Analysts who prepared this report are registered as research analysts in Korea but not in any other jurisdiction, including the U.S. PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END OF REPORT.

KMI Wire and Cable (KBLI IJ)

Bright prospects to drive valuation re-rating

Although shares of KMI Wire and Cable (KBLI/Not Rated) have jumped >50% YTD, we

believe the stock is still attractive. Key investment points include: 1) growing demand

for aluminum power transmission cables; 2) its fewer competitors (Voksel Electric [VOKS

IJ/Not Rated] is KBLI’s main competitor in supplying aluminum cables to Indonesia’s

state-owned electricity company, Perusahaan Listrik Negara [PLN]); 3) stable margin

delivery owing to the impact of natural hedging; and 4) expectations for a valuation re-

rating.

New facilities to start producing cables for PLN in 2017-18

For FY16, KBLI’s annual capacity stood at 42,000 tonnes (16,000 tonnes for aluminum;

26,000 tonnes for copper). This year, KBLI will start producing high-voltage

underground copper (HVUGC) cables after adding 3,000 tonnes of copper cable capacity

(for high- and medium-voltage cables). In addition, KBLI will also begin construction on

15,000 tonnes of aluminum cable capacity in 2H17, as management expects aluminum

cable utilization to reach 94% (the effective maximum level) this year. The additional

15,000 tonnes of capacity are expected to come online in 2018.

Impressive FY16F stokes expectations for better performance going forward

KBLI’s management estimates that, for FY16, top line reached around IDR2.8tr (+7.6%

YoY). Meanwhile, net profit is projected at IDR300bn (excluding a tax revaluation impact

of roughly IDR30bn), more than doubling on a YoY basis. In our view, KBLI’s strong

performance was supported by a more than twofold increase in PLN’s revenue

contribution (to roughly 39%) from the FY14 level.

KBLI expects the revenue contribution of transmission cables to expand during 2017-19,

in line with increasing demand from PLN for LVAL-ACCC and LVAL-ACSR transmission

cables. LVAL-ACCC is a specialty cable that: 1) can carry two times more current than

LVAL-ACSR; 2) reduces the probability of cable sag; and 3) is able to withstand the

higher temperatures generated by peak-load power (on which PLN has been relying

recently). According to KBLI’s management, the company boasts significant competitive

edges over competitors with regard to LVAL-ACCC, which is difficult to produce.

Notably, KBLI forecasts that revenue from PLN projects will reach around 51% of total

revenue by 2019, which we think will have a positive impact on earnings.

Valuation remains cheap; Re-rating expected

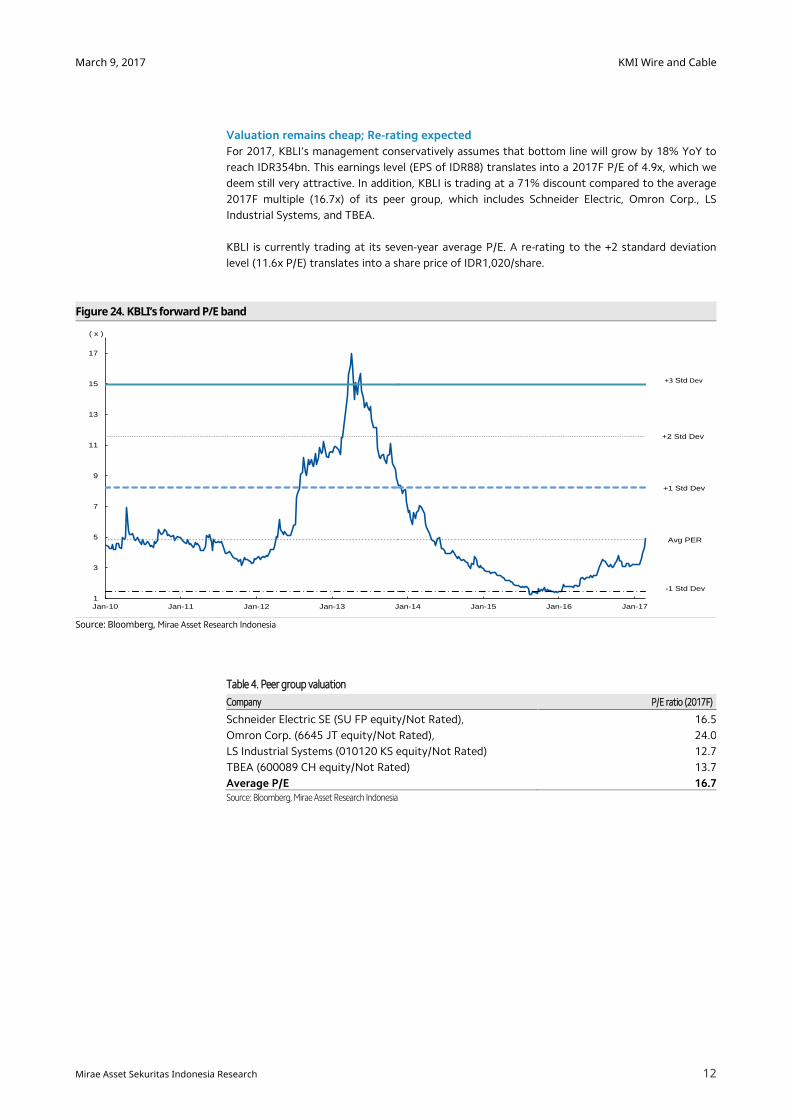

For 2017, KBLI’s management conservatively assumes that bottom line will grow by

18% YoY to reach IDR354bn. This earnings level (EPS of IDR88) translates into a 2017F

P/E of 4.9x, which we deem still very attractive. In addition, KBLI is trading at a 71%

discount compared to the average 2017F multiple (16.7x) of its peer group, which

includes Schneider Electric SE (SU FP equity/Not Rated), Omron Corp. (6645 JT Equity),

LS Industrial Systems (010120 KS equity), and TBEA (600089 CH equity).

KBLI is currently trading at its seven-year average P/E. A re-rating to the +2 standard

deviation level (11.6x P/E) translates into a share price of IDR1,020/share.

Cable

Company Report March 9, 2017

(Recommendation) Not Rated

Target Price (12M, IDR) -

Share Price (3/8/17, IDR) 434

Expected Return -

Consensus OP (17F, IDRtr) N/A

EPS Growth (17F, %) N/A P/E (17F, x) N/A Industry P/E (17F, x) 17.4 Benchmark P/E (17F, x) 15.6 Market Cap (IDRbn) 1,739.1

Shares Outstanding (mn) 4,007.2 Free Float (mn) 2,010.5 Institutional Ownership (%) 58.5 Beta (Adjusted, 24M) 1.2 52-Week Low (IDR) 139 52-Week High (IDR) 460

(%) 1M 6M 12M Absolute 55.0 59.6 199.3 Relative 54.4 59.1 187.2

PT. Mirae Asset Sekuritas Indonesia Miscellaneous Industry Christine Natasya +62-21-515-1140 [email protected]

FY (Dec.) 2010 2011 2012 2013 2014 2015

Revenue (IDRbn) 1,228.1 1,841.9 2,273.2 2,572.4 2,384.1 2,662.0 Gross Profit (IDRbn) 135.0 168.8 276.6 276.8 211.5 285.3 Operating Profit (IDRbn) 64.6 97.1 186.9 175.9 118.1 171.0 Net Profit (IDRbn) 48.3 63.7 125.2 73.5 72.0 115.4 EPS (IDR) 12.1 15.9 31.2 18.4 18.0 28.8 BPS (IDR) 163.7 179.7 210.9 221.3 231.2 256.4 P/E (x) 6.6 6.5 6.0 7.7 7.7 4.1 P/B (x) 0.5 0.6 0.9 0.6 0.6 0.5 ROE (%) 10.9 9.3 16.0 8.5 7.9 11.8 ROA (%) 6.7 6.2 11.2 5.9 5.4 8.0 Note: NP refers to net profit attributable to controlling interests Source: Company data, Mirae Asset Sekuritas Indonesia Research estimates

40

90

140

190

240

290

340

3/1

6

4/1

6

5/1

6

6/1

6

7/1

6

8/1

6

9/1

6

10

/16

11

/16

12

/16

1/1

7

2/1

7

3/1

7

JCI KBLI(D-1yr=100)

KMI Wire and Cable

2

March 9, 2017

Mirae Asset Sekuritas Indonesia Research

Efforts to increase access to electricity to benefit cable companies

The relatively low level of electrification in Indonesia is largely due to a power generation

shortage. In June 2016, the Ministry of Energy and Mineral Resources released its 2016–25

Electricity Supply Business Plan (Rencana Umum Penyediaan Tenaga Listrik; RUPTL), which

includes concrete steps to address this issue.

According to the plan, the Indonesian government aims to raise Indonesia’s electrification ratio

from 88.3% in 2015 to 99.7% in 2025, focusing heavily on rural areas. The plan indicates that, at

minimum, power plants with capacity of 80.5GW will need to be constructed by 2025 in order to

achieve that level of electrification. At present, PLN plans to add 18.2GW, and independent

power producers (IPPs) are projected to add 45.7GW. Arrangements for the remaining 16.6GW of

capacity have yet to be firmed up.

Figure 1. Government’s road map to 80.5GW of new capacity

Source: RUPTL, Mirae Asset Research Indonesia

Construction of the new power plants will require a minimum investment of around USD31.9bn

(roughly IDR430tr) from PLN, and approximately USD78.2bn from IPPs. As such, over the next 10

years, the private sector will play a greater role than ever before in the development of the

Indonesian power sector.

In addition, the mega project requires the construction of transmission networks, main

substations, and distribution networks, as well as an estimated 300,000km of aluminum

conductors. Therefore, PLN will also need to invest around USD43.7bn (IDR590tr) to expand its

transmission and distribution networks, which we believe will benefit aluminum cable producers

such as VOKS and KBLI.

Figure 2. Distribution of power plants and transmission networks

Source: PLN, Mirae Asset Sekuritas Indonesia

80,538

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2016 F 2017 F 2018 F 2019 F 2020 F 2021 F 2022 F 2023 F 2024 F 2025 F

MW

KMI Wire and Cable

3

March 9, 2017

Mirae Asset Sekuritas Indonesia Research

Cable companies producing transmission cables due to high demand from PLN

Since RUPTL’s first phase—35GW in new capacity by 2025—calls for investment exceeding

IDR1,000tr, we believe cable companies, such as VOKS and KBLI, are set to enjoy significant

boosts. The 35GW project requires the construction of power generators, transmission networks,

main substations, and distribution networks, as well as an estimated 300,000km of aluminum

conductors.

Notably, VOKS and KBLI are two of the largest IDX-listed aluminum cable players providing supply

to PLN. In terms of revenue, we estimate that KBLI is the second-largest player in the industry. In

the low-voltage copper (LVCU) cable segment, Supreme Cable Manufacturing & Commerce (SCCO

IJ; Not Rated) is KBLI’s chief rival. Generally speaking, LVCU cables (around 52.6% of KBLI’s total

revenue) are sold to private companies operating in the building works, property, mining, and

industrial sectors.

Through 2016, KBLI’s revenue contribution from the private sector (including LVCU, MVCU, LVAL,

etc.) was around 59.2%. Meanwhile, PLN’s contribution to KBLI’s total revenue was only 38.5%. In

the future, management expects the contribution of the private sector to shrink gradually as

revenue from PLN steadily increases due to strong demand stemming from the utility’s role as

the direct link to the end-consumer. (For further details, please read Perpres Indonesia No. 14/2017: https://goo.gl/Qy9f8M.) KBLI expects PLN’s revenue contribution to climb to 51% by

2019.

Figure 3. Low-voltage copper cable 1KV (supplied to private sector companies)

Source: Mirae Asset Research Indonesia

Figure 4. KBLI’s revenue breakdown (2016F) Figure 5. KBLI’s revenue breakdown (2016-2019F)

Source: Company data, Mirae Asset Research Indonesia

Source: Company data, Mirae Asset Research Indonesia

59%

38.5%

2%

Sales to private sector Sales to state owned (PLN) Export sales

19%

18%17%

16%

15%

17%21% 23%

5%10% 10% 12%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2016F 2017F 2018F 2019F

Export PLN - Unit Bisnis 3 PLN - Transmisi PLN- Distribusi Freemarket Distributor

51%

39%

KMI Wire and Cable

4

March 9, 2017

Mirae Asset Sekuritas Indonesia Research

As of 9M16, VOKS’ revenue exposure to PLN stood at 26%, lower than the 41% figure recorded

by KBLI. Yet, on an absolute basis, VOKS’ revenue from PLN was slightly higher than KBLI’s

(IDR376bn vs. IDR326bn). We believe that, for both companies, production capacity will

determine future revenue from PLN.

Figure 6. VOKS’ revenue from PLN vs. others (as of 9M16) Figure 7. KBLI’s revenue from PLN vs. others (as of 9M16)

Source: Company data, Mirae Asset Research Indonesia

Source: Company data, Mirae Asset Research Indonesia

Figure 8. Estimates of PLN’s contribution to KBLI’s total revenue

Source: Company data, Mirae Asset Research Indonesia

326

-

50

100

150

200

250

300

350

400

450

500

PLN Others

IDRbn

376

-

100

200

300

400

500

600

700

800

900

1,000

WSKT IJ PLN Others

IDRbn

15%23%

39% 45% 49% 51%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2014 2015 2016 F 2017 F 2018 F 2019 F

Others PLN

KMI Wire and Cable

5

March 9, 2017

Mirae Asset Sekuritas Indonesia Research

Margins should remain stable even if aluminum and copper prices rise

We believe KBLI’s margin stability has historically been supported by two key factors: 1) lower

aluminum and copper prices; and 2) a natural hedge built into KBLI’s business structure (i.e.,

selling price are pegged to current commodity prices). Going forward, we believe KBLI will be able

to maintain its margins given that that it can pass on higher raw material prices to customers.

Currently, three of KBLI’s cable divisions provide supply to PLN—the distribution, transmission

and unit businesses. KBLI expects the transmission cable business to become the biggest source

of revenue, with its contribution growing from 15% in 2016F to 23% in 2019F on the back of high

demand from PLN (stemming from power plant construction activities).

Figure 9. KBLI’s expected higher revenue contribution (%) from PLN mainly comes from transmission and unit businesses (2016-2019F)

Source: Company data, Mirae Asset Research Indonesia

The distribution segment mainly sells medium-voltage aluminum (MVAL) cables to PLN

(around 14% revenue contribution) with a margin of around 30%.

Figure 10. Cable for PLN's distribution projects (MVAL)

Source: Mirae Asset Research Indonesia

19% 18% 17% 16%

15% 17% 21% 23%

5%

10%

10%12%

0%

10%

20%

30%

40%

50%

60%

2016F 2017F 2018F 2019F

PLN - Unit Bisnis 3 PLN - Transmisi PLN- Distribusi

3 Year CAGR growth (2016F-2019F) =26.4%

KMI Wire and Cable

6

March 9, 2017

Mirae Asset Sekuritas Indonesia Research

The transmission cable business primarily sells low-voltage aluminum (LVAL) cables. Its

flagship products are LVAL-ACCC (aluminum conductor composite core) and LVAL-ACSR

(aluminum conductor steel-reinforced), which together deliver a revenue contribution

of 13.9% and a gross margin of 30-35%—marking the highest levels among KBLI’s cable

products. KBLI expects transmission business revenue to expand as demand from PLN

for LVAL-ACCC and LVAL-ACSR grows.

LVAL-ACCC is a specialty cable that can carry twice as much current as comparable

ACSR cables. In addition, it uses a cutting-edge composite core that: 1) lowers the

probability of sag; 2) boasts strength advantages over rival technologies; and 3) can

withstand higher peak-load temperatures. According to KBLI’s management, the

company boasts significant competitive edges over competitors with regard to LVAL-

ACCC, which is difficult to produce.

Figure 11. Cable for PLN’s transmission projects (LVAL-ACCC) Figure 12. Cable for PLN’s transmission projects (LVAL-ACSR)

Source: Mirae Asset Research Indonesia

Source: Mirae Asset Research Indonesia

The unit business mainly sells HVUGC cables. In 2016, its contribution to total revenue

was merely 2.5% due to a lack of capacity. (KBLI has traditionally imported HVUGC

cables from Korea-based LS Industrial Systems.)

Going forward, we predict KBLI’s performance to be solid due to its plan to largely shift

production toward HVUGC for supply to PLN (higher voltage higher margins).

According to the company, the need for HVUGC cables is likely to grow. This is likely to

benefit KBLI, which has just finalized its investment in a HVUGC cable plant. KBLI

expects the already-high margins from HVUGC cables to expand further going forward

due to strong demand from PLN arising from the 35GW project.

KMI Wire and Cable

7

March 9, 2017

Mirae Asset Sekuritas Indonesia Research

Figure 13. Cable for PLN’s unit business projects (HVUGC)

Source: Mirae Asset Research Indonesia

KBLI is expecting higher contributions from HVUGC and LVAL-ACCC and LVAL-ACSR cables

(which yield higher margins compared to LVCU) in 2017. However, the company is conservatively

forecasting that margins will stabilize at the current level (20-22%).

Figure 14. Gross margin estimates by segment

Source: Company data, Mirae Asset Research Indonesia

Figure 15. KBLI’s quarterly gross margin (%)

Source: Company data, Mirae Asset Research Indonesia

15%

20%

25%

30% 30%

35%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Private sector-distributor (LVCU)

Private sector-freemarket (LVCU)

PLN- Unit Business(HVUGC)

PLN- Distribution(MVAL)

PLN- Transmission(LVAL ACCC)

PLN- Transmission(LVAL ACSR)

2017-2019 F

-

5

10

15

20

25

Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 F

(%) Gross Margin (%)

KMI Wire and Cable

8

March 9, 2017

Mirae Asset Sekuritas Indonesia Research

New facilities to start producing cables for PLN in 2017

For FY16, KBLI’s annual capacity stood at 42,000 tonnes (16,000 tonnes for aluminum; 26,000

tonnes for copper). This year, KBLI will start producing HVUGC cables after adding 3.000 tonnes

of copper cable capacity (for high- and medium-voltage cables). In addition, KBLI will also start

constructing 15,000 tonnes of new aluminum cable capacity in 2H17, as management expects

aluminum cable utilization to reach 94% (the effective maximum level) this year. The additional

15,000 tonnes of capacity are expected to come online in 2018.

Table 1. KBLI’s production capacity

Production capacity

(Tonne)

2016F 2017F 2018F 2019F

Copper 26,000 29,000 29,000 29,000

Aluminum 16,000 16,000 31,000 31,000

Total capacity 42,000 45,000 60,000 60,000

Source: Company data, Mirae Asset Research Indonesia

Table 2. KBLI ‘s utilization rate

Utilization rate 2016F 2017F 2018F 2019F

Copper 62% 61% 67% 74%

Aluminum 74% 94% 66% 79%

Total utilization rate 67% 73% 66% 77% Source: Company data, Mirae Asset Research Indonesia

KMI Wire and Cable

9

March 9, 2017

Mirae Asset Sekuritas Indonesia Research

Figure 16. High-voltage cable extruder machine Figure 17. KBLI’s plant

Source: Company data, Mirae Asset Research Indonesia

Source: Company data, Mirae Asset Research Indonesia

Figure 18. KBLI’s factory Figure 19. KBLI’s factory

Source: Mirae Asset Research Indonesia

Source: Mirae Asset Research Indonesia

KMI Wire and Cable

10

March 9, 2017

Mirae Asset Sekuritas Indonesia Research

Java-Sumatra HVDC interconnection system is needed

To take advantage of the large coal deposits in Sumatra, three mine mouth coal-fired power

plants are being constructed in Bangko Tengah (South Sumatra) under the IPP scheme. The

plants will have total capacity of 3,000MW.

Java and Bali, which have limited energy resources and plants, generate the highest per-capita

demand for electricity; meanwhile, Sumatra boasts large coal deposits that can support coal-fired

steam power plants. In light of these dynamics, we believe that a Java-Sumatra high-voltage

direct current (HVDC) interconnection system would be mutually beneficial to both regions. An

HVDC system would improve the reliability of power supply by linking South Sumatra’s power

plants with a Java load center. Notably, the scheme would require a 500kV HVDC overhead

transmission line network, submarine cables, and a switching station.

We believe that an interconnection system could potentially improve power supply-demand

conditions in both Sumatra and Java. And If the project is brought to life, we think it would have

a positive impact on KBLI in the future.

Table 3. Electricity demand per capita (TWh)

Demand (TWh) 2016F 2018F 2020F 2022F 2024F 2025F

Indonesia 216.8 267.9 315.3 366.0 424.9 457.0

Jawa Bali 162.1 197.1 228.2 260.8 297.5 317.7

East Indonesia 22.7 29.8 36.4 43.6 52.2 56.4

Sumatra 32.1 41.0 50.7 61.7 75.2 82.9

Source: RUPTL, Mirae Asset Research Indonesia

Figure 20. Electricity demand per capita

Source: RUPTL, Mirae Asset Research Indonesia

KMI Wire and Cable

11

March 9, 2017

Mirae Asset Sekuritas Indonesia Research

Impressive FY16F stokes expectations for better performance going forward

KBLI’s management estimates that, for FY16, top line reached around IDR2.8tr (+7.6% YoY).

Meanwhile, core net profit is projected at IDR300bn (excluding a tax revaluation impact of

roughly IDR30bn), more than doubling on a YoY basis.

In our view, KBLI’s strong performance was supported by a more than twofold increase in PLN’s

revenue contribution (to roughly 39%) from the FY14 level. In addition, for 2016, PLN was

allocated around IDR23tr in state capital investment (Penanaman Modal Negara; PMN)—the

highest level among state-owned enterprises—and we believe this benefited KBLI and VOKS.

Notably, KBLI forecasts that revenue from PLN projects will account for around 51% of total

revenue by 2019, which we think will have a positive impact on earnings.

Figure 21. Larger contribution from PLN to total revenue Figure 22. State capital investment (PMN) 2016)

Source: Company data, Mirae Asset Research Indonesia

Source: Company data, Mirae Asset Research Indonesia

Figure 23. KBLI’s quarterly net profit

Source: Company data, Mirae Asset Research Indonesia

15%23%

39%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2014 2015 2016 F

Others PLN

23.6, 43.6%

4.2, 7.7%4.0, 7.4%

3.0, 5.6%

2.5, 4.5%

2.3, 4.2%

2.0, 3.7%

2.0, 3.7%

1.3, 2.4%

9.3, 17.1%

PLN

Sarana Multi Infrastruktur

Wijaya Karya (WIKA IJ)

Hutama Karya

Krakatau Steel (KRAS IJ)

Pembangunan Perumahan(PTPP IJ)

Angkasa Pura II

Perum Bulog

Jasa Marga (JSMR IJ)

Others

(IDRtr)

49

62

80

86

102

(20)

-

20

40

60

80

100

120

3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16F

(IDRbn)

KMI Wire and Cable

12

March 9, 2017

Mirae Asset Sekuritas Indonesia Research

Valuation remains cheap; Re-rating expected

For 2017, KBLI’s management conservatively assumes that bottom line will grow by 18% YoY to

reach IDR354bn. This earnings level (EPS of IDR88) translates into a 2017F P/E of 4.9x, which we

deem still very attractive. In addition, KBLI is trading at a 71% discount compared to the average

2017F multiple (16.7x) of its peer group, which includes Schneider Electric, Omron Corp., LS

Industrial Systems, and TBEA.

KBLI is currently trading at its seven-year average P/E. A re-rating to the +2 standard deviation

level (11.6x P/E) translates into a share price of IDR1,020/share.

Figure 24. KBLI’s forward P/E band

Source: Bloomberg, Mirae Asset Research Indonesia

Table 4. Peer group valuation

Company P/E ratio (2017F)

Schneider Electric SE (SU FP equity/Not Rated), 16.5

Omron Corp. (6645 JT equity/Not Rated), 24.0

LS Industrial Systems (010120 KS equity/Not Rated) 12.7

TBEA (600089 CH equity/Not Rated) 13.7

Average P/E 16.7 Source: Bloomberg, Mirae Asset Research Indonesia

-1 Std Dev

Avg PER

+1 Std Dev

+2 Std Dev

1

3

5

7

9

11

13

15

17

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

( x )

+3 Std Dev

KMI Wire and Cable

13

March 9, 2017

Mirae Asset Sekuritas Indonesia Research

APPENDIX 1

Important Disclosures & Disclaimers

Stock Ratings Industry Ratings

Buy Relative performance of 20% or greater Overweight Fundamentals are favorable or improving

Trading Buy Relative performance of 10% or greater, but with volatility Neutral Fundamentals are steady without any material changes

Hold Relative performance of -10% and 10% Underweight Fundamentals are unfavorable or worsening

Sell Relative performance of -10%

* Our investment rating is a guide to the relative return of the stock versus the market over the next 12 months. * Although it is not part of the official ratings at Mirae Asset Sekuritas Indonesia, we may call a trading opportunity in case there is a technical or short-term material development. * The target price was determined by the research analyst through valuation methods discussed in this report, in part based on the analyst’s estimate of future earnings. The achievement of the target price may be impeded by risks related to the subject securities and companies, as well as general market and economic conditions. Analyst Certification The research analysts who prepared this report (the “Analysts”) are registered with the Indonesian jurisdiction and are subject to Indonesian securities regulations. They are neither registered as research analysts in any other jurisdiction nor subject to the laws and regulations thereof. Opinions expressed in this publication about the subject securities and companies accurately reflect the personal views of the Analysts primarily responsible for this report. PT. Mirae Asset Seukritas Indonesia (“Mirae Asset Daewoo”) policy prohibits its Analysts and members of their households from owning securities of any company in the Analyst’s area of coverage, and the Analysts do not serve as an officer, director or advisory board member of the subject companies. Except as otherwise specified herein, the Analysts have not received any compensation or any other benefits from the subject companies in the past 12 months and have not been promised the same in connection with this report. No part of the compensation of the Analysts was, is, or will be directly or indirectly related to the specific recommendations or views contained in this report but, like all employees of Mirae Asset Daewoo, the Analysts receive compensation that is determined by overall firm profitability, which includes revenues from, among other business units, the institutional equities, investment banking, proprietary trading and private client division. At the time of publication of this report, the Analysts do not know or have reason to know of any actual, material conflict of interest of the Analyst or Mirae Asset Daewoo except as otherwise stated herein. Disclaimers This report is published by Mirae Asset Daewoo, a broker-dealer registered in the Republic of Indonesia and a member of the Indonesia Stock Exchange. Information and opinions contained herein have been compiled in good faith and from sources believed to be reliable, but such information has not been independently verified and Mirae Asset Daewoo makes no guarantee, representation or warranty, express or implied, as to the fairness, accuracy, completeness or correctness of the information and opinions contained herein or of any translation into English from the Indonesian language. In case of an English translation of a report prepared in the Indonesian language, the original Indonesian language report may have been made available to investors in advance of this report. The intended recipients of this report are sophisticated institutional investors who have substantial knowledge of the local business environment, its common practices, laws and accounting principles and no person whose receipt or use of this report would violate any laws and regulations or subject Mirae Asset Daewoo and its affiliates to registration or licensing requirements in any jurisdiction shall receive or make any use hereof. This report is for general information purposes only and it is not and shall not be construed as an offer or a solicitation of an offer to effect transactions in any securities or other financial instruments. The report does not constitute investment advice to any person and such person shall not be treated as a client of Mirae Asset Daewoo by virtue of receiving this report. This report does not take into account the particular investment objectives, financial situations, or needs of individual clients. The report is not to be relied upon in substitution for the exercise of independent judgment. Information and opinions contained herein are as of the date hereof and are subject to change without notice. The price and value of the investments referred to in this report and the income from them may depreciate or appreciate, and investors may incur losses on investments. Past performance is not a guide to future performance. Future returns are not guaranteed, and a loss of original capital may occur. Mirae Asset Daewoo, its affiliates and their directors, officers, employees and agents do not accept any liability for any loss arising out of the use hereof. Mirae Asset Daewoo may have issued other reports that are inconsistent with, and reach different conclusions from, the opinions presented in this report. The reports may reflect different assumptions, views and analytical methods of the analysts who prepared them. Mirae Asset Daewoo may make investment decisions that are inconsistent with the opinions and views expressed in this research report. Mirae Asset Daewoo, its affiliates and their directors, officers, employees and agents may have long or short positions in any of the subject securities at any time and may make a purchase or sale, or offer to make a purchase or sale, of any such securities or other financial instruments from time to time in the open market or otherwise, in each case either as principals or agents. Mirae Asset Daewoo and its affiliates may have had, or may be expecting to enter into, business relationships with the subject companies to provide investment banking, market-making or other financial services as are permitted under applicable laws and regulations. No part of this document may be copied or reproduced in any manner or form or redistributed or published, in whole or in part, without the prior written consent of Mirae Asset Daewoo.

Disclosures As of the publication date, PT. Mirae Asset Sekuritas Indonesia, and/or its affiliates do not have any special interest with the subject company and do not own 1% or more of the subject company's shares outstanding.

KMI Wire and Cable

14

March 9, 2017

Mirae Asset Sekuritas Indonesia Research

Distribution United Kingdom: This report is being distributed by Mirae Asset Securities (UK) Ltd. in the United Kingdom only to (i) investment professionals falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”), and (ii) high net worth companies and other persons to whom it may lawfully be communicated, falling within Article 49(2)(A) to (E) of the Order (all such persons together being referred to as “Relevant Persons”). This report is directed only at Relevant Persons. Any person who is not a Relevant Person should not act or rely on this report or any of its contents. United States: This report is distributed in the U.S. by Mirae Asset Securities (USA) Inc., a member of FINRA/SIPC, and is only intended for major institutional investors as defined in Rule 15a-6(b)(4) under the U.S. Securities Exchange Act of 1934. All U.S. persons that receive this document by their acceptance thereof represent and warrant that they are a major institutional investor and have not received this report under any express or implied understanding that they will direct commission income to Mirae Asset Daewoo or its affiliates. Any U.S. recipient of this document wishing to effect a transaction in any securities discussed herein should contact and place orders with Mirae Asset Securities (USA) Inc., which accepts responsibility for the contents of this report in the U.S. The securities described in this report may not have been registered under the U.S. Securities Act of 1933, as amended, and, in such case, may not be offered or sold in the U.S. or to U.S. persons absent registration or an applicable exemption from the registration requirements. Hong Kong: This document has been approved for distribution in Hong Kong by Mirae Asset Securities (HK) Ltd., which is regulated by the Hong Kong Securities and Futures Commission. The contents of this report have not been reviewed by any regulatory authority in Hong Kong. This report is for distribution only to professional investors within the meaning of Part I of Schedule 1 to the Securities and Futures Ordinance of Hong Kong (Cap. 571, Laws of Hong Kong) and any rules made thereunder and may not be redistributed in whole or in part in Hong Kong to any person. All Other Jurisdictions: Customers in all other countries who wish to effect a transaction in any securities referenced in this report should contact Mirae Asset Daewoo or its affiliates only if distribution to or use by such customer of this report would not violate applicable laws and regulations and not subject Mirae Asset Daewoo and its affiliates to any registration or licensing requirement within such jurisdiction. Mirae Asset Daewoo International Network

Mirae Asset Daewoo Co., Ltd. (Seoul) Mirae Asset Securities (HK) Ltd. Mirae Asset Securities (UK) Ltd. Global Equity Sales Team Mirae Asset Center 1 Building 26 Eulji-ro 5-gil, Jung-gu, Seoul 04539 Korea

Suites 1109-1114, 11th Floor Two International Finance Centre 8 Finance Street, Central Hong Kong China

41st Floor, Tower 42 25 Old Broad Street, London EC2N 1HQ United Kingdom

Tel: 82-2-3774-2124 Tel: 852-2845-6332 Tel: 44-20-7982-8000

Mirae Asset Securities (USA) Inc. Mirae Asset Wealth Management (USA) Inc. Mirae Asset Wealth Management (Brazil) CCTVM 810 Seventh Avenue, 37th Floor New York, NY 10019 USA

555 S. Flower Street, Suite 4410, Los Angeles, California 90071 USA

Rua Funchal, 418, 18th Floor, E-Tower Building Vila Olimpia Sao Paulo - SP 04551-060 Brasil

Tel: 1-212-407-1000 Tel: 1-213-262-3807 Tel: 55-11-2789-2100

PT. Mirae Asset Sekuritas Indonesia Mirae Asset Securities (Singapore) Pte. Ltd. Mirae Asset Securities (Vietnam) LLC Equity Tower Building Lt. 50 Sudirman Central Business District Jl. Jend. Sudirman, Kav. 52-53 Jakarta Selatan 12190 Indonesia

6 Battery Road, #11-01 Singapore 049909 Republic of Singapore

7F, Saigon Royal Building 91 Pasteur St. District 1, Ben Nghe Ward, Ho Chi Minh City Vietnam

Tel: 62-21-515-3281 Tel: 65-6671-9845 Tel: 84-8-3911-0633 (ext.110)

Mirae Asset Securities Mongolia UTsK LLC Mirae Asset Investment Advisory (Beijing) Co., Ltd Beijing Representative Office

#406, Blue Sky Tower, Peace Avenue 17 1 Khoroo, Sukhbaatar District Ulaanbaatar 14240 Mongolia

2401B, 24th Floor, East Tower, Twin Towers B12 Jianguomenwai Avenue, Chaoyang District Beijing 100022 China

2401A, 24th Floor, East Tower, Twin Towers B12 Jianguomenwai Avenue, Chaoyang District Beijing 100022 China

Tel: 976-7011-0806 Tel: 86-10-6567-9699 Tel: 86-10-6567-9699 (ext. 3300)

Shanghai Representative Office Ho Chi Minh Representative Office

38T31, 38F, Shanghai World Financial Center 100 Century Avenue, Pudong New Area Shanghai 200120 China

7F, Saigon Royal Building 91 Pasteur St. District 1, Ben Nghe Ward, Ho Chi Minh City Vietnam

Tel: 86-21-5013-6392 Tel: 84-8-3910-7715