Gas Competence SeminarMaputo, Mozambique – Septembre 2015

FUNDAMENTALREQUIREMENTSFOR MARKETDEVELOPMENT

Akmal M Zaghloul, MBABusiness Development Director

2

Energy Dimensions in Market Development

Engine for Economic Growth (High Correlation: Energy Consumption & GNP)

Facilitator of Social Progress

Key to Poverty Reduction

Employment Generation

Promotes Gender Equality

Vital Input in Production (All Sectors of Economy)

Increasingly Becoming a Need Rather than a Luxury

Key Element for Attracting Foreign Investment

Foreign Exchange Earner

2

3

Market development challenges

Energy Mix

Energy Pricing Crisis

Supply / Demand

Infrastructure

Legal, Governance & Regulatory framework

Social Impacts

4

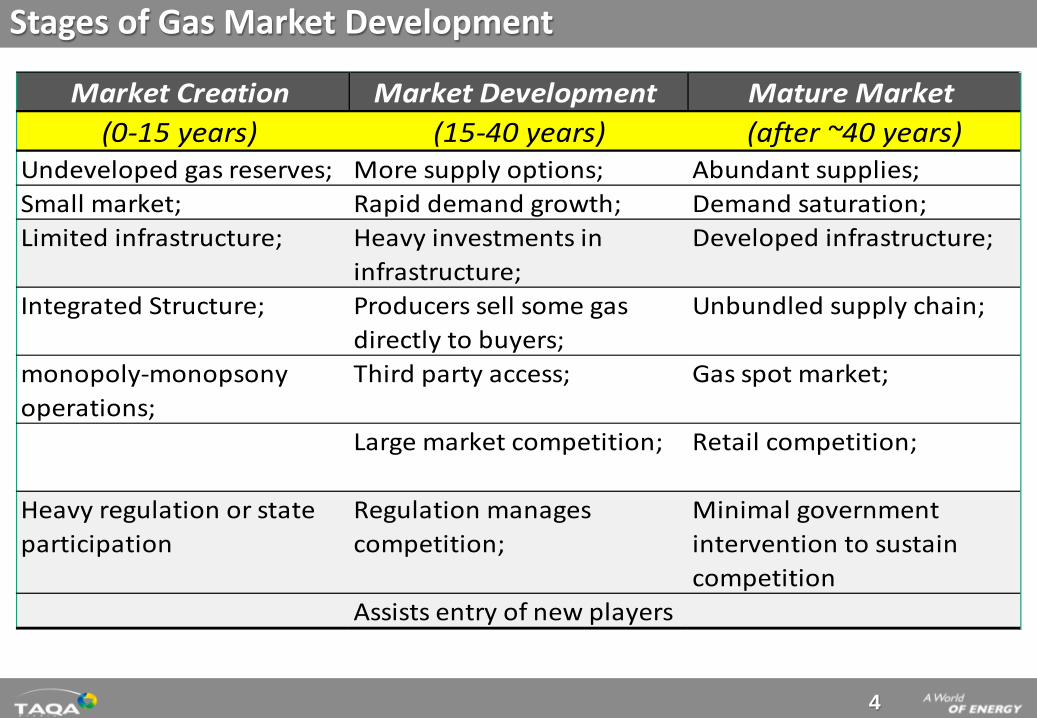

Stages of Gas Market Development

Market Creation Market Development Mature Market (0-15 years) (15-40 years) (after ~40 years)

Undeveloped gas reserves; More supply options; Abundant supplies;Small market; Rapid demand growth; Demand saturation;Limited infrastructure; Heavy investments in

infrastructure;Developed infrastructure;

Integrated Structure; Producers sell some gas directly to buyers;

Unbundled supply chain;

monopoly-monopsony operations;

Third party access; Gas spot market;

Large market competition; Retail competition;

Heavy regulation or state participation

Regulation manages competition;

Minimal government intervention to sustain competition

Assists entry of new players

5

Factors affecting level of development

Political differences

Different levels of economic development

Non-existance of own natural gas resources

Unavailability of foreign natural gas resourcescaused by their distance or a distance of supplygas pipelines

Availability of other own / imported energyresources

6

EGYPT CASE STUDY

7

Egypt’s Gas Industry Milestones

In 2014, Natural Gas share in Egypt total Energy Consumption: 52.5%

1st gasDiscovery

1967 1976 1981 1992 1996 2003 2012

1st

Industrialcustomer

1st

Residentialcustomer

1st CNG Vehicle

Private LDC

1st Gas Export

1st FSRUTender

2015

1st LNG import

8

New Exploration Concession Agreements

56 new upstream Exploration agreements signed$12 billion minimum commitment

9

Accelerate Existing Gas Development

Total Investment: $21.8 bn Total Production: 3,600 MMSCFD Total Condensate Production: 86.7 MBBL/D

10

Abu sir

West Abu Qir

North Idku

RavenScrab/safron

LNGDamietta

Arish &El masaid

Baltem

Port said

Hap’y

Theka

North Bardwell

Akhen

Naf

Roseta

El Sheikh Zowayed

East Port Said P.S & Ind. Area

East Gas

Flower

North SinaiHelm

Temsah

Talkha

Shabshir

Abu MadiAbu Qir

Abu Hommos South El Mansoura

Mahmudiya

Qara

Tanta

SouthBelquas

Abu sultan6 October

QusinaBanhaSadat

Suez

A’youn Moussa

Mostorud I-ATebbin

Koraymat

Ras BakrBeni Suef

Za’frana

October

Unit 103El Menia

Assuit

Unit 104

Unit 108

Zeit bay

Abu Rudis

Morgan

Ramadan

Esma 8

AgibaSea bird

Shoab Ali

Badri

Esma 2

Sinai Cement & industrial Area

Sedi Krier

Ameriya

King

El-Max

Intergene

BorgElarab

Ameriya Cement

12“- 14 Km

El obyed

Salam

South Aum Barkah

El Qasr

Tarek

Bed - 2

Abu Sannan

South Dab’aaMeleha Deep

Bed - 3Bed - 1 265 Km 24“-

Qena

LuxorAswan

Kima

Hurgada

Safaga

Cairo

Neag

A/GHKaroun

SouthEl-Tina

WestEl Tena

Jordan

DeniseTaurt

El GamilUGDC

South El Manzala

Shams

Saffaire

Simian/ sienna

Fayroz

Robi

Tarouse

Theth Med. South East Fields

Vegas fields

Desouk

A/RSuco

Belayim

Wastani

Fayoum

El Sokhna

• Existing . PL• Under cons. PL• Future. PL (5 Years)• Gas fields• Future Gas Fields• Facilities• Distribution Stations• Power stations• Industrial Areas• Consumer• Distribution Co.• Export

Ameriya

24“- 26 Km

18“- 12 Km

16“- 9 Km

24“- 26 Km

24“- 26 Km

32“- 160 Km

24“- 14 Km

30“- 26 Km

22“- 87 Km

24“- 25 Km

32“- 75 Km

24“- 215 Km

32“- 85 Km

28“- 86 Km

42“- 40 Km

30“- 28 Km

16“- 256 Km

16“- 192 Km

24“- 10 Km

22“- 40 Km

24“- 50 Km

36“- 196 Km

36“- 264 Km10 BCMY

20“- 660 Km

20“- 40 Km

12“- 40 Km

National Oil, Gas Grid & Facilities

Dahshour

Nubariya

North Port Said

Port Fouad

Sharm El Shikh

Suco

West Aswan

Ras Shukir

El Fayoum Offtake

Deshna

Quos

New Assuit

Upper Egypt P/L930 km, 1 Billon $

Total Length is 18000 Km with Capacity of 190 MM meter3/D In June 2012

11

Transmission Projects

Planned Projects: $355 million

12

Abu Madi

El Qara

Abu qir

Sedi Kreir

Ameriya 1

TarekEL-ObayiedSalamSouth Om Barka

Abu ElGhradikأ

Bed 2,3Ayoun Moussa

tebbin

suez

Zafrana

Ras bakr

Ras shoukier

المنیا

LTSLPGLTS & LPGNGLLNG

N. Abu Madi

Port said

Port fouadDamiatte

Production 2011/2012LPG : 1475 MTCond : 39.8 MMBBL Propane: 605 MT Ethane/ propane : 437 MT

Gas Treatment Facilities

Added Valuebillion $

Abu qirLPG& LTS

Design capacity:480 mmscf/d

sales Gas: 238 mmscf/dCond: 5530 bbl/d

Lpg: 220 Ton/d

SalamLTS

Design Capacity:400 mmscf/d

Sales Gas: 427 mmscf/dCond: 24000 bbl/d

TAREKLTS

Capacity: 100 mmscf/dsales gas: 111 mmscf/d

Cond: 12000 bbl/d

ObayiedLTS

Design capacity:420 mmscf/d

sales gas: 376 mmscf/dcond: 9500 bbl/d

Abu sanan / s. dabaaDesign capacity: 85 mmscf/d

Sales Gas: 38 mmscf/dCond: 980 bbl/d

Abu sanan

Bed 2,3LTS

Design capacity: 315 mmscf/dSales Gas: 275 mmscf/d

Cond: 5930 bbl/d

Abu ElghradigDesign capacity: 160 mmscf/d

Sales Gas: 72mmscf/d Cond: 1360 bbl/d

S.MansouraLTS

Design capacity:15 mmscf/d

Cond: 178 bbl/d

RosettaDesign capacity:

400 mmscf/d Sales Gas: 393mmscf/d

Cond: 340 bbl/d

BurullesFeed : 1328 mmscf/d

Cond: 6850 bbl/d

El GamilDesign capacity:1650 mmcsf/d

Sales Gas: 1368 mmscf/d Cond : 21685 bbl/d

WASCOSales Gas: 160 mmscf/d

Cond: 3920 bbl/dLPG: 190 Ton/d

W/ KHELALASales Gas:73 mmscf/d

Cond: 85 BBL/D

DahshourDesign capacity: 140 mmscf/d

Sales Gas: 0 mmscf/dLPG: 0 ton/d

Trans Gulf Design capacity : 130mmscf/d

Saled Gas : 1.8 mmscf/dCond : 1085 bbl/d LPG : 232 Ton/d

Ras ShoukierDesign capacity:

220 mmscf/dSales Gas: 24 mmscf/d

Cond: 555 bbl/d LPG: 185 Ton/d

Zeit BayDesign capacity : 90 mmscf/d

Sales Gas : 17 mmscf/dCond: 510 bbl/dLPG: 103 Ton/d

Abu RudiesDesign capacity: 50 mmscf/d

Sales Gas : 0.5 mmscf/dCond :1075 bbl/dLPG : 242 Ton/d

IdkuTrain1 : 580 mmscf/d Train2 : 580 mmscf/d

UGDCFeed : 1100mmscf/dPropane : 839 Ton/d

Lpg : 755Ton/ dCond : 3365 bbl/d

W/D Gas ComplexNGL Unit

Design capacity : 900 mmscfdEthane/ Propane : 1195 Ton/d

Propane : 815 Ton/d LPG : 1255 Ton/dCond : 2155 bbl/d

AmeriyaDesign capacity :

300 mmscf/dCond : 440 bbl/dLPG : 520 Ton/d

Hapy & TaurtDesign capacity:

600mm`scf/dSales Gas: 513 mmscf/d

Cond: 305bbl/d

N. SinaiDesign capacity:

180 mmscf/dSales Gas: 128 mmscf/d

Damiatte LNG Feed : 750 mmscf/d

LNG : 30 mscm/d

W.Dikrnis (Ph.1) S.Batra &Sales Gas : 14mmscfd

Cond :240 bbl/dLPG : 40 Ton/d

Abu Madi &N. Abu adiLTS

Design capacity : 360 mmscf/dLPG

Design capacity : 540 mmscf/d Sales Gas : 352 mmscf/d

Cond: 6600 bbl/d LPG : 290 Ton/d

S manzlaDesign capacity:

35 mmscf/dSales Gas: 18 mmscf/d

13

Expand & Upgrade Infrastructure

Projects in Refining: $9 bn

14

Develop the Petrochemicals Industry

Projects in Petrochemicals: $9.7 bn

15

Ensuring power generation security

16

Demand & Consumption Evolution

17

Gas Usages

Gas GridLocal Distribution

Gas Delivery

Fertilizers

Industry

CNG

Domestic

Power

Gas Value Chain in Egypt

18

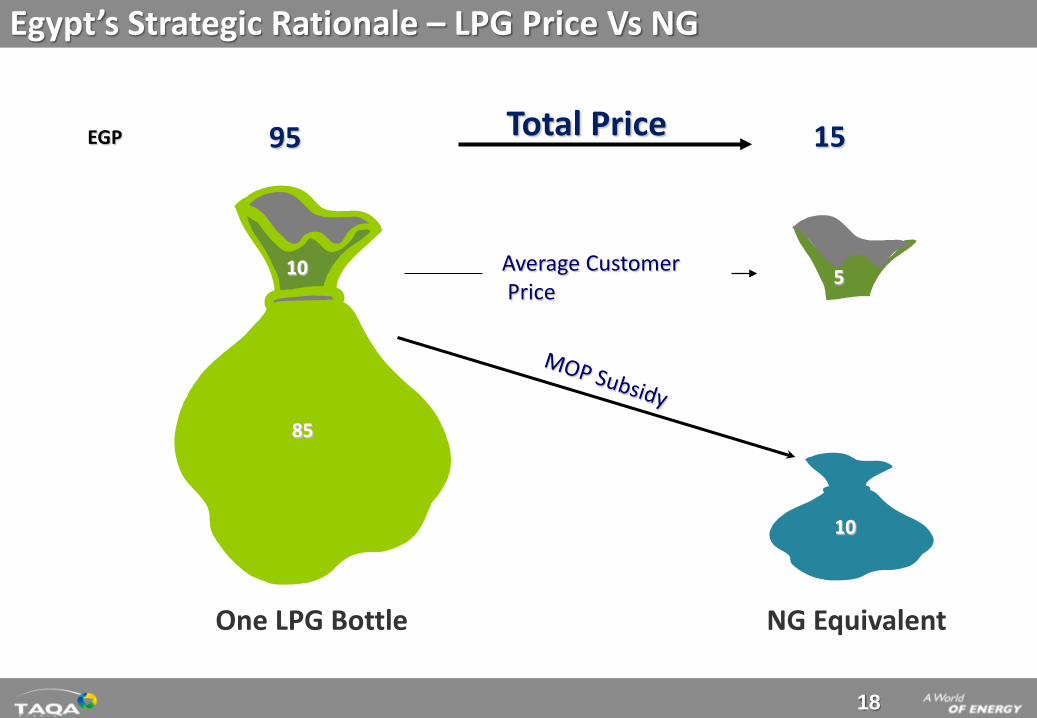

85

10

5

One LPG Bottle NG Equivalent

95 15Total Price

Average CustomerPrice

EGP

10

Egypt’s Strategic Rationale – LPG Price Vs NG

19

Gas to end users

• FactoriesMedium Heavy

- Chemical - Steel- Paint - Cement- Textile - Fertilizer- Food

Fuels substitution & conversionWater heating Space heating

Cooking Steam Generation

Furnaces Manufacturing Process Heat

Refrigeration Gas-fired Air-conditioning

Natural gas will replace:

• Diesel for water and central heating

• LPG for heating and cooking

• Fuel oil and diesel for industrial applications

• Gasoline in cars

Residential

Commercial

Industrial

• Apartments• Houses• Villas

• Hospitals• Schools and Universities• Offices• Restaurants• Bakeries etc.

20

GASCO

Power Stations HouseholdsIndustrial

FactoriesCommercial

Establishments

EGAS20-25Y Concession Agreement to :Finance, design, execute, operate& maintain Gas Networks

Manage, operate andmaintain the EgyptianNational Gas Grid

Transportation Vehicles

Gas Supply Contract

Agreement for :Gas Delivery & Metering

Gas Midstream & Downstream Market Structure

Gov. guarantees 18%IRR for LDCs (+ O&Mcosts +5Y tax exemption)

Local DistributionCompanies

EPCs

21

Gas Distribution – Deregulation Development

The Main National Grid / Trunk line is constructed & Operated by GASCO (on behalf of EGAS)Everything down stream of the Pressure Reduction Station is within the cost of the LDC connection rate. Payments made “per converted customer”

22

OverseasGas Maya Gas

Gas Contractor

LDC

Gas Distribution – Market Players

23

From ONE state monopoly …

… to 14 private sectors & 5 state-owned LDCs/EPCs

Development of the Egyptian Gas Distribution Sector

Off Take

P.R.SRegulator

Regulator

Typical Downstream Gas Network

Ongoing Distribution ActivitiesApprox. 3.5 Million customers connected

Over 1 bn $ of Foreign & Local investment

16 Egyptian Governorates covered by Gas networks

600 MM $ /Year Saved in subsidies

Enhanced HSE Standards

Introducing new technologies

Attracting the Multi-Nationals

Social Investment – Jobs/Employment - Environmental

Provide a better quality of life for Egypt’s citizens

24

Market based Incentives: CNG Smart Card

24

Mechanism

Financing 100% of cost of conversion throughcommercial lending on a debit card to bepresented at fueling stations by convertedvehicles’ drivers

Increase

No. of Vehicles Converted

25

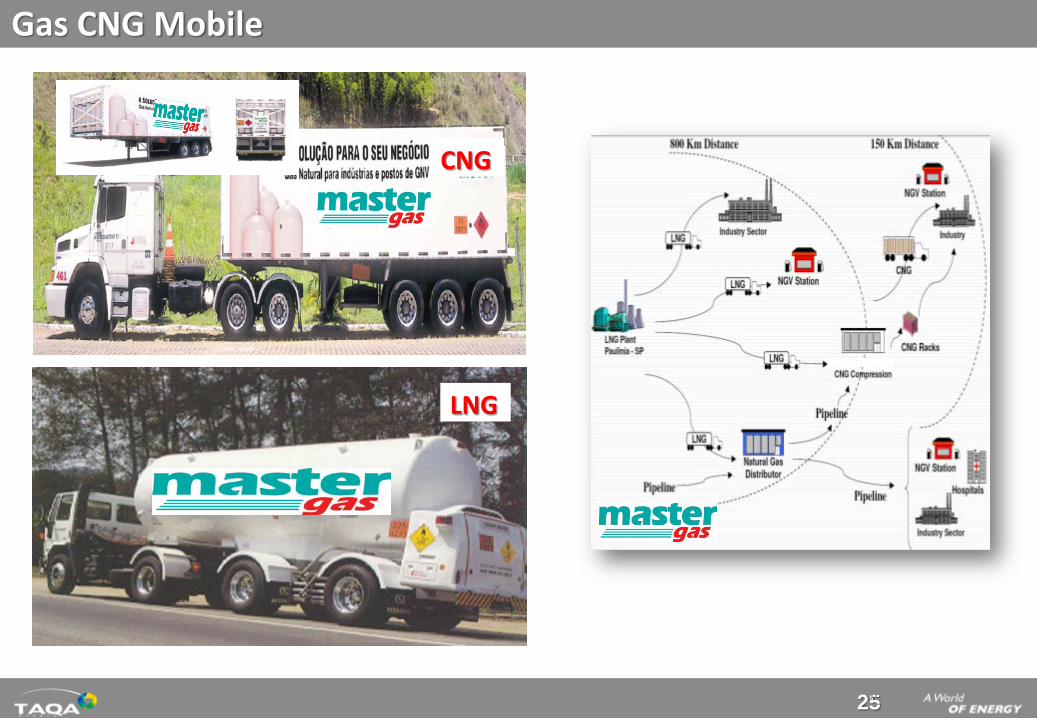

CNG

LNG

25

Gas CNG Mobile

26

Scope:• Using absorption chillers / heater units• BOO District cooling projects• 250 000 Ton

Clients Benefits:• Saving of 30-40% of operating cost

compared to electricity driven chillers• Less building Capex & Opex• Less Power • Less maintenance & staffing• Economical operating costs• No chillers noise & vibration• Space saving in the buildings

District cooling consists of 3 main parts:

Plant

Gas District Cooling

27

Synthetic Natural Gas (LPG+Air) Distribution Network

R

R

R

R

SNG StationLPG Tank

SNG =

LPG + Air

27

28

SNG Ready to use

29

30

31

EGYPT ENERGY STRATEGY

Winning hearts and changing mindsets ...

32

Egypt’s Strategic Investment/Development Rationale

Government Solutions Creating Market Opportunities

Egypt’s Economic Growth Vs. Energy Challenges

• Large increase in energy demand to 13 % annually• Economy growing at 7.2% before 2008 Global crisis• Energy subsidy increased from 30 B EGP in 2004 to 100 B in 2014-2015 budget.• National plan to convert additional 4 million customers to natural gas, to the existing 3

million• Government need to increase Power Generation capacity from 25 GW to 75 GW by 2030

• Egypt’s government is taking bold steps to liberalize the energy sector gradual phasingout of subsidies which is currently a burden on the budget, gradual market deregulation

• Implement and activate strong regulatory bodies• Encourage strong involvement of private sector investment and foreign direct investment

• Driven by rapidly rising domestic energy consumption on the back of population anddemographic dynamics, rising per capita income levels and a heightened level ofindustrialization, urbanization, real estate and tourism related investments, Egypt's primaryenergy demand continues to outpace energy supply infrastructure;

• From 2002 to 2012, oil products and natural gas consumption levels increased by 37%while electricity consumption increased by 30%. According to the Government's guidance,the former is expected to increase by 30-35% by 2015 and the latter is forecasted toincrease by 37-40% over the same period after incorporating the dragging effect of thecurrent economic slowdown.

Growing Energy Demand

33

Egypt Energy Challenges & Policy Options

33

Pricing Reform: Tariffs Subsidies

Institutional Restructure: Integrated Energy Regulator Market Liberalization (unbundling)

Legislation Modifications: New Electricity Law Hydrocarbon / Petroleum Law

Assessment & Prioritization of Energy DemandSecurity & Affordability of Energy Supply LNG import New & Renewable Energy Development

Energy Infrastructure DevelopmentAttraction of FDI in most of the Egyptian Energy Value ChainHuman Capacity Building & Best Practices Development

34

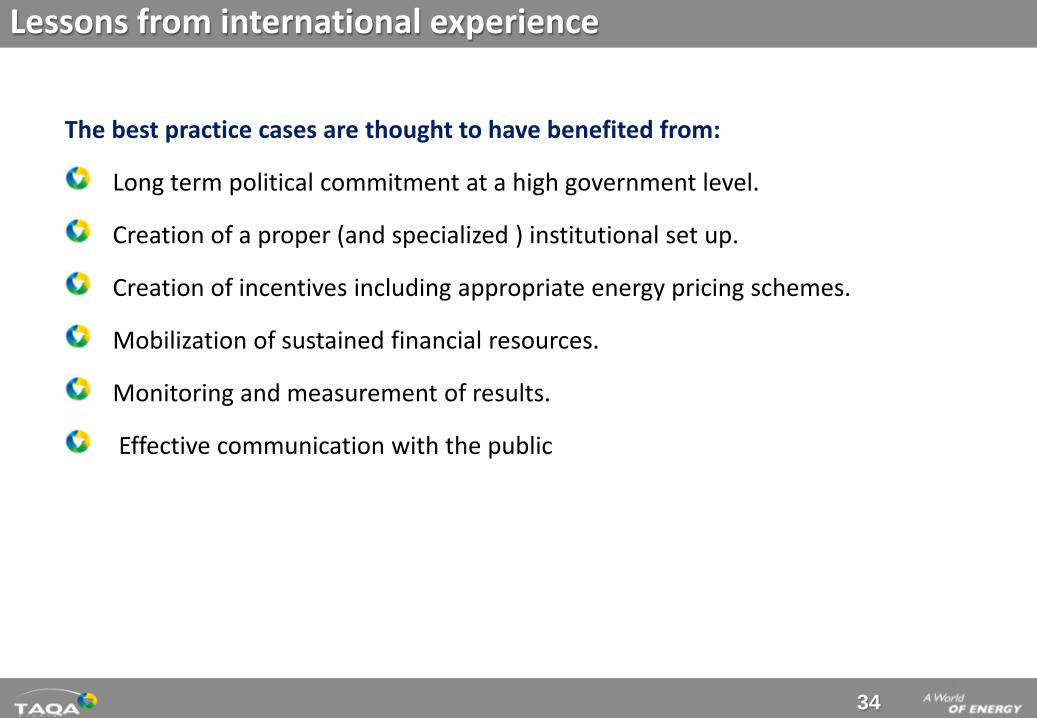

Lessons from international experience

34

The best practice cases are thought to have benefited from:

Long term political commitment at a high government level.

Creation of a proper (and specialized ) institutional set up.

Creation of incentives including appropriate energy pricing schemes.

Mobilization of sustained financial resources.

Monitoring and measurement of results.

Effective communication with the public