Disease Trends: Challenges and

Opportunities

Credit Insurers Association

Mark Skillan, M.D., Consulting Medical DirectorMay 11, 2017

Leading Causes of Death and Disease Trends in the U.S.

Select Areas of Interest

▪ Heart Disease

▪ Diabetes

▪ Cancer: Lung, Breast, Prostate, Colon, Melanoma

More Recent Trends/Challenges in Risk Assessment

▪ HIV

▪ e-Cigarettes

▪ Gender Identity

▪ Genetic testing/Rare Diseases

Agenda

2© 2015 Munich American Reassurance Company. All rights reserved.

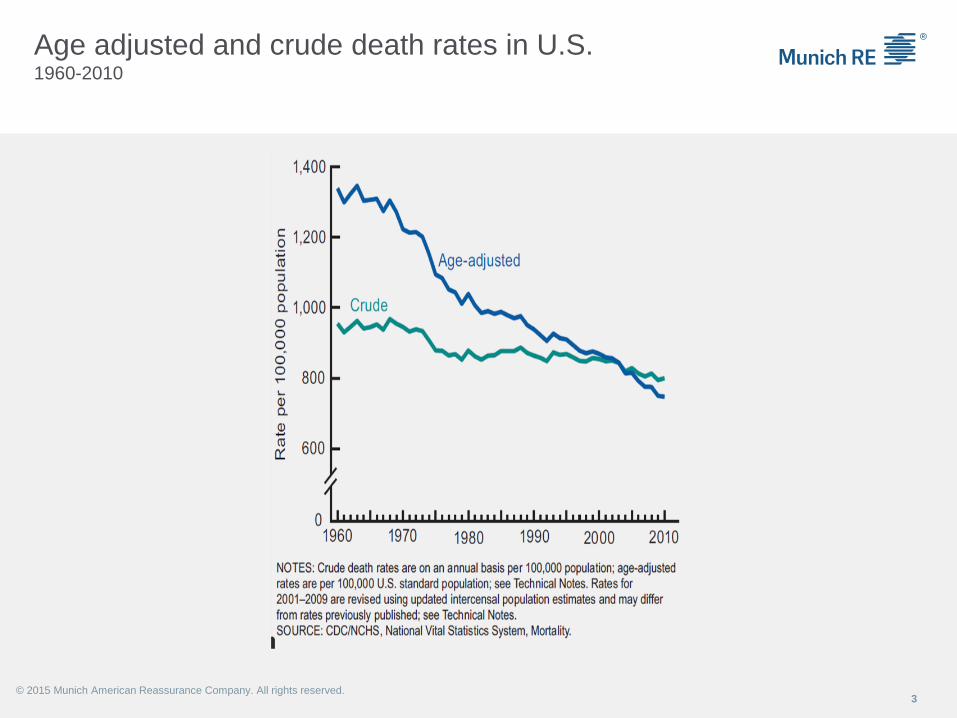

Age adjusted and crude death rates in U.S. 1960-2010

3© 2015 Munich American Reassurance Company. All rights reserved.

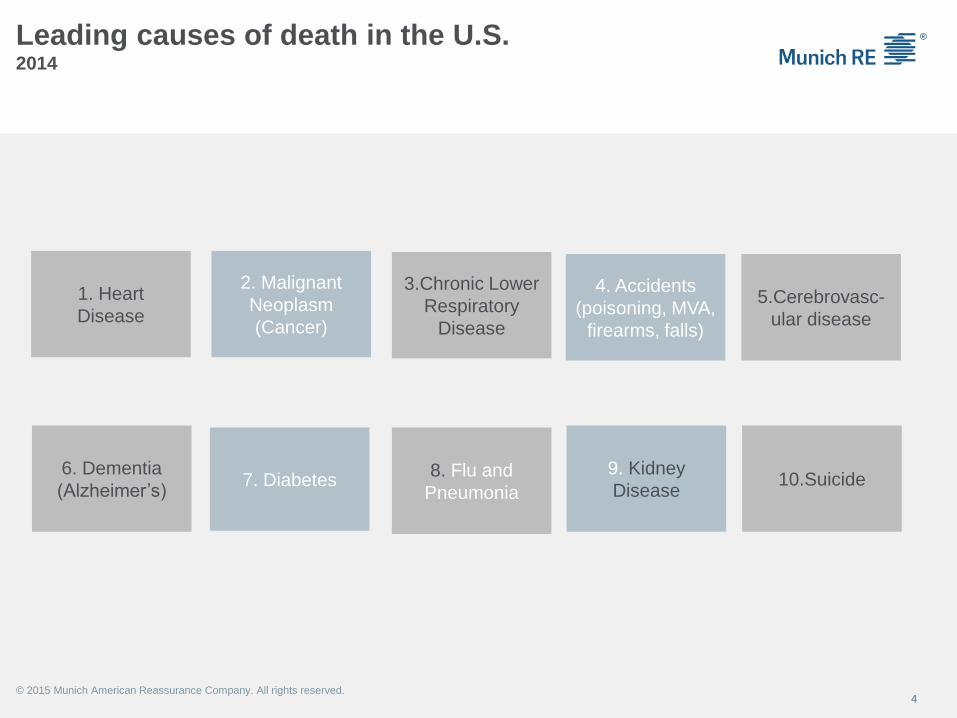

Leading causes of death in the U.S.2014

4

1. Heart

Disease

6. Dementia

(Alzheimer’s)

2. Malignant

Neoplasm

(Cancer)

7. Diabetes

3.Chronic Lower

Respiratory

Disease

8. Flu and

Pneumonia

4. Accidents

(poisoning, MVA,

firearms, falls)

9. Kidney

Disease

5.Cerebrovasc-

ular disease

10.Suicide

© 2015 Munich American Reassurance Company. All rights reserved.

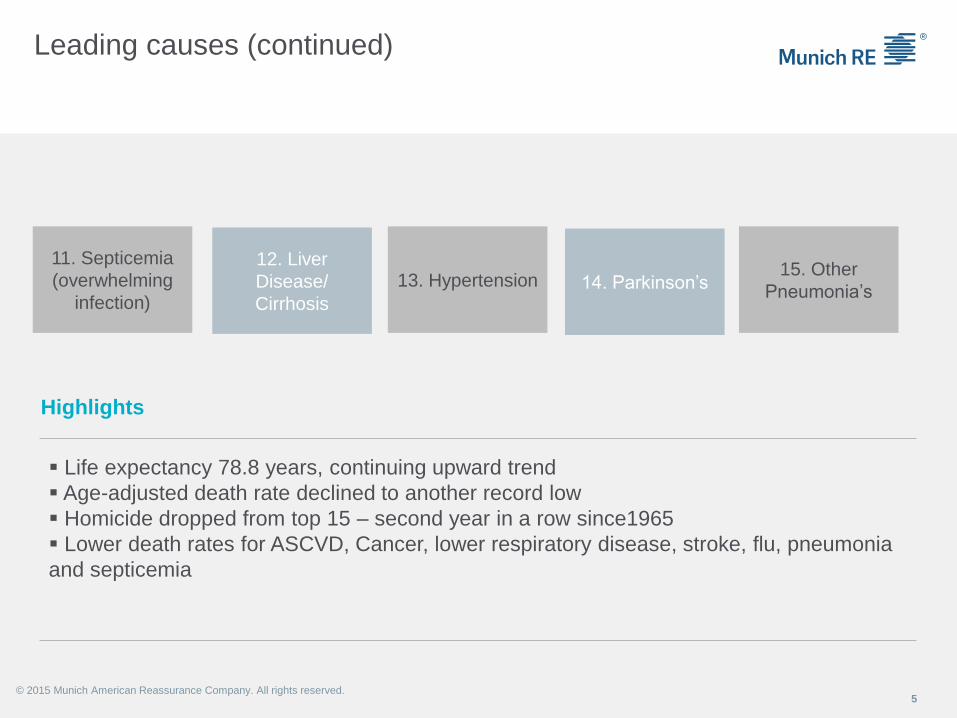

Leading causes (continued)

5

11. Septicemia

(overwhelming

infection)

12. Liver

Disease/

Cirrhosis

13. Hypertension 14. Parkinson’s15. Other

Pneumonia’s

▪ Life expectancy 78.8 years, continuing upward trend

▪ Age-adjusted death rate declined to another record low

▪ Homicide dropped from top 15 – second year in a row since1965

▪ Lower death rates for ASCVD, Cancer, lower respiratory disease, stroke, flu, pneumonia

and septicemia

Highlights

© 2015 Munich American Reassurance Company. All rights reserved.

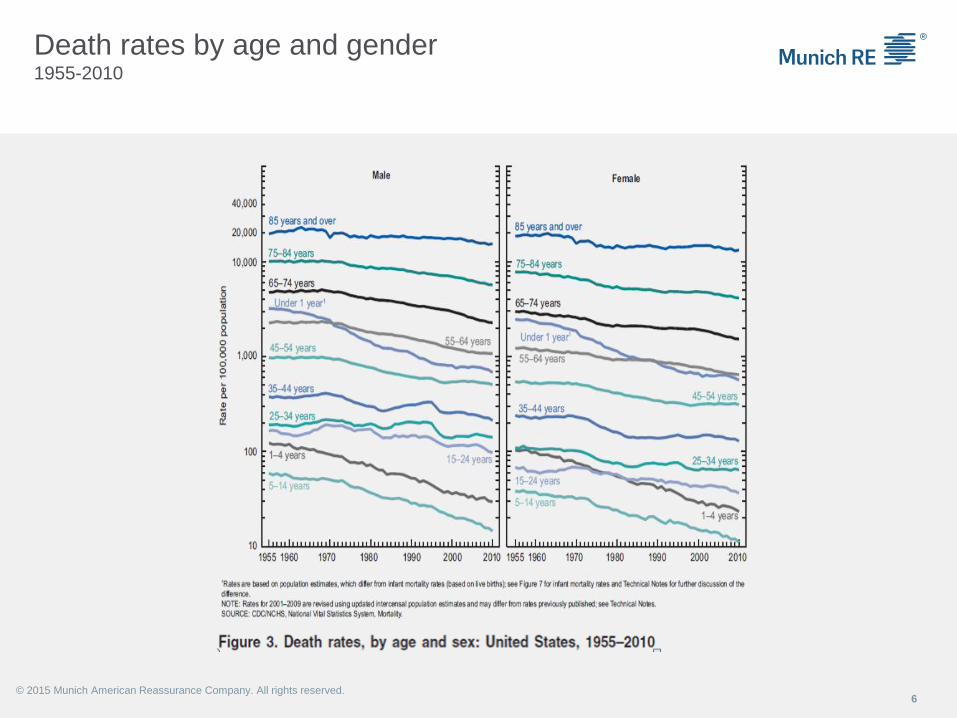

Death rates by age and gender 1955-2010

6© 2015 Munich American Reassurance Company. All rights reserved.

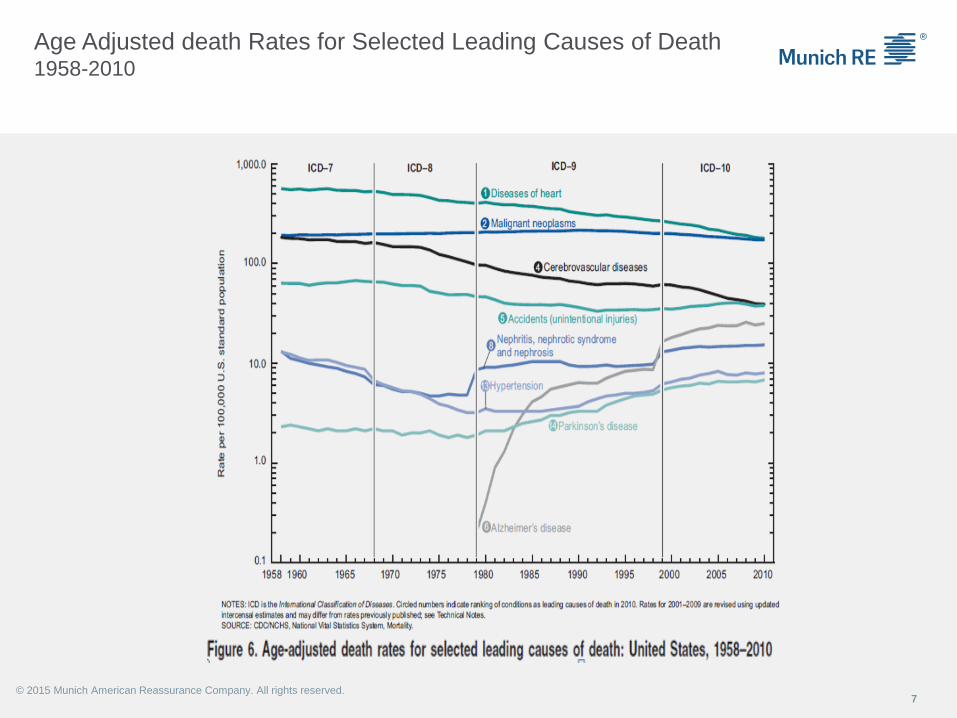

Age Adjusted death Rates for Selected Leading Causes of Death 1958-2010

7© 2015 Munich American Reassurance Company. All rights reserved.

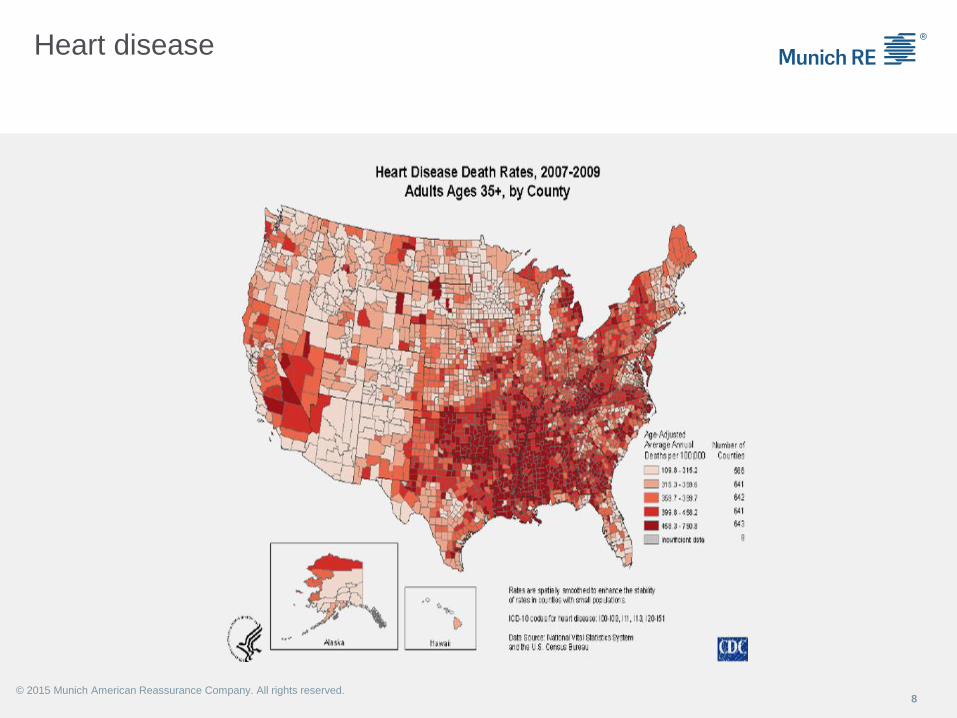

Heart disease

8© 2015 Munich American Reassurance Company. All rights reserved.

Interesting Observation…

5/15/2017Title of presentation and name of speaker 9

Heart disease

10

Leading cause of death for both men (>50%) and women

614,000 deaths per year (389,000 from CHD) in 2014

Incidence Trend

▪ Increasing with aging population and prevalence of overweight/diabetes

Mortality Trend

▪ Steady decline in age-adjusted death rate since 1980*

▪ Decreasing by 2% /yr in recent past

* small increase in 1993

© 2015 Munich American Reassurance Company. All rights reserved.

Heart disease – trends and implications

11

Mortality improvements related to risk factor modification ….and better care

▪ High blood pressure control – improved

▪ Lipids – definitely improved

▪ Smoking cessation – improved

▪ Diabetes – control improved in some groups

▪ Overweight/obesity – not so much

▪ Physical inactivity – improved in some groups

▪ Excessive alcohol – awareness improved

Improved meds – cardiac, BP, lipids

Improved care – diagnostics, PTCA, ICU/CCU, cardiac rehab, etc.

Trend likely to continue BUT impact of overweight/obesity may offset gains…

© 2015 Munich American Reassurance Company. All rights reserved.

Diabetes

12

Diabetes – 7th leading cause of death (7th likely an underrepresentation)

Estimated risk of death is about twice that of people of same age/gender without diabetes

Associated complications:

▪ Heart disease 2-4x risk

▪ Stroke 2-4x risk

▪ Hypertension – present in 67% of adults with DM

▪ Vision impairment/loss, a leading cause of acquired blindness

▪ Kidney disease – cause in 44% of new cases of renal failure

▪ Nervous system disease – leading cause of sensory, digestive issues, ED, CTS

▪ Limb loss – 60% of non-traumatic lower limb amputations are DM related

© 2015 Munich American Reassurance Company. All rights reserved.

Diagnosed diabetes, U.S. 1958-2010

13© 2015 Munich American Reassurance Company. All rights reserved.

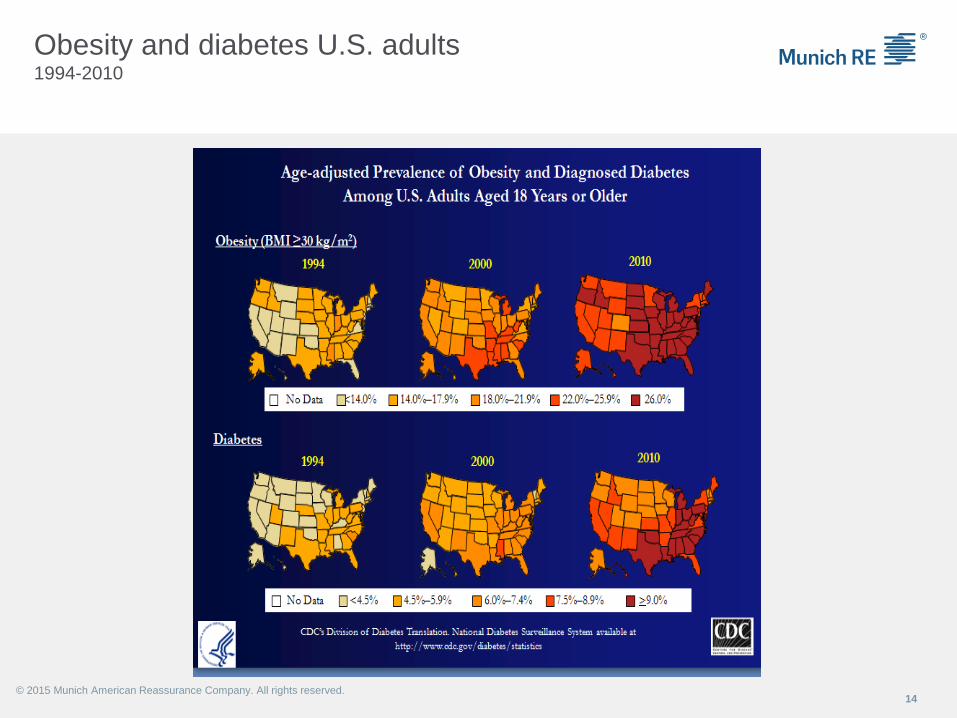

Obesity and diabetes U.S. adults 1994-2010

14© 2015 Munich American Reassurance Company. All rights reserved.

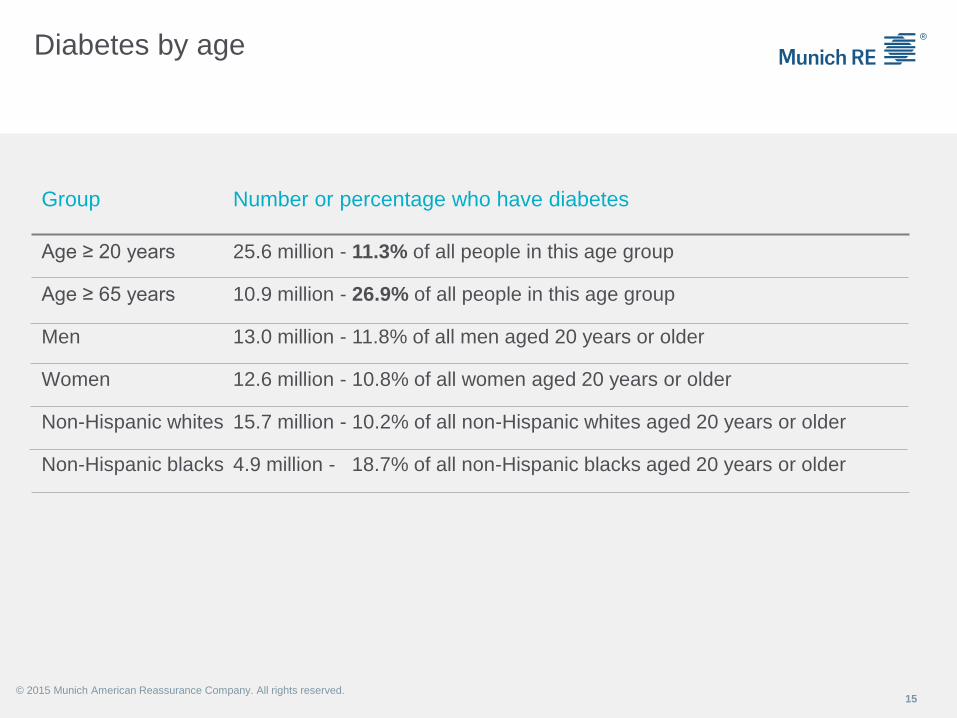

Diabetes by age

15

Age ≥ 20 years 25.6 million - 11.3% of all people in this age group

Group Number or percentage who have diabetes

Age ≥ 65 years 10.9 million - 26.9% of all people in this age group

Men 13.0 million - 11.8% of all men aged 20 years or older

Women 12.6 million - 10.8% of all women aged 20 years or older

Non-Hispanic whites 15.7 million - 10.2% of all non-Hispanic whites aged 20 years or older

Non-Hispanic blacks 4.9 million - 18.7% of all non-Hispanic blacks aged 20 years or older

© 2015 Munich American Reassurance Company. All rights reserved.

Age group and diabetes

16© 2015 Munich American Reassurance Company. All rights reserved.

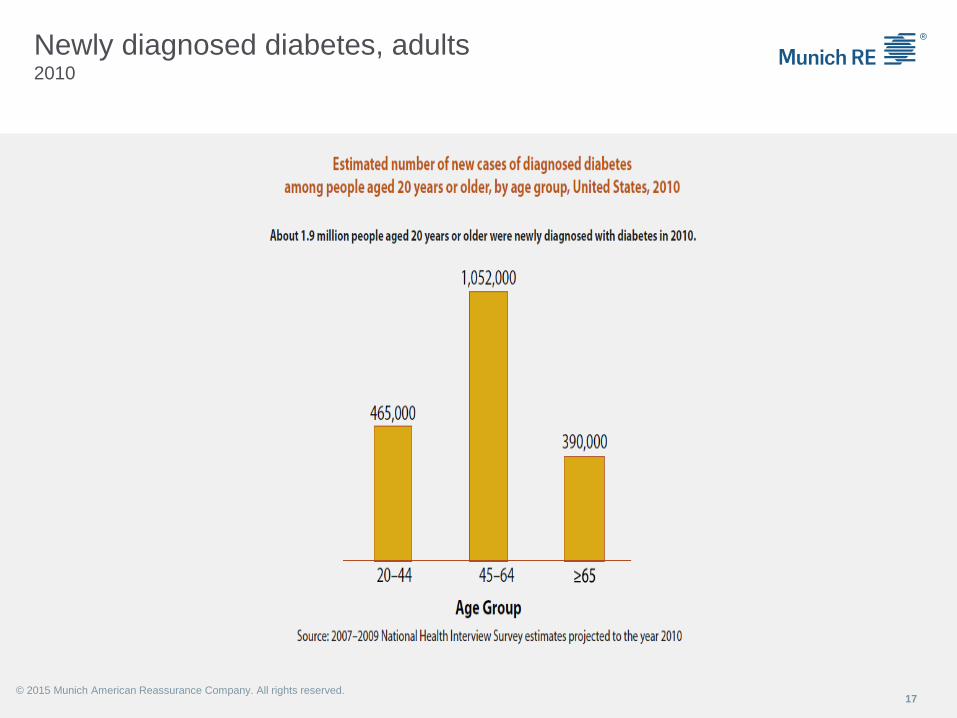

Newly diagnosed diabetes, adults2010

17© 2015 Munich American Reassurance Company. All rights reserved.

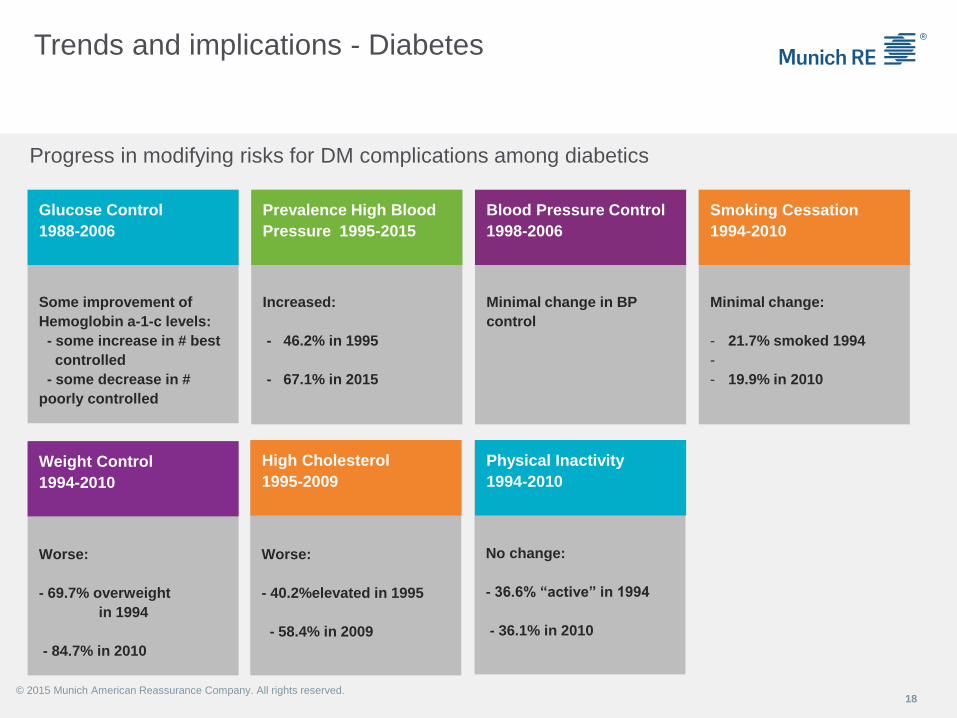

Trends and implications - Diabetes

18

No change:

- 36.6% “active” in 1994

- 36.1% in 2010

Worse:

- 40.2%elevated in 1995

- 58.4% in 2009

Worse:

- 69.7% overweight

in 1994

- 84.7% in 2010

Some improvement of

Hemoglobin a-1-c levels:

- some increase in # best

controlled

- some decrease in #

poorly controlled

Minimal change in BP

control

Minimal change:

- 21.7% smoked 1994

-

- 19.9% in 2010

Increased:

- 46.2% in 1995

- 67.1% in 2015

Glucose Control

1988-2006

Prevalence High Blood

Pressure 1995-2015

Blood Pressure Control

1998-2006

Smoking Cessation

1994-2010

Weight Control

1994-2010

High Cholesterol

1995-2009

Physical Inactivity

1994-2010

Progress in modifying risks for DM complications among diabetics

© 2015 Munich American Reassurance Company. All rights reserved.

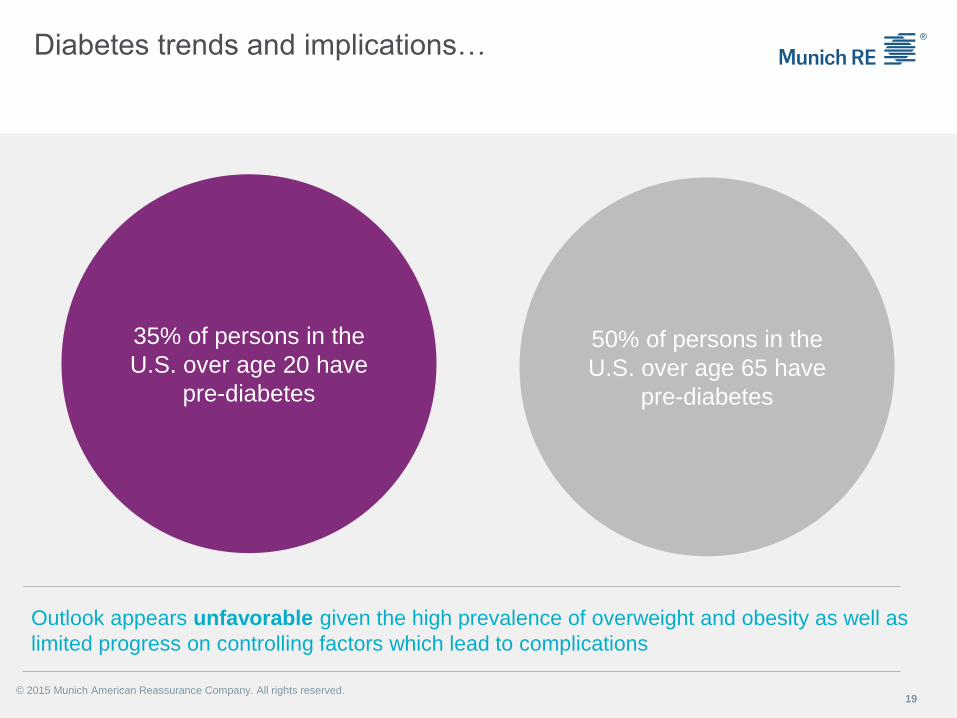

Diabetes trends and implications…

19

35% of persons in the

U.S. over age 20 have

pre-diabetes

50% of persons in the

U.S. over age 65 have

pre-diabetes

Outlook appears unfavorable given the high prevalence of overweight and obesity as well as

limited progress on controlling factors which lead to complications

© 2015 Munich American Reassurance Company. All rights reserved.

Breast Cancer

20

Most common cancer in women

▪ 207,000 women, 2000 men in 2010

▪ Second most common cause of cancer death in women (first among Hispanic)

Incidence trends, 2001-2010 – remained level

Mortality trends, 2001-2010 – decreased 1.5-2.0% per year

© 2015 Munich American Reassurance Company. All rights reserved.

▪ Earlier diagnosis

▪ Better treatment

Risk of breast cancer increases with age

21© 2015 Munich American Reassurance Company. All rights reserved.

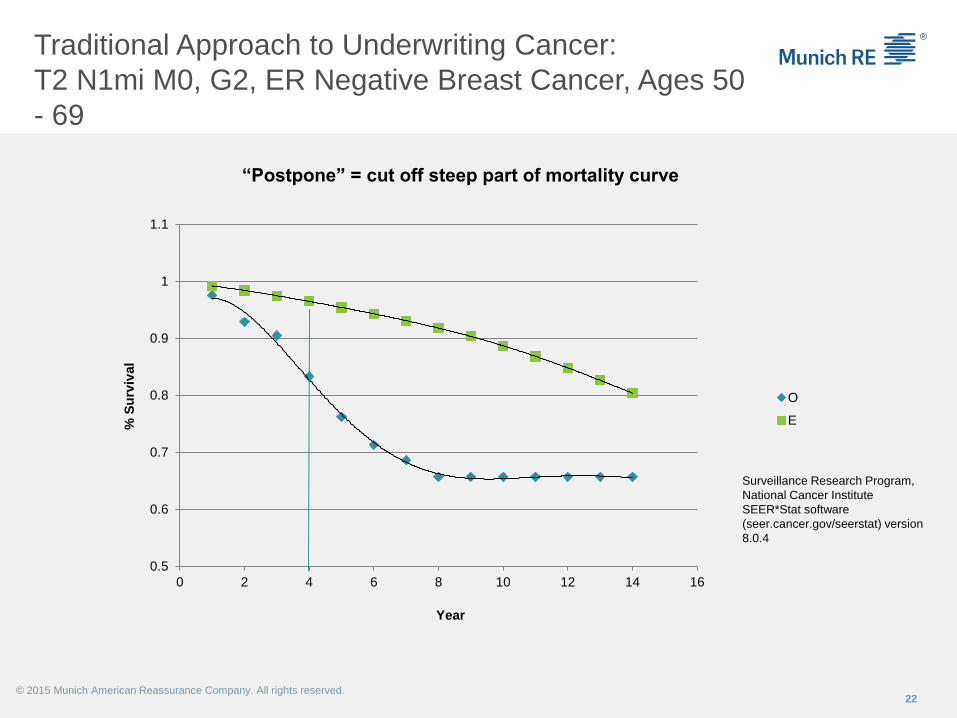

Traditional Approach to Underwriting Cancer:

T2 N1mi M0, G2, ER Negative Breast Cancer, Ages 50

- 69

22

Surveillance Research Program,

National Cancer Institute

SEER*Stat software

(seer.cancer.gov/seerstat) version

8.0.4

© 2015 Munich American Reassurance Company. All rights reserved.

0.5

0.6

0.7

0.8

0.9

1

1.1

0 2 4 6 8 10 12 14 16

% S

urv

ival

Year

“Postpone” = cut off steep part of mortality curve

O

E

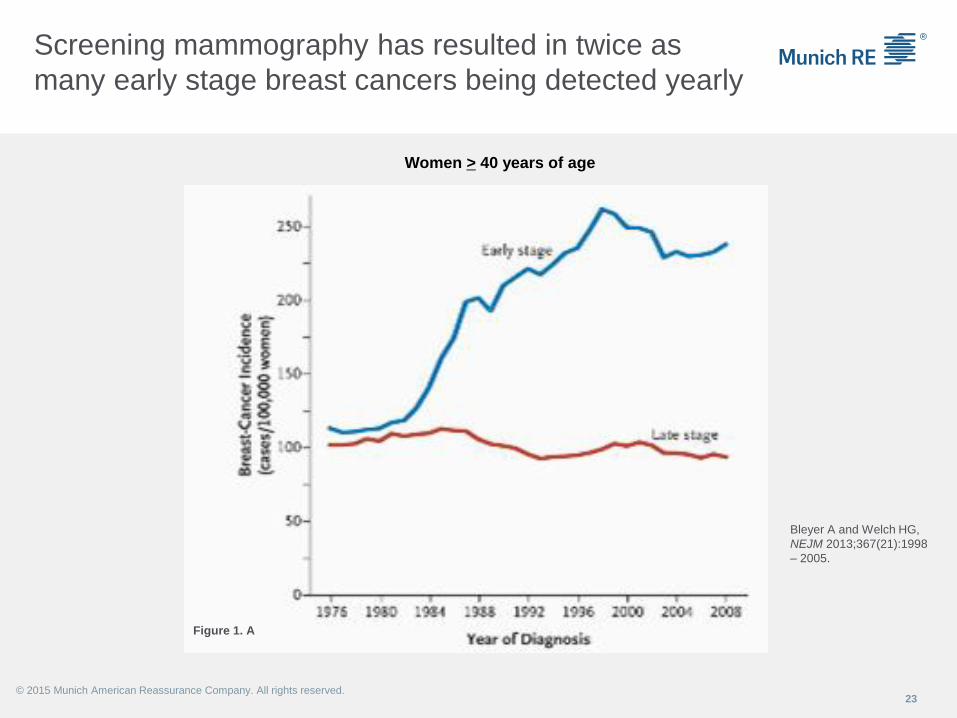

Screening mammography has resulted in twice as

many early stage breast cancers being detected yearly

23

Figure 1. A

Women > 40 years of age

Bleyer A and Welch HG,

NEJM 2013;367(21):1998

– 2005.

© 2015 Munich American Reassurance Company. All rights reserved.

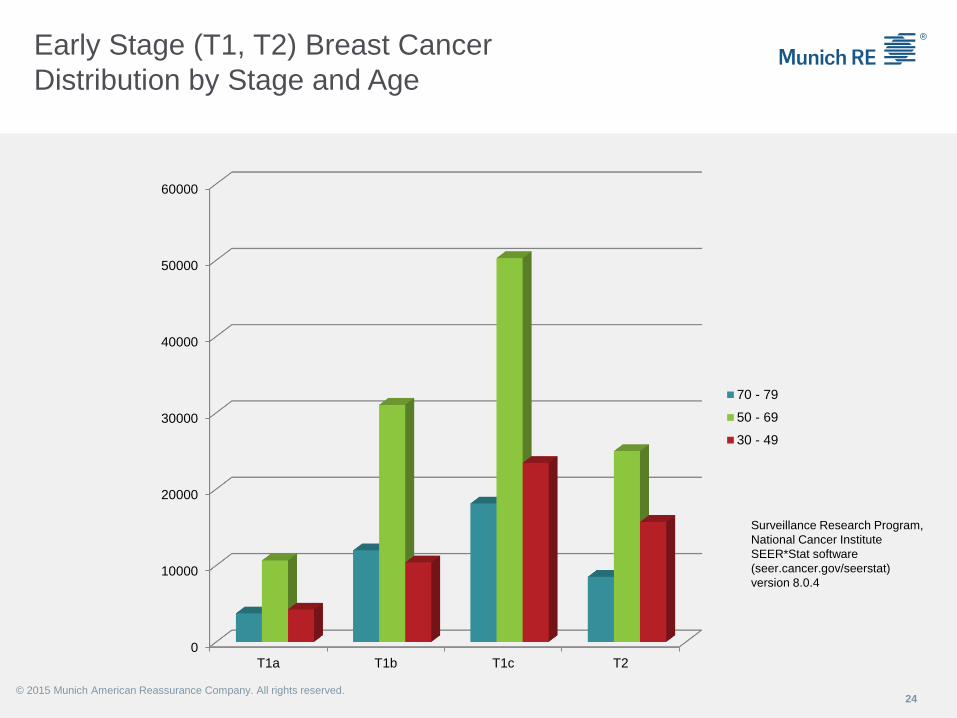

Early Stage (T1, T2) Breast Cancer

Distribution by Stage and Age

24

0

10000

20000

30000

40000

50000

60000

T1a T1b T1c T2

70 - 79

50 - 69

30 - 49

Surveillance Research Program,

National Cancer Institute

SEER*Stat software

(seer.cancer.gov/seerstat)

version 8.0.4

© 2015 Munich American Reassurance Company. All rights reserved.

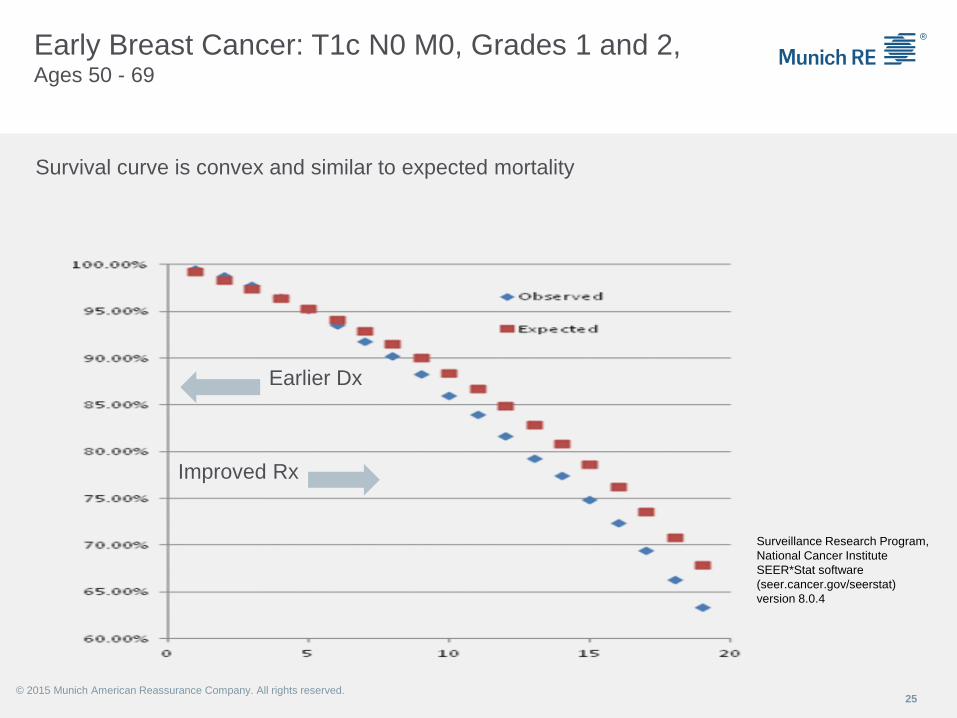

Early Breast Cancer: T1c N0 M0, Grades 1 and 2,Ages 50 - 69

25

Surveillance Research Program,

National Cancer Institute

SEER*Stat software

(seer.cancer.gov/seerstat)

version 8.0.4

Survival curve is convex and similar to expected mortality

Earlier Dx

Improved Rx

© 2015 Munich American Reassurance Company. All rights reserved.

Long-term adverse effects from therapy for early stage

breast cancer result in ongoing increased mortality risk

26

Radiation

▪ Increase incidence of coronary artery disease

▪ Myocardial damage from radiation

Chemotherapy

© 2015 Munich American Reassurance Company. All rights reserved.

▪ Increased incidence of hematologic malignancies

▪ Cardiomyopathy

Early Stage (T1 T2 N0 M0) Breast Cancer

27

Survival curves are convex

▪ Little advantage to postpone period

▪Debits better reflect the risk vs. temporary flat extra rating format

© 2015 Munich American Reassurance Company. All rights reserved.

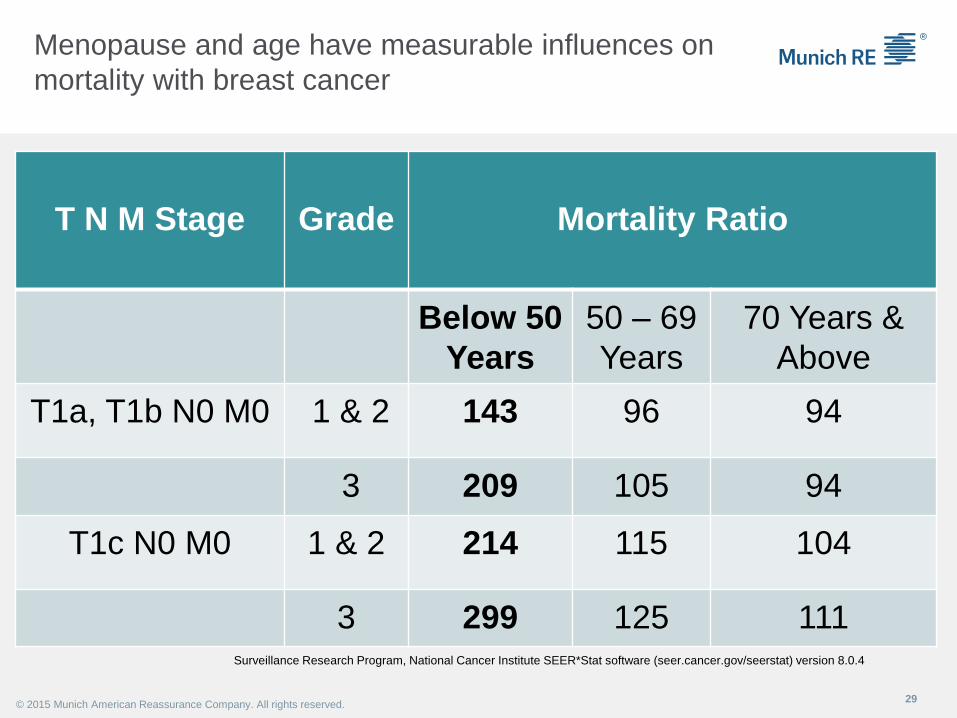

Menopause and Age alter mortality risk in early

stage breast cancer

Menopause and age have measurable influences on

mortality with breast cancer

29

T N M Stage Grade Mortality Ratio

Below 50

Years

50 – 69

Years

70 Years &

Above

T1a, T1b N0 M0 1 & 2 143 96 94

3 209 105 94

T1c N0 M0 1 & 2 214 115 104

3 299 125 111Surveillance Research Program, National Cancer Institute SEER*Stat software (seer.cancer.gov/seerstat) version 8.0.4

© 2015 Munich American Reassurance Company. All rights reserved.

And above age 70…

30

Early Stage breast cancer (T1 size) effectively treated with

lumpectomy and tamoxifen

More sensitive to effects of hormonal Rx in later years –

especially beyond 75 years

© 2015 Munich American Reassurance Company. All rights reserved.

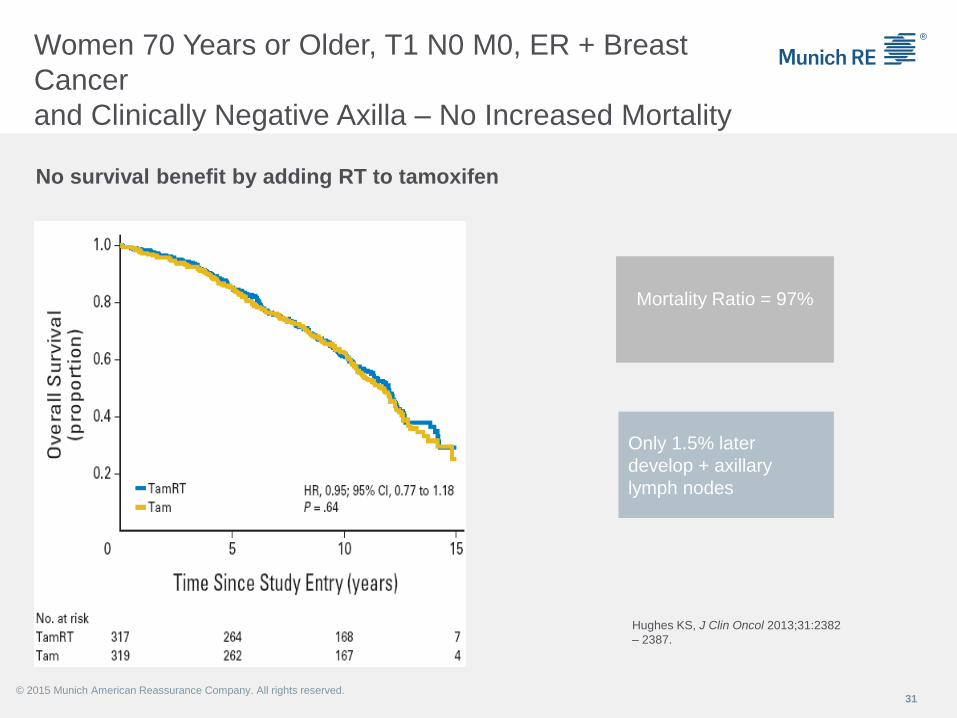

Women 70 Years or Older, T1 N0 M0, ER + Breast

Cancer

and Clinically Negative Axilla – No Increased Mortality

31

No survival benefit by adding RT to tamoxifen

Mortality Ratio = 97%

Only 1.5% later

develop + axillary

lymph nodes

© 2015 Munich American Reassurance Company. All rights reserved.

Hughes KS, J Clin Oncol 2013;31:2382

– 2387.

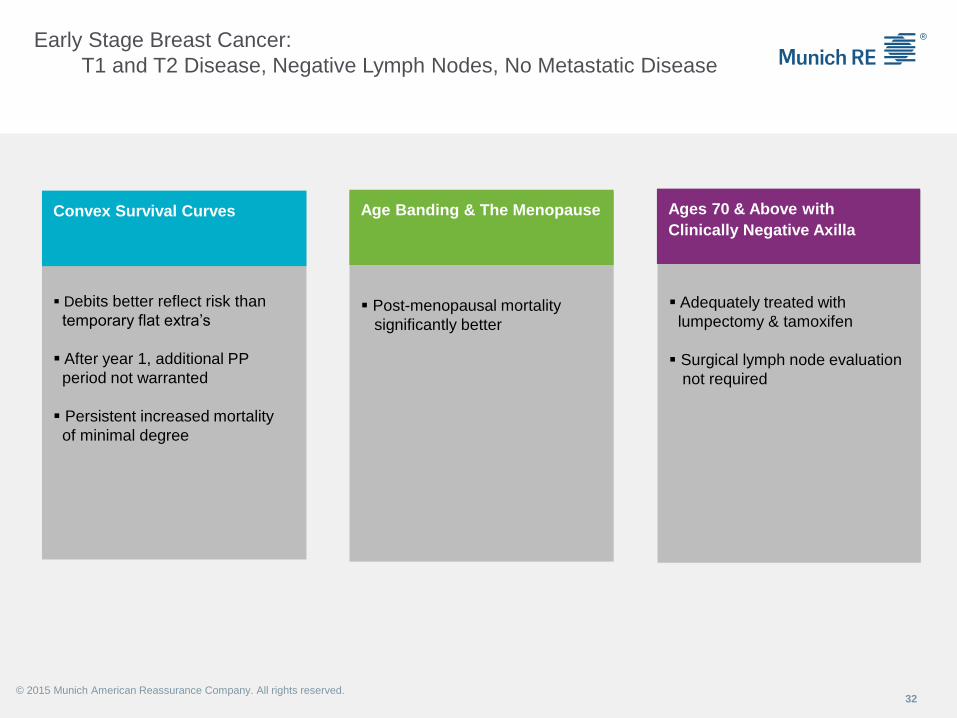

Early Stage Breast Cancer:

T1 and T2 Disease, Negative Lymph Nodes, No Metastatic Disease

32

▪ Debits better reflect risk than

temporary flat extra’s

▪ After year 1, additional PP

period not warranted

▪ Persistent increased mortality

of minimal degree

▪ Adequately treated with

lumpectomy & tamoxifen

▪ Surgical lymph node evaluation

not required

▪ Post-menopausal mortality

significantly better

Convex Survival Curves Age Banding & The Menopause Ages 70 & Above with

Clinically Negative Axilla

© 2015 Munich American Reassurance Company. All rights reserved.

Trends and implications – Breast Cancer

33

With aging population and better screening, incidence likely to rise

Outlook for early stage breast cancer has improved

Improved understanding of the most common breast cancer risks encountered:

▪ More limited PP period translates to earlier offers

▪ Small rating, no temporary extra premium charge

▪ Bottom line: More and more favorable offers than in past

For applicants with early stage breast cancer within 5 years of therapy

For the balance of the policy, more accurate pricing of the risk

© 2015 Munich American Reassurance Company. All rights reserved.

▪ Extra mortality for those entering insured pool after traditional PP period was often not

previously covered

Lung Cancer

34

More Americans die from lung cancer than any other cancer

▪ Diagnosed: 201,000 – M:F 107,000: 94,000 (2010)

▪ Deaths: 158,000 – M:F 88,000: 71,000 (2010)

Incidence trends 2001-2010

© 2015 Munich American Reassurance Company. All rights reserved.

▪ Decreased 2.3 – 2.7% per year in men

▪ Decreased 0.6 – 0.7% per year in women, stayed level in black women

Mortality trends 2001-2010

▪ Decreased 2.5 – 3.3% in men, biggest improvement among black men

▪ Decreased 0.9 – 1.0% in women

Trends and implications – Lung Cancer

35

Decrease incidence and mortality in men reflects smoking reduction over past 20-30 years in

men

Lack of improvement in women likely reflects both later adoption and discontinuance of

smoking among women

© 2015 Munich American Reassurance Company. All rights reserved.

Screening remains problematic and controversial – CXR vs. CT, etc

Therapies except for the earliest found lesions and one subgroup (NSCLC) remains less than

optimal

Key to future remains risk factor reduction

Colorectal Cancer

36

Third most common cancer in men and women

▪ Diagnosed: 132,000 – M:F 68,000: 64,000 (2010)

▪ Deaths: 52,000

Incidence trends 2001-2010

▪ Decreased 2.0 – 4.0% per year in men

▪ Decreased 2.0 – 3.3% per year in women

Mortality trends 2001-2010

▪ Decreased by 1.4 – 3.0% per year in men

▪ Decreased by 2.0 – 3.3% among women

Second leading cause of cancer death in cancers which affect both men and women

© 2015 Munich American Reassurance Company. All rights reserved.

Trends and implications: Colorectal Cancer

37

Education, screening and surveillance has had a favorable impact

▪ More earlier stage lesions at diagnosis

▪ Able to offer on best cases and do so earlier

Incidence increases with age thus incidence likely to increase

▪ Treatment for later stage disease remains sub-optimal

▪ Current ratings for these may be underpriced in the market

© 2015 Munich American Reassurance Company. All rights reserved.

Prostate Cancer

38

Most common cancer among men in U.S.

▪ Lifetime risk >16%

Second leading cause of cancer death in men

© 2015 Munich American Reassurance Company. All rights reserved.

▪ Diagnosed: 196,000 in 2010

▪ Deaths: 29,000

Incidence trends 2001-2010

▪ Decreased by 2.6 – 4.0% per year

Mortality trends

▪ Decreased by 3.0 – 3.8% per year (3.8% in black men!)

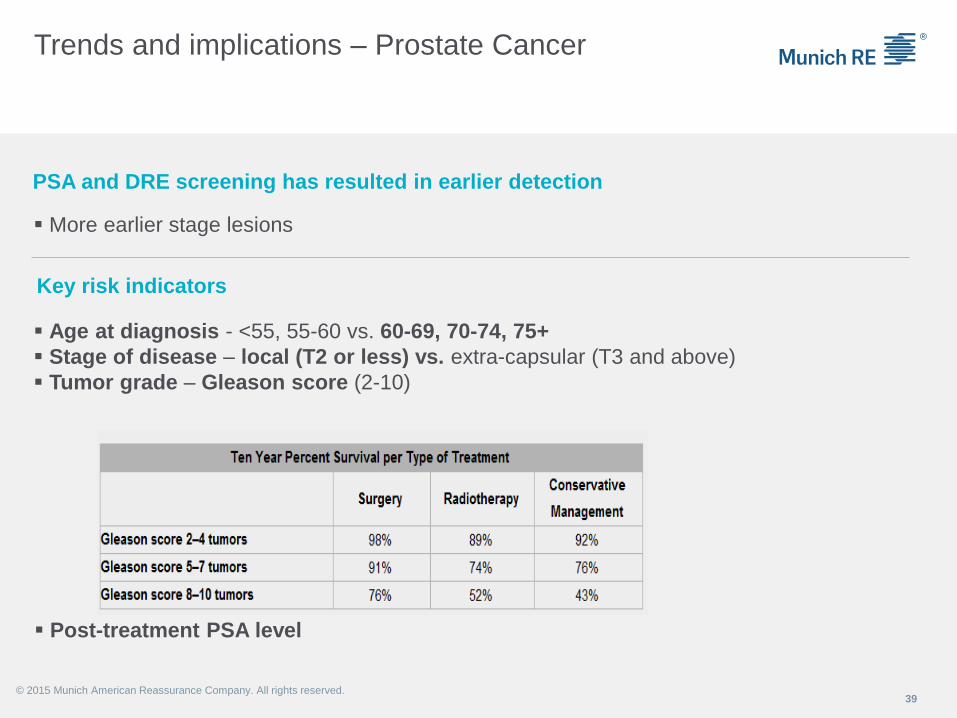

Trends and implications – Prostate Cancer

39

PSA and DRE screening has resulted in earlier detection

▪ More earlier stage lesions

Key risk indicators

© 2015 Munich American Reassurance Company. All rights reserved.

▪ Age at diagnosis - <55, 55-60 vs. 60-69, 70-74, 75+

▪ Stage of disease – local (T2 or less) vs. extra-capsular (T3 and above)

▪ Tumor grade – Gleason score (2-10)

▪ Post-treatment PSA level

Trends and implications – Prostate Cancer

(continued)

40

With latest SEER data, improved ability to quantify risk

▪ Earlier offers for better/best risks

▪ Better offers for many than before, especially at >60, >70

Second leading cause of cancer death in men

© 2015 Munich American Reassurance Company. All rights reserved.

▪ Controversy over screening/over-treatment may lower detection of early tumors

▪ More men may elect “watchful waiting”

▪ Focus on ED risk may likewise affect number of younger men opting for radiation

rather than surgery with less certain outlook for cure in some cases

Skin Cancer - Melanoma

41

Skin cancer is the commonest form of cancer in the U.S.

Most are basal cell or squamous cell cancers with minimal mortality impact

Melanoma is potentially a bad actor

▪ Diagnosed melanomas: 61,000 M:F 35,200:25,800 in 2010

▪ Deaths: 9,200 M:F 6,000:3,200

Incidence

© 2015 Munich American Reassurance Company. All rights reserved.

▪ Increased by 1.6% per year in white men, remained level in others

▪ Increased by 1.6% per year in white women, remained level in others

Mortality

▪ Increased by 1.0% per year in white men, remained level in others

Trends and implications: Melanoma

42

Education and screening has had an impact but this is likely being offset by

▪ Growth of aging population

▪ More outdoor activities

▪ Increasing residency in warmer climates

▪ Inadequate adherence to SPF protection measures

There is more data on mortality risk based on microscopic findings (stage, grade) at

diagnosis and other prognostic indicators

© 2015 Munich American Reassurance Company. All rights reserved.

▪ Improved offers for earlier stages with good prognosis markers

▪ Later stages remain problematic

▪ Newer therapies show promise

Challenges and Opportunities…

Heart Disease

Diabetes

Cancer: Breast , Lung, Colorectal, Prostate, Melanoma

Also on the disease trend horizon…

- HIV Disease – a treatable chronic disease?

- e Cigarettes – low or risk free?

- Gender identity – the Facebook response

- DTC Genetic testing – and consumer knowledge base

- Genetic Advances and Rare Diseases – potential social media impact

43© 2015 Munich American Reassurance Company. All rights reserved.

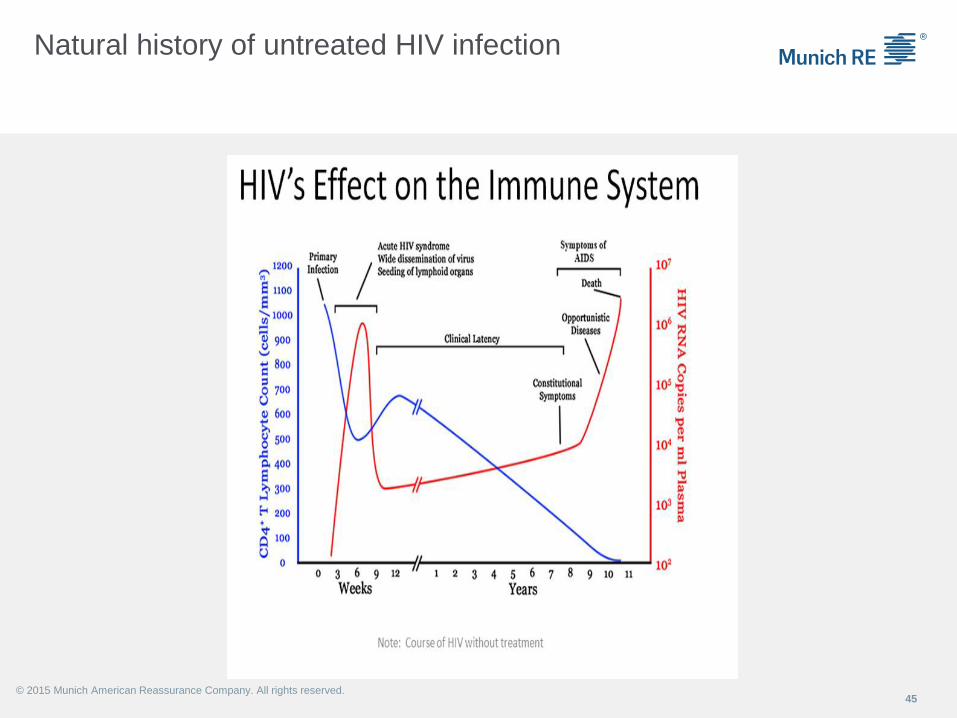

HIV Disease

44© 2015 Munich American Reassurance Company. All rights reserved.

Mortality trend for AIDS (Stage 3 HIV disease)

HIV infection incidence trend

▪ Remains level – 50,000 new infections per year M:F 39,000:11,000

▪ Most new infections ages 20-50

▪ Highest risk groups unchanged

▪ A leading cause of death ages 15-64

▪ 1.2 million AIDS cases to date, cumulative deaths 636,000

▪ Declining – 15,000 deaths in 2010

Prevalence of HIV infection in U.S.: 1,100,000 (180,000 or 16% unaware)

Recent advances in therapy (ART) appears to have changed the course for HIV disease

Natural history of untreated HIV infection

45© 2015 Munich American Reassurance Company. All rights reserved.

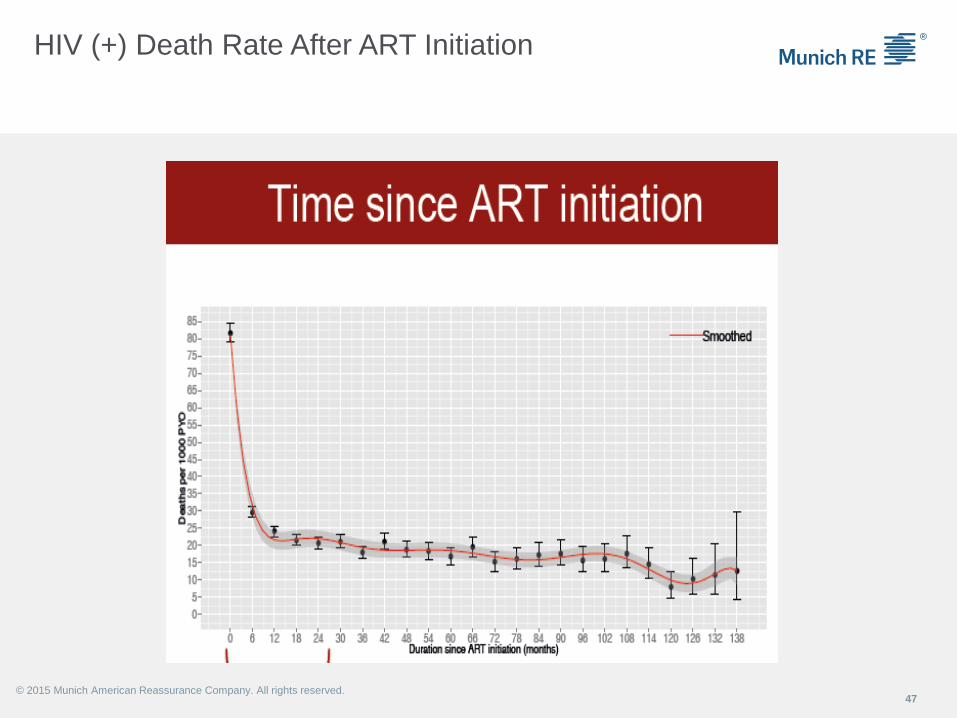

Trends and implications: HIV Disease

46© 2015 Munich American Reassurance Company. All rights reserved.

▪ Remarkable progress has been made in therapies since 1995

▪ The latest drug combo’s appear to be effective over the long term (so far) with

much more limited side effects than their predecessors

▪ There are reliable prognostic markers (CD4 count, HIV viral load, etc)

▪ Insurance (including whole life) is being offered in the US and abroad

▪ Just another chronic disease? Challenges include

▪ niche market

▪ the newer drug regimens are relatively novel (?2006)

▪ even if HIV is successfully suppressed, there appears to be some increased

risk for non-HIV related death (CAD, etc), i.e., premature aging

▪ A vaccine to prevent HIV infection seems a long way off.

▪ PreP for those at risk is here but not a panacea

▪A long-acting pre-exposure prophylactic medication may be available near term

HIV (+) Death Rate After ART Initiation

47© 2015 Munich American Reassurance Company. All rights reserved.

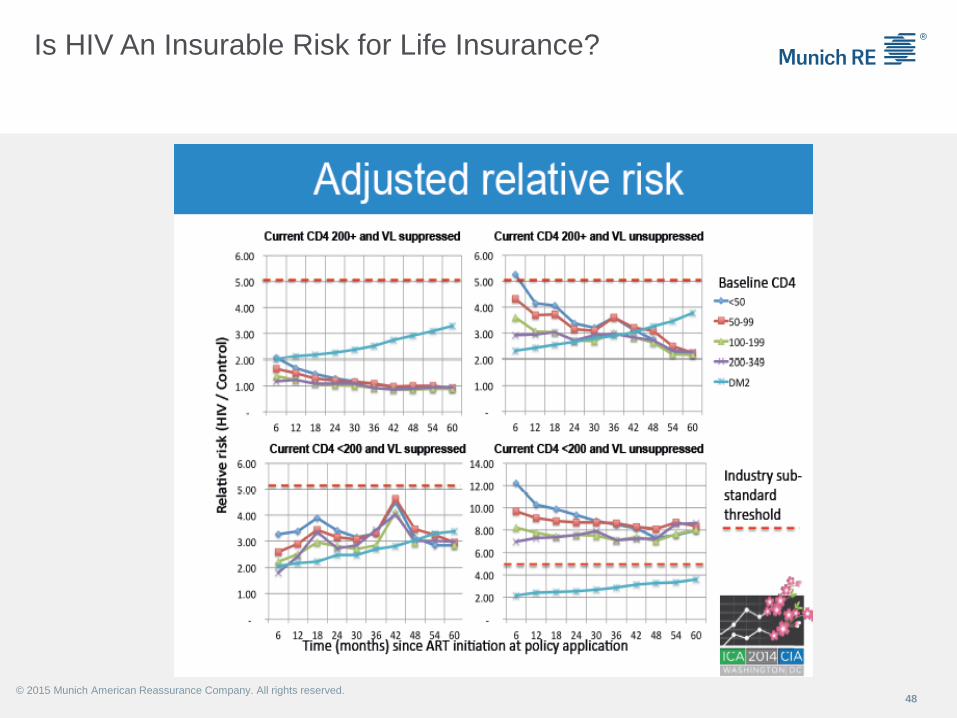

Is HIV An Insurable Risk for Life Insurance?

48© 2015 Munich American Reassurance Company. All rights reserved.

e-Cigarettes: ToB or not ToB

49© 2015 Munich American Reassurance Company. All rights reserved.

Cigs Appeal

50© 2015 Munich American Reassurance Company. All rights reserved.

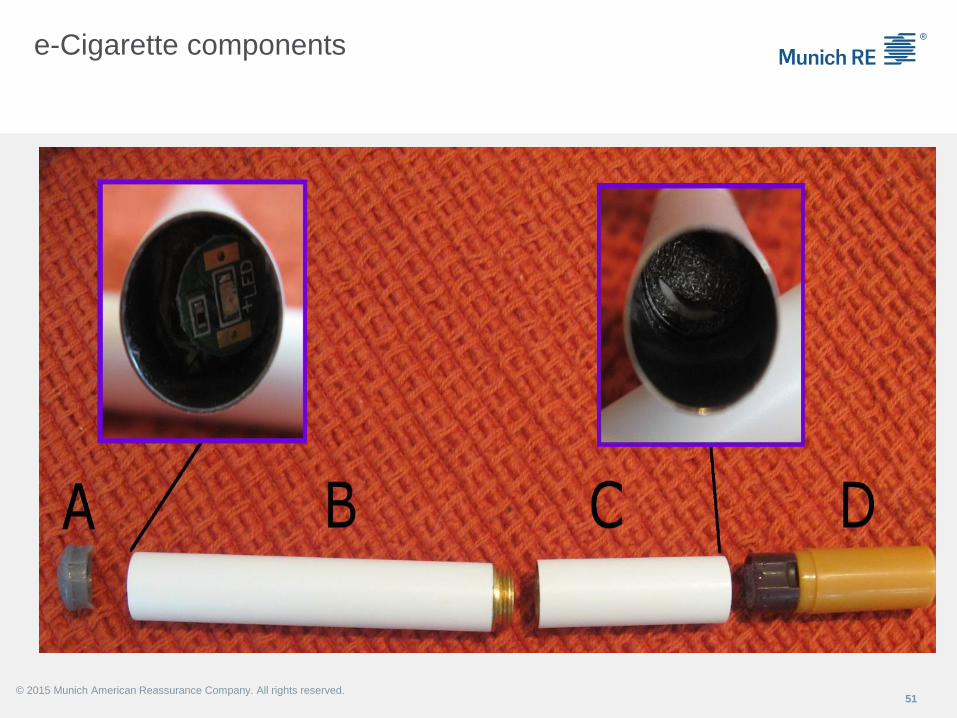

e-Cigarette components

51© 2015 Munich American Reassurance Company. All rights reserved.

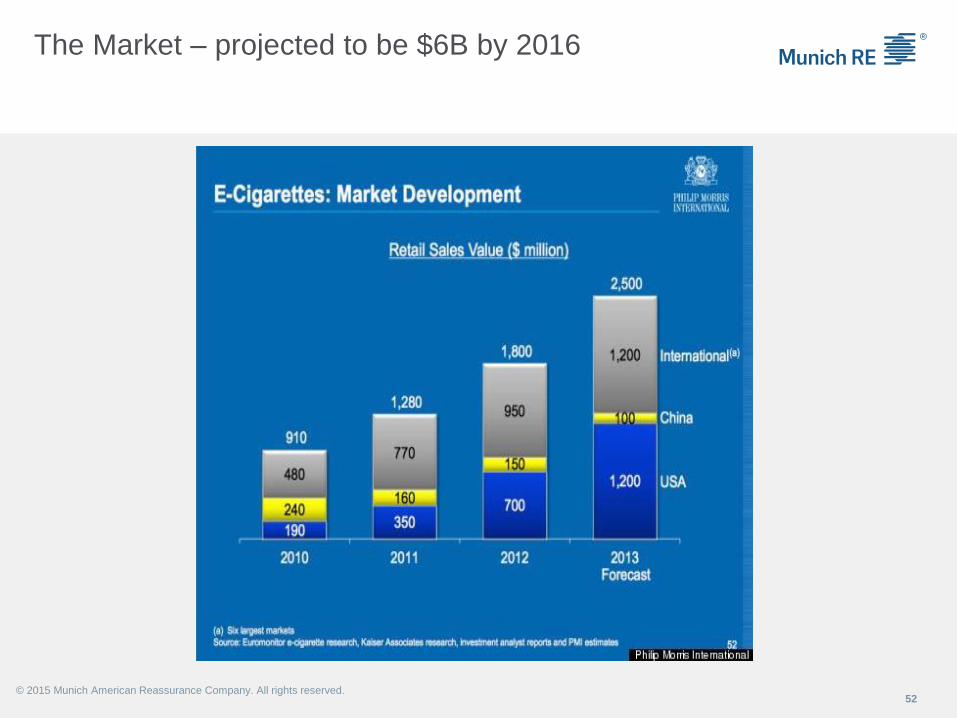

The Market – projected to be $6B by 2016

52© 2015 Munich American Reassurance Company. All rights reserved.

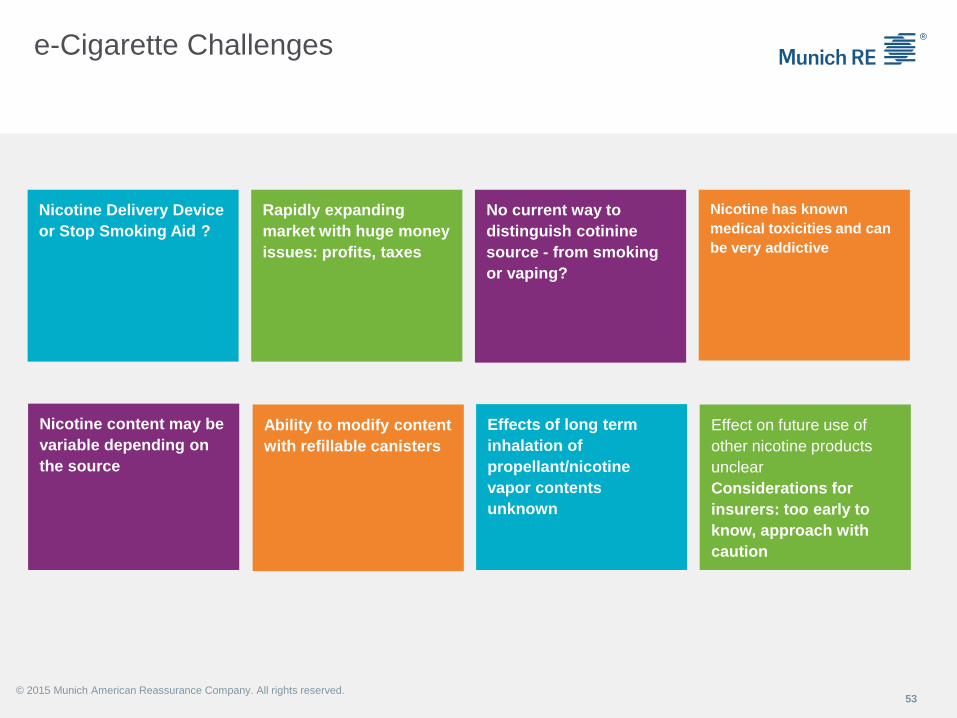

e-Cigarette Challenges

53

Nicotine Delivery Device

or Stop Smoking Aid ?

Rapidly expanding

market with huge money

issues: profits, taxes

No current way to

distinguish cotinine

source - from smoking

or vaping?

Nicotine has known

medical toxicities and can

be very addictive

Nicotine content may be

variable depending on

the source

Ability to modify content

with refillable canisters

Effects of long term

inhalation of

propellant/nicotine

vapor contents

unknown

Effect on future use of

other nicotine products

unclear

Considerations for

insurers: too early to

know, approach with

caution

© 2015 Munich American Reassurance Company. All rights reserved.

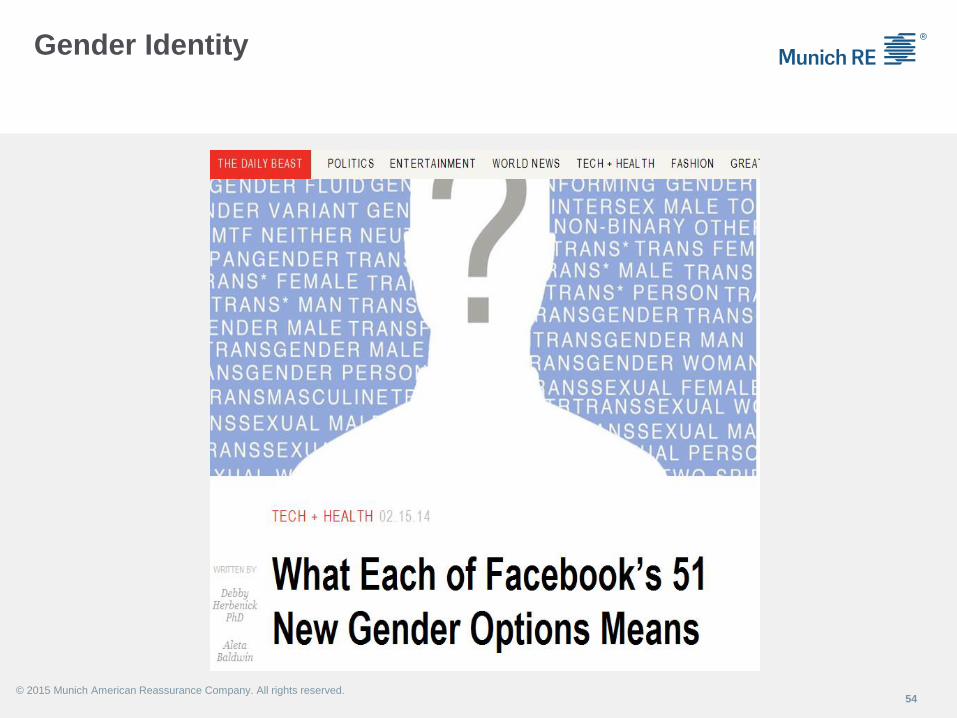

Gender Identity

54© 2015 Munich American Reassurance Company. All rights reserved.

Whose definition is it… anyway?

55

Gender identity vs. chromosomal make-up

▪ Which should prevail when applying for insurance?

▪ Activity in legislatures since 2013….

▪ Considerations for insurers –

▪ gender specific conditions remain, e.g., prostate cancer, ovarian cancer, breast

cancer

▪ supplemental hormone use side effects, tobacco, substance abuse

▪ co-morbid mental health issues may be part of the picture in some cases

▪ insurability may be more dependent on product line and co-morbidities

© 2015 Munich American Reassurance Company. All rights reserved.

Genetic testing

56

Genetic information

57

Medical, legal, social debates likely to re-surface

▪ Who can view a person’s genetic information?

▪ What constitutes genetic information?

Insurers consider genetic information part of routine medical information

Improving genetic tests (now at the research level) will highlight the issues

© 2015 Munich American Reassurance Company. All rights reserved.

▪ Become less costly to perform

▪ Direct to consumer testing (23 and me, etc) is far from perfect - now

▪ Genetic links to uncommon disorders are being uncovered

▪ Medical and actuarial data for uncommon disorders remain limited

Insurers will want to continue to “Do The Right Thing” but difficult challenges lie ahead

Rare Diseases: A Significant Underwriting Challenge

Ahead?

1. Rare disease defined

2. Challenge for insurance industry

3. Rare disease – patient perspective

4. Rare disease – medical perspective

5. Industry challenges ...and opportunities

© 2015 Munich American Reassurance Company. All rights reserved.

Exceptionally rare

▪ Rarest disease in the world

▪ One single diagnosed patient born in 1984

▪ No other patient since publication of the disease in 1999

Ribose-5-phosphate isomerase deficiency

© 2015 Munich American Reassurance Company. All rights reserved.

Rare ….but well known

▪ Cystic Fibrosis

▪ ALS (Steven Hawking)

▪ Sjögren Syndrome (Venus Williams)

▪ Parkinson‘s Disease (Michael J. Fox)

▪ Churg-Strauss-Syndrome (Taku Takeuchi)

60© 2015 Munich American Reassurance Company. All rights reserved.

Characteristics of rare diseases

▪ 80% genetic, hence generally chronic by nature

▪ May become apparent (symptomatic) at different ages, at birth or later

▪ 20% infectious or not genetic, may be transient

© 2015 Munich American Reassurance Company. All rights reserved.

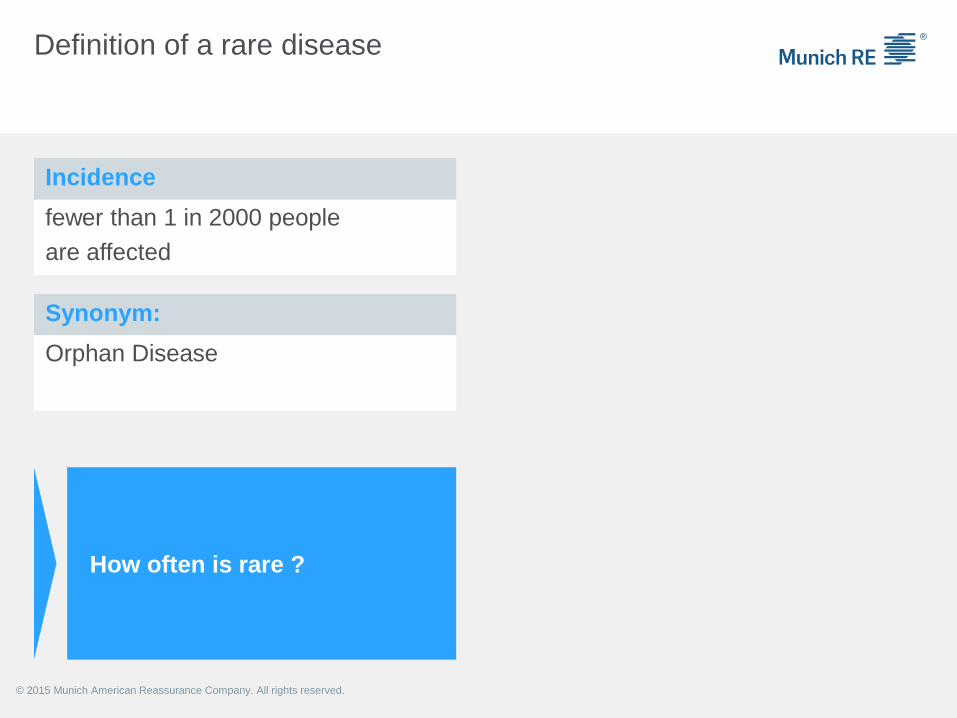

Definition of a rare disease

fewer than 1 in 2000 people

are affected

How often is rare ?

Incidence

Synonym:

Orphan Disease

© 2015 Munich American Reassurance Company. All rights reserved.

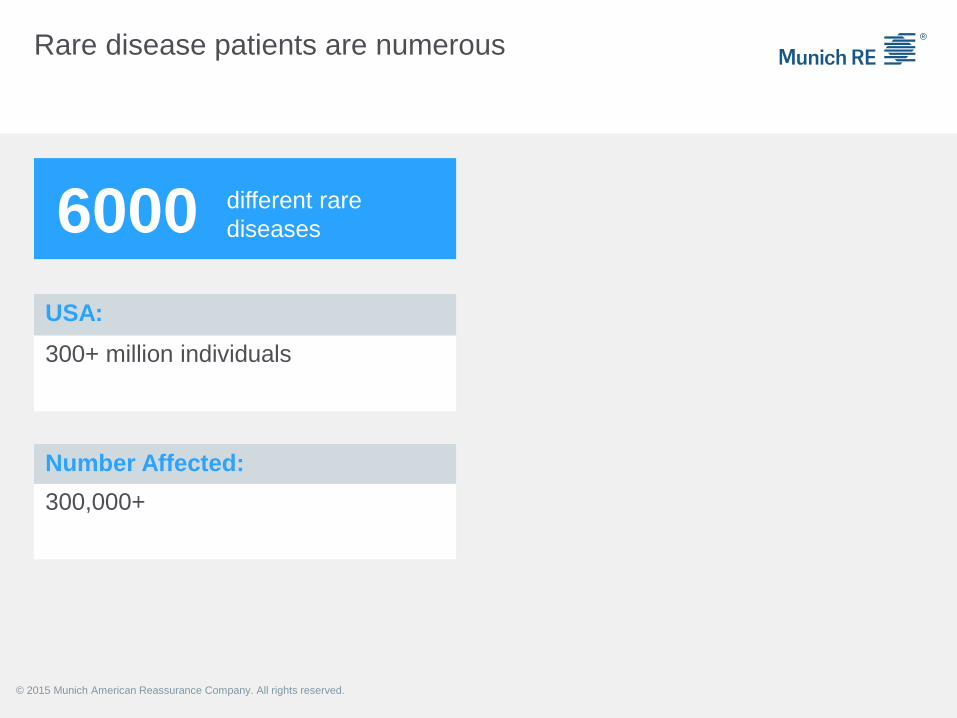

Rare disease patients are numerous

300+ million individuals

6000 different rare

diseases

USA:

Number Affected:

300,000+

© 2015 Munich American Reassurance Company. All rights reserved.

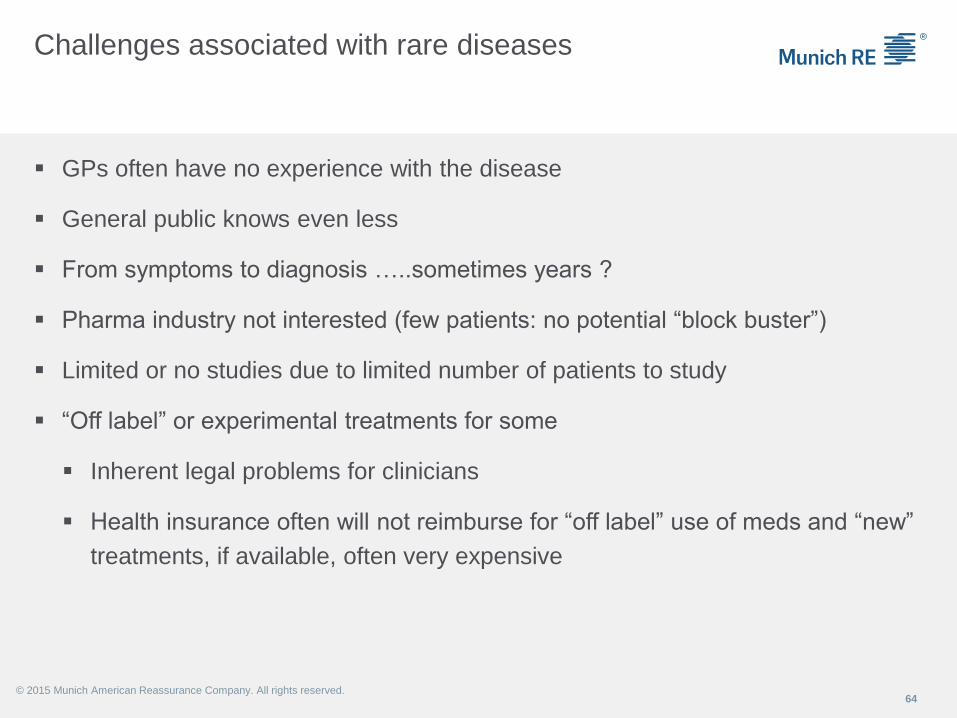

Challenges associated with rare diseases

▪ GPs often have no experience with the disease

▪ General public knows even less

▪ From symptoms to diagnosis …..sometimes years ?

▪ Pharma industry not interested (few patients: no potential “block buster”)

▪ Limited or no studies due to limited number of patients to study

▪ “Off label” or experimental treatments for some

▪ Inherent legal problems for clinicians

▪ Health insurance often will not reimburse for “off label” use of meds and “new”

treatments, if available, often very expensive

64© 2015 Munich American Reassurance Company. All rights reserved.

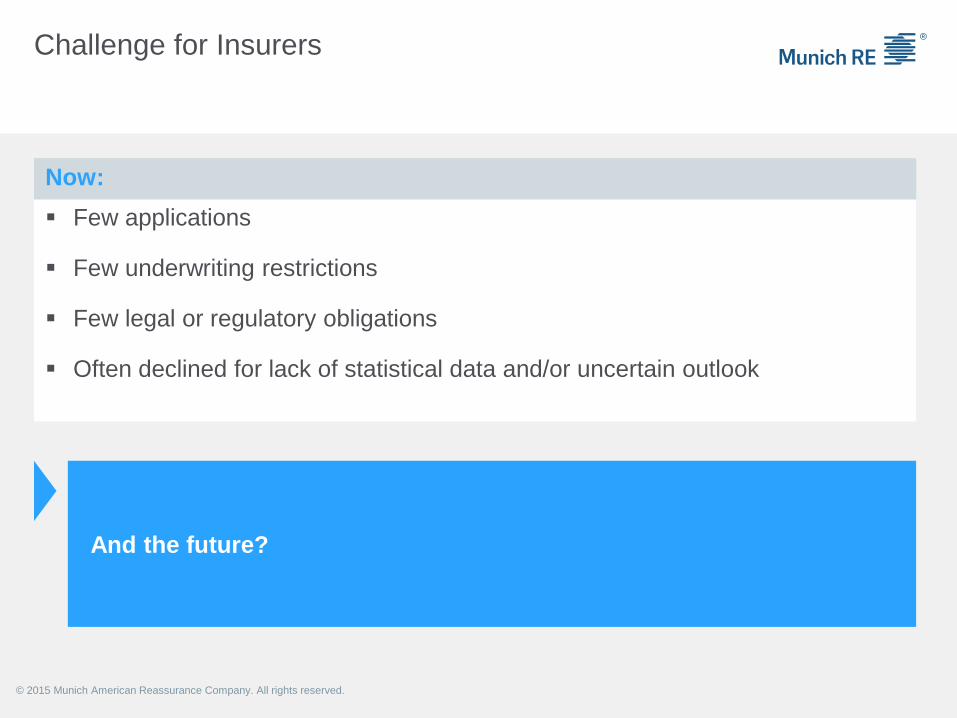

Now:

Challenge for Insurers

▪ Few applications

▪ Few underwriting restrictions

▪ Few legal or regulatory obligations

▪ Often declined for lack of statistical data and/or uncertain outlook

And the future?

© 2015 Munich American Reassurance Company. All rights reserved.

Challenge for Insurers

Challenge for insurance industry

Whole genome sequencing

Year 2020: most “idiopathic diseases”

will be classified as “genetic diseases”

Expected: up to 10% of the population

may be diagnosed with rare disease

Good news: New treatment options, better

prognosis, more will become insurable

More and more rare diseases are being discovered

© 2015 Munich American Reassurance Company. All rights reserved.

Challenge for Insurers

Challenge for insurance industry

High organizational level with

global networks via social media

Increased expectation for

justification of underwriting

decisions

Reputational risk for insurers and

reinsurers if an applicant with

a rare disease is considered unfairly

treated

Increasingly Linked Interest groups and regulators

© 2015 Munich American Reassurance Company. All rights reserved.

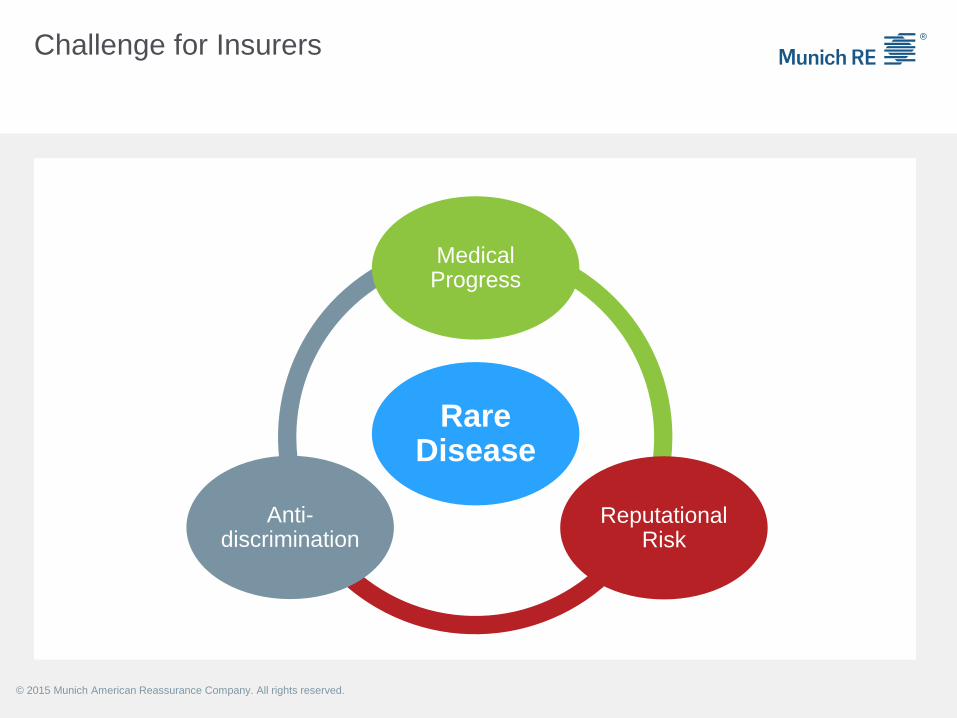

Challenge for Insurers

Rare Disease

Medical Progress

Reputational Risk

Anti-discrimination

© 2015 Munich American Reassurance Company. All rights reserved.

Challenge for Insurers

▪ The ideal: underwriting decisions should be individualized, consistent and –

as much as possible – based on medical evidence

▪ Decline based on lack of statistical data may no longer go unchallenged

Going forward:

© 2015 Munich American Reassurance Company. All rights reserved.

Challenge for Insurers

Challenge for insurance industry Evidence-Based Risk Assessment Today

Limited or no manual guidance for

rare diseases

Limited long-term clinical studies

Limited experiential data

Added medical expertise will be

essential

© 2015 Munich American Reassurance Company. All rights reserved.

Opportunity for Insurers

Doctors’ approachAnticipate the challenges coming

Facilitate research

Develop standards and

share morbidity and mortality findings

with the underwriting community and

clinicians as well

© 2015 Munich American Reassurance Company. All rights reserved.

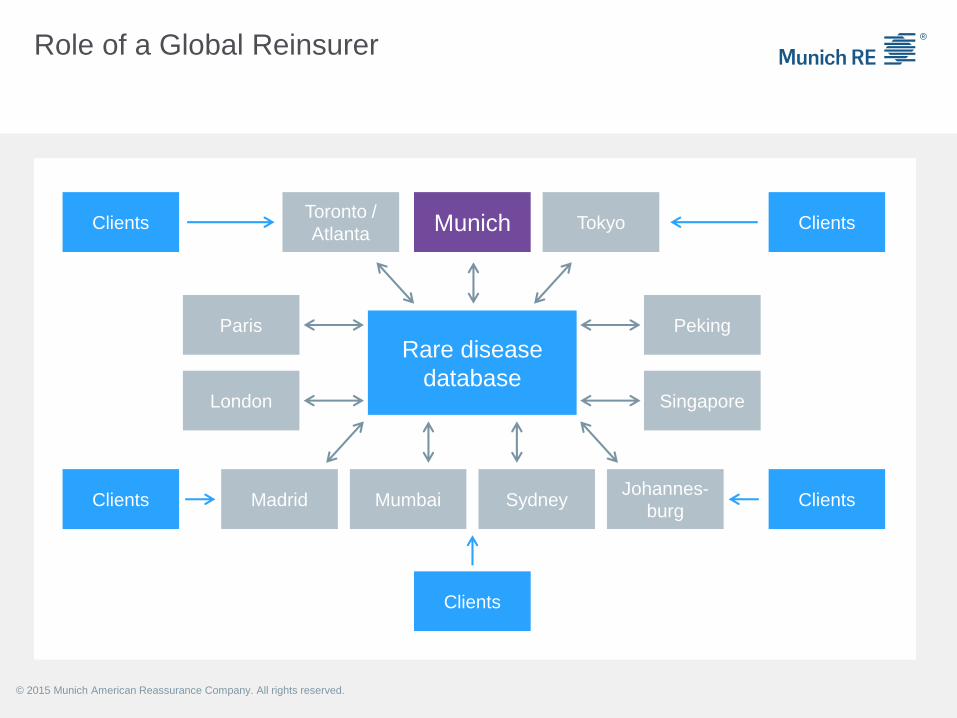

Role of a Global Reinsurer

Rare disease

database

MunichToronto /

AtlantaClients Tokyo Clients

ClientsClients

Clients

Paris

London

Peking

Singapore

Madrid Mumbai SydneyJohannes-

burg

© 2015 Munich American Reassurance Company. All rights reserved.

Global Approach

Better understand risks associated with rare or uncommon diseases

▪ Provide a globally consistent approach

▪ Provide actuarial or at least the best of known experience-based medical

opinions for underwriting of rare risks

▪ Advance the Industry

Munich Re Rare Disease Database

© 2015 Munich American Reassurance Company. All rights reserved.

Opportunity for Insurers – Rare Diseases

Be prepared to respond to an evolving market

• Determine insurability on evidence available

•Where feasible, offer a product that both meets an applicant’s needs and provides

an acceptable return

• Add to the Industry (and clinical) knowledge base

© 2015 Munich American Reassurance Company. All rights reserved.

Thank you

Mark Skillan, M.D.

© 2

012 M

ünchener

Rückvers

icheru

ngs-G

esellschaft ©

2012 M

unic

h R

ein

sura

nce C

om

pany