Download - Interim Report Sahil

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 1/28

A

project report

on

COMPARATIVE ANALYSIS OF MUTUAL

FUND AND ULIPS

By

SAHIL DHALL

10BSP1059

name of sip organisation

HDFC BANK

1

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 2/28

A

report on

COMPARATIVE ANALYSIS OF MUTUAL FUND AND ULIPS

Name of sip organisation

HDFC BANK

A report submitted on partial fulfilment of the requirements

At

Ibs- chandigarh

Date of submission- 8th april 2011

Submitted by

submitted to

Sahil dhall prof. sudhir

DIWAN

10BSP1059 ibsfaculty

2

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 3/28

ABSTRACT

The project aims at comparative analysis of mutual funds & unit linkedinvestment plans. Analyse insurance as an investment option/avenue.

To calculate the risk and return profile of ULIP & Mutual Funds .

The project has a detailed study of various insurance plans offered bythe major players in the insurance sector. Made a comparative analysisof the of HDFC life insurance plans with that of other major players.Carried out an in-depth study of all the major mutual funds available inthe market & analyse their performance since their inception. To makea comparison between the performances of mutual funds with that of unit linked investment plans (ULIP).The report include case studies inorder to illustrate the comparison between different ULIP schemes withMutual fund schemes. The project aims to help understand theconsumer behaviour towards various financial services like insuranceand mutual funds. The report enhances the knowledge on how variousmarketing concepts learned in the classroom are implemented in areal life environment.

The project required me design a questionnaire and to do a primarysurvey on investor perception towards ULIP & mutual Funds availablein the market. The target respondents of the primary survey weremanagers, executives and consultant working for life insurancecompanies.

The individual project assigned to me entitles me to calculate the risk& return profile of the ULIP plans & mutual funds available in themarket. The mathematical techniques that are to be used forcalculating the risk and return profile are beta values, variance, Sharperatio & standard deviations followed by graphically plotting thecalculated values and make a comparative analysis of the data.

Table of content

3

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 4/28

1. Chapter 1i. Purpose of the Project

ii. Scope of the Project

iii. Limitationsiv. Methodology

2. Chapter 2i. About the Company

3. Chapter 3i. Introduction to Mutual Fund

ii. Concept of Mutual Fund

iii. History of Mutual Fundiv. Types of Mutual Fund

4. Chapter 4i. Introduction to ULIPs

ii. Working of ULIP

iii. Types of ULIPsiv. Features of ULIPs

5. Chapter 5i. Difference between Mutual Funds and ULIPsii. Comparative analysis of Mutual funds Schemes

iii. Comparative analysis of ULIPs schemes

6. Chapter 6i. References

Chapter 1

4

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 5/28

Purpose of the project

To map the marketing & distribution strategy of HDFC fundschemes and to compare various strategies used by various

players in Life insurance sector. To do detailed analysis of the entire range of products/schemes

offered by HDFC. It will help in making a detailed analysis of thespectrum of insurance products available in the market acrossthe industry.

To analyse the performance HDFC Mutual fund and Life insuranceschemes, by calculating the Beta value, Sharpe ratio, standarddeviation of the investments.

To collect data through primary survey, using a comprehensivelydesigned questionnaire and analysing the same for mapping the

brand image of HDFC BANK and investor perception about theULIP and mutual funds available in the market, and to identify themajor factor that influence investor for choosing an insuranceplan.

Scope of the project

The scope of the project is to get the knowledge of insurance, industry

and its regulations from books, Internet and literature survey. This willgive us in-depth knowledge about the insurance sector as a whole.Data collection regarding the market share, products & servicesoffered by different life insurance company by visiting there corporateoffices. This will help in identifying the Unique Selling Proposition (USP)of different players in the market.Collection of brochures and pamphlets of different products offered bydifferent players and study them in order to compare and contrast thedifferent insurance products across industry. It will to find out the bestproduct available in the market, in its category.

Sample selection (Random Sampling Technique) and designing of aquestionnaire to collect primary data so as to map the investorperception regarding ULIP and Mutual funds available in the market.Sample selection (Random Sampling Technique) and designing of aquestionnaire to collect primary data to do a brand image survey of HDFC BANK. The data collected is used to do descriptive analyses (Pie

5

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 6/28

charts and histogram) for mapping the brand image assessment of HDFC.

Limitations of the study

The scope of the project is limited to conceptual andmarketing aspects of Life Insurance Companies anddoesn’t include Claim Settlement and the underwriting partof the operations which are equally important aspect of learning.

Project is limited to HDFC BANK, which is branchdedicated to High Net-worth Individual .It excludes theanalysis of low premium paying segment of the people.

The major limitation was in terms of collecting theright information from the various insurance players, as theinsurance players resist in revealing their marketingstrategies, etc.

Methodology

Define the information needed:- This first step states that what is the information that is actuallyrequired.Information in this case we require is that what is the approach of investors while investing their money in mutual funds and ulipse.g. what do they consider while deciding as to invest in which of the two i.e mutual funds or ulips. Also, it studies the extent towhich the investors are aware of the various costs that one bearswhile making any investment. So, the information sought andinformation generated is only possible after defining the

information needed.

Design the research:-A research design is a framework or blueprint for conducting theresearch project. It details the

6

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 7/28

procedures necessary for obtaining the information neededto solve research problems.

Construct a questionnaire:-A questionnaire is a formalized set of questions for obtaininginformation from respondents. Whereas pretesting refers to the testingof the questionnaire on a small sample of respondents in order toidentify and eliminate potentialproblems.

Sample Size – For the purpose of the study, 50 potentialinvestors in ulip and mutual funds were recruited as thesample. Data Collection – Research is explanatory in nature,hence information was sought from primary and secondarydata.

o PRIMARY DATA – Data was collected throughquestionnaire method, filled by the sample.o SECONDARY DATA – Information from HDFC Bank ulip andmutual funds brochures, HDFC Bank Knowledge center i.e. online

bank information, Business magazines and online articles regardingmutual funds and ulip

Chapter 2

About the company

HDFC BANK

The Housing Development Finance Corporation Limited (HDFC)was amongst the first to receive an 'in principle'approval from the Reserve Bank of India (RBI) to set up a bankin the private sector, as part of the RBI's liberalisation of theIndian Banking Industry in 1994. The bank was incorporated inAugust 1994 in the name of 'HDFC Bank Limited', with its

7

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 8/28

registered office in Mumbai, India. HDFC Bank commencedoperations as a Scheduled Commercial Bank in January 1995.

HDFC Bank's mission is to be a World-Class Indian Bank. Theobjective is to build sound customer franchises across distinct

businesses so as to be the preferred provider of bankingservices for target retail and wholesale customer segments,and to achieve healthy growth in profitability, consistent withthe bank's risk appetite. The bank is committed to maintain thehighest level of ethical standards, professional integrity,corporate governance and regulatory compliance. HDFC Bank'sbusiness philosophy is based on four core values - OperationalExcellence, Customer Focus, Product Leadership and People.

HDFC Bank is headquartered in Mumbai. The Bank at present

has an enviable network of 1,725 branches spread in 779 citiesacross India. All branches are linked on an online real-timebasis. Customers in over 500 locations are also servicedthrough Telephone Banking.

Its strategy emphasis on:-

• Increase our market share in India’s expanding banking andfinancial services industry by following a disciplined growthstrategy focusing on quality and not on quantity and delivering

high quality customer service.

• Leverage our technology platform and open scalable systems todeliver more products to more customers and to controloperating costs.

• Maintain our current high standards for asset quality throughdisciplined credit risk management.

• Develop innovative products and services that attract our

targeted customers and address inefficiencies in the Indianfinancial sector.

• Continue to develop products and services that reduce our cost

of funds. Focus on high earnings growth with low volatility.

8

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 9/28

Chapter 3

Introduction to mutual fund

Mutual fund is a trust that pools the savings of a number of investors who share a common financial goal. This pool of money is invested in accordance with a stated objective. The

joint ownership of the fund is thus “Mutual”, i.e. the fundbelongs to all investors. The money thus collected is theninvested in capital market instruments such as shares,debentures and other securities. The income earned throughthese investments and the capital appreciations realized areshared by its unit holders in proportion the number of unitsowned by them. Thus a Mutual Fund is the most suitableinvestment for the common man as it offers an opportunity to

invest in a diversified, professionally managed basket of securities at a relatively low cost.

SEBI (Mutual Fund) Regulations 1993 defines Mutual Fund as :-“A fund established in the form of a trust by a sponsor to raise

money by thetrustees through the sale of units to the public under one or

more schemes forinvesting securities in accordance with these regulations”

The rationale behind a mutual fund is that there are a largenumber of investors

who lack the time and or the skills to manage their money.Hence, professional fund managers, acting on behalf of the

Mutual Fund, managethe investments (investor’s money) for their benefit in return for

a managementfee. The organization that manages the investment is called the

AssetManagement Company (AMC). Thus, a Mutual Fund is the most

suitableinvestment for the common person as it offers an opportunity to

invest in adiversified, professionally managed basket of securities at a

relatively low cost.Anybody with an investible surplus of as little as a few thousand

rupees can invest

9

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 10/28

in mutual fund .Each mutual fund scheme has definedinvestment objective and

strategy.

Concept of Mutual Funds in India:

History of mutual funds

The origin of mutual fund industry in India is with the introduction of the concept of mutual fund by UTI in the year 1963. Though thegrowth was slow, but it accelerated from the year 1987 when non-UTIplayers entered the industry. Indian mutual fund industry has seen

dramatic improvements, both quality as well as quantity wise.

1. First phase (1964-1987) The Unit Trust if India (UTI) was established in the year 1963 by

passing an act in the parliament. In 1978 UTI was de-linked from the RBI and the Industrial

Development Bank of India (IDBI) took over the regulatory andadministrative control in place of RBI.

10

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 11/28

The first scheme launched by UTI was Unit Scheme 1964, whichis popularly known as US-64.

At the end of 1988 UTI had Rs.6, 700 crores of assets undermanagement (AUM).

2. Second phase (1987-1993) In the year 1987, public sector mutual funds setup by public

sector banks, life insurance corporation of India and generalinsurance of India are came into existence.

The end of 1993 marked Rs.47, 004 as assets undermanagement (AUM).

The following are the non-UTI mutual funds at their initial stages.1. SBI mutual fund in June 1987.2. Can bank mutual fund in December 1987.3. LIC mutual fund in June 1989.4. GIC mutual fund in June 1990

5. Punjab National Bank mutual fund in august 1989.

3. Third phase (1993-2003) Entry of private sector funds- a wide choice to Indian investors in

mutual fund. 1993 was the year in which the first Mutual Fund Regulations

came into being, under which all mutual funds, except UTI wereto be registered and governed

The 1993 SEBI (Mutual Fund) Regulations were substituted by amore comprehensive and revised Mutual Fund Regulations in

1996. The industry now functions under the SEBI (Mutual Fund)Regulations 1996.

As at the end of January 2003, there were 33 mutual funds withtotal assets of Rs. 1,21,805 crores.

4. Fourth phase (since 2003 February)Following the repeal of the UTI act in February 2003, it was UTI

bifurcated into 2 separate entities. One is the specified undertaking of the UTI with asset under

management of Rs.29835/- crass at the end of January 2003 The second is the UTI Mutual Fund Ltd, sponsored by SBI, PNB,

BOB and LIC. It is registered with SEBI and functions under theMutual Fund Regulations.

11

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 12/28

At the end March 2000 UTI had more than Rs.76,000 crores of AUM.

As at the end of September, 2004, there were 29 funds, which manageassets of Rs.153108 crores under 421 schemes.

TYPE OF MUTUAL FUND SCHEMES

Wide variety of mutual fund schemes exists to cater to the needs suchas financial position, risk tolerance and return expectations etc. thetable below gives an overview into the existing types of schemes inthe industry.

By structure• Open-Ended schemes•

Close-Ended schemes• Interval schemes

By investment objectives• Growth/Equity schemes• General purpose• Money market• Guilt funds• Balanced schemes

Other schemes• Tax saving schemes•

Sector specific schemes

Open-ended schemesA type of mutual fund where there are no restrictions on the amount of shares the fund will issue. If demand is high enough the fund willcontinue to issue shares no matter how many investors there are.Open-end funds also buy back shares when investors wish to sell.

Close-ended schemesUnder this scheme the corpus of the fund and its duration are prefixed.

In other words the corpus of the fund and the number of units aredetermined in advance. Once the subscription reaches the pre-determined level, the entry of investors is closed. After the expiry of the fixed period, the entire corpus is disinvested and the proceeds aredistributed to the various unit holders in proportion to their holdings.

Interval schemes

12

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 13/28

These schemes combine the features of open ended schemes. Theymay be traded on the stock exchange or may be open for sale orredemption during predetermined intervals at NAV based prices.

Growth/Equity schemes

These schemes also commonly called growth schemes, seek to investa majority of their funds in equities and a small portion in moneymarket instruments. Such schemes have the potential to deliversuperior returns over the long term. However, because they invest inequities, these schemes are exposed to fluctuations in value especiallyin the short term.

General Purpose Equity Schemes The investment objectives of general purpose equity schemes do not

restrict them to invest in specific industries or sectors. They thus havea diversified portfolio of companies across a large spectrum of industries.

Money Market Schemes These schemes invest in short term instruments such as commercialpapers, certificates of deposits (CD’S), treasury bills (T-bill) andovernight money (call).

Guilt Funds

These primarily invest in government debts. Hence, the investorusually does not have to worry about credit risk since government debtis generally credit risk free.Gilt Securities Fund - Short Term Gilt Plan &Long Term Gilt Plan are best example of such scheme.

Balanced Schemes These schemes invest in both equities as well as debt. By investing ina mix of this nature, balanced schemes seek to attain the objective of income and moderate capital appreciation. Such schemes are ideal forinvestors with a conservative long term orientation.

Tax Saving SchemesInvestors (Individuals and Hindu undivided families (HUFs)) are beingencouraged to invest in equity markets through equity linked savingsscheme (ELSS) by offering them a tax rebate.

13

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 14/28

Sector specific equity schemes: These schemes restrict their investing to one or more pre definedsectors e.g. technology sector. They depend upon the performance of these select sectors only and are hence inherently more risky than

general purpose equity schemes. These schemes are ideally suited forinformed investors who wish to take a view and risk on the concernedsector.

Risk vs. Return

Chapter 4

Introduction ulips

14

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 15/28

ULIPs are a category of goal-based financial solutions that combine thesafety of insurance protection with wealth creation opportunities. InULIPs, a part of the investment goes towards providing you life cover.

The residual portion is invested in a fund which in turn invests instocks or bonds. The value of investments alters with the performance

of the underlying fund opted by you.

Simply put, ULIPs are structured such that the protection element andthe savings element can be distinguished and hence managedaccording to your specific needs, offering unprecedented flexibility andtransparency.

WORKING OF ULIP

It is critical that you understand how your money gets invested onceyou purchase ULIP.

Once you decide the amount of premium to be paid and the amount of life cover you want, the insurer deducts some portion of the premiumupfront. This portion is known as the Premium Allocation charge andthis varies from product to product. The rest of the premium is

invested in the fund or mixture of funds chosen by you. Mortalitycharges and administration charges are thereafter deducted on aperiodic (mostly monthly) basis whereas the fund managementcharges are deducted on a daily basis

Since the fund of your choice has an underlying investment – either inequity or debt or a combination of the two – your fund value will reflectthe performance of the underlying asset classes. At the time of maturity of your plan, you are entitled to receive the fund value as atthe time of maturity. The pie-chart below illustrates the split of yourULIP premium in a graphical format.

15

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 16/28

In addition to the investment fund ULIPs give you the benefit of

insurance cover as well. The mortality charge mentioned above goestowards provision of this cover.

Over a period of time, the component of charges as a percentage of the premium paid tends to decrease. Which is why, you shouldcontinue paying your premiums regularly. That is the best way of making your ULIP deliver on its dual benefit of protection and wealthcreation.

Types of ulips

There are various unit linked insurance plans available in the market.However, the key ones are pension, children, group and capitalguaranteeplans.

The pension plans come with two variations — with and without lifecover —and are meant for people who want to generate returns for their

sunset years.

The children plans, on the other hand, are aimed at taking care of their

educational and other needs..

Apart from unit-linked plans for individuals, group unit linked plans are

also

available in the market. The Group linked plans are basically designed

16

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 17/28

for

employers who want to offer certain benefits for their employees such

as

gratuity, superannuation and leave encashment.

The other important category of ULIPs is capital guarantee plans. The

plan

promises the policyholder that at least the premium paid will be

returned at

maturity. But the guaranteed amount is payable only when the policy's

maturity value is below the total premium paid by the individual till

maturity.

However, the guarantee is not provided on the actual premium paid

but onlyon that portion of the premium that is net of expenses (mortality, sales

and

marketing, administration)

Features of ulips

• Premiums paid can be single, regular or variable. The payment

period too can be

regular or variable. The risk cover can be increased ordecreased.

• As in all insurance policies, the risk charge (mortality rate) varieswith

age.

• The maturity benefit is not typically a fixed amount and thematurity

period can be advanced or extended.

• Investments can be made in gilt funds, balanced funds, moneymarket

17

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 18/28

funds, growth funds or bonds.

• The policyholder can switch between schemes, for instance,balanced

to debt or gilt to equity, etc. \

Chapter 5

Difference between mutual funds and ulips

a) Expenses - Expenses incurred in a MF is lesser than the expenses of ULIPs. The reason is expenses in a mutual fund is capped, there is apre-set upper limit, whereas for ULIPs no upper limit in terms of

controlling the expenses is set by the insurance company.

b) Tax benefits - Any investment made in ULIP qualifies under 80 C of income tax act, where an investor can save tax on Rs 1,00, 000. Incase of MF, only investment in ELSS (equity linked tax savings scheme)a specific type of mutual fund scheme qualifies for tax benefits undersection 80 C.

c) Portfolio disclosure - MF houses are required to statutorily declaretheir portfolios on a quarterly basis, however there is no such

statutory requirements for ULIPs.

d) Return on investment - As both the products are long terminvestment products, these products has given good returns to itsinvestors. Many analysts' feels, from a long term view ULIP providesbetter return than MF. However this is not true in all cases, it alldepends on the type of investment and the fund manager's skills inmanaging the funds.

e) Liquidity - ULIPs score low on liquidity. According to guidelines of the

Insurance Regulatory and Development Authority (IRDA), ULIPs have aminimum term of five years and a minimum lockin of three years. Youcan make partial withdrawals after three years. The surrender value of a ULIP is low in the initial years, since the insurer deducts a large partof your premium as marketing and distribution costs. ULIPs areessentially long-term products that make sense only if your timehorizon is 10 to 20 years.

18

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 19/28

Mutual fund investments, on the other hand, can be redeemed at anytime, barring ELSS (equity-linked savings schemes). Exit loads, if applicable , are generally for six months to a year in equity funds. Somutual funds score substantially higher on liquidity.

Comparative analysis of mutual fund schemes

Mutual fund scheme of HDFC:-

HDFC TOP 200:-

Investment objective:- To generate long term capital appreciation froma portfolio of equity and equity-linked instruments primarily drawnfrom the companies in BSE 200 index.

Investment strategy:- The investment strategy of primarily restrictingthe equity portfolio to the BSE 200 Index scrips is intended to reducerisks while maintaining steady growth. Stock specific risk will beminimized by investing only in those companies / industries that havebeen thoroughly researched by the investment manager's researchteam. Risk will also be reduced through a diversification of the

portfolio.

Investment pattern:-

Sno. Asset Type (% of portfolio) Risk profile1 Equities and Equity

RelatedInstruments

Upto 100%(including use of derivatives for

hedging and otheruses as permittedby prevailing SEBIRegulations)

Medium to High

2 Debt & MoneyMarket Instruments

Balance in Debt &Money MarketInstruments

Low to Medium

Mutual fund scheme of ICICI:-

19

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 20/28

ICICI PRUDENTIAL DYNAMIC:-

Investment objective:- To generate capital appreciation by actively

investing in equity related securities. For defensive consideration thescheme may invest in debt, money market instruments, to the extentpermitted under the regulations. The AMC will have the discretion tocompletely or partially invest in any type of securities.

Investment strategy:- It is a diversified equity plan that follows thegrowth investment philosophy to invest in a portfolio of large and smallcap stocks. It has the ability to move gradually into the cash as marketgets overvalued.

Investment Pattern:- Equity and Equity related markets, Debt andMoney market instruments.

Mutual fund scheme for Reliance:-

Reliance Vision Fund:-

Investment objective:- The objective of the scheme is to achieve longterm growth of capital by investment in equity and equity related

securities through research based investment approach.

Investment Pattern:- 60-100% in equity and equity relatedinstruments, 0-30% in debt market instruments and 0-10% in moneymarket instruments.

Comparative analysis of ULIP fund schemes

Children Plans:-

PLAN HDFC YOUNGSTARCHAMPIONSUVIDHA

ICICI PRUSMARTKIDASSURE PLAN

BIRLA SUNLIFE SARALCHILDREN’SPLAN

SBI LIFE-UNITPLUS II CHILDPLAN

20

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 21/28

MINIMUMPREMUIM

Rs.15,000 p.a. Rs.15,000 p.a. Rs.10,000 p.a. Rs.18,000

POLICY TERM 10 TO 20 YRS 15 TO 25 YRS 10-20 YRS 8 TO 25 YRS

SUM ASSURED FIXED SUMASSURED- 5

TIMES ANNUALPREMUIM

FIXED SUMASSURED- 5

TIMESANNUALPREMUIM

FIXED SUMASSURED- 6

TIMESANNUALPREMUIM

MINIMUMSUMASSURED: 5

TIMESANNUALPREMUIMMAXIMUMSUMASSURED:3-5 YRS: 10XANNUALPREMUIM

6-18 YRS:20XANNUALPREMUIM

ADDITIONALALLOCATIONOF UNITS

BUMPERADDITION ONMATURITY : ASA % OFAVERAGEANNUALISEDPREMUIM

10 YRS TERM :25%15 TO 19 YRS :50 %20 YRS :100%

GUARANTEEDADDITIONSAT THE ENDOF 15TH YR :120% TO170% OF ONE

ANNUALPREMUIMDEPENDINGON NO. OFPREMUIMPAIDPLUSADDITIONALALLOCATION: FROM 6 TH

POLICY YR 2%OF PREMUIM

AT THEBEGINNINGOF EVERY

YEAR

GUARANTEED MATURITY ADDITION :PER 1000ANNUALPREMUIM10PAY/10YR

TERM: Rs.30010PAY/20YR TERM : Rs.80020PAY/20YR

TERM :Rs.1000

LOYALTY ADDITION:0.20% XAVERAGELAST24MONTHSFUND VALUE

X POLICY TERM

FUNDMANAGEMENTFEATURE

SMART TRANSFEROPTION

LIFECYCLEBASEDPORTFOLIOSTRATEGY

LIFECYCLEOPTION

DIVERSEFUND OPTION

21

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 22/28

POLICY ADMINCHARGE

0.95% OFORIGINALANNUALISEDPREMUIM PERMONTH

Rs. 60 PERMONTH IN 2ND

TO 5 TH YR

0.25% OFANNUALPREMUIM PERMONTH

Rs.50 PERMONTH OFEACH POLICYMONTH

FUNDMANAGEMENTCHARGE

1.25% ACROSSALL FUNDS.

0.75% TO1.35%ACROSSVARIOUSFUNDS

1.00% TO1.35%ACROSSVARIOUSFUNDS

0.25% TO1.35%ACROSSVARIOUSFUNDS

ALLOCATION

CHARGE YEAR 1 YEAR 2

10%1%0%

100%0%0%

17% TO 30%17% TO 30%17% TO 30%

12.5%3.5%0%

22

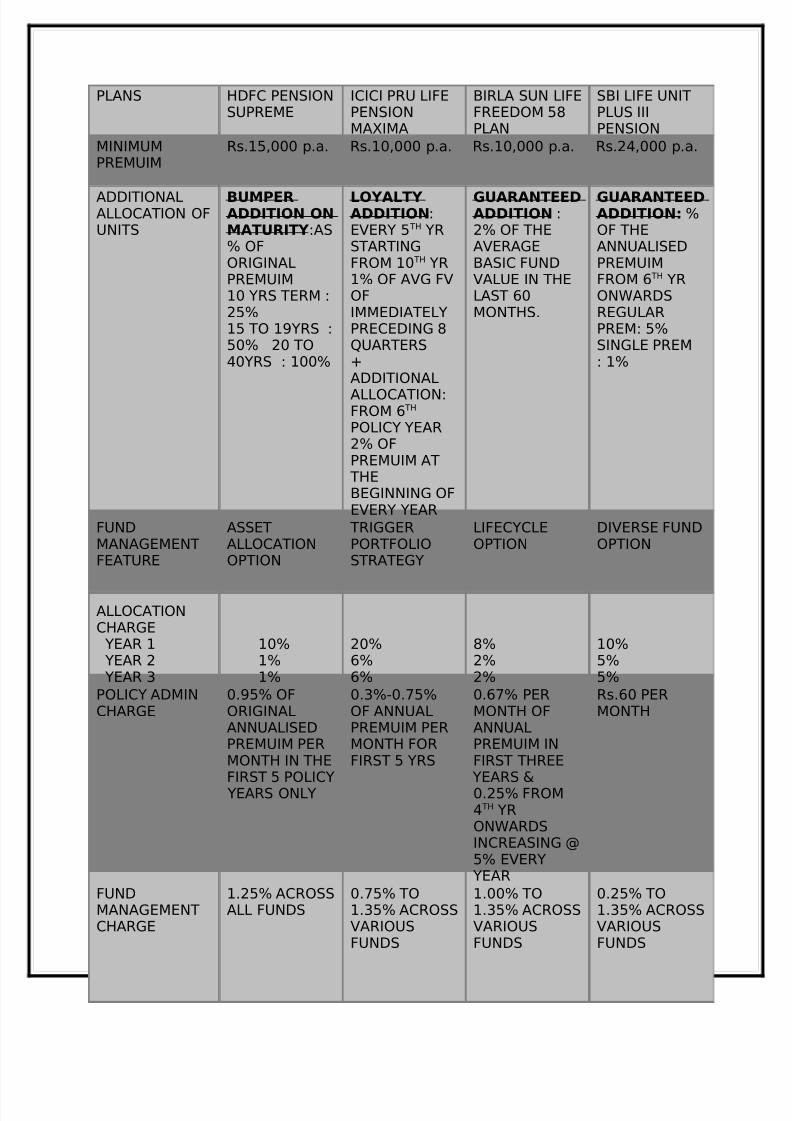

RETIREMENT PLANS:-

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 23/28

23

PLANS HDFC PENSIONSUPREME

ICICI PRU LIFEPENSIONMAXIMA

BIRLA SUN LIFEFREEDOM 58PLAN

SBI LIFE UNITPLUS IIIPENSION

MINIMUMPREMUIM

Rs.15,000 p.a. Rs.10,000 p.a. Rs.10,000 p.a. Rs.24,000 p.a.

ADDITIONALALLOCATION OFUNITS

BUMPERADDITION ONMATURITY :AS% OFORIGINALPREMUIM10 YRS TERM :25%15 TO 19YRS :50% 20 TO40YRS : 100%

LOYALTY ADDITION:EVERY 5 TH YRSTARTINGFROM 10 TH YR1% OF AVG FVOFIMMEDIATELYPRECEDING 8QUARTERS+ADDITIONAL

ALLOCATION:FROM 6 TH

POLICY YEAR2% OFPREMUIM AT

THEBEGINNING OFEVERY YEAR

GUARANTEEDADDITION :2% OF THEAVERAGEBASIC FUNDVALUE IN THELAST 60MONTHS.

GUARANTEEDADDITION: %OF THEANNUALISEDPREMUIMFROM 6 TH YRONWARDSREGULARPREM: 5%SINGLE PREM: 1%

FUNDMANAGEMENTFEATURE

ASSETALLOCATIONOPTION

TRIGGERPORTFOLIOSTRATEGY

LIFECYCLEOPTION

DIVERSE FUNDOPTION

ALLOCATIONCHARGEYEAR 1YEAR 2YEAR 3

10%1%1%

20%6%6%

8%2%2%

10%5%5%

POLICY ADMINCHARGE

0.95% OFORIGINALANNUALISEDPREMUIM PERMONTH IN THEFIRST 5 POLICY

YEARS ONLY

0.3%-0.75%OF ANNUALPREMUIM PERMONTH FORFIRST 5 YRS

0.67% PERMONTH OFANNUALPREMUIM INFIRST THREE

YEARS &0.25% FROM4 TH YRONWARDSINCREASING @5% EVERY

YEAR

Rs.60 PERMONTH

FUNDMANAGEMENTCHARGE

1.25% ACROSSALL FUNDS

0.75% TO1.35% ACROSSVARIOUSFUNDS

1.00% TO1.35% ACROSSVARIOUSFUNDS

0.25% TO1.35% ACROSSVARIOUSFUNDS

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 24/28

Questionnaire :-

COMPARATIVE ANALYSIS OF MUTUAL FUNDS AND ULIPS

Q1. What do investors prefer?

• Mutual Funds

• ULIPS

• Fixed Deposits

• Shares and Bonds

Q2. Have you invested in the following ?

(if yes go to Ques no. 4)

• Mutual funds

• ULIPS

•

Both

Q3. What is the reason for not investing?

• Uncertain

• High cost

24

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 25/28

• Not interested in investments

Q4. Do you think investing in Mutual Funds is worthy?

• Yes

• No

Q5. According to you why an individual should invest in

Mutual Funds?

• To multiply money

• Moderate return with minimum Risk

• To have faster rate of growth

• Others

Q6. Do you have any plan in investing in future?

• Yes

• No

Q7. When do you plan to invest?

• A month

• 1 month- 1 year

• After 1 year

• Non-Respondents

25

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 26/28

SECTION-B

Q1. Are you aware of ULIPS schemes?

• Yes

• No

Q2. In which companies you invested in?

• LIC

• ICICI PRU

• Aviva life insurance

• Reliance

• None

Q3. What made you go to the company?

• Brand name

• Services

• Customer Relationship

• Better policy option

Q4. What extra benefits you would like to have along life

insurance?

• Family income benefits

• Critical illness benefit

• Return

26

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 27/28

• Both family income and critical illness

Q5. Do you have any plan in investing in future?

• Yes

• No

Q6. When do you plan to invest?

• A month

• 1 month- 1 year

• After 1 year

• Non-Respondent

Q7. Rank ULIP as compared to Mutual Funds?

•Good

• Satisfactory

• Non-Respondent

PERSONAL DETAILS

Name:

27

8/6/2019 Interim Report Sahil

http://slidepdf.com/reader/full/interim-report-sahil 28/28

Age Group: Below 20 Between 20-30 Between 30-40 Above 40

Occupation: Salaried - Business - Housewife - Professional - Retired

References

Search Engines

Yahoo

Rediffmail

Websites

• www.money.livemint.com

• www.moneycontrol.com

• www.valuesearchonline.com

• www.hdfcfund.com

• www.mutualfundsindia.com

• www.reliancemutual.com

• Newspapers : Economic Times, Business Times.