Expert Group Meeting on Transport and Trade facilitation

Why Trade Logistics Matter in the Arab Region?

Mohamed A. Chemingui, ESCWA

Movenpick hotel, Dubai, 10-11 April 2013

2

Regional Characteristics

Economically diverse region …..In terms of:- Size of economy;- Size of population;- Economic structures and level of economic

diversification;- Geographical location and area;- Type of governance and institutions- Human capital and labor productivity- Level of integration to the world economy

Growth pattern has special characteristics……- Heavy reliance on oil exports; - Weak macroeconomic policies coordination- Weak regional trade and financial integration;- High population growth rates;- High unemployment rates, particularly youth and

women;- High weight of public sectors and inefficient

markets- High poverty rates outside GCC countries; - Very heterogeneous fiscal space levels;- Underdeveloped institutions;

Country Name Population GDP GDP per capita

% of Total population to overall ESCWA population

% of GDP constant to Total ESCWA GDP

GCC (Oil-Rich labor importing)

Bahrain 1.1 19.3 18.3 0.32 1.1Kuwait 2.5 105.9 41.6 0.76 6.0Libya 6.2 62.4 10.1 1.86 3.5Oman 2.6 46.9 17.8 0.79 2.7Qatar 1.4 97.6 69.9 0.42 5.5Saudi Arabia 26.2 376.7 14.4 7.86 21.4UAE 6.2 297.6 48.0 1.86 16.9Total 46.2 1006.4 220 13.87 57.1

Non-Oil middle income Labor exporting

Egypt 78.3 189.0 2.4 23.51 10.7Morocco 34.8 90.9 2.6 10.45 5.2Jordan 5.8 23.8 4.1 1.74 1.4Lebanon 4.2 34.9 8.4 1.25 2.0Syrian 19.6 53.9 2.7 5.90 3.1Tunisia 10.3 43.5 4.2 3.09 2.5

Total 153.0 436.1 24.5 45.93 24.7Others (Diversified Economies)

Algeria 34.8 138.1 4.0 10.45 7.8Djibouti 1.9 1.0 0.5 0.57 0.1Mauritania 3.0 3.0 1.0 0.90 0.2Iraq 30.2 81.1 2.7 9.06 4.6Sudan 41.4 67.0 1.6 12.43 3.8Yemen 22.6 31.0 1.4 6.79 1.8

Clear discrepancy in the region;

In 2009, Oil rich labor importing countries

recorded less that 14% of total Arab Pop; and more than 57% of Arab GDP In 2009, Non- oil

middle income labor exporting countries population

registered more than 3 times that of oil rich countless with only 25% share to total Arab GDP.

The 3rd group contributed 18% to total GDP and more than 40% of total Arab population.

Arab Economic

Performance –

selected indicators

(2009)

No data available for Palestine, Comoros and Somalia. Source WB

Institutions & Agreements in

support of regional economic

integration

Starting from Arab League in 1945… 1950 Treaty for Joint Defense and Economic

Cooperation; 1953 Agreement on Trade Facilitation and Regulating

Transit Trade; 1957 Arab Economic Unity Agreement; 1964 Arab Common Market Agreement; 1981 Agreement on Facilitation and Development of

Trade; 1981 Gulf Cooperation Council; 1989 Arab Maghreb Union; 1997 Greater Arab Free Trade Area; 2003 Initiation of the Framework Agreement for

Liberalizing Trade in Services; 2005 Full entry into force of Greater Arab Free Trade

Area.

Future actions• Main declarations of the third Arab Economic Summit 2013• 1. Removal of remaining barriers (tariffs and non tariffs) on intra-

Arab trade by end of 2013• 2. Creation of Arab Custom Union by 2015• 3. Accelerate the implementation of the “Aid for Trade” activities for

the 22 Arab countries under the coordination of the Islamic Development Bank

• Challenges:• Is there a room for an Arab Common Position for the Next WTO

ministerial conference in December 2013 and potential agreement?• What about the FTAs signed by some Arab countries with the EU

and USA if an Arab Custom Union will be implemented?

Export Performance:

Compared to other regions…

Arab region is less integrated, even compared to African countries.

Intraregional exports as % of total exports (2010)

Source: ITC

Arab league

GCC Maghreb UE 27 NAFTA Asean Africa0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

5.22.6 2.5

64.5

48.7

24.8

12.4

7

What determines divergent trade performance?

Export concentration index by regionindex (1995,2011)

World

DCs

Developed economies

DCs Africa

DCs America

DCs Asia

DCs Western Asia

0.0

0.1

0.2

0.3

0.4

0.5

0.6

1995 2011 -4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Tur

key

Leba

non

Jord

an

O.

Pal

estin

ian

T.

Syr

ian

Ara

b R

.

Bah

rain

UA

E

Qat

ar

Om

an

Yem

en

Kuw

ait

Sau

di A

rabi

a

Iraq

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

2000-2011 Volume of exports Growth

2011 concentration index

Export concentration index by county and export performance (2000-2011)

• Arab countries has high export concentration• Does high export concentration hindering export growth?

– Empirical Studies .. Yes – Western Asia .. Yes (oil sector), but there are windows for diversification

and improvements !

Understanding why intra-Arab trade is low in Arab countries?

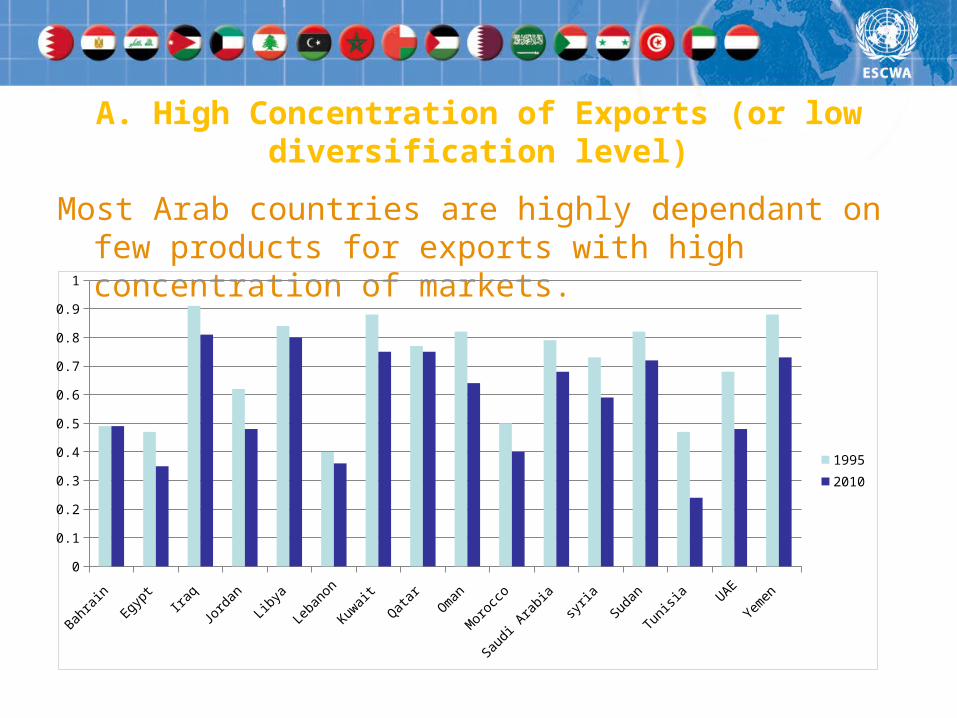

A. High Concentration of Exports (or low diversification level)

Most Arab countries are highly dependant on few products for exports with high concentration of markets.

Bahra

in

Egypt

Ira

q

Jord

an

Libya

Leba

non

Kuwait

Qatar

Oman

Mor

occo

Saudi

Arabia

syria

Sudan

Tunisi

a UAE

Yemen

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

1995

2010

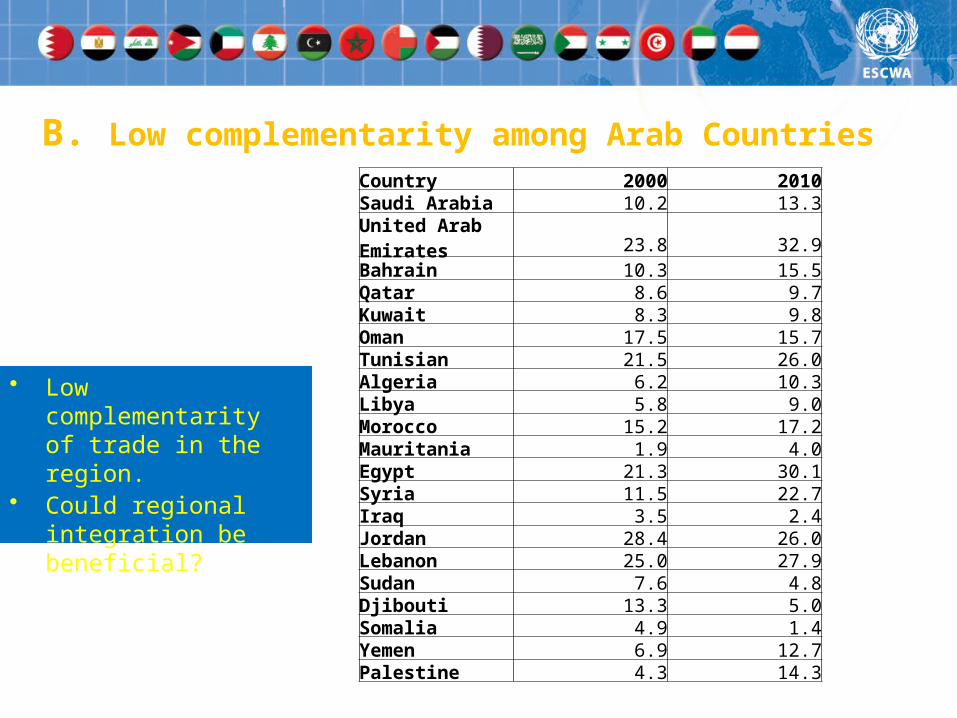

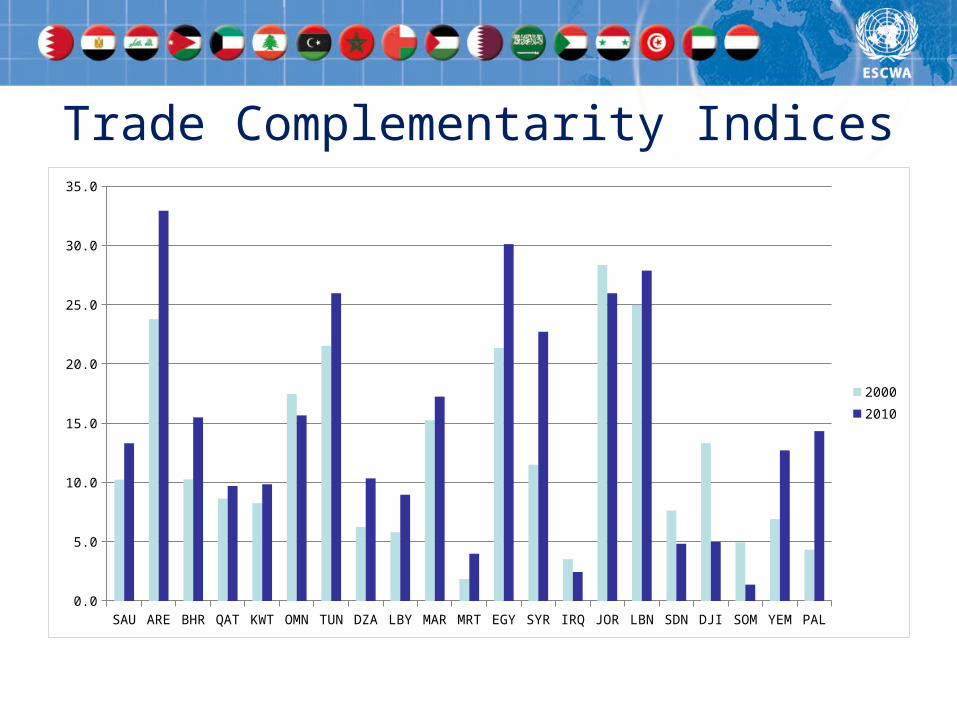

• Low complementarity of trade in the region.

• Could regional integration be beneficial?

B. Low complementarity among Arab Countries Country 2000 2010Saudi Arabia 10.2 13.3United Arab Emirates 23.8 32.9Bahrain 10.3 15.5Qatar 8.6 9.7Kuwait 8.3 9.8Oman 17.5 15.7Tunisian 21.5 26.0Algeria 6.2 10.3Libya 5.8 9.0Morocco 15.2 17.2Mauritania 1.9 4.0Egypt 21.3 30.1Syria 11.5 22.7Iraq 3.5 2.4Jordan 28.4 26.0Lebanon 25.0 27.9Sudan 7.6 4.8Djibouti 13.3 5.0Somalia 4.9 1.4Yemen 6.9 12.7Palestine 4.3 14.3

Trade Complementarity Indices

SAU ARE BHR QAT KWT OMN TUN DZA LBY MAR MRT EGY SYR IRQ JOR LBN SDN DJI SOM YEM PAL0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2000

2010

Structure of Arab Countries’ Exports

Bahra

in

Egypt

Ira

q

Jord

an

Libya

leban

on

Kuwait

Qatar

Oman

Mor

rocc

o

Saudia

Ara

bia

Syria

Sudan

Tunisi

a UAE

Yem

en

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Commodities and transactions not classified elsewhere in the SITC

Miscellaneous manufactured articles

Machinery and transport equipment

Manufactured goods classified chiefly by material

Chemicals and related products, n.e.s

Animal and vegetable oils, fats and waxes

Mineral fuels, lubricants and related mater-ials

Crude materials, inedible, except fuels

Beverages and tobacco

Food and live animals

• Trade agreements granting prefrencial market access DOES NOT eliminate problems created by NTMs.

• NTMs are particulary challanging in manufacturing sector.

• NTMs in Agriculture: Sanitary and Photosanitay measures (SPS), technical barriers to trade (TBT), and rules of origin.

Agriculture Manufacturing0

5

10

15

20

25

30

35

40

45

NTMExportP

erce

nt

Share of burdensome NTMs and exports in LAS

• NTMs in Manufacture: Rules of origin is the main callenge followed by SPS and TBT measures.

C. High Non-Tariff Measures (NTM) among Arab countries

• The most performing Arab countries is the UAE

• The second Arab country appears only at the 33 rank

• Most of the remaining countries still poor in terms of facility of trade.

• Poor logistics performance index means high cost of trade.

• In many Arab countries, the expected impacts from tariff removal have been offset by the high logistic costs

• To ensure gains from trade, Arab countries must make significant efforts in reducing technical barreirs to trade through the modernization of its infrastructure and logistics related to trade.

Economy rank score % of highest performer Singapore 1 4.13 100.00Hong Kong SAR, China 2 4.12 99.90United Arab Emirates 17 3.78 88.90Qatar 33 3.32 74.30Saudi Arabia 37 3.18 69.70Tunisia 41 3.17 69.40Morocco 50 3.03 65.00Egypt, Arab Rep. 57 2.98 63.30Oman 62 2.89 60.40Yemen, Rep. 63 2.89 60.30Kuwait 70 2.83 58.50Syrian Arab Republic 92 2.60 51.30Lebanon 96 2.58 50.60Jordan 102 2.56 49.80Algeria 125 2.41 45.30Mauritania 127 2.40 44.70Libya 137 2.28 41.00Iraq 145 2.16 37.10Sudan 148 2.10 35.30Djibouti 154 1.80 25.50Burundi 155 1.61 19.50

D. . High Cost of Logistics LPI is built around a survey of logistics

professionals. By asking freight forwarders to rate countries on key logistics issues— such as

customs clearance efficiency, infrastructure quality, and the ability to track cargo— It captures a broad

set of elements that affect perceptions of the efficiency of trade logistics in practice

The Logistics Performance Indicator provides a simple, global benchmarkto measure logistics performance

High disparities in terms of macroeconomic and sectoral policies

Convergence in macroeconomic and sectoral policies is found to be a key factor for the success of regional integration shemes

The three pillars for a successful regional integration are: - Convergence in terms of monetary policies-Convergence in terms of fiscal policies- Convergence in sectoral policies.

• Macroeconomic policies are too heterogeneous in the Arab word: Monetary policies are an example, where Arab countries did not achieved the minimum level of convergence. Some of them pegged their currencies to the US Dollar while others are more flexible.

• The objective of monetary policies itself is not homogeneous among countries: targeting inflation, increasing domestic investment, or mobilizing savings...

• Sectoral policies in terms of subsidies and public support harm competition and accordingly many countries excluded a significant lists of products from their inter-Arab agreements, mainly in Agriculture and related industries

E. . High disparities in terms of macroeconomic and sectoral policies

Impact of reduction of the cost of transport s in the Region within the

context of DAFAT?

Scenarios definition

18

Sim 1 (FTA): A full implementation of intra-Arab FTA

Sim2 (TR) =Sim1+ a 50% reduction of intra-Arab transport costs

Sim3 (CU) : Sim2+ a customs union between all Arab countries.

Sim4 (Migration): Sim3+the replacement of 20% of non Arab migrant stock by Arab migrants.

sim4:sim3+ An Arab

preference for migration

quotas in OPC

sim3: sim3+a common

external tariffs (for non

agriculture products

sim2: sim1+ 50% reduction in

transport cost

sim1: A complete Free trade Area

Simulations results:

Impacts on trade

Intra Arab trade variation

19

sim1 sim2 sim3 sim40.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

10.1

38.5

32.6 33.0

ref sim1 sim2 sim3 sim40.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

8.59.3

11.510.6 10.7

A full implementation of the FTA supports the increase of intra-Arab trade by around 10 per cent. If 50 per cent transport cost is reduced intra-Arab trade could increase by 38.5%.

The application of common external tariff increases trade with non-Arab partners as the market access will increase in both directions.

Share of the intra-Arab trade in total trade

Simulations results:

Impacts on GDP at regional

level

20

Variation of GDP

Impact on GDP ranges from 0.17 % in scenario 1 to more than 3.56% in scenario 4.

This increase is shown for both oil and non-oil producing Arab economies with more increase in non oil economies.

Scenario 4 shows, in oil producing countries the GDP increases around 3% compared to 4.45% increase in non oil producing countries.

Simulations results: Impacts

on GDP at country level

Substantially impact on GDP is shown in all Arab countries.

Egypt will in particular benefit and will enjoy a 5.49% increase in GDP.

A number of GCC countries will also benefit such as SA, UAE Bahrain, Kuwait.

The impact on GDP is low in Oman and Qatar.

Saudi Arabia

UAE

Bahrain

Kuwait

Oman

Qatar

Rest of North Africa

Egypt

Tunisia

Morocco

Rest of Mashreq

-1 0 1 2 3 4 5 6

0.12

0.12

0.15

0.04

0.05

0.01

-0.14

0.55

0.03

0.12

0.42

1.22

0.620000000000001

2.13

0.52

0.820000000000001

0.45

0.15

1.58

1.04

0.42

2.24

2.88

2.88

4.14

3.11

1.24

1.27

1.94

3.23

2.1

0.55

3.37

4

4.07

4.01

3.36

0.34

0.98

1.95

5.49

3.08

2.39

4.43

Migration CU Transport cost reduction FTA

21

How to reduce Trade Costs? ESCWA’s activities

• Current activities• 1. Identification and costing of

technical barriers to trade: A survey on trade costs in selected Arab countries and on selected commodities

• 2. Costing of strategies and impacts analysis: Impacts of reduction in trade costs on economic performance in the Arab region (by country) through alternative options of public-private investments and financing

• 3. Aid for Trade: • Identification of projects to

reduce trade costs (by country)• Costing the identified projects

(by country)• Comparative financing options

for trade costs related projects (by country)

• Economic implications (by country)

Conclusions

• Removing trade barriers is good but not enough

• Making countries able to take advantage from trade openness is more challenging than removing tariffs

• Other barriers and obstacles require specific and additional attention:

• - inefficient trade logistics• - costly transport and financial

services• - low productive capacities and

poor diversification• - poor policy coordination and

convergence

Thanks for your attention