CARAVEL MINERALS LIMITED Investor Presentation

November 2016. ASX: CVV

For

per

sona

l use

onl

y

Investor Presentation | November 2016 | Page 2

Rapidly advancing Calingiri Copper-MolybdenumProject in W.A.

- Large Resource (April 2016): Maiden JORCMineral Resource estimate released, 1.4Mt Cu

- Scoping Study (June 2016): Confirmed potentialas a low-cost mid-tier producer with low Capexand robust economics

- Tier-1 Partner: Leading international miner FirstQuantumMinerals (FQM:TX)

Bryah “Degrussa” style copper projectexploration program underway near Meekatharra

Management:Experienced,highlyskilledteamandBoard

LowBurn: Oneoftheleanestjuniorminingcompanies

Forward Strategy: Calingiri PFS in H1 2017followed by DFS and construction in late 2018

Company Highlights

For

per

sona

l use

onl

y

Investor Presentation | November 2016 | Page 3

Corporate SnapshotCaravelMineralsMajorShareholders*:

*asof8November2016

BoardandManagement:11.3%

Cash*: $1.5M

Debt*: Nil

SharePrice*: $0.07

12monthsrange: $0.06-$0.15

Avg dailyvolume: 121K

MarketCap(undiluted): A$5M

SharesOutstanding^: 68M

OptionsListed: 0M

Unlisted: 18M

Nov16:PlacementraisedA$1.2m

CKLShun&SLChoy 9.2%

FirstQuantumMinerals 8.8%

NESTORInvestment 5.1%

Eyeon Investments 4.9%

NewsteadHoldings 4.5%

Retzos Investment 4.2%

Waratah/Taylor 3.7%

PoustieGroup 3.7%

HilmerGroup 3.6%

HealyGroup 3.6%

GeoffreyLevy 3.4%

Clarkson’sBoathouse 3.0%

Goldfire Enterprises 2.8%

CorporatePropertyServices 2.4%

Calama Holdings 1.3%

Total– Top15 64.2%For

per

sona

l use

onl

y

50.1%projectequity

Calingiri and First Quantum Minerals

Investor Presentation | November 2016 | Page 4

1. FQMhasa“RightofFirstRefusal”afterobtaininga50.1%equitystake2. Thenotewasconvertedtoshareson8September2015at28.6cashare

FQM- Largeglobalcopperproducer:marketcap~A$8b(FM:TSX).OperatingsevenminesanddevelopingfivebulktonnageprojectsinZambia,Peru,ArgentinaandPanama

Farm-In1st Phase- $1.2m

ü

JVPartner’s1

11/2015 ~9/2016 ~9/2017

Equity$1.7m+Note$0.6m2

ü

Commencefarm-In2nd Phase- +$2.4m

by9/2017

2014/15

For

per

sona

l use

onl

y

Scoping Study1 Key Findings

Investor Presentation | November 2016 | Page 5

• NPV$520maftertax

• IRR23%

• Payback3years

• Netcashflow$1.5b

• Cu710ktLoM(92%Revenue)

• Moly14.5kt(5%)

• SilverandGold(3%)

• FloatConc25%

• Throughput15Mtpa(21Yrs)

• Oretreated310mt

• Recoveries92%

• Stripratio1:1

• Capitalcost$440m

• Opex- Lom$1.50/lb

• Opex– 1st 5Yrs$1.40/lb

• CuUS$2.75/lb(FXA$0.72)

Capex/Opex

Mine/Plant

EconomicsProduction

1 – Prepared by CSA Global Pty Ltd June 2016. Please read in conjunction with disclosures on page 2 andpublic releases available on the ASX

Economics

For

per

sona

l use

onl

y

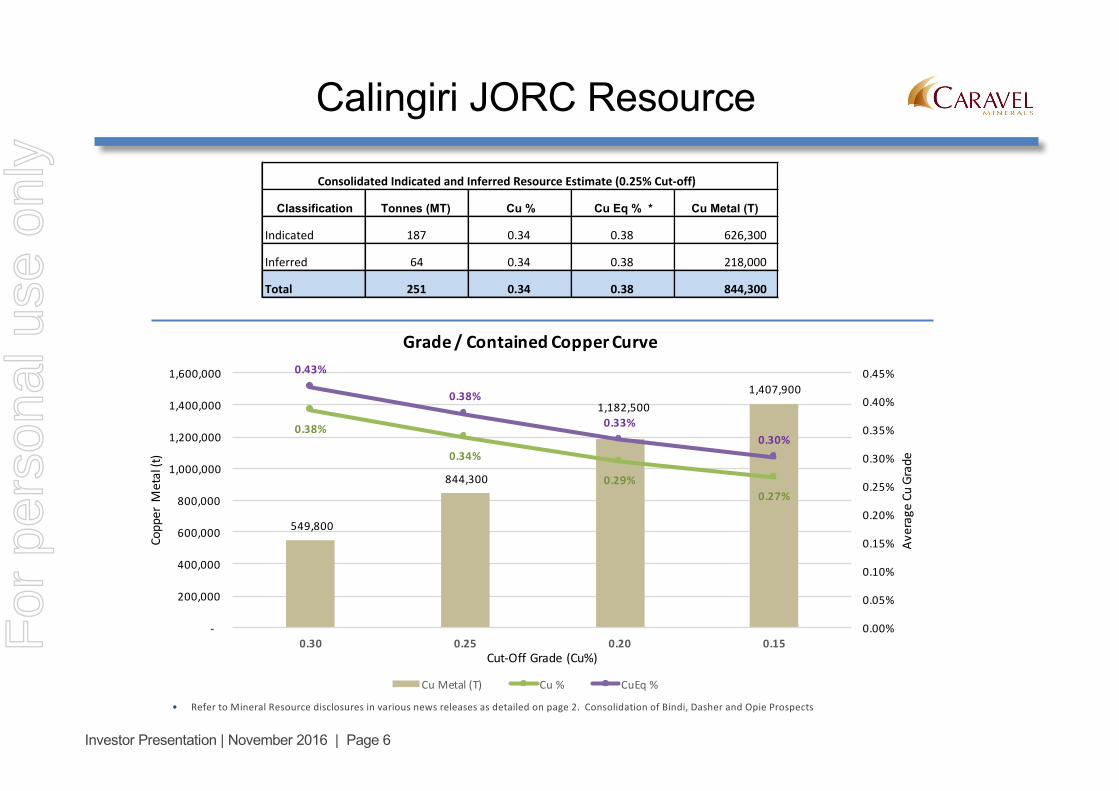

• RefertoMineralResourcedisclosuresinvariousnewsreleasesasdetailedonpage2.ConsolidationofBindi,DasherandOpieProspects

Investor Presentation | November 2016 | Page 6

Broadintersectionsofopencopper-molybdenum-silver-goldmineralisation:Dasher:1,050mlongandopen- extendingtoverticaldepthsof450mBindi:2,000mlongandopen- upto150mthickextendingtoverticaldepthsof300mOpie:300mlongandopen- upto172mthickextendingtoverticaldepthsof200m

549,800

844,300

1,182,5001,407,900

0.38%

0.34%

0.29%0.27%

0.43%

0.38%

0.33%0.30%

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

0.30%

0.35%

0.40%

0.45%

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

0.30 0.25 0.20 0.15

AverageCuGrade

CopperM

etal(t)

Cut-OffGrade(Cu%)

Grade/ContainedCopperCurve

CuMetal(T) Cu% CuEq%

Classification Tonnes (MT) Cu % Cu Eq % * Cu Metal (T)

Indicated 187 0.34 0.38 626,300

Inferred 64 0.34 0.38 218,000

Total 251 0.34 0.38 844,300

ConsolidatedIndicatedandInferredResourceEstimate(0.25%Cut-off)

Calingiri JORC Resource

For

per

sona

l use

onl

y

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

-

5

10

15

20

25

30

35

40

TotalTonnes

TotalTonnesMined

BindiWestStage1 BindiWestStage2 Bindi EastStage1 Bindi EastStage2 DasherStage1 DasherStage2 Opie StripRatio

Scoping Study Mining & Production

Investor Presentation | November 2016 | Page 7

0.000

0.050

0.100

0.150

0.200

0.250

0.300

0.350

0.400

-

5

10

15

20

25

30

35

40

45ProductionCu/Kt- CuGrade

Production Cu/Kt CuEqGrade

For

per

sona

l use

onl

y

Scoping Study Sensitivities

Investor Presentation | November 2016 | Page 8

• Economicoutcomesarerobust

• Mostsensitivetocopperprice

• Breakevenpre-taxNPV7 is$1.98/LbCu

• NotsensitivetoCapex

• LesssensitivetoOpex

$2.20

$2.48$2.75

$3.03$3.30

$530m $490m$440m

$400m $360m

$1.70$1.60

$1.50

$1.40 $1.30

-200.0

0.0

200.0

400.0

600.0

800.0

1000.0

-20% -10% Base 10% 20%

NPVUS

$/M

CuPrice$/lb CapitalCosts$m CashCosts(C1)$/lb

For

per

sona

l use

onl

y

Calingiri Pit Shells

Investor Presentation | November 2016 | Page 9

Bindi oblique with Cu>0.2%

Opie oblique with Cu>0.2%

Dasher oblique with Cu>0.2%

Low cost open pit mining

Low strip ratio: < 1:1

Two major pits situated close to the proposedplantFor

per

sona

l use

onl

y

Investor Presentation | November 2016 | Page 10

CAPEX & Process Plant Flowsheet

Based on a well understood and proven SAG/ball mill circuit

Prepare:MH|Review:ABDR|Approve:DR

COPPERCONCENTRATEFILTER

GYRATORYCRUSHER

CRUSHEDORESTOCKPILE

PEBBLECRUSHER

SAGMILL

SAGDISCHARGE

SCREENS

CYCLONECLUSTERFEED

HOPPER

BALLMILL

CYCLONECLUSTER

COPPERROUGHERFLOATATION(2*6)

CONDITIONER

COPPERCLEANERS COPPER2ndCLEANERS

COPPER3rdCLEANERSCOPPERSCAVENGERS

COPPERCONCENTRATETHICKENER

COPPERCONCENTRATE

PROCESSWATERPOND

TAILSTHICKENERTAILINGSSTORAGE

FACILITY

CONDITIONER

Cu/MoCircuitRougherFloatation

|ConditioningTanks(2)

|1st,2nd,3rdand4thCleaners

|1stand2ndColumnFeed

|MoFilter

|MoDryerandCooler

|BaggedMo

|FinalCuConThickener

|SurgeTank

PRELIMINARY–NOTFORCONSTRUCTION

CaravelMineralsLimitedCalingiriCopperProject

Level3,18RichardsonStreet,WestPerth6005WesternAustralia0894266400

A3|Rev7|Rel0|Pgs1

CapitalItems+/- 30%

Est.CostA$/M

Processplant,firstfill&spares 250

Miningcapital&pre-strip 70

Tailingsdisposal 10

Bulkwatersupply 10

Powersupply&substation 20

Owner’sandotheroutlays 10

EPCM 30

Contingency 40

ProjectCapital 440

Sustainingcapital(LoM) 110

For

per

sona

l use

onl

y

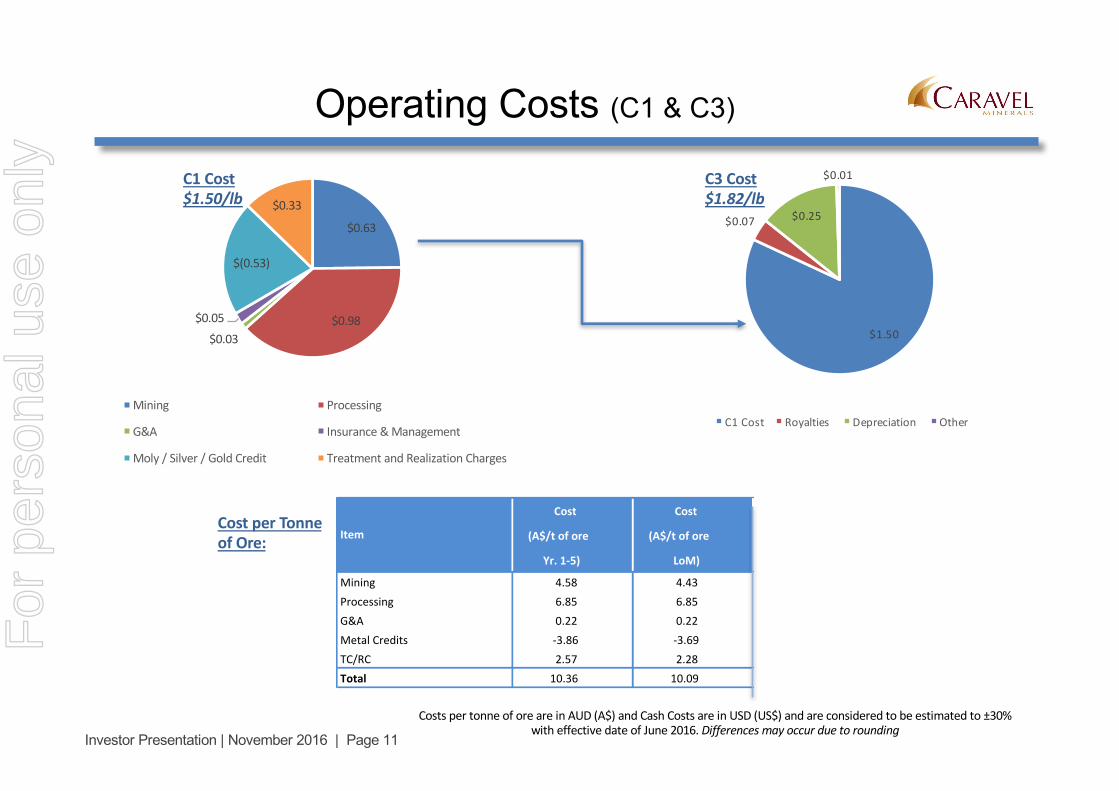

$1.50

$0.07 $0.25

$0.01

C1Cost Royalties Depreciation Other

Investor Presentation | November 2016 | Page 11

Operating Costs (C1 & C3)

CostspertonneoforeareinAUD(A$)andCashCostsareinUSD(US$)andareconsideredtobeestimatedto±30%witheffectivedateofJune2016.Differencesmayoccurduetorounding

Cost Cost Cost Cost %

(A$/tofore (A$/tofore (US$/lbCu (US$/lbCu ofCost

Yr.1-5) LoM) Yr.1-5) LoM)

Mining 4.58 4.43 0.59 0.63 42%Processing 6.85 6.85 0.89 0.98 65%G&A 0.22 0.22 0.07 0.08 6%MetalCredits -3.86 -3.69 -0.50 -0.53 -35%TC/RC 2.57 2.28 0.33 0.33 22%Total 10.36 10.09 1.40 1.50

Item

$0.63

$0.98$0.03

$0.05

$(0.53)

$0.33

Mining Processing

G&A Insurance&Management

Moly/Silver/GoldCredit TreatmentandRealizationCharges

C1Cost$1.50/lb

C3Cost$1.82/lb

CostperTonneofOre:

For

per

sona

l use

onl

y

Infrastructure

Investor Presentation | November 2016 | Page 12

Summary

Area Status

Buildings Buildrequirementsdetailedandcosted üPowerSupply Externalreportcompletedandcosted üWaterSupply

Abundantwaterwithinbothaperchedwatertableandbedrockaquifers.Hydrogeologicalinvestigationsunderway ü

TransportSealedroadsandrailwaylineswithcloseproximitytotheprojectsiteandportslocatedwithinWesternAustraliathataresuitable ü

TailingsManagement Externalreportcompletedandcosted üSiteCommunication

Locatedinafirst-worldhighlydevelopedandpopulatedregionwheretelephoneandhigh-speeddatainfrastructureisinplace üF

or p

erso

nal u

se o

nly

SS:ScopingStudyorPreliminaryEconomicAssessment.PFS:PreliminaryFeasibilityStudy.FS:FeasibilityStudyorDefinitive FeasibilityStudy.BluetextcellsareestimatedasnotmarketreleasedBasedonthereleasedCalingiriScopingStudyJune2016andothercompanydataisfrompubliclyavailableinformation.FulldetailsofCalingirireleasescanbefoundatwww.caravelminerals.com.au.

Investor Presentation | November 2016 | Page 13

GlobalComparableCopperStudies

UnitsCaravel

Minerals Calingiri

Hot Chili Productora

Red Hawk Resources

Copper Creek

Altona Little Eva

Avalon Viscaria

Study SS PFS SS FS SS

Location Australia Chilli USA Australia Sweden

Key FindingsInitial LoM Years 21 12 18 11 8

NPV - pre tax A$M 799 335 231 346 102

- post tax A$M 525 220 154 200 68

- DR % 7.0 7.0 7.5 7.5 7.0

IRR - pre tax % 31% 20% 12% 29% 22%

- post tax % 23% 15% 11% 16% 17%Capital Cost A$M 445 725 857 294 139

Production (LOM)Treatment throughput p.a. 15.0 14.7 8.5 7.0 1.2

Strip ratio t:t 0.9 2.7 4.0 1.8 5.8

Quantity ore treated Mt 310 167 156 77 10

Copper Eq. grade % 0.30% 0.43% 0.74% 0.52% 1.20%

Recoveries Cu % 92% 86% 89% 96% 90%

Cu sold Kt 709 527 950 366 107

Copper price (model input) US$Lb 2.75 3.00 3.00 3.10 3.25

Cash Costs (C1) US$Lb 1.49 1.47 1.85 1.65 1.86

ü

For

per

sona

l use

onl

y

Calingiri Roadmap

Investor Presentation | November 2016 | Page 14

Q22015ExplorationTargets

Q12016DrillingResults

Q12016MaidenResource

Q22016ScopingStudy

H12017Pre-FeasibilityStudy

Nov2016

A history of achieving significant milestones

Delivering on time and within budget

Long-term focus on completing a DFS, obtainingproject finance, construction and commissioning

For

per

sona

l use

onl

y

2.10 2.15

2.60

3.003.35

2016E 2017E 2018E 20189E LTPrice

CUPRICEUSDDriving the recovery with India following

The Smart Money is on Copper

Investor Presentation | November 2016 | Page 15

ChinaGrowth

PriceOutlook

DemandUp

Used in nearly every major industry of the world

SupplyRisks

Production delays, lack of major discoveries and mothballing of projects

LT Forecast US$3.35/lb

Demand by Region: UBS

End Use by Market: AME

Supply by Region: UBS, AMEWBMS

China Copper Demand: UBSAME WBMS

UBS August 2016

For

per

sona

l use

onl

y

Bryah Project

Investor Presentation | November 2016 | Page 16

Bryah (97.5%) is located ~80km north ofMeekatharra – 60km south-west of the DegrussaCopper-Gold Deposit.

Two zones of copper-zinc-gold anomalism, eachabout 2 km long and up to 500m wide. Therecent discovery of the Monty deposit, andexploration results from other explorers focusingon the southern margin of the Bryah Basin,indicate that these copper-zinc-gold anomaliesoverly the interpreted VMS target horizon.

Significantly there are a cluster of vein golddeposits, overlying the same horizon, betweenthese anomalies.F

or p

erso

nal u

se o

nly

A Very High Quality Leadership Team

MARCEL HILMER, CEO and Executive DirectorMr Hilmer is a Fellow of the Institute of Chartered Accountants and a Member of the Australian Institute of Company Directors withmore than 30 years experience in executive management of global public and private groups including 6 years as BusinessDevelopment Executive with First QuantumMinerals Limited and following as CEO of ForsysMetals

ROWENCOLMAN,CFOMr Colman is a Chartered Accountant with over 25 years of senior financial management experience and holds a Bachelor Degree inCommerce. Recently Mr Colman spent time as Development Director for a major sovereign wealth fund in the Middle East managingmultiple development projects globally

TONY POUSTIE, Director of ExplorationMr Poustie is a fellow of the Australian Institute of Mining and Metallurgy. He is a geologist with 47 years international experience inmineral exploration, resource definition, project evaluation and development, and mining. He was General Manager Exploration from1998 until the takeover of Dominion by Kingsgate Consolidated Limited in 2011, when he took on the role of Chief Geologist

GRAHAM KUBALE, ExplorationManagerMr Kubale is a Geologist with over 15 years’ experience in the resources sector, having worked extensively in greenfields and near-mine exploration for a range of gold, base metal and Iron Ore mineralisation styles in Australia, Asia and Canada. Graham spent severalyears at Newmont Mining Corporation, Kingsgate Consolidated and Cliffs Natural Resources. He holds a Bachelor of Applied Science(Geology)

PETER ALEXANDER, Non-Executive DirectorMr Alexander has over 40 years experience in the Australian and international mining and exploration industry. He was ManagingDirector of Dominion Mining Limited for 10 years. Mr Alexander is also Non-Executive Director of the ASX listed company DorayMinerals Limited

JAMES HARRIS, Non-Executive DirectorMr Harris has had extensive experience in both Government and private enterprise in Australia and overseas. He has worked for tenyears with both Alcoa of Australia and the United Group Limited. His qualifications are in Legal Studies and Public Administration andhe is a Fellow of the Australian Institute of Company Directors

Investor Presentation | November 2016 | Page 17

For

per

sona

l use

onl

y

Investor Presentation | November 2016 | Page 18

Strongfundingfarm-inpartner- FQM

Ideallocation–infrastructure– localworkforce

ScopingStudy:Openpitmine– lowcost– lowstrip– robusteconomics

Metallurgicalrecoveries- >90%CuandMo

Nonativetitleandlowenvironmentalrisk

Calingiri Investment Profile

For

per

sona

l use

onl

y

Investor Presentation | November 2016 | Page 19

Corporate and Operations:Marcel Hilmer, CEO orTony Poustie, Dir. Of Exploration

L3, 18 Richardson StreetWest Perth WA 6005+61 8 9426 6400

Corporate Advisors:Bridge Street Capital PartnersTelephone: +61 2 9002 5415

Contact Information

For

per

sona

l use

onl

y

DisclosuresandDisclaimer

Investor Presentation | November 2016 | Page 20

DisclaimerThe presentation materials (and the contents of the presentation) are for information purposes only and do not constitute an offer or invitation to subscribe for or purchase any securities,and neither the presentation materials nor anything contained therein nor the fact of their distribution nor the contents of the presentation shall form the basis of or be relied on inconnection with or act as any inducement to enter into any contract or commitment whatsoever.

The information contained in this presentation is subject to material updating, completion, revision, amendment and verification. No reliance should be placed on the information and norepresentation or warranty (express or implied) is made by the Company, any of their respective directors or employees or any other person, and, save in respect to fraud, no liabilitywhatsoever is accepted by any such person, in relation thereto. The Company does not provide any financial product advice.

Forward-Looking StatementsThis presentation includes certain statements that may be deemed “forward-looking statements”. All statements in this presentation, other than statements of historical facts, thataddress future production, reserve or resource potential, exploration drilling, exploitation activities and events or developments that Caravel Minerals Limited (the “Company”) expects tooccur, are forward-looking statements.

Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of futureperformance and actual results or developments may differ materially from those in the forward-looking statements. The ability of any person to achieve forward-looking production andeconomic targets is dependent on numerous factors that are beyond the Company’s control and that Caravel cannot anticipate. These factors include, but are not limited to, site-specificmining and geological conditions, management and personnel capabilities, availability of funding to properly operate and capitalize the operation, variations in cost elements and marketconditions, developing and operating the mine in an efficient manner, unforeseen changes in legislation and new industry developments. Any of these factors may substantially alter theperformance of any mining operation.

Investors are cautioned that any such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in the forward-looking statements. Readers should not place undue reliance on forward-looking information. The Company does not assume any obligation to update or revise its forward-lookingstatements, whether as a result of new information, future events or otherwise.

Competent Person StatementThe information in this report that relates to the Calingiri Mineral Resource estimates is extracted from an ASX Announcement dated 4 April 2016, (see ASX Announcement – 4 April 2016“Calingiri Maiden JORC Resource”, www.caravelminerals.com.au and www.asx.com.au ). The Company confirms that it is not aware of any new information or data that materially affectsthe information included in the original market announcement and that all material assumptions and technical parameters underpinning the Mineral Resource estimates in the relevantmarket announcement continue to apply and have not materially changed. The Company confirms that the form and context in which the Competent Person’s findings are representedhave not been materially modified from the original market announcement.

Production Targets and Financial InformationInformation in relation to the Calingiri Project Scoping Study , including production targets and financial information, included in this report is extracted from an ASX Announcement dated28 June 2016, (see ASX Announcement – 28 June 2016, “Scoping Study Confirms Outstanding WA Copper Project ”, www.caravelminerals.com.au and www.asx.com.au. The Companyconfirms that all material assumptions underpinning the production target and financial information set out in the announcement released on 28 June 2016 continue to apply and havenot materially changed.

For

per

sona

l use

onl

y

Investor Presentation | November 2016 | Page 21

Projects Status Target Location Holding Area(km2)

CALINGIRI Granted Copper,Gold,Molybdenum WA,Australia 16tenements– 100%

1tenement– 80% 760

BRYAH Granted Copper,Gold,Manganese WA,Australia 1tenement – 92.5% 123

Appendix

AustralianPortfolio

Options:November2016

Status Mn ExercisePrice ExpiryDate

Unlisted 3.80 $0.77 31/12/16

““ 5.26 $0.29 31/01/17

““ 0.20 $0.17 31/01/17

““ 8.80 $0.12 31/12/18

Total 18.06For

per

sona

l use

onl

y