)

\ )

INTERNATIONAL BUSINESS STRUCTURES

These materials were prepared by Timothy Wach of Smith Lyons, Toronto, Ont. for the Saskatchewan LegalEducation Society Inc. seminar, "Accessing the Global Market from Saskatchewan", September 1997.

)

\jI

TABLE OF CONTENTS

INTERNATIONAL BUSINESS STRUCTURES - AN OVERVIEW •...•.•.... 1

(i) Sales of Goods 1(ii) Provision of Services •..........••.....•......• 2(iii) Distribution Relationships . . . • . . . . . • . . . . . . • . . . . . .. 3(iv) Partnerships and Joint Ventures 4(v) Foreign Corporations ........•..........•.....• 5

CANADIAN TAXATION OF FOREIGN BUSINESS STRUCTURES . . . . . . . . .. 6

(i) Foreign Affiliates . . • . . . . . . . . . . . . . . . • . . . . . . . • .• 7(ii) Controlled Foreign Affiliates . . . • . • . . . . . . . . . • . . . . •• 7(iii) FAPI and Surplus Accounts ....•..•.......•..... 10(iv) Flow-Through of Surplus Accounts, Order of

Distributions and "Dividend Mixers" ............•.. 11(v) "Sandwich" Structures • . • • . . . . . • . • • • . . • . . . • . • .. 13

TAX-FAVOURED FOREIGN JURISDICTIONS .........•..•......•. 15

TAX TREATIES . . • . . . . . . . . . . . . . . • . . . . . . . . . . . . . . . . . . . . • .. 16

TRANSFER PRICING 17

CASE STUDIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 20

(i) The Computer Software Corporation .....•..•.•..•.. 20(ii) The American Supply Contract. . • . . . . . . . . . . . . . . • .• 21(iii) The Russian Supply Contract • . • . • . . . . . . . • . . . • . • •. 24

SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 25

INTERNATIONAL BUSINESS STRUCTURES

Timothy S. Wach

SMITH LYONS

The structuring of international business operations will be affected by many

different factors. These will include the type of business that you are engaged in, the

business and commercial exigencies of that,business and of the foreign jurisdiction in which

you wish to do business, legal restrictions imposed within that jurisdiction, foreign and

Canadian tax planning opportunities, the stage of development of your foreign operations

and finally, of course, costs. There will be considerable differences, for example, in how

to approach the operation of a uranium mine in Kazakstan, the expansion_ of software sales::;.

into Europe or the Far East, or the establishment of a vehicle for CanadUm pension plans

and RRSPs to invest in U.S. commercial real estate.

INTERNATIONAL BUSINESS STRUCTURES - AN OVERVIEW

There are a number of basic business structures that can be adopted in establishing or

expanding business operations in a foreign jurisdiction. These are briefly described below.

It should always be borne in mind that although a particular structure may be quite familiar

to western business people, and might be the most logical structure in particular

circumstances from our perspective, the structure may be quite novel for foreign business

associates or governments who may simply be unwilling to adopt the structure because they

are unfamiliar with it.

(i) Sales of Goods

Likely the simplest structure for business operations in a foreign jurisdiction is to simply

sell goods to persons in that jurisdiction. If your business is such that you may generate

2

orders for goods from that jurisdiction-without having -any·· substantial presence there,' then

your business relations with that jurisdiction will likely be fairly simple. However, you will

still have to address some legal and tax questions, such as:

(a) are any special permits needed to import goods into that jurisdiction?

(b) is the level of my activity in that jurisdiction so high that I may be considered

to be carrying on business there? If so, are any special permits or licences

needed and am I exposed to income tax liability in that jurisdiction? Is there

any tax treaty protection available to shelter me from such foreign income tax

liability? Do I have any foreign income tax reporting requirements?')

(c) what impoq duties or VAT or GST type taxes are payable upon importation

of goods?

These will be foreign issues for which you will likely require counsel from foreign advisers.

The necessity for such counsel should never be underestimated.

(ii) Provision of Services

The next level up from the pure sale of goods is likely the provision of services to non

residents of Canada. In some cases, this may be a simpler structure than if goods are sold

to non-residents. For example, if consulting services are provided without either party

crossing a border (an example would be legal services provided by telephone, electronically

and by mail), few issues will arise.

However, as soon as individuals begin to cross borders, the potential for complications

should not be underestimated. For example, what immigration restrictions or visa

requirements will be faced? An example is a case in respect of which my firm has been

3

consulted by a client which is a Canadian corporation that is part of a multi-national group

and which has a U.S. sister corporation. The group wished to integrate the sales efforts of

the Canadian and U.S. corporations in certain geographic areas and businesses in order to

take advantage of the different strengths of their respective sales and technical support

teams. However, even in this relatively straightforward fact-situation, the movement of

personnel across the border raised issues relating to (i) the need for business visas for the

individuals involved and (ii) income tax exposure for the individuals in the other

jurisdiction, including the need to make tax filings in the U.S. for Canadian residents

crossing the border to do business, as well as (iii) potential income tax exposure for the

corporations in the other jurisdiction.

(iii) Distribution Relationships

Attempting to do business in a foreign jurisdiction can often expose cultural differences

between Canada and that jurisdiction. This, together with language differences, legal

requirements and other difficulties of carrying on business in a foreign country can often

mean that there will be a need for a local "partner" in the foreign jurisdiction. One such

arrangement can be a distributorship relationship. Such a relationship can also permit you

to access the business networks of the foreign distributor. If the foreign distributor has

experience in working with others coming into its country from abroad, then the distributor

should be familiar with many of the licensing, taxation and other issues that can arise for

a foreigner doing business in that country.

Another advantage of a distributorship arrangement is that, in general, you will not be

considered to be carrying on business in the foreign jurisdiction. This will usually mean

that you will not be exposed to foreign income taxation and will also likely obviate the need

for any licences or other governmental permits in order to carry on business there.

However, this type of arrangement usually results in less control of the operations in that

jurisdiction and can be costly in terms of the percentages of sales that must be ceded to the

4

foreign distributor (although, presumably, one would choose to adopt this form of business

relationship only if it is expected to be more efficient and less costly than trying to carry

on business directly in the foreign jurisdiction).

However, some foreign tax exposure can arise, depending on the form of the arrangements

with the foreign distributor. For example, in one case a client of ours wished to enter into

an arrangement in which a local manufacturer and distributor both manufactured and

distributed our client's products for sale in the European Community. Our client would

receive a percentage of sales (in dollar terms) that the foreign distributor made. This gave

rise to concerns relating to exposure of our client for foreign withholding tax because the

.returns that it would be getting would likely be characterized as royalties for tax purposes

in the foreign jurisdiction. Compounding the concerns in this regard waS the fact that the

client was a Canadian-controlled private corporation which took maximum advantage of the

small business deduction and paid out its income in excess of $200,000 each year as bonuses

to its principal owner/managers. Accordingly, the foreign withholding tax would be an

absolute cost because there would have been very little foreign tax credit relief in Canada

for the foreign tax (largely because the corporation would be paying the foreign withholding

tax while the tax in Canada would be paid at the owner/manager level because of the bonus

arrangements). This necessitated a restructuring of the relationship with the foreign

manufacturer and distributor in order to minimize the potential for the payments to the

Canadian corporation being characterized as royalties in the foreign jurisdiction.

(iv) Partnetships and Joint Ventures

The term "partnership" is often used by lawyers and business people alike in a very loose

sense to include relationships such as distributorships, joint ventures and joint venture

corporations, and not simply for legal partnership relationships. In this paper, unless

otherwise indicated, any references to a partnership will mean a legal partnership, and any

5

other form ofjoint business arrangement such as those previously mentioned will be referred

by that other term.

From my own experience, partnership structures for foreign business are rarely seen. There

are a number of likely reasons for this, not the least of which are Canadian and foreign

income taxation considerations. One obvious concern would be that if the Canadian

corporation participates in a foreign partnership directly, rather than through a foreign

subsidiary, then more often than not it will be exposing all of its business and assets to

potential liabilities from the partnership activities, which normally is not wise given the

uncertainties of carrying on business in many foreign lands with a foreign partner. This can

often be avoided if the foreign partnership participation is effected through a subsidiary

corporation.

As well, as will be seen later, it is often beneficial from a Canadian income tax perspective

to carry on foreign operations through one or more foreign subsidiary corporations if those

operations will be characterized as the carrying on of an active business in a foreign

jurisdiction for Canadian tax purposes. In addition, if a Canadian corporation carries on

business directly in a foreign jurisdiction, such as it would through a direct participation in

a partnership relationship, then it may be required to file tax returns in the foreign

jurisdiction reflecting all of its revenues and income, not only the revenues and income

derived from the foreign jurisdiction. This will often be something you would prefer to

avoid. If a foreign subsidiary is used to participate in the partnership, then the foreign

sourced revenues and income can be isolated in the foreign subsidiary.

(v) Foreign Corporations

Finally, it may be necessary or preferable to carry on your foreign operations through a

foreign subsidiary corporation. This may be dictated by local law in the jurisdiction that

you have your foreign operations, it may be preferable in order to isolate the risks and

6

potential liabilities associated with the foreign business, or it may be preferable from a tax

planning perspective. A wholly-owned foreign corporation may be the vehicle through

which you participate in a foreign partnership or joint venture, or it may be the joint

business vehicle itself, with you and -your foreign business associates owning shares in the

foreign corporation.

CANADIAN TAXATION OF FOREIGN BUSINESS STRUCTURES

The Canadian tax treatment of most of the international business structures outlined above

is fairly straightforward. It is generally well known that a resident of Canada, whether an

individual or a corporation, is taxable in Canada on its world-wide income. Accordingly,

if a resident of Canada participates directly in a foreign business venture, either by direct

sales of goods or provision of services, including direct sales through distribution

relationships, or by direct participation in a foreign joint venture or partnership, the

Canadian resident will be required to include the full amount of any income derived from

the foreign business in its income for Canadian tax purposes. In general, foreign tax credits

will be available in Canada for the foreign income tax paid on the foreign sourced income

(although care must be taken in this regard to ensure that such things as differences between

the Canadian and foreign tax systems in terms of timing of income and expense recognition

do not result in a loss of foreign tax credits in Canada).

On the other hand, if the foreign business venture is carried on through a foreign subsidiary

corporation, then the tax treatment for a Canadian shareholder of the income of the foreign

corporation will depend on the extent of the shareholdings of the Canadian in the foreign

corporation and the characterization of the income earned by the foreign corporation.

7

(i) Foreign Affiliates

The first issue that must be addressed in considering the tax treatment of the income of a

foreign corporation is whether the corporation is a "foreign affiliate" of the Canadian

shareholder. In very general terms, a foreign corporation will be a foreign affiliate of a

Canadian shareholder if the Canadian holds at least I % of the shares of any class of the

foreign corporation, and the Canadian together with persons related to the Canadian hold

at least 10% of the shares of any class-ofthe-corporation;l

(ii) Controlled Foreign Affiliates

If a foreign corporation is a foreign affiliate of a Canadian shareholder, the next issue for

determination is whether the foreign corporation is a "controlled foreign affiliate" of the

Canadian shareholder. A foreign corporation will be a controlled foreign affiliate of a

Canadian shareholder if it is a foreign affiliate of the Canadian shareholder and it is

controlled by

(i) the Canadian, a person or persons who do not deal at arm's length with the

Canadian, or the Canadian and one or more non-arm's length persons together, or

(ii) four or fewer persons resident in Canada (who can be unrelated and deal at

arm's length with the Canadian) or, the Canadian and four such people resident in

Canada.2

See the definition of Rforeign affiliateRin subsection 95(1) of the Income Tax Act (Canada) (theRTax ActR) and of Rdirect equity percentageRand Requity percentageRin subsection 95(4) of the Tax Act. Thedetermination of foreign affiliate status of a foreign corporation is actually slightly more complicated, involvingdeterminations of Rdirect equity percentagesRand Requity percentagesR• In general, however, if a Canadian holds,directly or indirectly, at least 10% of the shares of a class of a foreign corporation, the foreign corporation willbe a foreign affiliate of the Canadian shareholder.

2 See the definition of Rcontrolled foreign affiliateRin subsection 95(1) of the Tax Act.

8

For these purposes, "control" means legal control, or ownership of shares of the corporation

carrying 50% plus one of the votes for the board of directors of the corporation.

Following are some examples of foreign affiliate and controlled foreign affiliate status. In

each case, it is assumed that each corporation has only one class of shares.

Example 1.

ForeignCanadian UnrelatedCorporation corporation

50% 50% <)

ForeignOpeo

In this example, Foreign Opco is a foreign affiliate of Canadian Corporation, but is not a

controlled foreign affiliate.

Example 2.

Foreign ForeignCanadian Unrelated Unrelatedcorpo~ation corporation 1 Corporation 2

33% 33% 33%

I Foreign Opeo I

)

9

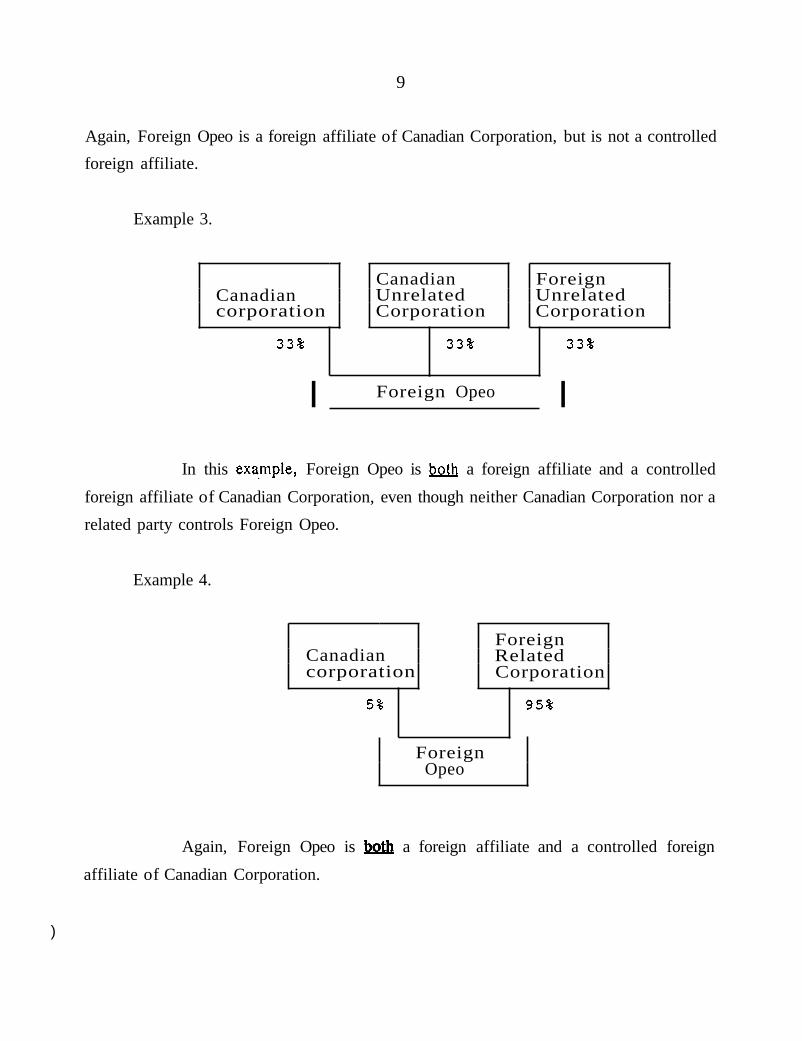

Again, Foreign Opeo is a foreign affiliate of Canadian Corporation, but is not a controlled

foreign affiliate.

Example 3.

Canadian ForeignCanadian Unrelated Unrelatedcorporation Corporation Corporation

33% 33% 33%

I Foreign Opeo I

In this eX3:mple, Foreign Opeo is hQth a foreign affiliate and a controlled

foreign affiliate of Canadian Corporation, even though neither Canadian Corporation nor a

related party controls Foreign Opeo.

Example 4.

ForeignCanadian Relatedcorporation Corporation

5% 95%

ForeignOpeo

Again, Foreign Opeo is hQ1h a foreign affiliate and a controlled foreign

affiliate of Canadian Corporation.

10

(iii) FAPI and Surplus Accounts

The status of a foreign corporation as a foreign affiliate or a controlled foreign affiliate of

a Canadian resident shareholder gives rise to potential beneficial and detrimental Canadian

tax results. First, if a foreign corporation is a controlled foreign affiliate of a Canadian

shareholder, the Canadian shareholder will be required to include in its income each year

its share of the foreign accrual property income ("FAPI") of the foreign corporation,

whether or not that income is distributed out of the foreign corporation.3 The FAPI of a

foreign corporation will include most passive income of the corporation, as well as income

from certain other sources that is deemed to be FAPI.4

On the other hand, foreign affiliate (including controlled foreign affiliate) status of a foreign

corporation will be advantageous if the foreign corporation earns income from an active

business and the Canadian resident shareholder is a corporation. In this case, the income

of the foreign affiliate from an active business will be characterized as either "taxable

earnings" or "exempt earnings". If the foreign affiliate is resident in a "designated treaty

country"5, then any income of the foreign affiliate from an active business that is allocable

to a designated treaty country will be included in the "exempt earnings" and "exempt

surplus" of the foreign affiliate. Any other income from an active business of a foreign

affiliate resident in a designated treaty country, or any income from an active business of

a foreign affiliate that is resident in other than a designated treaty country, will be included

in the "taxable surplus" of the foreign affiliate.

See subsection 91(1) of the Tax Act, the definition of Wparticipating percentageWin subsection 95(1) ofthe Tax Act and section 5904 of the Income Tax Regulations (the wTax RegulationsW), which prescribe the mannerin which FAPI of a foreign affiliate is allocated to its shareholders.

4 See, for example, the rules in subsection 95(2) of Tax Act which deem income from certain sources suchas from certain insurance, investment and money lending businesses to be FAPI.

See proposed subsection 5907(11) of the Tax Regulations.

)11

Unlike FAPI, taxable earnings and exempt earnings of a foreign affiliate are not taxed

annually in the hands of the Canadian shareholder. Instead, if the Canadian shareholder is

a corporation, then any distribution received by it out of the exempt surplus of the foreign

affiliate is received free of Canadian tax. Distributions received by such a shareholder out

of the taxable surplus of the foreign affiliate are taxed when received, but deductions are

provided in respect of underlying foreign income taxes paid by the foreign affiliate and the

Canadian corporate shareholder on such income.

As outlined above, in order to be included in the exempt or taxable surplus account of a

foreign affiliate, the income of the affiliate must be from an active business. It is worth

noting that income from an active business-of a foreign affiliate is deemed to include any

income of the affiliate for the year "that pertains to or is incidental to that business".6

(iv) Flow-Through of Surplus Accounts, Order of Distributions and "Dividend

Mixers"

As outlined above, in order for a foreign affiliate to generate exempt earnings, it must be

both resident in a designated treaty country and the earnings in question must be allocable

to a designated treaty country. However, if a lower level foreign affiliate generates exempt

surplus and pays a dividend up to an intermediary subsidiary, that dividend will reduce the

exempt earnings of the lower level affiliate and increase that of the intermediary affiliate,

effectively transferring the exempt surplus of the lower level affiliate up to the intermediary

affiliate to the extent of the dividend. Similar treatment is accorded dividends paid out of

the taxable surplus of a lower level foreign affiliate up to a higher level foreign affiliate.?

6 See the definition of "income from an active business" in subsection 95(1) of the Tax Act.

7 See the definitions of "exempt surplus" and "taxable surplus" in subsection 5907(1) of the TaxRegulations.

12

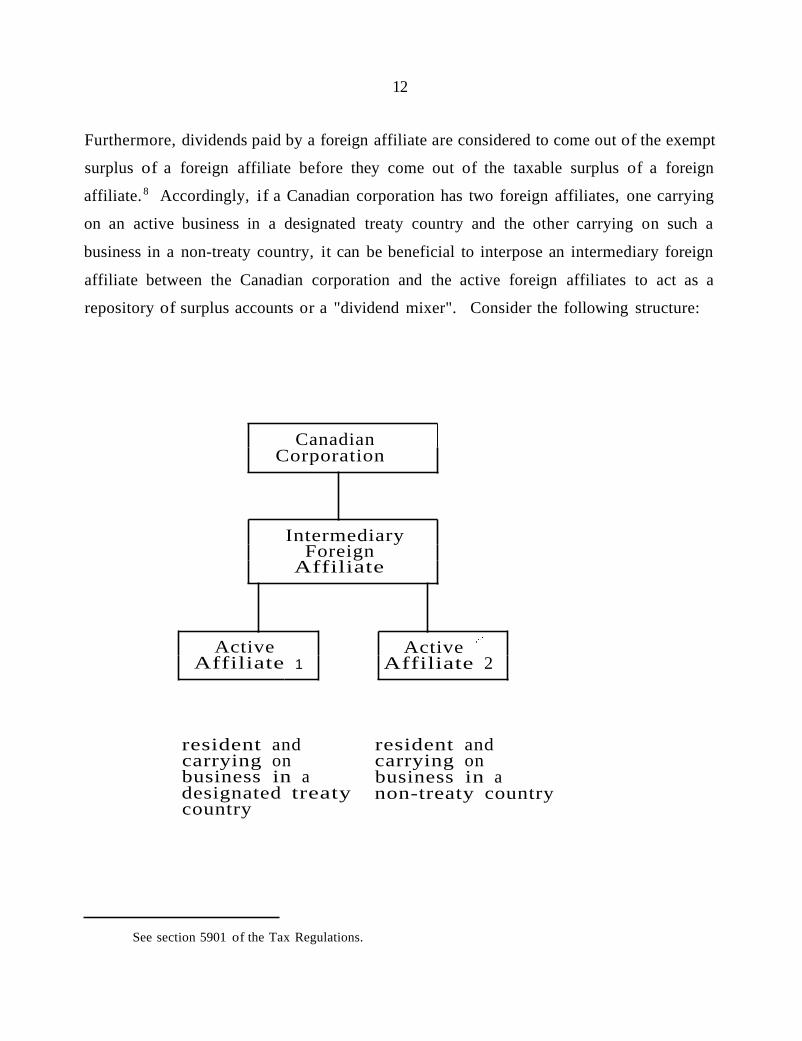

Furthermore, dividends paid by a foreign affiliate are considered to come out of the exempt

surplus of a foreign affiliate before they come out of the taxable surplus of a foreign

affiliate. 8 Accordingly, if a Canadian corporation has two foreign affiliates, one carrying

on an active business in a designated treaty country and the other carrying on such a

business in a non-treaty country, it can be beneficial to interpose an intermediary foreign

affiliate between the Canadian corporation and the active foreign affiliates to act as a

repository of surplus accounts or a "dividend mixer". Consider the following structure:

CanadianCorporation

IntermediaryForeign

Affiliate

Active Active,"

Affiliate 1 Affiliate 2

resident andcarrying onbusiness in adesignated treatycountry

See section 5901 of the Tax Regulations.

resident andcarrying onbusiness in anon-treaty country

)13

In this case, dividends from Active Affiliate 1 can effectively transfer exempt surplus from

Active Affiliate 1 to Intermediary Foreign Affiliate, while dividends from Active Affiliate

2 will transfer taxable surplus up to Intermediary Foreign Affiliate. Dividends from

Intermediary Foreign Affiliate to Canadian Corporation will come first out of the exempt

surplus of Intermediary Foreign Affiliate and only out of the taxable surplus of Intermediary

Foreign Affiliate if its exempt surplus is fully depleted. Accordingly, if the dividends out

of Intermediary Foreign Affiliate never exceed its exempt surplus, then Canadian

Corporation will never be taxable on distributions it receives. This can be achieved if all

of the income earned by Active Affiliate 2 is redeployed in the businesses of it and Active

Affiliate 1. The presence of a "dividend mixer" such as Intermediary Foreign Affiliate

permits this type of flexibility and planning of income and cash flows by collecting exempt

surplus and taxable surplus together in one place, allowing "layers" of exempt surplus to

be put over the taxable surplus. This type of planning would not be possible if Active

Affiliates 1 and 2 were owned directly by Canadian Corporation.

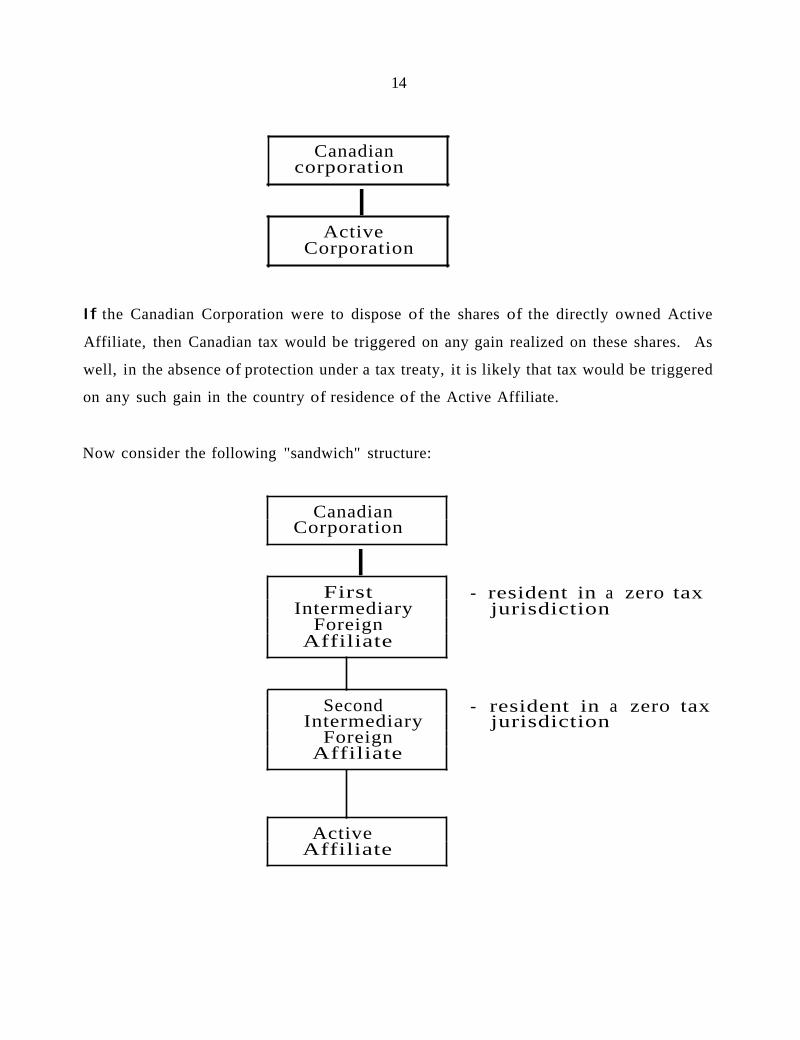

(v) "Sandwich" Structures

As outlined above, the interposition of an intermediary foreign corporation between a

Canadian corporation and a foreign operating affiliate will not alter the character of earnings

and surplus accounts of the foreign affiliate; the character of these amounts will simply flow

up a chain of foreign affiliates. The interposition of such an intermediate will also permit

greater flexibility and planning for a disposition of the foreign operating affiliate.

For example, consider the following simple structure:

14

Canadiancorporation

IActive

Corporation

If the Canadian Corporation were to dispose of the shares of the directly owned Active

Affiliate, then Canadian tax would be triggered on any gain realized on these shares. As

well, in the absence of protection under a tax treaty, it is likely that tax would be triggered

on any such gain in the country of residence of the Active Affiliate.

Now consider the following "sandwich" structure:

CanadianCorporation

IFirst

IntermediaryForeign

Affiliate

SecondIntermediary

ForeignAffiliate

ActiveAffiliate

- resident in a zero taxjurisdiction

- resident in a zero taxjurisdiction

)15

This structure would permit the Canadian corporation to dispose of its interest In the Active

Affiliate by having the First Intermediary Foreign Affiliate sell its shares of the Second

Intermediary Foreign Affiliate. Provided that the shares of the Active Affiliate are

"excluded property"9, then no immediate tax would be triggered if the sale were to be

effected by having the First Intermediary Foreign Affiliate dispose of the shares of the

Second Intermediary Foreign Affiliate. Instead, three-quarters of any gain realized would

be included in the taxable surplus of the First Intermediary Foreign Affiliate while the

remaining one-quarter would be included in the exempt surplus of the First Intermediary

Foreign Affiliate.10 In most cases, foreign capital gains tax in the jurisdiction of the

Active Affiliate is also avoided because the shares being sold are those of the Second

Intermediary Foreign Corporation which is resident in a zero tax jurisdiction, rather than")

of the Active Affiliate that is resident in a taxing jurisdiction.

TAX-FAVOURED FOREIGN JURISDICTIONS

Tax savings can be achieved in certain cases if foreign sourced income from an active

business can be earned in a foreign affiliate and taxed only in the foreign jurisdiction in

which the business is carried on. This is possible if two factors are present: first, the tax

rate in the foreign jurisdiction must be lower than in Canada, and second, the income of the

foreign affiliate from the business must be characterized as exempt earnings for Canadian

tax purposes. As outlined above, in order for a foreign affiliate to generate exempt

9 Pursuant to the definition of "excluded property" in subsection 95(2) of the Tax Act, shares of a foreignaffiliate will be "excluded property" if all or substantially all of the property of the foreign affiliate is used by theforeign affiliate principally for the purpose of gaining or producing income from an active business or is sharesof another foreign affiliate the property of which satisfies this requirement.

10 It should be noted that, pursuant to subsection 93(1.1) of the Tax Act, in these circumstances the gainrealized by the First Intermediary Foreign Affiliate on the disposition of shares of the Second Intermediary ForeignAffiliate will be deemed to have been realized as a dividend to the extent of the exempt surplus of the SecondIntermediary Foreign Affiliate. In this way, the taxable portion of the gain is automatically minimized and a"dividend strip" of the undistributed exempt surplus of the Second Intermediary Foreign Affiliate's exempt surplusis effected.

16

earnings, it must be both resident in a designated treaty country, and its income must be

allocable to a designated treaty country.

While many of Canada's tax treaty partners have tax rates that are lower than those

applicable in Canada, few have tax rates that rival thezero..,rated jurisdictions. However,

there are three countries with which Canada has tax treaties and which are, in most cases,

relatively high tax rate jurisdictions, but which offer incentive tax rates that are significantly

below those of Canada. These jurisdictions are Barbados, which offers a tax rate of 21h %

for "International Business Corporations", Cyprus, which offers a rate of 41,4 % to "offshore

corporations", and Ireland, which offers a rate of 10% to corporations holding certificates

and carrying on certain manufacturing activities, certain other activities within the Shannon

Airport region, or carrying on ·certain financing activities in the Dublin Docklands region.

In addition to the favourable corporate tax rate described above, Cyprus offers an additional

benefit, being a network of tax treaties with Eastern Europe (in particular, Russia and

Ukraine) that provide for significantly reduced withholding tax on payments out of those

countries, such as a nil rate for dividends, interest and royalties. II

TAX TREATIES

The presence of a tax treaty between Canada and the foreign jurisdiction in question will

potentially be of considerable relevance in planning a foreign business structure. This can

range from (i) reducing foreign withholding tax rates on licensing arrangements, to (ii)

shielding a Canadian resident from foreign tax (which is relevant if the operations of the

Canadian resident operations in the foreign jurisdiction are significant enough to give rise

to tax liability under the foreign law, but not under the relevant treaty), to (iii) giving the

II It is understood, however, that certain of these treaties, such as the Cyprus-Russia Treaty, are currentlybeing renegotiated.

)17

foreign country "designated treaty country" status for Canadian tax purposes so that a

foreign affiliate in that country can generate exempt surplus.

Canada has in place approximately 60 tax treaties with more in the process of being

negotiated. In fact, Canada's tax treaty network is in a constant state of change, with new

treaties being entered into and protocols to old treaties being entered into on a regular basis.

While the presence of a tax treaty can give rise to the benefits outlined above, it can also

complicate international tax structuring. For example, the use of a "dividend mixer" as

described earlier usually involves having a Canadian corporation hold shares of an active

foreign affiliate through a corporation incorporated in a low tax jurisdiction. However,

there are very few low tax jurisdictions that have well developed tax treaty networks.

Accordingly, using this type of structure can mean giving up the benefits of the tax treaty

between Canada and the jurisdiction of the active foreign affiliate.

One exception to this is the Netherlands. The Netherlands is a high tax rate jurisdiction

with a sophisticated tax treaty network which also offers low tax rates for holding companies

and financing companies in certain circumstances. .It is sometimes possible to interpose a

Dutch subsidiary between the holding company in a tax haven and the active company in

the high tax rate Jurisdiction. These structures are expensive to establish and maintain

(among other things, a tax ruling from the Dutch tax authorities must be obtained), but in

the right circumstances, they can yield significant tax benefits.

TRANSFER PRICING

Any non-arm's length relationship that gives rise to tax liability in more than one

jurisdiction will give rise to transfer pricing concerns. This will be the case whether the

Canadian resident is carrying on business directly in the other jurisdiction or if it does so

18

through a subsidiary corporation. In each case the taxation authorities in both Canada and

the other jurisdiction will be concerned that income is not being shifted away from their

jurisdiction, or that expenses are not being shifted into their jurisdiction. Of course, it will

ordinarily be the jurisdiction with the higher tax rate that will have the greatest interest in

these issues, which will usually be Canada. However, one should never underestimate the

interest of the IRS or other taxing authorities in these issues. The area of transfer pricing

has been an area of particular concern for both Revenue Canada and the IRS (and many

other taxation authorities) for a number of years.

In very general terms, under the transfer pricing policies of most taxing jurisdictions and

the principles developed by the Organization for Economic Co-operation and Development,

the Canadian resident and the other party, whether a separate entity or a foreign branch of

the Canadian entity, will be required to deal with one another as if they are separate entities

dealing at arm's length. In other words, taxing authorities will wish to ensure that prices

charged between related parties on cross-border transactions are the same as those that

unrelated parties would have changed in similar circumstances. Various methods for the

determination of appropriate transfer prices, such as the "comparable uncontrolled price",

the "cost plus" and the "resale price" methods, as well as several others, are suggested by

Revenue Canada and the OBCD.

Under proposals included in the most recent federal budget, Canadian taxpayers will also

be required to prepare contemporaneous documentation supporting transfer pricing policies

and practices that they adopt. It is not yet clear exactly what types of documentation will

be required or what the penalties for failing to do so will be, but it is clear that Canadian

taxpayers will no longer be able to prepare documentation supporting their transfer pricing

policies and practices after Revenue Canada has initiated an audit of the taxpayer's non

arm's length cross-border transactions.

19

Two other approaches are also available. First, it is possible to approach Revenue Canada

to obtain an advance pricing agreement. 12 This is, in effect, an advance blessing by

Revenue Canada of a transfer pricing policy or practice which the taxpayer can then rely

upon for future non-arm's length transactions. Such an agreement can be made on a

unilateral basis, involving only the applicant and Revenue Canada, although Revenue Canada

encourages bilateral applications that also involve the relevant foreign taxation authority.

However, developing an advance pricing agreement apparently can take up considerable

resources in terms of staff time and expense.

Secondly, in some cases, notably the U.S., it is possible to have the Competent Authorities

of the two jurisdictions (in the case of Canada and the U.S. this obviously would be

Revenue Canada and the IRS) resolve transfer pricing issues and come to agreement on

appropriate transfer prices. The ability to make a Competent Authority application is to be

found under an applicable tax treaty (in the case of the U.S., this would be found in Article

IX of the Canada-U.S. Income Tax Convention, 1980). Although the taxpayer loses control

of the process in these circumstances, the taxpayer also effectively eliminates the potential

for conflicting resolutions of transfer-pricing issues on opposite sides of the border)3

12 See Revenue Canada's Information Circular 94-4, RInternational Transfer Pricing: Advance PricingAgreements (APA)-.

13 Although the tax treaty between Canada and the U.S. does not obligate the taxing authorities to come toa mutual resolution of issues submitted to them and they formally reserve the right to come to their ownconclusions, Revenue Canada has indicated that they have yet to fail to come to an agreement with the IRS onissues submitted to them.

20

CASE STUDIES

(i) The Computer Software Corporation

"Softco" is a Canadian software producer with worldwide sales. Softco wished to increase

its sales into both Europe and the Far East. However, Softco, at least initially, did not have

the human or financial resources to plunge directly into these markets. Softco also faced

language and cultural barriers14 to entry into these markets and concerns relating to

importation of its goods into various countries (such as dealing with VAT compliance). In

order to deal with all of these issues, as well as to access local software distribution

networks, Softco entered into distribution agreements with software distributors in each of

the European and Asian markets that it sought to enter. These arrangements reflected the

commercial norms for each market.

The arrangements with local distributors worked well for Softco, its business flourished in

the Canadian and foreign markets, and its human and financial resources grew. Over time

the management of Softco began to consider the possibility of establishing an offshore sales

subsidiary.

Consideration was given to doing so in Barbados, where designated treaty status (so that the

sales subsidiary could generate exempt surplus) and the 2% % tax rate for International

Business Corporations, as well as a highly literate work force and good infrastructure (in

terms of banking, accounting, legal and other support as well as telecommunications), make

doing business attractive. However, Softco's management decided that Ireland would be a

more favourable jurisdiction, particularly for sales into Europe. Ireland similarly offered

a highly literate workforce and good infrastructure as well as attractive tax advantages

(being designated treaty country status and an incentive 10% tax rate until 2010, because

14 These are significant in the software business when one considers the need, for example, for manuals andtechnical support in the local language.

21

Softco's Irish subsidiary operates in the Shannon Airport region. However, Ireland also

offered more convenient access to the European market, both in terms of legal, VAT and

import duty considerations (because Ireland is a member of the European Community) and

in terms of travel to Canada and Europe from Ireland. Softco has successfully operated its

European and Asian sales through its Irish subsidiary for several years now (although it

maintains the relationships with the foreign distributors), generating exempt surplus through

that affiliate, and has slowly been moving its software development into its Irish subsidiary.

Softco's U.S. structure should also be mentioned briefly. As can be expected, Softco does

not face the same language and cultural barriers in the U.S. market as it does in Europe and

Asia. As well, Softco's personnel are familiar with the U.S. market and able to sell into

that market. Accordingly, Softco does not have the same need to access the assistance of

a local distributor for the U.S. market as it does for its other markets. However, Softco

was concerned about perceived U.S. xenophobia (principals of Softco, one of whom was a

U.S. citizen had this concern). Accordingly, Softco established a U.S. subsidiary, with a

U.S. address, to fulfil U.S. orders (as well as an 800 number for technical support, which

number is not identifiable as being Canadian). Because the U.S. subsidiary is subject to

lower taxes in the U.S. than Softco is in Canada, the U.S. subsidiary structure also

generates exempt surplus and tax savings for Softco.

(ii) The American Supply Contract

"Canco" is a Canadian designer and manufacturer of specialty marketing products (signage

and similar products for retailers). Canco secured a contract with a major American retailer

to supply to it marketing products for its outlets in most of the U.S. Canco does not have

the manufacturing facilities necessary to produce the goods in question. Accordingly, Canco

entered into a sub-manufacturing and supply contract with an American manufacturer. This

contract had to encompass many commercial and business issues, such as pricing, receipt

22

of orders from the American retailer, billing and collection, dispute resolution, and licensing

of technology. The relationship also gave rise to significant tax issues.

First, Canco had to be concerned about being subject to U.S. income tax. If the

relationship between Canco and the sub-manufacturer were such that the sub-manufacturer

accepted orders on behalf of Canco (for example, one of the initial proposals would have

had the retailer placing orders directly with the sub-manufacturer, who would have had

authority to accept such orders on behalf of Canco, which could raise concerns about Canco

having effectively connected income in the U.S.), then Canco could be considered to be

carrying on business in the U.S. through a permanent establishment in the U.S. This would

subject Canco to income tax in the U.S. on the income reasonably attributable to that. ~

business.

While that would often not be of particular concern because Canco should get credit in

Canada for. any U.S. tax liability, it did raise a number of concerns in this case. First,

there are the tax compliance concerns, such as the requirement to file U.S. tax returns.

This gives rise to additional related concerns, such as the allocation of income as between

the U.S. and Canada and the potential for being caught between conflicting assessments

between the IRS and Revenue Canada.

Of even greater concern in this case was the fact that Canco is a Canadian-controlled private

corporation ("CCPC") for the purposes of the Tax Act. As such, Canco is entitled to use

the small business deduction to reduce the tax rate on up to $200,000 of active business

income each year to approximately 23 %15. Accordingly, Canco follows the usual practice

of paying bonuses to its principal owner-managers of all of its income each year in excess

of the $200,000 small business deduction limit. As a result, if Canco were subject to

American taxation, a mis-match would have arisen because the taxpayer that was subject to

IS The small business deduction is available under subsection 125(1) of the Tax Act. This is the Ontariorate. The rate in Saskatchewan is approximately 21 %.

23

tax in the U.S., which would have been Canco, would not have been the same as the ones

that were subject to tax in Canada, being (largely) the owner-managers. The result would

have been a loss of a substantial portion of the foreign tax credit in Canada for the

American tax liability.

Canco and the American sub-manufacturer finally decided that Canco would receive

payments from the sub-manufacturer based on the quantity of each product sold and

delivered to the retailer. For relationships such as this between Canco and sub

manufacturers in many jurisdictions, this would have given rise to significant concern that

Canco would be in receipt of royalty payments and subject to withholding tax on the gross

amount of such payments. In many cases, even if there were a tax treaty in place between

Canada and the other jurisdiction, there may be no treaty reduction of the withholding tax

rate while in this case t1)e treaty between Canada and the U.S. may have excluded the

payments in question from American taxation. 16

In order to avoid these concerns, Canco and the American sub-manufacturer entered into

a relationship in which Canco would have direct on-going dealings with the American

retailer. The retailer would place orders directly with Canco in Canada (by telephone or

telecopier). This would avoid Canco having a permanent establishment in the U.S., thereby

avoiding U.S. tax liability and reporting·requirements;~ Canco would then place orders for

the manufacture and delivery of the goods with the American sub-manufacturer. Canco

would earn a spread on the goods equal to the difference between what the retailer pays for

goods and what the sub-manufacturer charges for the manufacture and supply of the goods.

As well, this structure avoids concerns about Canco earning royalties from a foreign source.

16 In this case, it was arguable, although by no means clear, that the payments would have been for the useof or the right to use a patent (the products involved included some that were patented) or information concerningindustrial, commercial or scientific experience, all of which are excluded from American taxation by reason ofArticle XII of the Canada-U.S. Income Tax Convention, 1980, as amended.

24

(iii) The Russian Supply Contract

"Canco" is a Canadian corporation that was presented with an opportunity to participate in

a Russian joint venture with a Russian state-owned entity. The terms of the joint venture

required that it be carried on through a Russian joint stock corporation (the "IV Co. "), but

permitted majority control of that corporation by Canco. The IV Co. would acquire supply

of raw materials in Russia, process those materials in Russia, and then export the finished

product to a third country which is one of the three major world markets for the product.

In this case, obviously, the terms of the joint venture agreement dictated the form of

business entity to be utilized in Russia. The majority control of IV Co. held by Canco

means that IV Co. is a foreign affiliate and a controlled foreign affiliate of Canco.

Because the IV Co. is resident and carrying on an active business in Russia, which is a

designated treaty country, IV Co. will earn exempt surplus on its active business income

earned in Russia. However, because the total tax in various forms in Russia is relatively

high, Canco would prefer to minimize the income that is earned by IV Co. in Russia.

Fortunately, the relationship with the Russian state-owned entity permits the structure of this

venture to include a distribution corporation ("Distribution Co. ") to be incorporated in the

third country, being the market for the goods. The tax regime in the third country is far

more favourable than is the Russian regime. Accordingly, subject to transfer pricing

restrictions in Russian, the relationship between IV Co. and Distribution Co. can be set up

to minimize profits, and therefore taxes, in Russia, and to maximize profits in the third

country. Because the third country is also a designated treaty country, Canco is indifferent

from a Canadian tax perspective as to~which of its~foreign~subsidiariesearn the profits from

the business.

As a further note, the principals behind Canco were faced with a difficult decision in terms

of how Canco would hold its shares in IV Co. By holding those shares directly, any

dividend distributions from IV Co. would be subject to withholding tax in Russia at a rate

25

of 10% (the maximum rate permitted under the tax treaty between Canada and Russia). By

routing such dividends through a Cypriot holding corporation, Canco could reduce the tax

on such dividends to 4.25%. This is because the tax treaty between Cyprus and Russia

provides for a nil rate of withholding tax on such dividends, and domestic tax laws in

Cyprus would impose tax of only 4.25% on the Cypriot holding corporation, with no

withholding tax imposed on dividends out of Cyprus.

However, there were three counteracting considerations. First, the tax treaty between

Cyprus and Russia is being renegotiated and indications are that the nil rate of withholding

tax on dividends will not survive. Secondly, apparently Cypriot corporations are regarded

with some suspicion in Russia. Finally, as outlined above, one of the objectives of this

structure is to minimize profits earned in Russia by JV Co, so that the benefits of using a

Cypriot holding corporation may not be great in any case (subject, of course, to whether

Russian transfer pricing restrictions result in greater profits being attributed to Russia,

notwithstanding the planning of the parties).- Accordingly,-thebenefits of using a Cypriot

holding corporation may not be worth the overall tax and non-tax costs of adopting such a

structure.

SUMMARY

There will be many tax and non-tax factors to be considered in structuring business

operations outside Canada. At times the legal or practical considerations will dictate the

structure to be adopted. At others, these will permit flexibility in structuring such that tax

planning opportunities can be exploited to considerable advantage. While the structuring

of foreign business operations can be complex, with that complexity come opportunities.