Going into DebtGoing into Debt

Americans and CreditAmericans and Credit What is credit?What is credit?

Receiving funds directly or indirectly, to buy Receiving funds directly or indirectly, to buy goods and services w/ promise to pay them backgoods and services w/ promise to pay them back

Principal – Amount originally borrowedPrincipal – Amount originally borrowed Interest – Amount of money, borrower must pay to use Interest – Amount of money, borrower must pay to use

someone else's money.someone else's money.

Everyone in the nation has a credit score based Everyone in the nation has a credit score based on your credit history.on your credit history.

Anytime you borrow money, whether from back, Anytime you borrow money, whether from back, store, or credit card company you go into debt.store, or credit card company you go into debt.

Americans and CreditAmericans and Credit Installment DebtInstallment Debt

Most common type of debt, paid back with equal Most common type of debt, paid back with equal payments over a given amount of time.payments over a given amount of time.

Monthly payment determined by length of contract, Monthly payment determined by length of contract, amount borrowed, and interest rateamount borrowed, and interest rate

The longer the life of the loan, the more you will pay back.The longer the life of the loan, the more you will pay back.

Largest and most common kind of ID is a mortgageLargest and most common kind of ID is a mortgage

All debt is not bad; housing, student loans, car All debt is not bad; housing, student loans, car loans.loans.

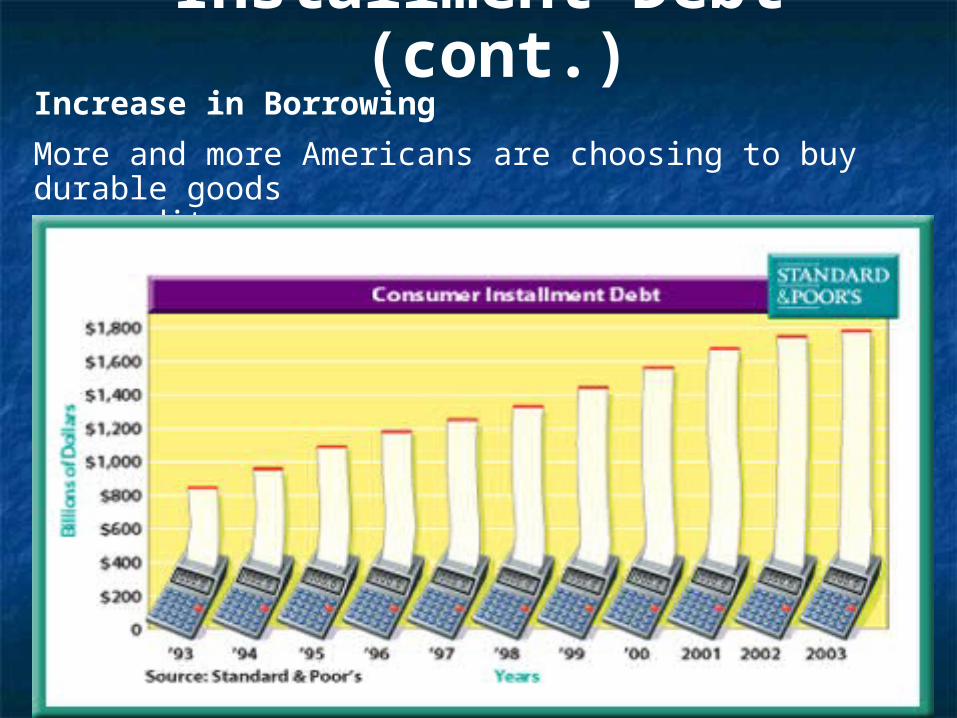

Increase in Borrowing

More and more Americans are choosing to buy durable goods on credit.

Installment Debt (cont.)

Pay Now or Pay Later

Your monthly payment is lower if you choose the 36-month loan.

Installment Debt (cont.)

Americans and CreditAmericans and Credit Why people use Credit?Why people use Credit?

People are impatient. Feel the need to satisfy People are impatient. Feel the need to satisfy wants immediately. wants immediately.

Again, some responsible, some notAgain, some responsible, some not

Spread payments out over timeSpread payments out over time Car, house, collegeCar, house, college

Build credit for future important purchasesBuild credit for future important purchases Only works with on-time, full monthly paymentsOnly works with on-time, full monthly payments

Sources of Loans and CreditSources of Loans and Credit Types of Financial Institutions Types of Financial Institutions

Commercial BanksCommercial Banks Accept deposits, lend money, transfer funds among Accept deposits, lend money, transfer funds among

people and businesses. Typical bank; Sun Trust, people and businesses. Typical bank; Sun Trust, Wachovia….Wachovia….

Typically higher interest rates and longer loan life.Typically higher interest rates and longer loan life. Typically only do small loansTypically only do small loans

Savings and LoansSavings and Loans Accepts deposits and gives out loansAccepts deposits and gives out loans Typically lower interest rates Typically lower interest rates Focus mainly on large loans; (Car, House)Focus mainly on large loans; (Car, House)

Sources of Loans and CreditSources of Loans and Credit Types of Financial InstitutionsTypes of Financial Institutions

Savings bankSavings bank Lend funds for homes, cars, loans…Lend funds for homes, cars, loans… Really non-existent anymoreReally non-existent anymore Originally served less wealthy customers overlooked by Originally served less wealthy customers overlooked by

commercial bankscommercial banks Tend to have higher interest rates.Tend to have higher interest rates.

Credit UnionCredit Union Offer all services only to members.Offer all services only to members. Usually forms around a given job field.Usually forms around a given job field. Typically lower interest rates Typically lower interest rates

Types of Financial Types of Financial InstitutionsInstitutions

Types of Financial InstitutionsTypes of Financial Institutions Finance CompaniesFinance Companies

Basically store credit cards.Basically store credit cards. Take over installment debt for stores and charges Take over installment debt for stores and charges

higher interest rateshigher interest rates

Credit/Debit Cards Credit Cards

The average American has 5 credit cards and about $12,000 in credit card debt

“Revolving Limit” meaning as long as you are under the maximum amount you may use.

Pay a certain amount back each month, plus interest

Interest (APR/MPR) determined by amount borrowed, and credit score.

Get charged a finance charge each month based upon amount owed and APR

Example you owe $5000 on your VISA, w/24% APR Monthly Bill ~$100.00 Finance Charge is $98.00 Next month you owe $4998.00

Debit Cards Link to checking account Limit is what you have in the bank Draws directly form your account. No Interest, or finance charge

Credit Rating What does your credit rating mean?

The risk involved in lending you money What factors determine your credit Rating?

Capacity to pay Ability to hold a job Current debt to income ration

Character Educational background Legal troubles

Collateral Size of your personal wealth Shows your past ability to pay or save as well as what

you might be able to see off to pay back a debt

Bankruptcy Legal right/ability for American Citizens to be

forgiven for debts

For people who absolutely cant pay back debts

Usually forced to give up most possessions to pay back debtors.

Remains on your credit report and effects you for 10 years. Difficult to reestablish credit during 1 this period. Can only claim once every 7 years

Types of Bankruptcy Several types, only two really pertain to

ordinary citizens. Chapter 7

Complete liquidation of assets. Possessions sold and profits split evenly among debtors. Savings (Not 401k), stock are distributed among debtors Remainder of debt forgiven by judge

In most cases allowed to keep; home, car, 401k. Chapter 13

Restructuring of debts according to court order Court decides how much you will pay each debtor

based on regular salary Debts repaid over 3-5 years, Keep possessions, usually works out in your favor

Assignment Pg. 87 #2,3 Pg. 94 #5 Pg. 99 #2, 3 Pg. 105 #3 Pg. 108 Recalling Facts and Ideas #2, 3, 9,

12.