s u p p l ie r s

FUTURE OF AIR TRAVEL

DREW MAGILLDirector - Marketing

Boeing Commercial Airplanes

Copyright © 2008 Boeing. All rights reserved.

BOEING is a trademark of Boeing Management Company.Copyright © 2008 Boeing. All rights reserved.

Boeing Commercial AirplanesSEPTEMBER 2008

Airlines are facing unprecedented challenges"If the current pricing dynamic does not change,” he said, “our industry will be severely challenged and will continue shrinking." (NWA CEO Douglas Steenland)

“We are not on the edge but we have come to a point of no return ” warns CEO Mats JanssonWe are not on the edge, but we have come to a point of no return, warns CEO Mats Jansson(SAS Group)

"Our industry is challenged as never before by the unrelenting price of oil.” United president, chairman and chief executive Glenn Tilton.

“The simple fact is that the U.S. airline industry, as it is constituted today, was not built for $125-per-barrel oil.” American Airlines CEO Gerard Arpey

"Airlines can't cut costs sufficiently to compensate for the cost of increases that are happening in fuel." Air New Zealand Chief Executive Rob Fyfe

``Over the next 12 years, many more airlines will vanish, unable to cope with high fuel prices, or they will be swallowed g p , yup in takeovers or mergers.” Qantas CEO Geoff Dixon

"What we've seen to date is the tip of

Copyright © 2008 Boeing. All rights reserved.

What we ve seen to date is the tip of the iceberg.” Air New Zealand Chief Executive Rob Fyfe

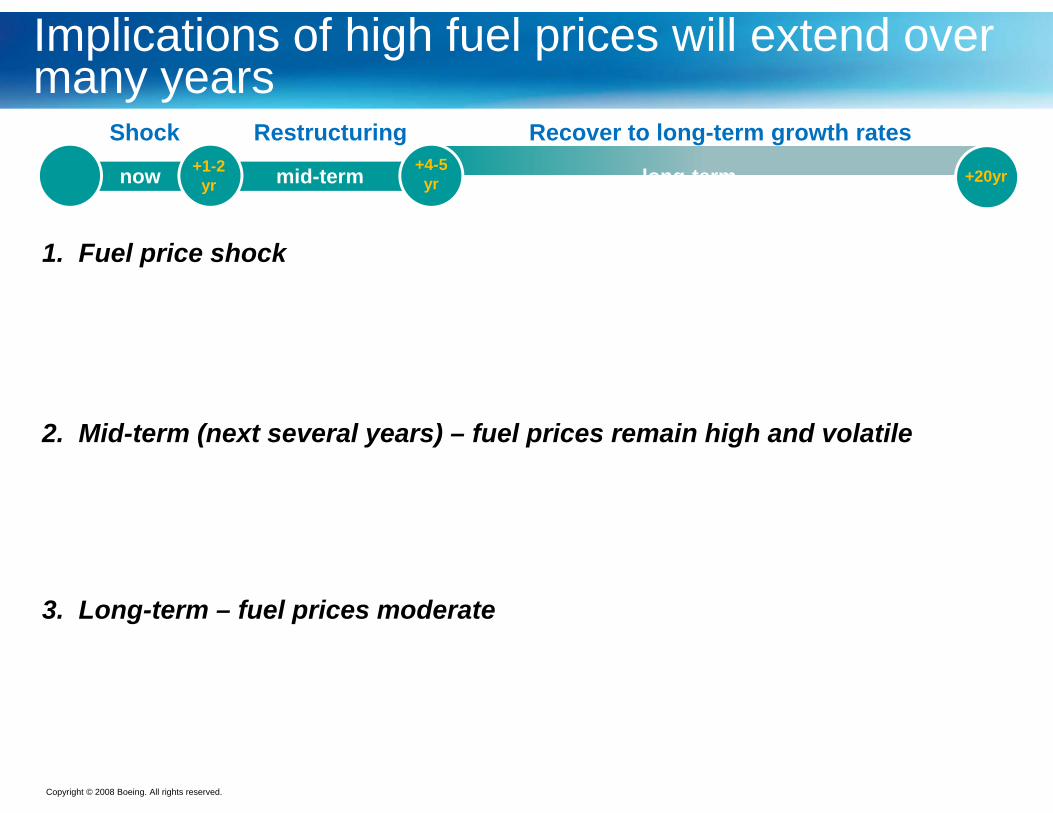

Implications of high fuel prices will extend over many years

Shock Restructuring Recover to long-term growth rates

mid-term+1-2yr +20yrnow +4-5

yr long-term

1. Fuel price shock$2.3B industry loss projected in 2008U S i li hit fi t d h d t d t li it d h d i $ ld fl tU.S. airlines hit first and hardest due to: limited hedging, $, economy, older fleet

Airline response: higher fares, capacity reductions, parking older airplanes, bankruptcies

2. Mid-term (next several years) – fuel prices remain high and volatileDecline from current levelsOPEC actions and emerging market demand are key driversO C ac o s a d e e g g a e de a d a e ey d e s

Airline response: industry restructuring, fleet renewal, less efficient fleet remains parked

3 L t f l i d t3. Long-term – fuel prices moderateOil supply growth more balanced with demandIndustry traffic growth returns to trend

Airline response: pursue growth opportunities; emerge more efficient; new entrants

Copyright © 2008 Boeing. All rights reserved.

Airline response: pursue growth opportunities; emerge more efficient; new entrants and innovations

Strong, balanced backlog validates Boeing’s product strategy

Backlog $Backlog $ ModelModel$ - Billions 747

275255

250

300

Single-Aisle32%

Large8%777 737

174200

250

Twin-Aisle60% 767

RegionRegion124150787

70

50

100AmericasLeasing Leasing

& Gov't& Gov't

Middle China & China &

0

2004 2005 2006 2007 2Q08Europe S.E.

Middle East & Africa

Asia-Pacific

East AsiaEast Asia

Russia

Copyright © 2008 Boeing. All rights reserved.

2004 2005 2006 2007 2Q08 Asia

Air Travel Demand: Long Term

Copyright © 2008 Boeing. All rights reserved.

Liberalization is spreading globally opening the market for more new airlines

160AirlinesEntrants

900

120

140

700

EntrantsExits

800

AirlnesAirlnes Differentiate Themselves Through:Differentiate Themselves Through:

80

100

500 Airlinesper Year

Total Numberof Airlines

600 Safe,Safe,ReliableReliable

Convenient air travelConvenient air travelfor lower faresfor lower fares

40

60

200

300

400 per Yearof Airlines ..for lower fares..for lower fares…in comfortable surroundings…in comfortable surroundings

20100

200

T Atl tiUS Domestic Europe

T P ifi I t A i

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Copyright © 2008 Boeing. All rights reserved.

Trans-Atlantic

1970’s 1980’s 1990’s 2000’s

1978pTrans-Pacific Intra Asia

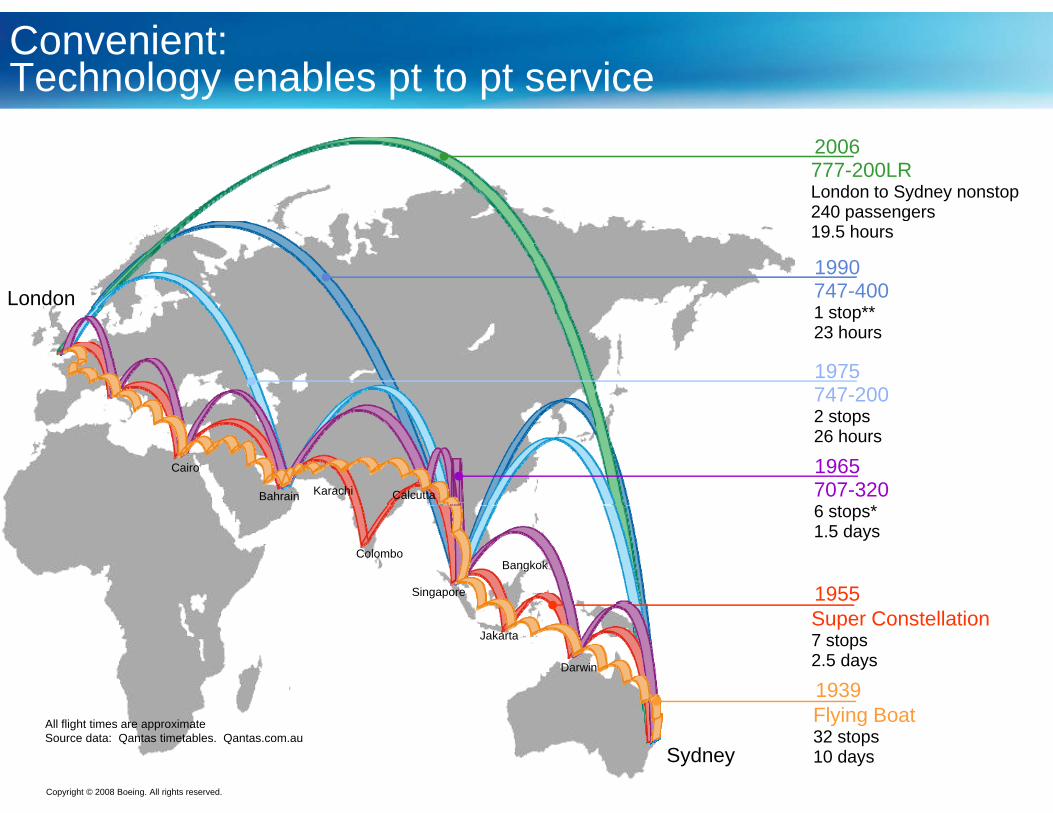

Convenient:Technology enables pt to pt service

777-200LRLondon to Sydney nonstop240 passengers

2006

747-4001 t **

240 passengers19.5 hours

London1990

1 stop**23 hours

747-2001975

2 stops26 hours

CalcuttaKarachiBahrain

Cairo

707-3206 t *

1965

Bangkok

Singapore

Colombo

6 stops*1.5 days

1955Super Constellation7 stops2.5 daysDarwin

Jakarta

1939

Copyright © 2008 Boeing. All rights reserved.

All flight times are approximateSource data: Qantas timetables. Qantas.com.au

Sydney

Flying Boat32 stops10 days

Air travel growth has been met by increased frequencies and nonstops

WorldIndex 1987=1.00

3 0

2.5

3.0

Air Travel Air Travel GrowthGrowth

2.0

2.5

Frequency Frequency GrowthGrowthNonstop Nonstop

1.5

ppMarketsMarkets

1.0 Average Average AirplaneAirplane

0.5

1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007

Airplane Airplane Size Size

Copyright © 2008 Boeing. All rights reserved.

August OAG

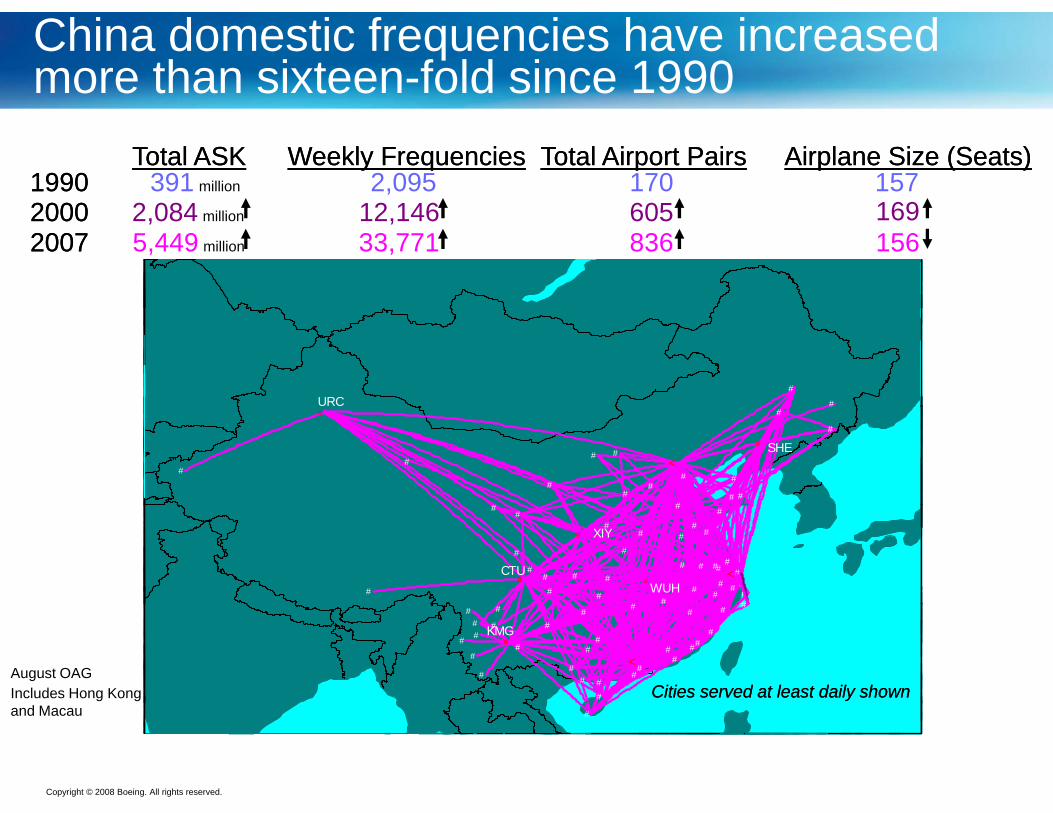

China domestic frequencies have increased more than sixteen-fold since 1990

2 084 12 146 605 16920002000

Total ASKTotal ASK Weekly FrequenciesWeekly Frequencies Total Airport PairsTotal Airport Pairs Airplane Size (Seats)Airplane Size (Seats)391 million 2,095 170 15719901990

2,084 million 12,146 605 169200020005,449 million 33,771 836 15620072007

#URC

#

#URC

#

#URC

#

#

#<

# SHE

#

#

#

#

#

##

#

<# SHE

#

#

#

#

#

##

#

#

#

#

#

##

##

<# SHE

#

#

#

#

#

##

#

#

#

##

CTU#

#

#

#<

#SIA

#

#WUH

#

#

#

#CTU #

#

#

####

#

# #

# ##<

##

##WUH

# XIY

#

#

#

#

#

#CTU #

#

#

###

#

#

#

#

##

##

#

#

##

#<

##

##WUH

##

# XIY

#

##

#

#

<

#

#

#KMG

##

##

#

##

#

<

##

# #

#

#

#

#

#

#KMG #

#

#

# #

##

# #

##

#

###

#

<

##

# #

#

#

#

#

#

#KMG #

#

#

## # #

#

#

##

# ###

#

##

Cities served at least daily shownCities served at least daily shownIncludes Hong KongAugust OAG

Copyright © 2008 Boeing. All rights reserved.

##and Macau

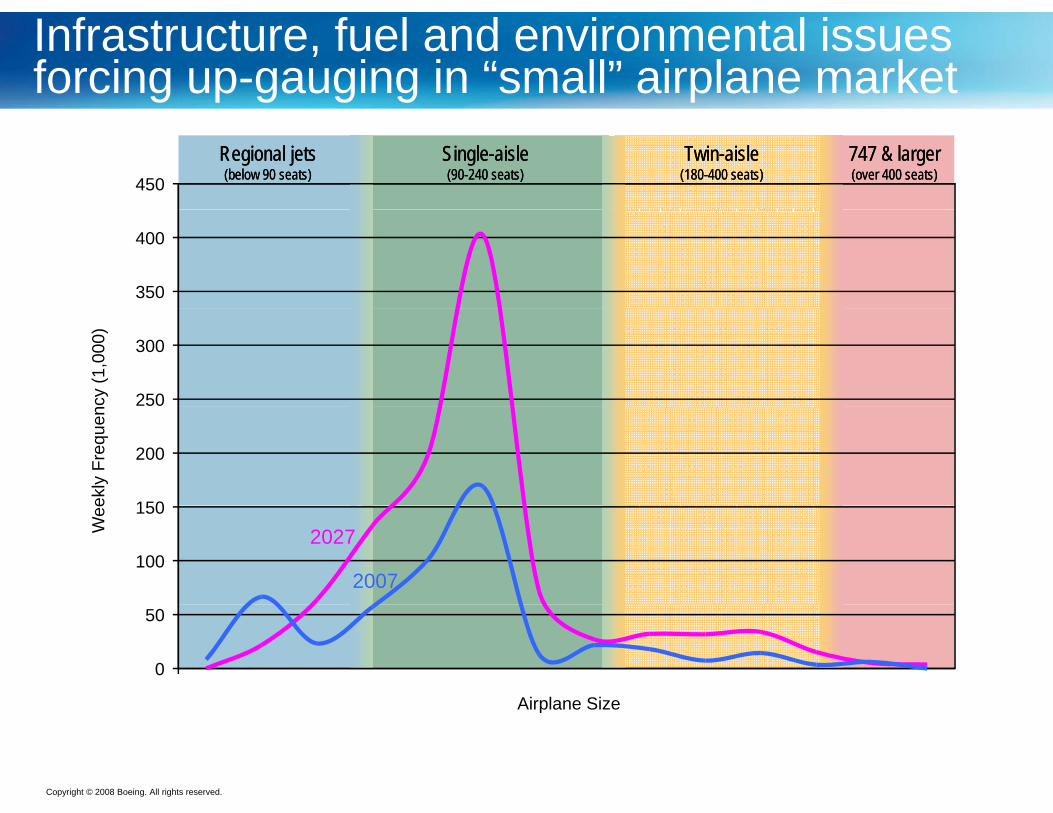

Infrastructure, fuel and environmental issues forcing up-gauging in “small” airplane market

Regional jetsRegional jets(below 90 seats)(below 90 seats)

SingleSingle--aisleaisle(90(90--240 seats)240 seats)

TwinTwin--aisleaisle(180(180--400 seats)400 seats)

747 & larger747 & larger(over 400 seats)(over 400 seats)450

350

400

250

300

cy (1

,000

)

150

200

ekly

Fre

quen

100

150

Wee

2027

2007

0

50

Airplane Size

Copyright © 2008 Boeing. All rights reserved.

Airplane Size

World fleet will double and adjust

2027

747 and larger747 and largerTwin-aisleSingle-aisleRegional jets

19,000airplanes

2007

19,000airplanes

35,800airplanes

Copyright © 2008 Boeing. All rights reserved.

airplanes

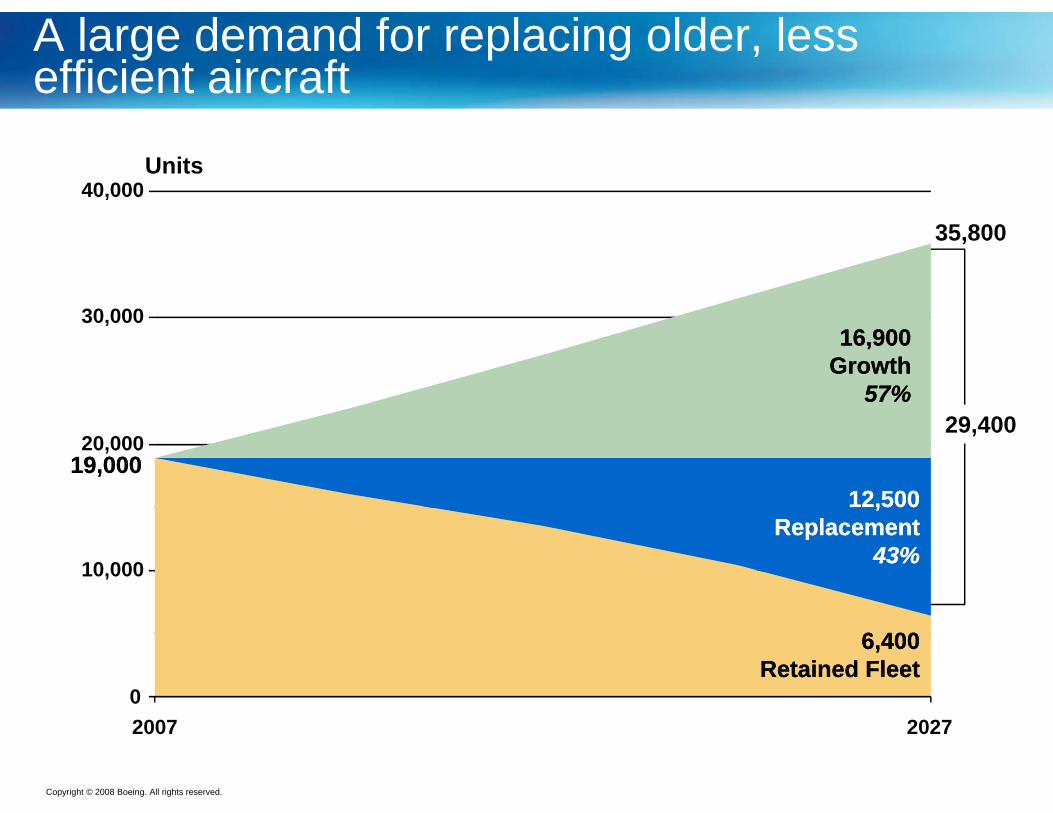

A large demand for replacing older, less efficient aircraft

A large demand for replacing older, less efficient aircraft

Units40,000less efficient aircraft

35,800

30,00016,900

Growth57%

16,900Growth

57%

19,00019,00020,000

29,400

12,50012,500

10,000

12,500Replacement

43%

12,500Replacement

43%

0

6,400Retained Fleet

6,400Retained Fleet

Copyright © 2008 Boeing. All rights reserved.

02007 2027

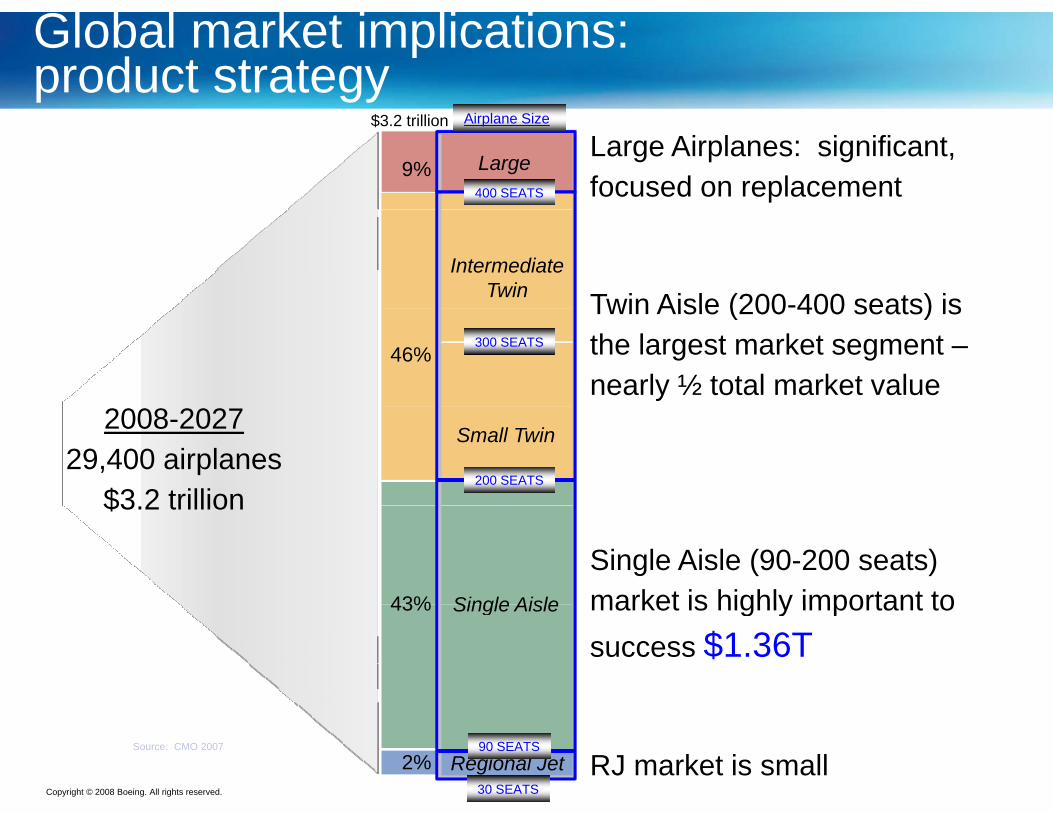

Global market implications:product strategy

Large9%

$3.2 trillion

Large Airplanes: significant, focused on replacement400 SEATS

Airplane Size

IntermediateTwin Twin Aisle (200-400 seats) is

46%

Twin Aisle (200 400 seats) is the largest market segment –nearly ½ total market value

300 SEATS

2008-202729,400 airplanes

$3 2 trillion

Small Twin

200 SEATS

Single Aisle

$3.2 trillion

43%

Single Aisle (90-200 seats) market is highly important toSingle Aisle43% market is highly important to success $1.36T

Copyright © 2008 Boeing. All rights reserved.

2% Regional JetSource: CMO 2007

RJ market is small30 SEATS

90 SEATS

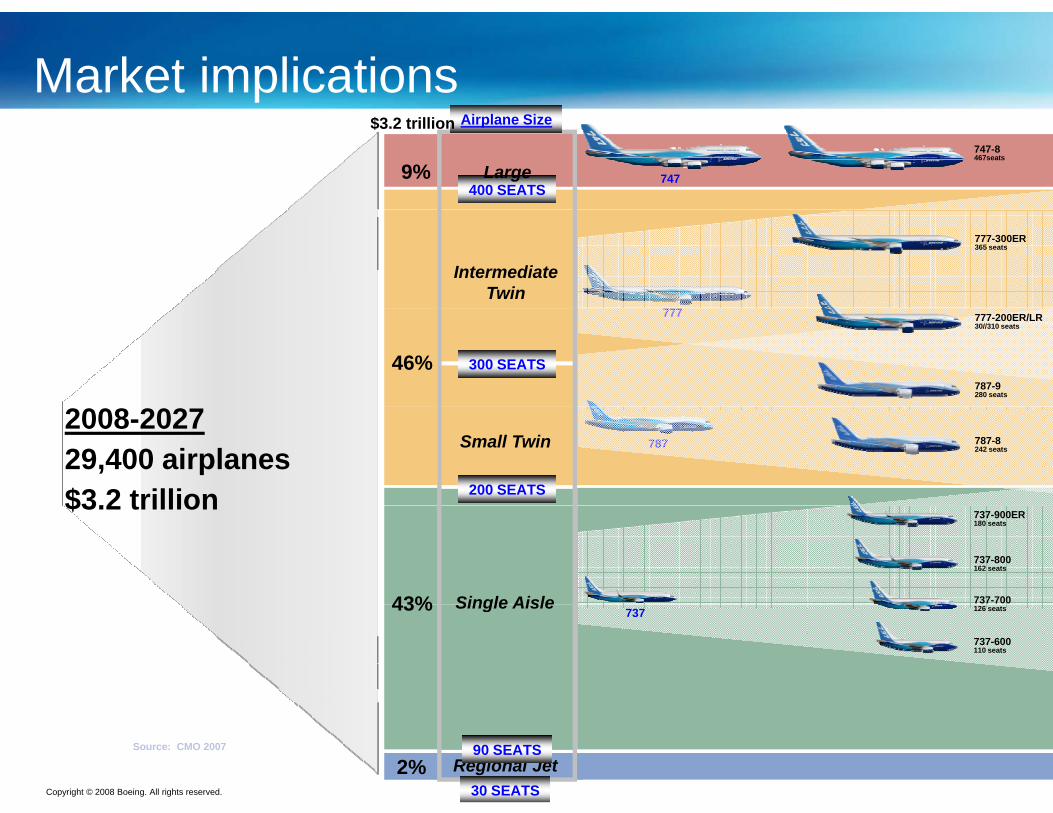

Market implications

747400 SEATS

Airplane Size

Large9%

$3.2 trillion747-8467seats

IntermediateTwin

777-300ER365 seats

777

300 SEATS46%

777-200ER/LR30//310 seats

787-9280 seats

787

200 SEATS

Small Twin 787-8242 seats

2008-202729,400 airplanes$3.2 trillion

Single Aisle43%

737-900ER180 seats

737-800162 seats

737-700

$3.2 trillion

737Single Aisle43%

4%

126 seats

737-600110 seats

Copyright © 2008 Boeing. All rights reserved.

Regional Jet30 SEATS

90 SEATSSource: CMO 2007

2%

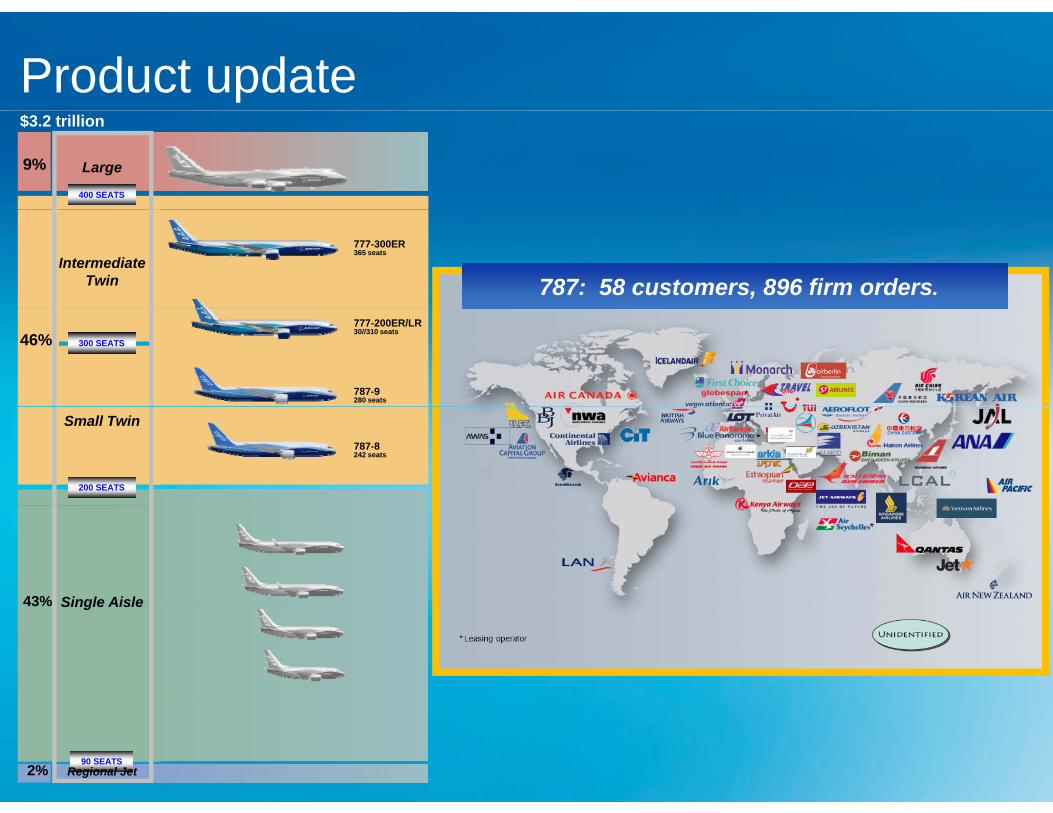

Product updateLarge9%

$3.2 trillion

400 SEATS

IntermediateTwin

777-300ER365 seats

737: 4,896 firm orders, 115 customers;737: 4,896 firm orders, 115 customers;

300 SEATS46%777-200ER/LR30//310 seats

787-9280 seats

200 SEATS

Small Twin787-8242 seats

Single Aisle43%

737-900ER180 seats

737-800162 seatsSingle Aisle43%

737-700126 seats

737-600110 seats

(June 2008)

Copyright © 2008 Boeing. All rights reserved.

90 SEATS2% Regional Jet

Product updateLarge9%

$3.2 trillion

400 SEATS

IntermediateTwin

777-300ER365 seats

787: 58 customers, 896 firm orders.787: 58 customers, 896 firm orders.

300 SEATS46%777-200ER/LR30//310 seats

787-9280 seats

200 SEATS

Small Twin787-8242 seats

Single Aisle43% Single Aisle43%

Copyright © 2008 Boeing. All rights reserved.

90 SEATS2% Regional Jet

Product updateLarge9%

$3.2 trillion

400 SEATS

IntermediateTwin

777-300ER365 seats

777: 1,084 firm orders; 726 delivered; 56 customers

777: 1,084 firm orders; 726 delivered; 56 customers

300 SEATS46%777-200ER/LR30//310 seats

787-9280 seats

200 SEATS

Small Twin787-8242 seats

Single Aisle43% Single Aisle43%

Copyright © 2008 Boeing. All rights reserved.

90 SEATS2% Regional Jet

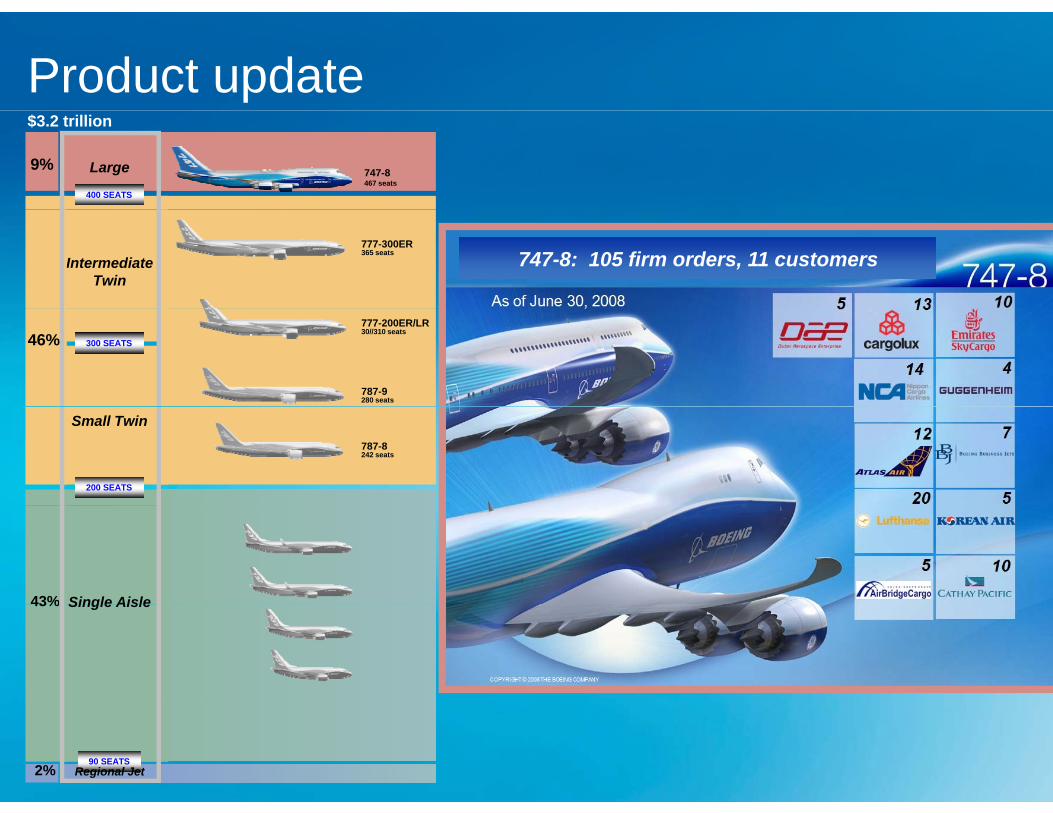

Product updateLarge9%

$3.2 trillion

747-8467 seats

400 SEATS

IntermediateTwin

777-300ER365 seats 747-8: 105 firm orders, 11 customers

300 SEATS46%777-200ER/LR30//310 seats

787-9280 seats

200 SEATS

Small Twin787-8242 seats

Single Aisle43% Single Aisle43%

Copyright © 2008 Boeing. All rights reserved.

90 SEATS2% Regional Jet

Market and Strategy SummaryAir travel is a crucial and fundamental

l di t t d d f…leading to strong demand for new airplanes

Aviation faces challenges− Economic uncertainty− Congestion, Fuel Costs, Environmental

Boeing focus: l d i ti t t tBoeing focus: lead aviation to meet strong demand and overcome challenges via technological innovations− Completing products in development− Completing products in development− Meeting strong demands for new airplanes− Collaborating with customers on the next

breakthroughs in airplanes and services

Copyright © 2008 Boeing. All rights reserved.