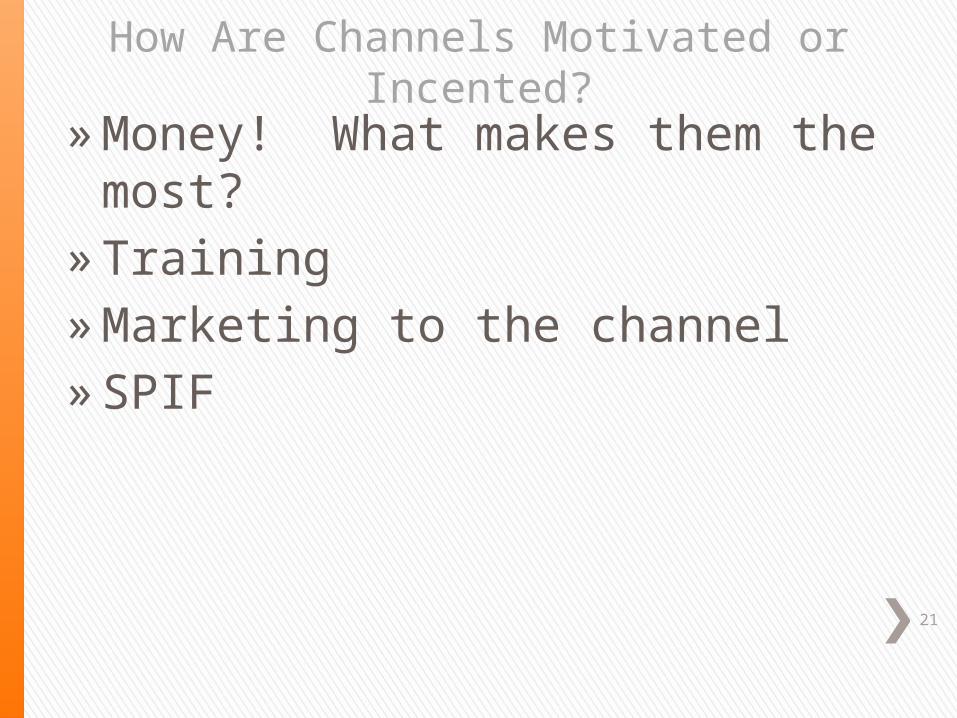

» Money! What makes them the most?» Training» Marketing to the channel» SPIF

How Are Channels Motivated or Incented?

21

Channel Economics: “Direct” Sales

Cost of Goods(Supply Chain)

Profit + SG&A + R&D EU

D

isco

un

ts

En

d C

on

sum

er

RevenueList

Price

Source: Mark Leslie, Stanford GSB

22

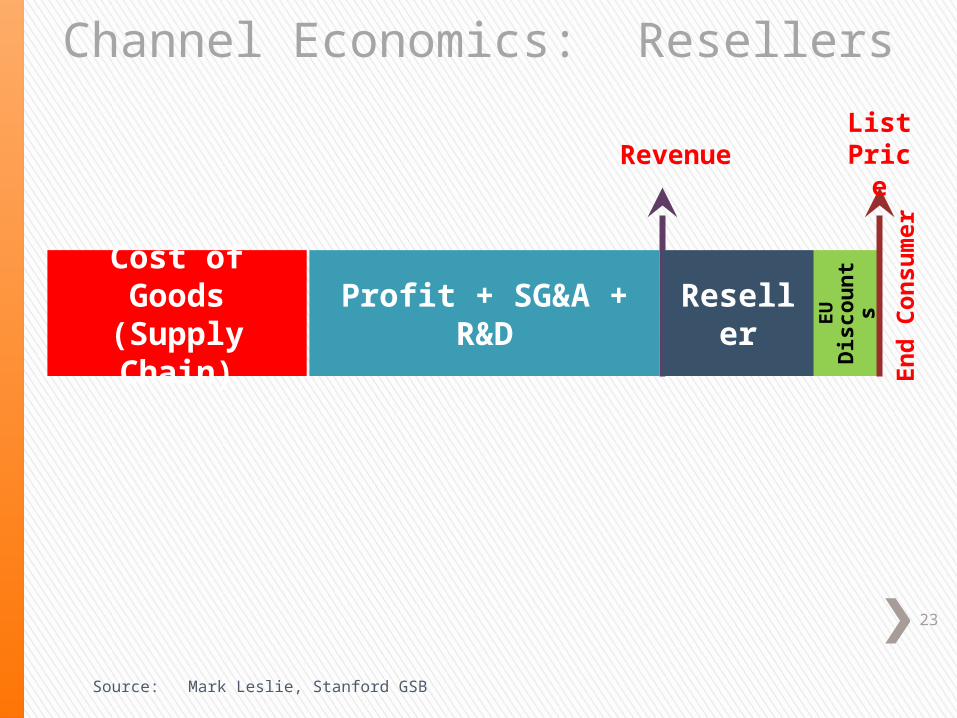

Channel Economics: Resellers

EU

D

isco

un

ts

En

d C

on

sum

er

RevenueList

Price

Source: Mark Leslie, Stanford GSB

Cost of Goods(Supply Chain)

Profit + SG&A + R&D Reseller

23

Channel Economics: Distributors/Resellers

EU

D

isco

un

ts

En

d C

on

sum

er

RevenueList

Price

Source: Mark Leslie, Stanford GSB

Cost of Goods(Supply Chain)

Profit + SG&A + R&D

Dis

trib

uto

r Reseller

24

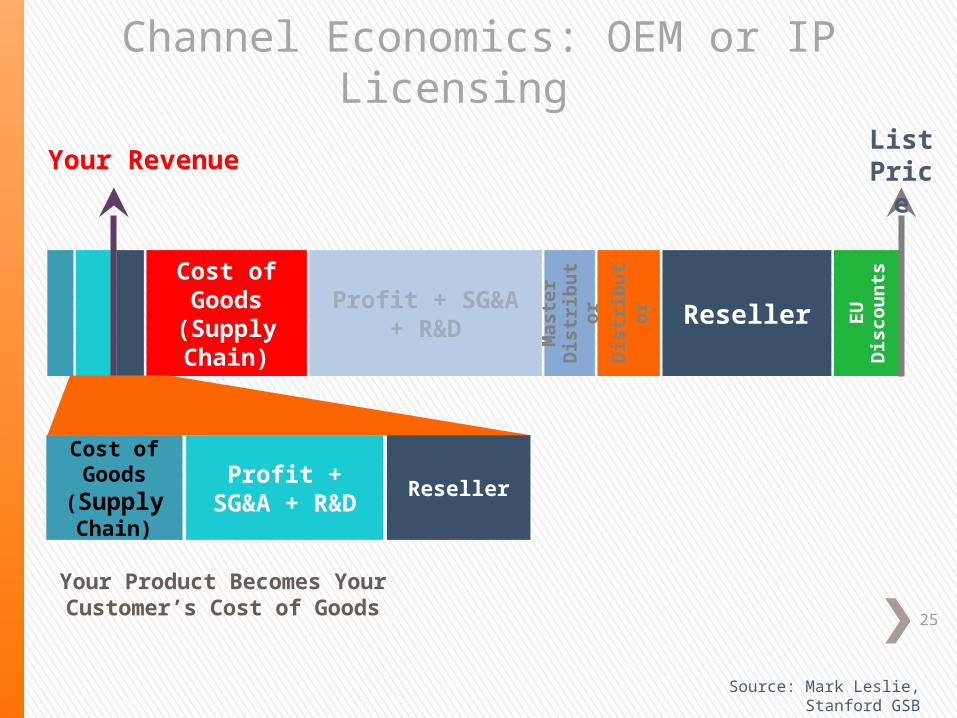

Channel Economics: OEM or IP Licensing

EU

D

isc

ou

nts

Reseller

Dis

trib

uto

r

Mas

ter

Dis

trib

uto

r

Profit + SG&A + R&D

Cost of Goods(Supply Chain)

Your RevenueList

Price

ResellerProfit + SG&A

+ R&D

Cost of Goods

(Supply Chain)

Your Product Becomes Your Customer’s Cost of Goods

Source: Mark Leslie, Stanford GSB

25

Example: Book Publishing

PublisherNational

DistributorPrinter Wholesaler Retailer Customer

26

Book Publishing

PublisherNational

WholesalerDistributor Retailer Customer

• Percent of Retail 35% 15% 10% 40%

$7.00 $3.00 $2.00 $8.00 $20.00

• You get- 35% of retail- the distributor gets 10%- the wholesaler gets 15% - the retailer gets 40%

- less any discount they offer the customer27

Book Publishing Economics

PublisherNational

DistributorWholesaler Retailer Customer

Allowances

Wholesale costs

Bills

Payment guarantees

Payment guarantees

Return rights

Credits

Payments

Credit guarantees

Markup

28

Book Publishing Delivery

PublisherNational

DistributorPrinter Wholesaler Retailer

Prepare film (content)

Receive Schedules Print

orders Bundle

counts Film

Determine allocations

Merchandise titles

Establish identity

Create demand

Prepare galleys

Print and ship

magazines

Deliver orders

Sell magazines

Acknowledge returns

29

» Access to customers changes dramatically

» Logistics related to product complexity» People as products

Nature of Products Impact Channel:Physical or Virtual?

30

Bits vs. Atoms

Channel

PhysicalWeb

Bits

Physical

Product

31

Product and Channel Are Bits

Channel

PhysicalWeb

Bits

Physical

Product

Rapid Agile and Customer Development

Fastest to acquire early customers and scale

32

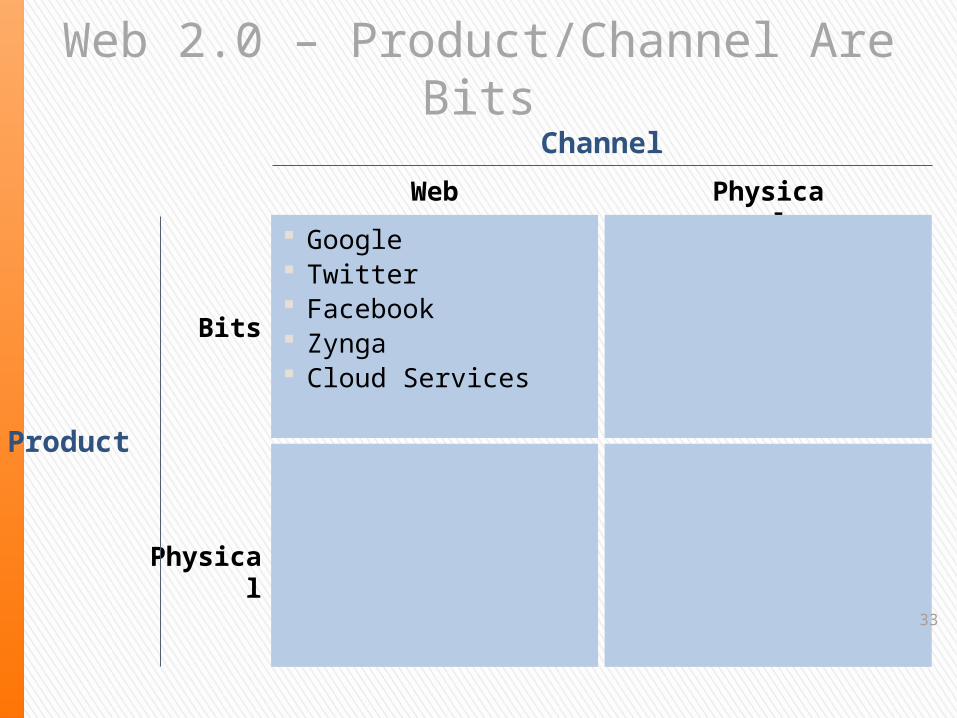

Web 2.0 – Product/Channel Are Bits

Channel

PhysicalWeb

Bits

Physical

Product

Google Twitter Facebook Zynga Cloud Services

33

Product Is Bits, but Channel Is People

Channel

PhysicalWeb

Bits

Physical

Product

Rapid Agile and Customer Development

Fastest to acquire early customers and scale

Rapid Agile and Customer development

Traditional sales channel May require installation

34

Traditional Enterprise Software

Channel

PhysicalWeb

Bits

Physical

Product

Google Twitter Facebook Zynga Cloud Services

Microsoft SAP Oracle

35

Physical Products Sold Over the Web

Channel

PhysicalWeb

Rapid Agile and Customer development

Traditional sales channel

May require installation

Rapid Agile and Customer development

Fastest to acquire early customers and scale

Rapid Customer development

Logistics, shipping and manufacturing critical

Customer service

Bits

Physical

Product

36

Killing Traditional Storefronts

Channel

PhysicalWeb

Bits

Physical

Product

Google Twitter Facebook Zynga Cloud Services

Microsoft SAP Oracle

ZapposAmazonCafepressNetflixConsumer electronics 37

The Factories May Be in China

Channel

PhysicalWeb

Rapid Agile and Customer development

Traditional sales channel May require installation

Rapid Agile and Customer development

Fastest to acquire early customers and scale

Rapid Customer development

Logistics, shipping and manufacturing critical

Customer service

Bits

Physical

Product Longer customer

feedback cycle May require large capital

requirements for scale

38

We Still Make Things that Need Salespeople

Channel

PhysicalWeb

Bits

Physical

Product

Google Twitter Facebook Zynga Cloud Services

Microsoft SAP Oracle

ZapposAmazonCafepressNetflixConsumer electronics

Cars Solar panels Wind turbines Bookstores Consumer electronics

39

Homework

» Talk to 10-15 potential channel partners + (Salesmen, OEM’s distributors, etc.)

» What were your hypotheses about who/what your channel would be? Did you learn anything different?

» Did anything change about Value Proposition? » Update your Google Group with Business Model Canvas» Draw your channel diagram

» Summarized in a 5 Minute Presentation

» Read» Startup Owner’s Manual pages :227-256, 332-342

40

Appendix

Real Examples 41

implantable drug infusion pumpswith remote physician control

for chronic pain patients at home

“the right dose at the right time and place”

Christian Gutierrez (EL), Ellis Meng (PI), Carol Christopher (IM), Tuan Hoang (FE)

42

KOLs

Foundations

Chronic Pain v3 FS Team

Advocacy Groups

OEMs

Wireless Developers

Trade showsFormulary Acceptance

FDA

IP

Proprietary knowledge

Human Resources

Product Dev Costs

Manufacturing Costs

Marketing Costs FDA/Clinical Trials

Faster relief

Efficient patient management and Dosing flexibility

Access to high-value therapies and pharmacoeconomics

Reduce length of hospital stays andpharmacoeconomics

Training

Clinical data

Support

Hospitals

Pain clinics

Unit sales

Support Services

Patients

Clinicians

Institutions

Payors

43

KOLs

Foundations

FS Team

Advocacy Groups

OEMs

Wireless Developers

Trade shows

Formulary Acceptance

FDA

IP

Proprietary knowledge

Human Resources

Product Dev Costs

Manufacturing Costs

Marketing Costs FDA/Clinical Trials

Faster relief

Efficient patient management and Dosing flexibility

Access to high-value therapies and pharmacoeconomics

pharmacoeconomics

Training

Clinical data

Support

Hospitals

Pain clinics

Unit sales

Support Services

Patients

Clinicians

Institutions

Payors

Electronic health record providers

CMS (Medicare)

Bundled kits Electronic records

Chronic Pain v4

44

Getting Out

Clinicians

Institutions/patients

Regulatory

Entrepreneurs/Industry

» Dr. Stan Louie, Drug Formulation Expert (USC Pharmacy)» Dr. Giovanni Cucchiaro, Anesthesiologist (CHLA)

» Dr. Diana Hull, Physician (Group Health in Washington state, formerly at Kaiser California)

» Thomas Hsu, Insurance Specialist (Network Medical Management; a California ICA)

» Two chronic pain patients ˃ Pump user and creator of support forum˃ User of oral narcotics and patches

» Dr. Frances Richmond (Director Regulatory Science Program, USC)

» Richard Hull (formerly at company selling Lapband)

45

Product Flow/Channel

Electronic Health

Records

.

Patients

Electronic Records

Fluid Synchrony

Support Services

Pump + Controller

Hospitals(AnesthesiologistsNeurosurgeons)

Pain Clinic(AnesthesiologistsNeurosurgeons)

Bundled Kits

Partners/OEMS

46

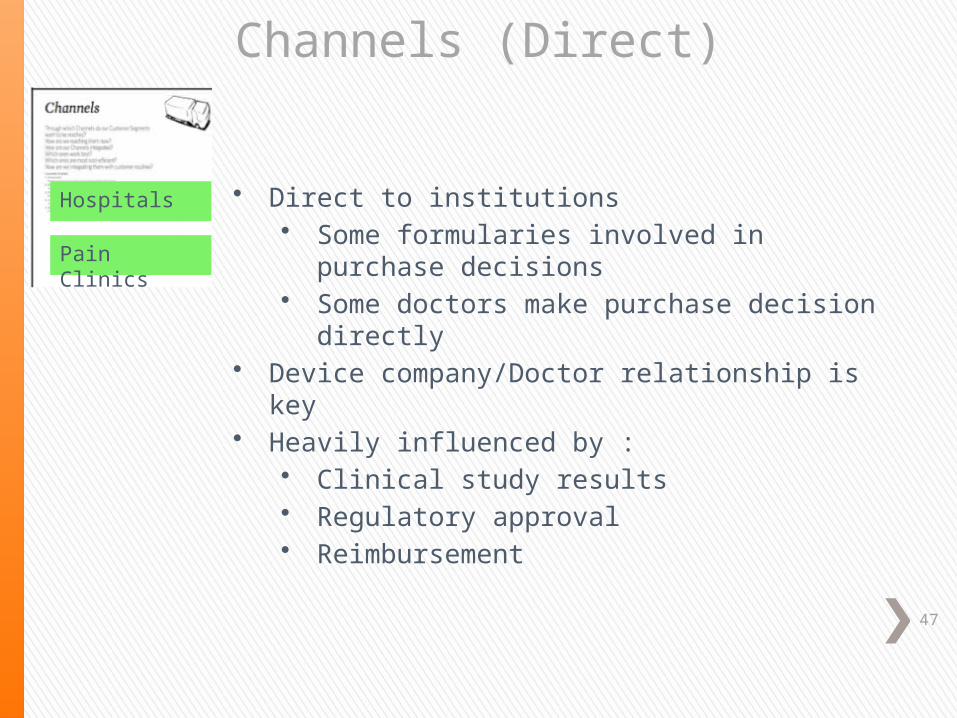

Channels (Direct)

Hospitals

Pain Clinics

• Direct to institutions• Some formularies involved in purchase decisions• Some doctors make purchase decision directly

• Device company/Doctor relationship is key • Heavily influenced by :

• Clinical study results • Regulatory approval• Reimbursement

47

Patient Care Flow (Now)

Fluid Synchrony

Bundled Kits

Partners/OEMS

Support Services

Pump + Controller

Hospitals(AnesthesiologistsNeurosurgeons)

Pain Clinic(AnesthesiologistsNeurosurgeons)

Surgery/Rx/reprogramming

Scheduled follow-up

Patient Discharged

Trial period/ Home setting

Weeks/months Key factors: Reimbursement , state regulations

48

Patient Care Flow (Proposed)

Electronic Health

Records

.

Patient Discharged

Trial period/ Home setting

Weeks/monthsDays

Actionable feedbackto doctors/institutions

E-prescription / closing loop

Scheduled follow-up

Surgery/Rx/reprogramming

Electronic Records

Fluid Synchrony

Support Services

Pump + Controller

Hospitals(AnesthesiologistsNeurosurgeons)

Pain Clinic(AnesthesiologistsNeurosurgeons)

Key factors: Reimbursement , state regulations

Bundled Kits

Partners/OEMS

49

Regulatory Considerations

PMA 510K

Trial size 100’s of patients 20-100

Costs Up to $100,000 per patient

$10-50 MM $1-10 MM

Time ~ 3-4 yrs + post approval follow-on

~ 2-3 yrs

• PMA approval with grouping of FDA approved drugs.• Clinical trials results used to obtain CMS (Medicare) approval• 510K restricts technology to predicate devices

• Can be more difficult to market against incumbents• European CE mark is easier to attain (safety and performance only)

50

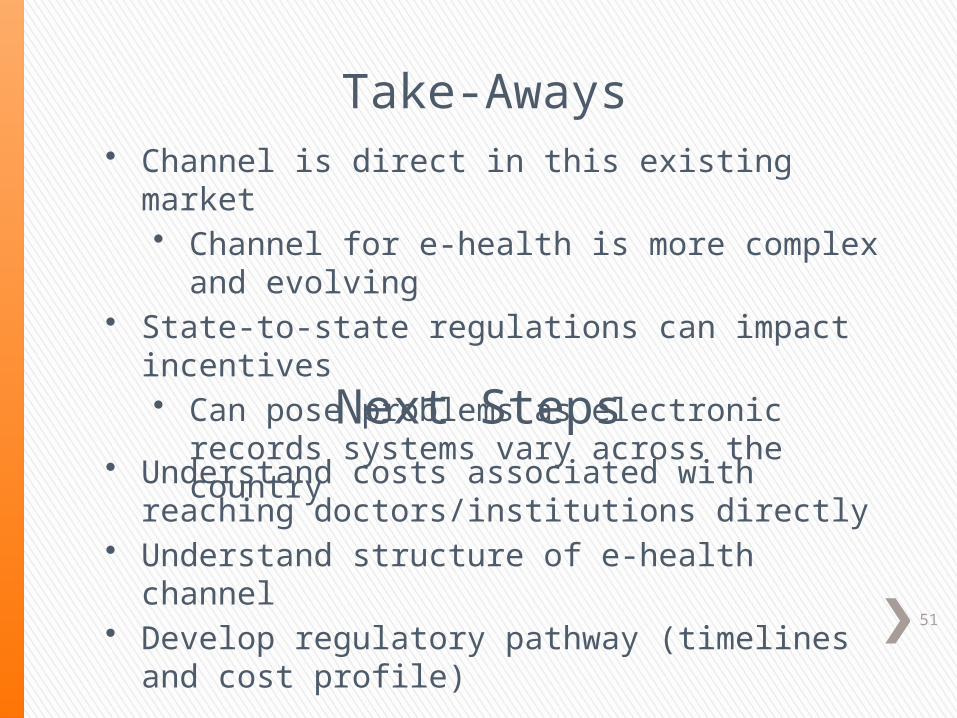

Take-Aways• Channel is direct in this existing market

• Channel for e-health is more complex and evolving• State-to-state regulations can impact incentives

• Can pose problems as electronic records systems vary across the country

Next Steps• Understand costs associated with reaching

doctors/institutions directly• Understand structure of e-health channel• Develop regulatory pathway (timelines and cost profile)

51

Advanced Chemistry for Pharmaceutical Progress

Team: Kiel Neumann (EL)

Stephen DiMagno (PI)

Allan Green (Mentor)52

PET is a non-invasive medical diagnostic technique for cardiac, brain, and tumor imaging

GFP technology makes new (unknown) and known (but clinically inaccessible) [18F]-labeled radiotracers readily available

Fast, multiplatform, high efficiency synthesis of these fleeting, precious agents.

Initial target indications: pediatric neuroblastoma, Parkinson’s disease.

53

The Business Model Canvas

cGMP manufacturerRadiopharmaciesNuclear Medicine and Radiology departments

Pharmaceutical development companies

Contract cGMP precursor manufactureSalary, RentsClinical trials

Sales of intermediates

Technology license

Product license (royalty)

SOPs for precursors and drugsRecruit clinical sitesIn vivo animal studiesDevelop regulatory plan for pre IND meetingID cGMP CROFund-raising

IPPoP data

IPPoP dataRegulatory planUnderstanding of the regulatory process

Accessibility (RCY)PuritySpeedPET/SPECTMultiplatformSensitivity (nca)Specific compounds

General methodology for

adding fluorine to lead compounds of

interest

Technical Assistance (Image Atlas)FDA regulatory support

Technical assistance

Direct sales of precursor

R&D and clinical studies presented in journals and meetingsSales of precursor through global finished pharmaceutical distributor

Radiopharmacies

Equipment producers

Prescribing physicians

Radiologist who perform studies

Drug developers

Radiologists

54

Getting out of the building

1) Radiologists and Nuclear Medicine Physicians2) Radiopharmacy companies (Cardinal Health, Siemens, GE Healthcare, IBA,

AAA)3) Equipment manufacturers (GE, Philips, IBA, Advion)4) cGMP manufacturers

1) Pharmaceutical companies2) Radiologists and Nuclear Medicine Physicians

55

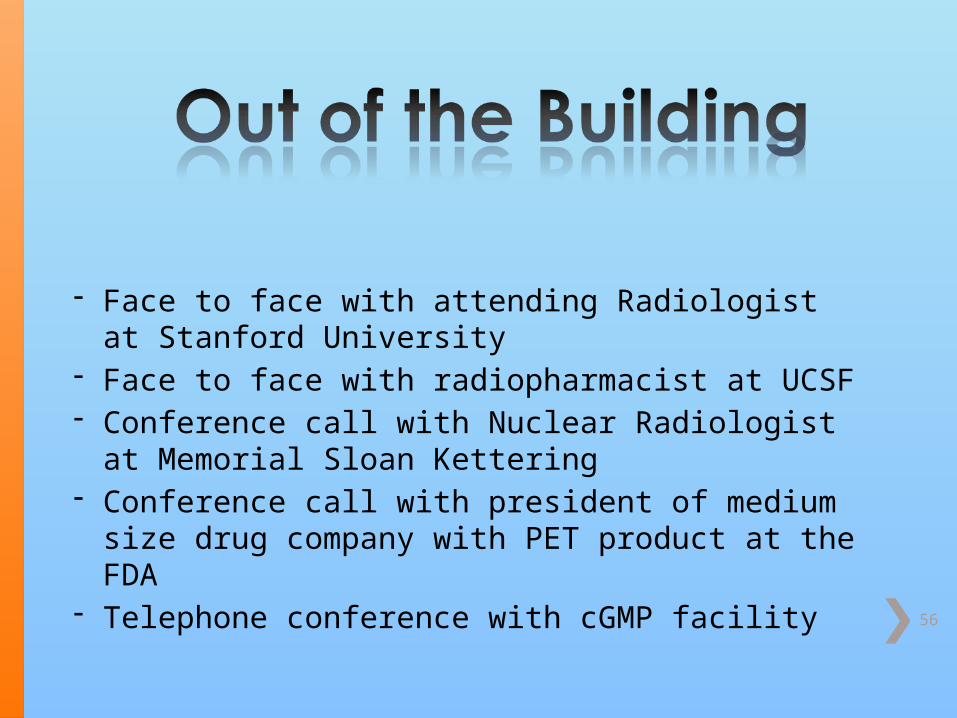

- Face to face with attending Radiologist at Stanford University

- Face to face with radiopharmacist at UCSF- Conference call with Nuclear Radiologist at

Memorial Sloan Kettering - Conference call with president of medium size drug

company with PET product at the FDA- Telephone conference with cGMP facility 56

- Immediate need for our product- Currently used SPECT product for neuroblastoma is limited by

absence of correlative CT data- Our lead PET agent would provide more information on existing

imaging equipment base- Two customers offered to participate in clinical trials- Potential for further development of other tracers identified in

interviews- Actual need for the general procedure- Allow access to previously unknown tracers

57

Face to Face meeting with president of small radiopharmaceutical company Face to face with a clinician at Memorial Sloan-Kettering Face to face with Global Production Manager of Molecular imaging for one of

world’s largest radiopharmaceutical companies OncoKinib collaboration between Geurbet, OncoDesign, and Ariana

pharmaceuticals Face to face meeting with head of R & D and International Production

Manager from Linz, Austria Eckert and Zeigler – German PET modular synthesis provider Face to face meeting with Executive Director and CEO of Scott Tech Center in

Omaha, NE Introductory teleconference to CEO of Innovation Accelerator 58

Significant Interest in our technology Radiopharmacies want GMP product

No interest in GMP reagent preparation Third-party manufacturers would use our developed synthetic pathways Internal competition with one world radiopharmaceutical leader

Best to approach one of other two world leaders

Scott Tech Center Willing to offer free advice on startup strategy Provided introduction to Innovation Accelerator Offered introduction to Director of Venture Technology of one of world’s leading

radiopharmaceutical companies 59

The Business Model Canvas

Sales of intermediates

Technology license

Product license (royalty)

Contract cGMP precursor manufactureSalary, RentsClinical trials

Technical Assistance (Image Atlas)FDA regulatory support

Technical assistance

Direct sales of precursor

R&D and clinical studies presented in journals and meetings

Sales of precursor through global finished pharmaceutical distributor

Accessibility (RCY)PuritySpeedPET/SPECTMultiplatformSensitivity (nca)Specific compounds

General methodology for

adding fluorine to lead compounds of

interest

SOPs for precursors and drugsRecruit clinical sitesIn vivo animal studiesDevelop regulatory plan for pre IND meetingID cGMP CROFund-raising

IPPoP data

IPPoP dataRegulatory planUnderstanding of the regulatory process

cGMP manufacturerRadiopharmaciesNuclear Medicine and Radiology departments

Pharmaceutical development companies

Radiopharmacies

Equipment producers

Prescribing physicians

Radiologist who perform studies

Drug developers

Radiologists

60

Reagents

• F-dopa iodonium intermediate• F-dopamine iodonium intermediate

GMP Cassette

or Components

•ABX•Eckert & Ziegler•GE MX module for TracerLab•Siemens Explora

GMP Complia

nt Synthesi

zer

•TracerLab/ GE•Eckert & Ziegler•Siemens Explora•Neoprobe•Synthra

PET Radiopharmacy distribu

tor

•Siemens PETNet•GE Amersham•Cardinal Health•AAA• Iason

We provide accessibility

Could license precursor synthesis for incorporation in modules

Require GMP precursor (or cassette) to develop our product with their synthesizer

Only want GMP precursor in modules without development

61

Conference call with top 40 Fortune 500 chemical distribution company Open to cGMP production of our potentially proprietary precursors Interested in developing a general “plug-and-play” cassette

Would allow implementation of our methodology and precursors for any radiochemistry module

Important for FDA compliant production of any drug used in patient diagnostics Face to face meeting with Director of Business Development of a leading drug

discovery outsourcing company Discussed preclinical studies and contract manufacturing of proprietary

intermediates Face to face with former Director of Chemistry of major pharmaceutical

company Significant interest in general methodology application to proprietary

compound syntheses62

» Initially seeking to market method technology-too diffuse, but many opportunities (i.e. product-driven opportunities more than general technology-driven)

» Need to identify specific imaging product opportunities» Validated hypothesis for immediate need of tracers» Raised question on identity of lead compound pipeline

for Parkinson’s disease» Recruited two potential partners for clinical trials

63

Approximately 2.2 million procedures in the US.

Drug costs range from $700 (on-patent) to ~$150 (generic FDG)

US sales of radiopharmaceuticals for PET and SPECT $1.2 billion

US sales expected to grow to $6 billion by 2018

Global numbers approximately 2x

Source: Bio-Tech Systems Report #330; data for 2010.64

2500 installed PET scannersPET radiopharmacies cover the entire US marketRadiopharmacies have an interest in proprietary agents as a basis of competition in their market.

65

Neuroblastoma

Prevalence: about 6000 US cases about 1000 new cases per year

Subjects receive 3-6 images/yearto follow response to therapeutic protocols

World market at U.S. x 2 gives potential of 40,000-70,000 scans/year

Drug costs $500/per gives ~$20 - $35 M

Parkinson’s Disease

DatSCAN sales in Europe ~$100 M

The world's highest recorded prevalence of Parkinson's Disease of any region is in Nebraska, with 329.3 people per 100,000 population

US – 600,000 patients 1 scan per year @ $500 = $300 M

66