1

Fiscal Regimes for Extractive Industries –

Old and New Challenges

Philip Daniel

IDS, Sussex 5 April 2017

A key revenue source during the boom years…Source: IMF (2012)

Why distinct fiscal regimes for EI?

Substantial rentsPervasive uncertainty

3

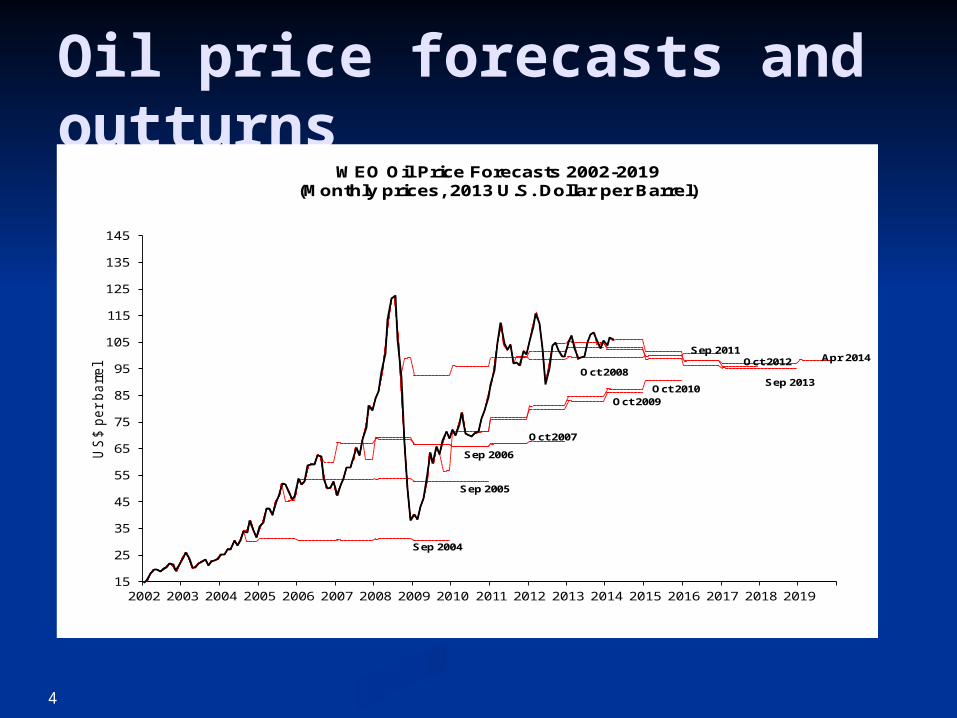

Oil price forecasts and outturns

4

15

25

35

45

55

65

75

85

95

105

115

125

135

145

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

US

$ pe

r bar

rel

WEO Oil Price Forecasts 2002-2019(Monthly prices, 2013 U.S. Dollar per Barrel)

Oct 2010

Sep 2004

Sep 2011

Oct 2008

Oct 2009

Oct 2007

Sep 2006

Sep 2005

Oct 2012

Sep 2013

Apr 2014

20022002200220022002200220022002200220022002200220032003200320032003200320032003200320032003200320042004200420042004200420042004200420042004200420052005200520052005200520052005200520052005200520062006200620062006200620062006200620062006200620072007200720072007200720072007200720072007200720082008200820082008200820082008200820082008200820092009200920092009200920092009200920092009200920102010201020102010201020102010201020102010201020112011201120112011201120112011201120112011201120122012201220122012201220122012201220122012201220132013201320132013201320132013201320132013201320142014201420142014201420142014201420142014201420152015201520152015201520152015201520152015201520162016201620162016201620162016201620162016201620172017201720172017201720172017201720172017201720182018201820182018201820182018201820182018201820192019201920192019201920192019201920192019201920202020202020202020202020202020202020202020202020212021202120212021202120212021202120212021202115

25

35

45

55

65

75

85

95

105

115

125

135

145

WEO (IMF) Oil Price Forecasts 2002-2021(Monthly prices, 2016 U.S. Dollar per Barrel)

US

$ pe

r bar

rel

Sep 2004

Sep 2011

Oct 2008

Oct 2009Oct 2007

Sep 2006

Sep 2005

Oct 2012Sep 2013

Oct 2014Oct 2010

Apr 2015

Oct 2015

Apr 2016

Volatility in costs

6

Upstream Capital Cost Index

Upstream Operating cost Index

Source: IHS Energy

Why distinct fiscal regimes for EI? Substantial rentsPervasive uncertaintyAsymmetric informationHigh sunk costs, long production periodsExtensive involvement of multinationals in some

countries…and of State-Owned Enterprises in others

7

Why distinct fiscal regimes for EI? (2)

Few of these considerations are unique to resources—they’re just bigger. What is unique is:

Exhaustibility

—Recognize revenues as transformation of finite assets in the ground into other assets

—Possible cost of extracting now rather than in future

8

Central objectives

Maximize PV of net government revenues

Timing of receipts

“Progressivity” – taxing rents

Ease of administration (for authorities) and compliance (for taxpayers)

9

Three main fiscal schemes (sometimes blended)…Contractual, including production sharing or

service contracts

Tax and royalty, with licensing of areas

State ownership or participation These can be made fiscally equivalent

Design to achieve efficiency and transparency in each case

10

Fiscal Instruments for EI Bonuses (with bidding) Royalty Corporate income tax Explicit rent taxes (and alternative forms) State participation

11

Evaluation is essential…Two approaches:

Model effects on exploration, development, and extraction

Scenario analysis – the FARI modeling system

Use indicators related to objectives and criteria, e.g.

—Average effective tax rate

—Progressivity in prices

12

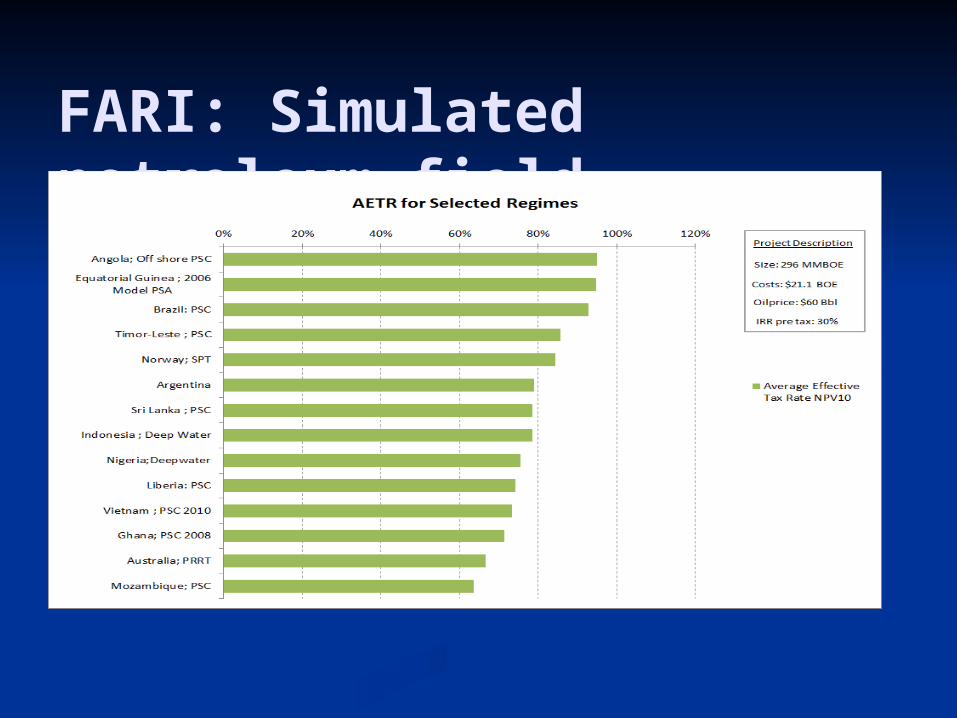

FARI: Simulated petroleum field

14

North American shale gas

- 20% 40% 60% 80% 100% 120%

Oklahoma; Conventional

Texas; Conventional

Texas; Unconventional

Oklahoma; Unconventional

North Dakota; Conventional

North Dakota; Unconventional

Pennsylvania; Unconventional

Pennsylvania; Conventional

Alberta; Conventional

Saskatchewan; Conventional

Saskatchewan; Unconventional

Alberta; Unconventional

Average Effective Tax Rate

Average Effective Tax Rate NPV0

Average Effective Tax Rate NPV0

Average Effective Tax Rate NPV10

Maginal

Not viableSize: 1 Tcf

Costs: $2.1 BOE

Oil price: $80

Gas price: $4 Mcf

Project

Field : Shale Gas North America

IRR pre tax: 34%

15

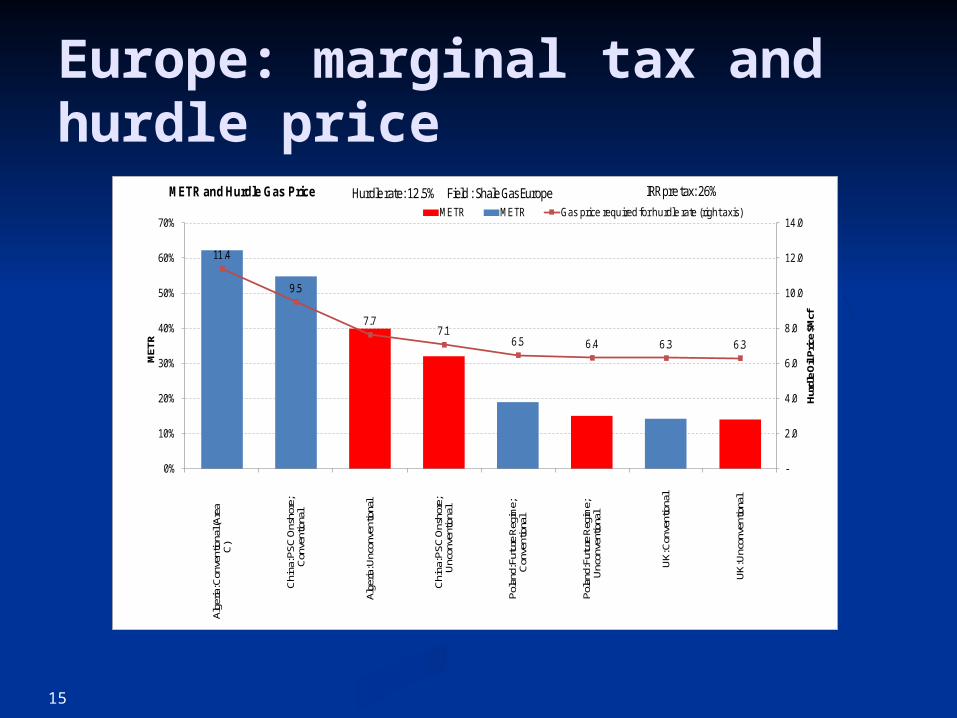

Europe: marginal tax and hurdle price

11.4

9.5

7.77.1

6.5 6.4 6.3 6.3

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

0%

10%

20%

30%

40%

50%

60%

70%Alg

eria

: Con

vent

iona

l (Are

a C

)

Chi

na: P

SC

Ons

hore

; C

onve

ntio

nal

Alg

eria

: Unc

onve

ntio

nal

Chi

na: P

SC

Ons

hore

; U

ncon

vent

iona

l

Pol

and:

Fut

ure

Reg

ime;

C

onve

ntio

nal

Pol

and:

Fut

ure

Reg

ime;

U

ncon

vent

iona

l

UK: C

onve

ntio

nal

UK: U

ncon

vent

iona

l

Hur

dle

Oil

Pric

e $M

cf

MET

R

METR and Hurdle Gas PriceMETR METR Gas price required for hurdle rate (right axis)

Hurdle rate: 12.5% IRR pre tax: 26%Field : Shale Gas Europe

Where does it all lead?(1)

Fiscal regimes for EI vary greatly Simulations for mining suggest government shares of 40-60

percent—but collection data suggest lower in practice

For petroleum the simulated shares are higher: 65 to 85

percent

Achieved shares below these ranges are cause for concern,

or regret

16

Where does it all lead?(2)

Country circumstances require tailored advice, but

generally within a framework that combines A royalty on gross revenue

A tax targeted explicitly on rents (and thus on the achieved

results of extraction)

Together with normal corporate income tax

Bonus-bidding may have a role in promising environments

17

And what will that do?Such a regime:

Ensures revenue from day one

Also that government’s revenue rises as rents increase – whether from rising prices or from favorable geological or cost conditions

Transparent rules and contracts promote stability and credibility

Inclusion of rent taxes reduces pressures to renegotiate or unilaterally change the rules

But processes to allow review and revision may be needed

18

Different for unconventional oil/gas?Justification for concessions to shale/tight oil and gas is not obvious

Concessions made have a fiscal cost

Concessions and incentives are perverse in the face of potential environmental costs

Fiscally neutral taxation of unconventionals would be the starting point for suitable environmental taxation.

19

EI fiscal regimes…and environmentChanging patterns of tax

Saturation of labor tax and consumption tax

Costs – evolution in high and low prices Elasticity of cost response to prices

Effects of carbon tax – is it just more royalty?External costs of resource extraction

Royalty? Additional charge? Bonuses?

Abandonment and reclamation

20

Administration EI tax administration should not in principle be hard

Nonetheless, often both difficult and badly done

Administration of profit/rent-based EI taxes is possible, impose royalties for policy reasons, not administration

Principles of effective modern tax administration are equally relevant to EI

21

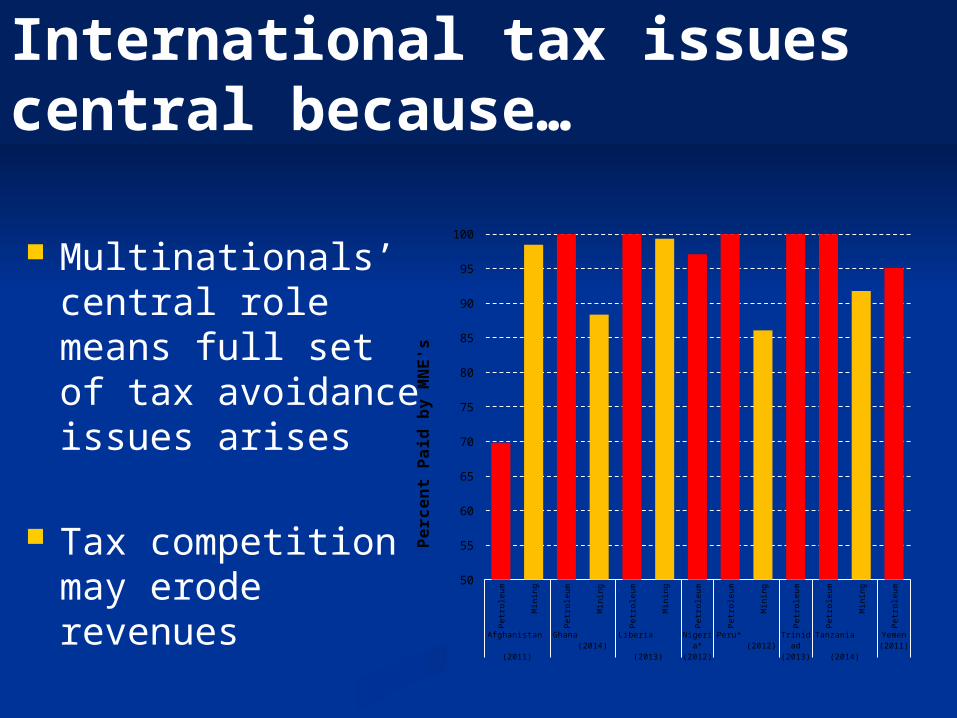

International tax issues central because…

Multinationals’ central role means full set of tax avoidance issues arises

Tax competition may erode revenues Pe

trole

um

Min

ing

Petro

leum

Min

ing

Petro

leum

Min

ing

Petro

leum

Petro

leum

Min

ing

Petro

leum

Petro

leum

Min

ing

Petro

leum

Afghanistan (2011)

Ghana (2014)

Liberia (2013)

Nigeria* (2012)

Peru* (2012)

Trinidad (2013)

Tanzania (2014)

Yemen (2011)

50

55

60

65

70

75

80

85

90

95

100

Perc

ent P

aid

by M

NE'

s

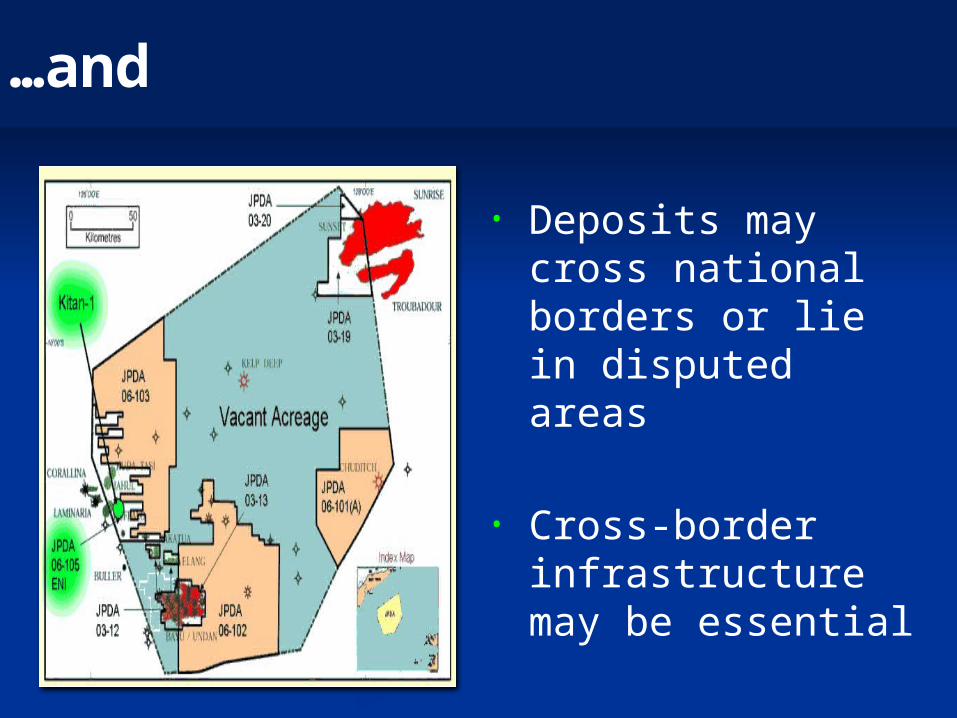

…and

• Deposits may cross national borders or lie in disputed areas

• Cross-border infrastructure may be essential

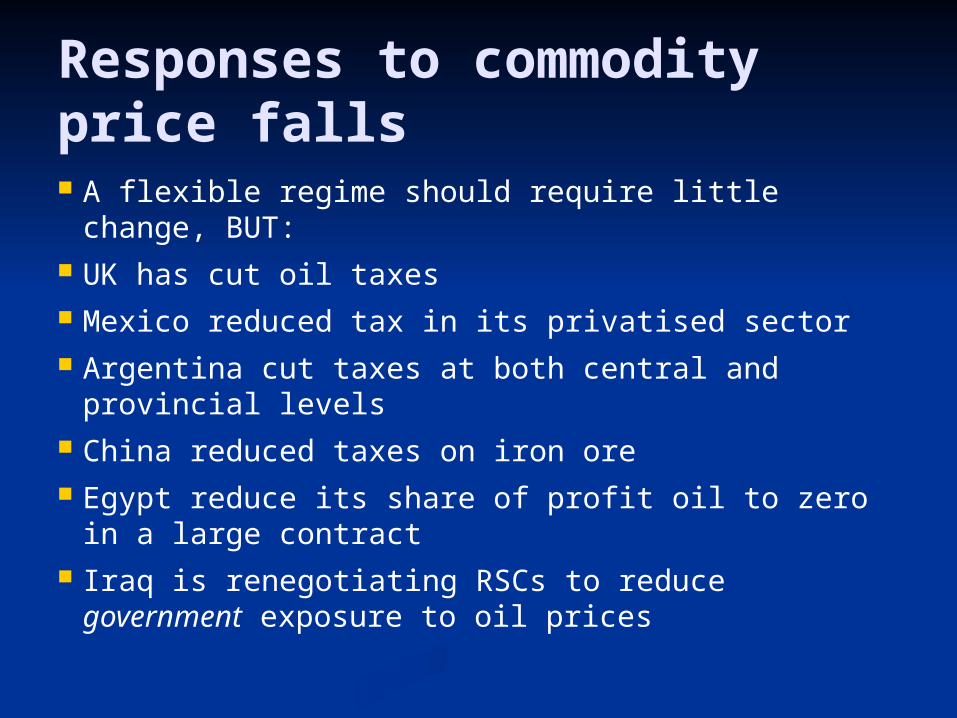

Responses to commodity price falls A flexible regime should require little change, BUT: UK has cut oil taxes Mexico reduced tax in its privatised sector Argentina cut taxes at both central and provincial levels China reduced taxes on iron ore Egypt reduce its share of profit oil to zero in a large

contract Iraq is renegotiating RSCs to reduce government

exposure to oil prices

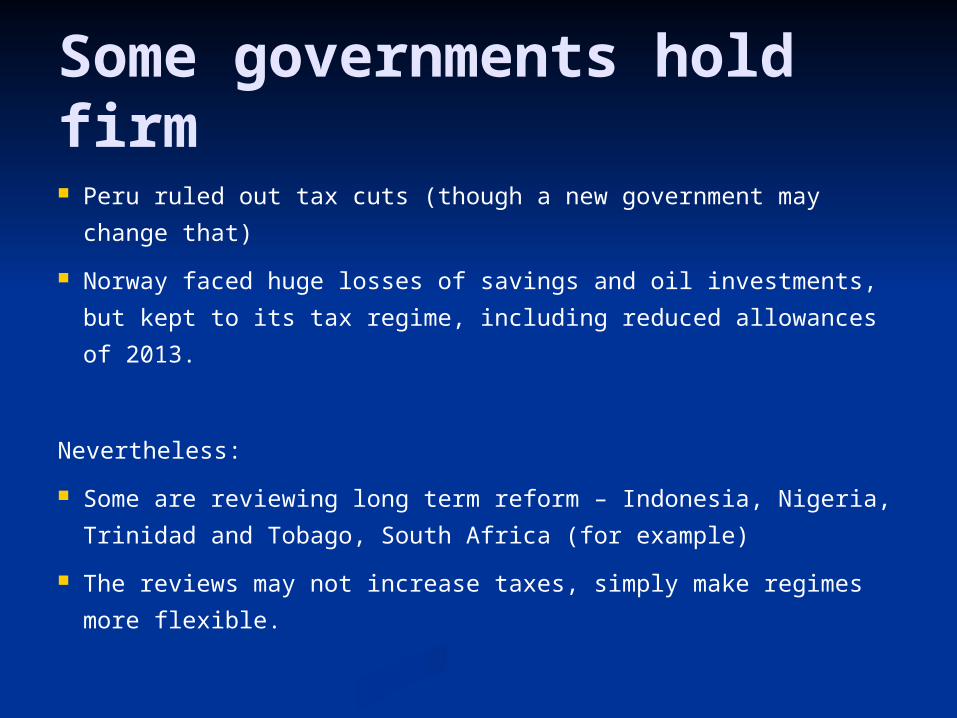

Some governments hold firm Peru ruled out tax cuts (though a new government may change that)

Norway faced huge losses of savings and oil investments, but kept to its tax regime, including reduced allowances of 2013.

Nevertheless:

Some are reviewing long term reform – Indonesia, Nigeria, Trinidad and Tobago, South Africa (for example)

The reviews may not increase taxes, simply make regimes more flexible.

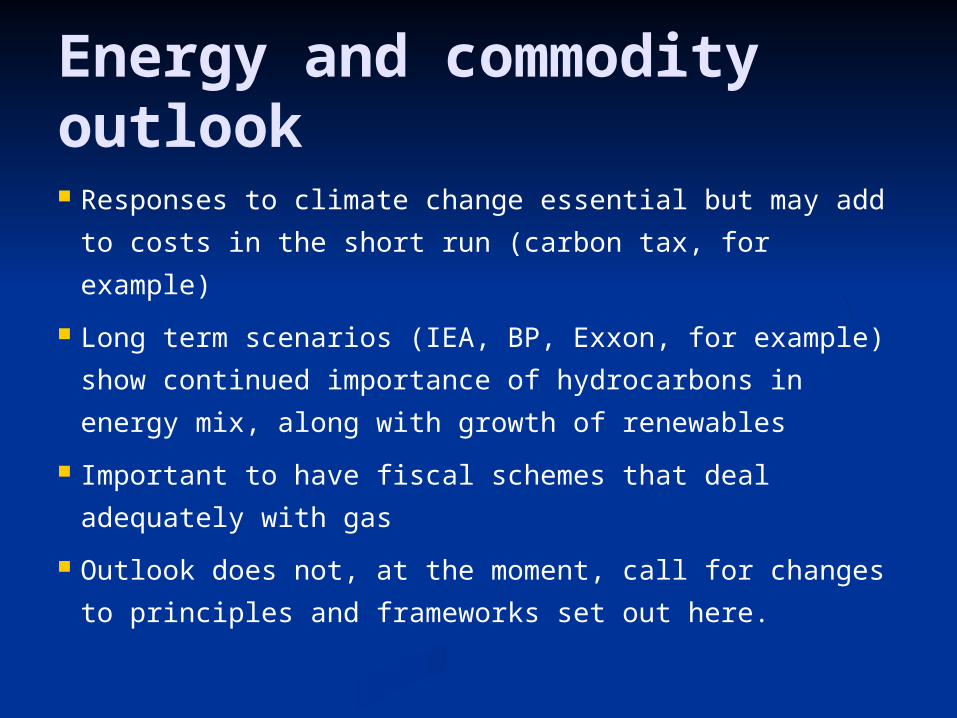

Energy and commodity outlook Responses to climate change essential but may add to

costs in the short run (carbon tax, for example)

Long term scenarios (IEA, BP, Exxon, for example) show continued importance of hydrocarbons in energy mix, along with growth of renewables

Important to have fiscal schemes that deal adequately with gas

Outlook does not, at the moment, call for changes to principles and frameworks set out here.

Transparency EITI, IMF Guide on Resource Revenue Transparency, Natural

Resource Charter…

Transparency in fiscal regime design and implementation is vital but often lacking

Transparency for environmental protection

Obligations on companies?

Obligations on governments

Educated and informed citizenry.

Draft IMF “4th Pillar”

27

International Taxation and the Extractive Industries

October 2016