Employee BenefitsEmployee BenefitsEmployee Benefits(IAS 19)

Employee Benefits(IAS 19)(IAS 19)(IAS 19)

ByByCA. Rajkumar S AdukiaCA. Rajkumar S Adukia

B Com (Hons )B Com (Hons ) FCA ACS MBA AICWAFCA ACS MBA AICWAB.Com (Hons.) B.Com (Hons.) FCA, ACS, MBA, AICWA, FCA, ACS, MBA, AICWA, LLBLLB ,,Dip IFRS(UK) DLL& LWDip IFRS(UK) DLL& LW

[email protected]@gmail.comwww carajkumarradukia cwww carajkumarradukia comom

www.carajkumarradukia.com 1

www.carajkumarradukia.cwww.carajkumarradukia.comom09820061049/0932306104909820061049/09323061049

Employee BenefitsEmployee Benefits

• In 1983, IAS 19 was titled as “Accounting f R ti t B fit i Fi i lfor Retirement Benefits in Financial Statements of Employers”

• In 1993, IAS 19 was titled as “Retirement Benefit Costs”

• In 1998, it was titled as “Employee Benefits”

www.carajkumarradukia.com 2

Objectives of IAS 19Objectives of IAS 19jj

• IAS 19 Employee Benefits prescribes the accounting andIAS 19 Employee Benefits prescribes the accounting and disclosure by employers for employee benefits.

Th St d d i tit t i• The Standard requires an entity to recognize:(a) A Liability: A liability when an employee has provided service in exchange for employee benefits to p g p ybe paid in the future; and(b) An Expense: An expense when the entity consumes the economic benefit arising from service provided by anthe economic benefit arising from service provided by an employee in exchange for employee benefits.

www.carajkumarradukia.com 3

Scope of IAS 19Scope of IAS 19

The scope is broad and includes wages, p gvacation or holiday pay, bonus,

termination benefits, etc. as well as retirement plans

Covers full-time, part-time, temporary staff and directors

www.carajkumarradukia.com 4

staff and directors

Basic Principle of IAS 19Basic Principle of IAS 19

• The cost of providing employee benefits h ld b i d i th i d ishould be recognized in the period in

which the benefit is earned by the l th th h it i idemployee, rather than when it is paid or

payable.

www.carajkumarradukia.com 5

IAS 19 – Employee Benefits -IAS 19 – Employee Benefits -p yp y

• The Standard identifies following• The Standard identifies following categories of employee benefits to be coveredcovered– Short term employee benefits

Post employment benefits– Post-employment benefits– Other long term employee benefits

T i ti b fit– Termination benefits• It covers formal plans, state plans,

( f )www.carajkumarradukia.com 6

constructive obligation (informal practices)

IAS 19 Applies toIAS 19 Applies to1. Wages and Salaries 2. Compensated Absences (paid vacation and sick leave) 3 P fi Sh i Pl3. Profit Sharing Plans 4. Bonuses 5. Medical and Life Insurance Benefits during employment 6 Housing Benefits6. Housing Benefits 7. Free or Subsidised goods or services given to employees 8. Pension Benefits 9 Post-Employment Medical and Life Insurance Benefits9. Post Employment Medical and Life Insurance Benefits 10. Long-Service or Sabbatical Leave 11. ‘Jubilee' Benefits 12. Deferred Compensation Programmes p g13. Termination Benefits.

www.carajkumarradukia.com 7

The Standard Does not apply toThe Standard Does not apply to

• This standard does not apply to benefits hi h d t d th IFRS2which needs to cover under the IFRS2

share-based payment• This Standard does not deal with reporting

by employee benefit plans (covered under IAS 26) e.g. accounting and reporting by trust plans

www.carajkumarradukia.com 8

Revised IAS 19 Revised IAS 19

• The IASB had published a revised version f IAS 19 E l B fit 16th Jof IAS 19 Employee Benefits on 16th June

2011. • The revised standard will be applicable for

reporting period starting on or after 1st January 2013

www.carajkumarradukia.com 9

Highlights of Revised IAS 19Highlights of Revised IAS 19• Revised IAS 19 requires full recognition of deficit or

surplus (actuarial gains and losses) to be fully p ( g ) yrecognized on the balance sheet date.

• Under the revised standard the net interest income is included is introduced as the equivalent of expectedincluded is introduced as the equivalent of expected return on plan assets under IAS 19.

• The defined benefit cost under the revised standard comprises of service cost net interest andcomprises of service cost, net interest and remeasurements.

• A very extensive disclosure requirements are put forth d h i d d d i ll h l iunder the revised standard especially those relating to

characteristics, risk and the presented figures in the financial statements regarding defined benefit plans

www.carajkumarradukia.com 10

The Revision impact on Enterprises

The Revision impact on Enterprises Enterprises Enterprises

• The “corridor approach” being removed• Assumption for the expected return on assets• Assumption for the expected return on assets

eliminated• Immediate recognition of the plan basedImmediate recognition of the plan based

amendments in the Profit or Loss account• Increased requirements on disclosure of

information• Removal of recognition of gains or losses in the

profit or loss accountprofit or loss account• Application of mark-to market approach and

‘ceiling tests’ on plan based assets

www.carajkumarradukia.com 11

ceiling tests on plan based assets

Revised Goal of Enterprises after Revision

Revised Goal of Enterprises after RevisionRevisionRevision

• Multinational companies with multiple pension funds should definitely increasepension funds should definitely increase their efforts to manage the risk of their pension fundspension funds.

• Listing of the most important local pension funds and stakeholdersfunds and stakeholders

• Evaluating the impact of the changed IAS 19 for your pensions19 for your pensions

• Looking at the possible IAS 19 proof solutions

www.carajkumarradukia.com 12

solutions

Revised Goal of Enterprises after Revision

Revised Goal of Enterprises after RevisionRevisionRevision

• Fix the corporate pension budget and redesign pension benefits within that budgetpension benefits within that budget

• Set up pension ambitions and acceptable levels of risk

• Fix a timeframe for derisking (if desired). • Initiate communications programme to support

the employer and employees • Given that pension risks have become more

obvious companies are no longer rewarded withobvious, companies are no longer rewarded with lower pension expenses resulting in increased risk

www.carajkumarradukia.com 13

Type of Employee Benefit Plans

Type of Employee Benefit PlansPlansPlans

• Defined Benefit : Some formula/Monetary• Defined Benefit : Some formula/Monetary promise.

• Defined Contribution : Just contribution defined no promise of benefit.p

www.carajkumarradukia.com 14

Type of Employee Benefit PlansType of Employee Benefit Plans

• Hybrid Plans : Where employer’s obligation is not limited to contributions toobligation is not limited to contributions to the fund but has legal or constructive obligation such asobligation such as– Scheme having benefit formula that is not

linked solely with accumulation (hybridlinked solely with accumulation (hybrid schemes)

– Scheme providing guarantee either indirectly– Scheme providing guarantee, either indirectly through a plan or directly, of a specified return on contributions

www.carajkumarradukia.com 15

Termination BenefitsTermination Benefits

• Termination benefits are employee benefits payable as a result ofbenefits payable as a result of– Employer’s decision to terminate an

employee’s employmentp y p y– Employee’s decision to accept voluntary

redundancy in exchange for those benefitsy g

www.carajkumarradukia.com 16

Termination BenefitsTermination Benefits• An entity is committed to a termination when,

and only when, the entity has a detailed formal y , yplan (with specified minimum contents) for the termination and is without realistic possibility of withdrawal.withdrawal.

• Where termination benefits fall due more than 12 months after the balance sheet date, they should be discountedshould be discounted.

• In the case of an offer made to encourage voluntary redundancy, the measurement of y ytermination benefits should be based on the number of employees expected to accept the offer

www.carajkumarradukia.com 17

M lti E l PlMulti Employer Plans

• Where it is defined benefit plan and information is available, account and disclose proportionate share as though it were defined benefit plan of reporting entitythough it were defined benefit plan of reporting entity

• If information is not available, account for it as though it were a defined contribution plane e a de ed co t but o p a

www.carajkumarradukia.com 18

Defined Contribution Plan - DCP

www.carajkumarradukia.com 19

Defined Contribution Plan Defined Contribution Plan

• Employer pays fixed contribution to an t l f d ( ll % f l )external fund (usually % of salary).

• Employer’s obligation is discharged upon payment of the contribution.

• Members benefits depend upon p pperformance of the fund over time.

• Employees run the risk of investmentEmployees run the risk of investment

www.carajkumarradukia.com 20

DCP – Financial StatementDCP – Financial Statement

• Income statement:– Record contribution as expense in Income

Statement• Balance sheet:

– No impact on balance sheet other than outstanding contributions payable to the investment funds.

www.carajkumarradukia.com 21

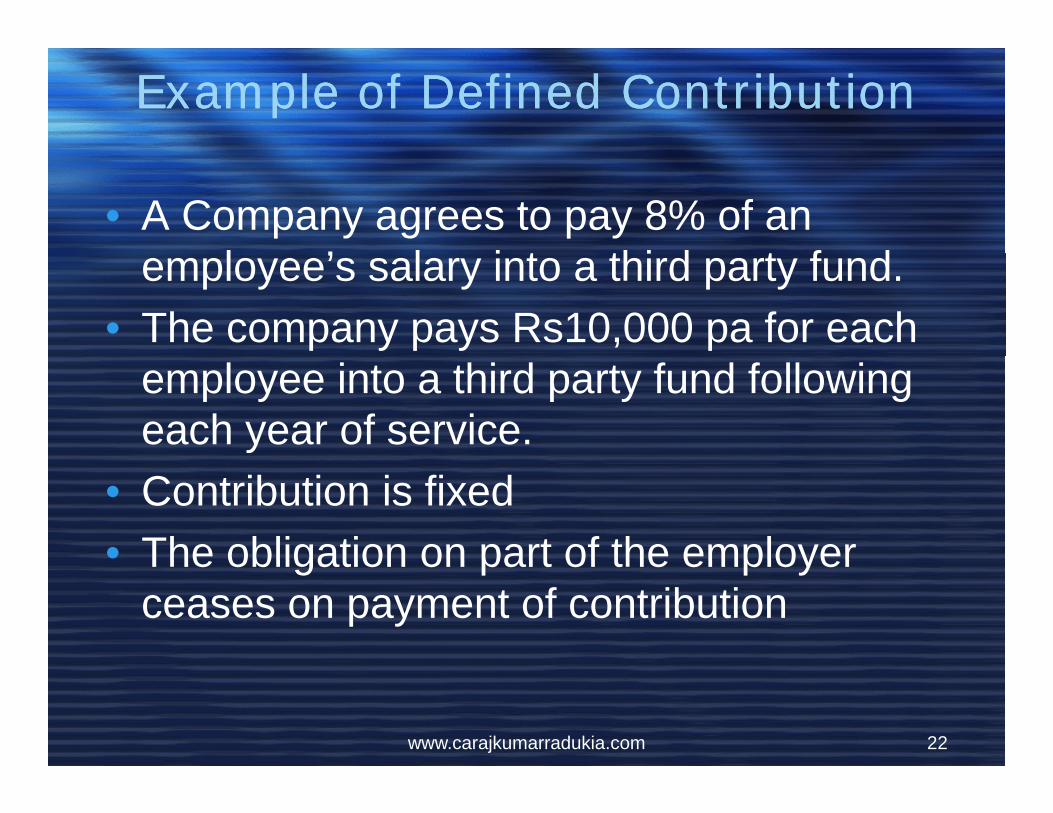

Example of Defined ContributionExample of Defined Contribution

• A Company agrees to pay 8% of an l ’ l i t thi d t f demployee’s salary into a third party fund.

• The company pays Rs10,000 pa for each employee into a third party fund following each year of service.

• Contribution is fixed• The obligation on part of the employerThe obligation on part of the employer

ceases on payment of contribution

www.carajkumarradukia.com 22

Defined Benefit Plan - DBP

www.carajkumarradukia.com 23

Defined Benefit PlanDefined Benefit Plan

• Expected Future Payments are required to ttl th b fitsettle the benefits

• An Actuary calculates the Obligation• The obligation can be arrived at

– Based on the Service and current SalaryBased on the Service and current Salary levels

– Based on the Service and future Salary levelsy– Based not on the future employee services

www.carajkumarradukia.com 24

Defined Benefit SchemesDefined Benefit Schemes

• It may be monthly pension or lump sum• Calculated based on the salary and years

of service• Pay is Final Pay or Average Pay• The actuary calculates the liabilityThe actuary calculates the liability• Company bears the risk of meeting the

future obligationfuture obligation

www.carajkumarradukia.com 25

Example of Defined BenefitExample of Defined Benefit

• The company agrees to pay 6% of their fi l l f h f ifinal salary for each year of service or

• The company agrees to provide a lump sum amount, amounting to 5 times of the final salary

Where any scheme does not fall within the rules of Defined Contribution it automatically falls under Defined Benefit

www.carajkumarradukia.com 26

Arriving at DBP LiabilityArriving at DBP Liability

• The defined benefit obligation (DBO) i d i th b l h t irecognized in the balance sheet is:

– Present value of DBO– Plus actuarial gains not yet recognized– Less actuarial losses not yet recognized– Less past services costs not yest recognized– Less fair value of plan assets

www.carajkumarradukia.com 27

Accounting for Defined Benefit Plan

www.carajkumarradukia.com 28

Valuation of Defined Benefit PlanValuation of Defined Benefit Plan

• Actuarial mathematics is typically used and it is specified by IAS 19 (Para 50(a))specified by IAS 19 (Para 50(a))

• It deals with – how liabilities should be apportioned in respect of “earned” andapportioned in respect of earned and “unearned” service

• It also deals with calculation of cost pertaining toIt also deals with calculation of cost pertaining to accrual of benefits in the plan over the most recent accounting periodg p

• Actuarial funding method known as “projected unit method” is prescribed by IAS 19

www.carajkumarradukia.com 29

Various Asset Valuation MethodsVarious Asset Valuation Methods

• Asset valuation methods can be classified i t f d i ifi th dinto four groups and nine specific methods– Fair market value (1 method) – Discounted cash flow (1 method)– Book value ( 3 methods cost, amortized,

contract)– Smoothed value ( blend of cost and market,

it d f d itiwrite-up, deferred recognition, average market value).

www.carajkumarradukia.com 30

List of 9 asset valuation methodsList of 9 asset valuation methods

1. Fair Market Value Method2 Di t d C h Fl M th d2. Discounted Cash Flow Method3. Cost Book Value Method4. Amortized Book Value Method5. Contract Book Value Method6. Blend of Cost and Market Value Method7. Write Up Value Method7. Write Up Value Method8. Deferred recognition Method9 Average Market Value Method

www.carajkumarradukia.com 31

9. Average Market Value Method

Actuarial Gains & Losses Recognized Immediately under

Actuarial Gains & Losses Recognized Immediately under

revised IAS 19 revised IAS 19

• Immediate Recognition of all Plans in the Statement of recognized income & expense.

www.carajkumarradukia.com 32

Funding of Pension Plansg

www.carajkumarradukia.com 33

Funding of Pension PlansFunding of Pension Plans

• Contribution of Assets to a legal entity t f th t f th E lseparate from that of the Employer

• The Legal Entity being a Trust• Value of Assets < or> Value of Liability• The scheme is funded in surplus if AssetsThe scheme is funded in surplus if Assets

are more• The scheme is funded in deficit if Liabilities• The scheme is funded in deficit if Liabilities

are more

www.carajkumarradukia.com 34

Pension Plans with no Funding Pension Plans with no Funding

• A very less secure Plan• Company Funds are used to pay the

Pension Plans• There is no question setting aside of

assets for payment of pension liabilitiesp y p

www.carajkumarradukia.com 35

Actuarial Assumptions

www.carajkumarradukia.com 36

Actuarial Valuation AssumptionsActuarial Valuation Assumptions

• Financial Assumptions• Demographic Assumptionsg p p

www.carajkumarradukia.com 37

How assumptions are arrived at?How assumptions are arrived at?

• Set by the Employer with advise from a t ditactuary or auditor

• Estimate that are compatible• Market expectation as at the balance

sheet date

www.carajkumarradukia.com 38

Financial AssumptionsFinancial Assumptions

• Discount Rate• Salary Rate Hikes• Expected Return on Assets (EROA)p ( )

www.carajkumarradukia.com 39

Demographic AssumptionsDemographic Assumptions

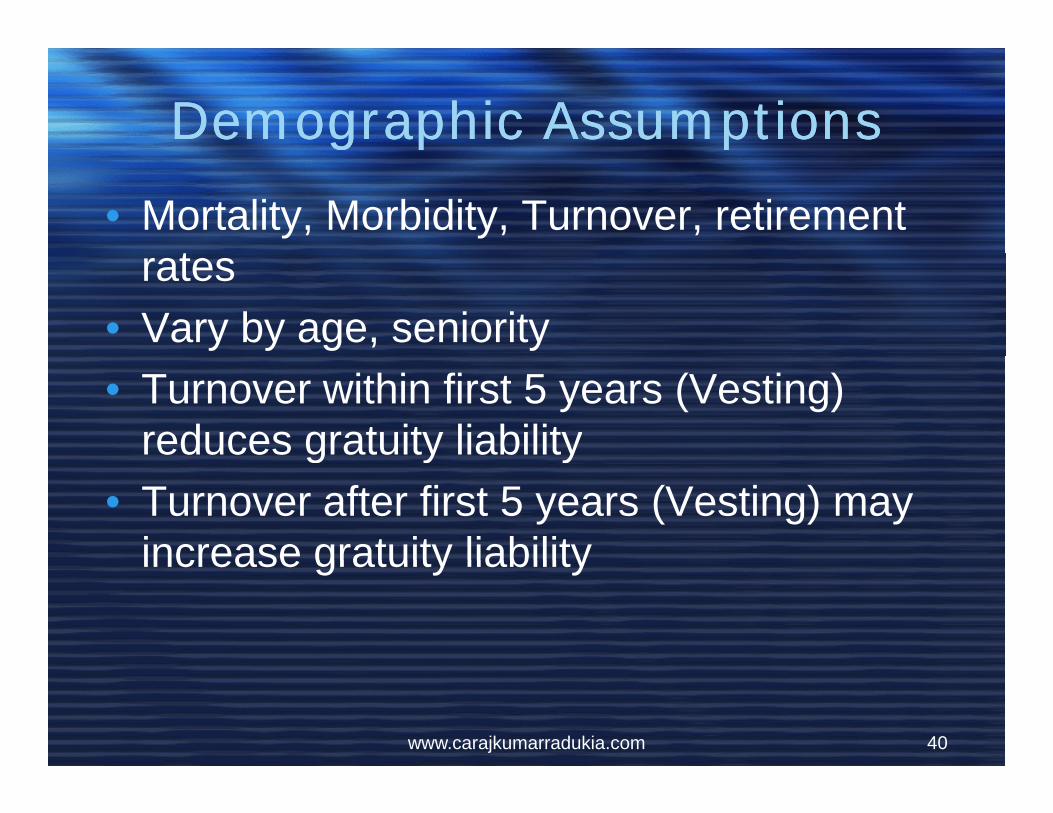

• Mortality, Morbidity, Turnover, retirement trates

• Vary by age, seniority• Turnover within first 5 years (Vesting)

reduces gratuity liabilityg y y• Turnover after first 5 years (Vesting) may

increase gratuity liabilityincrease gratuity liability

www.carajkumarradukia.com 40

Effects of changes in actuarial assumptions

Effects of changes in actuarial assumptionsassumptionsassumptions

Assumption Increase DecreaseLiab would

Discount rate

Liab would decrease and leads to actuarial

i

Liab would increase and

leads to actuarialrate gain leads to actuarial loss

Salary Liab would increase Liab would Salary Increase Rate

Liab would increase and leads to actuarial

loss

decrease and will lead to actuarial

igainExpected long-term High expected return Low expected

www.carajkumarradukia.com 41

long term rate of return

results in low pension cost

return results in high pension cost

Asset Ceiling Test

www.carajkumarradukia.com 42

Asset Ceiling Test (ACT)Asset Ceiling Test (ACT)

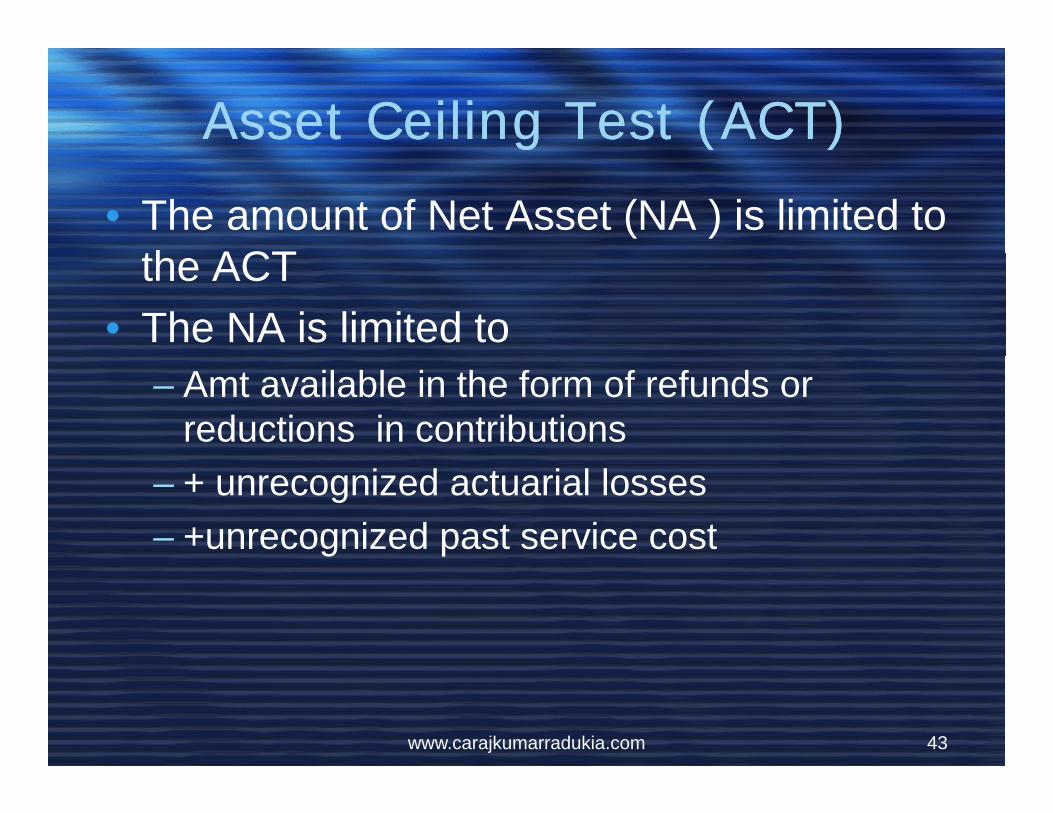

• The amount of Net Asset (NA ) is limited to th ACTthe ACT

• The NA is limited to – Amt available in the form of refunds or

reductions in contributions– + unrecognized actuarial losses– +unrecognized past service cost

www.carajkumarradukia.com 43

Why ACT?Why ACT?

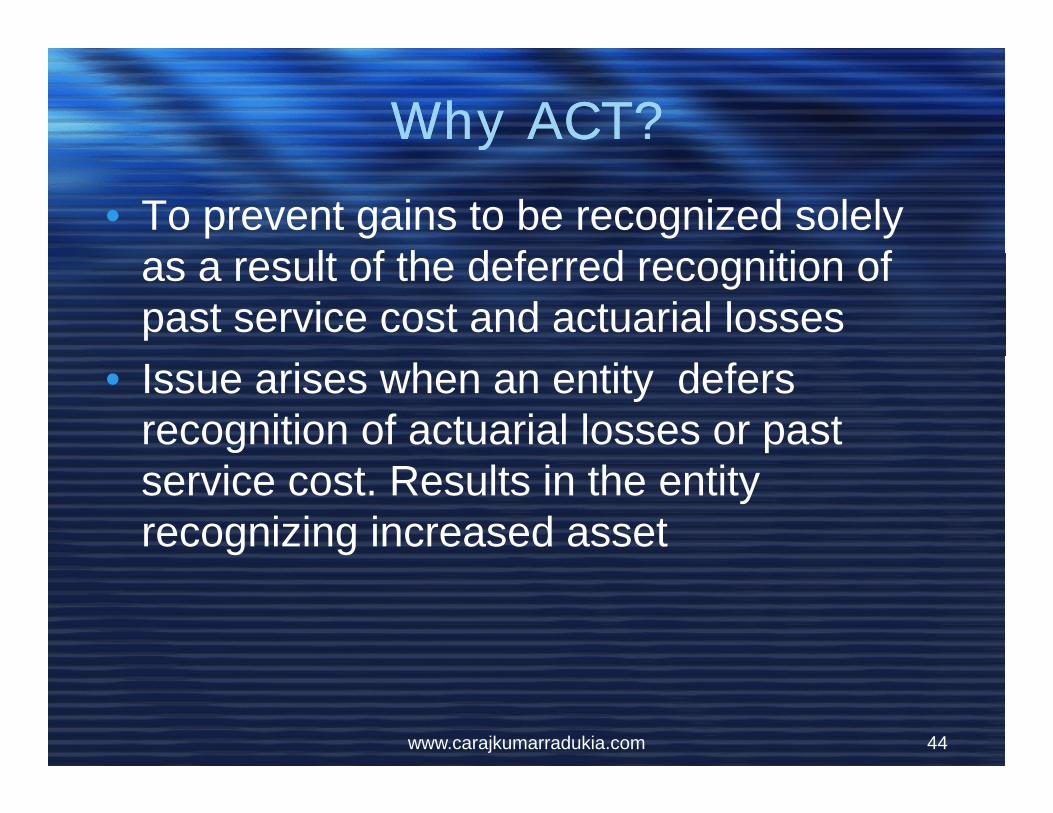

• To prevent gains to be recognized solely lt f th d f d iti fas a result of the deferred recognition of

past service cost and actuarial losses• Issue arises when an entity defers

recognition of actuarial losses or past service cost. Results in the entity recognizing increased asset

www.carajkumarradukia.com 44

IFRIC 14: IAS 19 - The Limit on a Defined Benefit Asset, Minimum Funding IFRIC 14: IAS 19 - The Limit on a

Defined Benefit Asset, Minimum Funding , gRequirement and their Interaction

, gRequirement and their Interaction

Th i dd d i thi i t t ti• The issues addressed in this interpretation are:• When refunds or reductions in future

t ib ti h ld b d d il bl icontributions should be regarded as available in accordance of IAS 19

• How a minimum funding requirement might• How a minimum funding requirement might affect the availability of reduction in future contributionscontributions

• When a minimum funding requirement might give rise to a liability

www.carajkumarradukia.com 45

g y

AS 15 – Employee BenefitsAS 15 – Employee Benefits

• It covers all type of employees full time part timeIt covers all type of employees, full time, part time, permanent , casual or temporary basis.

• This statement does not deal with accounting and reporting by employee benefit planreporting by employee benefit plan.

• Employee benefit expense should be charged to P & L, unless other accounting standard requires It to be d bit d t t f t ( AS 10)debited to cost of assets (e.g. AS-10).

• It does not apply to only benefits provided under formal plans and arrangement, it also applies to those informal p g , pppractices that give rise to an obligation (i.e where enterprise has no alternative but to pay employee benefit).

www.carajkumarradukia.com 46

)

AS 15 – Employee BenefitsAS 15 – Employee Benefits• The rate of discount should be determined with

reference to market yields on government bonds, the y g ,currency and terms of which should be consistent with the estimated terms of the obligation.

• Where an enterprise has its own Provident Fund, there is an obligation to pay the minimum interest prescribed by the authorities irrespective of the interest actually earnedthe authorities irrespective of the interest actually earned by the Fund. In such an event this would need to be treated as a defined “benefit” plan instead of as defined “contribution” plan and additional provisioning for anycontribution plan and additional provisioning for any expected shortfall in interest may need to be made.

www.carajkumarradukia.com 47

Ind AS 19Ind AS 19

• Ind AS 19 does not currently cover all of th b t f IAS 19 i d ithe above aspects of IAS 19 revised in 2011, but it does require actuarial gains

d l t b i d i thand losses to be recognised in other comprehensive income (OCI).

www.carajkumarradukia.com 48

Ind AS 19 Vs IAS 19Ind AS 19 Vs IAS 19• Actuarial gains and losses for post-employment defined

benefit plans and other long-term employee benefit plansp g p y p– Ind AS - All actuarial gains and losses for post-employment

defined benefit plans and other-long term employment benefit plans are recognised in OCI.

– IAS - Actuarial gains and losses for defined benefit plans can be recognised using one of the following three alternatives: in profit or loss; or in OCI or using corridor approach( no corridor approach available and immediate recognition (June 2011approach available and immediate recognition (June 2011 amendment),

– IAS - Actuarial gains and losses for other-long term employment benefit plans are recognised in profit or loss.p g p

www.carajkumarradukia.com 49

Ind AS 19 Vs IAS 19Ind AS 19 Vs IAS 19• Discount rate for employee benefit obligations

– Ind As - Discount rate used to discount employee benefit obligations shall be determined by referencebenefit obligations shall be determined by reference to market yields at the end of the reporting period on government bonds only.

– IAS - Discount rate used to discount employee benefit obligations shall be determined by reference to market yields at the end of the reporting period onmarket yields at the end of the reporting period on high quality corporate bonds.

www.carajkumarradukia.com 50

FAS 158 -Employers’ Accounting for Defined Benefit Pension and FAS 158 -Employers’ Accounting for Defined Benefit Pension and for Defined Benefit Pension and

Other Postretirement Plans for Defined Benefit Pension and

Other Postretirement Plans

This Statement requires an employer that is a business entity and sponsors one or more single-employer defined benefit plans to:

• Recognize the funded status of a benefit plan • Recognize as a component of other

comprehensive income, net of tax, the gains or l d i i di hlosses and prior service costs or credits that arise during the period but are not recognized as components of net periodic benefit cost pursuant

www.carajkumarradukia.com 51

components of net periodic benefit cost pursuant

FAS 158 -Employers’ Accounting for Defined Benefit Pension and FAS 158 -Employers’ Accounting for Defined Benefit Pension and

Other Postretirement PlansOther Postretirement Plans

• to FASB Statement No. 87, Employers’ Accounting for Pensions, or No. 106,Accounting for Pensions, or No. 106, Employers’ Accounting for Postretirement Benefits Other Than Pensions.Benefits Other Than Pensions.

• Measure defined benefit plan assets and obligations as of the date of theobligations as of the date of the employer’s fiscal year-end statement of financial position (with limited exceptions)

www.carajkumarradukia.com 52

financial position (with limited exceptions).

FAS 158 -Employers’ Accounting for Defined Benefit Pension and FAS 158 -Employers’ Accounting for Defined Benefit Pension and

Other Postretirement PlansOther Postretirement Plans• Disclose in the notes to financial statements• Disclose in the notes to financial statements

additional information about certain effects on net periodic benefit cost for the next fiscal year p ythat arise from delayed recognition of the gains or losses, prior service costs or credits, and transition asset or obligationtransition asset or obligation.

• This Statement also applies to a not-for-profit organization or other entity that does not report g y pother comprehensive income. This Statement’s reporting requirements are tailored for those entities

www.carajkumarradukia.com 53

entities.

Other FAS on Employee BenefitsOther FAS on Employee Benefits

• FAS Statement No. 87, Employers' Accounting for Pensionsfor Pensions

• FAS Statement No. 88, Employers’ Accounting for Settlements and Curtailments of Defined Benefit Pension Plans and for Termination Benefits,FAS St t t N 106 E l ' A ti• FAS Statement No 106, Employers' Accounting for Postretirement Benefits Other Than Pensions

• FAS Statement No 132 (revised 2003)FAS Statement No. 132 (revised 2003), Employers’ Disclosures about Pensions and Other Postretirement Benefits

www.carajkumarradukia.com 54

Disclosure Requirements

www.carajkumarradukia.com 55

Disclosure under IAS 19Disclosure under IAS 19IAS 19 requires company to disclose:• Positions of liabilities and assetsPositions of liabilities and assets• Key assumptions used to calculate these figures.• Explanations for the movement in balances• P&L expense recognized in the period• Material “one-off” transactions• Analysis of funded/ unfunded balances• Analysis of funded/ unfunded balances• Sensitivity information about medical cost trend rates• Five year history of experience adjustments on DBO and

on plan assets

www.carajkumarradukia.com 56

Questions/ Suggestions/ Questions/ Suggestions/ Comments???Comments???

Questions/ Suggestions/ Questions/ Suggestions/ Comments???Comments???

www.carajkumarradukia.com 57

www.carajkumarradukia.com 58