Israel from the perspective of foreign investors

page 2

Are the foreign investors here?

Saban-Apax-Arkin Cerberus Orascom

Institutional Investors Capital Group Templeton Fidelity Boston Company Pioneer Investment management T Rowe Price Schroders

page 3

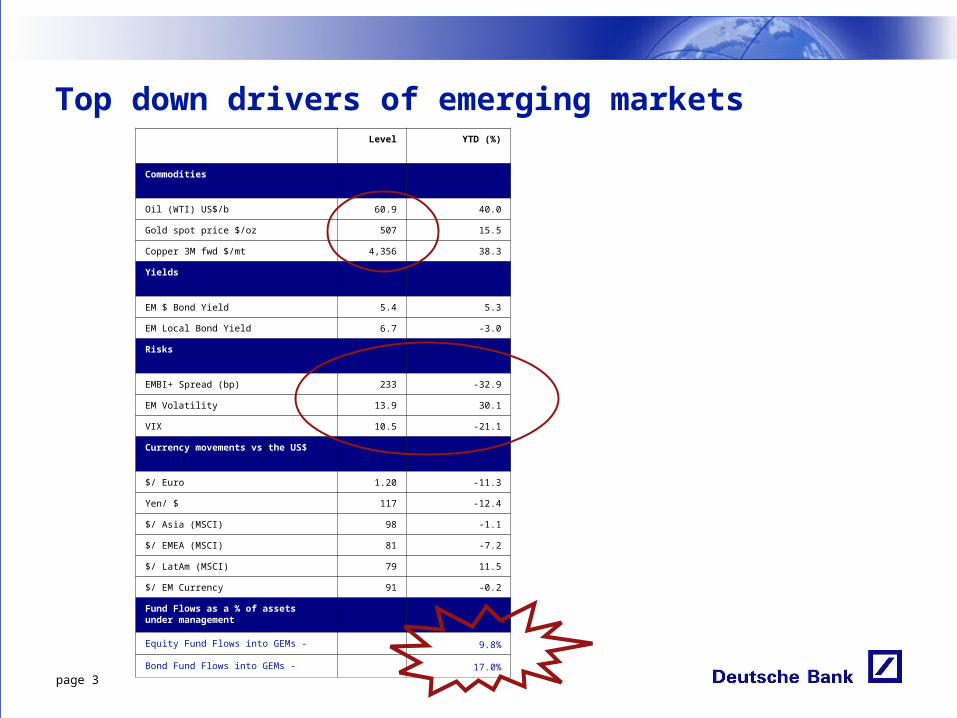

Level YTD (%)

Commodities

Oil (WTI) US$/b 60.9 40.0

Gold spot price $/oz 507 15.5

Copper 3M fwd $/mt 4,356 38.3

Yields

EM $ Bond Yield 5.4 5.3

EM Local Bond Yield 6.7 -3.0

Risks

EMBI+ Spread (bp) 233 -32.9

EM Volatility 13.9 30.1

VIX 10.5 -21.1

Currency movements vs the US$

$/ Euro 1.20 -11.3

Yen/ $ 117 -12.4

$/ Asia (MSCI) 98 -1.1

$/ EMEA (MSCI) 81 -7.2

$/ LatAm (MSCI) 79 11.5

$/ EM Currency 91 -0.2

Fund Flows as a % of assets under management

Equity Fund Flows into GEMs - 9.8%

Bond Fund Flows into GEMs - 17.0%

Top down drivers of emerging markets

page 4

Flow of funds into emerging markets in 2005 (1)

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000Ja

n-0

5

Feb-0

5

Mar

-05

Apr-05

May

-05

Jun-0

5

Jul-0

5

Aug-0

5

Sep-0

5

Oct

-05

YTD Cumulative fund flows into All dedicated EM funds

page 5

Flow of funds into emerging markets in 2005 (2)

-5%

0%

5%

10%

15%

20%

05-J

an-0

512

-Jan

-05

19-J

an-0

526

-Jan

-05

02-F

eb-0

509

-Feb

-05

16-F

eb-0

523

-Feb

-05

02-M

ar-0

509

-Mar

-05

16-M

ar-0

523

-Mar

-05

30-M

ar-0

506

-Apr

-05

13-A

pr-0

520

-Apr

-05

27-A

pr-0

504

-May

-05

11-M

ay-0

518

-May

-05

25-M

ay-0

501

-Jun

-05

08-J

un-0

515

-Jun

-05

22-J

un-0

529

-Jun

-05

06-J

ul-0

513

-Jul

-05

20-J

ul-0

527

-Jul

-05

03-A

ug-0

510

-Aug

-05

17-A

ug-0

524

-Aug

-05

31-A

ug-0

507

-Sep

-05

14-S

ep-0

521

-Sep

-05

28-S

ep-0

505

-Oct

-05

12-O

ct-0

519

-Oct

-05

26-O

ct-0

502

-Nov

-05

09-N

ov-0

516

-Nov

-05

23-N

ov-0

530

-Nov

-05

07-D

ec-0

514

-Dec

-05

Equity Weekly Flows (% of AUM) Bond Weekly Flows (% of AUM)

YTD Equity Cumulative Flows (% of AUM) YTD Bond Cumulative Flows (% of AUM)

– 10% of flows into equity funds allocated to emerging markets in 2005

– 17% of flows into bond funds allocated to emerging markets

page 6

0

20

40

60

80

100

120

140

160

Jan-

00

Apr

-00

Jul-0

0

Oct

-00

Jan-

01

Apr

-01

Jul-0

1

Oct

-01

Jan-

02

Apr

-02

Jul-0

2

Oct

-02

Jan-

03

Apr

-03

Jul-0

3

Oct

-03

Jan-

04

Apr

-04

Jul-0

4

Oct

-04

Jan-

05

Apr

-05

Jul-0

5

Oct

-05

MSCI DM MSCI EM

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

Dec

-99

Apr

-00

Aug

-00

Dec

-00

Apr

-01

Aug

-01

Dec

-01

Apr

-02

Aug

-02

Dec

-02

Apr

-03

Aug

-03

Dec

-03

Apr

-04

Aug

-04

Dec

-04

Apr

-05

Aug

-05

EM $ Yld EM Local Yld

Emerging vs developed market performance Israel vs emerging markets

0

20

40

60

80

100

120

140

160

Jan-

00

Apr

-00

Jul-0

0

Oct

-00

Jan-

01

Apr

-01

Jul-0

1

Oct

-01

Jan-

02

Apr

-02

Jul-0

2

Oct

-02

Jan-

03

Apr

-03

Jul-0

3

Oct

-03

Jan-

04

Apr

-04

Jul-0

4

Oct

-04

Jan-

05

Apr

-05

Jul-0

5

Oct

-05

MSCI Israel MSCI EM

Emerging market bond yields

page 7

Valuations in emerging markets still lower, though gap closing

0

5

10

15

20

25

30

35

Dec

-96

Jun-

97

Dec

-97

Jun

-98

Dec

-98

Jun-

99

Dec

-99

Jun-

00

Dec

-00

Jun

-01

Dec

-01

Jun-

02

De

c-02

Jun-

03

Dec

-03

Jun

-04

Dec

-04

Jun-

05

EM PE DM PE

page 8

Israel in a global context

PE EPS Growth PBV ROE Div Yld

Country 05 (x)

06 (x)

05 $(%)

06 $(%)

05 (x)

06 (x)

05 $(%)

06 $(%)

06 (x)

China 11 10 28% 7% 2.4 2.1 24% 22% 4.3%

India 16 14 20% 13% 3.6 3.0 25% 24% 1.8%

Indonesia 12 9 4% 33% 3.0 2.5 26% 30% 4.0%

Korea 13 11 -19% 16% 2.1 1.8 18% 18% 1.3%

Malaysia 15 14 -6% 13% 2.2 2.1 15% 16% 3.8%

Taiwan 15 13 -8% 17% 2.7 2.4 18% 19% 3.7%

Thailand 11 10 1% 4% 2.1 1.9 21% 20% 4.7%

Hungary 10 11 21% -7% 2.6 2.1 28% 22% 3.5%

Israel 21 17 12% 27% 3.5 2.9 18% 19% 4.8%

Poland 11 9 35% 21% 1.8 1.5 18% 18% 4.2%

Russia 8 11 46% -30% 1.8 1.6 26% 16% 2.1%

South Africa 11 11 38% 35% 2.5 2.8 23% 28% 3.3%

Turkey 15 12 27% 43% 2.4 2.3 15% 19% 1.4%

Brazil 8 7 77% 22% 2.4 1.8 35% 30% 3.4%

Chile 24 18 -26% 34% 2.2 2.0 10% 12% 0.3%

Mexico 17 14 26% 17% 4.2 3.8 26% 27% 0.5%

ASIA 14 12 -2% 15% 2.5 2.2 20% 20% 2.8%

EMEA 12 12 34% 17% 2.4 2.4 22% 22% 2.6%

LATAM 13 10 50% 21% 2.9 2.5 30% 27% 2.1%

EM 13 11 18% 17% 2.6 2.3 22% 22% 2.6%

US 16.4 15.3 15 8 2.8 17

Japan 15.5 17.4 18 16 1.6 10

Europe 13.9 13.0 18 13 2.3 17

page 9

Performance of MSCI Israel equity market in global context

-10 0 10 20 30 40 50 60 70 80

Taiwan

Malaysia

Thailand

US

Europe

Indonesia

China

Chile

Hungary

South Africa

Poland

J apan

Israel

India

Turkey

Korea

Mexico

Brazil

Russia

page 10

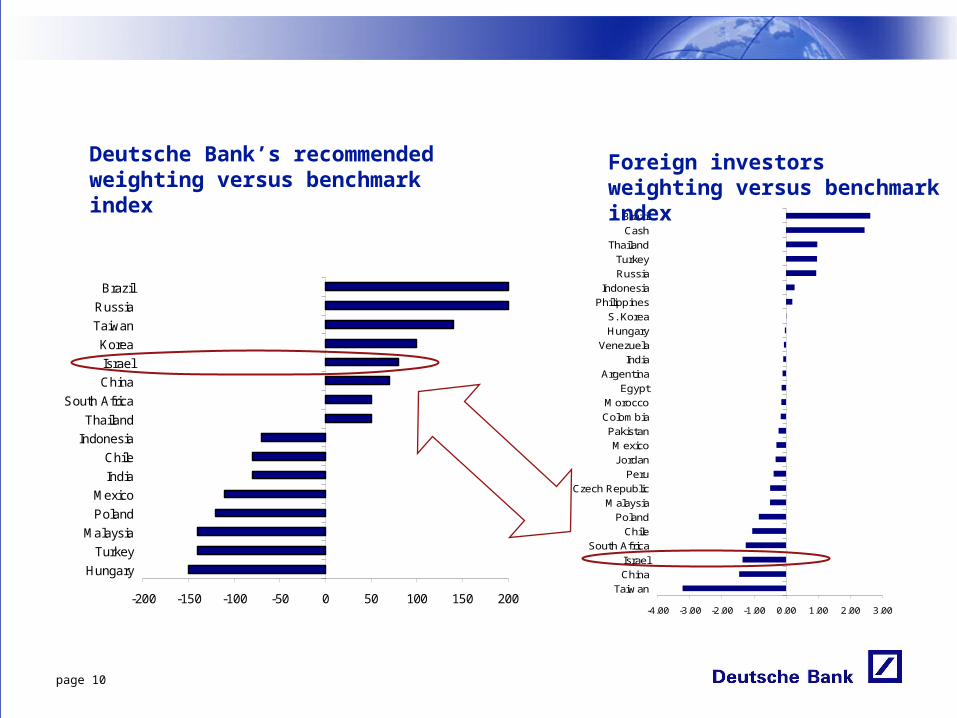

-200 -150 -100 -50 0 50 100 150 200

Hungary

Turkey

Malaysia

Poland

Mexico

India

Chile

Indonesia

Thailand

South Africa

China

Israel

Korea

Taiwan

Russia

Brazil

-4.00 -3.00 -2.00 -1.00 0.00 1.00 2.00 3.00

TaiwanChinaIsrael

South AfricaChile

PolandMalaysia

Czech RepublicPeru

J ordanMexico

PakistanColombiaMorocco

EgyptArgentina

IndiaVenezuela

HungaryS. Korea

PhilippinesIndonesia

RussiaTurkey

ThailandCashBrazil

Deutsche Bank’s recommended weighting versus benchmark index

Foreign investors weighting versus benchmark index

page 11

Currency value as % of 2005 PPP fair value

US

Russia

Brazil

Turkey

Taiwan

Malaysia

Philippines

Korea

Czech Republic

Thailand

Hungary

Poland

Israel

Argentina

South Africa

India

IndonesiaChina

Chile

Mexico

0%

20%

40%

60%

80%

100%

120%

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000GDP pc PPP terms US$

% o

f PPP fai

r va

lue

Cheap

Expensive

page 12

60 Day annualized Vol

Equity 5YR YTD Currncy

5YR YTD

Vol Avg chg (%)

Vol Avg chg (%)

Israel 11.0 24.9 -25.2 5.0 5.9 12.3

ASIA 14.4 19.6 1.7 3.6 4.2 -26.5

EMEA 18.4 17.5 43.5 8.0 11.4 -8.0

LATAM 22.3 20.9 51.4 9.8 11.3 13.3

EM 13.9 15.0 30.1 6.0 7.5 -9.7

US 11.1 17.5 13.0 nm nm nm

Japan 17.5 21.3 8.9 6.8 9.4 -26.1

Europe 11.2 17.4 7.3 8.6 10.1 7.4

1Y Beta 5YR

Current Avg

Israel 0.4 0.7

Turkey 1.3 1.3

Argentina 1.3 0.8

Brazil 1.5 1.2

Chile 0.7 0.6

Mexico 1.0 0.8

ASIA 0.9 1.1

EMEA 1.1 0.8

LATAM 1.3 0.9

EM 1.0 1.0

Country and currency volatility Beta to emerging markets

If we are not EM, what are we?

page 13

Key Deutsche Bank global forecasts

Current level 2006F

US inflation (core PCE) % 1.8% 2.0%

Fed Funds rate (YE) % 4.3% 5.0%

US real GDP growth % 3.7% 4.0%

China real GDP growth % 8.4%

WTI US$/b end period 61 50

Copper 3M fwd $/mt end period 4,372 2,976

Gold price US$/oz end period 524 500

Nickel US$/mt 14,165 12,566

$/ EUR end period 1.19 1.25

Yen/ $ end period 120 114

page 14

Deutsche Bank’s Israel forecasts2004 2005F 2006F

Nominal GDP (USDbn) 117.0 124.7 134.1Real GDP (YoY%) 4.4 4.5 4.1 Priv. consumption 5.0 5.0 4.5 Gov't consumption -2.4 1.0 1.0 Investment 4.0 5.5 5.0 Exports 17.4 7.9 6.5 Imports 11.8 6.0 5.3CPI 1.2 3.0 2.0Money (M1) 17.9 25.0 23.6Fiscal accounts, % of GDP -3.8 -1.5 -3.0Exports 36.6 40.2 45.1Imports 38.5 43.7 48.1Trade balance -1.9 -3.5 -3.0 % of GDP -1.6 -2.8 -2.2Current account balance 1.5 1.5 1.2 % of GDP 1.3 1.2 0.9FDI -1.5 3.5 1.0FX reserves (USDbn) 26.6 27.6 29.4ILS/USD (eop) 4.32 4.60 4.30ILS/EUR (eop) 5.88 5.20 5.46Debt Indicators (% of GDP) 106.0 100.1 96.3Industrial production 7.2 6.0 5.6Unemployment (pavg) 10.3 9.0 8.9

page 15

What can we do next?

Move to nominal reporting

Increase liquidity

Easy access to stock borrowing

Standardize OTC documentation

Netting

Free float