Prepared by Aon Benfield Analytics

Insurance Risk Study Brian Alvers 2014 Analytics Insights Conference July 22 - 24

Aon Benfield | Analytics

Proprietary & Confidential 2

Objective

Insurance Risk Study determines credible global insurance volatility benchmarks for use in underwriting risk modeling

Motivation: robust empirical quantification of all aspects of underwriting risk

Systemic volatility parameters by country, by line

– Forty nine countries, 90% of global premium

– Results for eight core lines of business

– Available as input to any simulation tool

Loss ratio correlation between lines within country

Correlation between macroeconomic and insurance variables

Aon Benfield approach to growth strategies

Insurance profitability, economic variables, and demographics by country

Detailed country profile of six individual insurance markets

Recognized by major US rating agencies

Published annually in September

Eighth edition released in 2013

Aon Benfield Insurance Risk Study Informed Parameterization of Risk Models

Aon Benfield | Analytics

Proprietary & Confidential 3

Introduction

Convergence of capital markets and insurance markets a reality for property catastrophe

– Pension fund, high-net worth individual, hedge fund and other capital

– Made it cheap to transfer catastrophe risk into the capital markets

Exciting prospect: extension to other, largely non-catastrophe driven perils

– Requires capital market and investor acceptance of underlying risk modeling

– Just what the Aon Benfield Insurance Risk Study has been focused on since 2006

For the first time, we are reporting combined ratios by country in order to identify potential growth opportunities

– Plus six in-depth country studies

Study is the cornerstone of Aon Benfield Analytics’ integrated and comprehensive risk modeling and risk assessment capabilities

– Reinsurance optimization framework

– ERM and economic capital modeling

Aon Benfield | Analytics

Proprietary & Confidential 4

Agenda

Section 1 Global Risk Parameters

Section 2 U.S. Reserve Adequacy and Risk

Section 3 Global Correlation Between Lines

Section 4 Macroeconomic Correlation

Section 5 Global Premium, Profitability and Opportunities

Section 6 Extending Insurance-Linked Securities

Section 1: Global Risk Parameters

Aon Benfield | Analytics

Proprietary & Confidential 6

Systemic Insurance Risk

Asset portfolio theory: risk does not diversify beyond systemic market risk

Insurance risk by line shows same behavior

– Risk does not completely diversify with increasing volume

• Naïve insurance risk model incorrectly assumes risk decreases to zero

– Level of systemic insurance risk varies by line

– Aon Benfield Insurance Risk Study determines level of systemic insurance risk by line

Asset Portfolio Risk Insurance Portfolio Risk

Aon Benfield | Analytics

Proprietary & Confidential 7

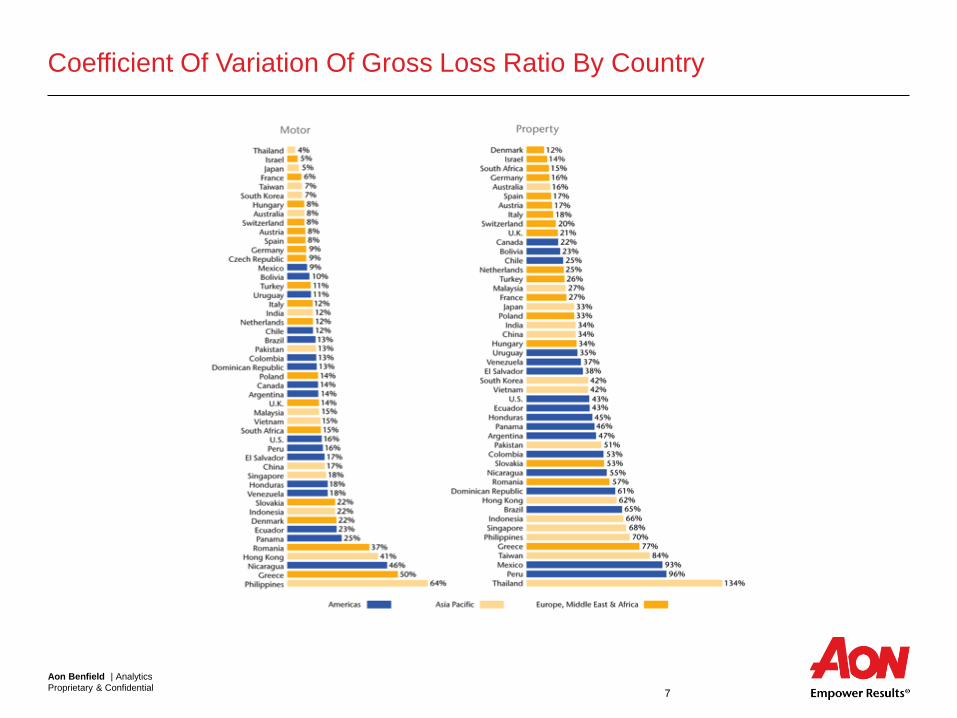

Coefficient Of Variation Of Gross Loss Ratio By Country

Aon Benfield | Analytics

Proprietary & Confidential 8

U.S. Risk Parameters Coefficient Of Variation Of Gross Loss Ratio, 1992-2012

Aon Benfield | Analytics

Proprietary & Confidential 9

Impact Of The Pricing Cycle

Aon Benfield | Analytics

Proprietary & Confidential 10

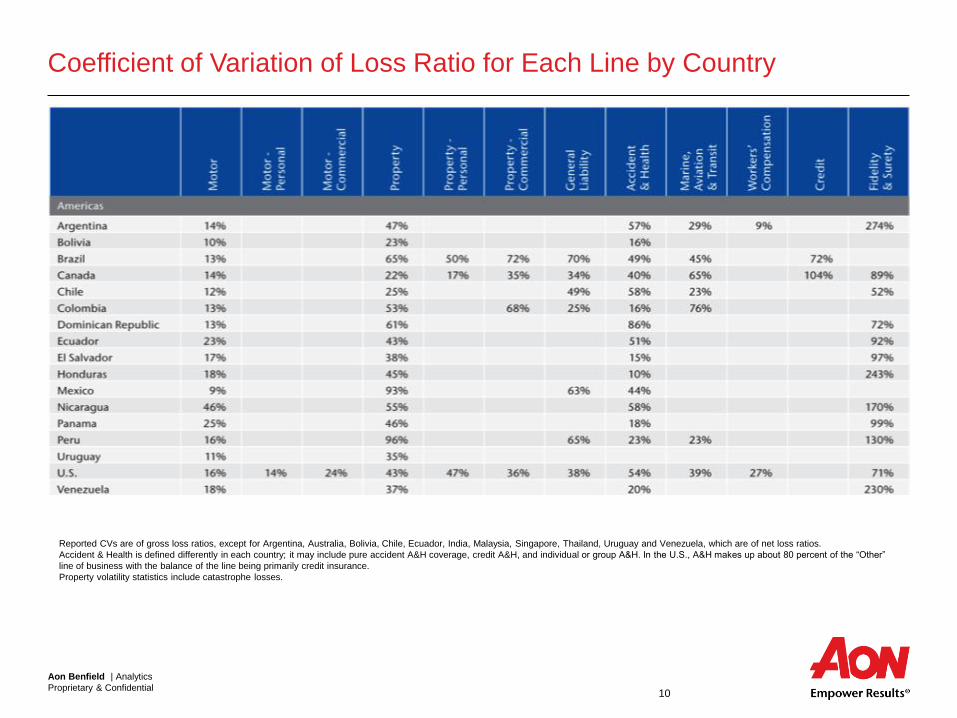

Coefficient of Variation of Loss Ratio for Each Line by Country

Reported CVs are of gross loss ratios, except for Argentina, Australia, Bolivia, Chile, Ecuador, India, Malaysia, Singapore, Thailand, Uruguay and Venezuela, which are of net loss ratios.

Accident & Health is defined differently in each country; it may include pure accident A&H coverage, credit A&H, and individual or group A&H. In the U.S., A&H makes up about 80 percent of the “Other”

line of business with the balance of the line being primarily credit insurance.

Property volatility statistics include catastrophe losses.

Aon Benfield | Analytics

Proprietary & Confidential 11

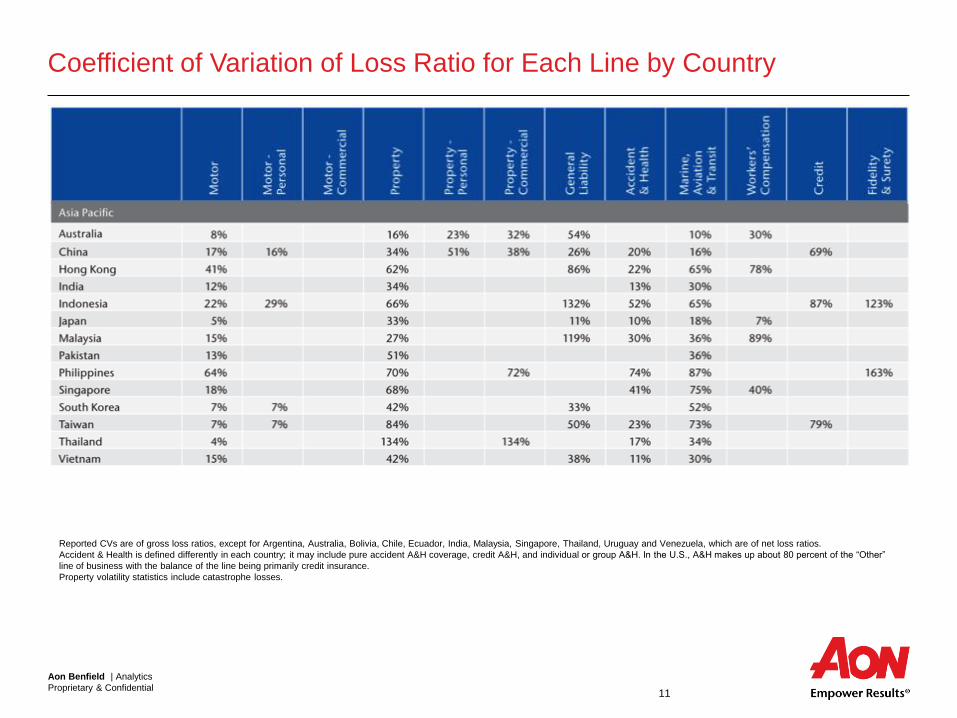

Coefficient of Variation of Loss Ratio for Each Line by Country

Reported CVs are of gross loss ratios, except for Argentina, Australia, Bolivia, Chile, Ecuador, India, Malaysia, Singapore, Thailand, Uruguay and Venezuela, which are of net loss ratios.

Accident & Health is defined differently in each country; it may include pure accident A&H coverage, credit A&H, and individual or group A&H. In the U.S., A&H makes up about 80 percent of the “Other”

line of business with the balance of the line being primarily credit insurance.

Property volatility statistics include catastrophe losses.

Aon Benfield | Analytics

Proprietary & Confidential 12

Coefficient of Variation of Loss Ratio for Each Line by Country

Reported CVs are of gross loss ratios, except for Argentina, Australia, Bolivia, Chile, Ecuador, India, Malaysia, Singapore, Thailand, Uruguay and Venezuela, which are of net loss ratios.

Accident & Health is defined differently in each country; it may include pure accident A&H coverage, credit A&H, and individual or group A&H. In the U.S., A&H makes up about 80 percent of the “Other”

line of business with the balance of the line being primarily credit insurance.

Property volatility statistics include catastrophe losses.

Section 2: U.S. Reserve Adequacy and Risk

Aon Benfield | Analytics

Proprietary & Confidential 14

U.S. P&C Industry Reserve Development (2002 – 2013)

2013 development per P&C Industry data as compiled by SNL through May 6, 2014

Total favorable development in 2013 of USD14.8 Billion

*Adjustments include Financial Lines development in 2008-2009 and AIG adverse development in 2010.

(22.3)

(14.1)

(10.5)

(0.6)

7.0 8.3

14.5

18.515.7

12.7 12.2 14.8

(25.0)

(20.0)

(15.0)

(10.0)

(5.0)

-

5.0

10.0

15.0

20.0

25.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Calendar Year

One Year Reserve Development ($B)

Adjusted *

Aon Benfield | Analytics

Proprietary & Confidential 15

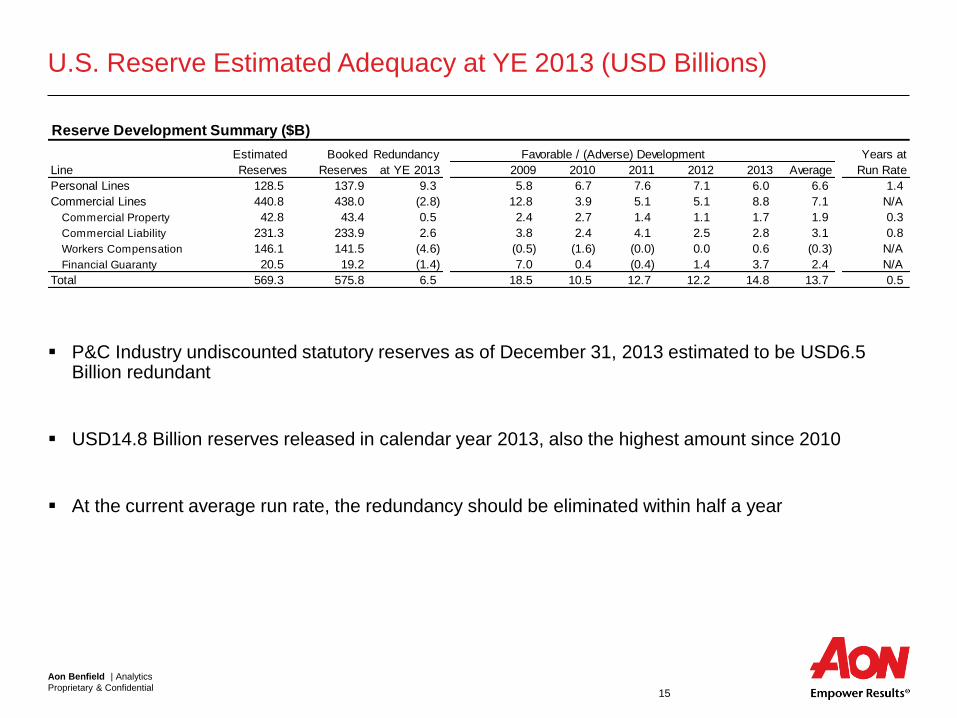

U.S. Reserve Estimated Adequacy at YE 2013 (USD Billions)

P&C Industry undiscounted statutory reserves as of December 31, 2013 estimated to be USD6.5 Billion redundant

USD14.8 Billion reserves released in calendar year 2013, also the highest amount since 2010

At the current average run rate, the redundancy should be eliminated within half a year

Reserve Development Summary ($B)

Estimated BookedEst. Redundancy Favorable / (Adverse) Development Years at

Line Reserves Reserves at YE 2013 2009 2010 2011 2012 2013 Average Run Rate

Personal Lines 128.5 137.9 9.3 5.8 6.7 7.6 7.1 6.0 6.6 1.4

Commercial Lines 440.8 438.0 (2.8) 12.8 3.9 5.1 5.1 8.8 7.1 N/A

Commercial Property 42.8 43.4 0.5 2.4 2.7 1.4 1.1 1.7 1.9 0.3

Commercial Liability 231.3 233.9 2.6 3.8 2.4 4.1 2.5 2.8 3.1 0.8

Workers Compensation 146.1 141.5 (4.6) (0.5) (1.6) (0.0) 0.0 0.6 (0.3) N/A

Financial Guaranty 20.5 19.2 (1.4) 7.0 0.4 (0.4) 1.4 3.7 2.4 N/A

Total 569.3 575.8 6.5 18.5 10.5 12.7 12.2 14.8 13.7 0.5

Aon Benfield | Analytics

Proprietary & Confidential 16

Drivers of 2013 Reserve Adequacy Deterioration All Lines

The total amount of industry reserve redundancy declined USD2.7B during 2013

Waterfall exhibit shows that the decline is driven by:

– Large amount of reserves released during 2013 of USD14.8B, offset by

– Favorable loss emergence from prior years worth USD11.9B

Most of the reserve cushion of USD6.5B at YE2013 has already been released as of Q1 2014, with

USD5.4B in reserve releases

+9.2

+6.5

(14.8)

+11.9 +0.2

-10

-5

0

5

10

15

YE2012Reserve

Redundancy

ReservesRelease During

2013

Prior YearFavorable Loss

Emergence

Accident Year2013

Redundancy

YE2013Reserve

Redundancy

Drivers of 2013 Reserve Adequacy DeteriorationAll Lines ($B)

Aon Benfield | Analytics

Proprietary & Confidential 17

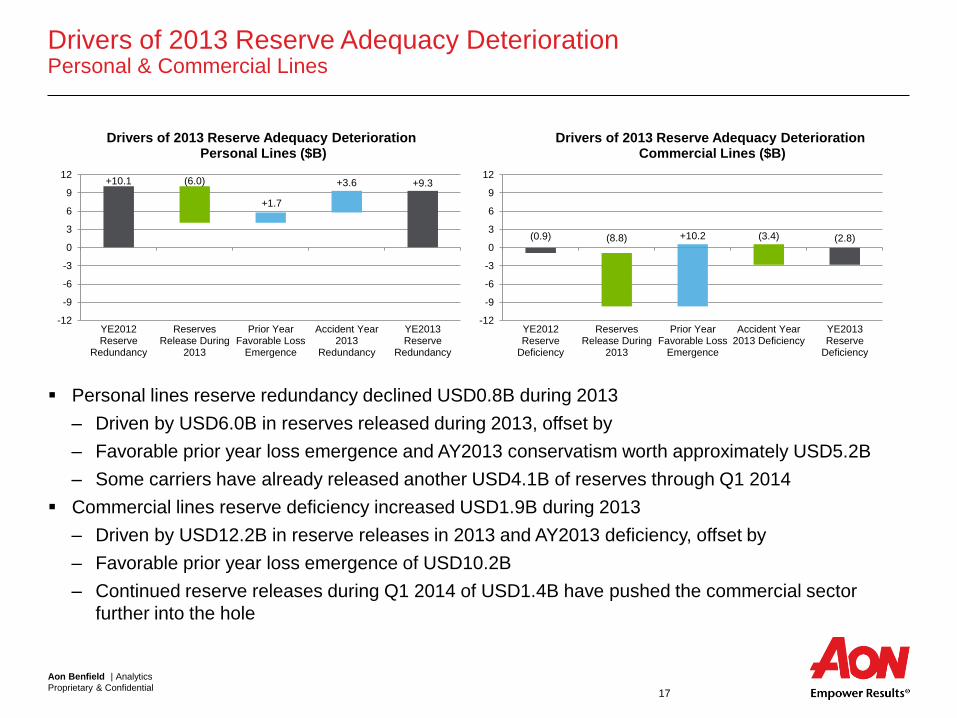

Drivers of 2013 Reserve Adequacy Deterioration Personal & Commercial Lines

Personal lines reserve redundancy declined USD0.8B during 2013

– Driven by USD6.0B in reserves released during 2013, offset by

– Favorable prior year loss emergence and AY2013 conservatism worth approximately USD5.2B

– Some carriers have already released another USD4.1B of reserves through Q1 2014

Commercial lines reserve deficiency increased USD1.9B during 2013

– Driven by USD12.2B in reserve releases in 2013 and AY2013 deficiency, offset by

– Favorable prior year loss emergence of USD10.2B

– Continued reserve releases during Q1 2014 of USD1.4B have pushed the commercial sector

further into the hole

+10.1 +9.3(6.0)

+1.7

+3.6

-12

-9

-6

-3

0

3

6

9

12

YE2012Reserve

Redundancy

ReservesRelease During

2013

Prior YearFavorable Loss

Emergence

Accident Year2013

Redundancy

YE2013Reserve

Redundancy

Drivers of 2013 Reserve Adequacy Deterioration Personal Lines ($B)

(0.9) (2.8)(8.8) +10.2 (3.4)

-12

-9

-6

-3

0

3

6

9

12

YE2012Reserve

Deficiency

ReservesRelease During

2013

Prior YearFavorable Loss

Emergence

Accident Year2013 Deficiency

YE2013Reserve

Deficiency

Drivers of 2013 Reserve Adequacy Deterioration Commercial Lines ($B)

Aon Benfield | Analytics

Proprietary & Confidential 18

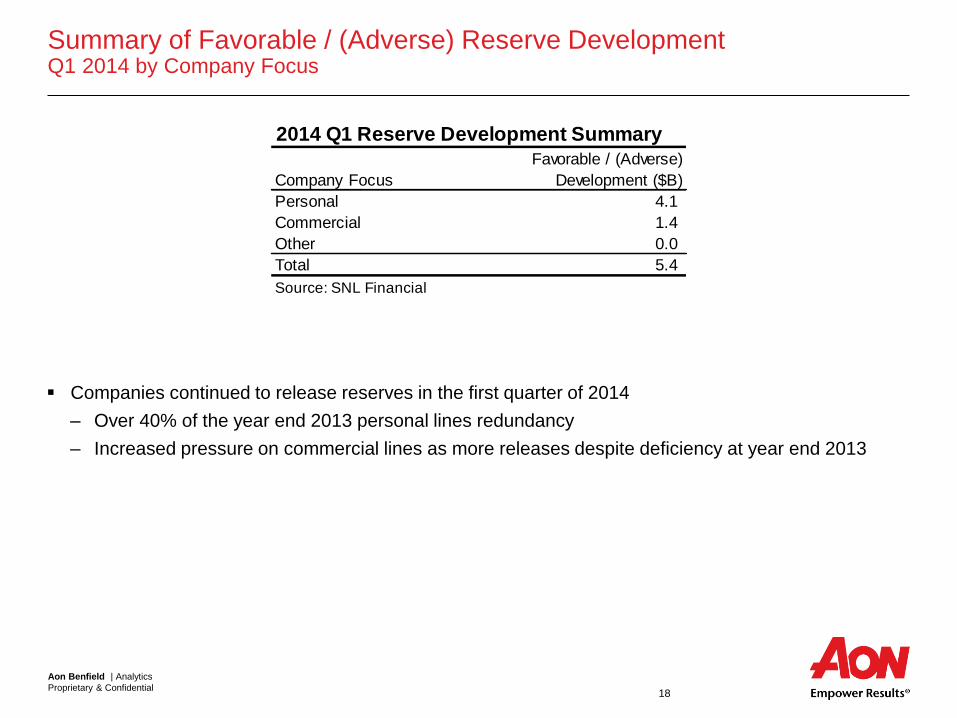

Summary of Favorable / (Adverse) Reserve Development Q1 2014 by Company Focus

Companies continued to release reserves in the first quarter of 2014

– Over 40% of the year end 2013 personal lines redundancy

– Increased pressure on commercial lines as more releases despite deficiency at year end 2013

2014 Q1 Reserve Development Summary

Company Focus

Favorable / (Adverse)

Development ($B)

Personal 4.1

Commercial 1.4

Other 0.0

Total 5.4

Source: SNL Financial

Aon Benfield | Analytics

Proprietary & Confidential 19

U.S. Reserve Volatility By Line, By Carried Reserve Size

U.S. Reserve Volatility by Line, by Reserve Size

One Year Reserve CV Ultimate Reserve CV

Line

Small

$10M - $100M

Medium

$100M - $500M

Large

> $500M

Small

$10M - $100M

Medium

$100M - $500M

Large

> $500M

All Lines 11.1% 8.4% 5.8% 13.8% 10.6% 7.4%

Homeow ners 16.7% 12.6% 10.0% 19.2% 14.4% 11.0%

Private Passenger Auto 8.9% 6.5% 3.0% 11.2% 7.7% 3.5%

Commercial Auto 12.5% 6.8% 4.4% 16.0% 9.0% 5.9%

Commercial Multi Peril 12.5% 10.6% 6.7% 16.4% 14.4% 8.5%

Workers Compensation 7.3% 5.3% 2.4% 9.7% 7.1% 3.7%

Medical PL - CM 17.8% 13.0% 7.6% 21.2% 15.8% 9.8%

Other Liability - CM 14.3% 15.1% 11.3% 17.2% 18.6% 14.1%

Other Liability - Occ 15.2% 11.9% 5.9% 19.0% 14.9% 8.8%

Products Liability - Occ 18.0% 12.7% 4.3% 23.5% 19.5% 11.0%

Ultimate reserve CV calculated using average of Mack and ODP Bootstrap methods applied to paid loss triangles by line. One-year reserve CV uses

average of the Merz-Wuthrich and ODP Bootstrap methods. All methods adjusted to account for tail factor volatility and reserves more than 10 years

old.

Section 3: Global Correlation Between Lines

Aon Benfield | Analytics

Proprietary & Confidential 21

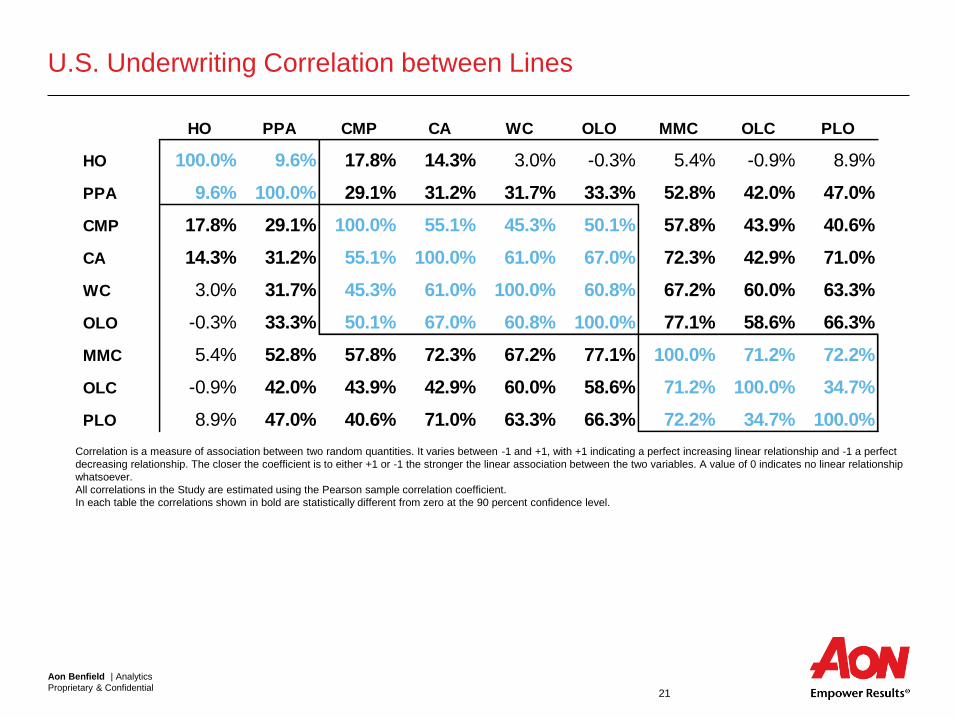

U.S. Underwriting Correlation between Lines

HO PPA CMP CA WC OLO MMC OLC PLO

HO 100.0% 9.6% 17.8% 14.3% 3.0% -0.3% 5.4% -0.9% 8.9%

PPA 9.6% 100.0% 29.1% 31.2% 31.7% 33.3% 52.8% 42.0% 47.0%

CMP 17.8% 29.1% 100.0% 55.1% 45.3% 50.1% 57.8% 43.9% 40.6%

CA 14.3% 31.2% 55.1% 100.0% 61.0% 67.0% 72.3% 42.9% 71.0%

WC 3.0% 31.7% 45.3% 61.0% 100.0% 60.8% 67.2% 60.0% 63.3%

OLO -0.3% 33.3% 50.1% 67.0% 60.8% 100.0% 77.1% 58.6% 66.3%

MMC 5.4% 52.8% 57.8% 72.3% 67.2% 77.1% 100.0% 71.2% 72.2%

OLC -0.9% 42.0% 43.9% 42.9% 60.0% 58.6% 71.2% 100.0% 34.7%

PLO 8.9% 47.0% 40.6% 71.0% 63.3% 66.3% 72.2% 34.7% 100.0%

Correlation is a measure of association between two random quantities. It varies between -1 and +1, with +1 indicating a perfect increasing linear relationship and -1 a perfect

decreasing relationship. The closer the coefficient is to either +1 or -1 the stronger the linear association between the two variables. A value of 0 indicates no linear relationship

whatsoever.

All correlations in the Study are estimated using the Pearson sample correlation coefficient.

In each table the correlations shown in bold are statistically different from zero at the 90 percent confidence level.

Aon Benfield | Analytics

Proprietary & Confidential 22

Volatility and Correlation Link to Volume

Volatility decreases as volume

grows, as impact of process

risk diversifies away, leaving

systemic/parameter risk

Correlation between segments

increases as volume grows, as

impact of process risk diversifies

away

Segment Volume

Volatility

Correlation

Aon Benfield | Analytics

Proprietary & Confidential 23

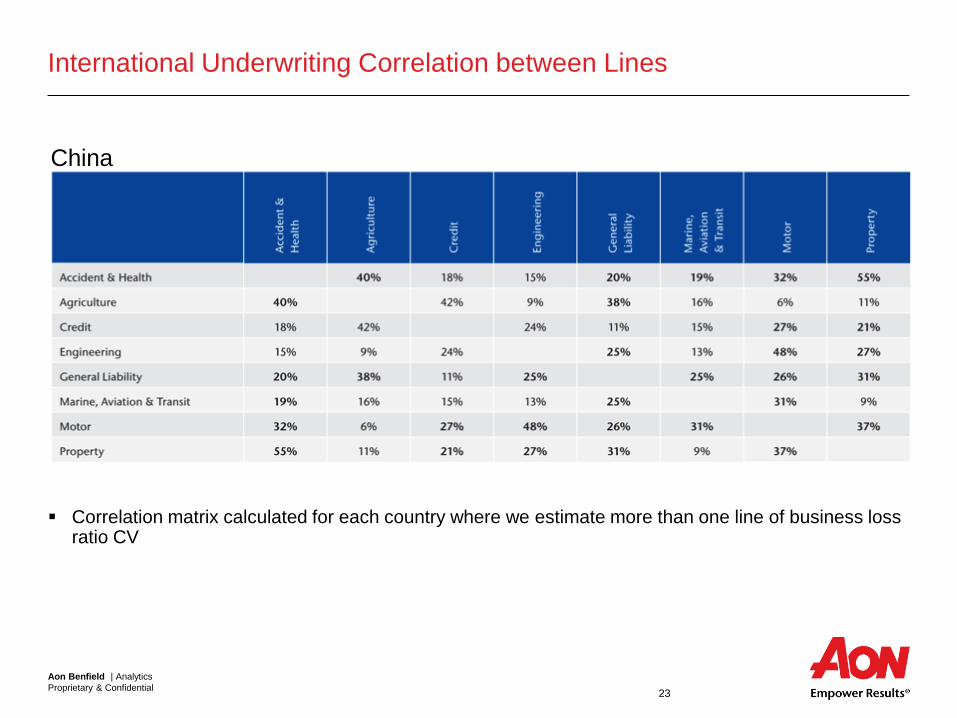

International Underwriting Correlation between Lines

Correlation matrix calculated for each country where we estimate more than one line of business loss ratio CV

China

Section 4: Macroeconomic Correlation

Aon Benfield | Analytics

Proprietary & Confidential 25

U.S. Macroeconomic Correlation

Aon Benfield | Analytics

Proprietary & Confidential 26

U.S. Macroeconomic Correlation Highlights

CPI and PPI highly correlated, but not strong with other factors

GDP growth shows strong negative correlation with changes in unemployment

Treasury yields and corporate bond spreads are inversely related

VIX is sensitive to fear and directionally has the appropriate signs:

– Positive correlation with spreads and unemployment

– Negative correlation with GDP and equity returns

Section 5: Global Premium, Profitability and Opportunities

Aon Benfield | Analytics

Proprietary & Confidential 28

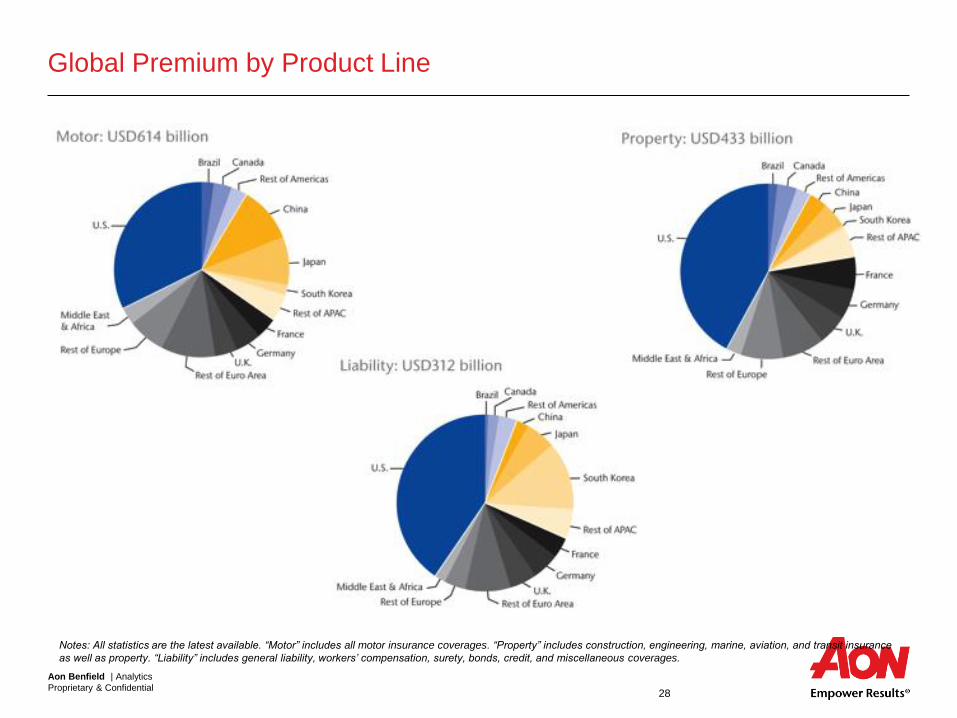

Global Premium by Product Line

Notes: All statistics are the latest available. “Motor” includes all motor insurance coverages. “Property” includes construction, engineering, marine, aviation, and transit insurance

as well as property. “Liability” includes general liability, workers’ compensation, surety, bonds, credit, and miscellaneous coverages.

Aon Benfield | Analytics

Proprietary & Confidential 29

Top 50 P&C Markets by Gross Written Premium

Aon Benfield | Analytics

Proprietary & Confidential 30

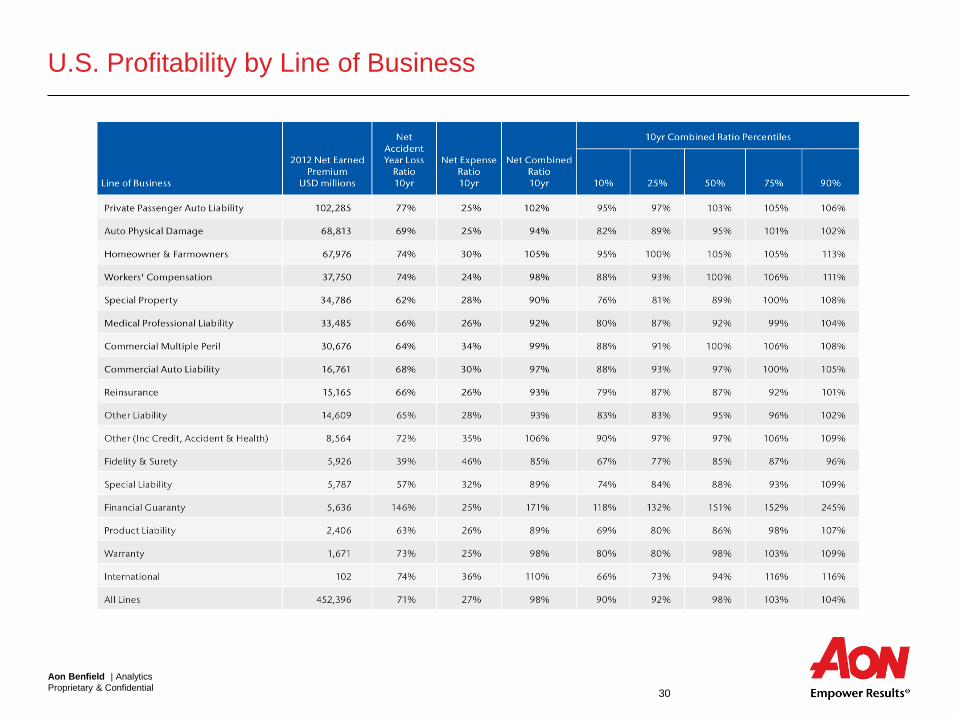

U.S. Profitability by Line of Business

Aon Benfield | Analytics

Proprietary & Confidential 31

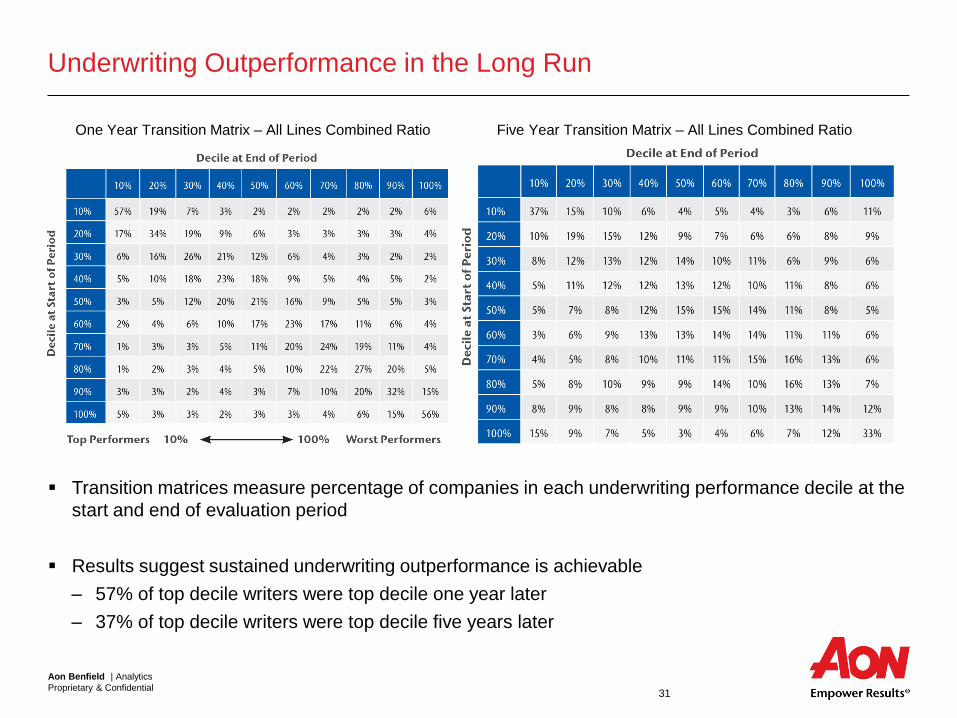

Underwriting Outperformance in the Long Run

One Year Transition Matrix – All Lines Combined Ratio Five Year Transition Matrix – All Lines Combined Ratio

Transition matrices measure percentage of companies in each underwriting performance decile at the

start and end of evaluation period

Results suggest sustained underwriting outperformance is achievable

– 57% of top decile writers were top decile one year later

– 37% of top decile writers were top decile five years later

Aon Benfield | Analytics

Proprietary & Confidential 32

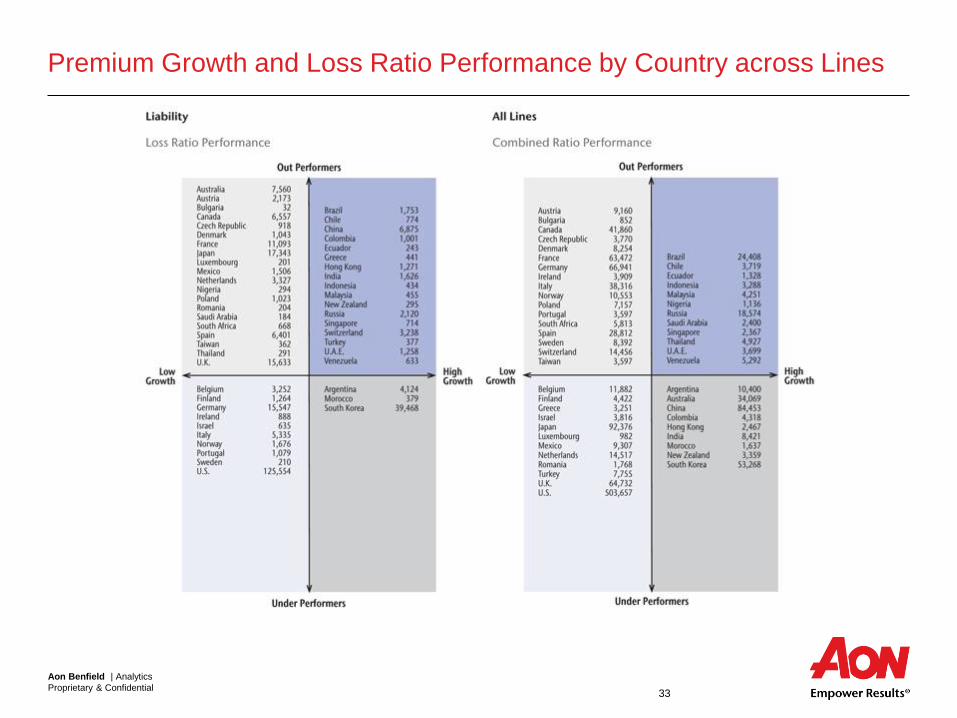

Premium Growth and Loss Ratio Performance by Country across Lines

Aon Benfield | Analytics

Proprietary & Confidential 33

Premium Growth and Loss Ratio Performance by Country across Lines

Aon Benfield | Analytics

Proprietary & Confidential 34

Aon Benfield Country Opportunity Index

Aon Benfield | Analytics

Proprietary & Confidential 35

Contender Geography Growth, Profitability and Volatility

Aon Benfield | Analytics

Proprietary & Confidential 36

Contender Geography Demographics

Aon Benfield | Analytics

Proprietary & Confidential 37

Contender Geography Credit Rating and Risk Perspectives

Aon Benfield | Analytics

Proprietary & Confidential 38

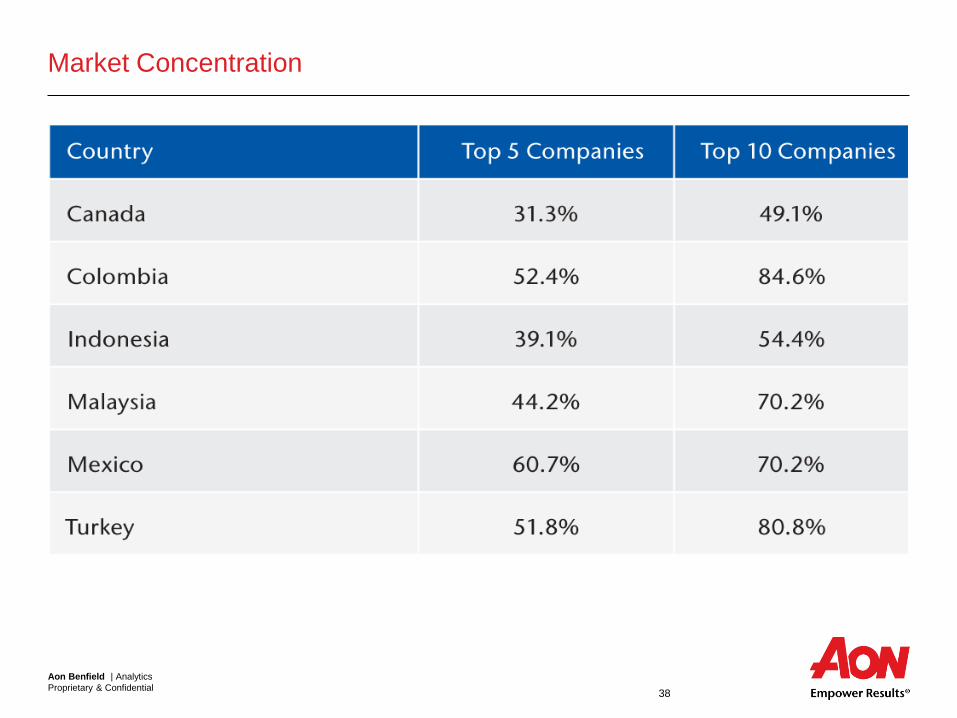

Market Concentration

Section 6: Extending Insurance-Linked Securities

Aon Benfield | Analytics

Proprietary & Confidential 40

Characteristics of Property Cat Risk

Natural Demand Property values and demographics have driven huge concentrations in the industry relative to even today’s very adequate capital levels, which in turn drives a natural demand for risk transfer products.

Loss Modeling The development of computer models for natural catastrophes, on-going since the late 1980’s, has created a generally accepted “currency” to value the loss potential a given risk portfolio. Modeling has been successful in part because natural catastrophe events are driven by laws of nature and are not social science phenomenon with changing, reflexive and reactive parameters and causes.

Loss Triggers Modeling, and the physical drivers of loss, also allows for a range of non-indemnity loss triggers.

Rating Agency Capital Rating agency capital models have separated out catastrophe risk and assigned a clearly defined capital charge specifically to cover it, unencumbered by complications of diversification benefits and other technicalities. The rating agency credit is often as much, or greater than, a company’s own economic capital model credit.

Credit Risk Purchasers of traditional covers are always concerned with the credit risk of the product they purchase, especially for top layers, as well as the historical volatility in pricing and availability. As a result, they are open to alternative solutions and find fully collateralized ILS structures very attractive.

Aon Benfield | Analytics

Proprietary & Confidential 41

Characteristics of Property Cat Risk, ctd.

Default Profile The loss profile of high layer catastrophe programs mirrors bond default profiles very closely: there is a low probability of a loss, but given a loss a reasonably high probability of a total loss, producing a loss profile familiar to fixed income investors.

Equity Tranche As a result of the loss profile, there is no need for an equity tranche in a cat bond. Equity tranches are a big complication in many (non-insurance) securitizations because they create a Variable Interest Entity (VIE) residual interest that generally remains on the balance sheet of the issuer.

Uncorrelated Returns The loss profile of cat bonds is manifestly uncorrelated with other asset classes, at least a priori. Investors saw the attractiveness of the ILS asset class during the financial crisis (collateral trust problems notwithstanding, but these problems have now been solved).

Quick Emergence Major property catastrophe risk events are headline news; the fact of a loss or potential loss emerges very quickly, indeed instantaneously for earthquakes.

Quick Loss Settlement Losses from property catastrophe events generally reach their final settlement valuation in a matter of months. There are very few issues with late reported claims or slow loss development.

Aon Benfield | Analytics

Proprietary & Confidential 42

Lines Potentially Suitable for Non-Cat Securitizations

Characteristic

Property

Risk

Workers

Comp

Commercial

Auto

Medical

PL Vanilla GL D&O Aviation

General Comments

Poor to

moderate data

Large losses

Data rich

Detailed rating

Good

exposures

Same as WC

Extends

personal auto

Frequency

risk = tort

reform

Data rich

Detailed rating

Heterogeneous

Data rich

Systemic?

Data rich

Already cat like

Natural Demand

(Reinsurance

purchased)

High limit

occurrence

Occ and

cat with

MOAL

Some occ Moderate

occ / agg

Little for low

limits

Little, unapp-

etizing product

Substantial; but

traditional is

cheap

Loss Modeling Evolving, no

standard

Predictive

models

Predictive

models

Good, but

tort risk

Predictive

models

Varies by

primary carrier

Very good;

AeroMetrica

Uncorrelated Returns / Terror / Terror ? / Terror

Quick Emergence Slow

Good:

claims

made

Moderate Good: claims

made Fast

Quick Loss Settlement

Slow, but

consistent;

BobCat

solution

Moderate

Slow

CWA vs

CWOP

Moderate Moderate Moderate

Aon Benfield | Analytics

Proprietary & Confidential 43

Contacts

Brian Alvers, FCAS, MAAA

Head of Actuarial - Americas

Aon Benfield Analytics

+1.312.381.5355