Download - funds management

FUNDS MANAGEMENT

The functions in this component support you in creating and executing budgets. The purpose of Funds Management is to budget all revenues and expenditures for individual areas of responsibility, to control future funds transactions in accordance with the distributed budget, and to stop the budget being exceeded. You can adapt the budget to changes in conditions by entering releases, supplements, returns, and transfers.

Funds Management is fully integrated with other components of the SAP System, especially with the Budget Control System (BCS). The components that are integrated depend on the specific requirements of your organization. A basic requirement for the use of Funds Management is integration with the General Ledger Accounting (FI-GL) component. .

Integration

Integrating the components Materials Management and Funds Management means that you can reproduce and monitor a procurement transaction from the purchase requisition through to the invoice for example. Integration also ensures that all the data you need for budget execution is available in Funds Management without additional data entry.

FeaturesFunds Management enables you to:Control revenues and expenditures and thus control the funding of business transactions of an organization.Closely control your budget, with the following questions in mind:What funds will the areas of responsibility receive?Where do these funds come from (source of funds)?What are the funds used for? (use of funds)Control the finances of your organization by comparing commitment and actual values with current budget values.

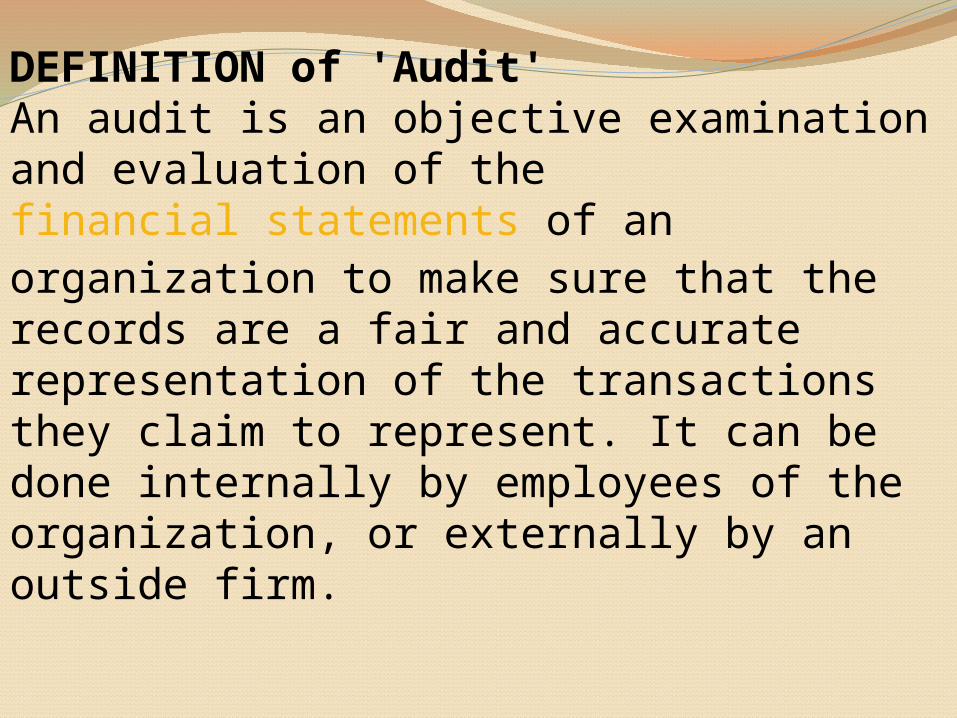

DEFINITION of 'Audit'An audit is an objective examination and evaluation of the financial statements of an organization to make sure that the records are a fair and accurate representation of the transactions they claim to represent. It can be done internally by employees of the organization, or externally by an outside firm.

Audit overviewPosting checkingTesting the existence and effectiveness of management controls that prevent financial statement misstatementCasting checkingPhysical examination and countConfirmationInquiryObservation

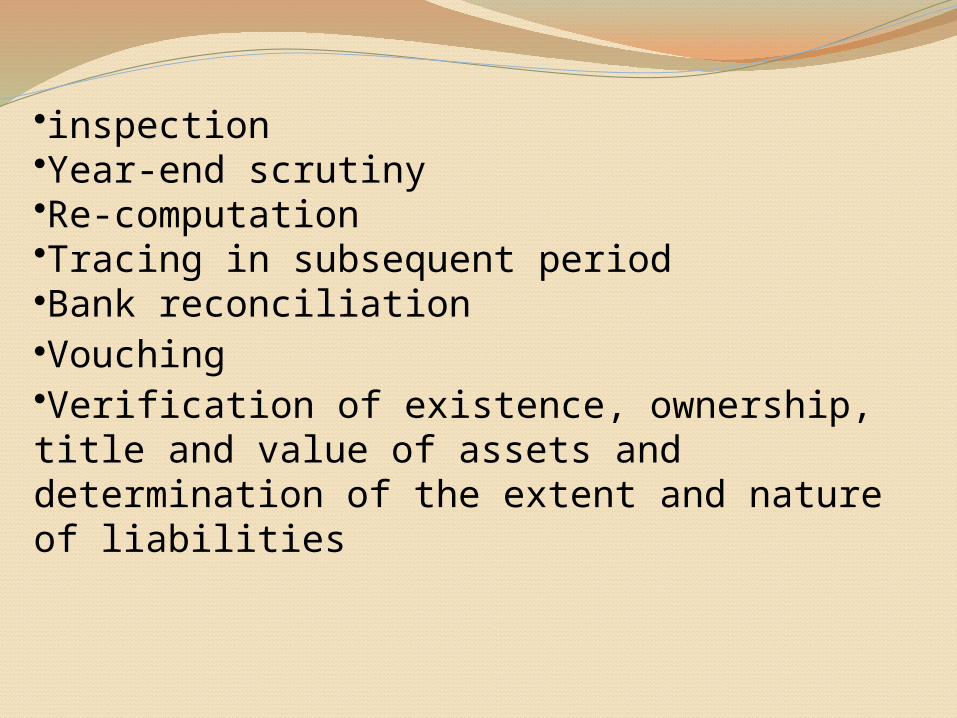

•inspection •Year-end scrutiny •Re-computation •Tracing in subsequent period •Bank reconciliation •Vouching •Verification of existence, ownership, title and value of assets and determination of the extent and nature of liabilities

What is Forecasting?

¨ Process of predicting a future event

¨ Underlying basis of all business decisions¨ Production¨ Inventory¨ Personnel¨ Facilities

Sales will be $200 Million!

Types of Forecasts by Time Horizon

Short-range forecastUp to 1 year; usually less than 3 monthsJob scheduling, worker assignments

Medium-range forecast3 months to 3 yearsSales & production planning, budgeting

Long-range forecast3+ yearsNew product planning, facility location

Short-term vs. Longer-term Forecasting

Medium/long range forecasts deal with more comprehensive issues and support management decisions regarding planning and products, plants and processes.

Short-term forecasting usually employs different methodologies than longer-term forecasting

Short-term forecasts tend to be more accurate than longer-term forecasts.

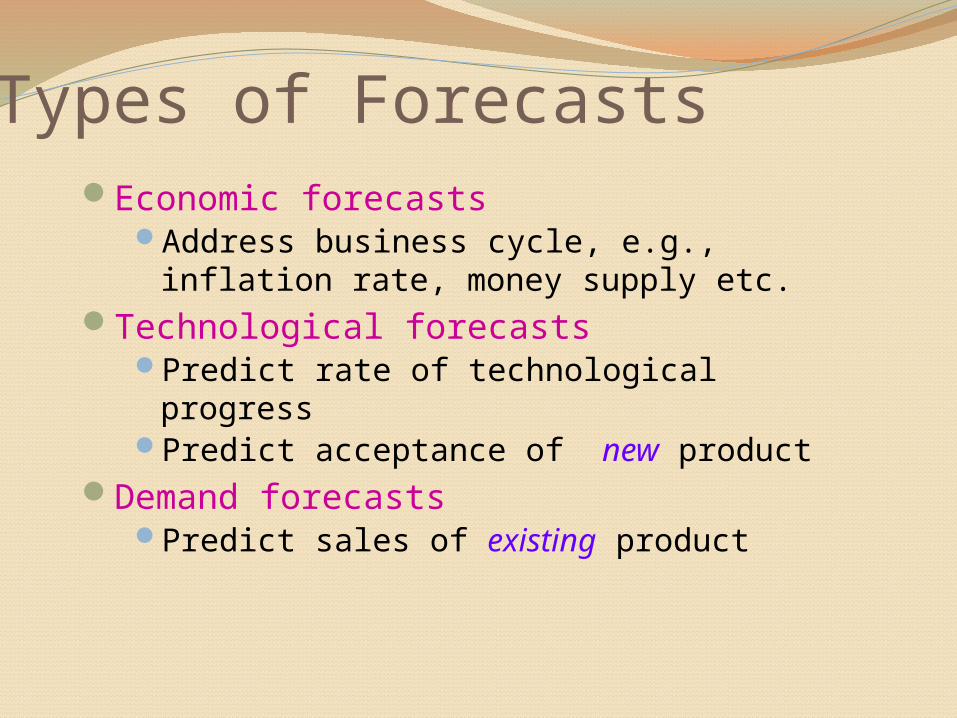

Types of ForecastsEconomic forecasts

Address business cycle, e.g., inflation rate, money supply etc.

Technological forecastsPredict rate of technological progressPredict acceptance of new product

Demand forecastsPredict sales of existing product

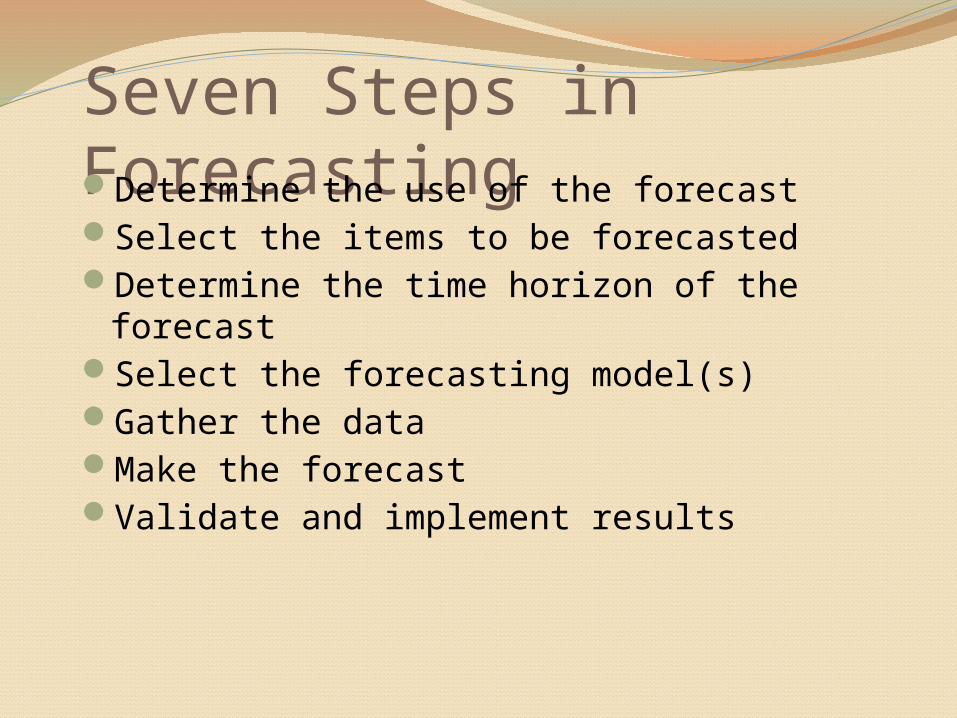

Seven Steps in ForecastingDetermine the use of the forecastSelect the items to be forecastedDetermine the time horizon of the forecastSelect the forecasting model(s)Gather the dataMake the forecastValidate and implement results

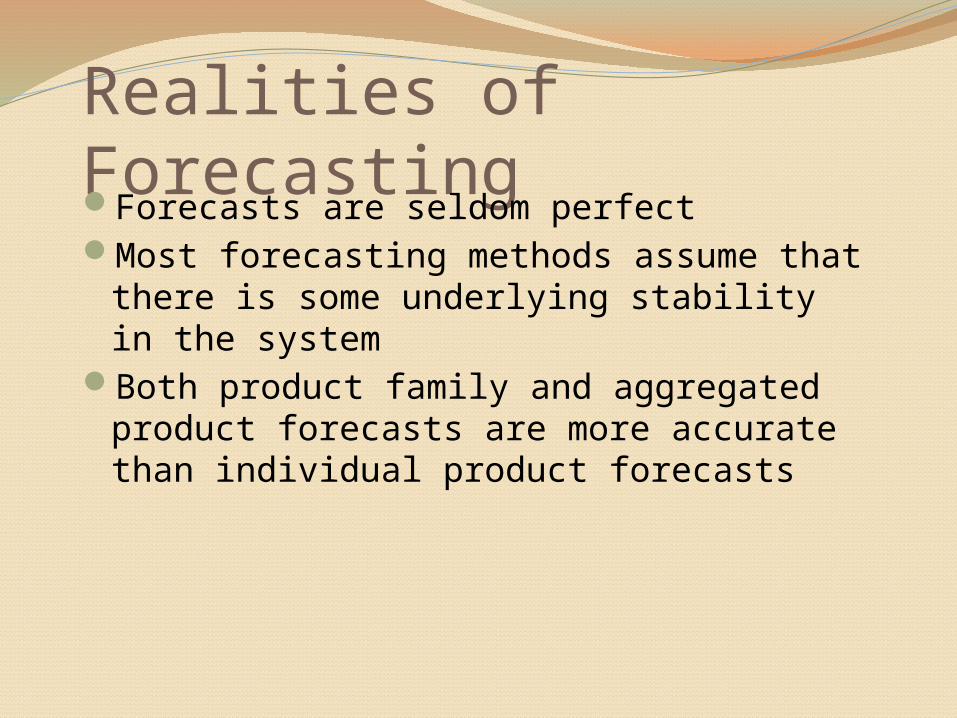

Realities of ForecastingForecasts are seldom perfectMost forecasting methods assume that

there is some underlying stability in the system

Both product family and aggregated product forecasts are more accurate than individual product forecasts

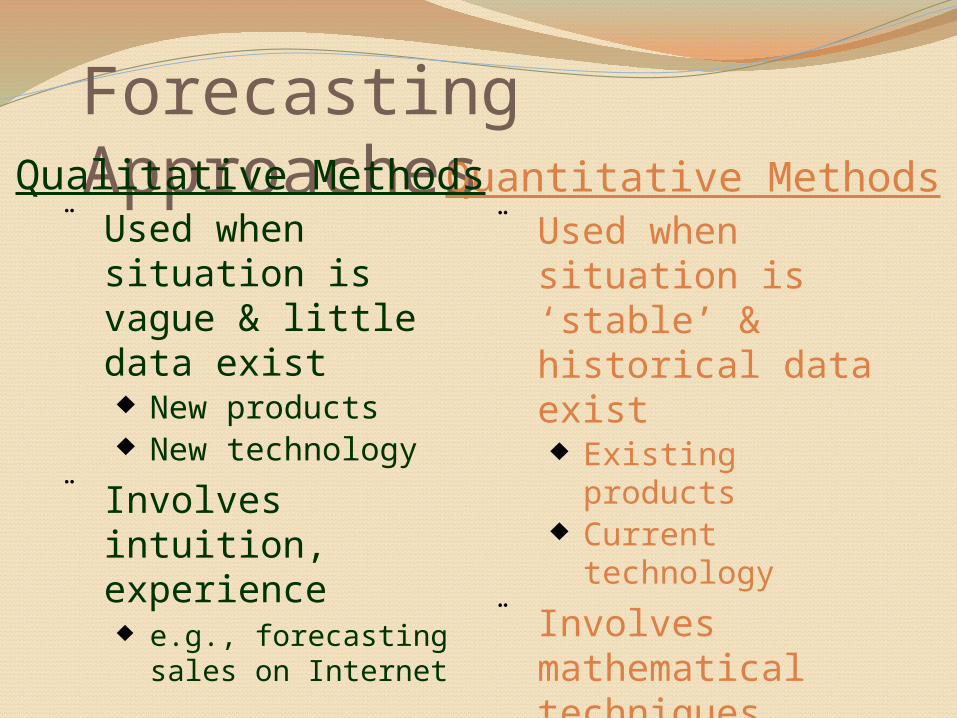

Forecasting Approaches

¨ Used when situation is ‘stable’ & historical data exist¨ Existing products¨ Current

technology¨ Involves

mathematical techniques¨ e.g., forecasting

sales of color televisions

Quantitative Methods¨ Used when

situation is vague & little data exist¨ New products¨ New technology

¨ Involves intuition, experience¨ e.g., forecasting

sales on Internet

Qualitative Methods