Download - Future of Corporate Mobility

1©2020 Deloitte Belgium Mobility@Deloitte

Future of Corporate Mobility

Future of Mobility Corporate Mobility

Discover our mobility webpages via the followinglinks:

2© 2021 Deloitte

Greenification of mobility taxationImpact for employers and employees

6 October 2021

3© 2021 Deloitte

Your hosts for today

Jolien VanheckeSenior Manager

Global Business Tax

+32 9 393 74 55

Timothy BruneelPartner

Global Employer Services

+32 9 393 74 62

Jan VrijsenDirector

Indirect Tax

+32 9 393 75 51

4© 2021 Deloitte

Content

2 What will be the impact for your employees?

3 Which incentives are made available to accelerate the transition?

4 Is the evolution to a broader mobility plan also supported?

1 What will be the impact on the cost of your fleet?Private and public sector

The long anticipated bill on the “Greenification” of mobility taxation in Belgium

5© 2021 Deloitte

What is the impact on the cost of my fleet?

1

6© 2021 Deloitte

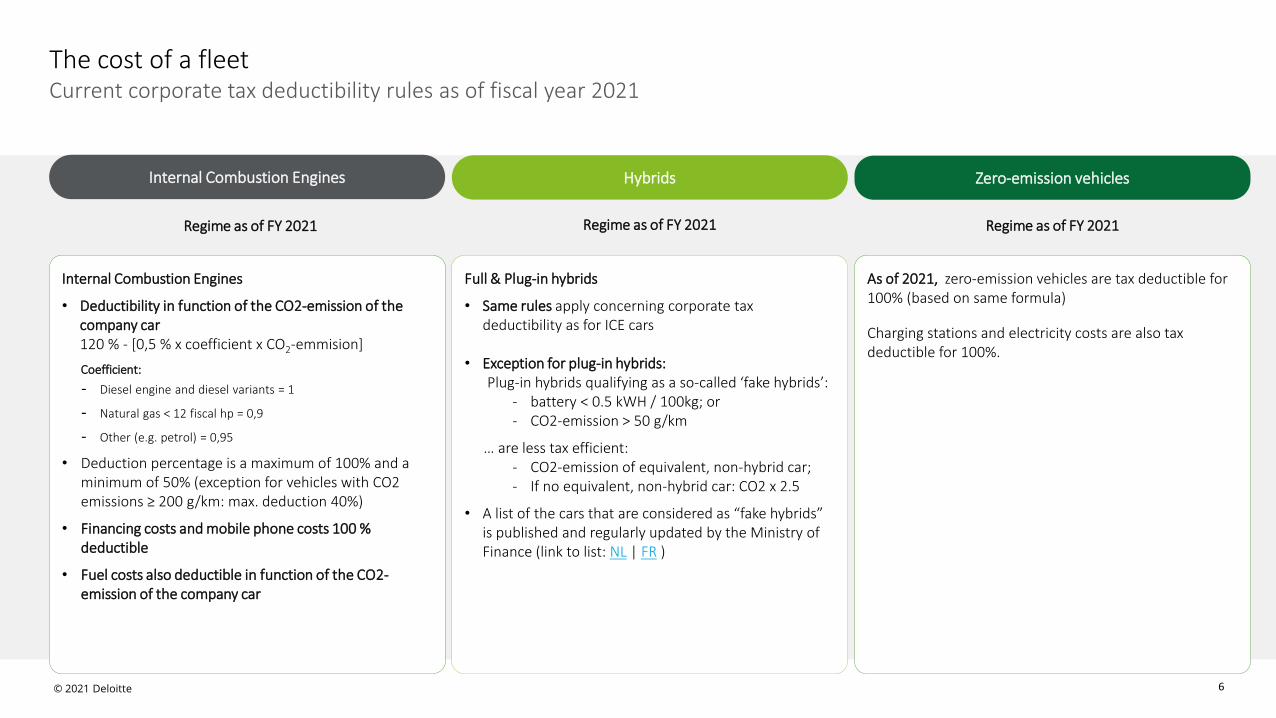

Current corporate tax deductibility rules as of fiscal year 2021The cost of a fleet

Internal Combustion Engines

• Deductibility in function of the CO2-emission of the company car120 % - [0,5 % x coefficient x CO2-emmision]

Coefficient:

- Diesel engine and diesel variants = 1

- Natural gas < 12 fiscal hp = 0,9

- Other (e.g. petrol) = 0,95

• Deduction percentage is a maximum of 100% and a minimum of 50% (exception for vehicles with CO2 emissions ≥ 200 g/km: max. deduction 40%)

• Financing costs and mobile phone costs 100 % deductible

• Fuel costs also deductible in function of the CO2-emission of the company car

Internal Combustion Engines Zero-emission vehicles

As of 2021, zero-emission vehicles are tax deductible for 100% (based on same formula)

Charging stations and electricity costs are also tax deductible for 100%.

Full & Plug-in hybrids

• Same rules apply concerning corporate tax deductibility as for ICE cars

• Exception for plug-in hybrids:Plug-in hybrids qualifying as a so-called ‘fake hybrids’:

- battery < 0.5 kWH / 100kg; or- CO2-emission > 50 g/km

… are less tax efficient:- CO2-emission of equivalent, non-hybrid car;- If no equivalent, non-hybrid car: CO2 x 2.5

• A list of the cars that are considered as “fake hybrids” is published and regularly updated by the Ministry of Finance (link to list: NL | FR )

Hybrids

Regime as of FY 2021 Regime as of FY 2021 Regime as of FY 2021

7© 2021 Deloitte

The cost of a fleetDifferent TCO methods in the market

Car costs

• Lease price / purchase price

• Insurance

• Maintenance

• Tires

• Damage

• ...

Fuel costs

• Based on an average ~ lease, or

• Based on historical data, or

• Reference consumption of the vehicle model

• Taxation regime for electricity is more diffuse/complex

Belgian Corporate tax(or legal entities tax)

Disallowed expenses will be determined as follows:

• Disallowed expenses on car and fuel costs, determined on the CO2-emission of the car

• If used for private purposes, an additional disallowed expense of 17%/40%, depending on the provision of a fuel card

Belgian CO2-tax

Actual CO2-tax should be calculated, taking into account:

• CO2-tax formula

• CO2-emissions according to WLTP

Belgian VAT

• VAT deduction on car expenses for zero emission vehicles is the same as for non-zero emission vehicles (VAT recovery limitation of 35% - 50%).

• Specific rules can apply for charging infrastructure

Update Attention pointUpdate

8© 2021 Deloitte

The cost of a fleetDifferent TCO methods in the market

Car costs • Corporate income tax deductibility• Disallowed expenses on BIK• Often does not take into account the offsetting

of the BIK to the disallowed expenses

• Disallowed expenses on car costs• Disallowed expenses on BIK• Does take into account the offsetting of the BIK

to the disallowed expenses

Fuel costs • Corporate income tax deductibility • Disallowed expenses on fuel costs

Example – comparison net employer cost vs. gross employer cost (subject to corporate tax)

The calculation methods use a different method to reflect the fiscal impact on costs, but both can be used to calculate and monitor the TCO of the current and future vehicle fleet.

Net employer cost Gross employer cost

in line with legislative framework on mobility budget

Possible assumptions on fuel consumption:

- Lump-sum estimate on fuel cost

- Mark-up on standard consumption, # kilometers on lease contract & assumption on fuel cost

- Average actual consumption / 100km, average # km’s driven, average fuel costs

- …

9© 2021 Deloitte

The cost of a fleetDifferent TCO methods in the market – comparative calculation

Example – comparison gross employer cost vs. net employer cost (subject to corporate tax) calculated by a lease company

We have worked out a comparative TCO calculation for a company car (excl. fuel cost) as an illustration.The table reflects the different methodology, resulting in either the net or the gross cost.

Company car details

Catalogue value: € 30.000 (incl. options and VAT)

CO2-value: 91 g/km (WLTP)

Fuel type: diesel

Lease price/month (excl. VAT) : € 455

Finance cost/month (excl. VAT): € 45,50

CO2-tax/year: € 330,50

Benefit in kind (BIK)/year: € 1.594 (IY 2021)

Corporate income tax deductibility: 74,50%

Gross employer cost Net employer cost

Lease price (excl. VAT) € 4.909,09 € 4.909,09

Finance cost (excl. VAT) € 545,45 € 545,45

Non-deductible VAT on lease price and finance cost (i.e. 65% - method 3) € 744,55 € 744,55

CO2-tax € 330,50 € 330,50

Corporate income taxes on disallowed expenses car costs (i.e. € 1.035,13 X 25%)

€ 1.035,13 = (lease price excl. VAT (€ 4.909,09) + non-deductible VAT on lease price (€ 744,55) -BIK (€ 1.594)) * 25,5% (non-deductibility rate)

€ 258,78

Corporate income taxes on disallowed expenses BIK (i.e. BIK X 40% X 25%) € 159,43 € 159,43

Gross TCO € 6.947,81

Less corporate income taxes on deductible car costs (i.e. € 5.247,35 X 25%) - € 1.311,84

Net TCO€ 5.635,97

10© 2021 Deloitte

Non zero-emission vehicles include:

- Passenger cars (incl. ‘fake’ light trucks), cars for double use and minivans

- Ordered = purchased, leased or rented

Evolution of corporate tax deductibility for non zero-emission vehicles

The cost of a fleet

Ordered until 1.07.2023, the current tax deductibility rules will continue to apply

Ordered as of 1.01.2026, the car costs will no longer be tax deductible

2021

2023

2026

Ordered between 1.07.2023 – 31.12.2025, adjustment tax deductibility limits:

IY 2023-24 Min 50% Max. 100%

IY 2025 - Max. 75%

IY 2026 - Max. 50%

IY 2027 - Max. 25%

IY 2028 - 0%

2021

2023

No impact on the calculation of the CO2-tax for company cars also used for commuting and/or private purposes

Increase of the CO2-tax for all non-ZEV ordered as of 1.07.2023:

As of 1.07.2023, multiplied by 2.25min. € 20.83 per month (not indexed)

As of 1.01.2025, multiplied by 2.75min. € 23.41 per month (not indexed)

As of 1.01.2026, multiplied by 4min. € 25.99 per month (not indexed)

Exception – between 01.01.2023 – 31.12.2026, the fossil fuel costs would be tax deductible for max. 50% for PHEVS ordered as of 01.01.2023

2023

The current tax deductibility rules will continue to apply (i.e. same limitation as the company car)2021

2026For cars ordered as of 1.01.2026, fuel costs will no longer be tax deductible

Impact CO2-tax Impact tax deductibility Impact fuel costs

As of 1.01.2027, multiplied by 5.5min. € 28.57 per month (not indexed)

As of 1.01.2028, min. multiplied by 5.5min. € 31.15 per month (not indexed)2028

Fossil fuel costs will remain to follow the tax deductibility percentage of the company car

Further increasing compliance burden!

11© 2021 Deloitte

Example on the evolution of the cost of non zero-emission vehicles

The cost of a fleet

Vergroening van de mobiliteit & Future of mobility | Webinar

Car Volkswagen Golf Skoda Superb Hybrid

Catalogue value € 30.000 € 38.000

Monthly leaseprice (incl. VAT)Part related to financing

€ 550€ 55

€ 560€ 56

Engine type Diesel Hybrid – Petrol

CO2-emission (WLTP) 91 35

Current % corporate tax deductibility 74,50% 100%

Current TCO € 6.947,81 € 6.779,30

TCO per year if ordered as of 01.07.2023 Delta current TCO Delta current TCO

In 2023 (max 100% tax deductible) € 7.360,94 + 6% € 7.192,43 + 6%

In 2025 (max 75% tax deductible) € 7.526,20 + 8% € 7.631,84 +13%

In 2026 (max 50% tax deductible) € 8.187,96 + 18% € 8.319,12 + 23%

In 2027 (max 25% tax deductible) € 8.937,43 + 29% € 9.089,03 + 34%

In 2028 (0% tax deductible) € 9.191,14 + 32% € 9.363,18 + 38%

Annual TCO if ordered in 2026 € 8.695,38 + 25% € 8.867,42 + 31%

Annual TCO if ordered in 2027 € 9.191,14 + 32% € 9.363,18 + 38%

To reflect the impact from the changing (social) tax regime, we keep all other variables stable

12© 2021 Deloitte

Zero-emission vehicles include:

- Passenger cars (incl. ‘fake’ light trucks), cars for double use and minivans

- Ordered = purchased, leased or rented

Evolution of corporate tax deductibility for zero-emission vehicles

The cost of a fleet

Ordered until 31.12.2026, the current tax deductibility rules will continue to apply (100% tax deductible)

2021

2027 Ordered as of 1.01.2027, adjustment tax deductibility limits:

Ordered in IY 2027 95%

Ordered in IY 2028 90%

Ordered in IY 2029 82.5%

Ordered in IY 2030 75%

Ordered in IY 2031 67.5%

2021

2023

No impact on the calculation of the CO2-tax for company cars also used for commuting and/or private purposes

Increase of min CO2-tax for all vehicles ordered as of 1.07.2023 (not indexed):

As of 1.07.2023, min. € 20.83 per month

As of 1.01.2025, min. € 23.41 per month

2028

As of 1.01.2026, min. € 25.99 per month

The current tax deductibility rules will continue to apply (i.e. same limitations as the company car)2021

2027

2030

As of 1.01.2027, the costs related to charging stations will remain 100% tax deductible

As of 1.01.2030, the costs related to charging stations will be tax deductible for 75%.

As of 1.01.2027, min. € 28.57 per month

As of 1.01.2028, min. € 31.15 per month

Impact CO2-tax Impact tax deductibility Impact charging

The multiplicator as mentioned for non-zero emission cars, will

not apply for zero-emission cars.

Further increasing compliance burden!

13© 2021 Deloitte

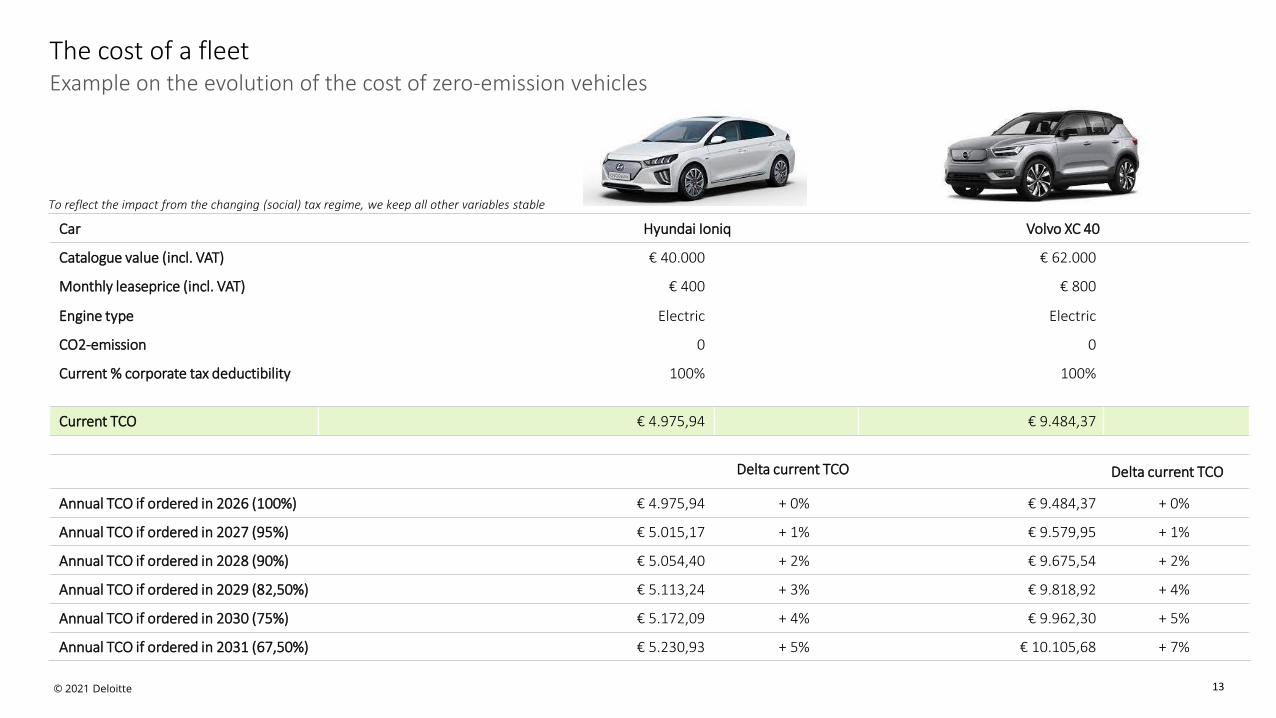

Example on the evolution of the cost of zero-emission vehicles

The cost of a fleet

Car Hyundai Ioniq Volvo XC 40

Catalogue value (incl. VAT) € 40.000 € 62.000

Monthly leaseprice (incl. VAT) € 400 € 800

Engine type Electric Electric

CO2-emission 0 0

Current % corporate tax deductibility 100% 100%

Current TCO € 4.975,94 € 9.484,37

Delta current TCO Delta current TCO

Annual TCO if ordered in 2026 (100%) € 4.975,94 + 0% € 9.484,37 + 0%

Annual TCO if ordered in 2027 (95%) € 5.015,17 + 1% € 9.579,95 + 1%

Annual TCO if ordered in 2028 (90%) € 5.054,40 + 2% € 9.675,54 + 2%

Annual TCO if ordered in 2029 (82,50%) € 5.113,24 + 3% € 9.818,92 + 4%

Annual TCO if ordered in 2030 (75%) € 5.172,09 + 4% € 9.962,30 + 5%

Annual TCO if ordered in 2031 (67,50%) € 5.230,93 + 5% € 10.105,68 + 7%

To reflect the impact from the changing (social) tax regime, we keep all other variables stable

14© 2021 Deloitte

Evolution of taxation under legal entities tax of (non) zero-emission vehicles

The cost of a fleet

Only for entities subject to legal entities tax of category 2 and 3 (cf. Art. 220, 2° and 3° ITC)

• Non zero-emission vehicles = Internal combustion engine & hybrids (full & plug-in)

• Zero emission vehicles = full electric cars

Pm.: entities of category 1 (cf. Art. 220, 1° ITC) are not impacted (vehicles remain untaxed)

For cars ordered as from 1.01.2026, the ‘non-deductible’ cost of the use of the car (incl. fuel costs) is added to the taxable base

Future regimeNon zero-emission vehicles

Current regimeAll vehicles

Future regimeZero-emission vehicles

impact as of income year 2026 impact as of income year 2027until income year 2025

For company cars which can be used for private purposes, an amount is added to the taxable base equal to:• 17% if fuel costs are not borne by the employer• 40% if fuel costs are borne by the employer

For company cars which can be used for private purposes, an amount is added to the taxable base equal to:• 17% if fuel costs are not borne by the employer• 40% if fuel costs are borne by the employer

For company cars which can be used for private purposes, an amount is added to the taxable base equal to:• 17% if fuel costs are not borne by the employer• 40% if fuel costs are borne by the employer

For cars ordered as from 1.01.2027, a percentage of the cost of use of the car (incl. electricity costs & charging stations) is added to the taxable base:

in 2027: 5%

in 2028: 10%

in 2029: 17.5%

in 2030: 25%

as of 2031: 32.5%

Category 2 (cf. Art. 180 ITC) : o.a. ‘care associations’, STIB/MIVB, Infrabel, Le Fonds de participation/Participatiefonds, …Category 3 : ‘not for profit’ entities (including ‘externalized’ public entities) and entities active in a ‘privileged activity’ (o.a. education, lobbying, …)

New administrative process to be considered to identify these costs and include them in the tax return!

15© 2021 Deloitte

Example on the evolution of the cost of non zero-emission vehicles

The cost of a fleet

Vergroening van de mobiliteit & Future of mobility | Webinar

Car Volkswagen Golf Skoda SuperbHybrid

Catalogue value € 30.000 € 38.000

Monthly leaseprice (incl. VAT) € 550 € 560

Engine type Diesel Hybrid – Petrol

CO2-emission (WLTP) 91 35

Benefit in kind € 1.594 € 1.370

Current TCO € 6.689,02 € 6.779,31

Delta current TCO

Delta current TCO

Annual TCO if ordered in 2026 € 8.238,80 + 23% € 8.357,26 + 23%

To reflect the impact from the changing (social) tax regime, we keep all other variables stable

16© 2021 Deloitte

Example on the evolution of the cost of zero-emission vehicles

The cost of a fleet

Car Hyundai Ioniq Volvo XC 40

Catalogue value (incl. VAT) € 40.000 € 62.000

Monthly leaseprice (incl. VAT) € 400 € 800

Engine type Electric Electric

CO2-emission 0 0

Current % corporate tax deductibility 100% 100%

Current TCO € 4.975,94 € 9.484,37

Delta current TCO Delta current TCO

Annual TCO if ordered in 2027 (5%) € 5.032,29 1% € 9.597,07 1%

Annual TCO if ordered in 2028 (10%) € 5.088,65 2% € 9.709,79 2%

Annual TCO if ordered in 2029 (17,5%) € 5.173,18 4% € 9.878,85 4%

Annual TCO if ordered in 2030 (25%) € 5.257,71 6% € 10.047,92 6%

Annual TCO if ordered in 2031 (32,5%) € 5.342,24 7% € 10.216,98 8%

To reflect the impact from the changing (social) tax regime, we keep all other variables stable

17© 2021 Deloitte

What about the impact for my employees?

2

18© 2021 Deloitte

Consequences of the new bill for individuals/employees

Impact for employees

The bill focuses mainly on reducing the tax deductibility of vehicles. However, an indirect impact for employees/individuals in the future needs to be considered.

Impact WLTPImpact parameters benefit in kind Impact deductible expenses

impact as of income year 2026

New bill does not include a change of the calculation method of the benefit in kind for employees

However, the CO2-coefficient is indexed based on the average CO2-emission of the Belgian fleet, meaning that an increase of electric vehicles will cause for a higher benefit in kind for ICE and (certain) hybrid models.

Status quo - new bill does not include an update on the exact entry into force of the WLTP method for tax purposes.

The following scenarios apply, based on the information mentioned on the registration form:

1. Only NEDC mentioned -> NEDC applies

2. Only WLTP mentioned -> WLTP applies

3. Both NEDC & WLTP mentioned -> free choice

Update - As of 2026, the lump sum cost deductions for commuting of 0,15 EUR/km, will only be applied for the following vehicles:

- Zero emission vehicles

- Vehicles ordered before 1.07.2023

- Vehicles ordered between 01.07.2023 – 31.12.2025

19© 2021 Deloitte

Which incentives are made available to accelerate the transition?

3

20© 2021 Deloitte

IncentivesCharging of electric vehicles

In order to facilitate the use of electric company cars, drivers need to be supported in their charging needs throughout their full trajectory: at the office, on the road and at home.

On road chargingOffice charging Home charging

Currently, charging stations installed at the office are 100% tax deductible.

Update – the new bill includes a temporary, increased corporate tax deduction for new charging stations under the following conditions:

- installed between 1.09.2021 and 31.08.2024; and

- the charging stations are publicly accessible.

For the company, the electricity cost follows the corporate tax deductibility of the company car (i.e. 100% until income year 2026, and gradually decreasing as of income year 2027)

For the company, the electricity cost follows the corporate tax deductibility of the company car (i.e. 100% until income year 2026, and gradually decreasing as of income year 2027)

For the employee, the provision of a charging pass is considered to be included in the benefit in kind of the company car.

The placement of a charging station at home can be facilitated as follows:

- Private purchaseUpdate – the new bill includes a tax credit for newly placed charging stations between 01.09.2021 –31.08.2024

- Put at disposal by the employerConsidered to be included in the benefit in kind of the company car

For the company, the electricity cost follows the corporate tax deductibility of the company car (i.e. 100% until income year 2026, and gradually decreasing as of income year 2027)

21© 2021 Deloitte

IncentivesCharging of electric vehicles – update for office charging

Goal

Incentivize the installation of charging stations by companies to facilitate office and public charging, and reducing the investment burden on the level of the government

Who?

Enterprises (both personal & corporate income tax)

What?

As of 01.09.2021, an increased corporate tax deduction would apply to newly placed “intelligent” charging stations under the condition that they would be publicly accessible:

- 200% for charging stations acquired between 01.09.2021 and 31.12.2022

- 150% for charging stations acquired between 01.01.2023 and 31.08.2024

Conditions?

✓ Publicly accessible:

- Accessible for third parties, at least during the normal business hours or during the closing hours of the enterprise

- The charging station needs to be reported to the Ministry of Finance

✓ Intelligent charging station

- Charge time and charge power must be controllable by an energy management system (+ specific technical requirements).

VAT considerations

- VAT deduction on installation: according to general VAT deduction of the company as a whole.

- VAT deduction on consumption: electricity = fuel so limited to professional use of company car (35% - 50%). Practical implications?

Practical considerations

- Feasible for third party access to the premises for charging:

- from a security perspective?Is it possible for third parties to access the premises?

- from an infrastructure perspective?Is the current network powerful enough to support a multitude in charging stations?

- from an employee perspective?Do you want to make charging stations for employees accessible to third parties?

22© 2021 Deloitte

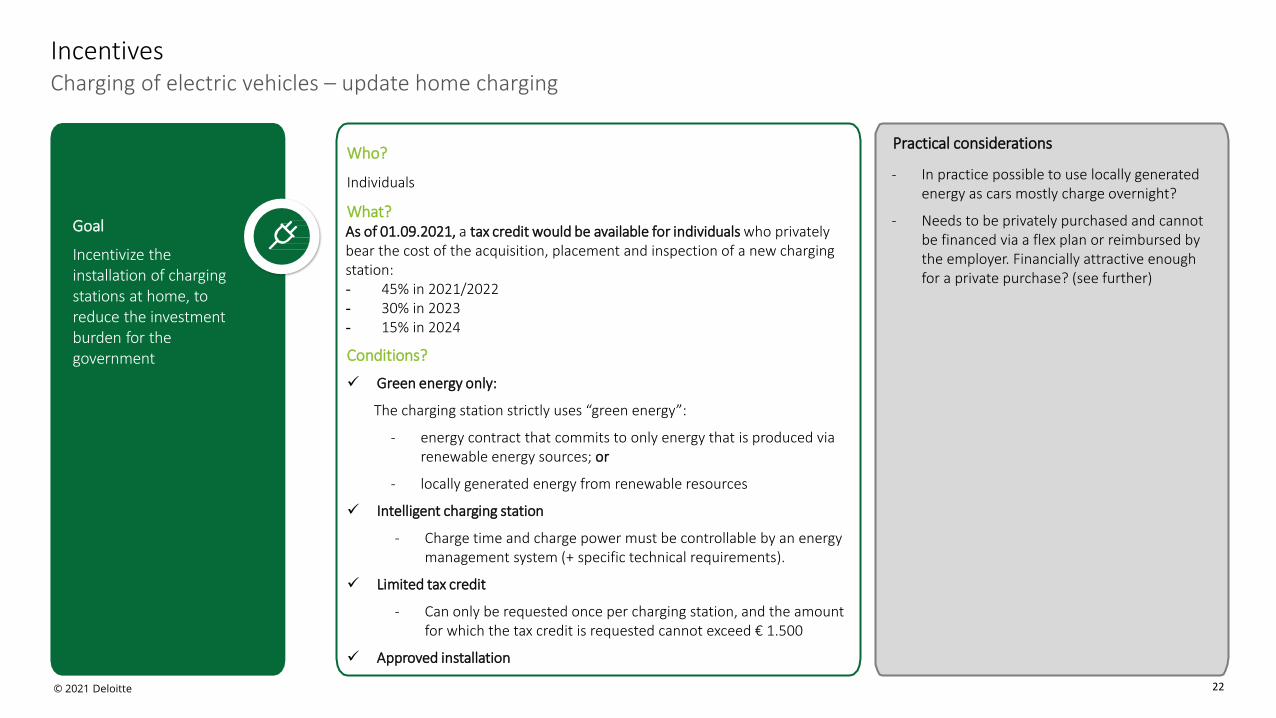

IncentivesCharging of electric vehicles – update home charging

Goal

Incentivize the installation of charging stations at home, to reduce the investment burden for the government

Who?

Individuals

What? As of 01.09.2021, a tax credit would be available for individuals who privately bear the cost of the acquisition, placement and inspection of a new charging station:- 45% in 2021/2022- 30% in 2023- 15% in 2024

Conditions?

✓ Green energy only:

The charging station strictly uses “green energy”:

- energy contract that commits to only energy that is produced via renewable energy sources; or

- locally generated energy from renewable resources

✓ Intelligent charging station

- Charge time and charge power must be controllable by an energy management system (+ specific technical requirements).

✓ Limited tax credit

- Can only be requested once per charging station, and the amount for which the tax credit is requested cannot exceed € 1.500

✓ Approved installation

Practical considerations

- In practice possible to use locally generated energy as cars mostly charge overnight?

- Needs to be privately purchased and cannot be financed via a flex plan or reimbursed by the employer. Financially attractive enough for a private purchase? (see further)

23© 2021 Deloitte

IncentivesCharging of electric vehicles – putting a charging station at the disposal of employees

Goal

Providing employees with the opportunity to charge their electric car at home by putting a charging station at their disposal

Who?

Employees

What?

When the employer puts a charging station at the disposal of employees with a company car, the benefit of the charging station is considered as included in the benefit in kind of the company car (i.e. no additional benefit in kind, based on current ruling practice).

Conditions?

✓ not applicable in case of a transfer of property (i.e. employee purchasing the charging station via the employer)

✓ excluded from the tax credit for newly placed charging stations as of 01.09.2021

✓ The cost of the charging station is 100% tax deductible for the employer. As of 2030, this will be reduced to 75%.

✓ No restrictions on which energy can be used for the charging station (cf. tax reduction for privately purchased charging stations).

VAT considerations

- In general subject to 21% VAT but 6% possible for “old” private dwellings (>10y)

- VAT deduction on installation: limited to professional use of company car (i.e. VAT recovery limitation:35% - 100%)

- Attention point from a VAT perspective regarding the electricity cost of the charging station related to home charging(see further)

Practical considerations

✓ Can be included as a benefit in a flexible benefit scheme to safeguard cost neutrality for the employer

✓ Attention point in case of termination to determine the potential residual value as a benefit in kind

24© 2021 Deloitte

IncentivesCharging of electric vehicles – electricity cost for home charging

VAT treatment

Whether or not the VAT on the electricity costs for the home charging is deductible for the employer, depends on the actual set-up

Direct intervention by employer in the home charging costs

Scenario:

Reimbursement by employer of the home charging costs

Scenario:

Other electricity consumption

Cost home charging

Employee Employer

Invo

ice

Invo

ice

Full electricity consumption

Employee Employer

Invo

ice

Reimbursement of home charging costs

Impact – VAT can be recovered by employer

Because the employer directly receives an invoice from the energy provider (including VAT) for the electricity cost for the home charging, the employer will be able to partially recover the VAT on the electricity cost related to the professional use (e.g. 35% according to method 3).

Attention should be paid to the set-up so that no additional non-deductible VAT is created.

Impact – VAT cannot be deducted by employer

The employer will reimburse the amount of the consumed electricity inclusive VAT to the employee. This VAT cannot be deducted by the employer.

In case a 3rd party is involved, the 3rd party should issue a settlement/payment request (no invoice) to ask for reimbursement of this amount from the employer.

Cost increase of 7% for the employer on the electricity cost,

compared to the direct intervention by the employer

(directly or via 3rd party)

25© 2021 Deloitte

IncentivesCharging of electric vehicles – putting a charging station at the disposal of employees

In order to electrify your fleet, it will need to be considered how the charging of the electric company car at home will be facilitated. With the new bill, the below options would be available (example with a charging station valued at € 1.500, including VAT).

Charging station put at disposal via flexible benefits scheme

Charging station put at disposal by employer Privately purchased charging station

Scenario:

A charging station would be put at the disposal of the employee, and the full cost of the charging station would be borne by the employer

The VAT on the charging station could be partially recovered by the employer (e.g. 35% via method 3)

No additional benefit in kind needs to be considered in the hands of the employee.

Total gross employer costCost charging stationNon-deductible VAT

€ 1.408,88€ 1.239,67

€ 169,21

Net impact employee € 0

Scenario:

A charging station would be put at the disposal of the employee and would be financed via a gross salary sacrifice by the employee.

The VAT on the charging station could be partially recovered by the employer (e.g. 35% via method 3)

No additional benefit in kind needs to be considered in the hands of the employee.

Total gross employer cost € 0

Net impact employee* € 451,45

Scenario:

A charging station would be purchased privately by the employee, and the employee would apply for the tax reduction.

Total gross employer cost € 0

Net impact employee

In 2021/22 – tax reduction @ 45%In 2023 – tax reduction @ 30%In 2024 – tax reduction @ 15%

€ 825€ 1.050€ 1.275

* Taking into account that the cost is financed over 1 year, with an employer social security rate of 28%, marginal tax rate of 53,5% and corporate income tax rate of 25%.

26© 2021 Deloitte

Increased investment deduction for carbon-free trucks and certain infrastructureIncentives

Incentive applies to (i) the purchase of carbon-free trucks (in new condition) and (ii) the installation of refueling infrastructure for blue/green/turquoise hydrogen and of electric charging infrastructure for zero carbon trucks:

Trucks? Any truck, trailer or semi-trailer of category N1, N2 or N3, as defined in the Technical Regulations for Vehicles and which are qualified at registration on the code "CV = Camion/ Vrachtwagen" or "TR = Tracteur/ Trekker“

Excluded? E.g. ‘entreprise en difficulté / onderneming in moeilijkheden’, assets for which regional aid was obtained, …

Year investment is made Investment deductionin 2023 35%in 2024 29.5%in 2025 24%in 2026 18.5%as of 2027 13.5%

27© 2021 Deloitte

Is the evolution to a broader mobility plan also supported?

3

28© 2021 Deloitte

Current status on the facilitation of a broader mobility program

Broader mobility plan

New bill

The initially foreseen update to the mobility budget legislation has been lifted from the current bill as this topic is still subject to further discussions on the level of the social partners. The current mobility budget will therefore be updated via a separate law.

Current situation

Currently, the legislation on the mobility budget allows for company car eligible employees to exchange their current company car for a mobility budget that can be spend in the following pillars:

- Pillar I: environmentally friendly company car

- Pillar II: alternative mobility

- Pillar III: annual cash allowance

The initial pre-draft law on the future of mobility included measures to:

- further extend the scope of Pillar II on the mobility solutions possible within the mobility budget

- limit over time the scope of application only to zero-emission mobility solutions

Given the impact of the mobility budget in broader social context, this topic as lifted from the current bill and proposed to the social partners for further discussions.

The social partners have recently published their opinion on the proposed measures of the bill.

To be continued…

Practical considerations

✓ Does the current mobility budget fit within your organisation?

✓ The mobility budget is still limited to company car eligible employees. Can you offer a mobility budget to all employees?

✓ Is it attractive to implement the mobility budget in it’s current form?

✓ …

The implementation of a broader mobility program requires a tailored and holistic approach based on the wants & needs within your organisation…

© 2021 Deloitte Belgium

The evolution to a broader mobility plan6 building blocks to a successful new mobility program

29

1. Vision & Principles• Vision• KPIs• Guiding Principles• Clear narrative of the

purpose• Fit in Reward strategy

3. Mobility solutions• (Electric) Car / Fuel• Train / Bus• (e-) bicycle (lease)• Carpool / Pool car• Remote work / Flex hub• Parking

5. Policies & Procedures• Car / mobility policies• Supporting processes

2. Cost/Data analysis• Geographical data• Demographical data• Work regime data• Cost data• Employee needs and

preferences

• Assist to facilitate the change throughout the entire organization (e.g. campaigns, incentives, ambassadors, trainings HR / business)

6. Comms & activation

• Parking / mobility apps• Mobility Platform• Hardware

4. Tools & Enablers

30© 2021 Deloitte© 2021 Deloitte

Questions?