Download - Foley’s M&A Briefing Series

1

1

©2009 Foley & Lardner LLP • Attorney Advertising • Prior results do not guarantee a similar outcome • Models used are not clients but may be representative of clients • 321 N. Clark Street, Suite 2800, Chicago, IL 60654 • 312.832.4500

Foley’s M&A Briefing SeriesAn Exchange to Power Your M&A Deals

For Audio Participation, Please Call 1.866.283.8243, pass code *1349975*

2

©2009 Foley & Lardner LLP

Distressed M&A: Issues and Opportunities

12 p.m. – 1:30 p.m. Central April 28, 2009

Steven H. Hilfinger Daljit S. Doogal Geoffry S. Goodman Alexander Tracy

2

3©2009 Foley & Lardner LLP

Housekeeping Issues

Call 866.493.2825 for technology assistanceDial *0 (star/zero) for audio assistanceAmple time for Q & A will be allotted at the end of the formal presentation

– Pull Down Menu

We encourage you to Maximize the PowerPoint to Full Screen Usage:

– Hit F5 on your keyboard; or

– Select “View” from the toolbar menu and click “Full Screen”

To print a copy of this presentation:– Click on the printer icon in the lower right hand corner

– Convert the presentation to PDF and print as usual

4©2009 Foley & Lardner LLP

Today’s Presenters

Steven H. HilfingerFoley & Lardner LLP

Geoffrey S. GoodmanFoley & Lardner LLP

Daljit S. DoogalFoley & Lardner LLP

Alexander TracyMiller Buckfire & Co.

3

5©2009 Foley & Lardner LLP

Topics We Will Address

M & A/Distressed M & A Market Update

Structuring Alternatives – Distressed Sales– – Inside vs. Outside of Bankruptcy

– – Bankruptcy: Section 363 vs. Plan of Reorganization

Perspectives of Buyers, Sellers, Creditors and Others in Distressed Sales in Bankruptcy

Cash Management and DIP Financing Issues

Purchase Agreement Issues

Questions and Answers

6©2009 Foley & Lardner LLP

M & A/Distressed M & A Market Update

4

7©2009 Foley & Lardner LLP

Global Announced M&A VolumeAnnounced M&A Transaction Volume(1)

___________________________________(1) Source: Thompson Financial(2) 2009 Year-To-Date as of April 21, 2009

$0

$1

$2

$3

$4

$5

$6

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Volume ($tm)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

# of Deals (000s)

Volume Number of Deals

8©2009 Foley & Lardner LLP

Global Announced Market Volume by Target Industry

2008 - $3.1 Trillion 2009 YTD - $0.6 Trillion

23.6%14.9%

13.7%

6.4%4.4%

4.3% 3.9%

28.7%

TechnologyHealthcare

FinancialsEnergy and Power

Industrials

Consumer Staples

Real EstateMedia & Telecommunications

22.2%6.2%

7.0%

7.1%

11.1%

12.1%

15.9%

18.4%

Technology

Healthcare Financials

Energy and Power

Industrials

Consumer

Media &Telecommunication

Real Estate

5

9©2009 Foley & Lardner LLP

Leveraged Loan Issuance(1)

___________________________________(1) Source: S&P LCD.

New-Issue Leveraged Loan Volume Institutional New-Issue Spreads

YTD Institutional New-Issue Volume Single B Secondary Trading Spreads

150

250

350

450

Dec-00 Nov-01 Oct-02 Sep-03 Aug-04 Jul-05 Jun-06 May-07 Apr-08 Mar-09

BB/BB- Spreads B+/B Spreads

Spread over Libor (bps)

BB+/BB/BB-, 3.1%

Split BB/B, 2.6%

Split BBB/BB, 8.8%

Not Rated, 85.5%

2,505

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

3500.0

Mar-07 Aug-07 Jan-08 Jun-08 Nov-08 Mar-09

Spread over Libor (bps)

139105 74

112 112159 149

8222

46

34 59 91

183

321387

71

24818

153

3$11

$153

$535

$480

$295$265

$166$139$139

$185

$46

$0

$100

$200

$300

$400

$500

$600

2000 2001 2002 2003 2004 2005 2006 2007 2008 1Q08 1Q09

$ in billions

Pro Rata Institutional

10©2009 Foley & Lardner LLP

Institutional Loans by Type(1)

1Q09 Institutional Loans by Type1Q08 Institutional Loans by Type

___________________________________(1) Source: S&P LCD.

LBO45%

Other4%DIP

2%Refinancing

5%

M&A (non-LBO)23%

Exit Financing21%

Total: $26 billion

Exit Financing 11%

Refinancing5%

DIP74%

Corp Purpose10%

Total: $3 billion

Bankruptcy-related financing represented 85% of new issue-volume during 1Q 2009

6

11©2009 Foley & Lardner LLP

Key Trends in Today’s M&A Market

Three principal M&A trends dominate the current market:

Default rates / Bankruptcies increase– Economy and business model failures– Capital structure and liquidity crises– Rescue sales and financings

Constrained companies forced to de-lever– Business restructurings and recapitalizations– Spin-offs / Split-offs / Carve-outs– Divestitures of non-core assets

Unconstrained companies “on the move”– Valuation declines create opportunistic buying– Unique opportunity for strategic acquisitions– Scale and synergies to weather currently lower earnings

12©2009 Foley & Lardner LLP

Default Rates Update

The default rate increased sharply during 1Q 2009 and is expected to double during 2009

The U.S. speculative grade default rate reached 5.7% on an issuer-basis at the end of February 2009, and 7.6% on a dollar-volume basis, nearly 8 times where it stood a year ago

Moody’s predicts that the U.S. speculative grade default rate will increase to 13.8% on an issuer basis by the end of 2009(1)

The default rate for leveraged loans rose to 4.79% on an issuer-basis and 8.02% on a dollar volume basis at February 2009

Trailing 12-Month Leveraged Loan Default Rates(3)Moody’s Speculative Grade Default Rates(2)

0%

1%

2%

3%

4%

5%

6%

Jul-05 Feb-06 Sep-06 Apr-07 Jan-08 Aug-08 Mar-09

Default Rate (Issuer Basis)

Issuer-Weighted Default Rates

___________________________________(1) Based on latest Moody’s predictions as of March 20, 2009. (2) Moody’s Global Credit Research, March 2009. Trailing 12-month speculative grade default rate equals the number of issuers defaulting on Moody’s rated debt divided by the number

of issuers that potentially could have defaulted on Moody’s-rated debt, adjusted to reflect the withdrawal from the market of some of those issues.(3) Source: S&P LCD.

0%

4%

8%

12%

16%

Oct-05

Aug-06

Jun-07

Apr-08

Feb-09

Dec-09

Actual Forecast

7

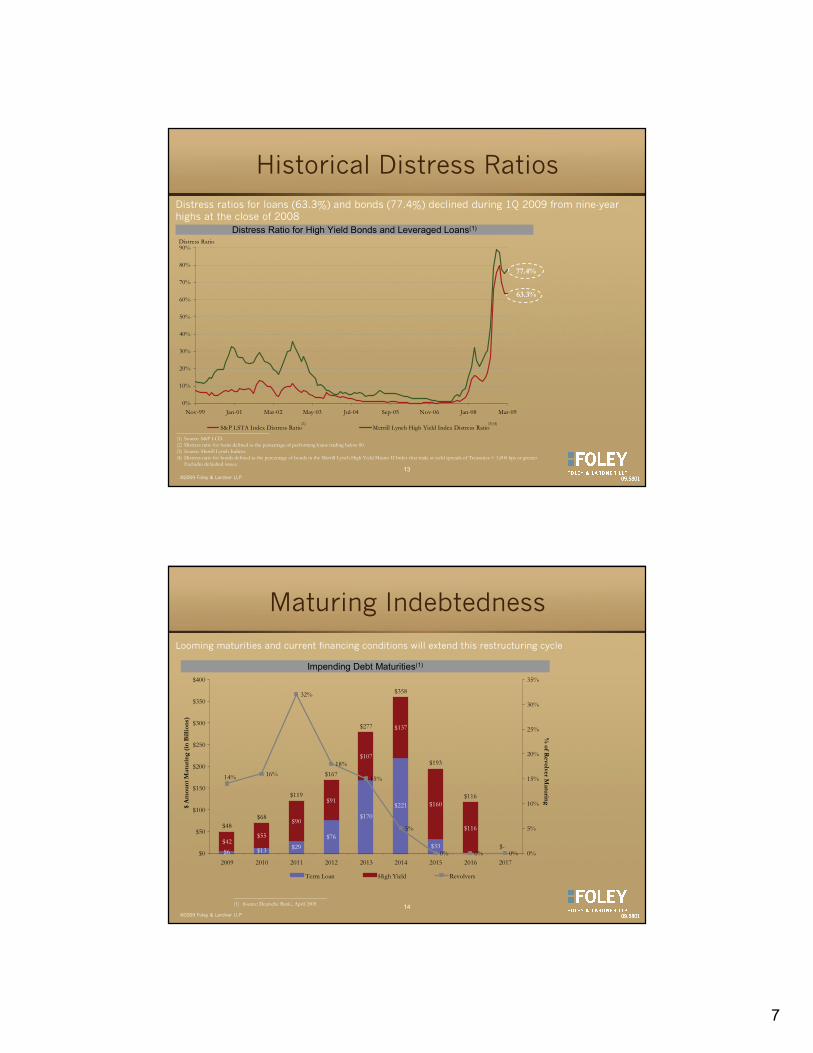

13©2009 Foley & Lardner LLP

Historical Distress Ratios

___________________________________(1) Source: S&P LCD.(2) Distress ratio for loans defined as the percentage of performing loans trading below 80.(3) Source: Merrill Lynch Indices. (4) Distress ratio for bonds defined as the percentage of bonds in the Merrill Lynch High Yield Master II Index that trade at yield spreads of Treasuries + 1,000 bps or greater.

Excludes defaulted issues.

Distress Ratio for High Yield Bonds and Leveraged Loans(1)

63.3%

77.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Nov-99 Jan-01 Mar-02 May-03 Jul-04 Sep-05 Nov-06 Jan-08 Mar-09

Distress Ratio

S&P LSTA Index Distress Ratio Merrill Lynch High Yield Index Distress Ratio(2) (3)(4)

Distress ratios for loans (63.3%) and bonds (77.4%) declined during 1Q 2009 from nine-yearhighs at the close of 2008

14©2009 Foley & Lardner LLP

Maturing Indebtedness

Impending Debt Maturities(1)

___________________________________(1) Source: Deutsche Bank., April 2009.

Looming maturities and current financing conditions will extend this restructuring cycle

$6 $13 $29$76

$170

$221

$33$42

$55

$90

$91

$107

$137

$160

$116$48$68

$119

$167

$277

$358

$193

$116

$-

16%

32%

18%

15%

5%

0% 0% 0%

14%

$0

$50

$100

$150

$200

$250

$300

$350

$400

2009 2010 2011 2012 2013 2014 2015 2016 2017

$ A

mou

nt M

atu

rin

g (i

n B

illio

ns)

0%

5%

10%

15%

20%

25%

30%

35%

% of R

evolver Matu

ring

Term Loan High Yield Revolvers

8

15©2009 Foley & Lardner LLP

Completed Date Target Acquiror

Value ($ Bln)

2006 Adelphia Communications Corp. Time Warner Inc. / Comcast Corp. $17.6

2009 IndyMac Federal Bank OneWest Bank Group LLC 13.9

2 2007 Yukos Corporation (Certain Assets) Rosneft Oil Company 6.8

3 2001 Trans World Airlines, Inc. AMR Corp. 4.2

4 2002 Budget Group, Inc. Cendant Group 3.1

5 2004 CrossCountry Energy LLC (Enron Corp.) General Electric Co. / Southern Union Co. 2.5

6 2003 ANC Rental Corp. Cerberus Capital Management LP 2.4

2008 Washington Mutual Bank FSB J.P. Morgan Chase & Co 1.9

7 2003 Bethlehem Steel Corp. International Steel Group, Inc. 1.5

8 2005 Refco, Inc. Man Group plc 1.3

2008 Lehman Brothers Inc. Barclays Bank plc 1.3

9 2007 Tower Automotive Cerberus Capital 1.1

0 2004 Pegasus Satellite Comm., Inc. (Broadcast Satellite Assets)

DirecTV Group, Inc. 1.0

Notable Bankruptcy Related M&A Deals(1)

___________________________________(1) Source: Bankruptcy Insider

16©2009 Foley & Lardner LLP

Structuring Alternatives –Acquiring Distressed Assets

9

17©2009 Foley & Lardner LLP

Distressed Companies – Sale Options

A distressed company typically faces three options when it contemplates a sale of its assets:

– The company may sell its assets as part of a conventional transaction outside of bankruptcy

– The company may enter chapter 11 and pursue a sale of assets pursuant to Section 363 of the Bankruptcy Code

– The company may enter chapter 11 and seek to sell its assets as part of a Plan of Reorganization

18©2009 Foley & Lardner LLP

Advantages

DisadvantagesSubject to higher and better offers (buyer may be used

as a “stalking horse”)Auction procedures will be imposedBankruptcy Courts are often sympathetic to the Debtor

in the event of a dispute with the buyerMultiple constituencies have a voice in the case and

may delay or impede the sales process.Representations and warranties of the Debtor rarely

survive the closingPurchase Agreement may be limited or non-existentBreak-up fee or expense reimbursement provisions

may not be approved by the Bankruptcy Court in the amounts requested

The buyer may be deemed not to have standing to be heard in the bankruptcy case absent a direct impact on its rights

No benefit of a court order that the sale is free and clear of all liens and claims

Assumption or rejection of certain leases and contracts may be difficult or impossible

No protection against fraudulent transfer or preference challenges

No accessible forum to enforce rights without significant procedural hurdles

The Debtor’s assets can be acquired free and clear of liens and claims

The Debtor may assume and assign existing contracts and leases

Transaction can be consummated over creditor objections

Avoids risk of the transactions being characterized as a fraudulent transfer or a preference

Minimizes any risk of successor liabilityThe buyer has a convenient and accessible forum to

enforce its rights (i.e., the Bankruptcy Court)The process is typically transparent

Speed and flexibility determined by buyer and sellerDoes not necessarily require competitive biddingImmediate distribution of proceeds to stakeholdersMay avoid unnecessary disclosure and costsAbility to preserve value for equity holdersRepresentations and warranties of the seller can

survive the closing

In-Court (Bankruptcy)Out-of-Court

Distressed M&A Alternatives

10

19©2009 Foley & Lardner LLP

Out-of-Court Sales

Major issues with out-of-court sales include:– Timing pressures– “Fire sale” valuation concerns

Cash maximization vs. mortgaging future earningsRetained liabilities

– Buyer’s comfort with seller indemnifications– Fraudulent conveyance

Will seller inevitably end up in bankruptcy?“Reasonably equivalent value” test (i.e., is the buyer paying a fair price for the assets)Is the seller insolvent?

– Successor liability concerns– Dealing with prior lienholders

Will proceeds be sufficient to pay secured debt?UCC Article 9 sales

20©2009 Foley & Lardner LLP

In-Court Sales

Significant considerations for in-court sales include:

– Form of consideration

– “Highest and best” standard

– Timing: 363 vs. Plan of Reorganization sale

– Creditor involvement and participation

11

21©2009 Foley & Lardner LLP

Section 363 Sale vs. Plan

For sales in bankruptcy, a significant decision is whether to pursue a transaction through a “Section 363 sale”or through a sale pursuant to a chapter 11 Plan of Reorganization or Liquidation

22©2009 Foley & Lardner LLP

Section 363 Sales

Process– The Debtor files a motion to approve the sale

in the Bankruptcy Court pursuant to Section 363 of the Bankruptcy Code

– Auction procedures govern the marketing of the Debtor’s assets and competitive bidding

– All creditors receive notice and an opportunity to object and be heard, but do not vote on the proposed sale

12

23©2009 Foley & Lardner LLP

Section 363 Sales (cont’d)

Advantages to Section 363 SalesNeed for Speed

– Section 363 sales can proceed much faster than a chapter 11 Plan process

– Not uncommon to have Section 363 sales consummated in 45-75 days from the filing of the sale motion

Sale Over Creditor Objections – The sale can be consummated over creditor objectionsLower Standard for Approval – The various requirements in the Bankruptcy Code for confirming a Plan need not be satisfied

24©2009 Foley & Lardner LLP

Section 363 Sales (cont’d)

Disadvantages to Section 363 SalesReluctance of Some Courts

– Some Bankruptcy Courts are reluctant to allow sales of substantially all of the Debtor’s assets outside of a Plan

– More common concern in jurisdictions not used to “mega” chapter 11 cases

Obstacles to Consensus Building – More difficult to direct the use of the sale proceeds in order to build consensus among chapter 11 constituencies

13

25©2009 Foley & Lardner LLP

Chapter 11 Plan Sales

Process– The Debtor proposes to sell its assets as part of a

chapter 11 Plan of reorganization or liquidation filed in the Bankruptcy Court

– Auction procedures continue to govern the marketing of the Debtor’s assets and competitive bidding, with the sales process proceeding concurrently with the Plan confirmation process

– Creditors have the ability to vote to accept or reject the Plan (and thus the sale)

– Approval of the sale is dependent on confirmation of the underlying Plan

26©2009 Foley & Lardner LLP

Chapter 11 Plan Sales (cont’d)

Advantages to Sales Under a PlanFlexibility

– More flexibility in terms of form and timing of consideration

– Can help build consensus among constituencies in chapter 11 and result in a consensual deal

Comfort of Court – May provide more comfort to the Bankruptcy Court in approving the sale, particularly if the sales price is less than the amount of the Debtor’s senior secured debtNo Securities Registration – No need to register securities issued under the Plan

14

27©2009 Foley & Lardner LLP

Chapter 11 Plan Sales (cont’d)

Disadvantages to Sales Under a PlanSlow Process

– The Plan confirmation process is time consuming – Both a disclosure statement (explaining the Plan) and the Plan itself

must be approved– Delays are virtually inevitable– Costs increase as the process drags on– Delays may be used strategically by the Debtor and other constituencies

to pursue refinancing options while keeping the buyer “locked up”

Higher Standard for Approval – In order to consummate the sale, the Debtor must satisfy all elements required under the Bankruptcy Code to confirm a Plan

Creditors Vote – Creditors have the right to vote on the sale as part of the Plan solicitation process

28©2009 Foley & Lardner LLP

Perspectives of Buyers, Sellers, Creditors and Others in Distressed Sales in Bankruptcy

15

29©2009 Foley & Lardner LLP

Buyer Perspectives

Assets to be acquired and liabilities to be assumed

Due diligence

Financing considerations

Purchase price and adjustments

Escrows/other protections

Contract assumption issues/cure costs

Representations and warranties

Exclusivity

Funding of costs and break-up fees

30©2009 Foley & Lardner LLP

Seller Perspectives

Scope of the transaction and assumption of liabilities

Timing

Consideration requirements

Representations and warranties and survival post-closing

Carve-out or transition issues

Certainty of closing

16

31©2009 Foley & Lardner LLP

Secured Creditor Perspectives

Speed – Request that the sale proceed as expeditiously as reasonably possible in order to avoid diminution in value of their liens and minimize costs expended funding the chapter 11 case

Focus on Stalking Horse – Substantial effort focused on locking in a “floor”of value through stalking horse bid

Get Paid at Closing – “Cash is king” and secured creditors often demand that the buyer transfer the purchase price directly to them at closing

Auction Procedures – Attempt to maintain voice in the auction process (i.e., not ceding total authority to the Debtor)

“It’s our Money” – Attempt to minimize consideration payable to other constituencies

32©2009 Foley & Lardner LLP

Unsecured Creditor Perspectives

Creditors’ Committee – Principal unsecured creditor voice in chapter 11 is the Official Committee of Unsecured Creditors

Stretch out the Process– The Committee often is in favor of a longer marketing/sales process in order to “kick the

tires” and try to generate additional value– Alternative bids or refinancing options always being explored

Aggressive Opposition to Unsatisfactory Bids– The Committee will typically fight break-up fees, expense reimbursements and other stalking

horse protections if the bid does not put unsecured creditors “in the money”– If not brought “on board” with the deal, the Committee will oppose the sale throughout the

process

Opposition to Lingering Liabilities– Unsecured creditors will strongly oppose any potential post-closing adjustments to the

purchase price – Take position that representations and warranties should not survive closing

17

33©2009 Foley & Lardner LLP

Other Perspectives

Customers– Are customers supporting the sale?

– Does the business meet a critical business need?

– What resourcing or other customer alternatives available?

Suppliers– Are suppliers being paid on a current basis?

– Will the suppliers do business with buyer, and on what terms?

– What is status of A/P and what funding requirements at closing?

Management and Employees– Is management stable or at risk?

– What retention or incentive programs are in place/should be?

– Any union, WARN Act or other employment issues to consider?

34©2009 Foley & Lardner LLP

Cash Management and DIP Financing Issues

18

35©2009 Foley & Lardner LLP

Managing Cash Pre-Bankruptcy

Selective payment of outstanding payables

Avoiding termination of contracts

Managing UCC Section 2-609 demands

Consider defensive draw under existing credit facility if no current defaults and borrowing availability exists

36©2009 Foley & Lardner LLP

Using Cash in Bankruptcy

Pre-bankruptcy liens do not continue in property acquired after the bankruptcy except as to proceeds of property subject to such prepetition liens (e.g. A/R, cash)

“Cash collateral” means cash, negotiable instruments, documents of title, securities, deposit accounts, or other cash equivalents subject to a lien

A debtor cannot use cash collateral post-petition without (i) the consent of the creditor who has a lien on such cash, or (ii) a court order entered after notice and hearing

19

37©2009 Foley & Lardner LLP

Using Cash in Bankruptcy (cont’d)

The lender with an interest in the cash can request that the court condition or prohibit the use of cash collateral as is necessary to provide the lender “adequate protection” for the interest in the cash

Adequate protection can be cash payments, a replacement lien, an equity cushion or other “indubitable equivalent”

Because debtors need cash immediately, hearings are held for interim relief (amounts required to be used to avoid immediate and irreparable harm)

38©2009 Foley & Lardner LLP

DIP Financing

Cash collateral is unlikely to fully meet a debtor’s needs during its chapter 11

The debtor might need additional financing to continue operating its business and preserve going concern value of the company for secured and other creditors

As such, the Bankruptcy Code contains provisions that might serve to entice lenders to offer financing in bankruptcy

20

39©2009 Foley & Lardner LLP

DIP Financing (cont’d)

Unsecured Credit– Unsecured credit in the ordinary course of business is

permitted, with repayment to be given administrative expense priority under 11 U.S.C. § 364(a) (e.g. trade debt)

Obtaining Credit on a Superpriority or Secured Basis– If the debtor is unable to obtain unsecured credit as an

administrative expense, the court may authorize the obtaining of credit or the incurring of debt

With superpriority over other administrative expense claims;Secured by a lien on unencumbered property; orSecured by a junior lien on encumbered property

– The debtor must be able to demonstrate that it has reasonably attempted, and failed, to obtain the credit on an unsecured basis (or without superpriority status)

40©2009 Foley & Lardner LLP

Selected Recent DIP PricingCOMPANY

FILING

DATE LENDER(S) /

AGENT DIP STRUCTURE MATURITY INTEREST RATE FEE(S)

4/20/09 GE Capital $63 million new money revolver $102 million new money TL

12 months L+1200 bps (LIBOR floor of 3.25%)

Upfront fee: 4.0% Administrative fee: $200,000

4/16/09 Pershing Square

Capital Management

$375 million new money TL 18 months

L+1,200 bps (LIBOR floor of 3.0%) Warrants: 4.9% of fully-diluted post-reorganization equity

Upfront fee: 4.0% Exit fee: 3.0%

3/20/09

Barclays

$75 million ABL revolver $150 million TL

12 months L+600 bps (LIBOR floor of 3.0%) L+600 bps (LIBOR floor of 3.0%)

Undisclosed

3/18/09 Citigroup $86.5 million roll-up revolver $63.5 million new money revolver $250 million new money TL

12 months L+350 bps L+750 bps L+750 bps

New money upfront fee: 3.0% New money exit fee: 3.0% Roll-up exit fee: 2.0%

3/11/09 GE Capital

Avenue Capital / DDJ Capital

$55 million roll-up ABL revolver $80 million TL 6 months

L+600 bps (LIBOR floor of 3.0%) L+1,500 bps (LIBOR floor of 4.00%)

Unused line: 100 bps Backstop fee: 4.0% Unused line: 300 bps

2/19/09 Deutsche Bank / Bank of America

$575 million roll-up ABL $500 million roll-up TL $500 million new money TL

12 months L+650 bps (LIBOR floor of 3.0%) 10% cash / 12% PIK L+1000 bps (LIBOR floor of 3.0%)

New TL upfront fee: 3.5% New TL exit fee: 3.5%

2/18/09 Bank of America /

MatlinPatterson Global Advisors

$95 million facility (roll-up of $39 million of pre-petition debt)

MatlinPatterson to arrange additional $50 million multi-draw term DIP facility

MatlinPatterson, stalking horse, may potentially credit bid for the company

6 months

14% paid in-kind

Upfront fee: $1.7MM Agent fee $375,000

2/11/09 Bank of New York

Mellon / DDJ / Wayzata

$75 million new money multi-draw TL

9 months L+1,200 bps (LIBOR floor of 4.0%)

Fees: Undisclosed Prepayment Premium: 5% of commitment

2/3/09

Wachovia

D.E. Shaw/ Avenue Capital/

Harbinger

$190 million new money revolver

$45 million new money ABL revolver

12 months

L+450 bps (LIBOR floor of 3.0%)

L+1,450 bps (LIBOR floor of 3.00%)

Upfront fee: 3.0% Exit Fee: 1.0% Exit Fee on TL: 5.0% if converted; 4.0% if repaid; 9.9% of reorganized equity if Spectrum is sold

21

41©2009 Foley & Lardner LLP

Selected Recent DIP Pricing (cont’d)

COMPANY FILING

DATE LENDER(S) /

AGENT DIP STRUCTURE MATURITY INTEREST RATE FEE(S)

1/30/09 Wayzata

Investment Partners

$65 million TL 3 months

L+1,000 bps (LIBOR floor of 5.0%)

Upfront fees: 3.0% Exit fees: 3.0%

1/26/09

JP Morgan / Deutsche Bank /

GE Capital / Bank of America /

Foothill / Bank of Nova Scotia

$250 million ABL revolver (U.S. & CAN) $400 million TL (U.S.) $65 million ABL Revolver (U.S. & CAN) $35 million TL (CAN)

12 months Option of 2 three month extensions

L+650 bps (LIBOR floor of 3.5%)

− 100 bps per extension

− L+850 bps if both extensions exercised

Upfront fee: 1.0% 100 bps fee for each extension

1/12/09 Credit Suisse $125 million ABL revolver $35 million existing L/Cs roll up into new second lien DIP facility

12 months L+950 bps (LIBOR floor of 3.5%) Upfront fee: 3.0%

Unused line: 300 bps

1/06/09 Citigroup / UBS /

Apollo

$1.5 billion ABL revolver $3.25 billion new money term loan

$3.25 billion roll-up junior term loan

12 months

L+700 bps (LIBOR floor of 3.0%) L+1,000 bps (LIBOR floor of 3.00%)

L+350 bps (LIBOR floor of 3.25%)

Upfront fees: 2.0% Upfront fees: 3.5% with 3.0% exit fee

Upfront fees: 3.5% with 3.0% exit fee

12/01/08 Bank of Montreal $450 million priming ABL revolver $20 million L/C sub-limit

12 months Base Rate+800 bps Upfront fee: 2.5%

Unused line: 50 bps

11/10/08 GECC, Wells

Fargo / Bank of America

$1.1 billion revolving credit facility $350 million L/C sublimit By December 29, 2008, commitment is reduced to $900 million

12 months

L+400 bps 400 bps on L/Cs

Upfront fee: Undisclosed

Unused line: 75 bps

11/04/08 Wayzata, Trilogy,

AIG/ UBS, Agstar

$190 million triple-draw term loan $30 revolving credit facility 12 months

Fixed 16.5% L+700bps

Upfront fee: 2.0% Exit Fee: 5.0% of amount prepaid

10/20/08 Cerberus,

Centerbridge, D.E.Shaw / UBS

$73.6 million delayed draw term loan

$60 million L/C sublimit for term loan cash collateralized L/Cs

5 months

Base Rate (BR) +600 bps (BR floor of 5.25%)

Base Rate (BR) + 600 bps + 325 bps backstop fee (925 bps all-in)

Upfront fee: 300 bps Backend fee: sliding

scale from 200 bps to cap of 800 bps

42©2009 Foley & Lardner LLP

Current DIP Financing Market

Scarcity of third-party financing has led to “defensive DIPs”being arranged within pre-petition group

Increase in DIP pricing and fees relative to pre-credit crunch period

Decreased investor confidence has led to lower leverage / debt capacity and DIP size

Bifurcated collateral structure may create divergent goals between ABL and term lenders

Tension between “old money” desire to include roll-up DIP tranches and new money / company desire for “cleaner”structure

DIPs receiving increased ratings attention, as CLOs require new debt instruments to be rated

22

43©2009 Foley & Lardner LLP

Control Through the DIP

Lenders use the DIP funds and covenants to control bankruptcy proceedings

More typical controls include:– Shorter DIP maturity

– Sale milestones

– Plan milestones

– Other covenants

– Managing “carve outs” for professional fees

– Payment of prepetition secured debt in full

44©2009 Foley & Lardner LLP

Purchase Agreement Issues

23

45©2009 Foley & Lardner LLP

Purchase Agreement Issues

Section 363 of the Bankruptcy Code– Non-ordinary course transactions require Court approval– Free and clear of all liens, claims and encumbrances– Can “cherry pick” assets and liabilities

Identity of Purchaser– Newly formed entity?– What if there is a “breach”?

Deposit– Forfeiture events – Liquidated damages?

Purchased Assets/Excluded Assets– Need to be specific as to assets to be sold/retained– Consider transition/operating issues

46©2009 Foley & Lardner LLP

Purchase Agreement Issues (cont’d)

Contracts/Liabilities to be Assumed– Identify in Purchase Agreement at time of signing– Ability to identify additional contracts after signing of

Purchase Agreement or for a limited time period post-closing

– Must pay “cure amounts” for assumed contracts– Use rejection threat as leverage to re-negotiate– Third party consents

Purchase Price – Fixed purchase price– Working Capital adjustment– Limited duration escrow

24

47©2009 Foley & Lardner LLP

Purchase Agreement Issues (cont’d)

Representations and Warranties– “As-Is”– Limited representations and warranties– Non-survival of representations and warranties

Conditions to Closing– MAC Condition– Due Diligence/Financing/Third Party Approval conditions (must be

removed prior to Auction)– HSR and other antitrust considerations

Termination Provisions– Need to be “tight” to ensure certainty– “Back-up Bidder”

Bidding Procedures/Auction Process– Time period for competitive bidding– Bidding increments

48©2009 Foley & Lardner LLP

Purchase Agreement Issues (cont’d)

Break-Up Fee for Stalking Horse Purchaser– Typically 3-5% of the purchase price – When payable?

Successor Liability– Tax, ERISA, product liability, environmental issues

– Generally, bankruptcy sales do not cut off all potential successor liability claims; although court decisions have been inconsistent

– Need to ensure that all potential claimants receive “notice”– Mitigate risk by including specific language in Purchase

Agreement and Sale Order– Specific finding in Sale Order that purchaser is not a successor– Consider larger escrow or purchase price reduction

25

49©2009 Foley & Lardner LLP

Purchase Agreement Issues (cont’d)

No-Post Closing Indemnification– If there are any known issues, an escrow

should be established (or other security)

– Representations and warranties generally do not survive closing

Post-Closing Issues– Transition Services Agreements

– Continued use of employees/contractors

50©2009 Foley & Lardner LLP

Questions and Answers

26

51©2009 Foley & Lardner LLP

Presenter Contacts

Steven H. Hilfinger(313) [email protected]

Daljit S. Doogal(313) 234-7122 [email protected]

Geoffrey S. Goodman(312) [email protected]

Alexander Tracy(212) [email protected]

52©2009 Foley & Lardner LLP

Mark Your Calendars

Please save the date for the remaining topics in the 2009 M&A Briefing Series:

June 23Due Diligence Considerations After the Recent Financial Crisis

July 30 Indemnification: Trends and Hot Topics

September 16Insurance in the M&A Industry

November 5Impact of the Transition to International Financial Reporting Standards on M&A

Please visit www.foley.com/mabs to register and for more details.

27

53©2009 Foley & Lardner LLP

Thank You

A copy of the PowerPoint presentation and a multimedia recording will be available on our website within 24 to 48 hours: http://www.foley.com/news/event_detail.aspx?eventid=2747

We welcome your feedback. Please take a few moments before you leave the web conference today to provide us with your feedback.http://www.zoomerang.com/Survey/?p=WEB2294MF94BFZ