Grow VC Group ++ www.growvc.com ++

@growvc ++ Enabling Digital Finance ++

Copyrights © Grow VC Group 2016 1

Digital Hybrid Finance: Bringing Traditional Finance and Fintech Together Jouko Ahvenainen, Hong Kong, September 27, 2016

Download this presentation from Grow VC Group Slideshare:

http://www.slideshare.net/growvc

Digital Finance Companies

Digital Finance Startups

New Concepts in Acceleration

Grow VC Group

Worldwide pioneer and leader in the digital finance, fintech and crowd & p2p finance solutions

Hong Kong - London - New York - San Francisco - Milan

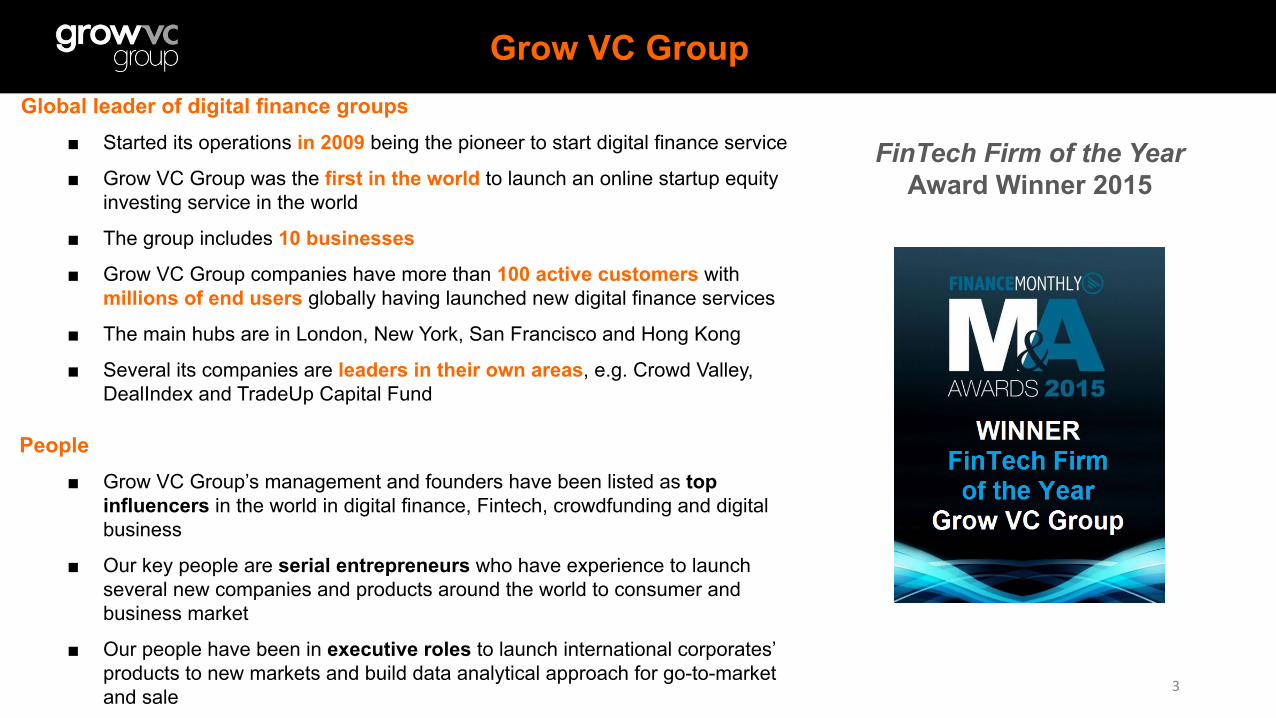

Global leader of digital finance groups

■ Started its operations in 2009 being the pioneer to start digital finance service

■ Grow VC Group was the first in the world to launch an online startup equity investing service in the world

■ The group includes 10 businesses

■ Grow VC Group companies have more than 100 active customers with millions of end users globally having launched new digital finance services

■ The main hubs are in London, New York, San Francisco and Hong Kong

■ Several its companies are leaders in their own areas, e.g. Crowd Valley, DealIndex and TradeUp Capital Fund

People ■ Grow VC Group’s management and founders have been listed as top

influencers in the world in digital finance, Fintech, crowdfunding and digital business

■ Our key people are serial entrepreneurs who have experience to launch several new companies and products around the world to consumer and business market

■ Our people have been in executive roles to launch international corporates’ products to new markets and build data analytical approach for go-to-market and sale

Grow VC Group

FinTech Firm of the Year Award Winner 2015

3

Grow VC Group Works with Industry Leaders

4

Demand from capital requirements, customers and efficiency needs

The Great Disruption

5

Finance Sector Challenges

6

1. The finance crisis in 2008 started a chain reaction that impacted regulation, credibility and business models of banks

2. More regulation and requirements on capital have limited banks’ capability to lend to business customers

3. Digital currencies and especially underlining technology, like blockchain, enables new ways to make transactions without payment processors and banks

4. People and companies are more critical towards finance institutions and service costs, e.g. in fund raising, wealth management and asset management

› Leads to try alternative providers

› Crowdfunding and p2p lending have emerged

5. Goldman Sachs has estimated that the alternative finance addressable market is $3.3 Trillion

6. Average growth rate of the UK alternative Finance market is 159%

47% 68%

23% 49%

UK US

Level of confidence in banks

2008 2013

Source: Edelman Trust Barometer 350m

873m

2337m

0

500

1000

1500

2000

2500

2012 2013 2014

The UK alternative finance market growth

Source: University of Cambridge and EY: The European Alternative Finance Benchmarking Report

EARLY ADOPTERS ARE SKEWED TOWARDS MILLENNIALS

Boomers Gen X Millennials Gen Z 6.2m We can build a vibrant digital community that increases connections

► Born 1946–1964 ► 4.2% use FinTech

products

5.7m Established in the business world, mostly married with homes and children

► Born 1965–1980 ► 17.9% use FinTech

products

6.2m Largest customer group in history, target group for most major corporations

► Born 1981–1998 ► 28.4% use FinTech

products

5.5m (7m in 2020)

The first truly mobile generation

► Born 1998–present ► Attention span of ~8s ► Make up ~25% of

workforce in 2020

= 1m customers

Source: http://www.forbes.com/sites/danschawbel/2013/09/04/why-you-cant-ignore-millennials/ http://urbantimes.co/2013/07/the-difference-between-baby-boomers-gen-x-and-gen-y-infographic/, http://www.huffingtonpost.com/rhonda-l-randall-do/baby-boomers-redefining-aging_b_1448949.html EY FinTech Adoption Index http://www.ey.com/GL/en/Industries/Financial-Services/ey-fintech-adoption-index

Grow Advisors material

HIGH-INCOME MILLENNIALS ARE PARTICULARLY HEAVY FINTECH USERS

44% 58%

24% 43%

15% 33%

Current use

Future use

6% 18%

Over US$150,000

US$70,001-150

,000

US$30,001-70,

000

Less than US$30,000

Consumers who have used at least 2 FinTechs in the past 6 months

Current and expected use of FinTech by income segment

US$150,001 over

Source: EY FinTech Adoption Index

US$70,001 - 150,000

Grow Advisors material

DRIVERS AND BARRIERS TO THEIR FINTECH ADOPTION

Source:http://www.ey.com/GL/en/Industries/Financial-Services/ey-fintech-adoption-index

9.0% for better quality of service

Why use fintech?

13.0% do not trust it

Why not use fintech? 52.5% think it is easy to set

up an account

13.4% use for access to different products and

services

8.1% use for the better online experience and functionality

7.8% think there are more attractive fees

51.7% were not aware it existed

29.1% prefer to use a traditional Financial services

provider

35.3% did not have a need to use it

19.0% don’t understand how it works

Grow Advisors material

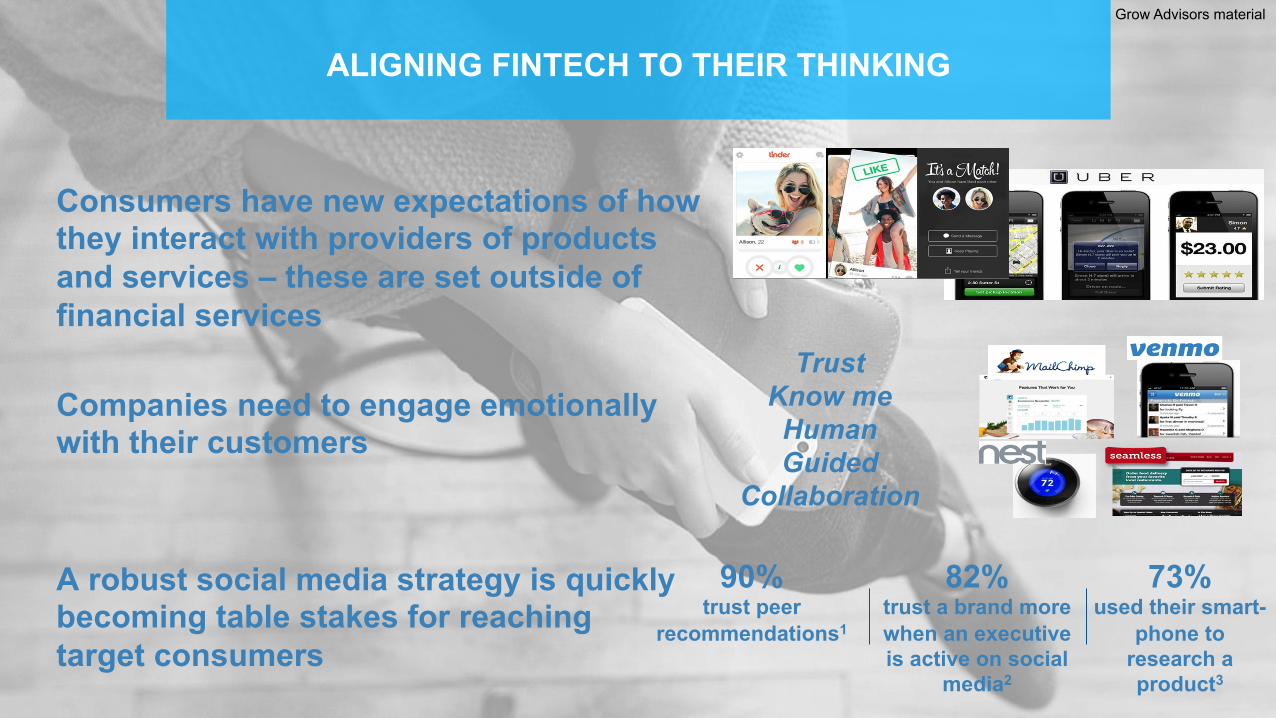

ALIGNING FINTECH TO THEIR THINKING

Consumers have new expectations of how they interact with providers of products and services – these are set outside of financial services

Companies need to engage emotionally with their customers

A robust social media strategy is quickly becoming table stakes for reaching target consumers

82% trust a brand more when an executive is active on social

media2

73% used their smart-

phone to research a product3

90% trust peer

recommendations1

Trust Know me Human Guided

Collaboration

Grow Advisors material

Two categories of fintech and digital finance

Approach based on products

1. Digital transaction processing

• Payments

• Money transfer • Process

transactions to 3rd parties

• Success based on # of transactions

2. Digital finance services and instruments

• Investing & lending

• Instruments for alternative finace

• Success based on long-term healty

profitability

The success of transactions and instruments are measured in very different way

How incumbents can operate in digital finance?

Form a “white label” partnership

Launch own digital finance platform

Collaborate as an investor or offer

finance instruments

Collaboration models Compete directly

Some collaboration examples

Blackrock purchased $320mio consumer debt

Santander Consumer agrees to buy 25% of

all loans issued

Estimated 80% of all loans purchased by

institutions

2/3rd of all loans purchased by HNWI, institutions, private

banks

€230 mio. agreement with Victory Park

capital to lend through platform + agreements with many institutions

Santander direct

borrowers who don’t meet traditional requirements

Source: Grow Advisors

Translating data into actionable insights to drive business outcomes

TRACK PRIVATE COMPANIES RAISING CAPITAL IN REAL-TIME

USE INTELLIGENT FILTERS TO SCREEN DEALS

HOW DOES DEALFLOW FLUCTUATE OVER TIME?

WHERE’S INVESTOR MONEY GOING?

INTERNATIONAL / AGGREGATE EQUITY CROWDFUNDING GLOBAL INDEX

Equity Crowdfunding Marketplace Lending RE Crowdfunding Online M&A Private Deals

Combine, Optimize, and Distribute

Digital Hybrid Finance

15

Emerging New API Ecosystems

16

Digital Back Office Services: • Authentications, transaction processing, user accounts, transaction history, reporting

• Assets and their securities, ownership ‘tables’, finance instrument models • Interfaces to 3rd party components, databases, ‘blockchain ledger’ processing

Payment processing Credit Rating ID verification 3rd party

services Blockchain

‘type’ services

Investing Service A

Investing Service B

P2P Lending Service A

Users: Private & Institutionals M

arke

t Dat

a Se

rvic

es

Wealth Management A

Secondary Market

Service A

Asset Management A

Syndicate Service A

Digital Fund Service A

Ris

k M

anag

emen

t an

d in

sura

nce

serv

ices

Many possible positions in the ecosystem

Wholesale offering

Consumer offering

Transaction focus

Refined instruments

Independent offering

API economy

Ecosystem example: Crowd Valley – the fast lane to implement a digital finance service

● 100+ enterprise clients served, including banks ● Digital Infrastructure enables online finance models and

facilitates billions in deals globally ● Open API, Certified Developer Ecosystem ● Use cases from real estate, private company financing,

solar bonds, investment banking, multi asset strategies ● Clients from California to Japan

Digital Finance Infrastructure: a Back Office platform to create, operate and manage your online investing or lending marketplace

Origination Compliance

Deal Origination, Investor Onboarding

KYC, AML, ID Verification, Accreditation services

Diligence Execution

Screening, Deal Rooms, Document Access Control

Payments, Escrow, E-Signature

Settlement

Closing & Settlement, Digital Ledgering

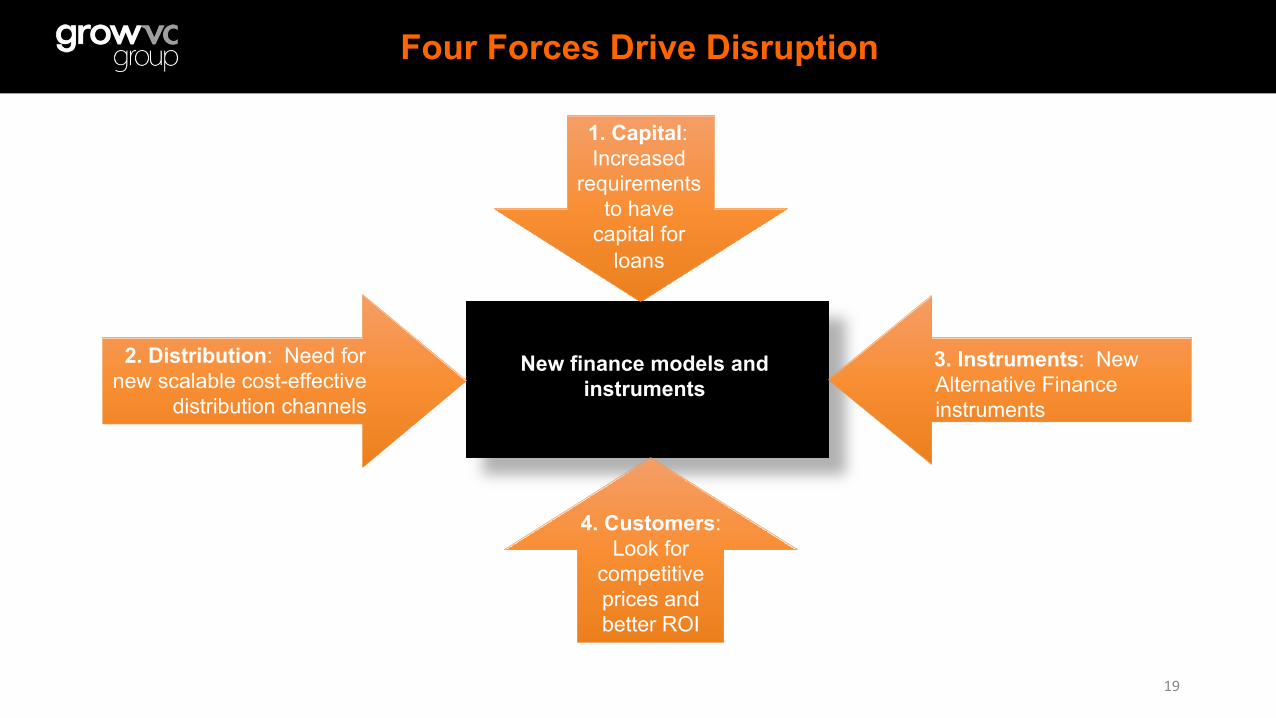

Four Forces Drive Disruption

19

New finance models and instruments

2. Distribution: Need for new scalable cost-effective

distribution channels

3. Instruments: New Alternative Finance instruments

1. Capital: Increased

requirements to have

capital for loans

4. Customers: Look for

competitive prices and better ROI

1. Better Capital Efficiency

20

Investors

• Combining equity and lending enables, for example, to

1. Leverage equity investments

2. Get collateral for loans

• Investors can use platforms to attract more co-investors and syndicate investments

• Participate in the securitization of p2p loans as an additional option to invest

Banks • Banks have regulatory requirements (e.g. Basel II / III) to

have a certain capital ratio for their risk-weighted assets

• Even well profitable loans can tie so much capital that capital requirements make them to have sub par ROI

• Equity investors, other lenders, different lender seniority levels and use of equity or loan from p2p as a collateral helps manage the capital ratio

• Possible to develop instruments (funded through platforms) that can offset loan liability or in cases work as a guarantee for loans

Ins,tu,onalInvestorsorLenders

P2PLendersorInvestors

RequiredCapital

Lesscapitalrequired,ifotherinvestorsorlendersdecreaseriskofloans

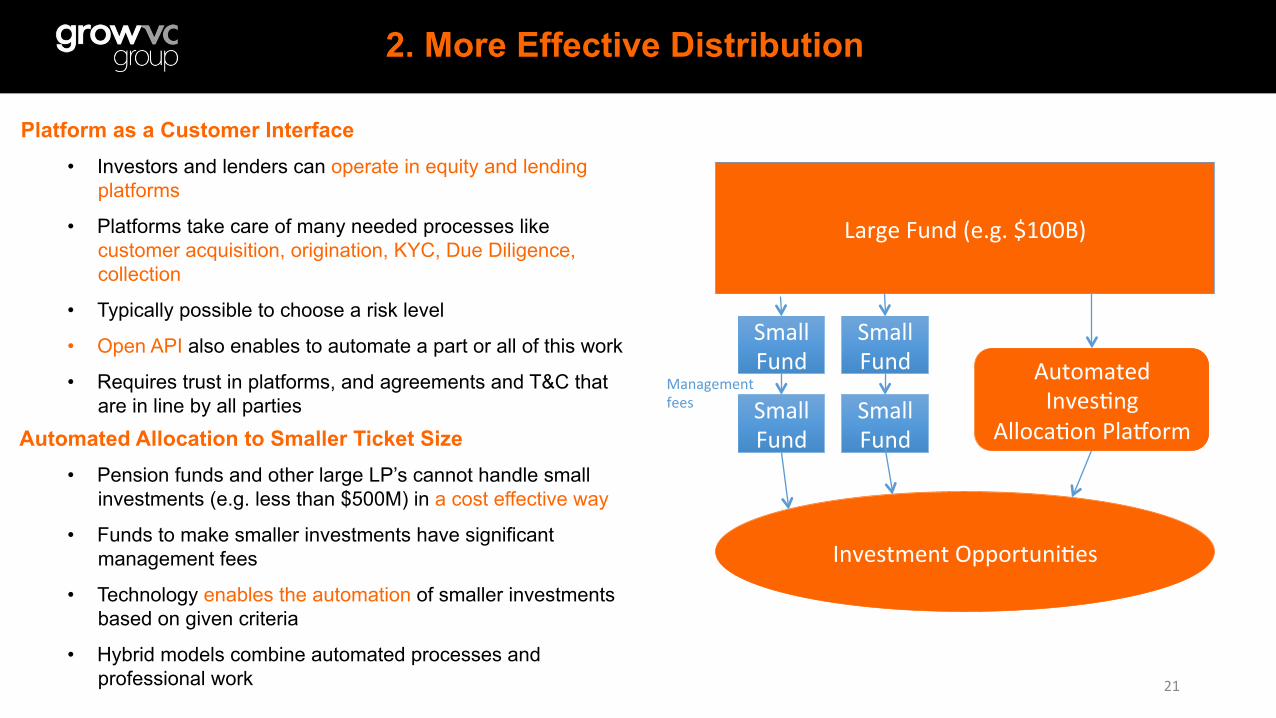

2. More Effective Distribution

21

Platform as a Customer Interface

• Investors and lenders can operate in equity and lending platforms

• Platforms take care of many needed processes like customer acquisition, origination, KYC, Due Diligence, collection

• Typically possible to choose a risk level

• Open API also enables to automate a part or all of this work

• Requires trust in platforms, and agreements and T&C that are in line by all parties

Automated Allocation to Smaller Ticket Size • Pension funds and other large LP’s cannot handle small

investments (e.g. less than $500M) in a cost effective way

• Funds to make smaller investments have significant management fees

• Technology enables the automation of smaller investments based on given criteria

• Hybrid models combine automated processes and professional work

LargeFund(e.g.$100B)

SmallFund

SmallFund

SmallFund

SmallFund

InvestmentOpportuni,es

AutomatedInves,ng

Alloca,onPlaMorm

Managementfees

3. New Instruments for Investors

22

New Finance Instruments

• Alternative Finance offers new attractive investment opportunities and its securitizations make the market more liquid

• Instruments to invest and lend money in platforms

• E.g. ‘p2p trust’ type instruments

• Securitization of online and p2p loans

• Risk management and guarantee instruments

• Work needed to find optimal regulatory and instrument models for these instruments (e.g. Open-Ended, Closed-Ended, ETF, or Evergreen fund)

• Crucial to have enough data from platforms and assets

Fund Simulators • Technically implemented investment services that work like

funds

• Investors can define their investment criteria, e.g.

• Geographical, industry sector, and risk level

• No costs from traditional management work

• Data and analytics needed to enable these products

Investment/LendingPlaMorm

Investment/LendingPlaMorm

P2PFundCrowdFund

Securi,za-,on

FundSimulator

Investors

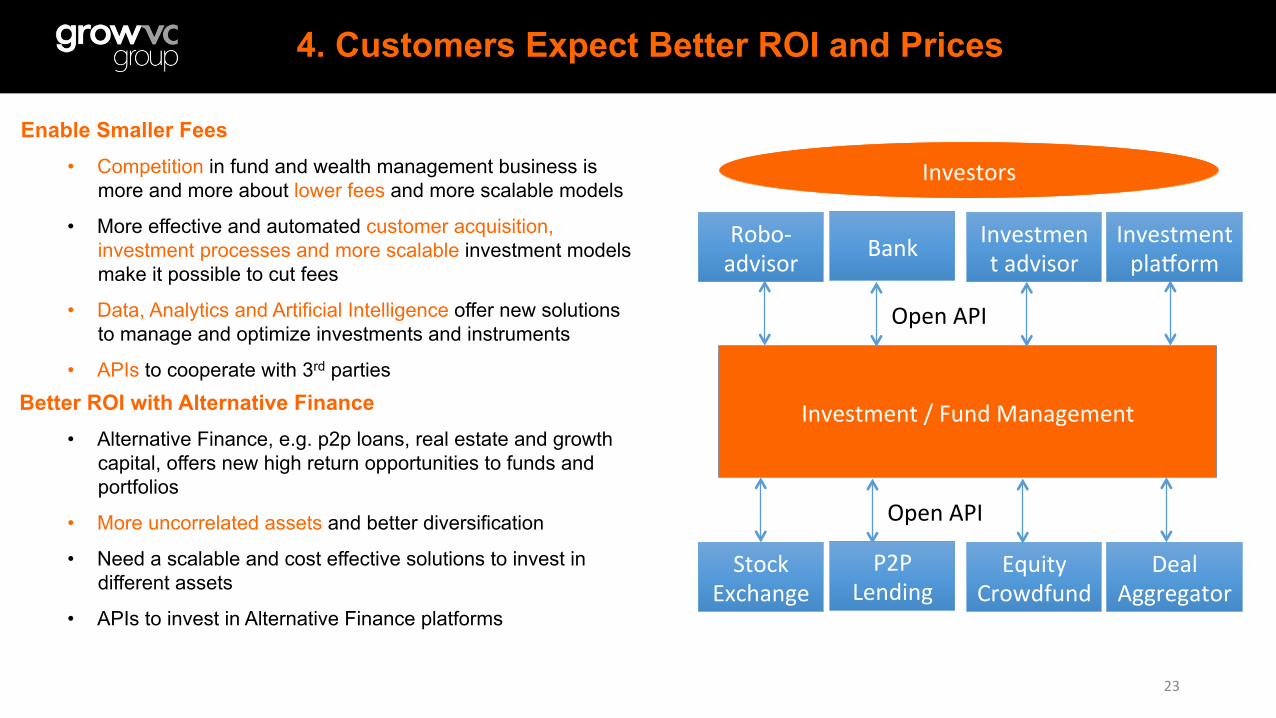

4. Customers Expect Better ROI and Prices

23

Enable Smaller Fees

• Competition in fund and wealth management business is more and more about lower fees and more scalable models

• More effective and automated customer acquisition, investment processes and more scalable investment models make it possible to cut fees

• Data, Analytics and Artificial Intelligence offer new solutions to manage and optimize investments and instruments

• APIs to cooperate with 3rd parties

Better ROI with Alternative Finance • Alternative Finance, e.g. p2p loans, real estate and growth

capital, offers new high return opportunities to funds and portfolios

• More uncorrelated assets and better diversification

• Need a scalable and cost effective solutions to invest in different assets

• APIs to invest in Alternative Finance platforms

Investment/FundManagement

OpenAPI

Robo-advisor Bank Investmen

tadvisorInvestmentplaMorm

OpenAPI

Investors

StockExchange

P2PLending

EquityCrowdfund

DealAggregator

What Enables All This?

24

1. Knowledge and Competence to Develop New Models ■ Combination of finance, banking, technology, and data science competences

■ Important to understand the API Ecosystem and innovate new business models

■ More global knowledge and mindset are needed 2. Data

■ Data enables institutional investors and banks to participate in the market ■ Data is the key component to develop new instruments and service

■ Advanced analytics and Artificial Intelligence (AI) enables new services and instruments 3. Technology

■ Open API

■ Ubiquitous back offices and middle ware for fundamental finance functions ■ Agile models to develop new applications on an open API back office

4. New innovation models ■ Building a new ecosystem, no one can do it alone

■ Accelerate innovation and ecosystem with partnering and open interfaces

Where is your organization?

25

Business Unit 1

Business Unit 2

Business Unit 3

Digital Digital Digital

Digital centre of excellence Business

Unit 1 Business

Unit 2 Business

Unit 3

Digital Digital Digital

Business Unit 1

Business Unit 2

Business Unit 3

Digital centre of excellence

Digital DNA Digital

Opportunism Digital

Centralism

Source: Grow Advisors analysis adapted from an original idea by BCG

Pros • Builds digital tools, digital

processes, and digital talent at scale

• Provides clear ownership and specialised expertise

• Delivers integrated and standardised end-to-end customer experience

Cons • Requires a strong mandate to

create change • Requires strong digital leaders • Requires tight integration

between the centre and business units for execution

Pros • Manages digital policy from the

centre to maintain quality and create scale

• Entrusts digital execution fully to business units

• Ensures a cohesive digital strategy at the enterprise level

Cons • Resistance from business units

around strategic priorities • Requires significant resources

in each business unit that deeply understand digital

Pros • Champions digital adoption

within the business, building groundswell of support

• Allows for quick wins Cons • Limits innovation outside the

core business • Creates business-unit-centric

thinking and fragmented customer experience

Summary – 4 points to remember

26

1. Digital and Alternative Finance are changing finance value chain and products ■ More de-centralized models, e.g. based on API ecosystem and blockchain

■ From service silos to more more seamless collected services 2. Four key areas: 1) Capital, 2) Distribution, 3) Instruments, and 4) Customers

■ This is not only about technical, but it is one key driver to enable new services, business models, better efficiency, and new finance instrument

■ Data is a key components for many new services

■ Develop fast – test – improve 3. Accelerating innovation and competence development

■ Open interfaces are needed to be fast enough and utilize ‘external resources’

■ New comers need to build competence and work with right partners, incumbent must especially focus on culture and attitude change

■ Digital economy is not just add technology or services, but adapt to a new business 4. Grow VC Group works in the core of these changes

■ Competence, technology, data, global presence, and constant innovating

Jouko Ahvenainen – [email protected] +44 7889 833 165 (UK), +1 646 363 6664 (US)

Twitter: @jahven, LinkedIn: joukoahvenainen Grow VC Group - growvc.com

ENABLING DIGITAL FINANCE

27

Download this presentation from Grow VC Group Slideshare:

http://www.slideshare.net/growvc