Investor Presentation

June 2021

Forward Looking Statements & Non-IFRS Measures

2

Notice to Reader: This presentation and the oral statements made during this meeting contain certain statements that constitute forward-looking information within the meaning of applicable securities laws ("forward-looking statements"). Such forward-looking statements involve known and unknown risks, uncertainties and other factors including those related to the COVID-19 pandemic that may cause the actual results, performance or achievements of ATS, or developments in ATS’ business or in its industry, to differ materially from the anticipated results, performance, achievements or developments expressed or implied by such forward-looking statements. Forward-looking statements include all disclosure regarding possible events, conditions or results of operations that is based on assumptions about future economic conditions and courses of action. Forward-looking statements may also include, without limitation, any statement relating to future events, conditions or circumstances. ATS cautions you not to place undue reliance upon any such forward-looking statements, which speak only as of the date they are made. Forward-looking statements relate to, among other things, the BioDot transaction. The risks and uncertainties that may affect forward-looking statements include, among others, the duration and impact of the COVID-19 pandemic, general market performance, performance of the Canadian dollar, performance of the market sectors that ATS serves, success and impact of the initiatives that ATS is undertaking, and other risks and uncertainties detailed from time to time in ATS’ filings with Canadian provincial securities regulators, including ATS’ Annual Report and Annual Information Form for the fiscal year ended March 31, 2020. Forward-looking statements are based on management's current plans, estimates, projections, beliefs and opinions, and ATS does not undertake any obligation to update forward-looking statements should assumptions related to these plans, estimates, projections, beliefs and opinions change.

Non-IFRS Measures: This presentation uses the non-IFRS measures adjusted EBITDA, and adjusted EBITDA margin. These terms do not have any standardized meanings prescribed within IFRS and therefore may not be comparable to similar measures presented by other companies. These measures should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Adjusted EBITDA is defined as earnings from operations excluding depreciation and amortization (which includes amortization of intangible assets and right-of-use assets) before items excluded from management’s internal analysis of operating results, such as amortization expense of acquisition-related intangible assets, acquisition-related transaction and integration costs, restructuring charges, and certain other adjustments which would be non-recurring in nature. Adjusted EBITDA margin is an expression of an entity’s adjusted EBITDA as a percentage of revenues. Adjusted EBITDA is used by the Company to evaluate the performance of operations. Management believes that adjusted EBITDA is an important indicator of the Company’s ability to generate operating cash flows to fund continued investment in operations. Management believes that ATS shareholders and potential investors in ATS use these non-IFRS financial measures in making investment decisions and measuring operational results.

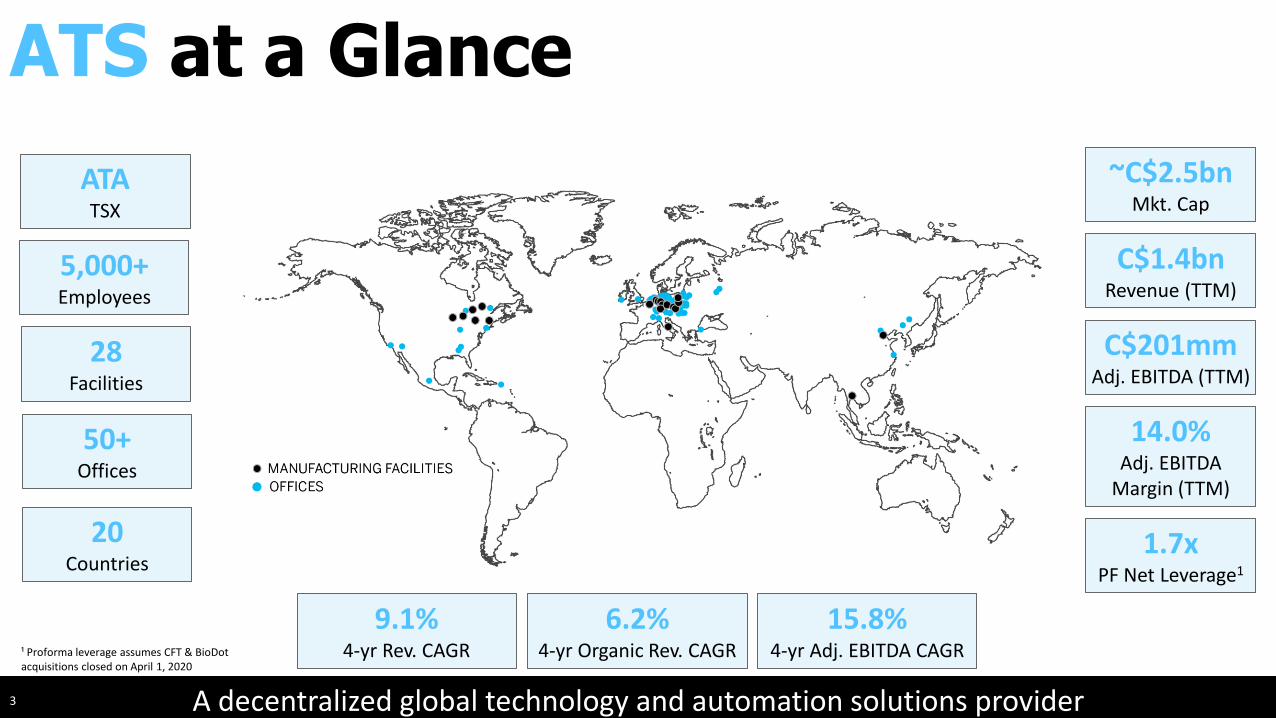

A decentralized global technology and automation solutions provider

ATATSX

C$1.4bnRevenue (TTM)

5,000+Employees

28Facilities

20Countries

50+ Offices

ATS at a Glance

3

v21

C$201mmAdj. EBITDA (TTM)

~C$2.5bnMkt. Cap

14.0%Adj. EBITDA

Margin (TTM)

1.7xPF Net Leverage1

9.1%4-yr Rev. CAGR

6.2%4-yr Organic Rev. CAGR

15.8%4-yr Adj. EBITDA CAGR¹ Proforma leverage assumes CFT & BioDot

acquisitions closed on April 1, 2020

End-to-end solutions to transform, streamline, and optimize customer operations

What We Do

4

Products & ComponentsAutomation & Integration

Solutions Services

ATS developed products & components (hardware /

software)

ExamplesSuperTrak™ - revolutionary

pallet transport system

Illuminate™ Factory Floor Management System

ATS Smartvision software

MARCO LineMaster - IoT enabled weighing scale

10% of Revenue

Standalone machines, complete systems & Enterprise programs

ExamplesHigh speed tube filling

Semi-autonomous food weighing & handling

Battery & EV motor assembly and test lines

High speed assembly lines for inhalers / IV sets

60% of Revenue

Front-end design & analysis, after-market services

(retooling / retrofitting, supply chain management,

maintenance)

ExamplesRetrofit of nuclear power

plants

Remote diagnostics

Process optimization

Preventative maintenance

Emergency and on-call support

30% of Revenue

Diversified Customer & Revenue Base

ATS Brands

¹ Fiscal 2021

Life Sciences56%

Transportation19%

Consumer17%

Energy8%

Revenue By

Segment1

North America

48%

Europe40%

Asia/Other12%

Revenue By Region1

5

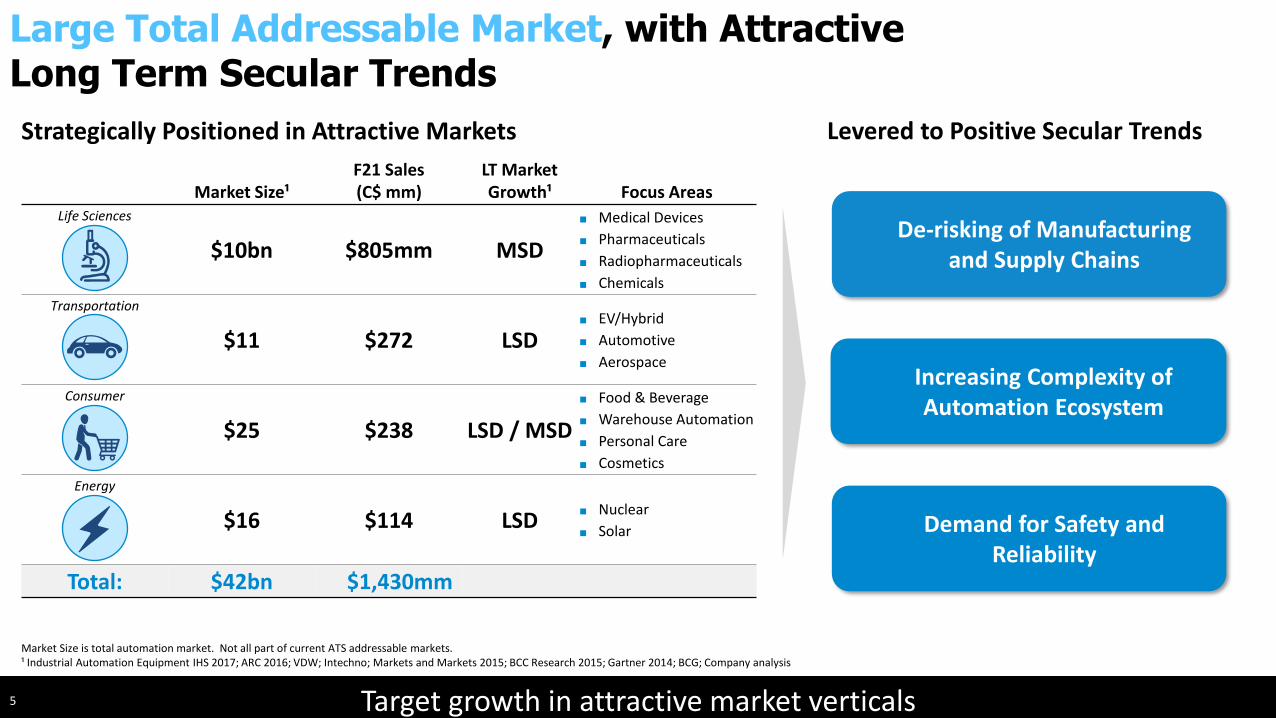

Strategically Positioned in Attractive Markets Levered to Positive Secular Trends

De-risking of Manufacturing and Supply Chains

Demand for Safety and Reliability

Increasing Complexity of Automation Ecosystem

Market Size is total automation market. Not all part of current ATS addressable markets.¹ Industrial Automation Equipment IHS 2017; ARC 2016; VDW; Intechno; Markets and Markets 2015; BCC Research 2015; Gartner 2014; BCG; Company analysis

Market Size¹F21 Sales (C$ mm)

LT Market Growth¹ Focus Areas

Life Sciences

$10bn $805mm MSD

■ Medical Devices

■ Pharmaceuticals

■ Radiopharmaceuticals

■ Chemicals

Transportation

$11 $272 LSD■ EV/Hybrid

■ Automotive

■ Aerospace

Consumer

$25 $238 LSD / MSD

■ Food & Beverage

■ Warehouse Automation

■ Personal Care

■ Cosmetics

Energy

$16 $114 LSD■ Nuclear

■ Solar

Total: $42bn $1,430mm

Target growth in attractive market verticals

Large Total Addressable Market, with Attractive Long Term Secular Trends

19%

17%

Revenue by Market(F2021)

56%

8%

Diversified Customer Base

Life SciencesMedical Devices

PharmaceuticalsChemicals

Transportation

EV/Hybrid

Automotive

Consumer

Cosmetics

Food & Beverage

EnergyNuclear Solar

Radiopharmaceuticals

Warehouse Automation

Repeat customers represent >85% of Order Bookings 6

Personal Care

Aerospace

Repeatable model to drive performance and growth7

Daily Management

STRENGTHEN OUR CORE

DELIVER GROWTH PURSUIT OFEXCELLENCE

Long Term Value

Goal Deployment

Strategic Planning Process

Continuous Improvement

Pioneering Innovation

Customer Success

Organization/Talent Development

Monthly Business Reviews

Annual Operating Plan

Customer First

PerformanceManagement

KPI’s

Value Drivers

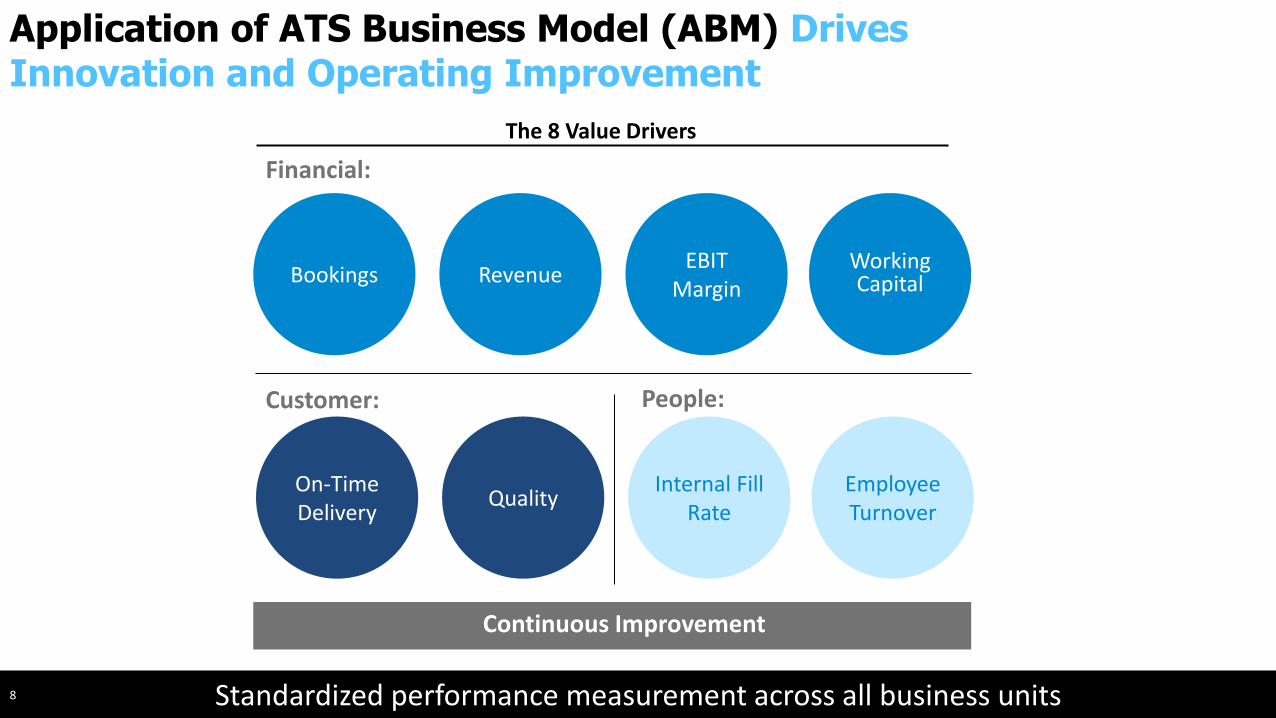

Application of ATS Business Model (ABM) Drives Innovation and Operating Improvement

Financial:

Customer: People:

Bookings RevenueEBIT

MarginWorking Capital

On-Time Delivery

QualityInternal Fill

RateEmployee Turnover

Continuous Improvement

Standardized performance measurement across all business units8

The 8 Value Drivers

Application of ATS Business Model (ABM) Drives Innovation and Operating Improvement

Targeting attractive markets with high barriers to entry and strong secular growth drivers

Expanding Presence in Strategic Core Markets

9

Life Sciences Food

New FrontiersElectric Vehicles

INNOVATION

DIGITAL GROWTH

STRATEGIC M&A

MARGIN IMPROVEMENT

Enablers Differentiated technologies / products

IIOT, serialization, predictive maintenance, real-time optimization

Strengthen and expand portfolio

Standardization, supply chain, operational leverage, after-sales services growth, ABM

Attractive Markets

Barriers to Entry:▪ Regulated environments▪ Technologically intense▪ Complex processes▪ Quality critical

Market Dynamics:▪ Life Sciences: demographics, new treatments,

new ailments, disposables ▪ Food: government regs, quality, demographics▪ EV: government regs, CO2 reduction ▪ New frontiers, factory optimization, digitization

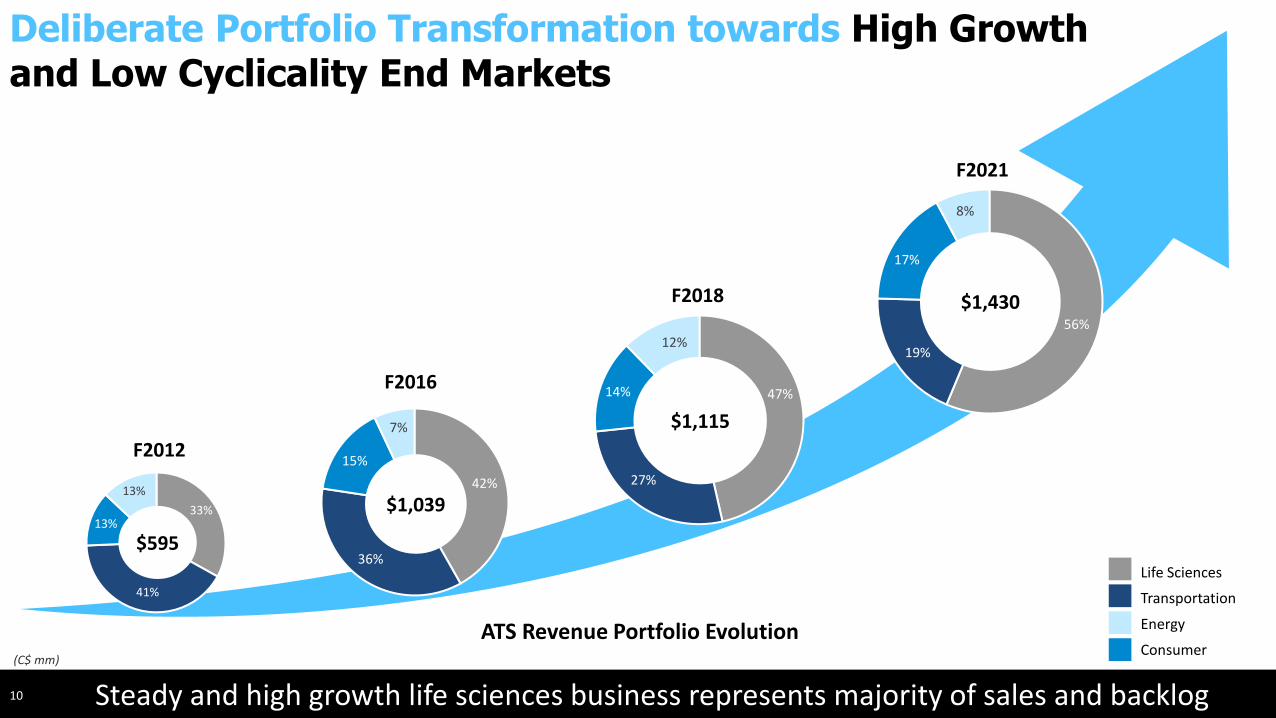

10 Steady and high growth life sciences business represents majority of sales and backlog

Deliberate Portfolio Transformation towards High Growth and Low Cyclicality End Markets

F2012

33%

41%

13%

13%

$595

42%

36%

15%

7%

$1,039

F201647%

27%

14%

12%

$1,115

F2018

56%

19%

17%

8%

$1,430

F2021

(C$ mm)

ATS Revenue Portfolio Evolution

Life Sciences

Transportation

Energy

Consumer

11

Life Sciences – 56% of F2021 sales Transportation – 19% of F2021 sales

Consumer – 17% of F2021 sales Energy – 8% of F2021 sales

Revenue (C$ mm)

Revenue (C$ mm)

Revenue (C$ mm)

Revenue (C$ mm)

Trends / Opportunities

■ Favorable demographics

■ Robust new product pipeline

■ Focus on quality, cost rationalization and efficiency

Trends / Opportunities

■ EV shift (75% of ATS’ Transport business is levered to EV)

■ Record number of launches

■ Standardized automation globally

Trends / Opportunities

■ Growing middle class (emerging markets)

■ New products/rapid design and scale

■ Significant investment in production capacity

Trends / Opportunities

■ Increasing global demand for clean energy

■ Major tooling and equipment life cycle management

■ Nuclear decommissioning and solar

Numerous opportunities across segments for stable growth

Targeting End Markets with Favourable Tailwinds

$415$518

$609

$770 $805

2017 2018 2019 2020 2021

$285 $299 $302

$385

$272

2017 2018 2019 2020 2021

$138$161

$203$172

$238

2017 2018 2019 2020 2021

$174

$137 $140

$102 $114

2017 2018 2019 2020 2021

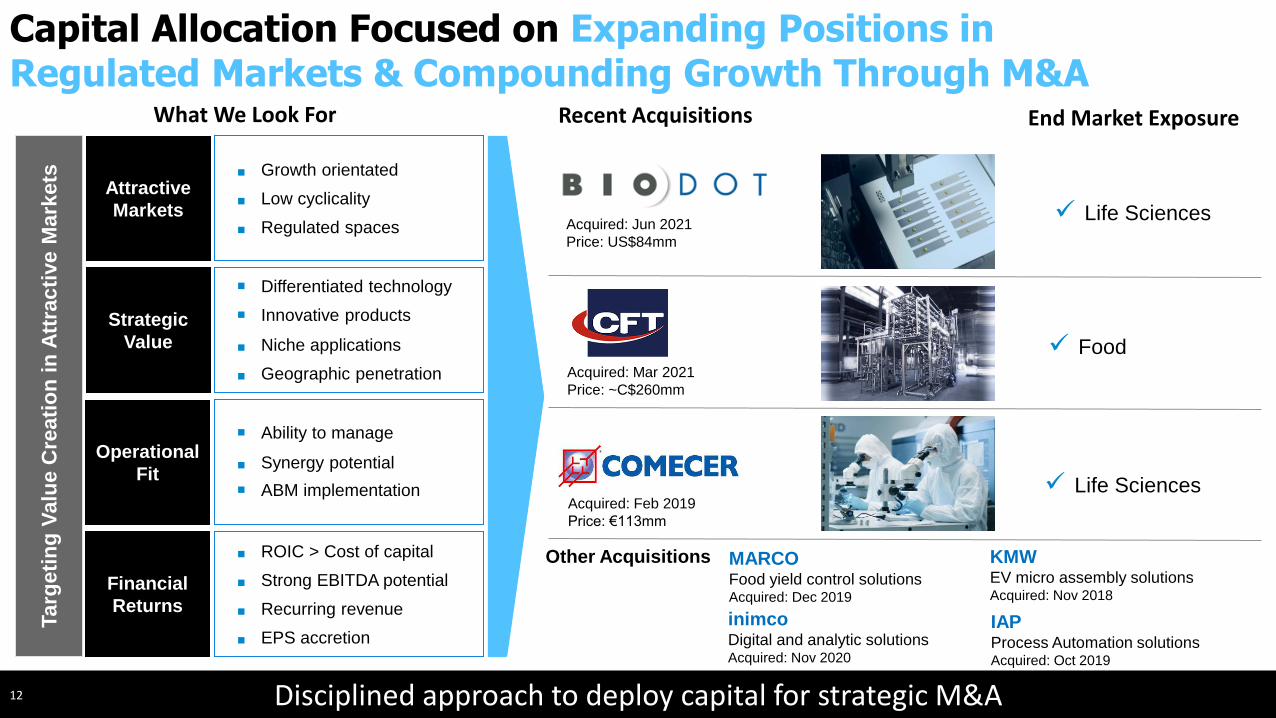

Disciplined approach to deploy capital for strategic M&A

Targ

eti

ng

Valu

e C

reati

on

in

Att

rac

tive M

ark

ets

What We Look For

Attractive

Markets

Strategic

Value

Operational

Fit

Financial

Returns

■ Growth orientated

■ Low cyclicality

■ Regulated spaces

■ Differentiated technology

■ Innovative products

■ Niche applications

■ Geographic penetration

■ Ability to manage

■ Synergy potential

■ ABM implementation

■ ROIC > Cost of capital

■ Strong EBITDA potential

■ Recurring revenue

■ EPS accretion

Recent Acquisitions

Acquired: Mar 2021

Price: ~C$260mm

Acquired: Jun 2021

Price: US$84mm

Other Acquisitions KMWEV micro assembly solutionsAcquired: Nov 2018

End Market Exposure

✓ Life Sciences

✓ Food

✓ Life Sciences

12

Capital Allocation Focused on Expanding Positions in Regulated Markets & Compounding Growth Through M&A

MARCOFood yield control solutionsAcquired: Dec 2019

Acquired: Feb 2019

Price: €113mm

inimcoDigital and analytic solutionsAcquired: Nov 2020

IAPProcess Automation solutionsAcquired: Oct 2019

Building a track record of successfully integrating acquisitions

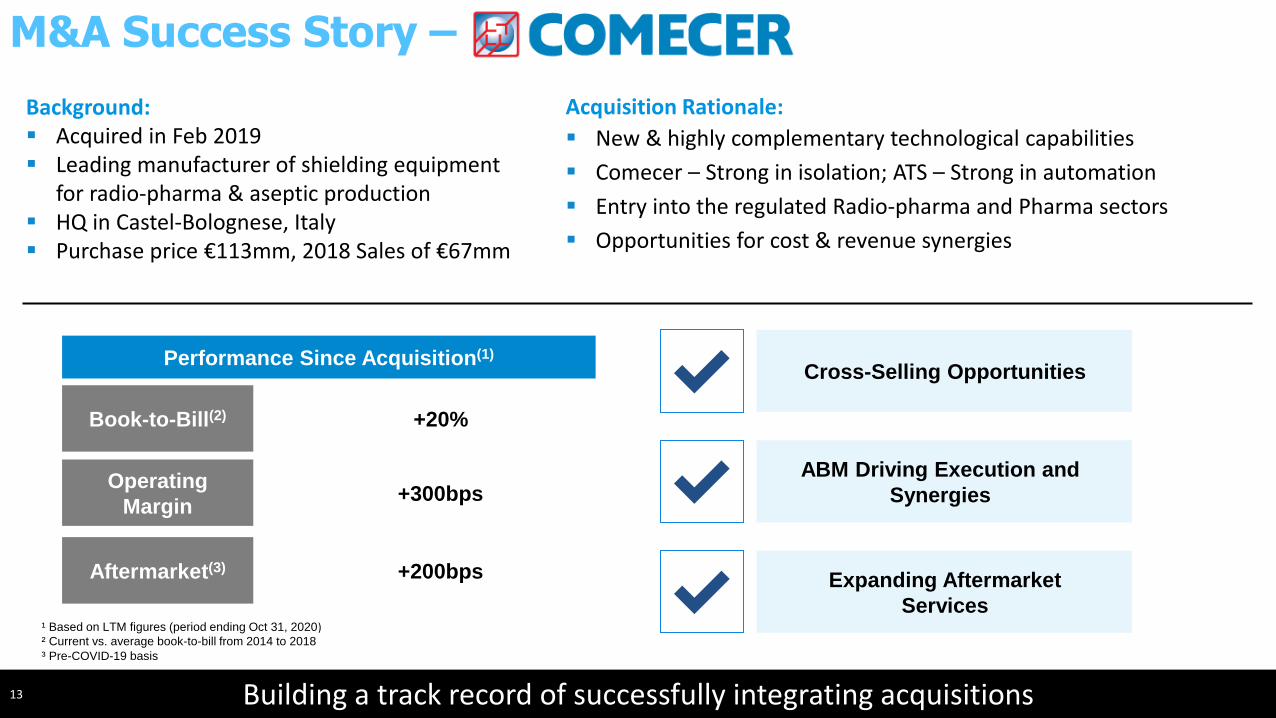

M&A Success Story –

13

Background:▪ Acquired in Feb 2019 ▪ Leading manufacturer of shielding equipment

for radio-pharma & aseptic production ▪ HQ in Castel-Bolognese, Italy ▪ Purchase price €113mm, 2018 Sales of €67mm

Acquisition Rationale:

▪ New & highly complementary technological capabilities

▪ Comecer – Strong in isolation; ATS – Strong in automation

▪ Entry into the regulated Radio-pharma and Pharma sectors

▪ Opportunities for cost & revenue synergies

¹ Based on LTM figures (period ending Oct 31, 2020)² Current vs. average book-to-bill from 2014 to 2018

³ Pre-COVID-19 basis

Performance Since Acquisition(1)

Cross-Selling Opportunities

ABM Driving Execution and

Synergies

Expanding Aftermarket

Services

✔

✔

✔

Book-to-Bill(2)

Operating

Margin

Aftermarket(3)

+20%

+300bps

+200bps

Platform acquisition in the highly regulated Food & Beverage market

Recent Acquisition of CFT is the Next Step in Executing ATS’ M&A Strategy

14

Linear Motion

SymphoniTM

IIOT

COVID-19

ATS Innovation Centre

Advisory Council oversight

▪ CFT Group is a global supplier of processing and packaging automation equipment

▪ Strongly positioned in attractive fresh produce sorting, processing, and packaging niches

▪ Adds complementary technologies that can be combined to create unique market offerings

▪ Attractive deal economics with strong synergy potential

▪ Purchase Price: €4.60 per share, Enterprise value €166mm (~C$260mm)

▪ Transaction Close: March 2021

Growing business focused on attractive markets

CFT Overview

15

▪ Established in 1945 and based in Parma, Italy

▪ Global supplier of processing and packaging equipment to

the Food & Beverage industry

▪ Leading brands in attractive market segments

▪ Global operations with 8 facilities in Italy, Spain, Germany

and Ukraine

▪ 900+ employees

€170 €189

€209 €226

€254

2015 2016 2017 2018 2019

North America

23%

Rest of Europe

23%Italy18%

Africa16%

Asia13%

Other7%

(1)

Diversified Customer & Revenue Base

Attractive Revenue Profile

Figures in Millions

Single

Machines

30%

Completed Lines

50%

Aftermarket

20%

Business Overview

¹ Other includes Central & South America (6%) and Oceania (1%)

Strong Brand Portfolio

Note: CFT financial information presented herein is for illustrative purposes only & has been derived solely from publicly available

information of CFT & includes certain adjustments. As a result, CFT's EBITDA is not directly comparable to ATS' EBITDA/Adj. EBITDA

and is not indicative of anticipated ATS EBITDA/Adj. EBITDA if acquisition is consummated. Pro Forma Leverage should not be relied

upon as reflective of what actual leverage of ATS would have been if acquisition had occurred at beginning of relevant period.

Numerous levers to drive significant value creation

Compelling Strategic Rationale

16

▪ Platform acquisition into attractive Food & Beverage market

▪ Technological leadership in niche market areas

▪ 140 patents

▪ Access to multiple elements of the value chain, creating cross-selling opportunities

▪ Synergies through technology sharing and joint development

▪ Opportunities to significantly enhance margins

▪ Application of ATS Business Model to drive supply chain and operational synergies

Strategic Rationale Selected Synergy Opportunities

Material

Handling

ATS automation expertise

to accelerate CFT's

robotics development

Optical Sorting

and Inspection

MARCO and Raytec’s

commercial overlap drives

customer opportunities

Liquid Filling

Leverage CFT aseptic

filling across multiple ATS

platforms

Drive Continuous Improvement Mindset

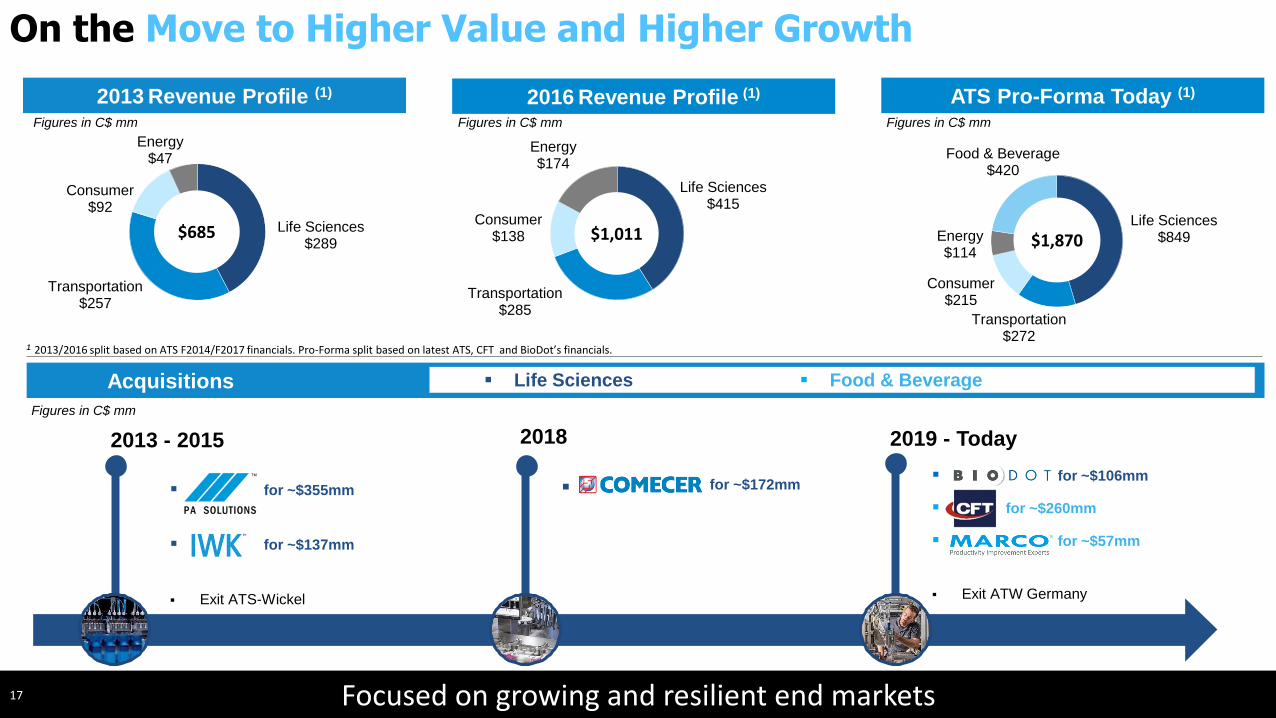

2013 Revenue Profile (1) 2016 Revenue Profile (1) ATS Pro-Forma Today (1)

Figures in C$ mmFigures in C$ mmFigures in C$ mm

Focused on growing and resilient end markets

On the Move to Higher Value and Higher Growth

17

▪ for ~$355mm

▪ for ~$137mm

▪ Exit ATS-Wickel

■ for ~$172mm▪ for ~$106mm

▪ for ~$260mm

▪ for ~$57mm

▪ Exit ATW Germany

2013 - 2015 2018

¹ 2013/2016 split based on ATS F2014/F2017 financials. Pro-Forma split based on latest ATS, CFT and BioDot’s financials.

2019 - Today

Acquisitions ▪ Life Sciences ▪ Food & Beverage

Life Sciences$289

Transportation$257

Consumer$92

Energy$47

$685

Life Sciences$415

Transportation$285

Consumer$138

Energy$174

$1,011Life Sciences

$849

Transportation$272

Consumer$215

Energy$114

Food & Beverage$420

$1,870

Figures in C$ mm

$1,011$1,115 $1,254

$1,430 $1,430

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2017 2018 2019 2020 2021

$1,134$1,182

$1,408$1,468 $1,626

$0

$500

$1,000

$1,500

$2,000

2017 2018 2019 2020 2021

$112

$133

$162$195 $201

11.0%

12.0%

12.9%13.6%

14.0%

10.0%

12.5%

15.0%

17.5%

20.0%

$0

$50

$100

$150

$200

$250

$300

$350

2017 2018 2019 2020 2021

Adj. EBITDA % Margin

Supported by strong balance sheet

Strong Track Record of Revenue Growth and Margin Expansion, with Low Capex Requirements

18

1 Adjusted EBITDA is adjusted for items excluded from management’s internal analysis of operating results. ² Includes capex and acquisition of intangibles.

Revenues (C$ mm) Order Bookings (C$ mm)

Capex² (C$ mm)Adj. EBITDA1 (C$ mm)

+9.1% CAGR

+15.8 % CAGR

+9.4% CAGR

$18

$26

$41

$57

$32

$0

$10

$20

$30

$40

$50

$60

$70

2017 2018 2019 2020 2021

Growth capex in F2019/20; LT capex ~2-3% of Revenues

$639 $656 $633

$377

$776

$287$330

$225

$359

$188

$0

$200

$400

$600

$800

$1,000

2017 2018 2019 2020 2021

Cash Available Credit

$110

$144

$230

$194

$348

$0

$50

$100

$150

$200

$250

$300

$350

2017 2018 2019 2020 2021

8.0% 8.3%7.1%

12.3%

6.0%

0%

5%

10%

15%

20%

2017 2018 2019 2020 2021

Supported by strong balance sheet19

0.4x

-0.1x

0.8x

1.6x 1.6x

-0.4x

0.0x

0.4x

0.8x

1.2x

1.6x

2.0x

2017 2018 2019 2020 20211 FCF defined as earnings from operations less capex less acquisition of intangibles. 2 Adjusted EBITDA is adjusted for items excluded from management’s internal analysis of operating results.

2x-2.5x Target Range (3x-4x for Acquisitions)

Working Capital as a % of Revenues Cumulative FCF Since 20171 (C$ mm)

Historical Leverage (Net Debt/Adj. EBITDA2)Liquidity (C$ mm)

Strong Track Record of Revenue Growth and Margin Expansion, with Low Capex Requirements

Target Range of <15% of Sales

Appendix: Reconciliation of Non-IFRS Measures to IFRS Measures

20

Notice to reader: Non-IFRS measures and additional IFRS measuresThroughout this presentation management uses certain non-IFRS measures to evaluate the performance of the Company. The terms “adjusted EBITDA”, “adjusted EBITDA margin”, “non-cash working capital”, “Order Bookings” and “Order Backlog” do not have any standardized meaning prescribed within IFRS and therefore may not be comparable to similar measures presented by other companies. Such measures should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Adjusted EBITDA is defined as earnings from operations excluding depreciation and amortization (which includes amortization of intangible assets and right-of-use assets) before items excluded from management’s internal analysis of operating results, such as amortization expense of acquisition-related intangible assets, acquisition-related transaction and integration costs, restructuring charges, and certain other adjustments which would be non-recurring in nature (“adjustment items”). Adjusted EBITDA margin is an expression of the Company’s adjusted EBITDA as a percentage of revenues. Non-cash working capital is defined as the sum of accounts receivable, costs and earnings in excess of billing on contracts in progress, inventories, deposits, prepaids and other assets, less accounts payable, accrued liabilities, provisions and billings in excess of costs and earnings on contracts in progress. Order Bookings represent new orders for the supply of automation systems, services and products that management believes are firm. Order Backlog is the estimated unearned portion of revenues on customer contracts that are in process and have not been completed at the specified date.

Adjusted EBITDA and adjusted EBITDA margin are used by the Company to evaluate the performance of its operations. Management believes that adjusted EBITDA is an important indicator of the Company’s ability to generate operating cash flows to fund continued investment in its operations. The adjustment items used by management to arrive at these metrics are not considered to be indicative of the business’ ongoing operating performance. Management uses the measure non-cash working capital as a percentage of revenues to evaluate the Company’s management of its investment in non-cash working capital. Management calculates non-cash working capital as a percentage of revenues using period-end non-cash working capital divided by trailing two fiscal quarter revenues annualized. Order Bookings provide an indication of the Company’s ability to secure new orders for work during a specified period, while Order Backlog provides a measure of the value of Order Bookings that have not been completed at a specified point in time. Both Order Bookings and Order Backlog are indicators of future revenues the Company expects to generate based on contracts that management believes to be firm. Management believes that ATS shareholders and potential investors in ATS use these additional IFRS measures and non-IFRS financial measures in making investment decisions and measuring operational results.

A reconciliation of Order Bookings and Order Backlog to total Company revenues are contained in this presentation. A reconciliation of adjusted EBITDA to net income, is contained in this presentation.

Appendix: Reconciliation of Non-IFRS Measures to IFRS Measures

Measure (C$ mm) F2017 F2018 F2019 F2020 F2021

Adjusted EBITDA 111.7 133.3 161.9 195.1 200.7

Restructuring charges 2.3 11.2 - 26.6 14.3

Share purchase allowance 2.9 - - - -

Gain on sale of facility - - - - (5.3)

Contingent consideration adjustment - - - - (5.6)

Acquisition-related transaction costs - - 4.7 1.5 6.7

EBITDA 106.5 122.1 157.2 167.0 190.6

Less: depreciation and amortization expense

34.6 36.6 42.4 71.4 71.0

Earnings from operations 71.9 85.5 114.8 95.6 119.6

Less: net finance costs 25.6 23.8 20.9 28.1 40.1

Less: provision for income taxes 11.3 14.5 23.1 14.6 15.4

Net income 35.0 47.2 70.8 52.9 64.1

21

Measure (C$ mm) F2017 F2018 F2019 F2020 F2021

Opening Order Backlog 652 681 746 904 942

Revenues (1,011) (1,115) (1,254) (1,430) (1,430)

Order Bookings 1,134 1,182 1,408 1,468 1,626

Order Backlog Adjustments

(94) (2) 4 - 22

Ending Order Backlog 681 746 904 942 1,160

Measure (C$ mm) F2017 F2018 F2019 F2020 F2021

Cash and cash equivalents

286.7 330.2 224.5 358.6 187.5

Bank indebtedness (1.4) (2.7) (2.0) (4.6) (1.1)

Current portion of long-term debt

(1.3) (0.4) (18.6) (0.1) (0.1)

Long-term debt (326.0) (315.1) (328.2) (598.0) (430.6)

Net cash (debt) prior to IFRS 16

(42.0) 12.0 (124.2) (244.1) (244.3)

Lease liabilities - - - (62.9) (73.0)

Net cash (debt) (42.0) 12.0 (124.2) (307.0) (317.3)

Measure (C$ mm) F2017 F2018 F2019 F2020 F2021

Net Debt (42.0) 12.0 (124.2) (307.0) (317.3)

Adjusted EBITDA 111.7 133.3 161.9 195.1 200.7

Historical Leverage (Net Debt/Adj. EBITDA)

0.4x -0.1x 0.8x 1.6x 1.6x

22

Appendix: Reconciliation of Non-IFRS Measures to IFRS Measures

Measure (C$ mm) F2017 F2018 F2019 F2020 F2021

Cash flows provided by operating activities

127.9 59.7 127.6 20.3 185.2

Acquisition of property, plant and equipment

(9.9) (19.9) (21.1) (45.4) (21.5)

Acquisition of intangible assets

(8.0) (6.1) (19.8) (11.1) (10.0)

Free Cash Flow 110.0 33.7 86.7 (36.2) 153.7

Cumulative Free Cash Flow 110.0 143.7 230.4 194.2 347.9

Measure (C$ mm) F2017 F2018 F2019 F2020 F2021

Accounts receivable 166.1 213.0 222.2 294.8 294.1

Net contract assets 48.2 69.0 52.4 113.8 54.5

Inventories 47.9 58.5 68.0 68.4 135.0

Deposits, prepaids and other assets

16.1 22.5 28.7 31.2 37.8

Accounts payable and accrued liabilities

(183.8) (246.4) (262.0) (292.4) (400.2)

Provisions (14.1) (20.9) (13.9) (32.1) (29.0)

Working Capital 80.4 95.7 95.4 183.7 92.2

Revenue run rate = (prior + current quarter) x 2

1,006.1 1,152.0 1,340.0 1,498.6 1,539.3

Working Capital % 8.0% 8.3% 7.1% 12.3% 6.0%