Download - Forrester for astra_cloud_2016

Catching The Wave™: The Rising Public

Cloud Platforms MarketMaxim Tambiev

Country Manager, Russia

December, 2016

© 2016 Forrester Research, Inc. Reproduction Prohibited 3

We work with business and technology leaders to develop customer-obsessed strategies that drive growth.

© 2016 Forrester Research, Inc. Reproduction Prohibited 4

Agenda

› Trends driving the cloud platform market

› The public cloud platform vendor landscape

› The Forrester Wave™: Global Public Cloud Platforms For Enterprise Developers, Q3 2016

© 2015 Forrester Research, Inc. Reproduction Prohibited 5

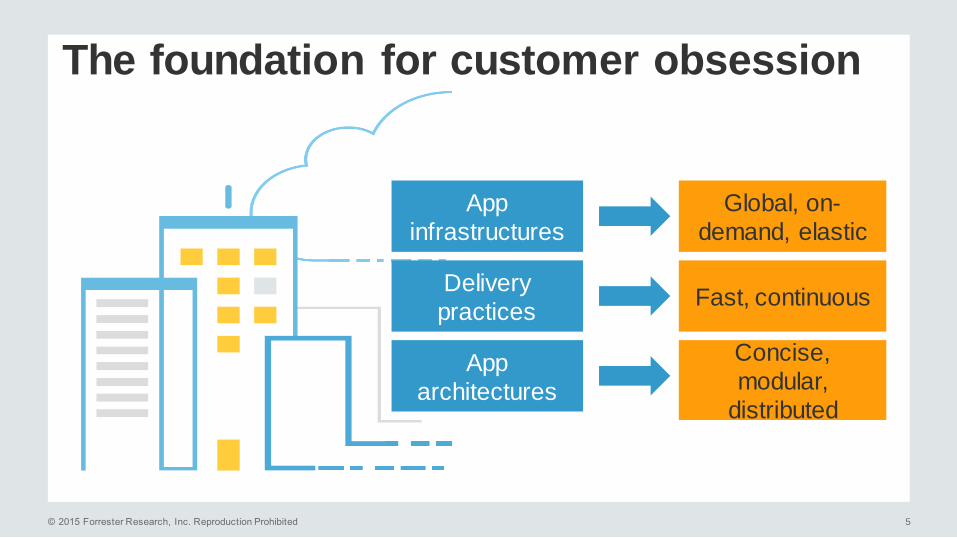

The foundation for customer obsession

App

infrastructures

Delivery

practices

App

architectures

Global, on-

demand, elastic

Fast, continuous

Concise,

modular,

distributed

© 2016 Forrester Research, Inc. Reproduction Prohibited 6

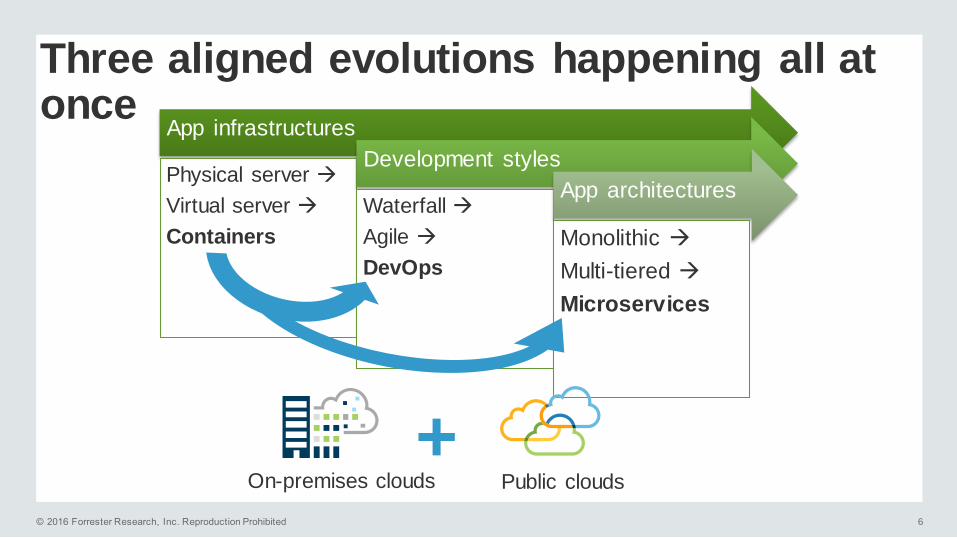

Three aligned evolutions happening all at once

App infrastructures

Physical server

Virtual server

Containers

Development styles

Waterfall

Agile

DevOps

App architectures

Monolithic

Multi-tiered

Microservices

On-premises clouds Public clouds

+

© 2016 Forrester Research, Inc. Reproduction Prohibited 7

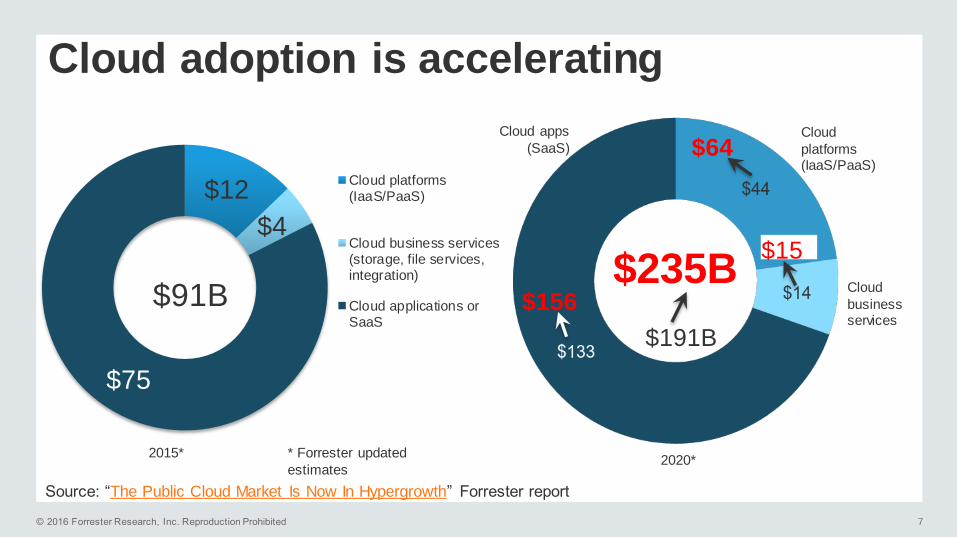

Cloud adoption is accelerating

Source: “The Public Cloud Market Is Now In Hypergrowth” Forrester report

$12

$4

$75

Cloud platforms(IaaS/PaaS)

Cloud business services(storage, file services,integration)

Cloud applications orSaaS

$91B

2015* * Forrester updated

estimates

Cloud

platforms (IaaS/PaaS)

Cloud

businessservices

Cloud apps

(SaaS)

2020*

$235B$156

$64

$15

$191B

© 2016 Forrester Research, Inc. Reproduction Prohibited 8

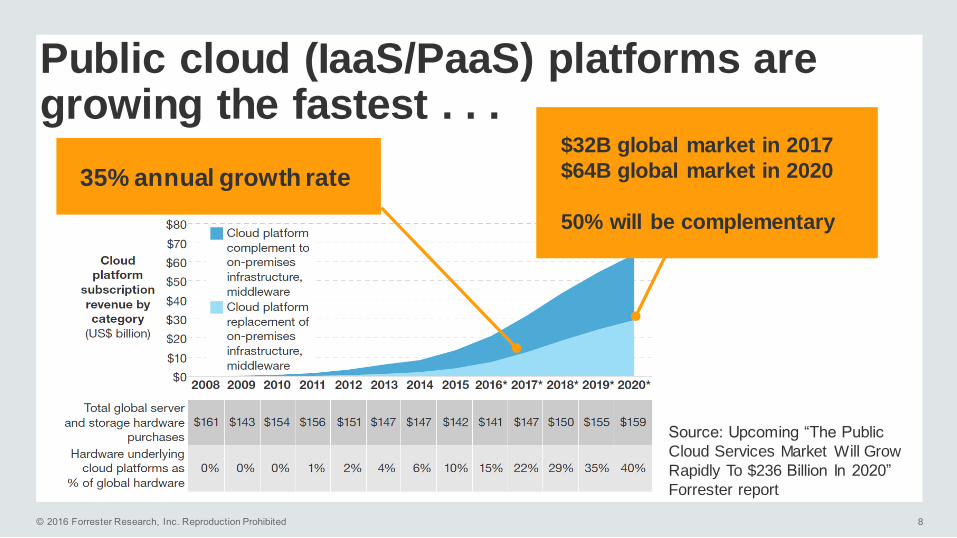

Public cloud (IaaS/PaaS) platforms are growing the fastest . . .

Source: Upcoming “The Public

Cloud Services Market Will Grow

Rapidly To $236 Billion In 2020”

Forrester report

35% annual growth rate

$32B global market in 2017

$64B global market in 2020

50% will be complementary

© 2016 Forrester Research, Inc. Reproduction Prohibited 9

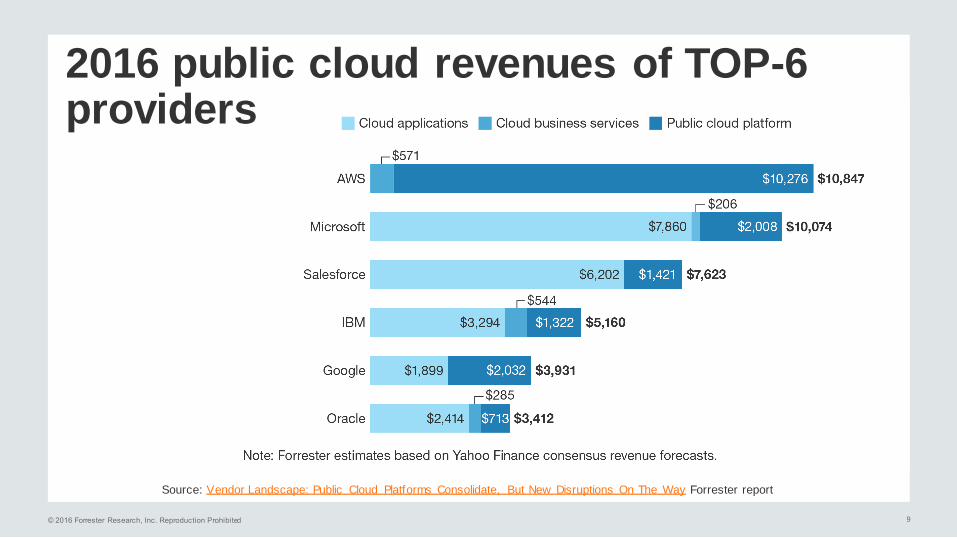

Source: Vendor Landscape: Public Cloud Platforms Consolidate, But New Disruptions On The Way Forrester report

2016 public cloud revenues of TOP-6 providers

© 2016 Forrester Research, Inc. Reproduction Prohibited 10

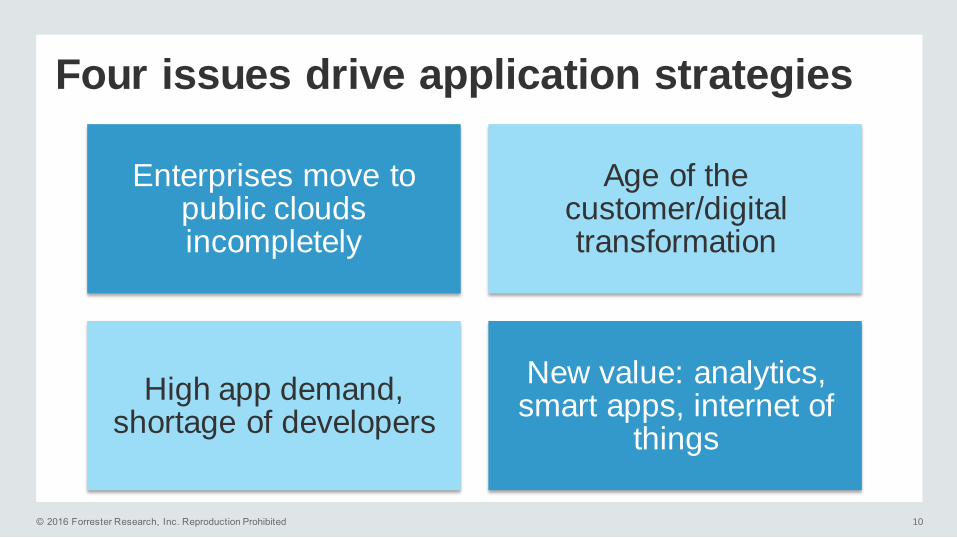

Four issues drive application strategies

Enterprises move to public clouds incompletely

Age of the customer/digital transformation

High app demand, shortage of developers

New value: analytics, smart apps, internet of

things

© 2016 Forrester Research, Inc. Reproduction Prohibited 11

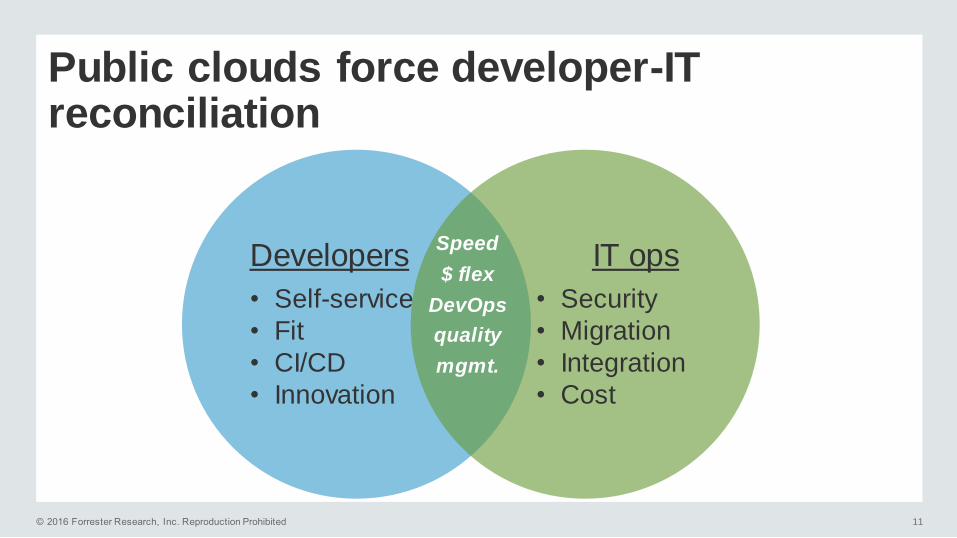

Public clouds force developer-IT reconciliation

Developers

• Self-service

• Fit

• CI/CD

• Innovation

IT ops

• Security

• Migration

• Integration

• Cost

Speed

$ flex

DevOps

quality

mgmt.

© 2016 Forrester Research, Inc. Reproduction Prohibited 12

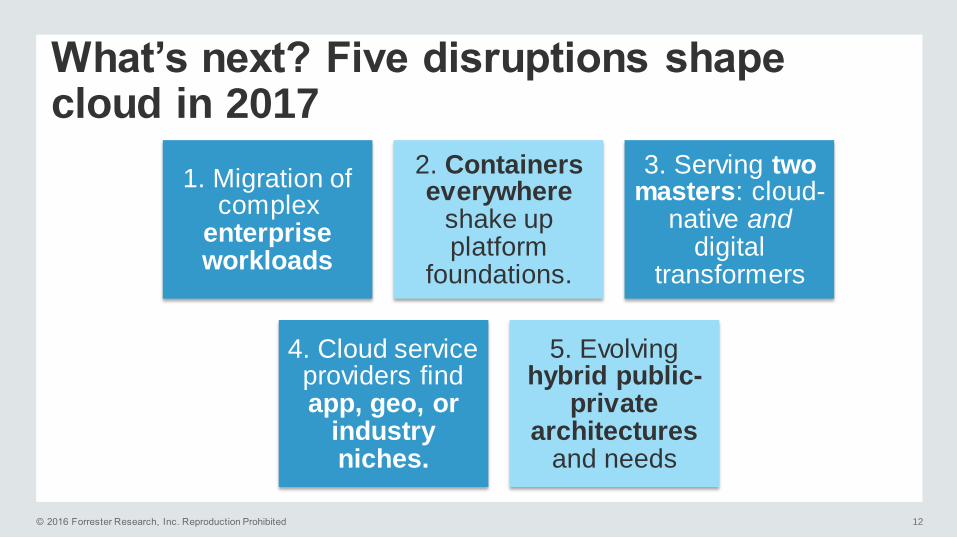

What’s next? Five disruptions shape cloud in 2017

1. Migration of complex

enterprise workloads

2. Containers everywhere

shake up platform

foundations.

3. Serving two masters: cloud-

native anddigital

transformers

4. Cloud service providers find app, geo, or

industry niches.

5. Evolving hybrid public-

private architectures

and needs

© 2016 Forrester Research, Inc. Reproduction Prohibited 13

Source: “Vendor Landscape: Public Cloud Platforms Consolidate, But New Disruptions On The Way” Forrester report

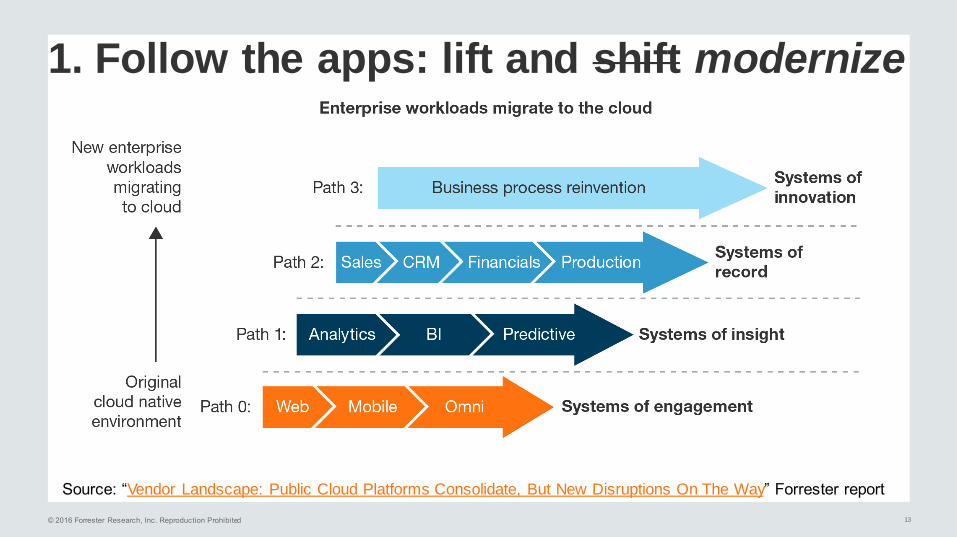

1. Follow the apps: lift and shift modernize

© 2016 Forrester Research, Inc. Reproduction Prohibited 14

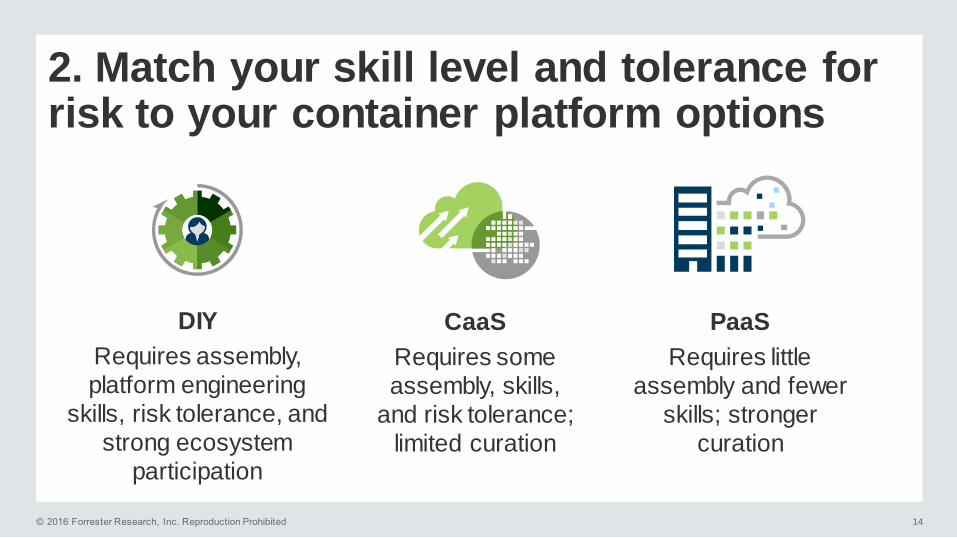

2. Match your skill level and tolerance for risk to your container platform options

DIY

Requires assembly,

platform engineering

skills, risk tolerance, and

strong ecosystem

participation

CaaS

Requires some

assembly, skills,

and risk tolerance;

limited curation

PaaS

Requires little

assembly and fewer

skills; stronger

curation

© 2016 Forrester Research, Inc. Reproduction Prohibited 15

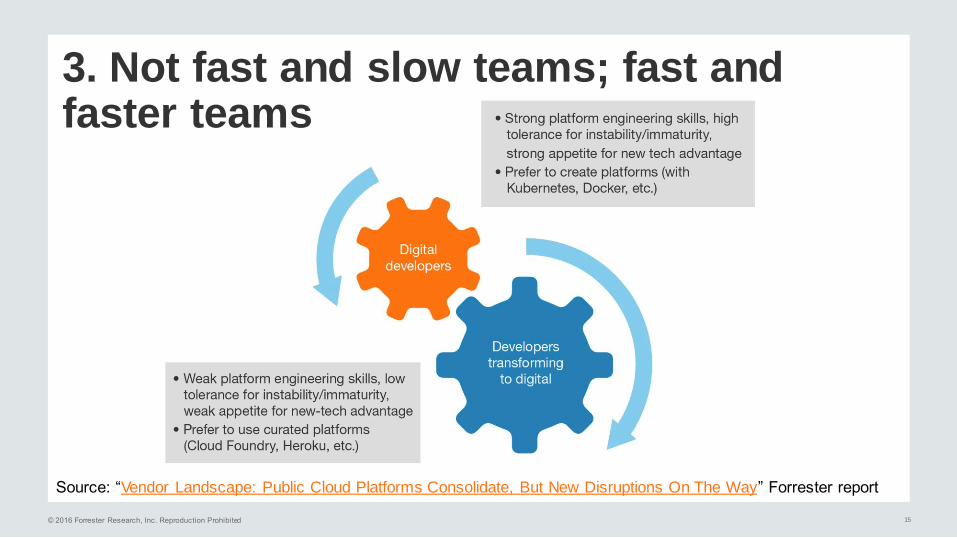

Source: “Vendor Landscape: Public Cloud Platforms Consolidate, But New Disruptions On The Way” Forrester report

3. Not fast and slow teams; fast and faster teams

© 2016 Forrester Research, Inc. Reproduction Prohibited 16

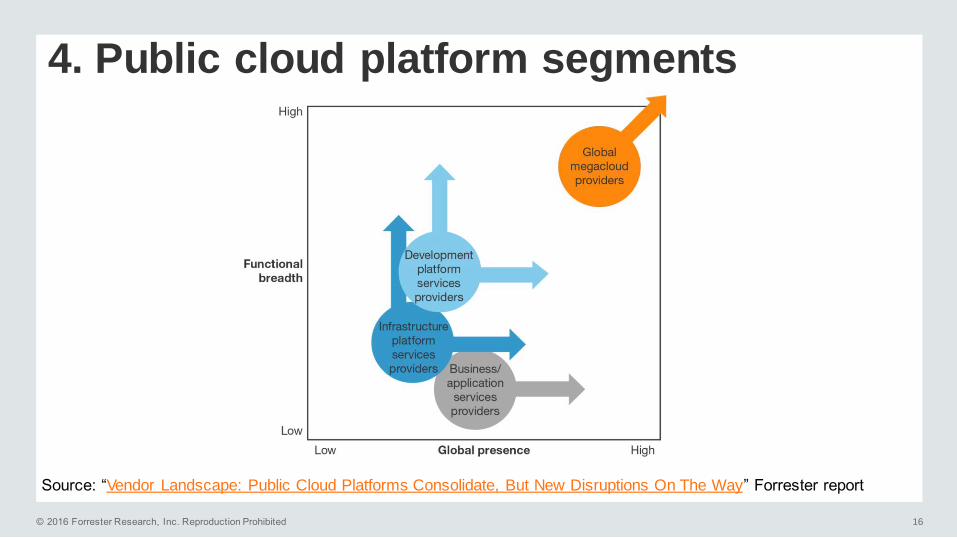

4. Public cloud platform segments

Source: “Vendor Landscape: Public Cloud Platforms Consolidate, But New Disruptions On The Way” Forrester report

© 2016 Forrester Research, Inc. Reproduction Prohibited 17

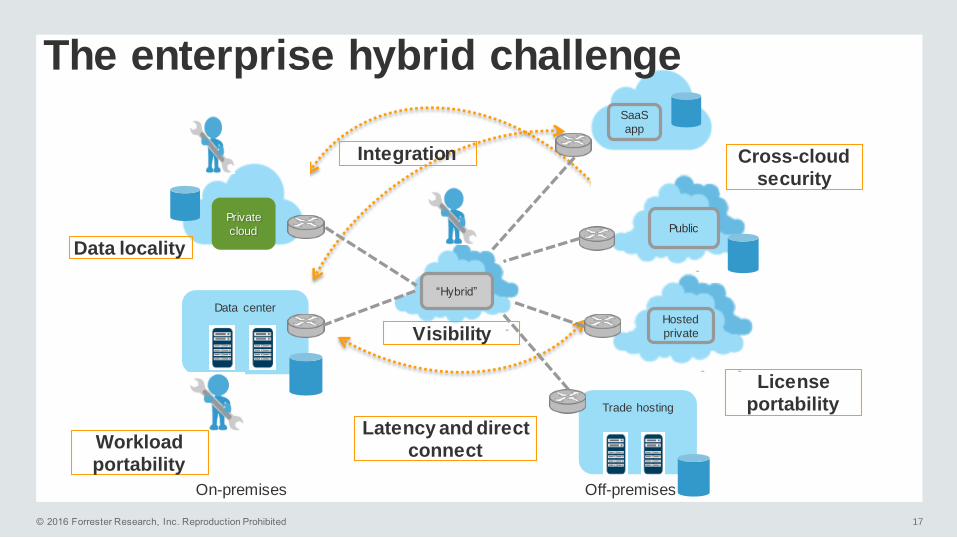

The enterprise hybrid challenge

Hosted

private

Trade hosting

Public

SaaS

app

Private

cloud

“Hybrid”

Data center

On-premises Off-premises

Integration

Visibility

Cross-cloud security

License portability

Workload portability

Data locality

Latency and direct connect

© 2016 Forrester Research, Inc. Reproduction Prohibited 18

How Forrester tracks the public cloud

› Cloud applications (SaaS) — complement + replacement

• CRM, eCommerce, ePurchasing SaaS $ > traditional licensing/maintenance $

• NetSuite, O365, Salesforce, Workday, many others

› Cloud platforms (IaaS/PaaS) — complement + replacement

• Publicly available platforms on which developers build and deploy apps

• Amazon Web Services, CenturyLink, Google, IBM, Microsoft Azure, Oracle

› Cloud business services (cloud “middleware”)

• Targeted solutions for certain business needs, extensible by developers — fill gaps in large

vendor portfolios, target niche needs, and bridge multiple cloud services

• DBaaS (SQL, NoSQL), integration/IoT, file (Box), communications (Twilio), DRaaS, etc.

© 2016 Forrester Research, Inc. Reproduction Prohibited 19

The Forrester Wave™: Global Public Cloud Platforms For Enterprise Developers, Q3 2016

›We required each vendor to offer:

• Native development services (PaaS)

• Some degree of configurable infrastructure services

(IaaS), exposed directly or via PaaS

›We did not evaluate IaaS-only providers.

© 2016 Forrester Research, Inc. Reproduction Prohibited 20

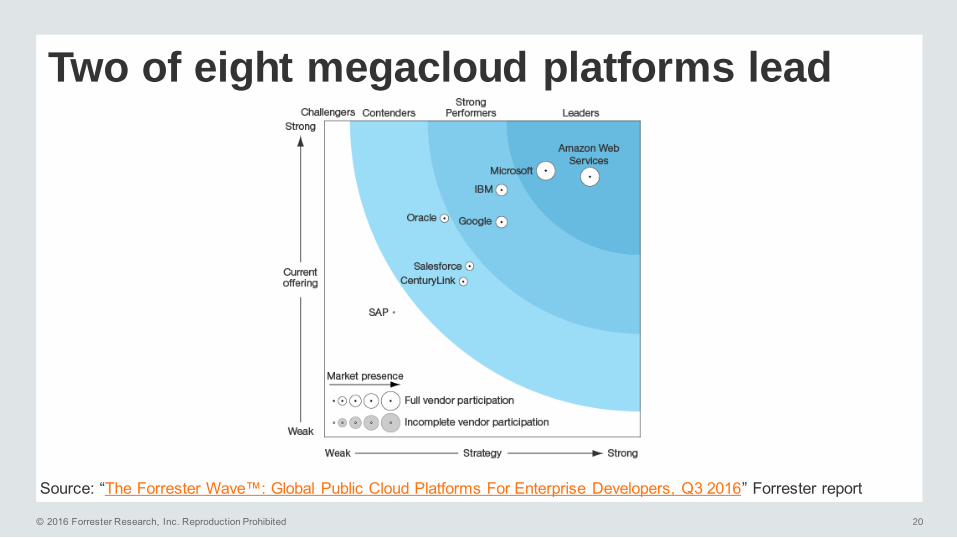

Two of eight megacloud platforms lead

Source: “The Forrester Wave™: Global Public Cloud Platforms For Enterprise Developers, Q3 2016” Forrester report

© 2015 Forrester Research, Inc. Reproduction Prohibited 21

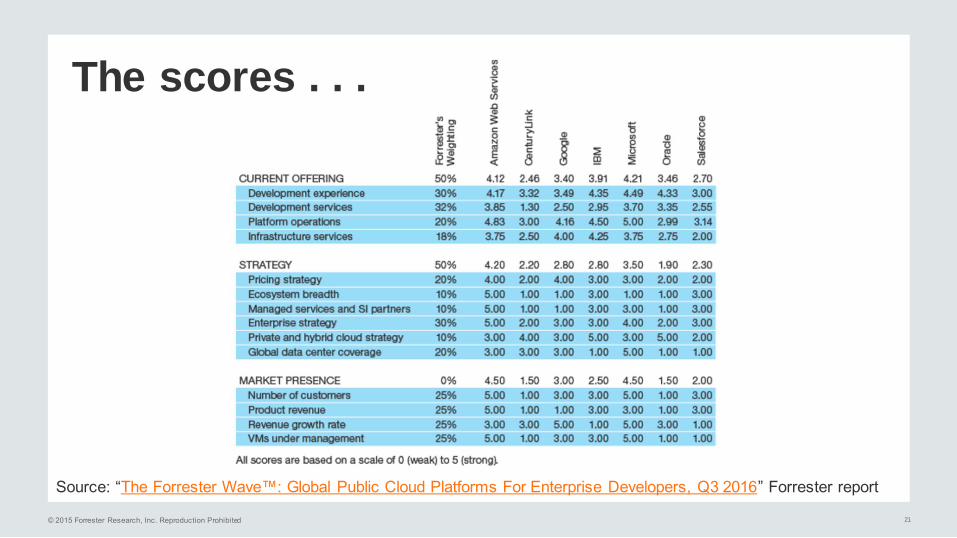

Source: “The Forrester Wave™: Global Public Cloud Platforms For Enterprise Developers, Q3 2016” Forrester report

The scores . . .

© 2016 Forrester Research, Inc. Reproduction Prohibited 22

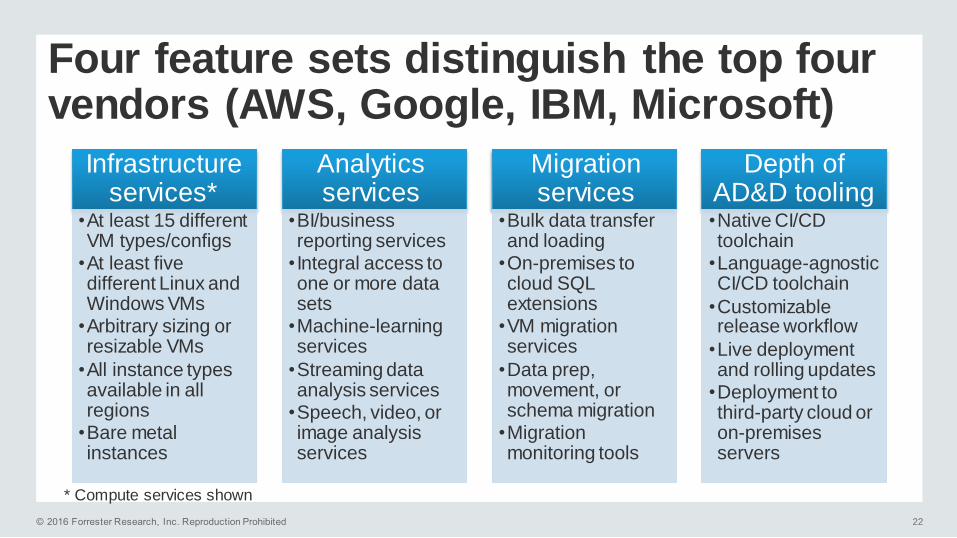

Four feature sets distinguish the top four vendors (AWS, Google, IBM, Microsoft)

Infrastructure services*

•At least 15 different VM types/configs

•At least five different Linux and Windows VMs

•Arbitrary sizing or resizable VMs

•All instance types available in all regions

•Bare metal instances

Analytics services

•BI/business reporting services

• Integral access to one or more data sets

•Machine-learning services

•Streaming data analysis services

•Speech, video, or image analysis services

Migration services

•Bulk data transfer and loading

•On-premises to cloud SQL extensions

•VM migration services

•Data prep, movement, or schema migration

•Migration monitoring tools

Depth of AD&D tooling•Native CI/CD toolchain

•Language-agnostic CI/CD toolchain

•Customizable release workflow

•Live deployment and rolling updates

•Deployment to third-party cloud or on-premises servers

* Compute services shown

© 2016 Forrester Research, Inc. Reproduction Prohibited 23

What it means: innovation and consolidation in parallel

› Portability will only get stronger.

› Infrastructure platform vendors must move up.

› Development platform vendors will grow.

› Business/application services will get acquired.

› Innovation will come from specialists.

© 2016 Forrester Research, Inc. Reproduction Prohibited 24

Is Europe any different?

›Scale matters in Europe too.

• We see the same Leaders here as overseas.

›Next-gen apps need both IaaS and PaaS.

• Many home-grown European IaaS providers proving slow to

add credible PaaS offerings.

› ‘Europe’ is less coherent than it pretends.

• Customers like data centers in-country

• And an option to go on-premises always helps.