IFRS 4 – Insurancecontracts

www.pwc.co.uk

Andre RohayemME insurance leader

November 2015

PwC

Agenda

IFRS 4 Phase I:key impacts

IFRS 4 Phase II:Measurementmodels

Transition anddisclosures

Financialreporting vsRegulatoryframework

Implications forinsurers

1 2

3 4

5 6

2November 2015

7 Appendix

PwC

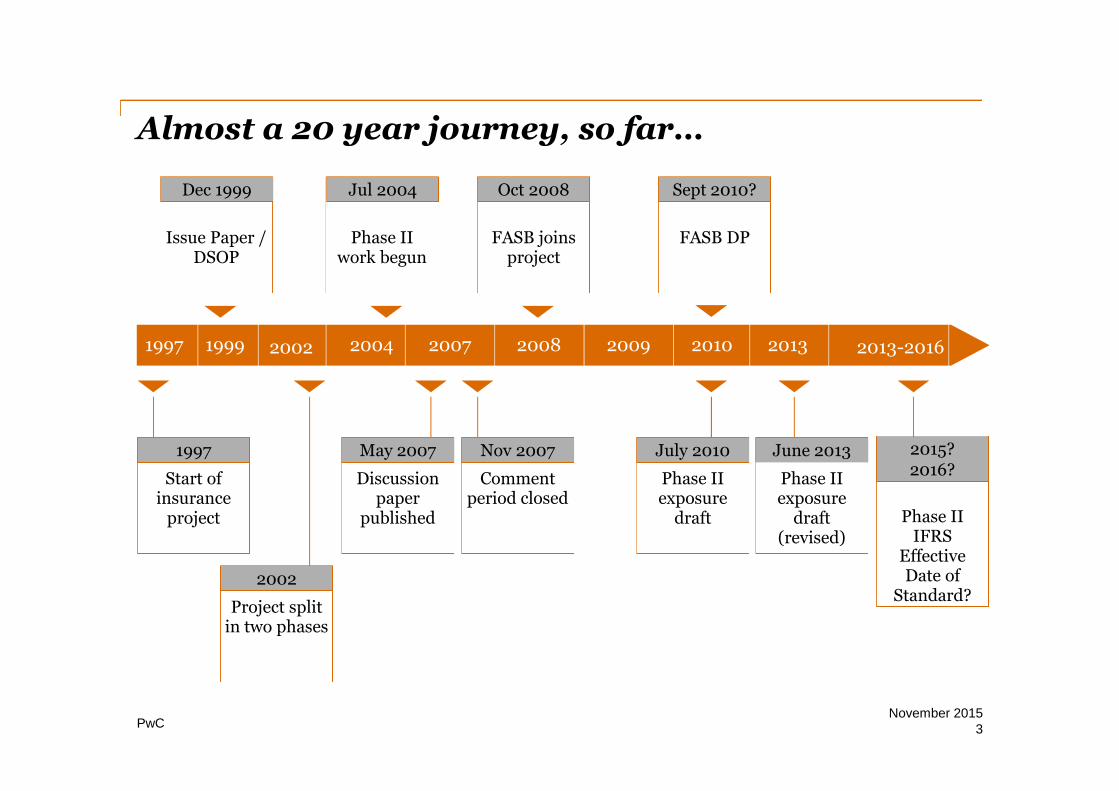

Almost a 20 year journey, so far…

Discussionpaper

published

May 2007

Commentperiod closed

Nov 2007

Phase IIexposure

draft

July 2010

Phase IIexposure

draft(revised)

June 2013

Phase IIIFRS

EffectiveDate of

Standard?

2015?2016?

Start ofinsurance

project

1997

1997 1999 2004 2007 2008 2009 2010 2013 2013-2016

Oct 2008

FASB DP

Sept 2010?

FASB DP

Sept 2010?

FASB joinsproject

Oct 2008

November 20153

Phase IIwork begun

Jul 2004

Issue Paper /DSOP

Dec 1999

2002

Project splitin two phases

2002

PwC

IFRS 4 Phase I:Key impacts

4November 2015

PwC

Definition of an Insurance Contract

November 20155

“A contract under which one party (the insurer) accepts significantinsurance risk from another party (the policyholder) by agreeing to

compensate the policyholder if a specified uncertain future event (theinsured event) adversely affects the policyholder.”

• Insurance risk = other than financial risk

• Uncertainty: if, when or how much

• Same definition for reinsurance

PwC

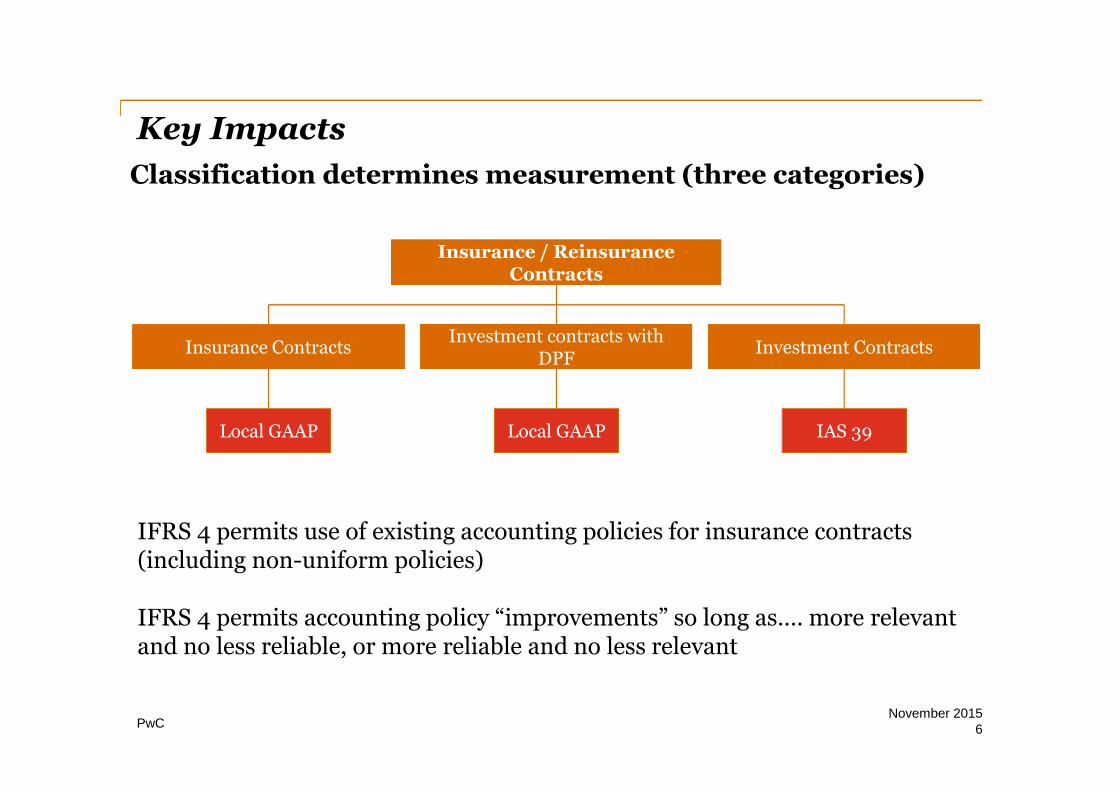

Key Impacts

November 20156

Classification determines measurement (three categories)

Insurance / ReinsuranceContracts

Investment ContractsInvestment contracts with

DPFInsurance Contracts

Local GAAP Local GAAP IAS 39

IFRS 4 permits use of existing accounting policies for insurance contracts(including non-uniform policies)

IFRS 4 permits accounting policy “improvements” so long as…. more relevantand no less reliable, or more reliable and no less relevant

PwC

Key Impacts

November 20157

Changes introduced by IFRS 4

• ‘Insurance contract’ defined – determines if contract in IFRS 4 or IAS 39

• Equalisation provisions - eliminated

• Liability adequacy test – introduced and required

• Embedded derivatives – accounting in certain cases

• Discretionary participation feature - introduced

• Unbundling – introduced and required in certain cases

• No offsetting of reinsurance against related insurance - balance sheet and inP&L

• Reinsurance asset impairment testing - required

• Accounting policy improvements - introduced to assist insurers duringPhase I.

PwC

Disclosures

November 20158

• Accounting policies

• Assumptions used in determining insurance liabilities

• Effect of changes in assumptions

• Management of Insurance risk (incl. financial risk, currency risk, credit risk)

• Movement in insurance liabilities and reinsurance assets

• Claims development tables

• Other

PwC

IFRS 4 Phase II:Measurement models

November 20159

PwC

Measurement models

Undiscountedreserves forpast claims(including

IBNR)

CurrentIFRS/GAAP

BBA throughout PAA PAA andundiscounted

incurred claims

Discounting

Risk adjustment

Best estimate offulfilment cash flows

Discounting

Risk adjustment

Best estimate offulfilment cash flows

Discounting

Risk adjustment

Best estimate offulfilment cash flows

Contractual ServiceMargin

UPR less DACPremium (less

acquisition costs)unearned

Premium (lessacquisition costs)

unearned

Ex

pir

ed

ris

kU

ne

xp

ire

dr

isk

Best estimate offulfilment cash flows

Risk adjustment

November 201510

PwC

Default measurement model in IFRS 4 Phase IIOverview of building block approach ‘BBA’

• Default model for all insurancecontracts.

• Based on discounted bestestimate of future cash flows.

• Explicit margins:

- Contractual service marginto prevent gain on policyinception.

- Risk adjustment.

• Day 1 loss recognised in incomestatement.

• Cash flow approach for allliabilities: past claims(including IBNR) andfuture cover.

Unearned profits recognised overcoverage period.

Reflect compensation for uncertainty.Quantifies the value difference betweencertain and uncertain liability.

Discounting future cash flows using‘top-down’ or ‘bottom-up’ approach fordiscount rates to reflect characteristicsof the liabilities.

Best estimate cash flows – explicit,unbiased and probability weightedestimate of fulfilment cash flows.

Discounting

Risk adjustment

Contractual servicemargin

Best estimate offulfilment cash flows

Expired and unexpired risk

November 201511

PwC

Optional model for short term contractsPremium Allocation Approach ‘PAA’

• Optional simplified model forfuture cover based on theunearned premium.

• Permitted for short durationcontracts (period of cover <= 1year) or where a ‘reasonableapproximation’ of BBA.

• ‘Reasonable approximation’does not apply when entityexpects significant variability incash flows – No furtherguidance on what this means.

• Incurred claims liability(including IBNR) calculatedin the same way as for theBBA approach.

Unexpired premiums lessacquisition costs

Discounting

Risk adjustment

Best estimate offulfilment cash flows*

Expired risk Unexpired risk

* Probability weighted,essentially a mean.

November 201512

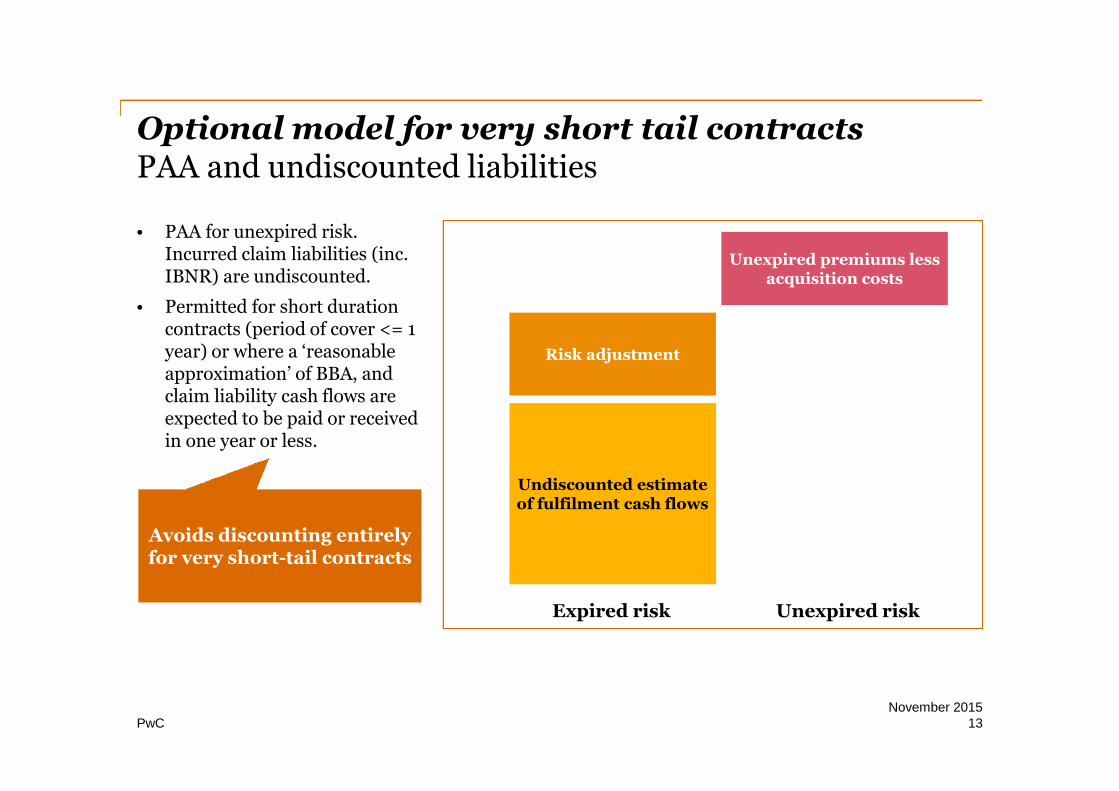

PwC

Optional model for very short tail contractsPAA and undiscounted liabilities

Unexpired premiums lessacquisition costs

Expired risk Unexpired risk

Risk adjustment

Undiscounted estimateof fulfilment cash flows

Avoids discounting entirelyfor very short-tail contracts

• PAA for unexpired risk.Incurred claim liabilities (inc.IBNR) are undiscounted.

• Permitted for short durationcontracts (period of cover <= 1year) or where a ‘reasonableapproximation’ of BBA, andclaim liability cash flows areexpected to be paid or receivedin one year or less.

13November 2015

PwC

Transition & Disclosures

14November 2015

PwC

Transition

• Each portfolio measured using BBA with contractual service margin

• Difference between BBA and current carrying value reflected in openingretained earnings

• Retrospective application unless impracticable

• If impracticable, simplifications required for building blocks:

• Derecognise balances for deferred acquisition costs

15November 2015

PwC

Disclosures

Amounts

• Detailed roll forward schedules andreconciliations

• Reconciliation of sources of profit• Contracts written in the period• Relationship interest and investment return

Significantjudgements

• Processes to estimate inputs to methods• Effect of changes in methods and inputs• Confidence level for determining risk

adjustment• Yield curve(s) used to discount cash flows

Nature and extentof risks

• Nature and extent of risks• Insurance risk on gross/net basis• Concentrations of insurance risk and claims

development• Quantitative disclosures on non-insurance risks

16November 2015

PwC

Financial reporting vsRegulatory framework

17November 2015

PwC

Financial reporting vs Regulatory framework

• Financial reporting and regulatory reporting under IFRS in Lebanon(impacted by local laws and Decrees for measurement of insuranceliabilities)

• No separate regulatory framework (ie Solvency II or equivalent)

• IFRS 4 Phase II: introduction of major changes to the measurementof insurance contracts and significant impact on financial statements

• Current regulatory framework not aligned to IFRS 4 Phase II

• Requirement to introduce a new regulatory framework (equivalent toSolvency II as mostly aligned to IFRS 4 Phase II)

• Significant implications on local insurance market and little time left

18November 2015

PwC

Implications forinsurers

19November 2015

PwC

Implications

• Impact on financial statements will vary for entities depending onnature of contracts and current local GAAP

• Likelihood of increased volatility since measurements reflect currentestimates

• Profit recognition on transition for existing contracts

• Measuring and communicating business performance

• Practical implementation issues (e.g. definition of cash flows,discount rate, risk margin, scope of stochastic modelling)

• Need for new systems and data and related staff training

November 201520

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon theinformation contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to theaccuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members,employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining toact, in reliance on the information contained in this publication or for any decision based on it.

© 2015 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers to the UK member firm, and may sometimes refer to the PwCnetwork. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

141229-145004-BO-OS

Thank you