IFRS 16 Seminar

One year later; your next stop before the IFRS 16 finish line

__________

20 March 2018

2© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

The contacts at KPMG in connection with this presentation are:

Ruben RogPartner KPMG Advisory N.V.T: +31 20 656 88 30E: [email protected]

Niels EbbinkhuijsenDirectorKPMG Advisory N.V.T: +31 20 656 86 85E: [email protected]

3© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

4© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

13:00 – 13:30 Registration

13:30 – 13:50 Welcome and introduction

13:50 – 14:30 KLM – the path to early adoption

14:30 – 15:10 Ahold Delhaize – a transition project in action

15:10 – 15:30 Break for coffee and a sandwich

15:30 – 16:00 LeasePlan – a lessor perspective

16:00 – 16:50 KPMG’s Global IFRS 16 Lead Brian O’Donovan

16:50 – 17:15 Tax perspective

17:15 Drinks reception

Agenda for today

5© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Today’s presenters (1/2)

Client perspective

Wim MolenaarAccounting & Reporting Air France KLM

Introduction

Niels

EbbinkhuijsenDirector CMAAS KPMG NL

Welcome

Ruben RogPartner CMAAS KPMG NL

Client perspective

Wouter Nijmeijer &

Maryke KeetSenior Vice President Accounting & Reporting, Risk & Controls Ahold Delhaize & Director Financial Reporting Ahold Delhaize

6© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Today’s presenters (2/2)

Tax perspective

Johan SwagersSenior Manager KPMG Meijburg

KPMG Global IFRS 16 LeadClient perspective

Ajolt BosLease Accounting Specialist LeasePlan

Brian

O’DonovanPartner KPMG International Standards Group

Polling statements and questions

8© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

A few polling statements and questions to start…

— Please get your mobile phone

— Go to: www.menti.com

— Fill in the code: 76 84 85

— And lets get started!

9© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

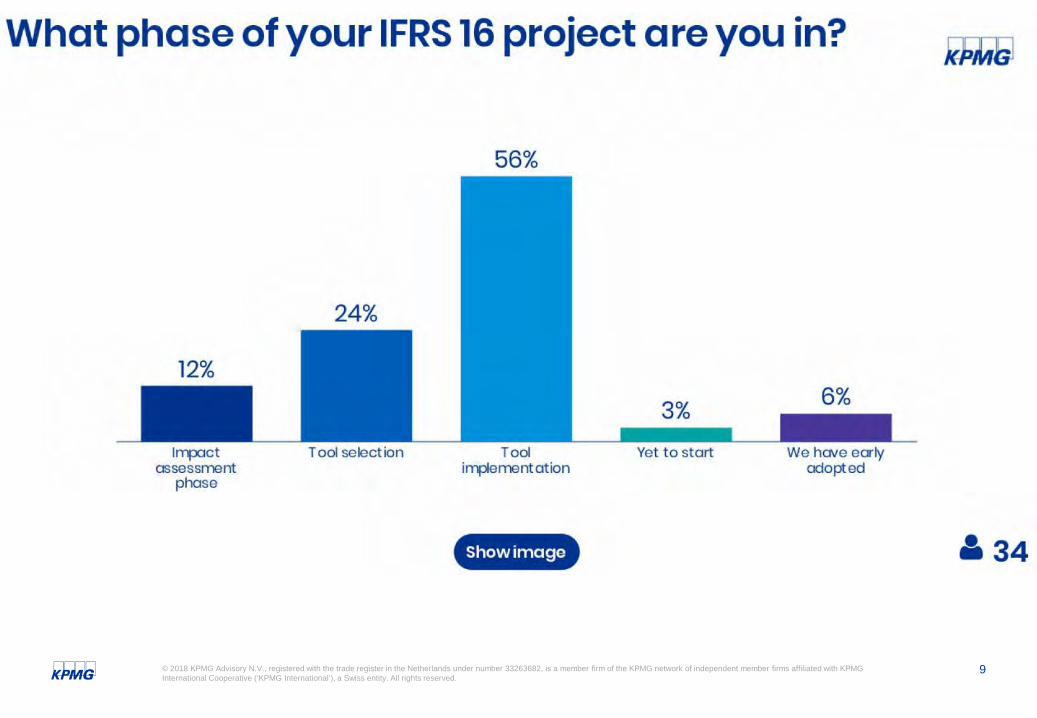

10© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

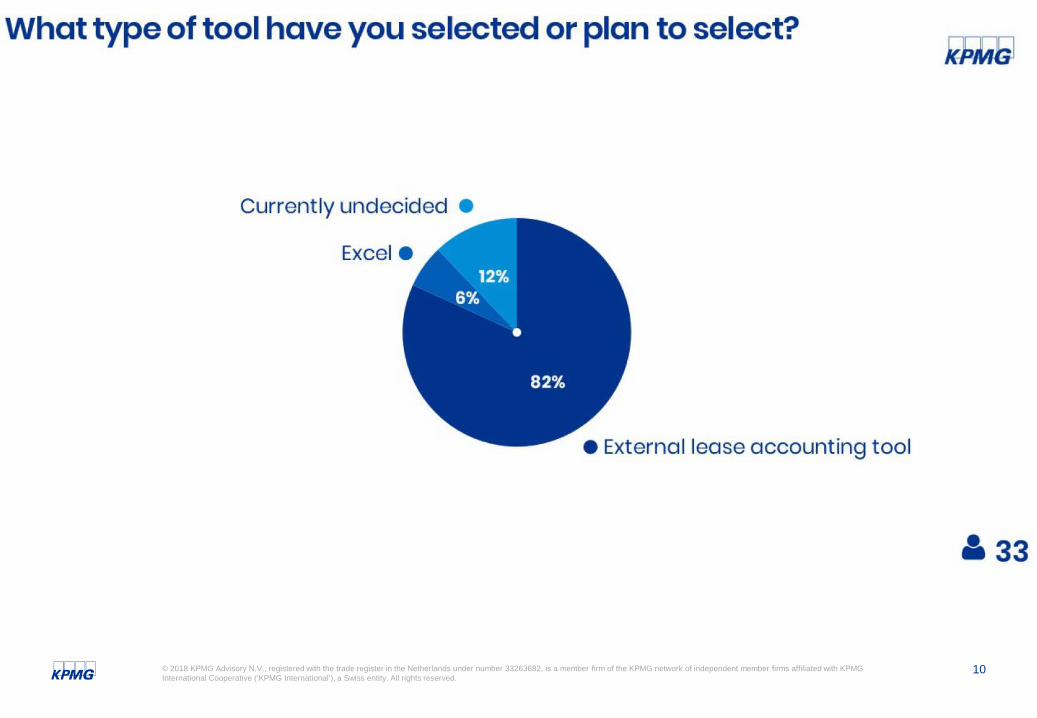

11© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

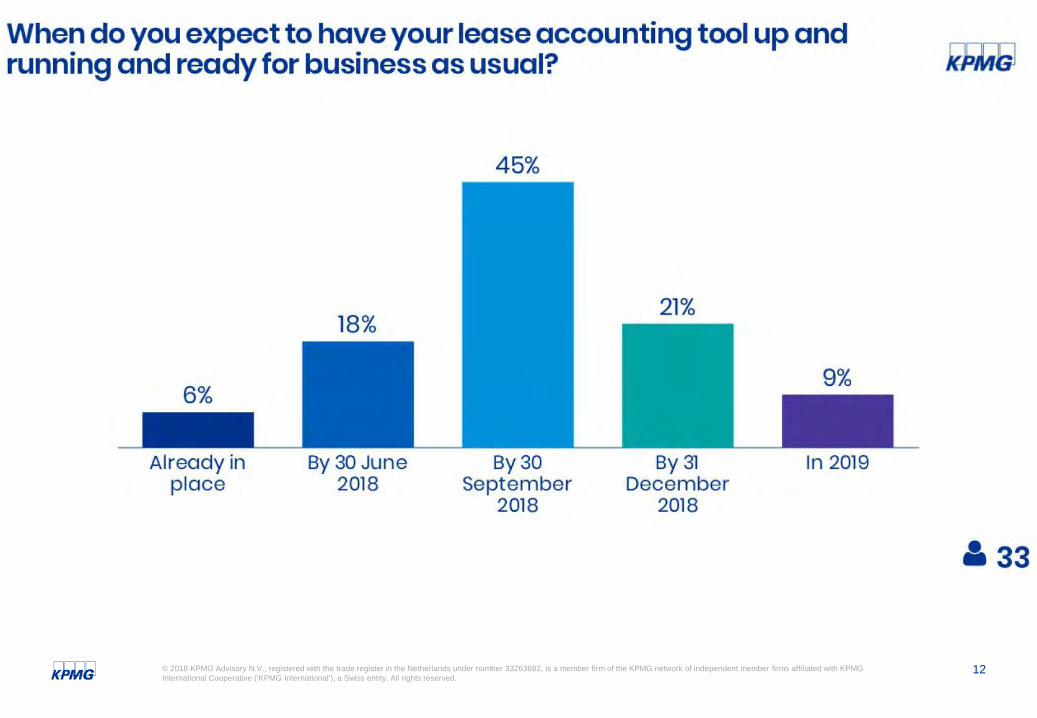

12© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

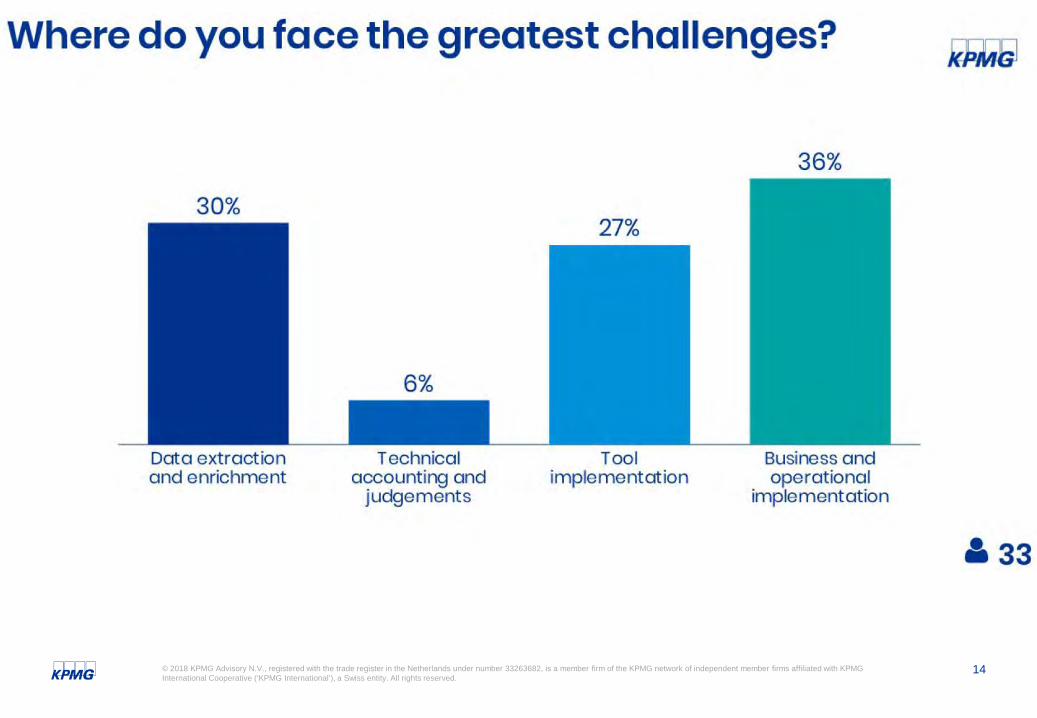

13© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

14© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

One year further -what has happened?

16© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

PROJECT STATUS

― Majority AEX companies is in (IT) implementation mode;

― Smaller listed companies and private equity owned companies are behind

ACCOUNTING JUDGEMENTS

— Challenges of determination of:- Discount rate; - Lease term

— Considering ‘short cuts’ from a materiality perspective PRACTICAL CHALLENGES

— Data collection:- Availability of necessary data points;- who owns the process?

— How does the lease process going forward look like?

— How to include IFRS 16 in budget/forecasting process?

Regulators

― EU endorsement is a fact; ― No ‘lighter’ approach allowed;― ESMA limited ‘instructions’ for IFRS 16, but still focussed on

IFRS 9 and IFRS 15― Silence from most

tax authorities

IFRS 16: One year further… some observations from KPMG

COMMUNICATIONS

― Need to determine plan to communicate with investors― Seems limited interest from analysts and financing

institutions to date― Current disclosure on operating leases

TRANSITION

— Limited early adoption (in general)— Most companies would ideally go “fully retrospective” but is

rather complex— Presentation of 5 year summary and non-GAAP measures

Observations

17© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Disclosure on IFRS 16 in 2017 financial statements – some observations

The other companies have chosen either the modified retrospective approach (45%) or

have not yet decided (43%)

20% of Dutch listed companies have quantified the expected impact of IFRS 16 in

their latest financial statements

4 companies reported that they are planning to apply the full retrospective approach to

transition.

35 Dutch listed companies have issued their 2017 financial statements

18© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

— If you would like to stay up to date with IFRS 16, please sign up to our IFRS 16 newsletter

You can do this by leaving your email address with our KPMG staff during this seminar— In addition, we have multiple publications dealing with the complex issues of IFRS 16 (Transition, discount

rate, lease liability etc.). Please indicate to us what publications you would like to receive and leave your contact details so we can send the publications to you.

For further information: CMAAS IFRS 16 newsletter and publications

IFRS implementatie KLM

Maart 2018

Richard van der Laan

Wim Molenaar

Agenda

• Introduction• Main structuring choices

– Fleet– Lease duration fleet– Real Estate– Other– Maintenance– Discount rate to use

• Financial Impact• Risk Management• Project Planning (timeline, resources)• IT Tooling

20

High over scenario’s for aircraft

• Lease duration:– Low (prime contractual period of the lease)– Medium (Lease with extentions / discounts taken into account)– High (max allowed duration under the contract, no discounts)– (Or 20 years)

• Discount rate– Incremental Borrowing Rate– Implicit Rate

21

IFRS 16 – Structuring – Aircraft lease contracts

• Aircraft lease contracts:– The contractual lease term will be used as a basis for the lease debt calculation (KLM

almost 100 aircraft)– KLM will only have a view on a potential renewal 15 to 12 months prior the renewal

option date. Before this period no renewals are taken into account.– Extensions are included in the debt calculation in case of:

• An engine contract with a duration longer than the contractual lease term, the longer term is applied in the calculation (not exceeding the latest ending date of the lease contract). Applicable for KLC Embraer 190

• Cabin retrofit investments with a depreciation longer than the contractual lease term indicating that it is reasonable certain that the lease will be renewed.

• Renewal exceptions deviating from the 15-12 months rule may occur following broader re-negotiations (multiple contracts) with the lessor because of the fleet profile.

• For aircraft the discount rate used corresponds to the implicit rate of the contract. For other contracts (buildings, cars, other) the incremental rate (IBR) will be used

22

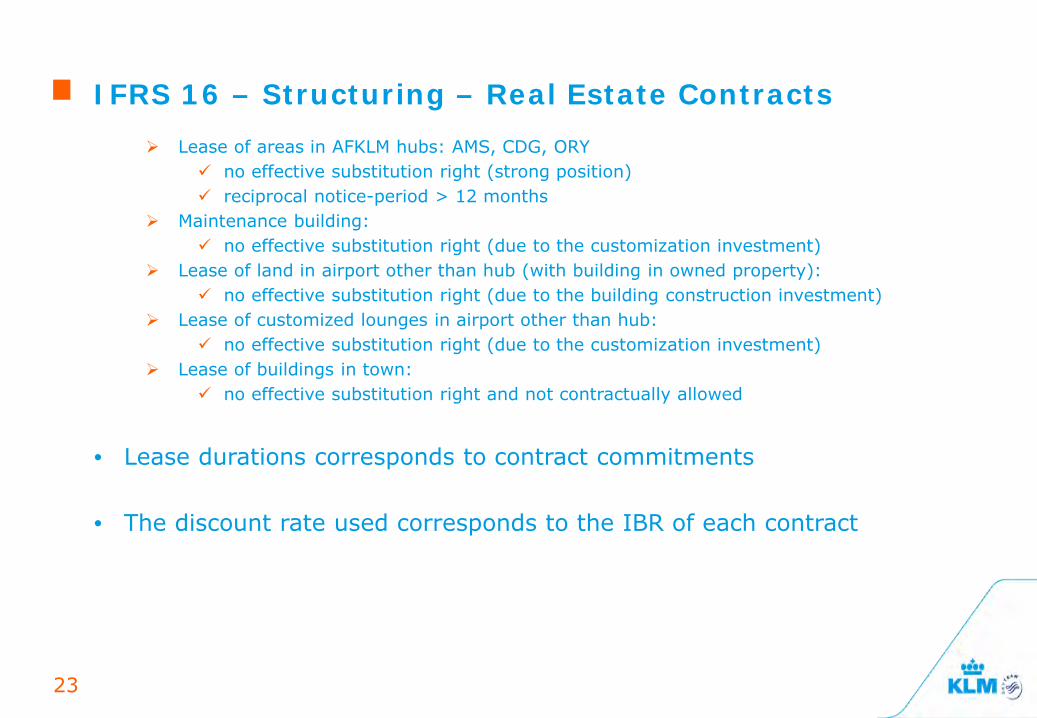

IFRS 16 – Structuring – Real Estate Contracts Lease of areas in AFKLM hubs: AMS, CDG, ORY

no effective substitution right (strong position) reciprocal notice-period > 12 months

Maintenance building: no effective substitution right (due to the customization investment)

Lease of land in airport other than hub (with building in owned property): no effective substitution right (due to the building construction investment)

Lease of customized lounges in airport other than hub: no effective substitution right (due to the customization investment)

Lease of buildings in town: no effective substitution right and not contractually allowed

• Lease durations corresponds to contract commitments

• The discount rate used corresponds to the IBR of each contract

23

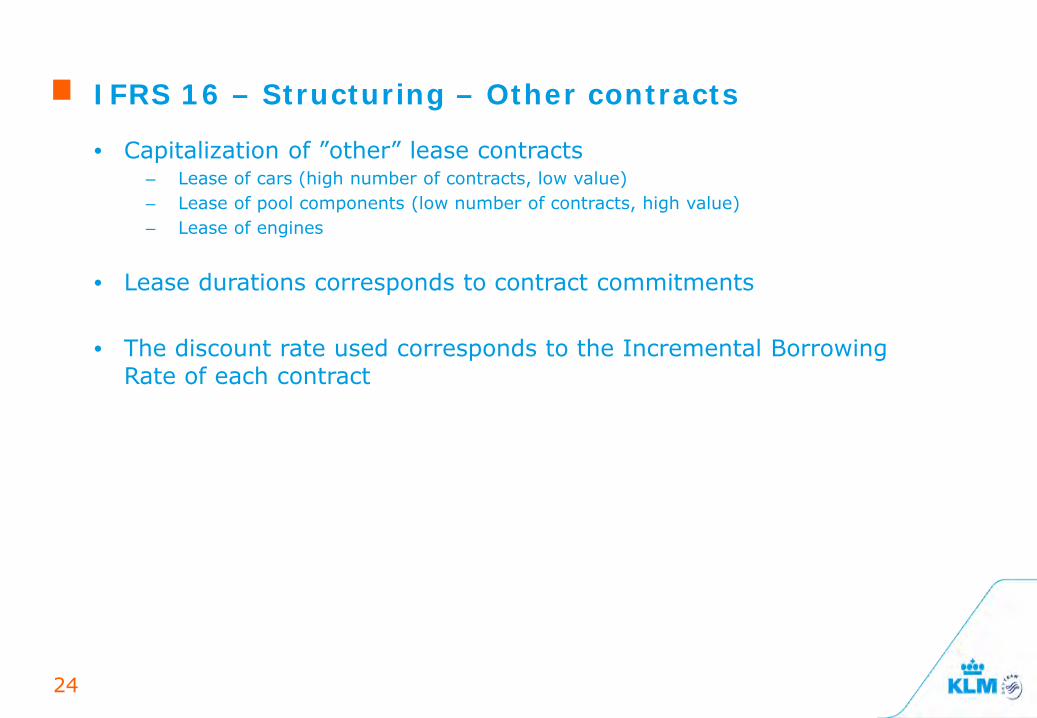

IFRS 16 – Structuring – Other contracts

• Capitalization of ”other” lease contracts– Lease of cars (high number of contracts, low value)– Lease of pool components (low number of contracts, high value)– Lease of engines

• Lease durations corresponds to contract commitments

• The discount rate used corresponds to the Incremental Borrowing Rate of each contract

24

25© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

IFRS 16 – Structuring – Maintenance

• Today, the accounting of the normal maintenance (overhaul of airframe and engines) is different to the property type of the aircraft:

– Aircraft owned: maintenance costs are capex no EBITDA impact– Aircraft leased: maintenance costs are covered by a provision reversal EBITDA

impact

• The Group has taken the opportunity of IFRS 16 deployment to revisit these two maintenance accounting schemes and to align them as much as possible.

• Discussions on Aircraft Return Obligations

26

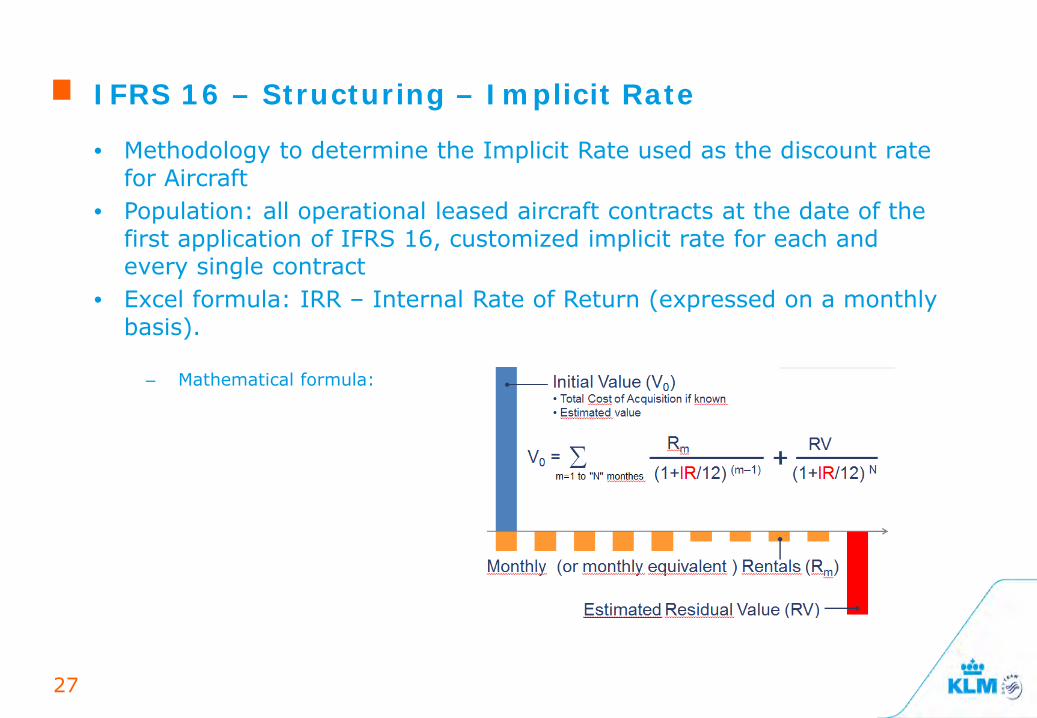

IFRS 16 – Structuring – Implicit Rate

• Methodology to determine the Implicit Rate used as the discount rate for Aircraft

• Population: all operational leased aircraft contracts at the date of the first application of IFRS 16, customized implicit rate for each and every single contract

• Excel formula: IRR – Internal Rate of Return (expressed on a monthly basis).

– Mathematical formula:

27

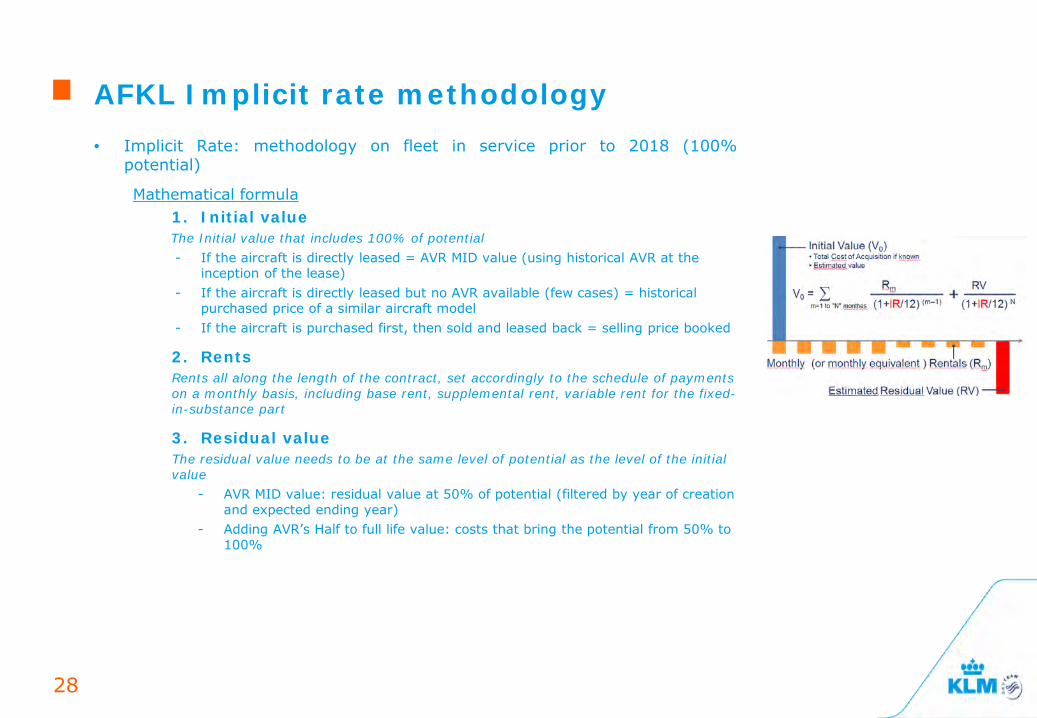

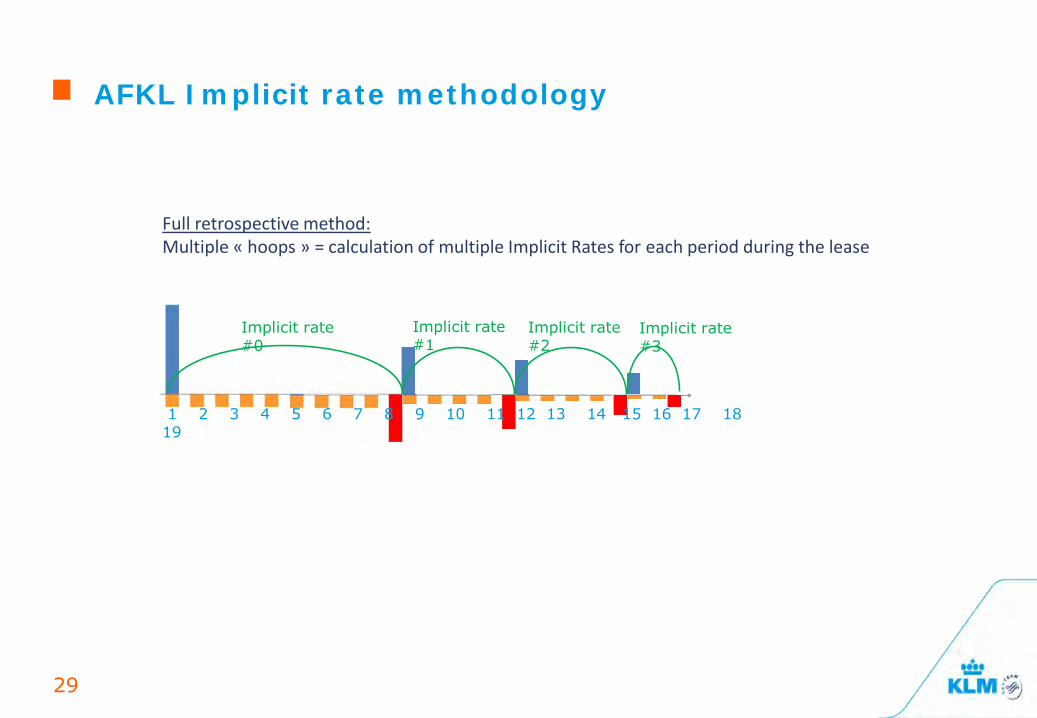

AFKL Implicit rate methodology • Implicit Rate: methodology on fleet in service prior to 2018 (100%

potential)

Mathematical formula1. Initial valueThe Initial value that includes 100% of potential- If the aircraft is directly leased = AVR MID value (using historical AVR at the

inception of the lease)- If the aircraft is directly leased but no AVR available (few cases) = historical

purchased price of a similar aircraft model- If the aircraft is purchased first, then sold and leased back = selling price booked

2. RentsRents all along the length of the contract, set accordingly to the schedule of payments on a monthly basis, including base rent, supplemental rent, variable rent for the fixed-in-substance part

3. Residual valueThe residual value needs to be at the same level of potential as the level of the initial value

- AVR MID value: residual value at 50% of potential (filtered by year of creation and expected ending year)

- Adding AVR’s Half to full life value: costs that bring the potential from 50% to 100%

28

Implicit rate #0

Implicit rate #1

Implicit rate #2

Implicit rate #3

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19

Full retrospective method: Multiple « hoops » = calculation of multiple Implicit Rates for each period during the lease

AFKL Implicit rate methodology

29

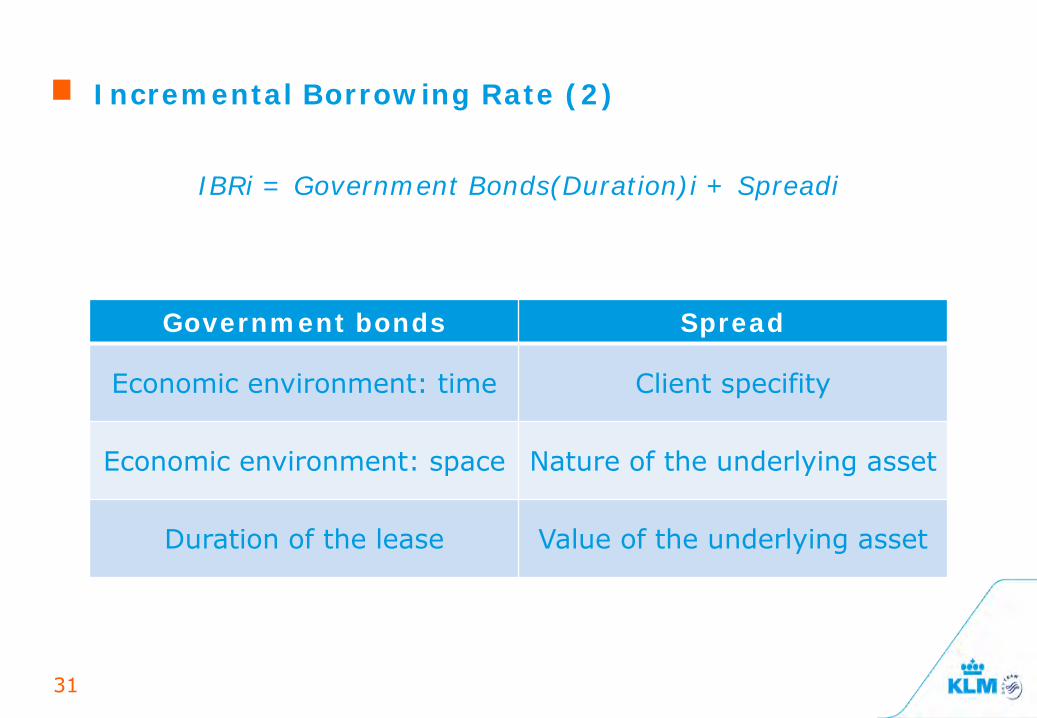

Incremental Borrowing Rate

Defined Terms: “lessee’s incremental borrowing rate: The rate of interest that a lessee would have to pay to borrow over a similar term, and with a similar security, the funds necessary to obtain an asset of a similar value to the right-of-use asset in a similar economic environment.”

Main characteristics:• Nature and valuation of the underlying asset• The economic environment in time and space, by using data

specific to the region of the lease• The lessee, because credit rates are often company dependents• The duration of the lease

IBRi = Government Bonds(Duration)i + Spreadi

30

Incremental Borrowing Rate (2)

IBRi = Government Bonds(Duration)i + Spreadi

31

Government bonds Spread

Economic environment: time Client specifity

Economic environment: space Nature of the underlying asset

Duration of the lease Value of the underlying asset

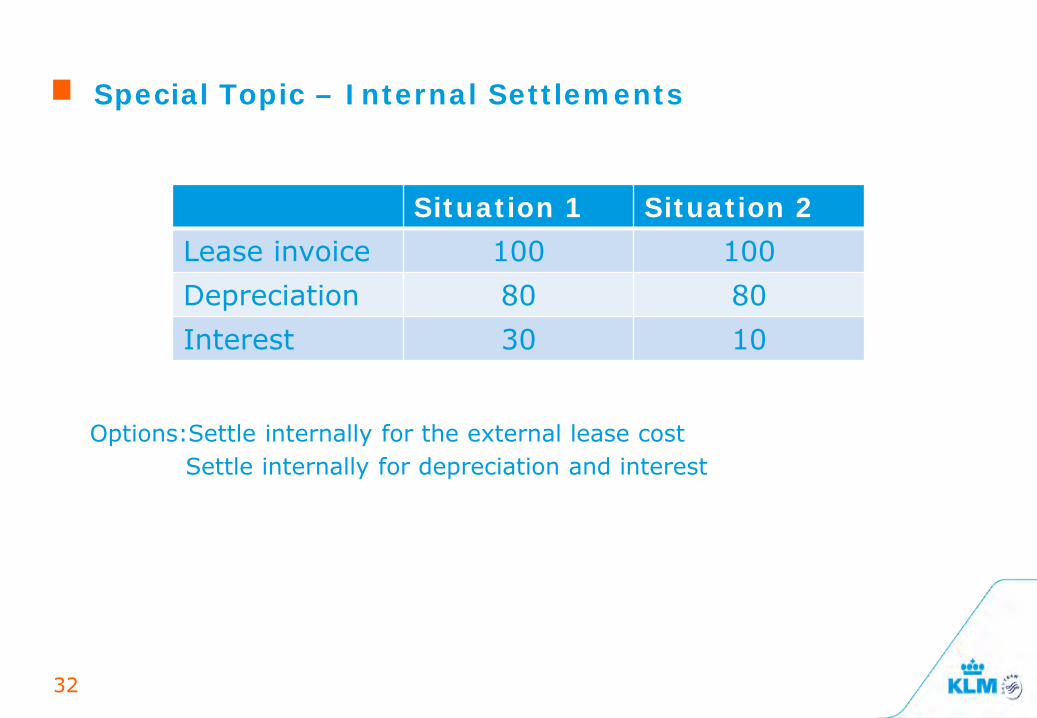

Special Topic – Internal Settlements

32

Situation 1 Situation 2Lease invoice 100 100Depreciation 80 80Interest 30 10

Options:Settle internally for the external lease costSettle internally for depreciation and interest

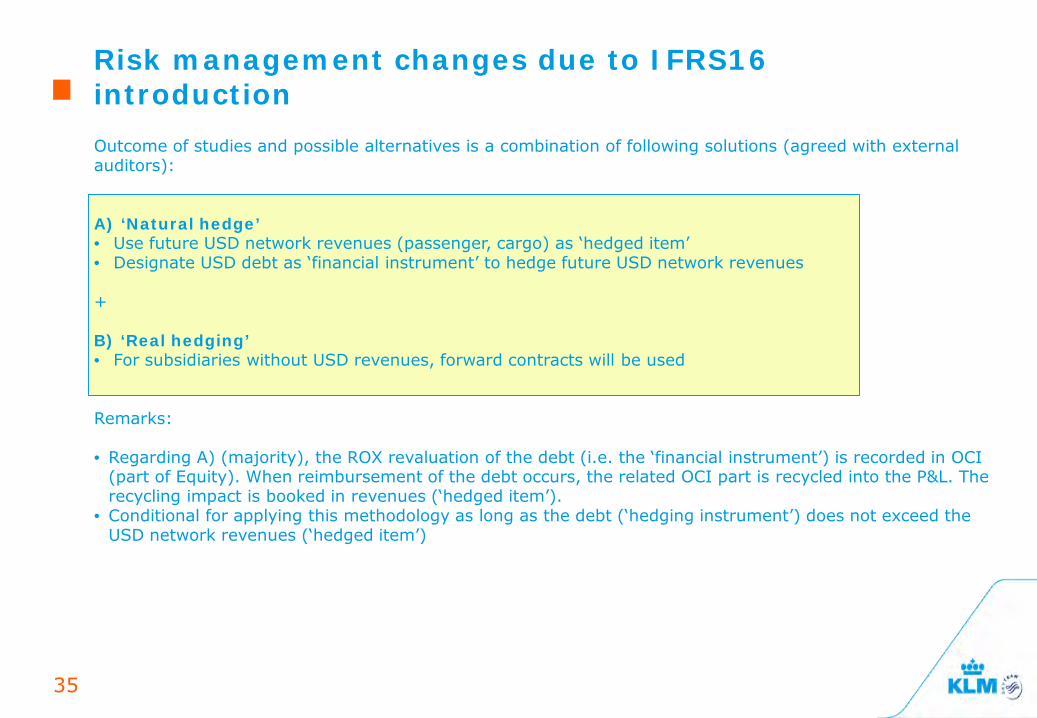

Risk management changes due to IFRS16 introduction

• Due to IFRS16, the on-balance sheet debt will increase with operating lease contracts. These contracts are largely denominated in USD. Consequently, the on-balance sheet debt denominated in USD will increase.

• This debt is to be periodically revaluated against latest currency exchange rates.

• The right-of-use asset however is recognized based on the currency conversion rate at the moment of inception of the contract (and remains stable during the contract period) ‘mismatch’

• Therefore, without additional measures, due to IFRS16, both balance sheet and P&L will be subject to increased reported currency volatility

Key question: How to mitigate this increased currency risk and keep results as stable as possible?

33

34© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Outcome of studies and possible alternatives is a combination of following solutions (agreed with external auditors):

A) ‘Natural hedge’• Use future USD network revenues (passenger, cargo) as ‘hedged item’• Designate USD debt as ‘financial instrument’ to hedge future USD network revenues

+

B) ‘Real hedging’• For subsidiaries without USD revenues, forward contracts will be used

Remarks:

• Regarding A) (majority), the ROX revaluation of the debt (i.e. the ‘financial instrument’) is recorded in OCI (part of Equity). When reimbursement of the debt occurs, the related OCI part is recycled into the P&L. The recycling impact is booked in revenues (‘hedged item’).

• Conditional for applying this methodology as long as the debt (‘hedging instrument’) does not exceed the USD network revenues (‘hedged item’)

Risk management changes due to IFRS16 introduction

35

Projectplanning

36

37© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

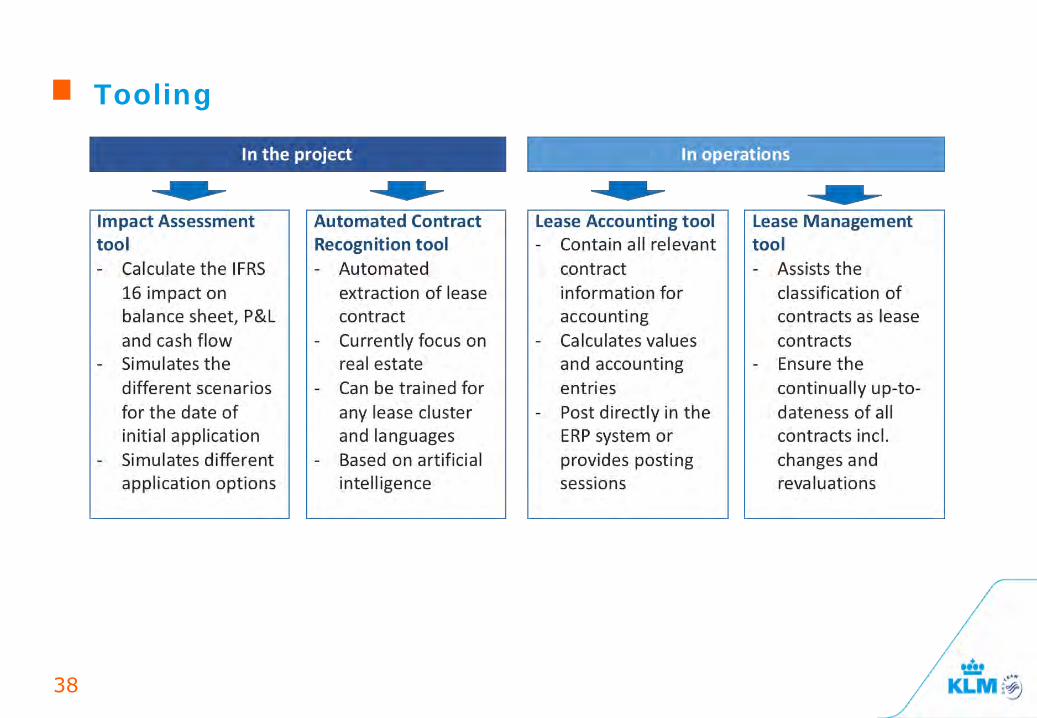

Tooling

38

IT Landscape

39

IFRS 16: Leases

March 20, 2018

Ahold Delhaize's experience with IFRS 16

Presenting to you todayAhold Delhaize's experience with IFRS 16

41

Maryke KeetDirector Financial Reporting

Wouter NijmeijerSVP Accounting & Reporting, Risk & Controls

Agenda

• Ahold Delhaize – background• Project setup, governance and timeline• IT tool selection• Local resources for data enrichment• Accounting challenges, policy choices and practical expedients• Training & communication• Internal controls

Ahold Delhaize's experience with IFRS 1642

Ahold Delhaize -Background

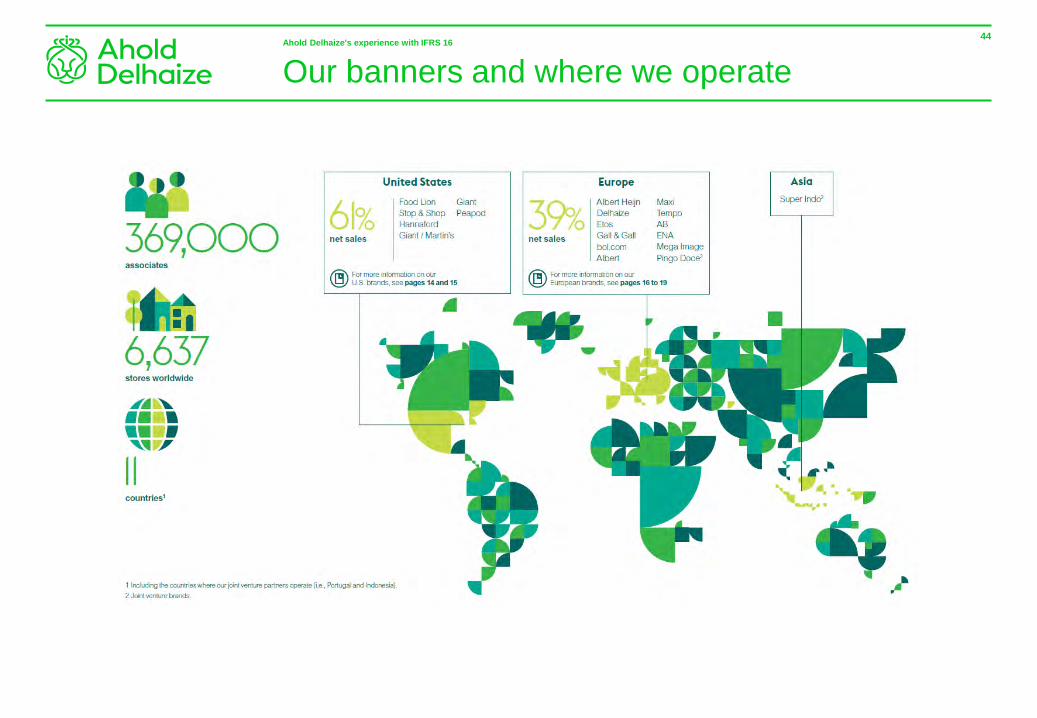

Our banners and where we operateAhold Delhaize's experience with IFRS 16 44

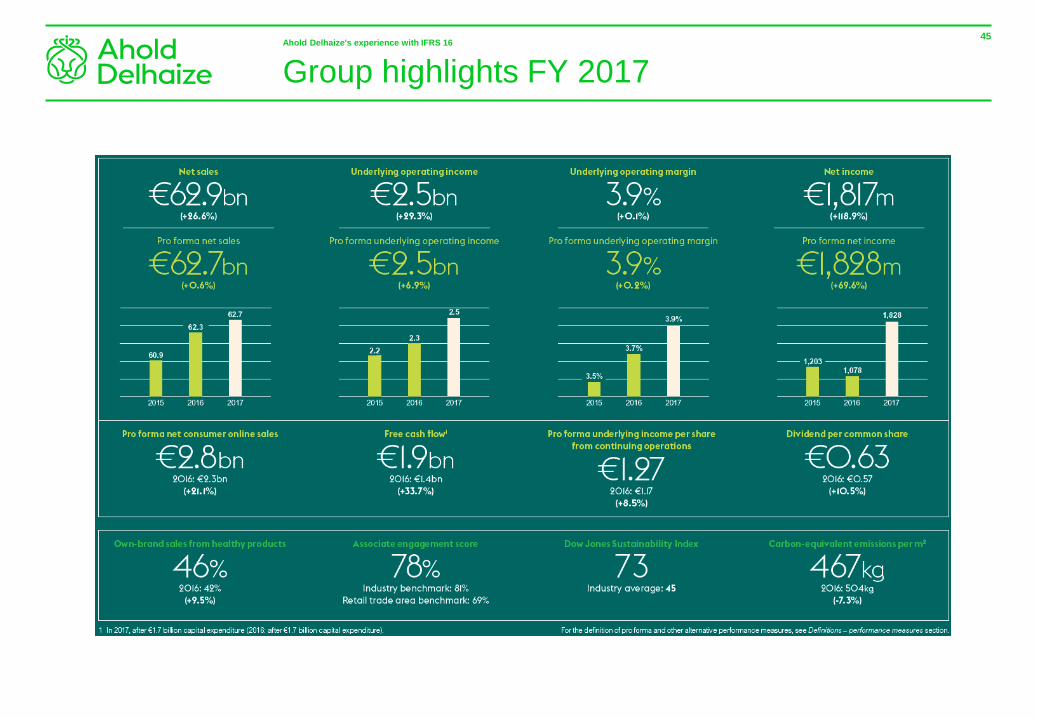

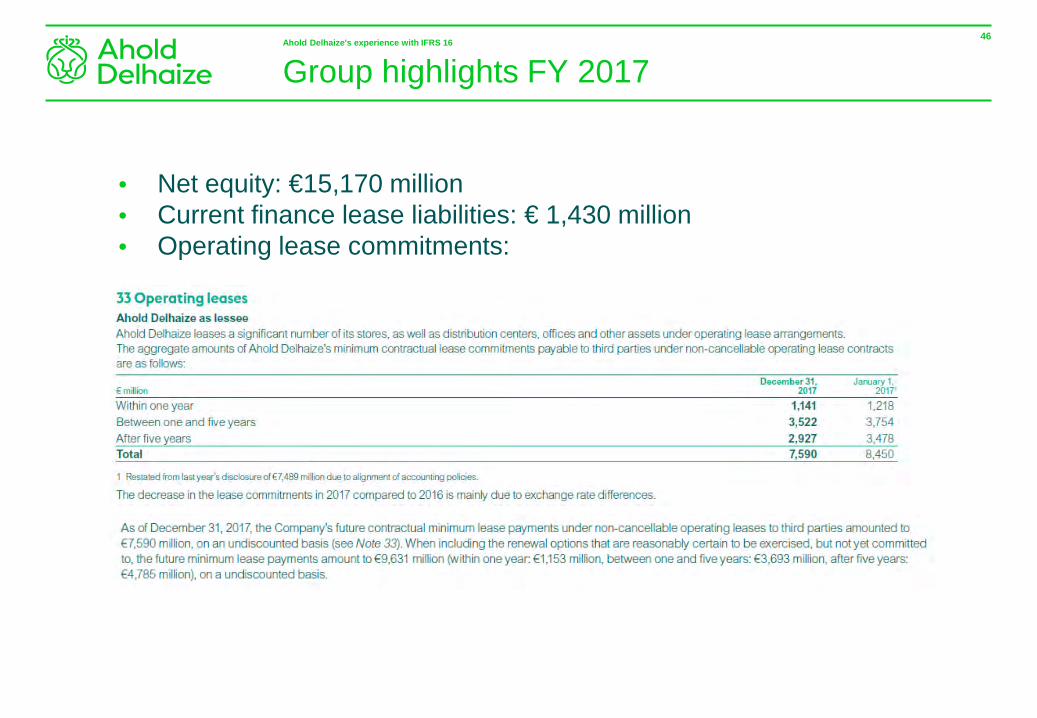

Group highlights FY 2017Ahold Delhaize's experience with IFRS 16 45

Group highlights FY 2017

• Net equity: €15,170 million• Current finance lease liabilities: € 1,430 million• Operating lease commitments:

Ahold Delhaize's experience with IFRS 16 46

Group highlights FY 2017

• Approximately 14,000 lease contracts (excluding I/C leases, low value, short term and lessor operating leases)– Approximately 10,000 real estate

– Remainder mainly car leases• Both lessee and lessor contracts

Ahold Delhaize's experience with IFRS 16 47

Training & communicationProject setup, governance and timeline

Project governanceAhold Delhaize's experience with IFRS 16 49

Work streams are adjusted in different phases of the project based upon needs. For example, a country coordinator brought in when OpCo activities increased.

Original project timelineAhold Delhaize's experience with IFRS 16 50

AD strategic planning *

6-8 weeks 10-12 weeks 10-12 weeks

Possible IFRS 16 Parallel Reporting

Phase 1 Phase 2 Phase 3

AD YE

16-20 weeks

Phase 4

1 Year

Phase 5

Objectives:

Set the project up through the definition of project scope, objectives, project governance, and a project-, communication and resourcing plan.

Ensure Executive buy-in.

Define a detailed plan for Phase 2 and kick-off the project with the head office, US and European Project Teams, including training.

Phase 1Project set-up and scoping

Objectives:

Gaining a detailed understanding of transition and ongoing impacts through identification of the in-scope lease universe.

Inventorying of these leases in a data repository and performing high-level impact assessment.

Sensitivity analysis activities as well as an IT gap assessment.

Phase 2Data inventory and high-level impact

assessment

Objectives:

Definition and selection of a flexible, effective and sustainable solution that meets project and stakeholder goals and objectives.

Detailed design of the solution and implementation plan across all locations, identification of relevant work streams and stakeholder areas affected.

Phase 3Solution Design

Objectives:

On-time and on-budget build and test of the chosen IFRS 16 solution.

Full implementation of the new standard and updated processes across all locations, relevant work streams and stakeholder areas affected.

Phase 4Implementation

Objectives:

Go-live and parallel run of a solution that can be trusted to deliver complete and accurate results to internal stakeholders and the investor community.

Phase 5Monitor

SteerCoJune 12

SteerCoMay 8

SteerCoMarch 23

* Budget 2018 and LTP based on IAS 17

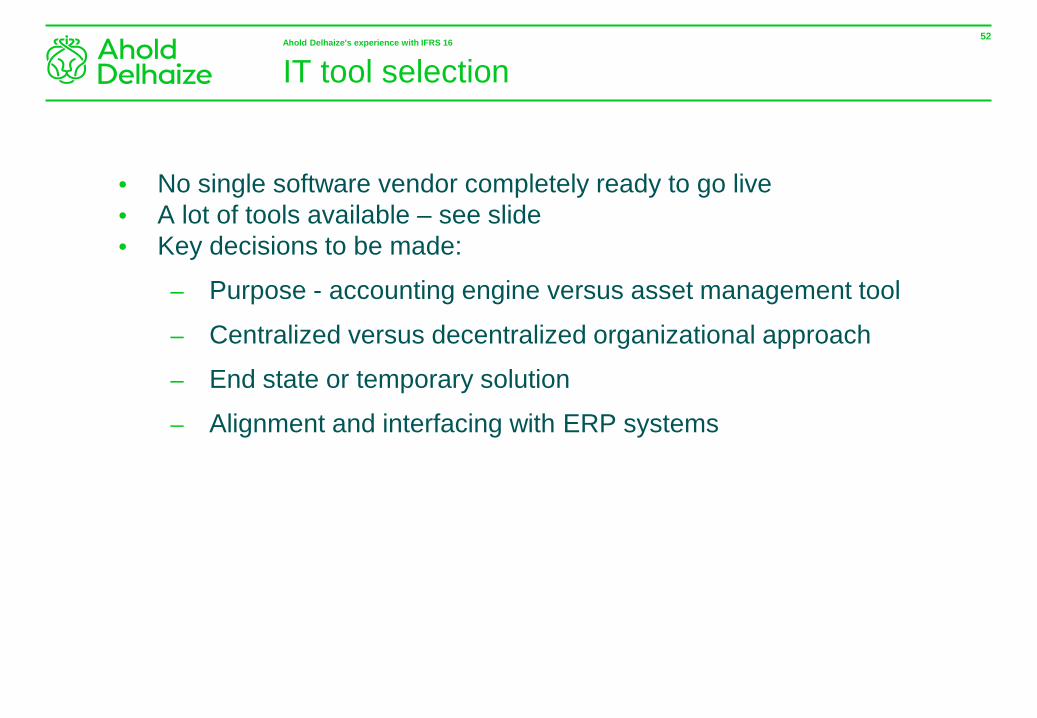

IT tool selection

IT tool selection

• No single software vendor completely ready to go live• A lot of tools available – see slide• Key decisions to be made:

– Purpose - accounting engine versus asset management tool

– Centralized versus decentralized organizational approach– End state or temporary solution– Alignment and interfacing with ERP systems

Ahold Delhaize's experience with IFRS 16 52

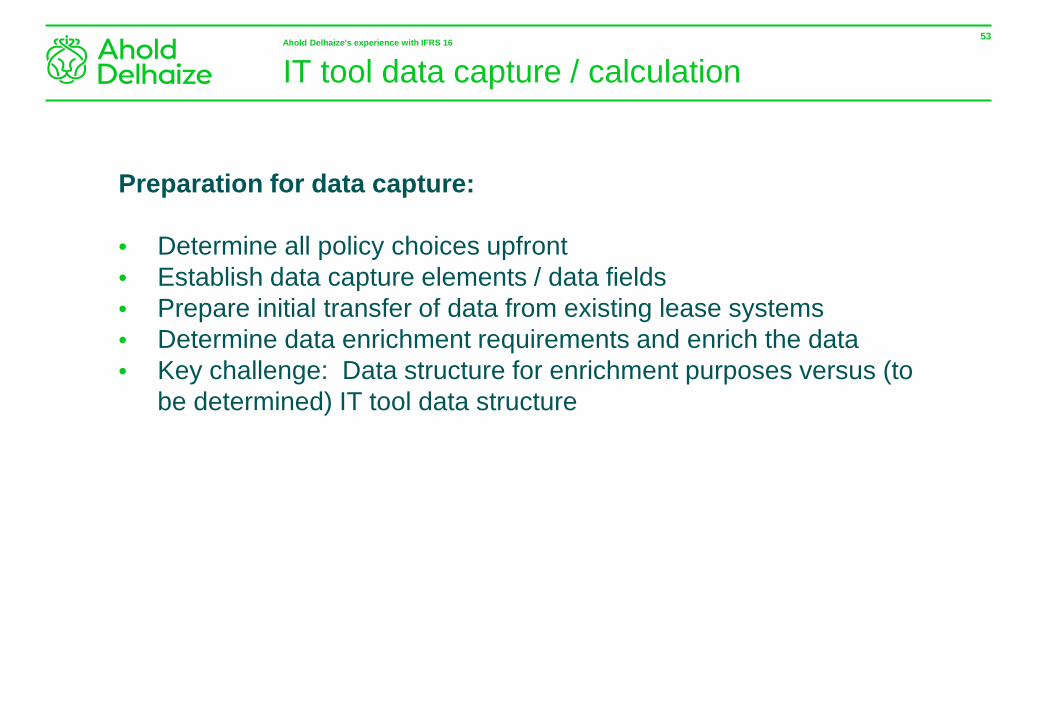

IT tool data capture / calculation

Preparation for data capture:

• Determine all policy choices upfront• Establish data capture elements / data fields• Prepare initial transfer of data from existing lease systems• Determine data enrichment requirements and enrich the data• Key challenge: Data structure for enrichment purposes versus (to

be determined) IT tool data structure

Ahold Delhaize's experience with IFRS 16 53

IT solution vendors (examples)Ahold Delhaize's experience with IFRS 16 54

Vendor Tool type

Tagetik CCH Tagetik Lease Accounting Solution

Sigma conso SigmaConso IFRS16

Anaplan IFRS 16 application

Lease Accelerator Lease accounting

Powerplan Lease accounting

KPMG lease tool Lease accounting

EY lease tool Lease accounting

SAP Nakisa Lease Administration

Peoplesoft Lease administration

Innervision LOIS Lease Accounting

Leverton Contract data extraction

Accruent Lease Administration

CoStar Real estate and Lease administration

AMT Real estate and Lease administration

Sequentra Lease administration

Trimble Manhattan Lease administration

Planon Real estate and Lease administration

LCM Truck lease accounting

SAP Flexible real estate Real estate management

SAP Ariba Contract management tool

IBM Tririga Real estate management

OTHERS

55© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Local resources for data enrichment

Resources

Indication of data enrichment and capture efforts:

• For The Netherlands:

– Approximately 540 man-days (students) will be spent to enrich and capture data points for approximately 2,500 real estate contracts.

– Straight forward contracts takes approximately 1,5 hours and complex contracts can take up to 8 hours.

• For the Czech Republic:

– Approximately 294 man-days (students) will be spent to enrich and capture data points for approximately 1,100 real estate and 400 other lease contracts.

– Lessee contracts take approximately 5 hours (but up to 16 in complex situations) and lessor contracts approximately 2 hours

• This excludes time spent on accounting issues, extracting and converting available data to standardized format in a database, coordination, reporting process development and system implementation.

Ahold Delhaize's experience with IFRS 16 57

58© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Accounting challenges, policy choices and

practical expedients

Accounting policy decisionsAhold Delhaize's experience with IFRS 16 60

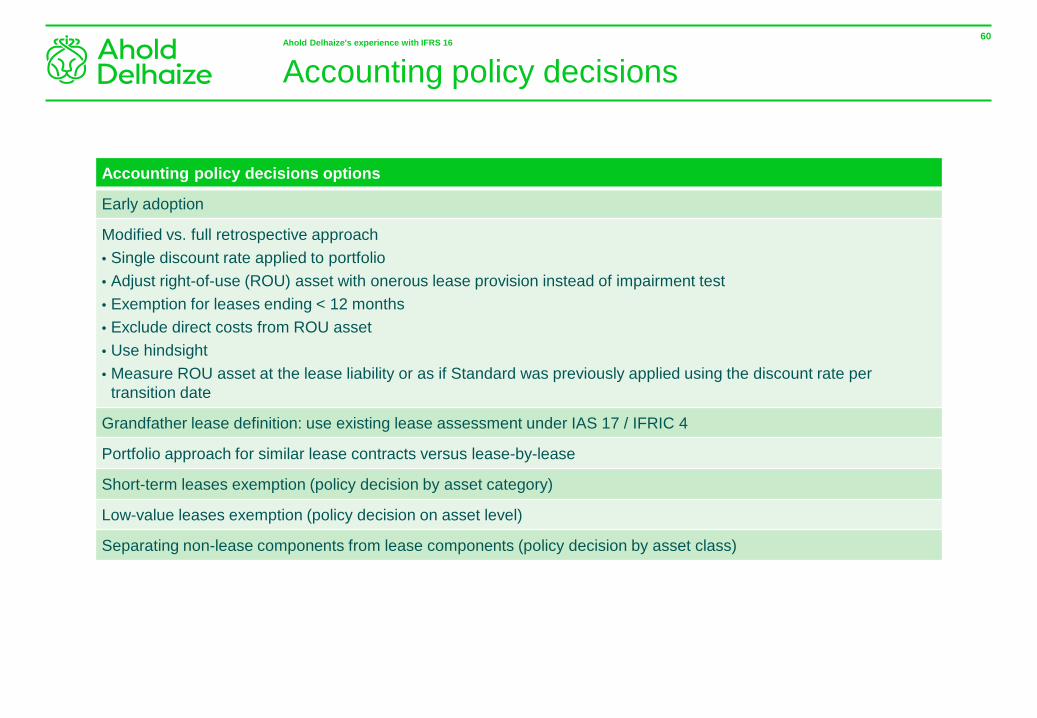

Accounting policy decisions options

Early adoption

Modified vs. full retrospective approach• Single discount rate applied to portfolio• Adjust right-of-use (ROU) asset with onerous lease provision instead of impairment test• Exemption for leases ending < 12 months• Exclude direct costs from ROU asset• Use hindsight• Measure ROU asset at the lease liability or as if Standard was previously applied using the discount rate per

transition date

Grandfather lease definition: use existing lease assessment under IAS 17 / IFRIC 4

Portfolio approach for similar lease contracts versus lease-by-lease

Short-term leases exemption (policy decision by asset category)

Low-value leases exemption (policy decision on asset level)

Separating non-lease components from lease components (policy decision by asset class)

Accounting challenges

• Intercompany leases

– Mismatch lessor (operating lease) and lessee accounting

– Treat all intercompany as either operating or finance lease?

– Impact on management reporting / statutory financials?• Lessor accounting: sub-leases

– Classify operating / finance lease based on head lease instead of underlying asset

– How to allocate the value a single head-lease to multiple sub-leases for the classification of operating versus finance lease?

– How to estimate the residual value and gain/loss on the contract to account for finance sub-leases?

• Materiality

– How to reconcile a $5,000 threshold in the basis of conclusions with IAS 1 concept (principles based)?

– Which lease contracts are really important to the business?

Ahold Delhaize's experience with IFRS 16 61

62© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Accounting challenges

• Lease term and lease commitments not shown in balance sheet– Indicators for assuming extension options: past practice versus

economic incentive?

– Impact on 2017 disclosures (if disclosed commitments differ from reasonably certain extension options)?

• Dedicated supplier agreements / embedded leases– What clauses and factors are indicative for control over

identified assets, in particular regarding substitution rights?

• Non lease components– Which components (Common Area Maintenance, Insurance,

etc.) are separable?

Ahold Delhaize's experience with IFRS 16 63

Accounting topics still open

• Discount rate • Mixed property • Cash flow statement presentation• Impairment of lease receivables under IFRS 9

Ahold Delhaize's experience with IFRS 16 64

Training & communication

Training & communication

Training

• IFRS 16 technical training to Finance community of each banner during first half of 2017

• General awareness training to wider organization

• 2 day workshop, in October 2017, where all OpCos discussed their approach along with continued IFRS 16 training and discussion of project

• Weekly OpCo calls – feedback on issues / questions raised, including technical guidance

• Weekly meetings with the central project team

• Weekly meeting with the IT department and Planon to monitor implementation of the lease calculation tool

• Temporary calculation engine – training for UAT purposes

Communication

• Regular Steering Committee meetings (approximately every 6 weeks)

• Twice per year an update has been issued to the Audit Committee on progress of the implementation

• IFRS 16 project website - regularly updated with instructions, guidance and other documents

Ahold Delhaize's experience with IFRS 16 66

Thank youInternal controls

Internal controls

• Three areas:– To be created “once-off” controls: i.e. Data capture and

conversion controls

– IT system implementation controls: Execution of already existing controls around implementation of new IT systems

– Revision of existing controls embedded in current processes due to changes in processes

Ahold Delhaize's experience with IFRS 16 68

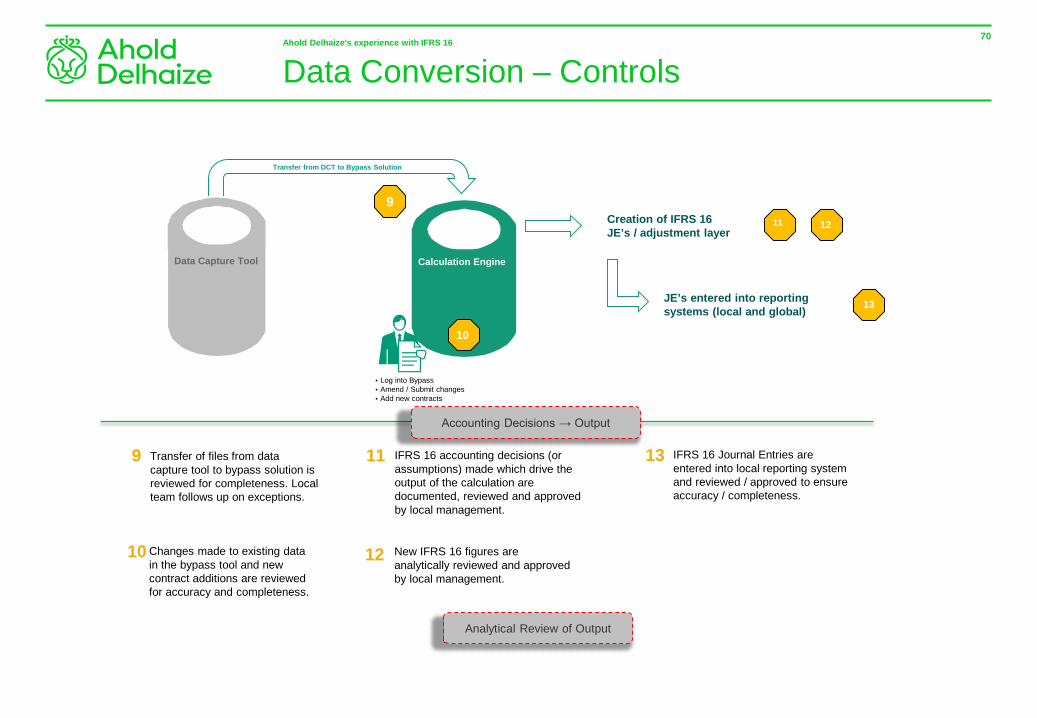

Data capture – controls* Ahold Delhaize's experience with IFRS 16 69

Data capture tool

• Log into front engine• Amend / Enrich• Submit changes

Landing Zone (Shared File)

Source Files

Local teams review the integrity of the final data within the data capture tool for reasonableness and to ensure that the data capture tool reconciles with source data base.

Data Maintenance Reporting

Local Contract Database

Transfer of files from local shared files to the data capture tool is reviewed for completeness.

Transfer of Source Files to DCT

Data CollectionData Governance (Kick-off)

Export Data

Load Data

IFRS 16 Data Field Requirements Template provided to local teams

(Local) Data capture strategy and resource plan

Local IFRS 16 team lead confirms understanding of IFRS 16 data requirements.

Local IFRS 16 team lead establishes, communicates and confirms the final data capture strategy and resource plan

Manual and automated upload of files to Shared file is reviewed for accuracy and completeness.

1

2

1

2

3

4

4

Control Objective**: All contracts and key information are located and collected to ensure completeness of contract population.

6

5

Automated data validation checks Automated data validation checks prevent users from entering inappropriate character types dependent upon field type.

6

8

83

Changes made to existing data (entered pre cut-off) and new contract additions (or amendments) submitted are reviewed for accuracy and completeness.

7

7

5

* This list of controls is not intended to be exhaustive, but provides a minimum set of controls that should be followed (specific to Ahold Delhaize).

Buy in Completeness Enrichments / Changes Analytical Review

Data Conversion – ControlsAhold Delhaize's experience with IFRS 16 70

Transfer from DCT to Bypass Solution

Bypass Solution / Calculation Engine

• Log into Bypass• Amend / Submit changes• Add new contracts

9

Data Capture Tool

Creation of IFRS 16 JE’s / adjustment layer

10

11

13

12

Transfer of files from data capture tool to bypass solution is reviewed for completeness. Local team follows up on exceptions.

Changes made to existing data in the bypass tool and new contract additions are reviewed for accuracy and completeness.

New IFRS 16 figures are analytically reviewed and approved by local management.

9

10

11

12

IFRS 16 accounting decisions (or assumptions) made which drive the output of the calculation are documented, reviewed and approved by local management.

13 IFRS 16 Journal Entries are entered into local reporting system and reviewed / approved to ensure accuracy / completeness.

JE’s entered into reporting systems (local and global)

Accounting Decisions → Output

Analytical Review of Output

Questions?

Ajolt Bos

20 March 2018

72

Preparing for a smooth landing

Lease accounting 2019: Lessor perspective

Introduction

LeasePlan and its customer base

Our solutions for Lease accounting 2019

Market observations

73

Agenda

Q&A

74

Company profile

>150,000clients

32countries

Owned by consortium of long-term investors, including pension funds and investments funds

1.7 million cars

Founded in 1963

Corporate Head Office in Amsterdam

Strong growth in SME and

international clients

World’s leading fleet management company

Dutchorigin

75

Project team ‘Lease accounting’

Reinoud SchilderTax director

Jef van OosterbosGlobal Segment Director Commercial Operations

Ajolt BosLease Accounting specialist

Ron DroogProject Manager Lease Accounting

76

LeasePlan has offices in 32 countries…

Global market presence:IFRS & US-GAAP

Introduction

LeasePlan and its customer base

Our solutions for Lease accounting 2019

Market observations

77

Agenda

Q&A

78

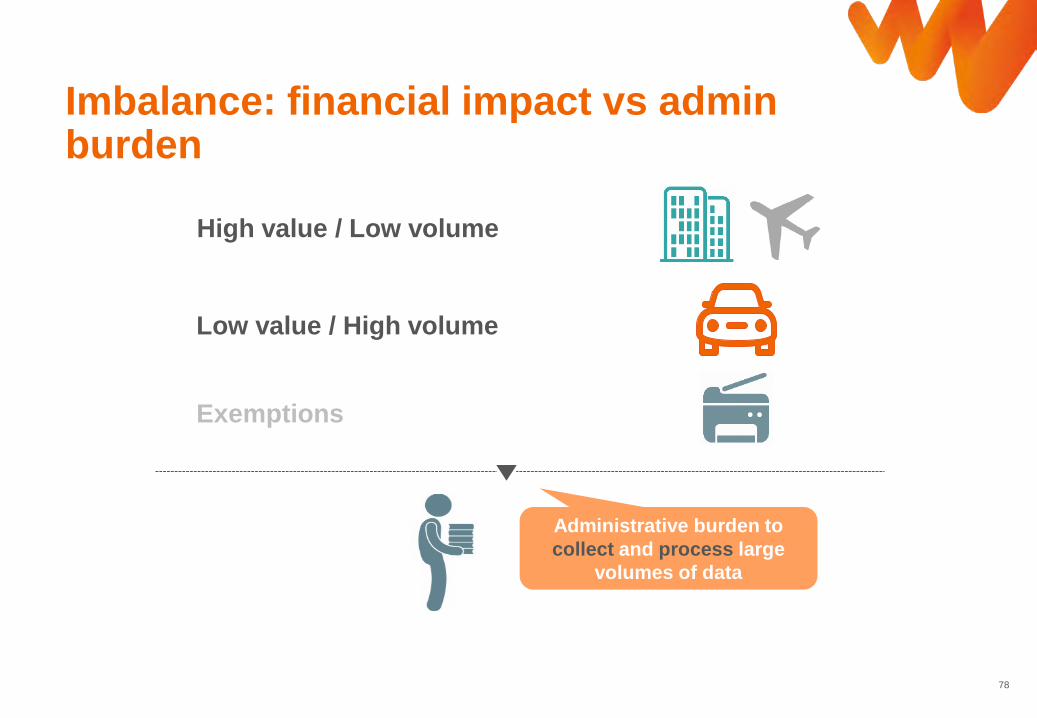

Imbalance: financial impact vs admin burden

High value / Low volume

Exemptions

Low value / High volume

Administrative burden to collect and process large

volumes of data

79

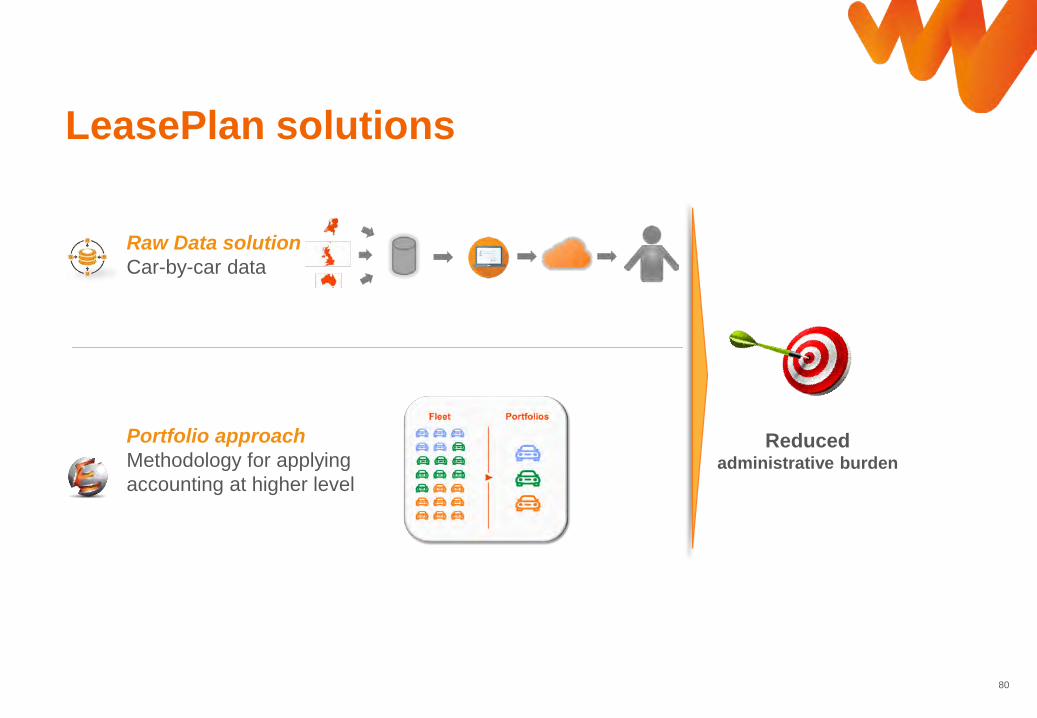

Lifecycle events

Raw Data solutionCar-by-car data

Reducedadministrative burden

Portfolio approachMethodology for applying accounting at higher level

80

LeasePlan solutions

81

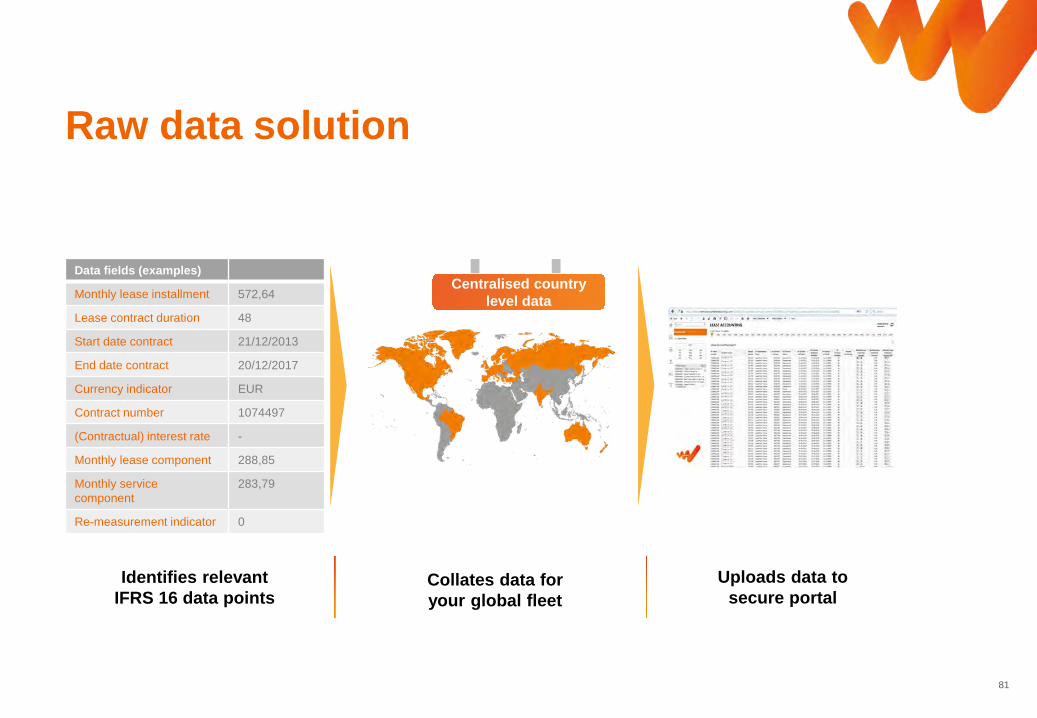

Raw data solution

Data fields (examples)

Monthly lease installment 572,64

Lease contract duration 48

Start date contract 21/12/2013

End date contract 20/12/2017

Currency indicator EUR

Contract number 1074497

(Contractual) interest rate -

Monthly lease component 288,85

Monthly service component

283,79

Re-measurement indicator 0

Identifies relevant IFRS 16 data points

Collates data for your global fleet

Uploads data to secure portal

Centralised country level data

82

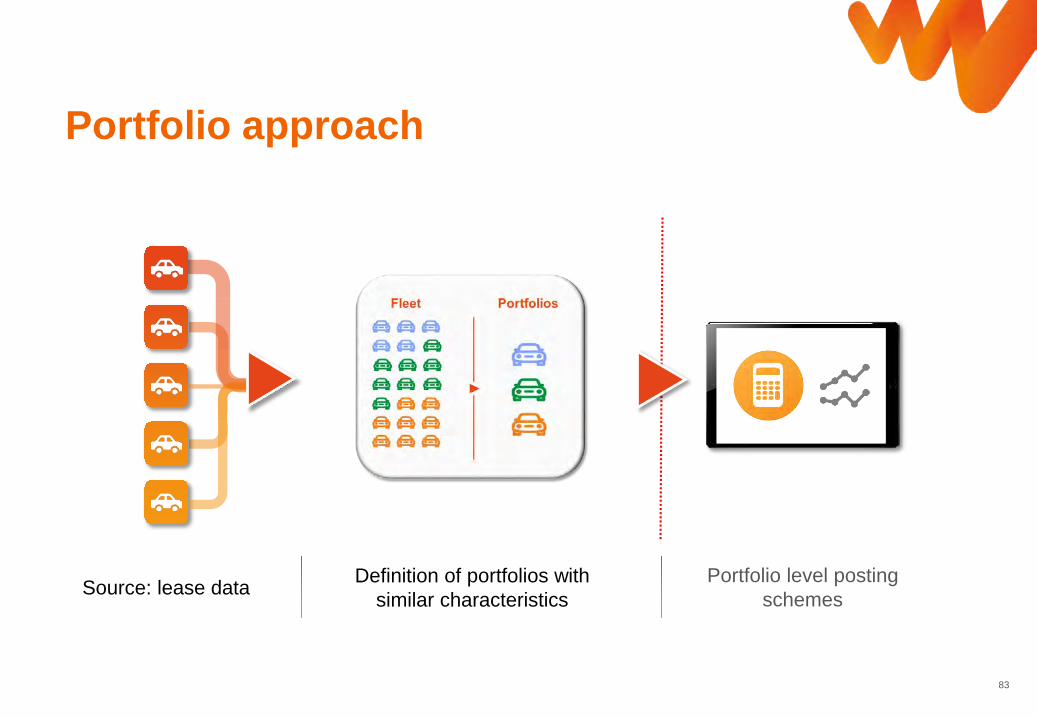

IFRS16“This Standard specifies the accounting for an individual lease. However, as a practical expedient, an entity may apply this Standard to a portfolio of leases with similar characteristics if the entity reasonably expects that the effects on the financial statements of applying this Standard to the portfolio would not differ materially from applying this Standard to the individual leases within that portfolio. If accounting for a portfolio, an entity shall use estimates and assumptions that reflect the size and composition of the portfolio.”

US GAAP ASC842“(…) lessees and lessors are permitted to apply the leases guidance at a

portfolio level. The Board acknowledged that an entity would need to apply judgment in selecting the size and composition of the portfolio in such a way that the entity reasonably expects that the application of the leases model to the portfolio would not differ materially from the application of the leases model to the individual leases in that portfolio”.

Portfolio approach

83

Portfolio approach

Source: lease data Portfolio level posting schemes

Portfolio data

Definition of portfolios with similar characteristics

84

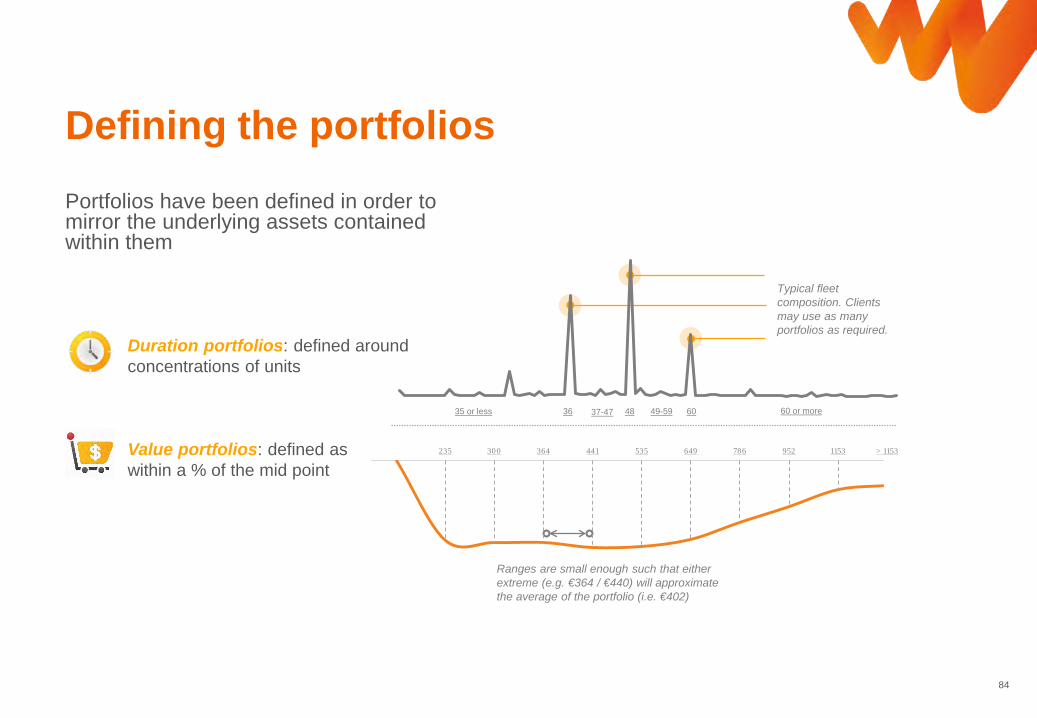

Portfolios have been defined in order to mirror the underlying assets contained within them

Defining the portfolios

Duration portfolios: defined around concentrations of units

Value portfolios: defined as within a % of the mid point

Ranges are small enough such that either extreme (e.g. €364 / €440) will approximate the average of the portfolio (i.e. €402)

0.0 235 300 364 441 535 649 786 952 1153 > 1153

35 or less 36 48 60 or more37-47 49-59 60

Typical fleet composition. Clients may use as many portfolios as required.

85

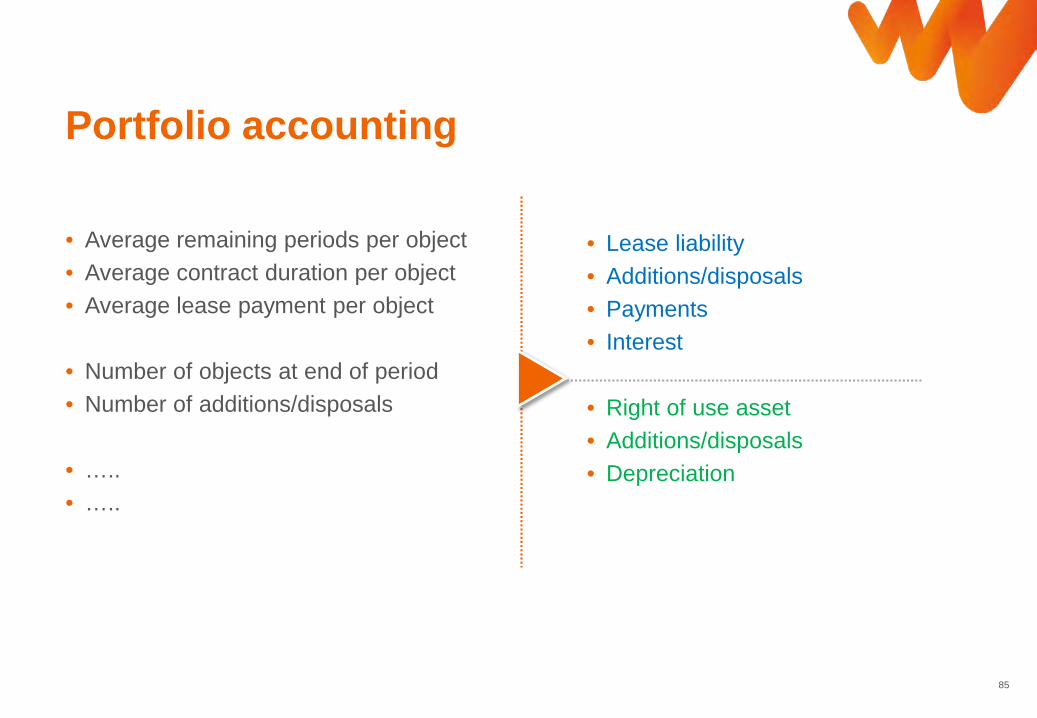

• Average remaining periods per object• Average contract duration per object• Average lease payment per object

• Number of objects at end of period• Number of additions/disposals

• …..• …..

Portfolio accounting

• Lease liability• Additions/disposals• Payments• Interest

• Right of use asset• Additions/disposals• Depreciation

Introduction

LeasePlan and its customer base

Our solutions for Lease accounting 2019

Market observations

86

Agenda

Q&A

87

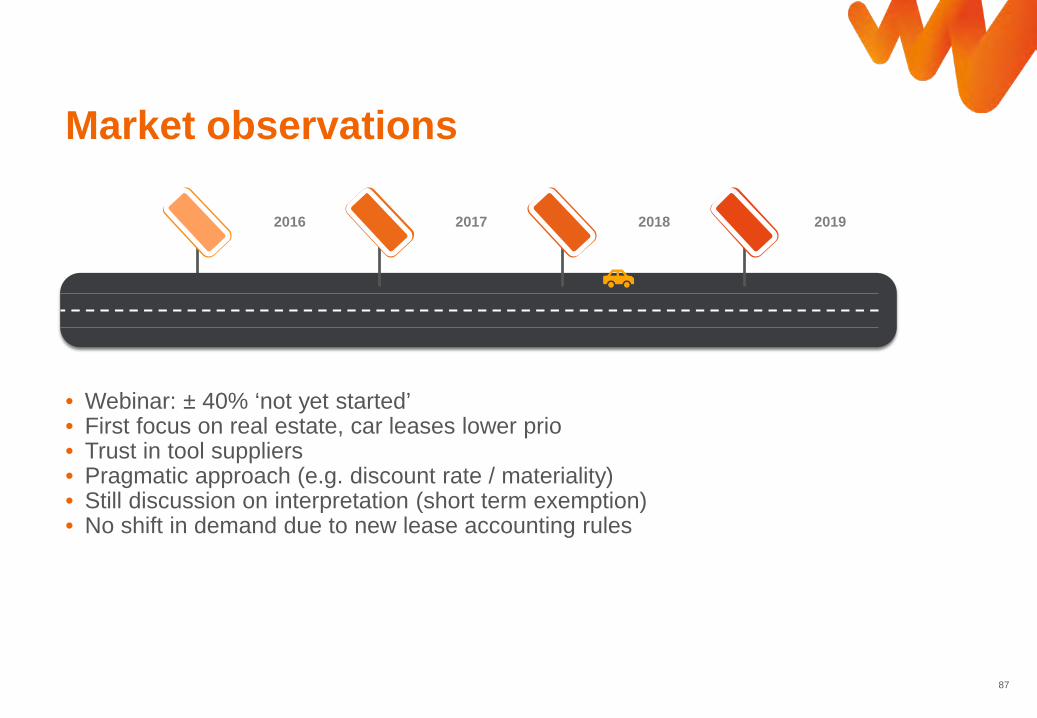

• Webinar: ± 40% ‘not yet started’• First focus on real estate, car leases lower prio• Trust in tool suppliers• Pragmatic approach (e.g. discount rate / materiality)• Still discussion on interpretation (short term exemption)• No shift in demand due to new lease accounting rules

Market observations

2016 2017 20192018

88

• Not spending capital on buying assets• A predictable mobility cost• Avoidance of residual value and maintenance risk• Operational flexibility• Efficient servicing and administration

Main benefits of operational car leasing stay intact

90

Leasesseminar

March 2018

KPMG International Standards GroupFor Internal Use Only

AgendaTransition method

Hot topics

Resources

Transition method

94© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

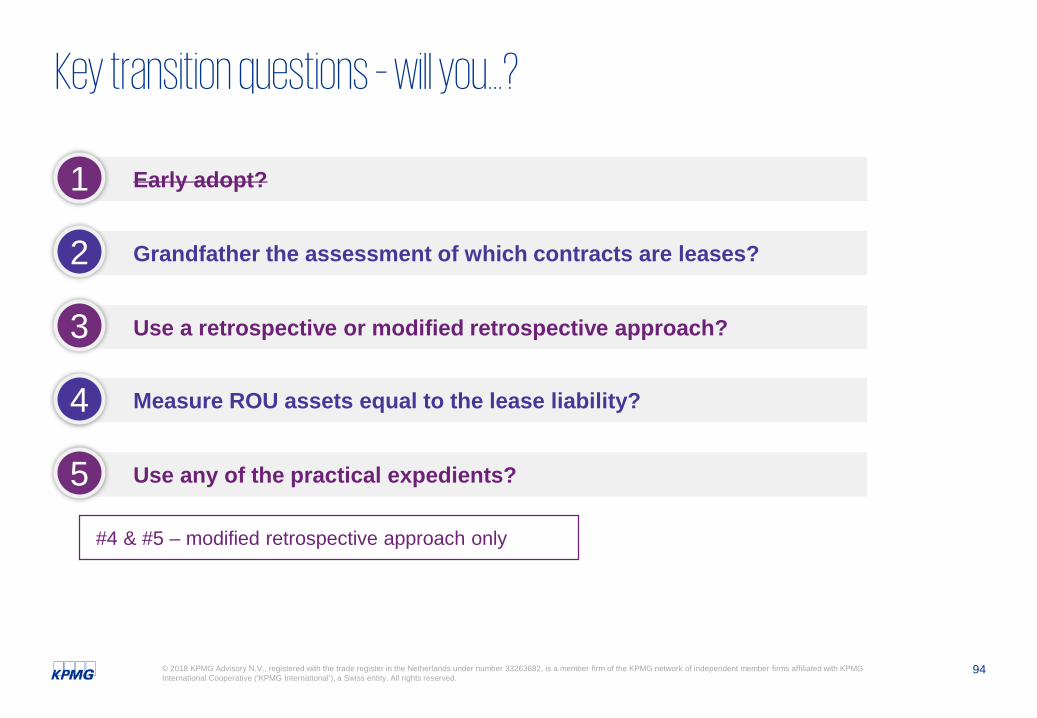

Key transition questions – will you…?

Early adopt?

Grandfather the assessment of which contracts are leases?

Use a retrospective or modified retrospective approach?

Measure ROU assets equal to the lease liability?

Use any of the practical expedients?

1

2

3

4

5

#4 & #5 – modified retrospective approach only

95© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

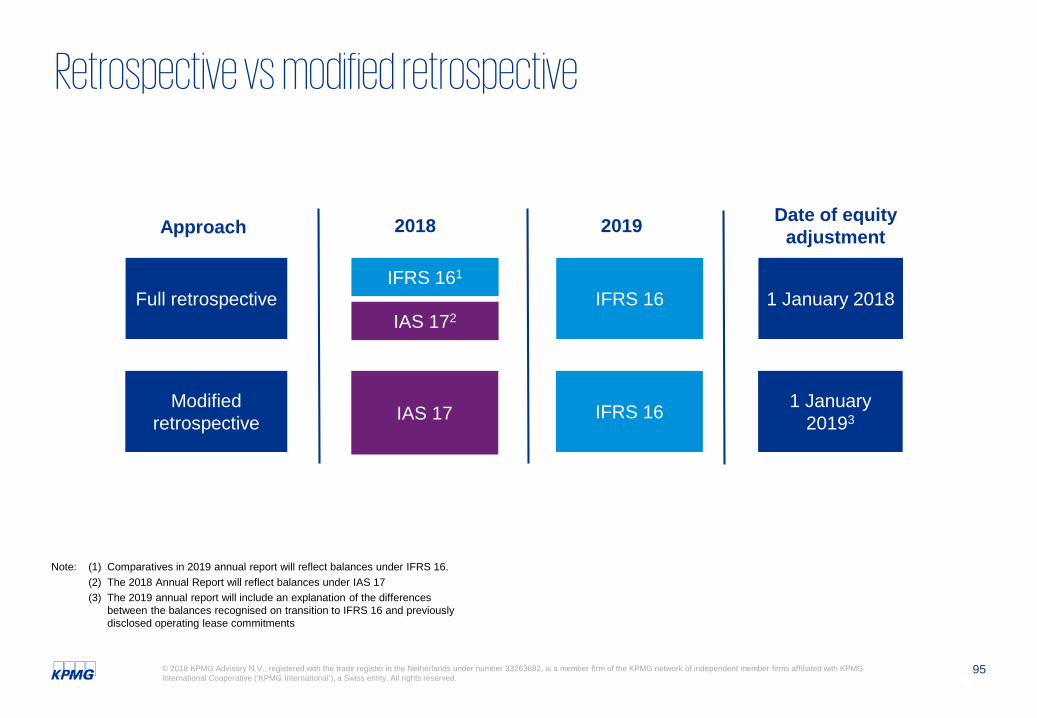

Retrospective vs modified retrospective

Full retrospective

Approach 2018 2019 Date of equity adjustment

IFRS 161

1 January 2018IFRS 16IAS 172

Modified retrospective

1 January 20193IFRS 16IAS 17

Note: (1) Comparatives in 2019 annual report will reflect balances under IFRS 16.(2) The 2018 Annual Report will reflect balances under IAS 17(3) The 2019 annual report will include an explanation of the differences

between the balances recognised on transition to IFRS 16 and previously disclosed operating lease commitments

96© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

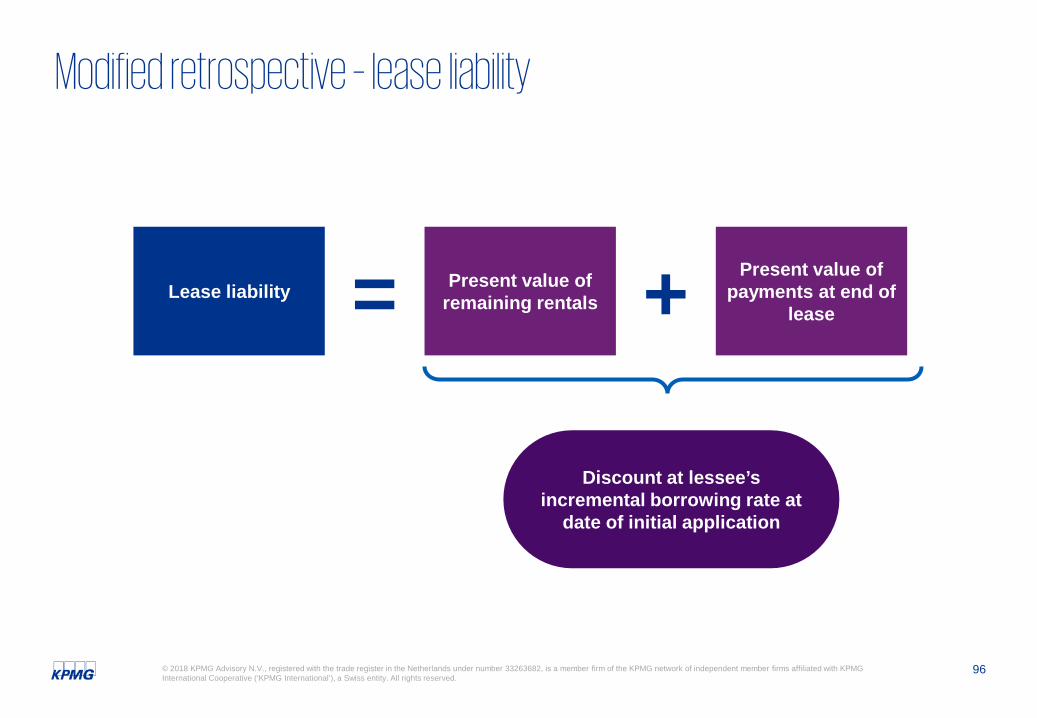

Modified retrospective – lease liability

Present value of payments at end of

lease

Present value of remaining rentals +=Lease liability

Discount at lessee’s incremental borrowing rate at

date of initial application

97© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

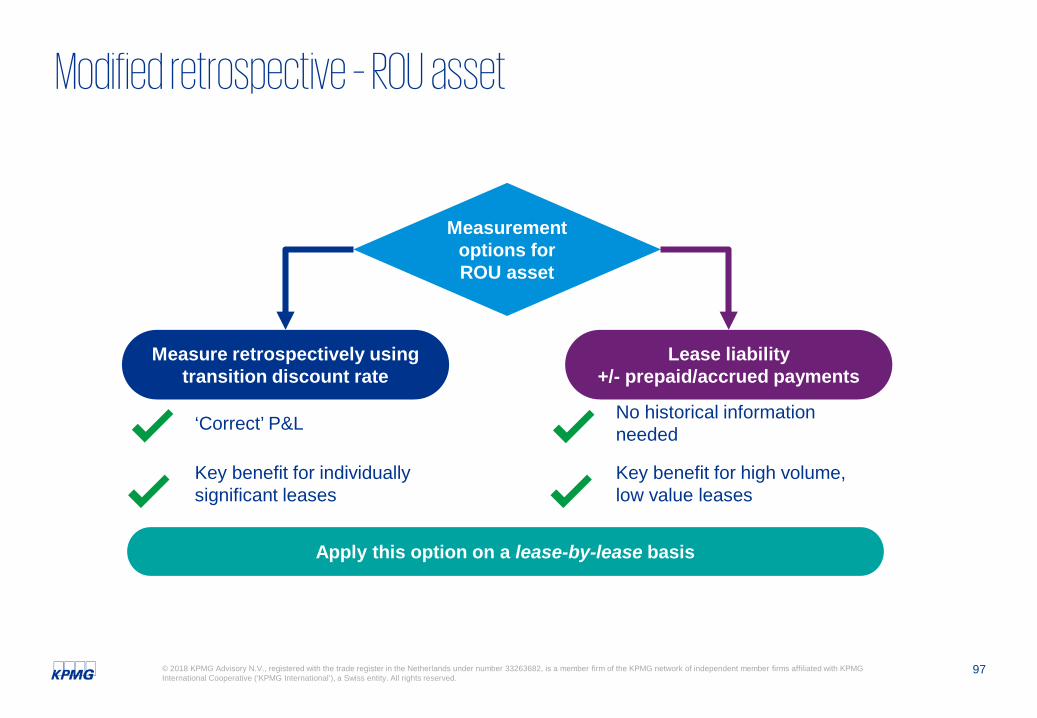

Modified retrospective – ROU asset

Measurement options for ROU asset

Measure retrospectively using transition discount rate

Lease liability+/- prepaid/accrued payments

Apply this option on a lease-by-lease basis

‘Correct’ P&L

Key benefit for individually significant leases

No historical information needed

Key benefit for high volume, low value leases

98© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

The chart shows total lease expense for an entity with:— Portfolio of 120 leases— Annual rental of 100— Lease terms of 10 years— New lease written as each lease expires— Zero inflation

Ongoing impact on comparability

99© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

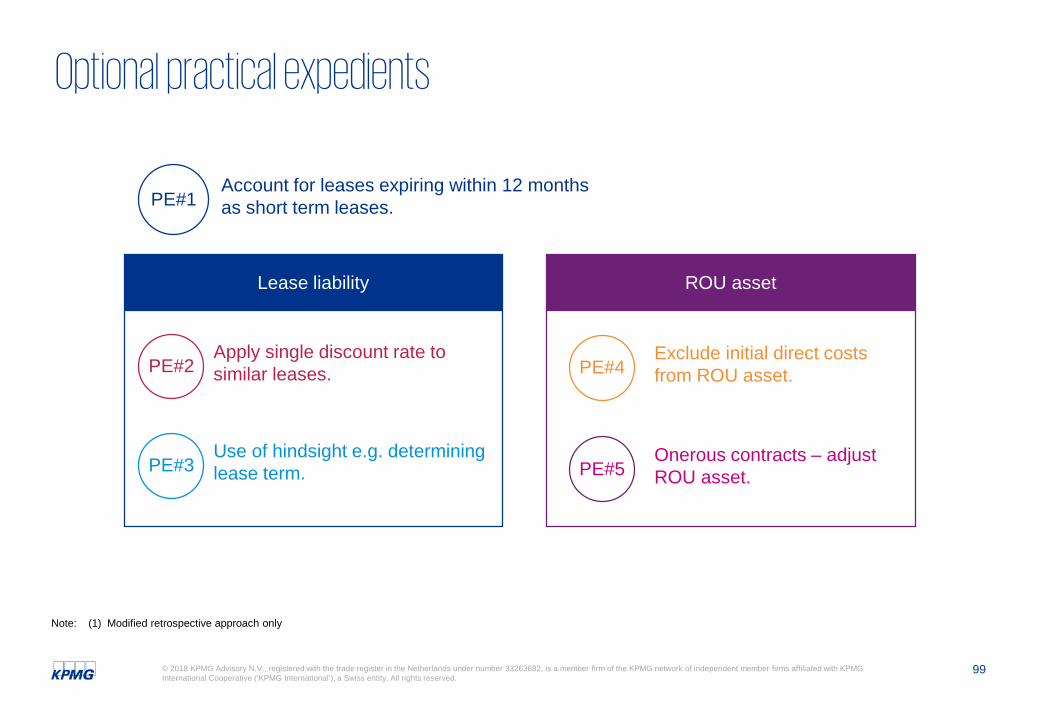

PE#3

Optional practical expedients

Lease liability

Account for leases expiring within 12 months as short term leases.

PE#2Apply single discount rate to similar leases.

Use of hindsight e.g. determining lease term.

PE#4Exclude initial direct costs from ROU asset.

PE#5Onerous contracts – adjust ROU asset.

ROU asset

PE#1

Note: (1) Modified retrospective approach only

100© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Choosing a transition method

Significance of change in accounting Availability of

historical information

Comparability of information and

investor perceptions

Systems and processes Disclosure

requirements

Contract structure and volume of

contracts

Costs Future profit trends

Hot topics

102© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

103© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

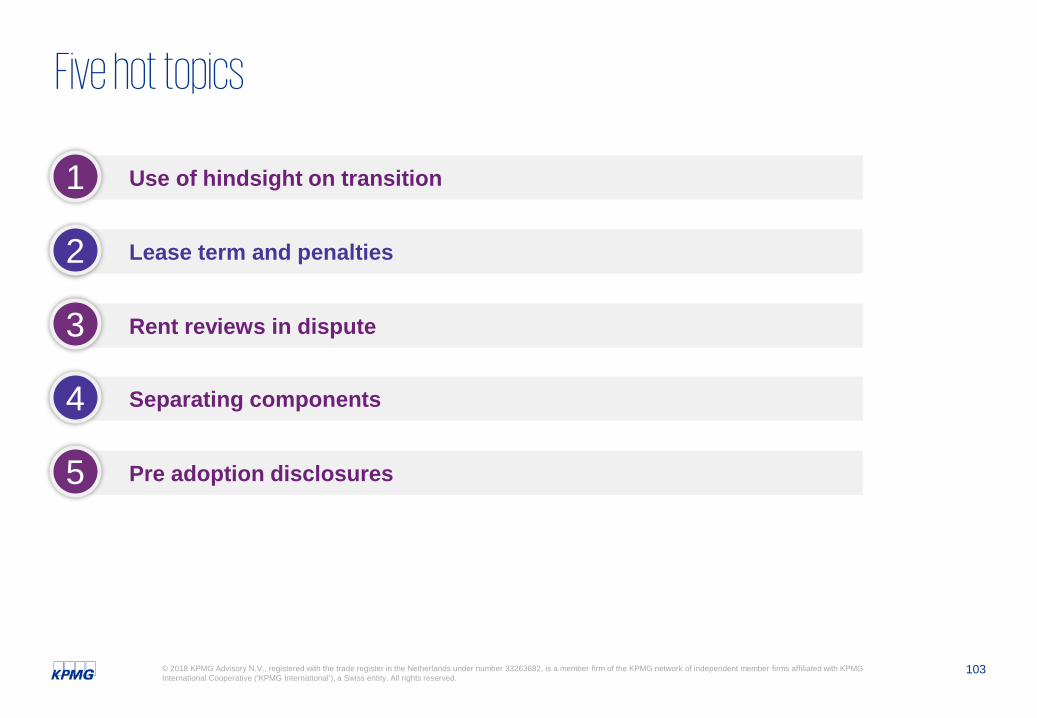

Five hot topics

Use of hindsight on transition

Lease term and penalties

Rent reviews in dispute

Separating components

Pre adoption disclosures

1

2

3

4

5

104© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

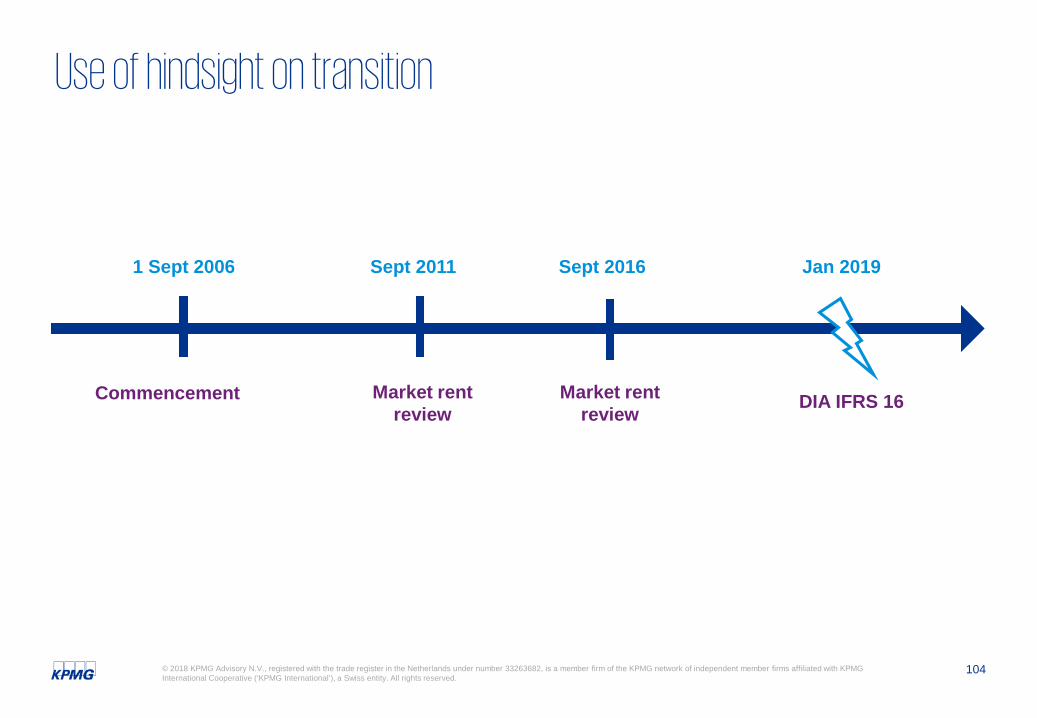

Use of hindsight on transition

1 Sept 2006 Sept 2011 Sept 2016

Commencement Market rent review

Market rent review

Jan 2019

DIA IFRS 16

105© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

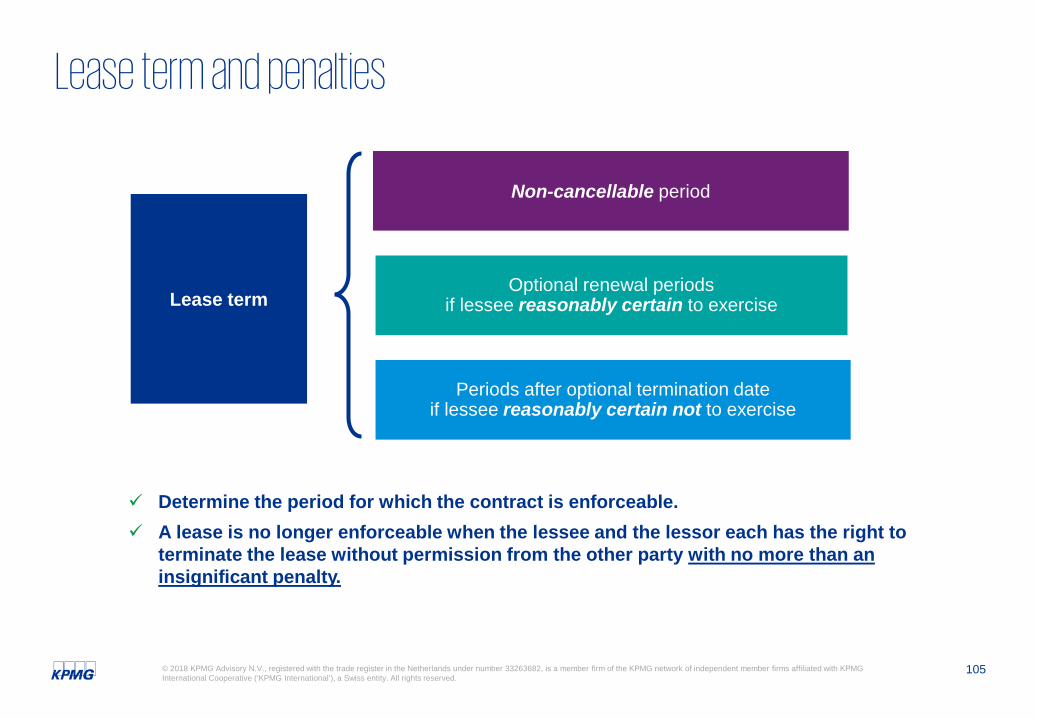

Lease term and penalties

Lease term

Non-cancellable period

Optional renewal periods if lessee reasonably certain to exercise

Periods after optional termination date if lessee reasonably certain not to exercise

Determine the period for which the contract is enforceable. A lease is no longer enforceable when the lessee and the lessor each has the right to

terminate the lease without permission from the other party with no more than an insignificant penalty.

106© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

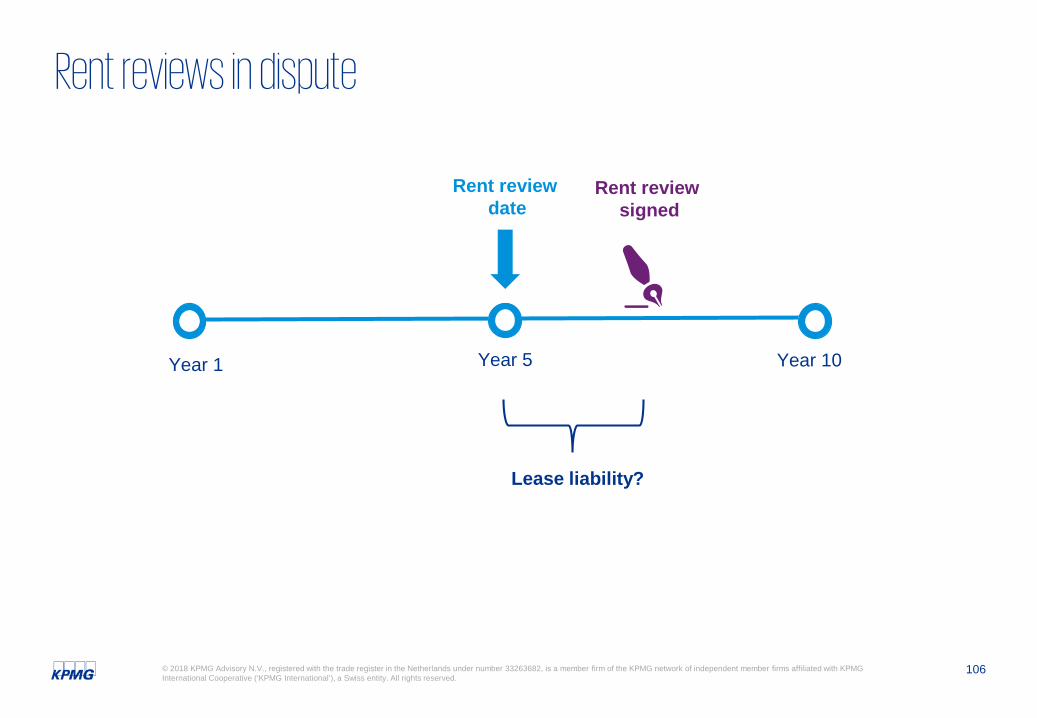

Rent reviews in dispute

Year 1 Year 5 Year 10

Rent review signed

Rent review date

Lease liability?

107© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

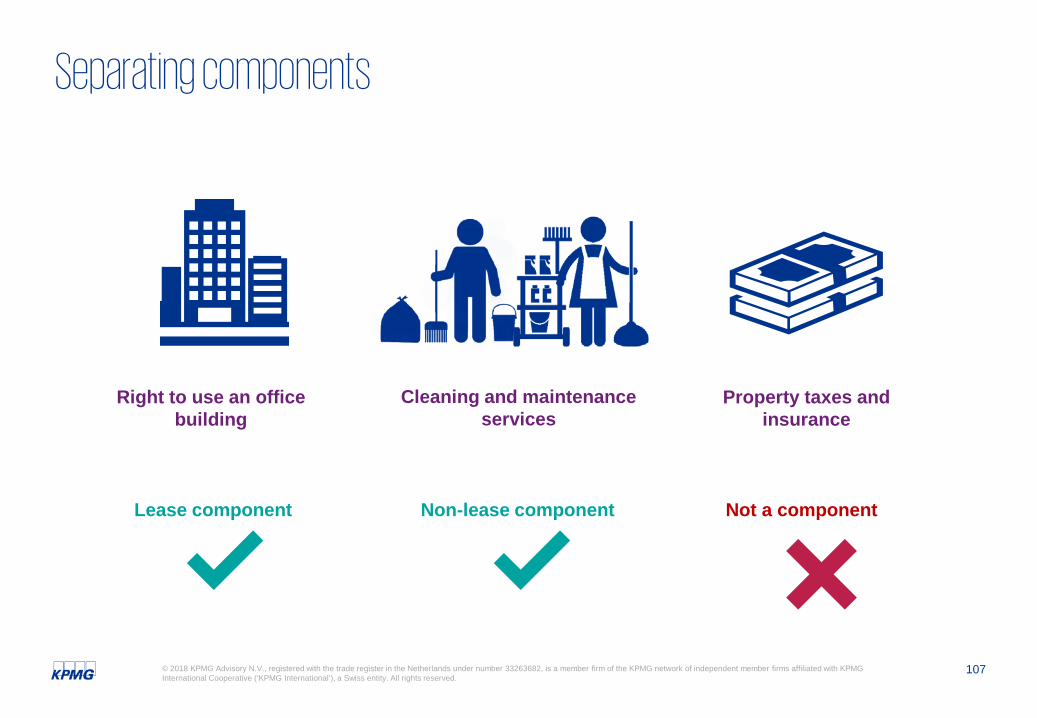

Separating components

Right to use an office building

Cleaning and maintenance services

Property taxes and insurance

Lease component Non-lease component Not a component

108© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Pre-adoption disclosures

Transition method?Practical

expedients?

Expected impact?

Project status?

109© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

What questions do you have?

Thank you

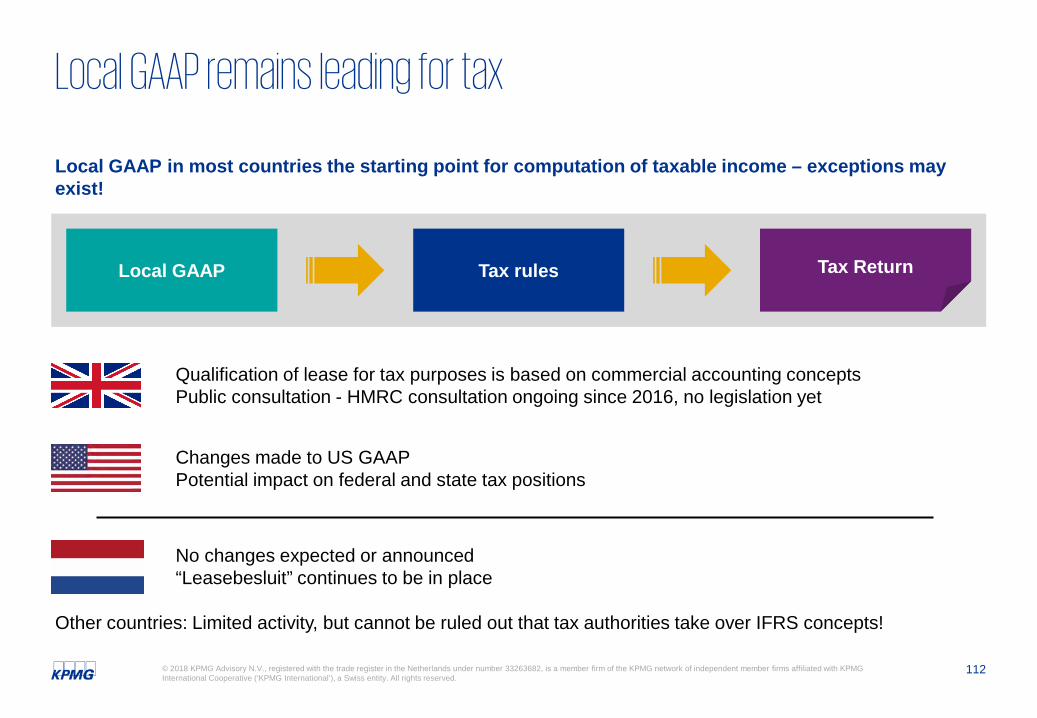

Tax perspective

112© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Local GAAP in most countries the starting point for computation of taxable income – exceptions may exist!

Local GAAP remains leading for tax

Tax rulesLocal GAAP Tax Return

Qualification of lease for tax purposes is based on commercial accounting concepts Public consultation - HMRC consultation ongoing since 2016, no legislation yet

Other countries: Limited activity, but cannot be ruled out that tax authorities take over IFRS concepts!

Changes made to US GAAP Potential impact on federal and state tax positions

No changes expected or announced“Leasebesluit” continues to be in place

113© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

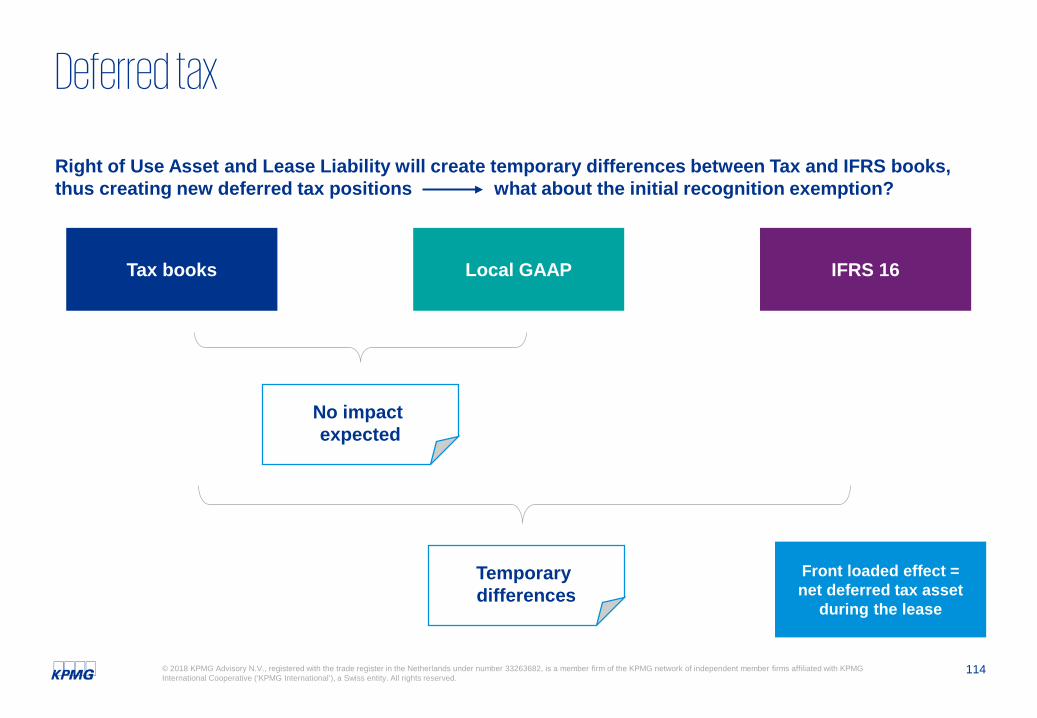

114© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Right of Use Asset and Lease Liability will create temporary differences between Tax and IFRS books, thus creating new deferred tax positions what about the initial recognition exemption?

Deferred tax

Tax books Local GAAP IFRS 16

No impact expected

Temporary differences

Front loaded effect = net deferred tax asset

during the lease

115© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Tax accounting take awaysIFRS 16 – Potential Tax impacts

make sure that your tax department / tax accounting team is involved in your IFRS 16 implementation project

jurisdiction by jurisdiction review to determine any local changes to tax rules and/or local GAAPs

What should each company implementing IFRS 16 at least consider from a tax accounting perspective?

1.

2.

116© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Other tax areas potentially impacted IFRS 16 – Potential Tax impacts

Non-deductibility and / or withholding tax on lease liability interest

Non-deductibility of depreciation expense on the ROU asset

Wage tax impact for incentive plans based on EBITDA metrics

Transfer pricing and valuation models relying on EBITDA should be revisited. Benchmarking more complex

Existing (tax) lease structures to be tested for continued working as intended

1

2

3

4

5

117© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

— Dutch tax accounting governed by sound business principle: ‘goedkoopmansgebruik’— Main rules: as long as the accounting standard is in line with rules of business economics

(bedrijfseconomische beginselen) and not contrary to general tax principles or specific tax rules— Thus, can IFRS16 be considered as:

i. in line with rules of business economics; and ii. not contrary to tax rules and principles

— Why not?

Can IFRS16 also be applied for tax purposes?

Is it possible? Is it beneficial?

118© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Can IFRS16 also be applied for tax purposes?

Is it possible? Is it beneficial?

— Additional liability: many countries apply debt:equity rules or other forms interest deductibility restrictions— Increased EBITDA: could be beneficial for interest restrictions based on EBITDA

– New rules expected: any interest above 30% of EBITDA non-deductible— Additional asset: is the depreciation on the ROU deductible?— Adjustment in equity upon adoption of IFRS16: for tax purposes through P&L?

119© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

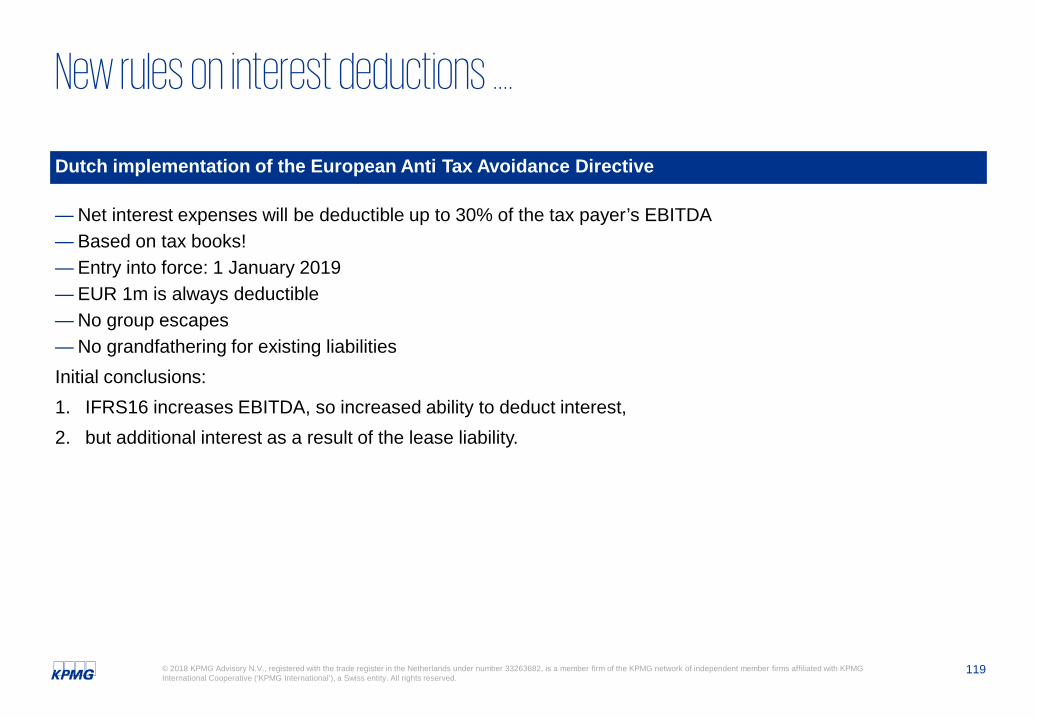

Dutch implementation of the European Anti Tax Avoidance Directive

— Net interest expenses will be deductible up to 30% of the tax payer’s EBITDA — Based on tax books!— Entry into force: 1 January 2019— EUR 1m is always deductible— No group escapes — No grandfathering for existing liabilitiesInitial conclusions: 1. IFRS16 increases EBITDA, so increased ability to deduct interest, 2. but additional interest as a result of the lease liability.

New rules on interest deductions ….

120© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

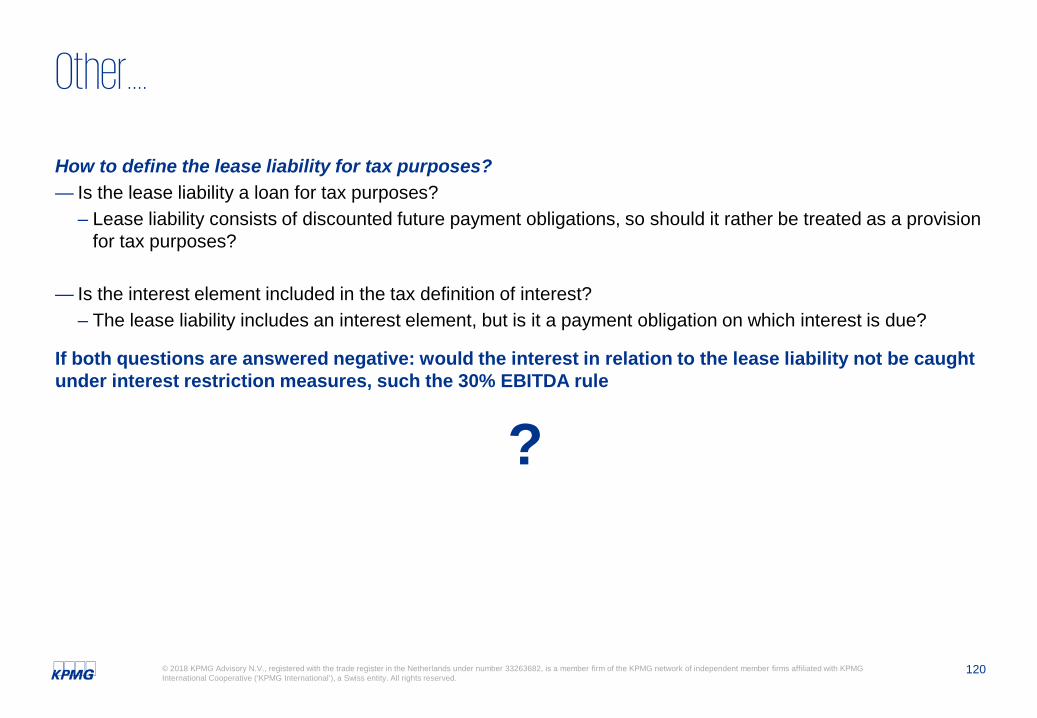

How to define the lease liability for tax purposes?— Is the lease liability a loan for tax purposes?

– Lease liability consists of discounted future payment obligations, so should it rather be treated as a provision for tax purposes?

— Is the interest element included in the tax definition of interest?– The lease liability includes an interest element, but is it a payment obligation on which interest is due?

If both questions are answered negative: would the interest in relation to the lease liability not be caught under interest restriction measures, such the 30% EBITDA rule

?

Other….

121© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

What Questions Do You Have?

122© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

Resources

First Impressions Transition Options

IFRS 16 Webinar (Podcast)

Lease Definition Discount Rates

IFRS 16 Leases website

Lease Payments Illustrative Disclosures

IFRS 16 Update mail

Thank you

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

KPMG on social media KPMG app

© 2018 KPMG Advisory N.V., registered with the trade register in the Netherlands under number 33263682, is a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved.

The KPMG name and logo are registered trademarks of KPMG International.