The Future of MobilityThe Future of Mobility

From Mega Trends to the Driverless CarFrom Mega Trends to the Driverless Car

by

Dorman Followwill

Partner

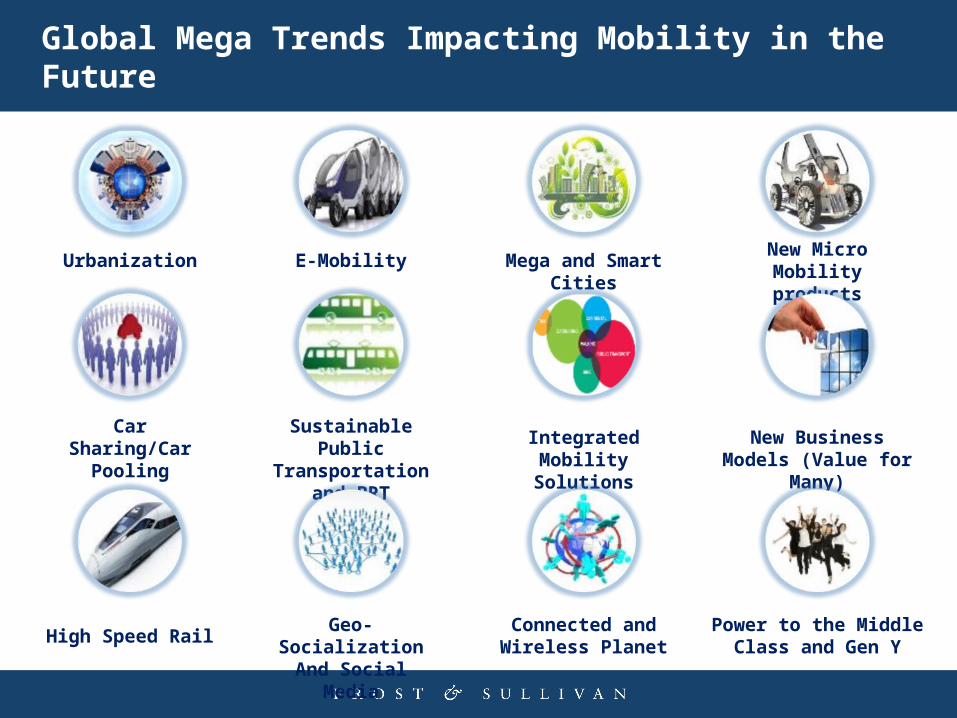

Mega Trends Impacting Mobility

Global Mega Trends Impacting Mobility in the Future

Car Sharing/Car

Pooling

Geo-SocializationAnd Social Media

New Micro Mobility products

Integrated Mobility Solutions

E-Mobility

Connected and Wireless Planet

Sustainable Public Transportation and

BRT

High Speed Rail

Urbanization Mega and Smart Cities

New Business Models (Value for Many)

Power to the Middle Class and Gen Y

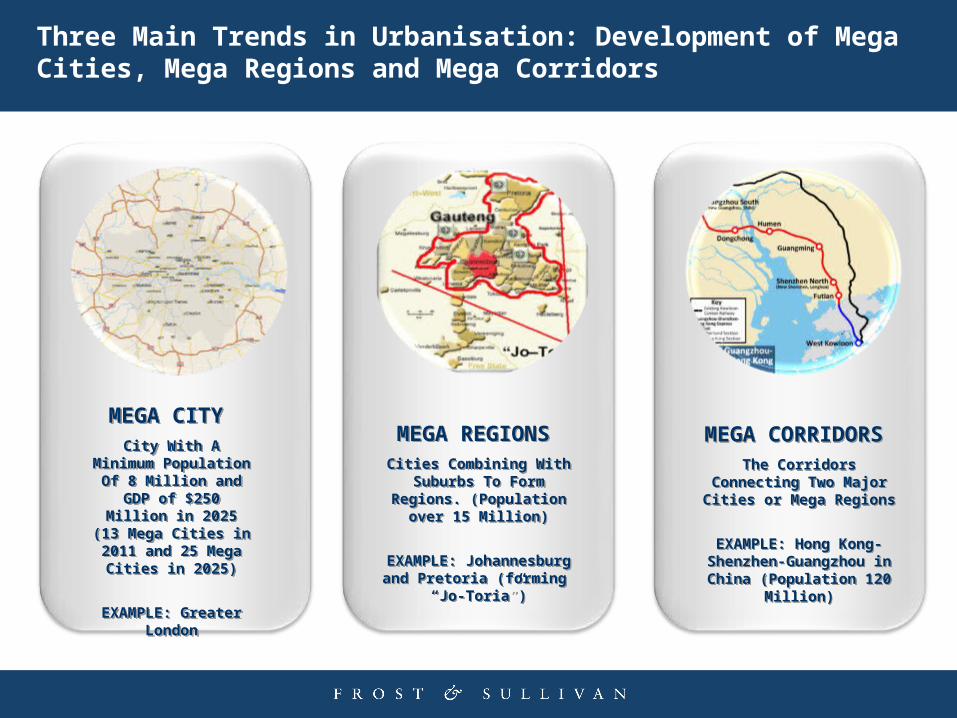

Three Main Trends in Urbanisation: Development of Mega Cities, Mega Regions and Mega Corridors

MEGA CITY

City With A Minimum Population Of 8 Million

and GDP of $250 Million in 2025 (13

Mega Cities in 2011 and 25 Mega Cities in

2025)

EXAMPLE: Greater London

MEGA CITY

City With A Minimum Population Of 8 Million

and GDP of $250 Million in 2025 (13

Mega Cities in 2011 and 25 Mega Cities in

2025)

EXAMPLE: Greater London

MEGA REGIONS

Cities Combining With Suburbs To Form Regions. (Population over 15 Million)

EXAMPLE: Johannesburg and Pretoria (forming

“Jo-Toria”)

MEGA REGIONS

Cities Combining With Suburbs To Form Regions. (Population over 15 Million)

EXAMPLE: Johannesburg and Pretoria (forming

“Jo-Toria”)

MEGA CORRIDORS

The Corridors Connecting Two Major Cities or Mega

Regions

EXAMPLE: Hong Kong-Shenzhen-Guangzhou in

China (Population 120 Million)

MEGA CORRIDORS

The Corridors Connecting Two Major Cities or Mega

Regions

EXAMPLE: Hong Kong-Shenzhen-Guangzhou in

China (Population 120 Million)

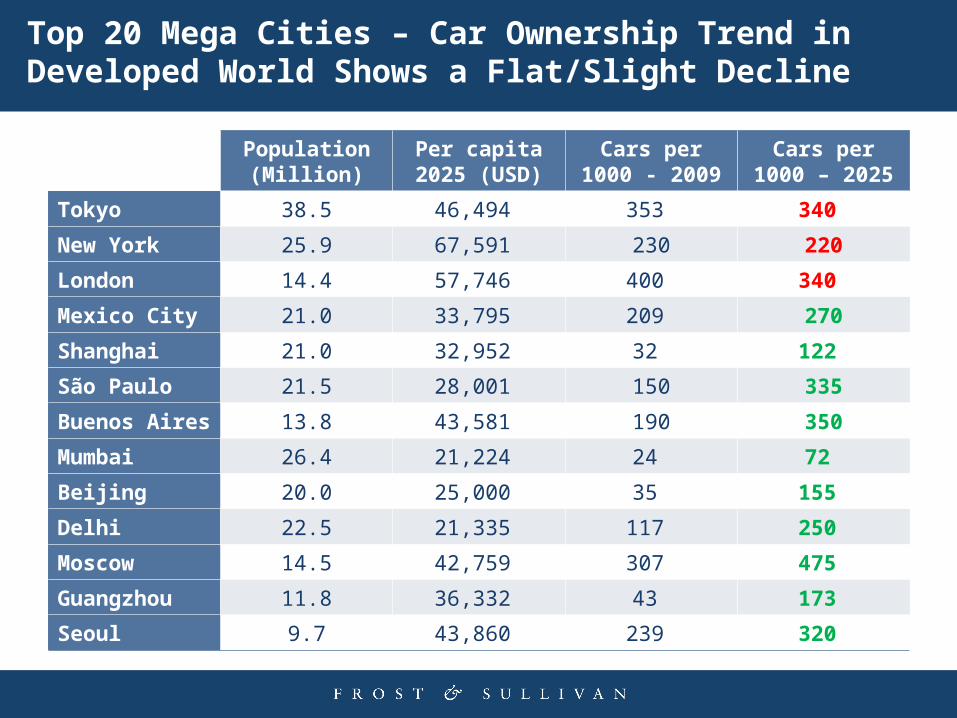

Top 20 Mega Cities – Car Ownership Trend in Developed World Shows a Flat/Slight Decline

Population (Million)

Per capita 2025 (USD)

Cars per 1000 - 2009

Cars per 1000 – 2025

Tokyo 38.5 46,494 353 340

New York 25.9 67,591 230 220

London 14.4 57,746 400 340

Mexico City 21.0 33,795 209 270

Shanghai 21.0 32,952 32 122

São Paulo 21.5 28,001 150 335

Buenos Aires 13.8 43,581 190 350

Mumbai 26.4 21,224 24 72

Beijing 20.0 25,000 35 155

Delhi 22.5 21,335 117 250

Moscow 14.5 42,759 307 475

Guangzhou 11.8 36,332 43 173

Seoul 9.7 43,860 239 320

Top 20 Mega Cities – Regional Transportation PoliciesCongestion, low emission zones and road user charging initiatives in the emerging economies will have a major impact on car mobility

Delhi Mumbai Beijing Shanghai Moscow Seoul New York London Tokyo

Bus Rapid

Transit Lanes2011 2011

Metro/Subway 2011

Congestion

ChargingPlanned Planned 2012 2012 Future Planned Future

Parking Cuts

Road use

Charging/BanYes

1 Week Day

Ban

1 week Day

Ban

1 Week Day

Ban*Future

EV/Hybrid

Incentives

Bicycle Lanes

Emission

StandardEuro 4 Euro 4 Euro 4 Euro 4

Euro 3 Euro

4 by 2012Euro 4

CAFÉ

27.5mpg.

34.1 mpg

by 2016

Euro 4 Euro

5 by 2011

25%

reduction

by 2015

Not planned Existing currently * Voluntary no road usage incentive Source: Frost & Sullivan

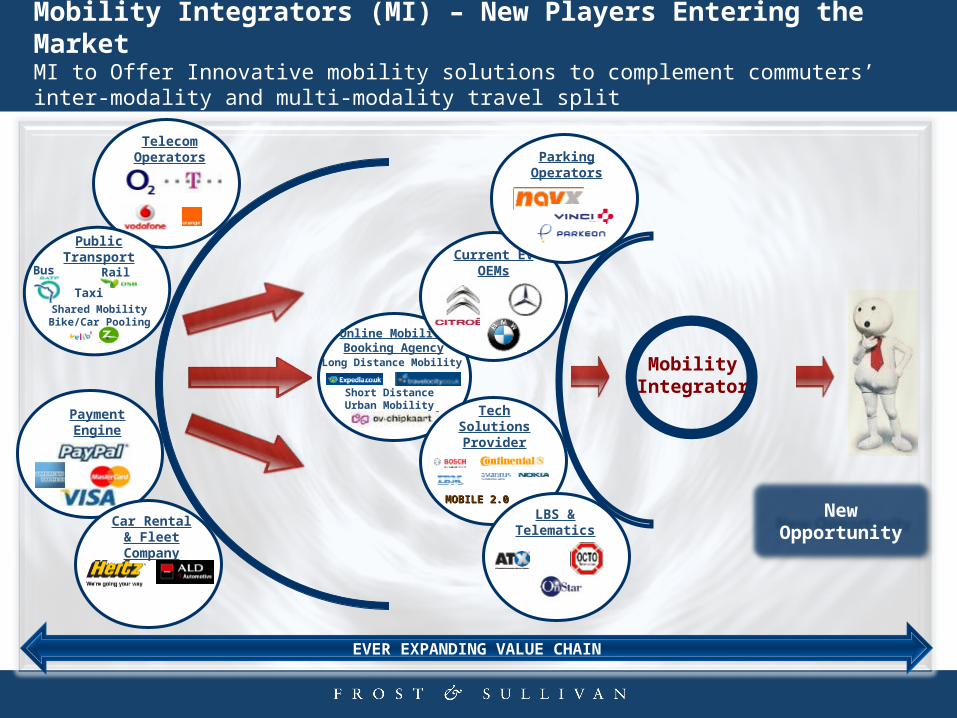

Mobility Integrators (MI) – New Players Entering the MarketMI to Offer Innovative mobility solutions to complement commuters’ inter-modality and multi-modality travel split

Payment Engine

Online Mobility Booking Agency

Long Distance Mobility

Short Distance Urban Mobility

Telecom Operators

Tech Solutions Provider

MOBILE 2.0MOBILE 2.0

PublicTransport

RailBus

Shared Mobility Bike/Car Pooling

Taxi

Mobility Integrator

Car Rental & Fleet

Company

LBS & Telematics

Current EV OEMs

Parking Operators

EVER EXPANDING VALUE CHAIN

New Opportunity

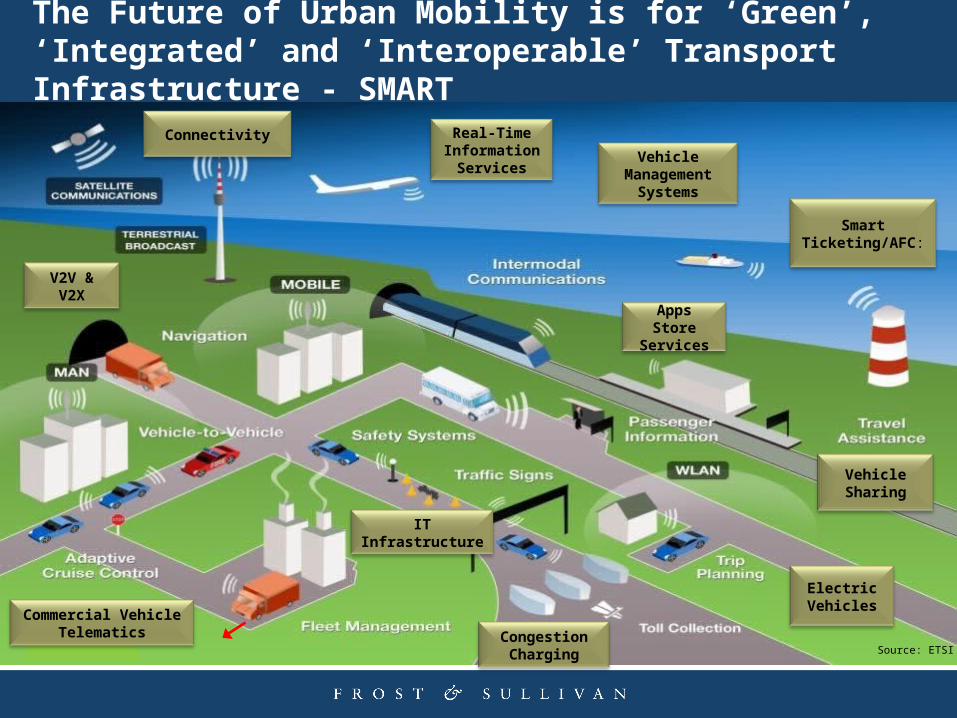

The Future of Urban Mobility is for ‘Green’, ‘Integrated’ and ‘Interoperable’ Transport Infrastructure - SMART

Vehicle Sharing

Source: ETSI Congestion Charging

Connectivity

Commercial Vehicle Telematics

V2V & V2X

Electric Vehicles

Real-Time Information

Services

Smart Ticketing/AFC:

Vehicle Management

Systems

Source: ETSI

Apps Store Services

IT Infrastructure

Car of the Future - The Driverless Car

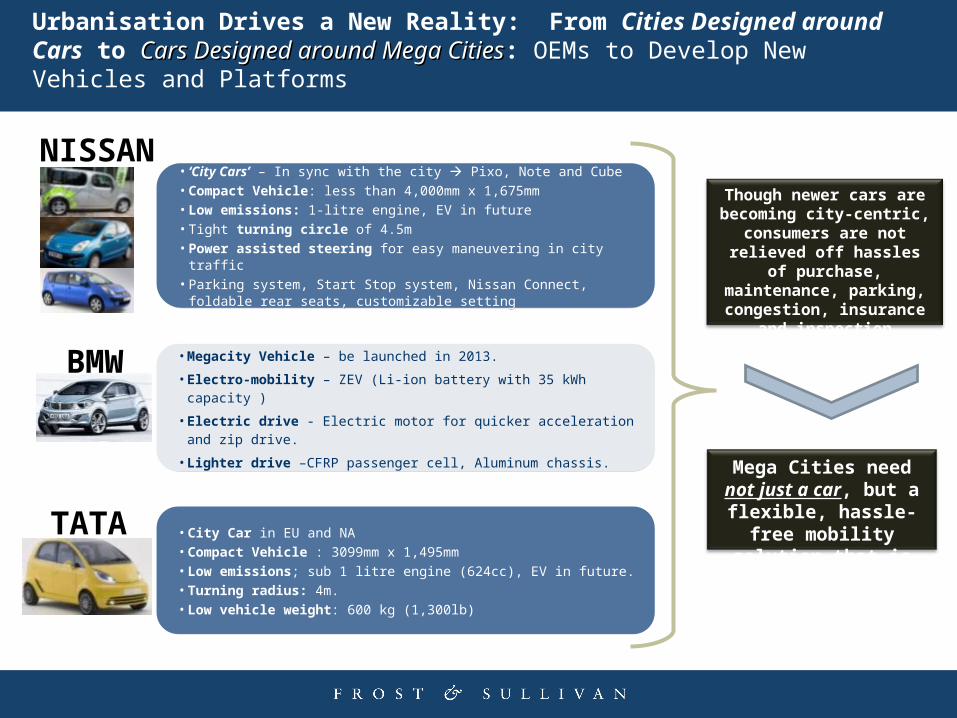

Urbanisation Drives a New Reality: From Cities Designed around Cars to Cars Cars Designed around Mega CitiesDesigned around Mega Cities: OEMs to Develop New Vehicles and Platforms

•Megacity Vehicle – be launched in 2013.

•Electro-mobility – ZEV (Li-ion battery with 35 kWh capacity )

•Electric drive - Electric motor for quicker acceleration and zip drive.

•Lighter drive –CFRP passenger cell, Aluminum chassis.

•Megacity Vehicle – be launched in 2013.

•Electro-mobility – ZEV (Li-ion battery with 35 kWh capacity )

•Electric drive - Electric motor for quicker acceleration and zip drive.

•Lighter drive –CFRP passenger cell, Aluminum chassis.

•City Car in EU and NA •Compact Vehicle : 3099mm x 1,495mm•Low emissions; sub 1 litre engine (624cc), EV in future.•Turning radius: 4m.•Low vehicle weight: 600 kg (1,300lb)

•City Car in EU and NA •Compact Vehicle : 3099mm x 1,495mm•Low emissions; sub 1 litre engine (624cc), EV in future.•Turning radius: 4m.•Low vehicle weight: 600 kg (1,300lb)

• ‘City Cars’ – In sync with the city Pixo, Note and Cube•Compact Vehicle: less than 4,000mm x 1,675mm•Low emissions: 1-litre engine, EV in future•Tight turning circle of 4.5m •Power assisted steering for easy maneuvering in city traffic•Parking system, Start Stop system, Nissan Connect, foldable rear

seats, customizable setting

• ‘City Cars’ – In sync with the city Pixo, Note and Cube•Compact Vehicle: less than 4,000mm x 1,675mm•Low emissions: 1-litre engine, EV in future•Tight turning circle of 4.5m •Power assisted steering for easy maneuvering in city traffic•Parking system, Start Stop system, Nissan Connect, foldable rear

seats, customizable setting

NISSAN

BMW

TATA

Though newer cars are becoming city-centric,

consumers are not relieved off hassles of purchase,

maintenance, parking, congestion, insurance and

inspection

Mega Cities need not just a car, but a flexible, hassle-free mobility solution that is eco-

friendly.

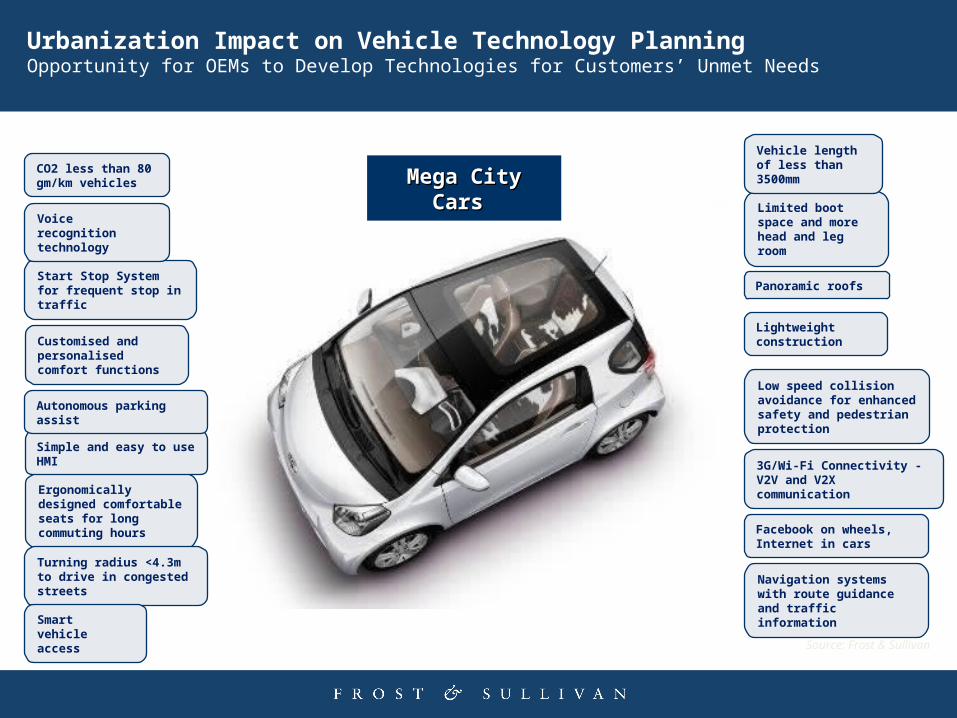

Urbanization Impact on Vehicle Technology PlanningOpportunity for OEMs to Develop Technologies for Customers’ Unmet Needs

Ergonomically designed comfortable seats for long commuting hours

Turning radius <4.3m to drive in congested streets

Start Stop System for frequent stop in traffic

Facebook on wheels, Internet in cars

3G/Wi-Fi Connectivity - V2V and V2X communication

Limited boot space and more head and leg room

CO2 less than 80 gm/km vehicles

Lightweight construction

Panoramic roofs

Navigation systems with route guidance and traffic information

Customised and personalised comfort functions

Smart vehicle access

Low speed collision avoidance for enhanced safety and pedestrian protection

Simple and easy to use HMI

Vehicle length of less than 3500mm

Source: Frost & Sullivan

Autonomous parking assist

Voice recognition technology

Mega City Cars Mega City Cars

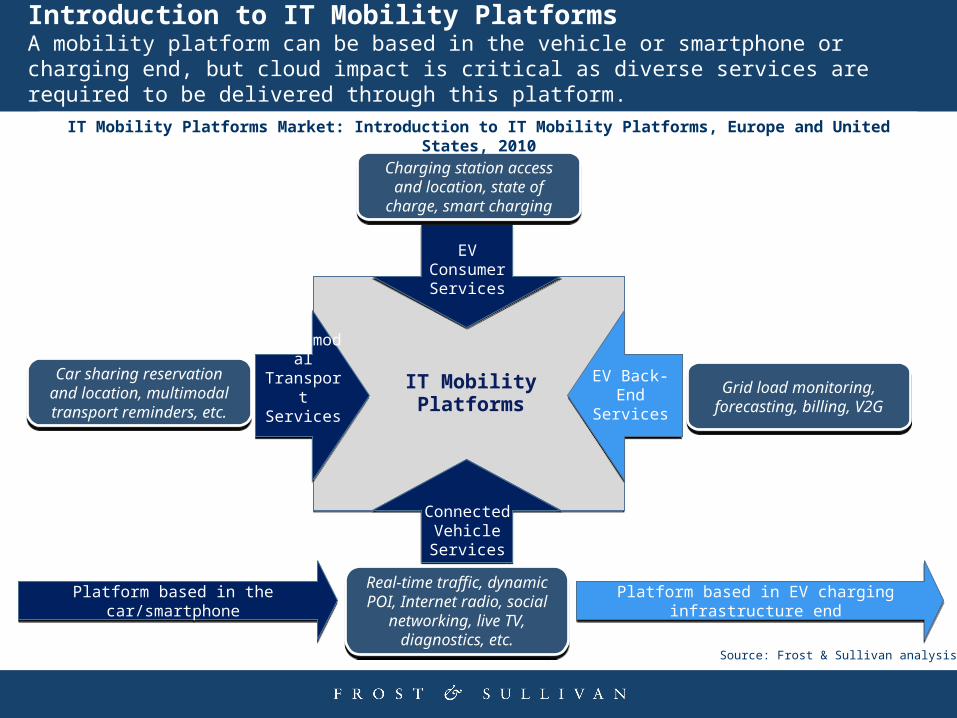

EV Consumer Services

IT Mobility Platforms

EV Back-End

Services

Multimodal Transport Services

Connected Vehicle Services

Charging station access and location, state of charge,

smart charging

Charging station access and location, state of charge,

smart charging

Platform based in the car/smartphonePlatform based in the car/smartphone Platform based in EV charging infrastructure endPlatform based in EV charging infrastructure end

Introduction to IT Mobility PlatformsA mobility platform can be based in the vehicle or smartphone or charging end, but cloud impact is critical as diverse services are required to be delivered through this platform.

Car sharing reservation and location, multimodal transport

reminders, etc.

Car sharing reservation and location, multimodal transport

reminders, etc.Grid load monitoring,

forecasting, billing, V2GGrid load monitoring,

forecasting, billing, V2G

Real-time traffic, dynamic POI, Internet radio, social

networking, live TV, diagnostics, etc.

Real-time traffic, dynamic POI, Internet radio, social

networking, live TV, diagnostics, etc.

IT Mobility Platforms Market: Introduction to IT Mobility Platforms, Europe and United States, 2010

Source: Frost & Sullivan analysis.

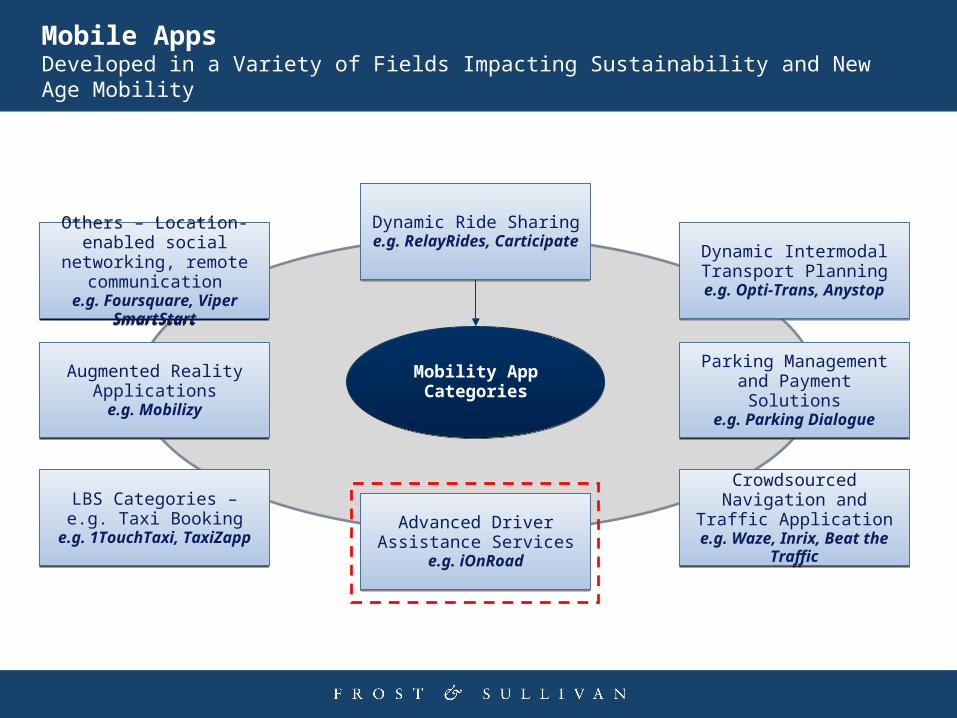

Mobility App Categories

Mobility App Categories

Advanced Driver Assistance Services

e.g. iOnRoad

Advanced Driver Assistance Services

e.g. iOnRoad

Dynamic Intermodal Transport Planning

e.g. Opti-Trans, Anystop

Dynamic Intermodal Transport Planning

e.g. Opti-Trans, Anystop

Parking Management and Payment Solutions

e.g. Parking Dialogue

Parking Management and Payment Solutions

e.g. Parking Dialogue

LBS Categories – e.g. Taxi Booking

e.g. 1TouchTaxi, TaxiZapp

LBS Categories – e.g. Taxi Booking

e.g. 1TouchTaxi, TaxiZapp

Crowdsourced Navigation and Traffic Application

e.g. Waze, Inrix, Beat the Traffic

Crowdsourced Navigation and Traffic Application

e.g. Waze, Inrix, Beat the Traffic

Dynamic Ride Sharinge.g. RelayRides, Carticipate

Dynamic Ride Sharinge.g. RelayRides, Carticipate

Augmented Reality Applicationse.g. Mobilizy

Augmented Reality Applicationse.g. Mobilizy

Others – Location-enabled social networking, remote

communicatione.g. Foursquare, Viper

SmartStart

Others – Location-enabled social networking, remote

communicatione.g. Foursquare, Viper

SmartStart

Mobile Apps Developed in a Variety of Fields Impacting Sustainability and New Age Mobility

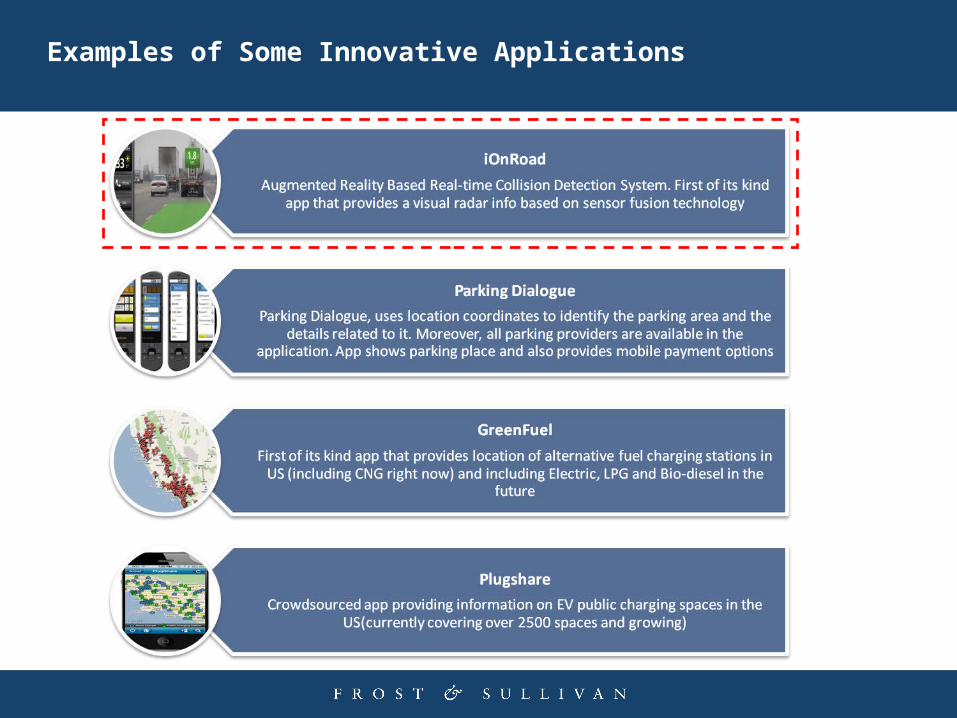

Examples of Some Innovative Applications

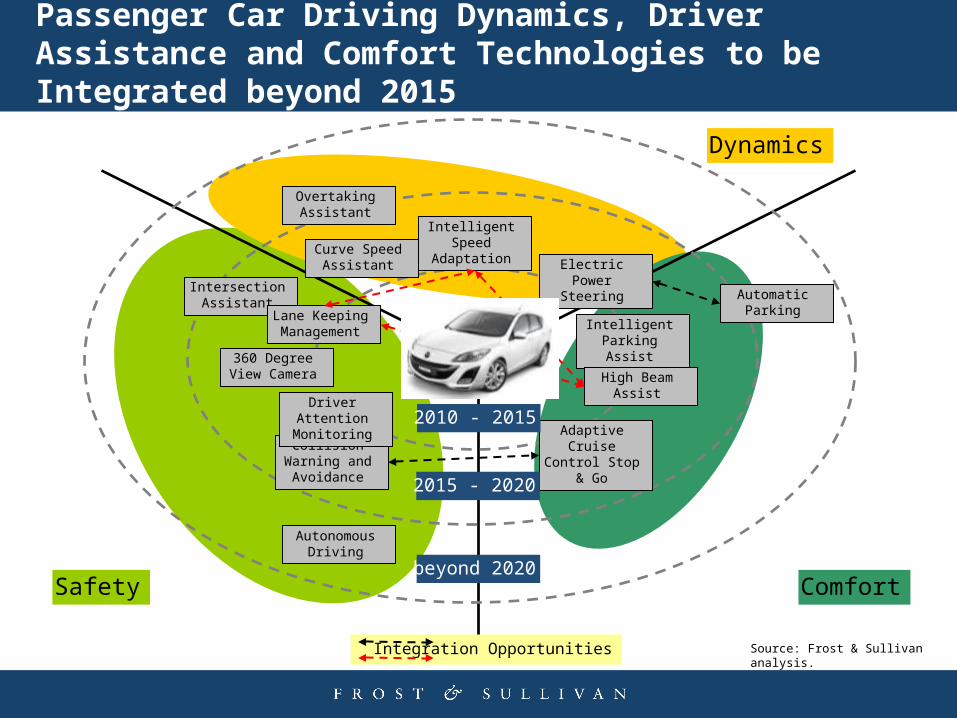

Passenger Car Driving Dynamics, Driver Assistance and Comfort Technologies to be Integrated beyond 2015

Safety Comfort

Dynamics

beyond 2020

Intersection Assistant

Collision Warning and Avoidance

Driver Attention Monitoring

Overtaking Assistant

Electric Power Steering

Intelligent Speed Adaptation

Intelligent Parking Assist

Adaptive Cruise Control Stop &

Go

High Beam Assist

2010 - 2015

Lane Keeping Management

Integration Opportunities

Automatic Parking

360 Degree View Camera

2015 - 2020

Curve Speed Assistant

Autonomous Driving

Source: Frost & Sullivan analysis.

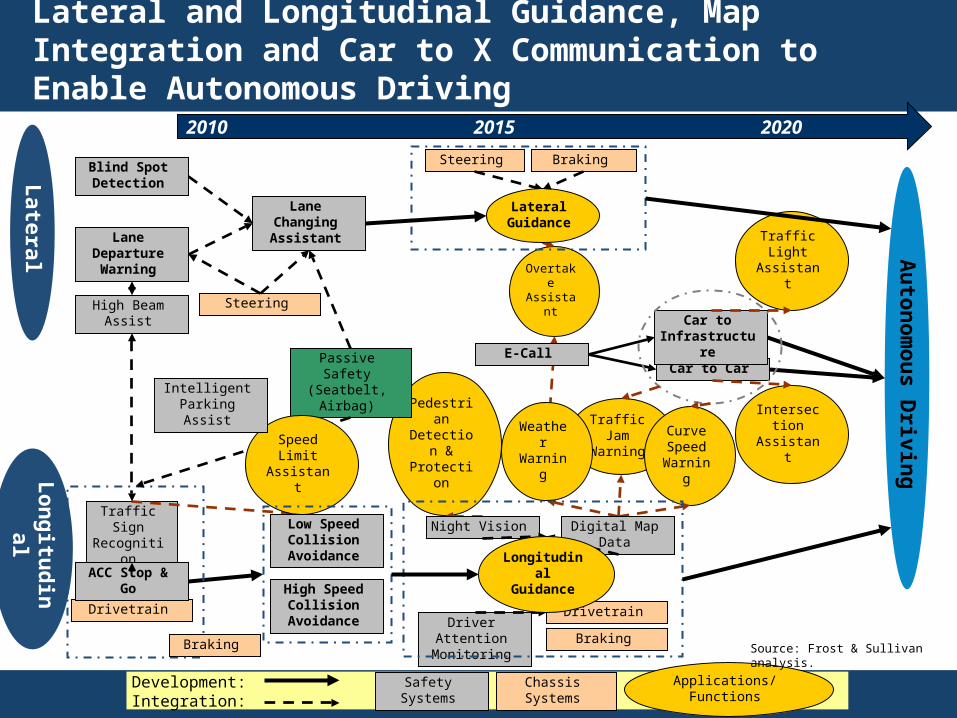

Lateral and Longitudinal Guidance, Map Integration and Car to X Communication to Enable Autonomous Driving

Driver Attention Monitoring

Blind Spot Detection

High Beam Assist

Lane Changing Assistant

Au

ton

om

ou

s Drivin

g

Lo

ng

itud

inal

Lateral

Lane Departure Warning

Pedestrian Detection & Protection

Traffic Jam

WarningCurve Speed

Warning

Traffic Sign Recognition

Overtake Assistant

Weather Warning

2010 2015 2020

E-CallCar to Car

Traffic Light

Assistant

Intersection Assistant

Car to Infrastructure

Passive Safety (Seatbelt, Airbag)

Speed Limit

Assistant

Drivetrain

Steering

ACC Stop & Go

Braking

Drivetrain

Steering

Night Vision Digital Map Data

Intelligent Parking Assist

Safety Systems Chassis Systems Applications/FunctionsDevelopment:Integration:

Braking

Low Speed Collision

Avoidance

High Speed Collision

Avoidance

Braking

Lateral Guidance

Longitudinal Guidance

Source: Frost & Sullivan analysis.

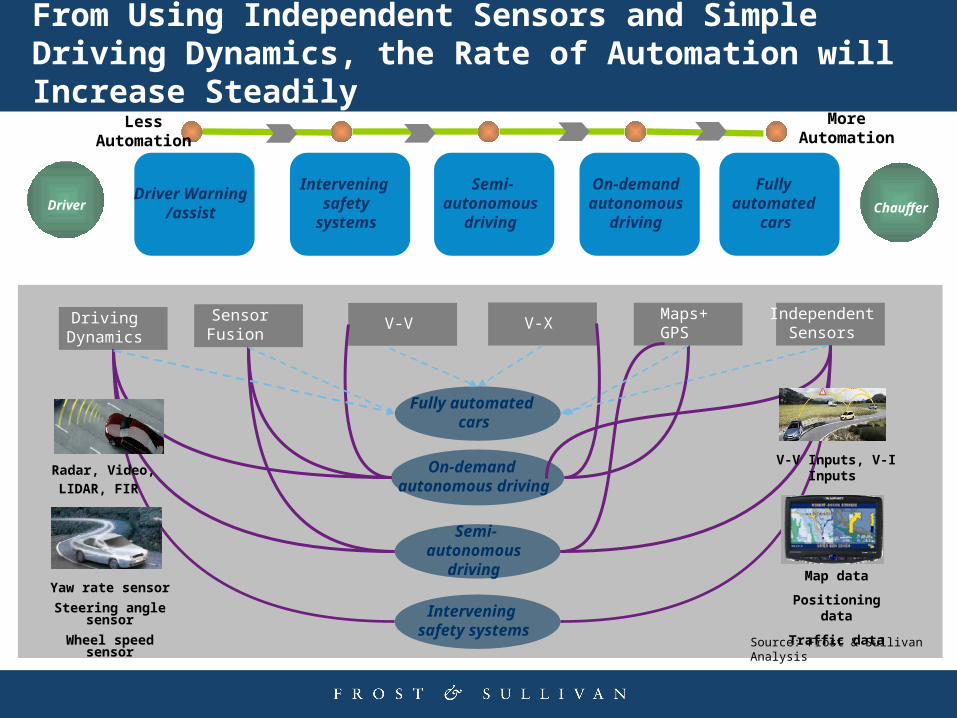

From Using Independent Sensors and Simple Driving Dynamics, the Rate of Automation will Increase Steadily

Driver Warning /assist

Intervening safety

systems

Semi-autonomous

driving

On-demand autonomous

driving

Fully automated

cars Driver Chauffer

Less Automation

More Automation

Independent Sensors

Sensor Fusion

Maps+GPS

V-VDriving Dynamics

Intervening safety systems

Semi-autonomous

driving

On-demand autonomous driving

Fully automated cars

V-X

Radar, Video,

LIDAR, FIR

Yaw rate sensor

Steering angle sensor

Wheel speed sensor

Map data

Positioning data

Traffic data

V-V Inputs, V-I Inputs

Source: Frost & Sullivan Analysis

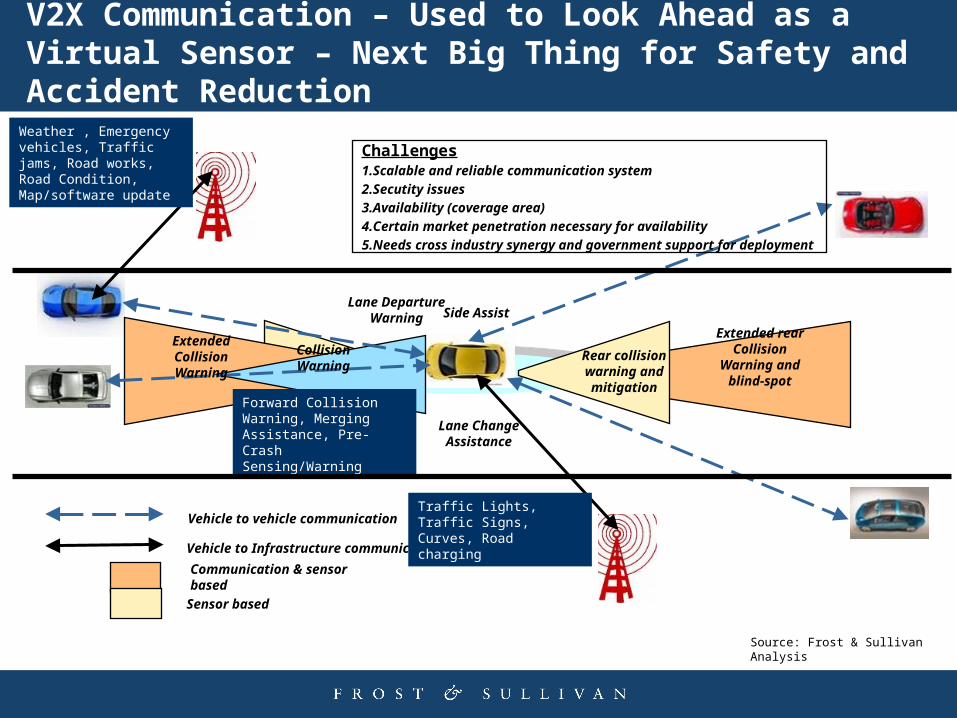

Vehicle to vehicle communication

Vehicle to Infrastructure communication

Lane Change Assistance

Side AssistLane Departure

Warning

Collision Warning

Rear collision warning and mitigation

Extended Collision Warning

Extended rear Collision

Warning and blind-spot

Communication & sensor based

Sensor based

Challenges1.Scalable and reliable communication system

2.Secutity issues

3.Availability (coverage area)

4.Certain market penetration necessary for availability

5.Needs cross industry synergy and government support for deployment

Traffic Lights, Traffic Signs, Curves, Road charging

Weather , Emergency vehicles, Traffic jams, Road works, Road Condition, Map/software update

Forward Collision Warning, Merging Assistance, Pre-Crash Sensing/Warning

V2X Communication – Used to Look Ahead as a Virtual Sensor – Next Big Thing for Safety and Accident Reduction

Source: Frost & Sullivan Analysis

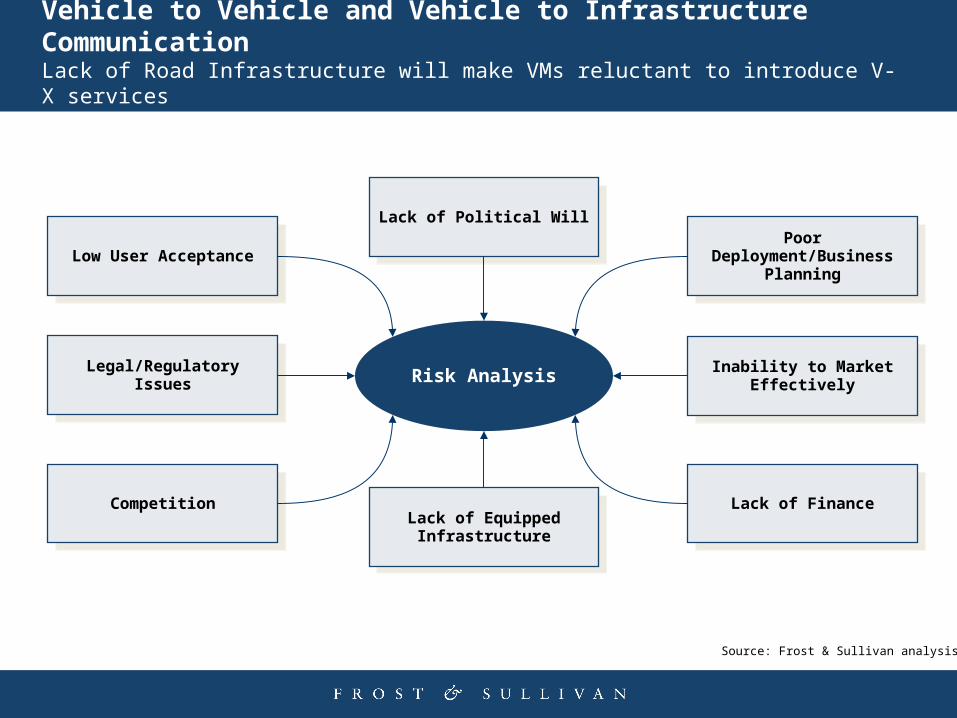

Vehicle to Vehicle and Vehicle to Infrastructure CommunicationLack of Road Infrastructure will make VMs reluctant to introduce V-X services

Risk Analysis

Lack of Equipped Infrastructure

Lack of Equipped Infrastructure

Poor Deployment/Business Planning

Poor Deployment/Business Planning

Inability to Market Effectively

Inability to Market Effectively

CompetitionCompetition Lack of FinanceLack of Finance

Lack of Political WillLack of Political Will

Legal/Regulatory IssuesLegal/Regulatory Issues

Low User AcceptanceLow User Acceptance

Source: Frost & Sullivan analysis.

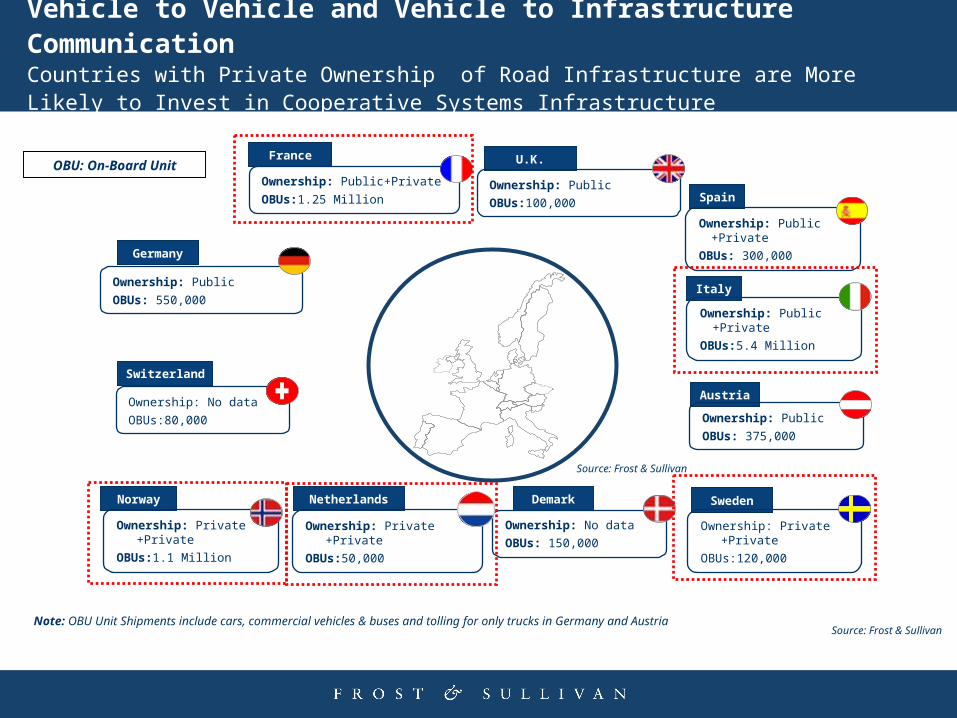

Vehicle to Vehicle and Vehicle to Infrastructure Communication Countries with Private Ownership of Road Infrastructure are More Likely to Invest in Cooperative Systems Infrastructure

Spain

U.K.

Germany

France

Ownership: Public

OBUs: 550,000

Ownership: Public+Private

OBUs:1.25 Million Ownership: Public

OBUs:100,000

Ownership: Public +Private

OBUs: 300,000

Norway

Ownership: Private +Private

OBUs:1.1 Million

Netherlands

Ownership: Private +Private

OBUs:50,000

Italy

Ownership: Public +Private

OBUs:5.4 Million

Switzerland

Austria

Ownership: Public

OBUs: 375,000

Ownership: No data

OBUs:80,000

Demark

Ownership: No data

OBUs: 150,000

Sweden

Ownership: Private +Private

OBUs:120,000

Source: Frost & Sullivan

OBU: On-Board Unit

Note: OBU Unit Shipments include cars, commercial vehicles & buses and tolling for only trucks in Germany and Austria Source: Frost & Sullivan

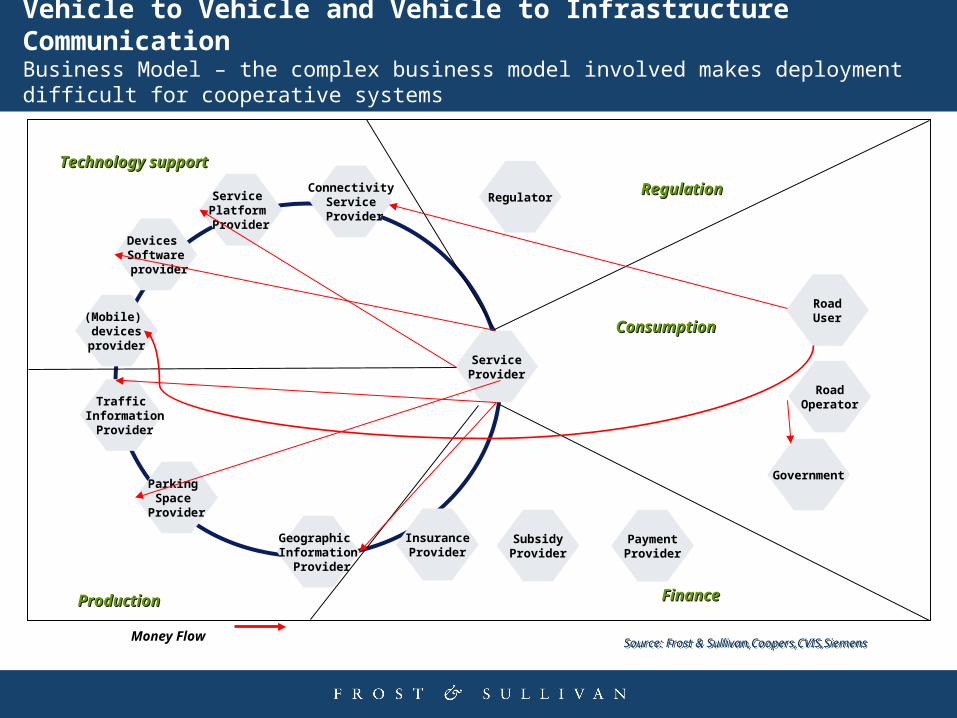

RoadUser

Regulator

ServiceProvider

Geographic Information

Provider

Parking Space

Provider

Traffic Information

Provider

(Mobile) devicesprovider

Devices Software provider

Service Platform Provider

RoadOperator

ConnectivityService

Provider

Government

PaymentProvider

SubsidyProvider

InsuranceProvider

RegulationRegulation

Consumption Consumption

Finance Finance

Technology support Technology support

Production Production

Vehicle to Vehicle and Vehicle to Infrastructure Communication Business Model – the complex business model involved makes deployment difficult for cooperative systems

Money Flow Source: Frost & Sullivan,Coopers,CVIS,Siemens Source: Frost & Sullivan,Coopers,CVIS,Siemens

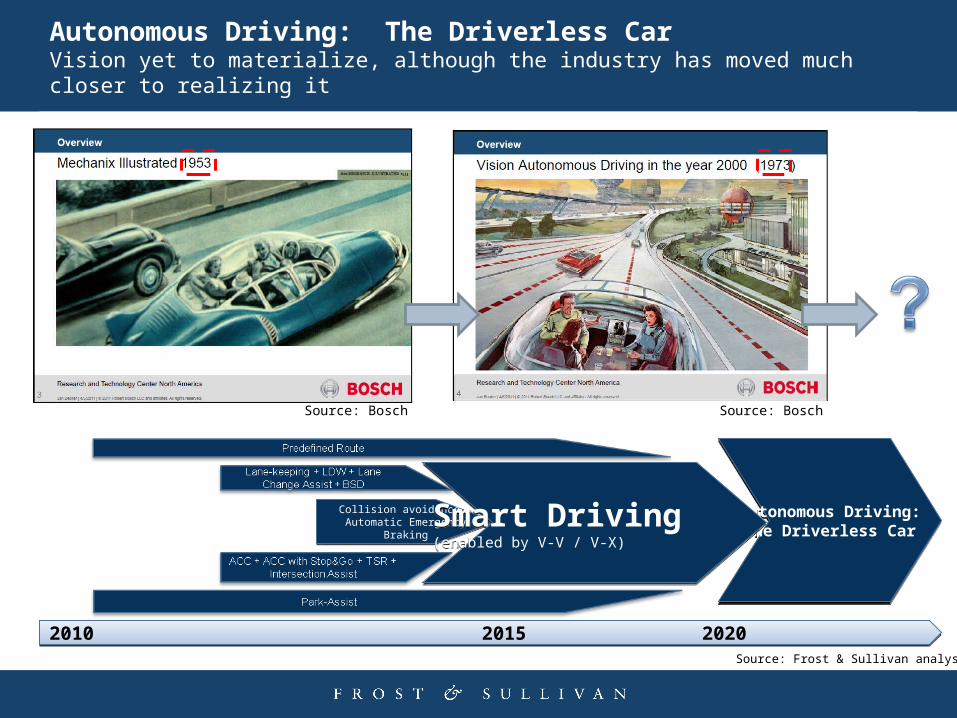

Autonomous Driving: The Driverless CarVision yet to materialize, although the industry has moved much closer to realizing it

Source: BoschSource: Bosch

Collision avoidance + Automatic Emergency Braking

Collision avoidance + Automatic Emergency Braking

Autonomous Driving: The Driverless Car

Autonomous Driving: The Driverless CarSmart Driving

(enabled by V-V / V-X)

Smart Driving(enabled by V-V / V-X)

2010 2015 2020 20252010 2015 2020 2025Source: Frost & Sullivan analysis.

Frost & Sullivan’s Global Urban Mobility Research

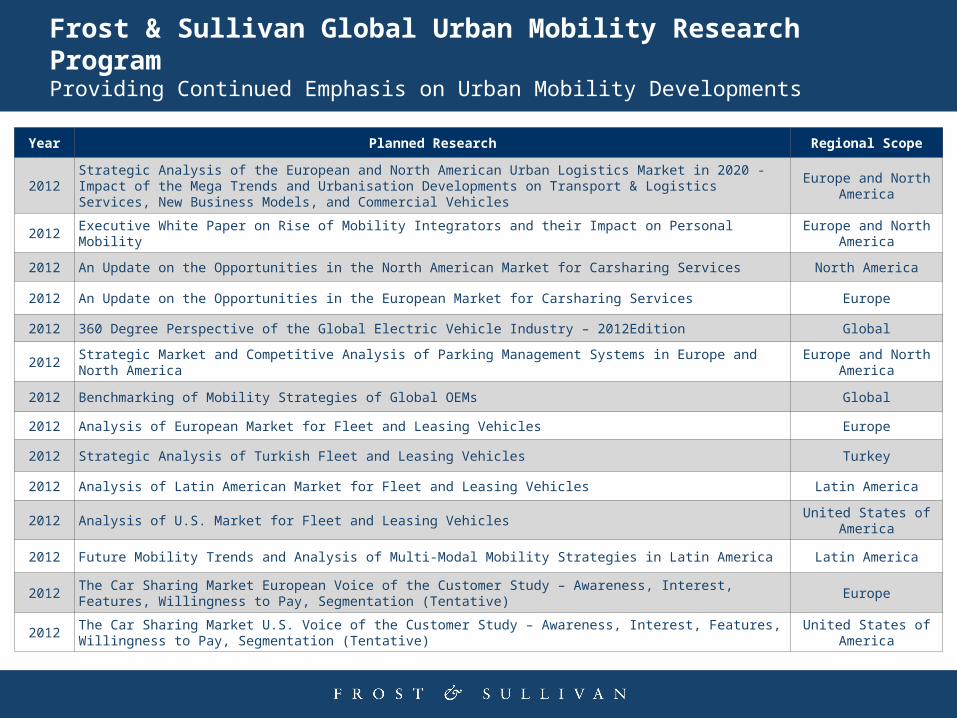

Frost & Sullivan Global Urban Mobility Research ProgramProviding Continued Emphasis on Urban Mobility Developments

Year Planned Research Regional Scope

2012Strategic Analysis of the European and North American Urban Logistics Market in 2020 - Impact of the Mega Trends and Urbanisation Developments on Transport & Logistics Services, New Business Models, and Commercial Vehicles

Europe and North America

2012 Executive White Paper on Rise of Mobility Integrators and their Impact on Personal MobilityEurope and North

America

2012 An Update on the Opportunities in the North American Market for Carsharing Services North America

2012 An Update on the Opportunities in the European Market for Carsharing Services Europe

2012 360 Degree Perspective of the Global Electric Vehicle Industry – 2012Edition Global

2012 Strategic Market and Competitive Analysis of Parking Management Systems in Europe and North AmericaEurope and North

America

2012 Benchmarking of Mobility Strategies of Global OEMs Global

2012 Analysis of European Market for Fleet and Leasing Vehicles Europe

2012 Strategic Analysis of Turkish Fleet and Leasing Vehicles Turkey

2012 Analysis of Latin American Market for Fleet and Leasing Vehicles Latin America

2012 Analysis of U.S. Market for Fleet and Leasing Vehicles United States of

America

2012 Future Mobility Trends and Analysis of Multi-Modal Mobility Strategies in Latin America Latin America

2012The Car Sharing Market European Voice of the Customer Study – Awareness, Interest, Features, Willingness to Pay, Segmentation (Tentative)

Europe

2012The Car Sharing Market U.S. Voice of the Customer Study – Awareness, Interest, Features, Willingness to Pay, Segmentation (Tentative)

United States of America

Frost & Sullivan Global Urban Mobility Research ProgramExisting Research

Study Code

Planned Research Regional Scope

NA5E-18Strategic Analysis of Global Bus Rapid Transit Systems Market - Rapid Urbanization Stoking Demand for Cost-Effective and Energy Efficient Mass Transit Solutions

Global

NADC-18 Analysis of Chinese Electric Buses Market Chinese

P5F7-18 Strategic Analysis of Car Sharing Market in APAC Asia Pacific

P5F5-18 Mobility Trends in Select Indian Cities India

P5C4-18 Strategic Analysis of Micro cars market in Japan Japan

M79C-18Beliefs and Attitudes Towards Environment and Personal Mobility Needs and Vehicle Preferences of EU Generation “Y” - 2010 Voice of Consumer

Europe

N80C-18Beliefs and Attitudes Towards Environment and Personal Mobility Needs and Vehicle Preferences of U.S. Generation “Y” - 2010 Voice of Consumer

North America

M651-18Strategic Analysis of IT Mobility Platforms for European and North American Automotive Market - Billing and Smart Charging are Two Key Opportunity Areas in the EV Infrastructure Segment

Europe and North America

M7BB-18Strategic Analysis of Medium-Heavy Hybrid and Electric Commercial Vehicle Markets in China and India India, China

M783-18Strategic Analysis of Hybrid and Electric Medium and Heavy Commercial Vehicles in EMEA Region EMEA

N9FF-18Strategic Analysis of the North & South American Hybrid and Electric Medium-Heavy Truck and Bus Markets

North America, South America

M785-18Connectivity, App Stores and Cloud-based Delivery Platforms Future of Connected Infotainment and Telematics Market Global

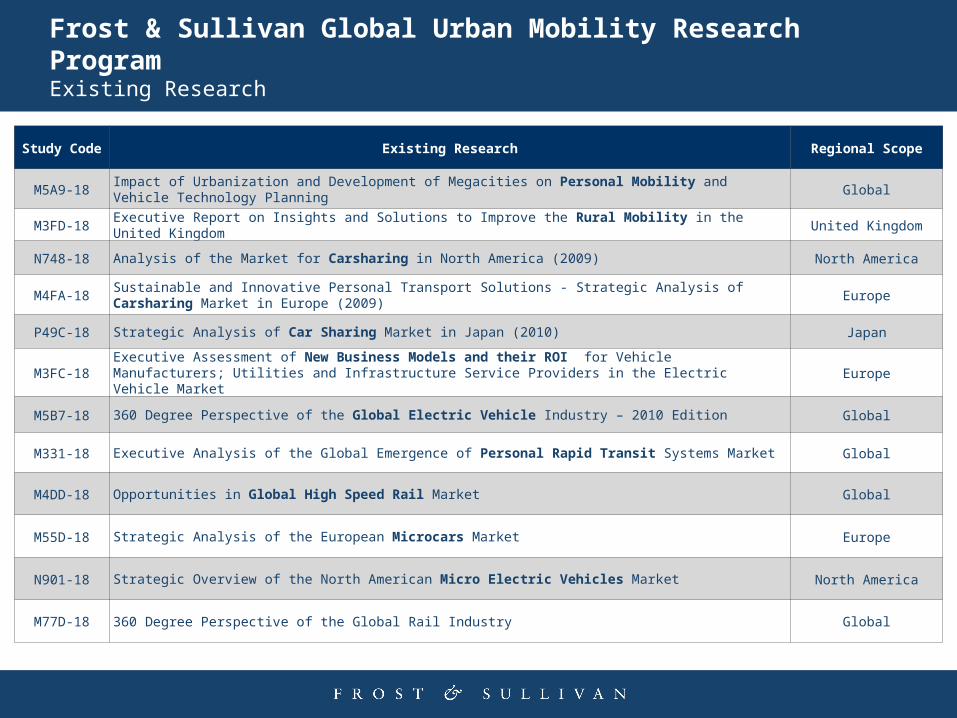

Frost & Sullivan Global Urban Mobility Research Program Existing Research

Study Code Existing Research Regional Scope

M5A9-18Impact of Urbanization and Development of Megacities on Personal Mobility and Vehicle Technology Planning Global

M3FD-18 Executive Report on Insights and Solutions to Improve the Rural Mobility in the United Kingdom United Kingdom

N748-18 Analysis of the Market for Carsharing in North America (2009) North America

M4FA-18Sustainable and Innovative Personal Transport Solutions - Strategic Analysis of Carsharing Market in Europe (2009) Europe

P49C-18 Strategic Analysis of Car Sharing Market in Japan (2010) Japan

M3FC-18Executive Assessment of New Business Models and their ROI for Vehicle Manufacturers; Utilities and Infrastructure Service Providers in the Electric Vehicle Market Europe

M5B7-18 360 Degree Perspective of the Global Electric Vehicle Industry – 2010 Edition Global

M331-18 Executive Analysis of the Global Emergence of Personal Rapid Transit Systems Market Global

M4DD-18 Opportunities in Global High Speed Rail Market Global

M55D-18 Strategic Analysis of the European Microcars Market Europe

N901-18 Strategic Overview of the North American Micro Electric Vehicles Market North America

M77D-18 360 Degree Perspective of the Global Rail Industry Global