Honda Canada Inc.

Presentation on theAssociates Pension Plan

March 2017

Steve Gendron, FCIA, Principal, Eckler Ltd.

Agenda

1

Bill C-27

CPP Enhancements

Associates Pension Formula and CPP

Access to Associates Pension Plan Assets

Competitive Position of Associates Pension Plan

Questions

Appendix Associates Pension Plan Actuarial Valuation Results

Agenda

2

Bill C-27

CPP Enhancements

Associates Pension Formula and CPP

Access to Associates Pension Plan Assets

Competitive Position of Associates Pension Plan

Questions

Appendix Associates Pension Plan Actuarial Valuation Results

Bill C-27

3

October 2016; Bill C-27, Amend the Pension Benefits Standards Act

“PBSA” is applicable to federally registered pension plans sponsored by federally

regulated organizations such as banks, marine/air/railway companies, phone and

cable companies, etc.

Not applicable to Honda Canada or the Associates Pension Plan

Key provisions of C-27:

1. Introduce legislation for “Target Benefit Plans” (TBP)

A TBP is a cross between a DB and a DC pension plan

TBPs introduce risk-sharing on behalf of the employees in that the target benefit pension

can be adjusted based on the plan’s funding status (i.e. accrued pensions can be reduced

if the plan’s assets are less than liabilities)

2. Plans may purchase immediate or deferred annuities from Canadian insurance

companies to fully settle the plan’s obligations

The Associates Pension Plan is a defined benefit plan registered in Ontario and cannot reduce accrued benefits. If the assets in the Associates plan are less than the liabilities, Honda is required by law to make additional contributions

Agenda

4

Bill C-27

CPP Enhancements

Associates Pension Formula and CPP

Access to Associates Pension Plan Assets

Competitive Position of Associates Pension Plan

Questions

Appendix Associates Pension Plan Actuarial Valuation Results

CPP Enhancements

5

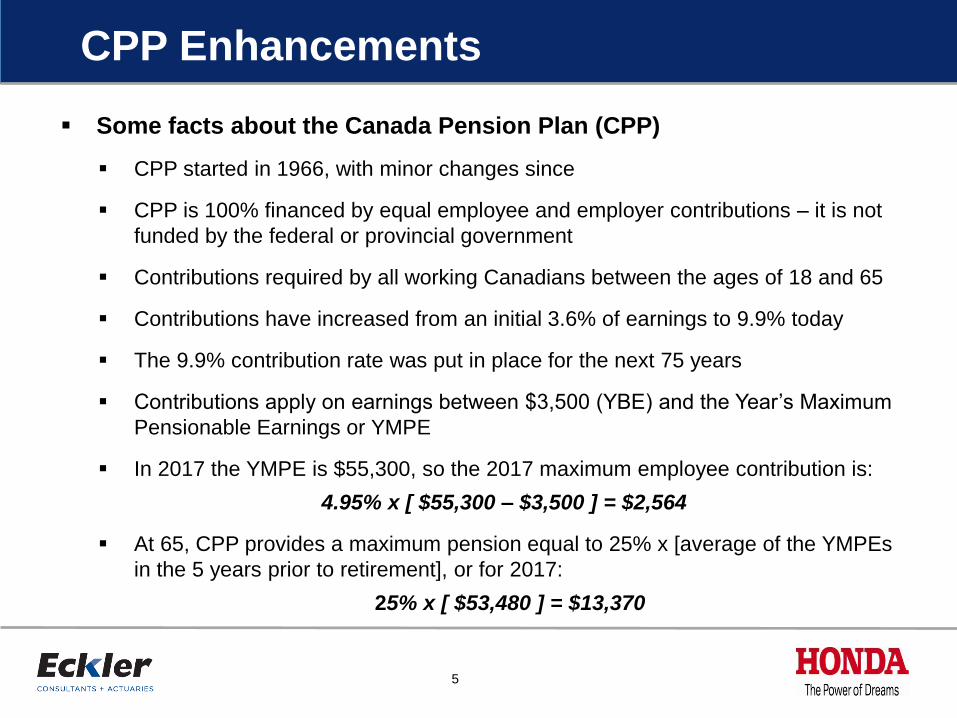

Some facts about the Canada Pension Plan (CPP)

CPP started in 1966, with minor changes since

CPP is 100% financed by equal employee and employer contributions – it is not

funded by the federal or provincial government

Contributions required by all working Canadians between the ages of 18 and 65

Contributions have increased from an initial 3.6% of earnings to 9.9% today

The 9.9% contribution rate was put in place for the next 75 years

Contributions apply on earnings between $3,500 (YBE) and the Year’s Maximum

Pensionable Earnings or YMPE

In 2017 the YMPE is $55,300, so the 2017 maximum employee contribution is:

4.95% x [ $55,300 – $3,500 ] = $2,564

At 65, CPP provides a maximum pension equal to 25% x [average of the YMPEs

in the 5 years prior to retirement], or for 2017:

25% x [ $53,480 ] = $13,370

CPP Enhancements

6

CPP should form only part of your retirement income

Other sources of retirement income include:

Old Age Security

100% paid for by Federal government

Payable at age 65

Associates Pension Plan – DB or DC

Your DC contributions are tax deductible and interest is not taxable

Income is taxable when taken

Registered Retirement Savings Plan (RRSP)

Contributions are tax deductible and interest is not taxable

Income is taxable when taken

Tax Free Saving Account (TFSA)

Contributions are not tax deductible and interest is not taxable

Income is not taxable when taken

Non-registered savings

Contributions are not tax deductible and interest is taxable annually

Income is not taxable when taken

Government

Honda

Associate

CPP Enhancements

7

Why Enhance the CPP?

Federal government concerned that Canadians are not saving enough for

retirement

Canadians favoured expanding CPP vs. other options such as Ontario’s “ORPP”

What is changing?

Employee and employer contributions are increasing starting in 2019

Retirement pension will gradually increase over a 40-year period with pro-rated

enhancements for those that retire before 40 years of higher contributions

No changes for those currently retired and receiving CPP pension

Impact to Employer Sponsored Pension / Savings Plans?

All employers will face increased CPP contributions starting in 2019

Too early at this point to say whether employers will embrace the CPP

enhancements or offset their increased costs in some fashion

CPP Enhancements

8

What’s new: 3 Tiers of Employee Contributions:

Tier 1 (“Base Contributions”)

Current contribution rate of 4.95% of earnings between YBE and YMPE

No change from existing CPP

Tier 2 (“First Additional Contributions”)

Additional 1.0% of earnings between YBE and YMPE

Phased in gradually starting in 2019 over 7 years

0.15% in 2019, 0.3% in 2020, 0.5% in 2021, 0.75% in 2022 and 1.0% > 2023

Tier 3 (“Second Additional Contributions”)

Additional 4.0% of earnings between YMPE and new YAMPE

Starting in 2024

YAMPE will be 7% higher than YMPE in 2024 and 14% higher in 2025

Employer must match employee contribution rate

CPP Enhancements

9

Three Tiers of Employee CPP Contributions*

*This diagram shows the three tiers of employee CPP contribution rates that will be in effect, as well as the pensionable earnings to which the rates will apply. Honda will be required to contribute the same amount.

Three Tiers of Employee CPP Contributions*

CPP Enhancements

10

Impact on Employee Contributions in 2025 Associate A Associate B

Earnings in 2025 $50,000 $100,000

YBE $3,500 $3,500

Projected 2025 YMPE $72,500 $72,500

Projected 2025 YAMPE $82,700 $82,700

Tier 1: 4.95% x [ Earnings between YBE and YMPE ] $2,301 $3,415

Tier 2: 1.0% x [ Earnings between YBE and YMPE ] $465 $690

Tier 3: 4.0% x [ Earnings between YMPE and YAMPE] $0 $408

Total $2,766 $4,513

% increase in employee contributions 20.2% 32.2%

% increase in employer contributions 20.2% 32.2%

CPP replacement ratio at 65

35%

30%

25%

20%

15%

10%

5%

0%

20 40 60 20 40 60 20 40 60 20 40 60

Age in 2016

Note: Assumes all wor ker s star t contr ibut ing to the CPP at age 20.

Workers

earning

Workers

earning

Workers

earning

Workers

earning

$40,000 $60,000 $80,000 $100,000

in 2016 in 2016 in 2016 in 2016

Basic CPP

Enhanced CPP

Rat

e of

ea

rnin

gs r

epl

ace

d by

CP

P a

t 6

5

CPP Enhancements

11

Agenda

12

Bill C-27

CPP Enhancements

Associates Pension Formula and CPP

Access to Associates Pension Plan Assets

Competitive Position of Associates Pension Plan

Questions

Appendix Associates Pension Plan Actuarial Valuation Results

Associates Pension Formula & CPP

13

Associates Pension Plan lifetime pension formula:

[1.25% x Best 5-year average earnings up to 5-year average YMPE

plus

1.75% x Best 5-year average earnings over 5-year average YMPE ]

times

Service (to a maximum of 35 years)

Associates Plan does not reference the new YAMPE, therefore any

enhancement to the CPP will not impact your Associates pension

Question: Will CPP enhancements impact my Associates DB Pension?Answer: No

Associates Pension Formula & CPP

14

Your accrued pension (for service to date) can never decrease!

Your projected pension (for all service) is estimated on your annual pension

statement and assumes that your earnings will remain constant until

retirement

If your actual earnings do not increase in a given year, your projected

pension at retirement will decrease when the YMPE increases

Example 2015 Annual Statement 2016 Annual Statement

Projected best average earnings $90,000 $90,000

Projected average YMPE $52,200 $53,200

Projected service at retirement 30 30

Pension formula[1.25% x $52,200 +

1.75 x ( $90,000 - $52,200 )] x 30= $39,420

[1.25% x $53,200 +1.75 x ( $90,000 - $53,200 )] x 30

= $39,270

Question: Can my projected pension decrease on my annual statement?Answer: Yes, if your salary increase is less than the increase in YMPE

Agenda

15

Bill C-27

CPP Enhancements

Associates Pension Formula and CPP

Access to Associates Pension Plan Assets

Competitive Position of Associates Pension Plan

Questions

Appendix Associates Pension Plan Actuarial Valuation Results

Access to Honda Pension Assets

16

The Associates Plan is governed by the Ontario Pension Benefits Act (PBA)

The Ontario PBA specifies:

“The administrator of a pension plan shall exercise the care, diligence and skill in

the administration and investment of the pension fund that a person of ordinary

prudence would exercise in dealing with the property of another person”

“…employer who is required to make contributions under a pension plan…shall

make payments to the pension fund”

The assets of the Associates Plan are held in a trust – separate and distinct

from Honda. Northern Trust is the trustee for the Associates Plan.

The Ontario PBA requires Honda to file audited financial statements in

respect of the Associates Plan annually. The audit is conducted by KPMG,

who reviews all transactions that occurred during the year, such as

contributions, benefit payments, fees, etc. Copies of the audited financial

statements are available upon request.

Agenda

17

Bill C-27

CPP Enhancements

Associates Pension Formula and CPP

Access to Honda Canada Pension Assets

Competitive Position of Associates Pension Plan

Questions

Appendix Associates Pension Plan Actuarial Valuation Results

Competitive Position of Honda Plan

18

DB Plan – For Associates hired before January 1, 2014

Non-contributory Most plans require member contributions

Final average earnings Your pension is based on your average earnings at retirement

Early retirement provisions Unreduced at earliest of 30 years service, 85 points or age 60 & 10

Pension Enhancement Account Allows you to make tax-deductible contributions and “buy” benefits

The DB plan would be in the top 25% of all private sector employer sponsored plans

DC Plan – For Associates hired after December 31, 2013

Honda’s Base contribution 4%, 5% or 6% of earnings (based on your years of service)

Your optional contributions 0% - 8% of earnings

Honda’s matching contributions 100% match of your contributions up to 4%

The DC plan would be in the top 25% of all private sector employer sponsored plans

Competitive Position of Honda Plan (DB)

19

Observations:

Honda and Toyota DB plans are final average earnings type plans, therefore pensions

increase automatically as earnings increase (Detroit-3 have to negotiate pension

increases)

Honda’s DB plan provides the highest lifetime pension

All pension amounts assume 30 years of service. Detroit 3 pension amounts are based on current collective agreements.

2,055 2,055

2,430

2,070 2,070

2,448

2,050

2,410

2,910

2,183

2,809

3,246

2,131

0

500

1,000

1,500

2,000

2,500

3,000

3,500

70,000 80,000 90,000

Mo

nth

ly p

en

sio

n

Annual earnings

Lifetime Pension Comparison - from age 65

GM/Chrysler Ford Toyota Honda

71,800 80,000 90,000

3,515 3,515 3,5153,545 3,545 3,5453,615 3,615

4,010

3,566

4,191

4,629

3,515

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

70,000 80,000 90,000

Mo

nth

ly p

en

sio

n

Annual earnings

Minimum Pension Comparison - prior to age 65

GM/Chrysler Ford Toyota Honda

71,800 80,000 90,000

Agenda

20

Bill C-27

CPP Enhancements

Associate’s Pension Formula and CPP

Access to Associates Pension Plan Assets

Competitive Position of Associates Pension Plan

Questions

Appendix Associates Pension Plan Actuarial Valuation Results

21

Appendix:

Associates Pension Plan Actuarial Valuation Results

Associates Plan – Valuation Results

22

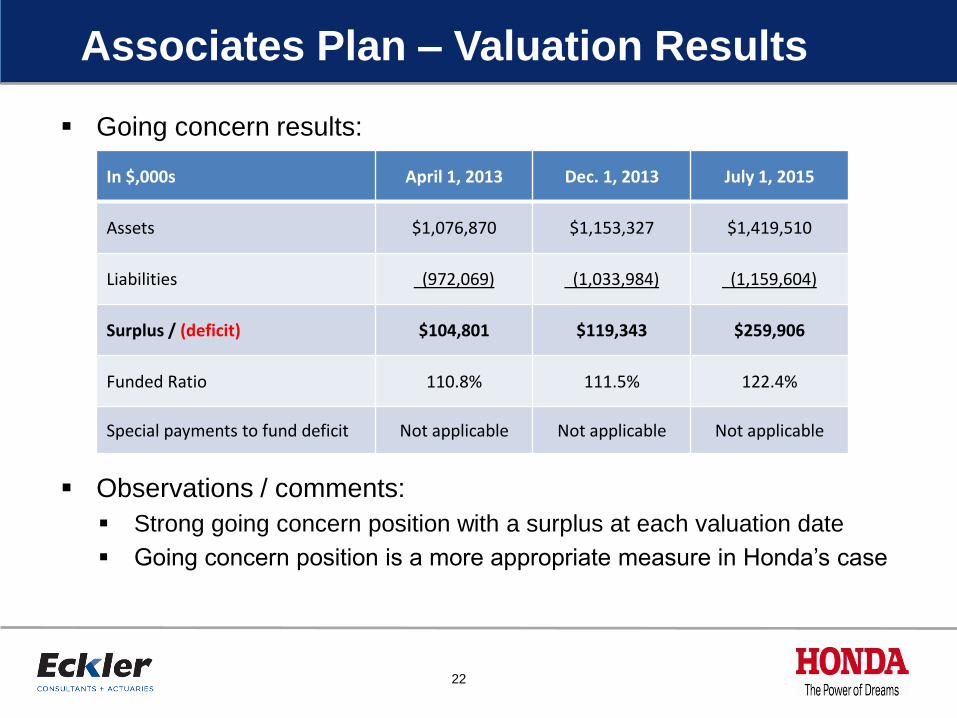

Going concern results:

In $,000s April 1, 2013 Dec. 1, 2013 July 1, 2015

Assets $1,076,870 $1,153,327 $1,419,510

Liabilities (972,069) (1,033,984) (1,159,604)

Surplus / (deficit) $104,801 $119,343 $259,906

Funded Ratio 110.8% 111.5% 122.4%

Special payments to fund deficit Not applicable Not applicable Not applicable

Observations / comments:

Strong going concern position with a surplus at each valuation date

Going concern position is a more appropriate measure in Honda’s case

Associates Plan – Valuation Results

23

Wind-up results:

In $,000s April 1, 2013 Dec. 1, 2013 July 1, 2015

Assets $1,067,823 $1,199,721 $1,451,830

Liabilities (1,302,625) (1,241,831) (1,630,825)

Surplus / (deficit) ($234,802) ($42,110) ($178,995)

Funded Ratio 81.8% 96.6% 89.0%

Special payments to fund deficit$50.1M per year

for 5 years$50.1M per year

for 11 months$38.9M per year

for 5 years

Observations / comments:

Significant fluctuation in results which are almost entirely due to fluctuations in prescribed interest rates

Wind-up position is only appropriate if the plan is wound up

Associates Plan – Valuation Results

24

Honda’s annual contribution requirements:

In $,000s April 1, 2013 December 1, 2013 July 1, 2015

Defined benefit component $52,175 $53,542 $54,215

Defined contribution component n/a 1,000 1,828

Special payments towards deficit 50,116 42,110 38,909

Total contributions $102,291 $96,652 $94,952

Observations / comments:

Honda’s contributions have averaged around $97M per year for the last four years

Associates Plan – Investment returns

25

Historical investment returns:

Calendar Year “Benchmark” Return Honda’s Fund Return

2016 7.2% 8.6%

2015 3.6% 2.1%

2014 9.6% 8.8%

2013 10.2% 10.9%

2012 8.1% 8.5%

2011 -0.6% -1.0%

2010 10.0% 8.5%

2009 15.5% 16.3%

2008 -15.9% -14.6%

2007 2.1% 0.1%

2006 12.1% 13.3%

2005 12.0% 11.9%

2004 9.4% 10.0%

2003 14.1% 12.3%

2002 -4.1% -3.2%

10-year annualized return of 4.5%

15-year annualized return of 5.9%