December 1, 2016

Christopher M. Holt, ACAS, MAAALegaré Gresham, FCAS, MAAA

Insurance and Technology: Are You Prepared for the Coming Disruptions?

1

About Presenters

• Christopher M. Holt, ACAS, MAAA• Consulting Actuary• Atlanta, Georgia• Pinnacle Actuarial Resources, Inc.

• Legaré Gresham, FCAS, MAAA• Consulting Actuary• Atlanta, Georgia• Pinnacle Actuarial Resources, Inc.

2

• Introduction

• Future Technologies

– Autonomous / Driverless Cars

– Wearables

– Connected Homes

– Drones

– Financial Technology

– Artificial Intelligence

• Wrap-up

Agenda

3

Introduction - “May you live in interesting times!”

Sources: U.S. Patent and Trademark Officehttps://www.uspto.gov/web/offices/ac/ido/oeip/taf/us_stat.htmhttp://www.multpl.com/united-states-population/table

4

• Driverless - A robotic vehicle that is designed to travel between destinations without a human operator

• Sometimes called a self-driving car, an automated car or an autonomous vehicle

Autonomous/Driverless Cars

5

• Where are we now?

– Features already available on mainstream cars include self parking, adaptive cruise control, lane-keeping, automatic braking (classified as Level 2 by NHTSA)

– Testing of Levels 3 and 4 ongoing

Autonomous/Driverless Cars

6

• Where are we now?

– Features already available on mainstream cars include self parking, adaptive cruise control, lane-keeping, automatic braking (classified as Level 2 by NHTSA)

– Testing of Levels 3 and 4 ongoing

• Where might this go?

– Will we skip Level 3?

– Level 4 – As early as 2019?

– Could car ownership become a thing of the past?

Autonomous/Driverless Cars

7

• Change in how we drive– Car ownership – Average vehicle age ~11.5 years– Number of vehicles/miles driven

• Claims– Frequency decrease– Severity increase – Injury/Repair

• Liability – Who’s at fault?• Insurance Regulation

– No-fault– Tort systems

• Underwriting– Use of telematics/UBI– Who is buying/selling policies?

• Cyber Risk• APEX on December 15

Effects of Autonomous/Driverless Cars

8

• Electronics that can be worn on the body, either as an accessory or as part of material used in clothing.

• One of the major features of wearable technology is its ability to connect to the Internet, enabling data to be exchanged between a network and the device.

Wearables

9

• Where are we now?

– Wristbands/Smartwatches/Glasses

– Usually need to pair with another device

– Bulky

– Limited battery life

– Accuracy Concerns

Wearables

0

5,000

10,000

15,000

20,000

25,000

2010 2011 2012 2013 2014 2015

Number of Fitbit devices sold worldwide from 2010 to 2015 (in

1,000s)

Source: https://www.statista.com/statistics/472591/fitbit-devices-sold

10

• Where are we now?

– Wristbands/Smartwatches/Glasses

– Usually need to pair with another device

– Bulky

– Limited battery life

– Accuracy Concerns

• Where might this go?

– Wearable clothing – power source?

– Nanosensors – Heart rate sensors, speech

– Synthetic skin

Wearables

0

5,000

10,000

15,000

20,000

25,000

2010 2011 2012 2013 2014 2015

Number of Fitbit devices sold worldwide from 2010 to 2015 (in

1,000s)

Source: https://www.statista.com/statistics/472591/fitbit-devices-sold

11

• Marketing/Underwriting– New product development

– Bonus/penalty programs

• Risk Management– Monitoring pilot or truck driver fatigue

– Return-to-work programs

• Workers’ Compensation– Monitoring personnel handling hazardous materials or in

dangerous situations

– Tracking the position and status of employees

– Is there liability because company does not invest in wearable?

Effects of Wearables

12

• Health/Life Insurance

• Claims Management

– Document damages, take statements, share with others

– Document lifestyle changes

• Cyber Risk/Privacy Concerns

Effects of Wearables

13

– A development of the Internet in which everyday objects have network connectivity, allowing them to send and receive data

Connected Homes/Products

14

• Where are we now?– Cool Gadgets

• Refrigerators – cameras, smart screens

• Learning Systems – thermostats, smoke alarms

• Security Systems

• Voice Control Systems – Alexa, Google Home

– Fragmented

– Costly

Connected Homes/Products

15

• Where are we now?– Cool Gadgets

• Refrigerators – cameras, smart screens

• Learning Systems – thermostats, smoke alarms

• Security Systems

• Voice Control Systems – Alexa, Google Home

– Fragmented

– Costly

• Where might this go?– Home systems will be automated, personalized and optimized

– Connected classrooms/connected communities

Connected Homes/Products

16

• Risk Management

– Monitoring home or workspace

• Privacy Concerns

– Availability on the web

• Product Liability

• Cyber Risk

– Peeping – or “Cyber” – Toms

– False alerts

– Criminal use of data

Effects of Connected Homes/Products

17

• An aircraft without a human pilot aboard

• Also referred to as an unpiloted aerial vehicle and a remotely piloted aircraft by the International Civil Aviation Organization

Drones

18

Drones

• Where are we now?– Delivering burritos at Virginia Tech

– Racing drones

– Surfing with drones

– Drones kill Dallas shooter

19

• Where are we now?– Delivering burritos at Virginia Tech

– Racing drones

– Surfing with drones

– Drones kill Dallas shooter

• Where might this go? (FAA Part 107)– Hazardous jobs

– Meter reading

– Construction

– Spying

Drones

20

• Insurance

– Commercial and Personal Liability Insurance

– Property Considerations

• Can view property remotely to bind coverage

• Can view an insured’s roof without climbing up

• Can send to crash site

– Privacy Concerns

– Product Liability

Effects of Drones on Insurance

21

• Over 40 recalls since 2002, notably:

– Individual parts tested/certified but parts may not have been tested together

– Competition/rush to market

Drones and Lithium Ion Batteries

Year Event

2006 Sony recalls ~9.6 million laptop batteries

2013 Boeing grounds 787 Dreamliners for several

months due to overheating batteries igniting

2015 Several airlines stop carrying bulk shipments

after series of explosions beginning in 2010

2015 Exploding hoverboards

2016 Samsung Galaxy Note 7

2010-

Present

Plug-In electric vehicle fires

Source: http://www.livescience.com/50643-watch-lithium-battery-explode.htm

22

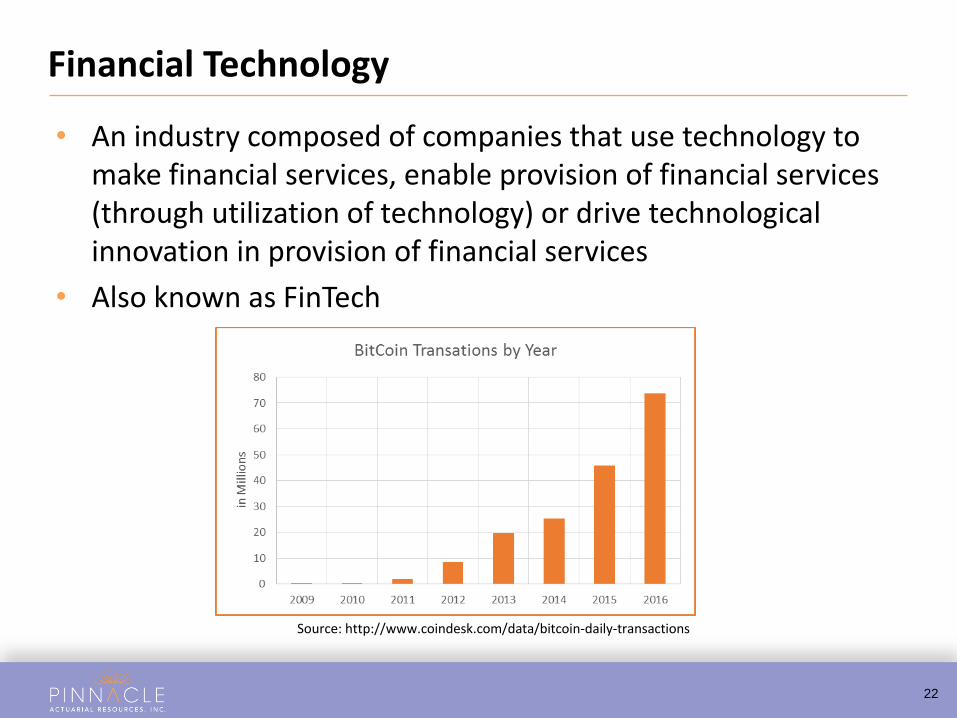

• An industry composed of companies that use technology to make financial services, enable provision of financial services (through utilization of technology) or drive technological innovation in provision of financial services

• Also known as FinTech

Financial Technology

Source: http://www.coindesk.com/data/bitcoin-daily-transactions

23

• Where are we now?– Amazon.com

– PayPal, other on-line billing services

– eTrade

– Openbazaar.org

Financial Technology

24

• Where are we now?– Amazon.com

– PayPal, other on-line billing services

– eTrade

– Openbazaar.org

• Where might this go?– Full peer-to-peer transactions

– Contract binding

– New payment methods or currencies

Financial Technology

25

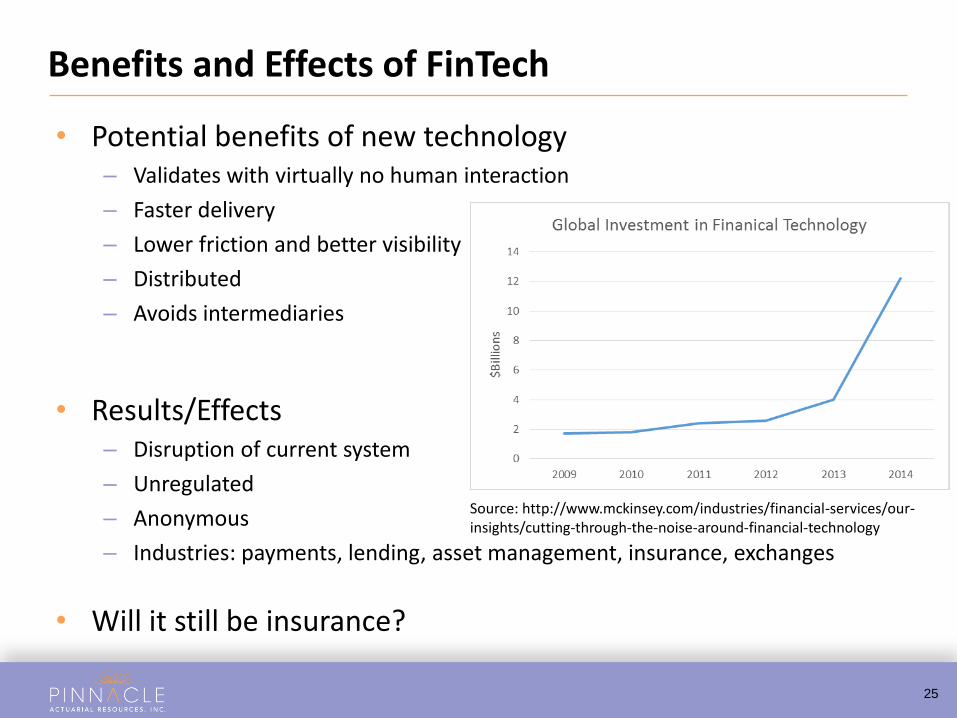

• Potential benefits of new technology– Validates with virtually no human interaction

– Faster delivery

– Lower friction and better visibility

– Distributed

– Avoids intermediaries

• Results/Effects– Disruption of current system

– Unregulated

– Anonymous

– Industries: payments, lending, asset management, insurance, exchanges

• Will it still be insurance?

Benefits and Effects of FinTech

Source: http://www.mckinsey.com/industries/financial-services/our-insights/cutting-through-the-noise-around-financial-technology

26

• The theory and development of computer systems able to perform tasks that normally require human intelligence, such as visual perception, speech recognition, decision-making, and translation between language

Artificial Intelligence

27

• Where are we now?

– Neural networks or machine learning

– Optical charter recognition

– Driverless cars

– Watson – natural language processing

– Abie – Allstate Business Insurance Expert

– Evia – Insurify (virtual insurance agent)

Source: Bloomberg Technology

Artificial Intelligence

28

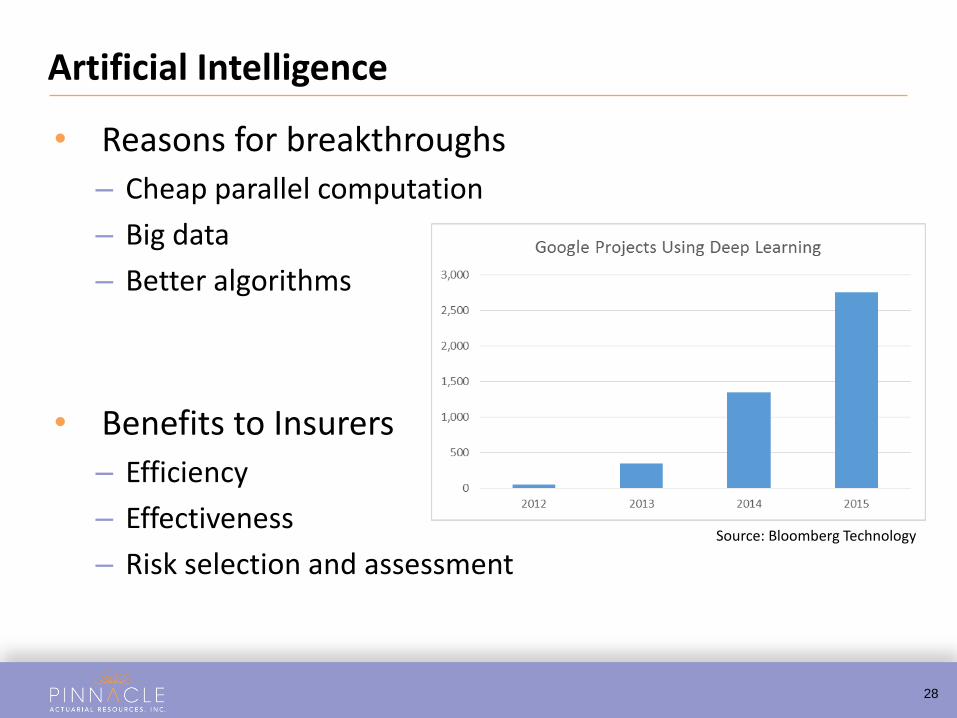

• Reasons for breakthroughs

– Cheap parallel computation

– Big data

– Better algorithms

• Benefits to Insurers

– Efficiency

– Effectiveness

– Risk selection and assessment

Artificial Intelligence

Source: Bloomberg Technology

29

• Where might this go?

– Underwriting and risk identification

– Customer experience

– Claims handling

– Fraud

– Actuarial

Artificial Intelligence

30

Autonomous / Driverless Cars

Wearables

Connected Homes

Polling Question

Which technology do you think will have the greatest impact on insurance in the next 5 years?

Drones

Financial Technology

A

B

C

D

E

Artificial IntelligenceF

31

Questions

32

Join Us for the Next APEX Webinar

33

• We’d like your feedback and suggestions

• Please complete our survey

• For copies of this APEX presentation

• Visit the Resource Knowledge Center at Pinnacleactuaries.com

Final notes

34Commitment Beyond Numbers

Thank You for Your Time and Attention

Chris Holt

Legaré Gresham