Country Risk AnalysisCountry Risk Analysis

2020 Lecture Lecture

16 - 2

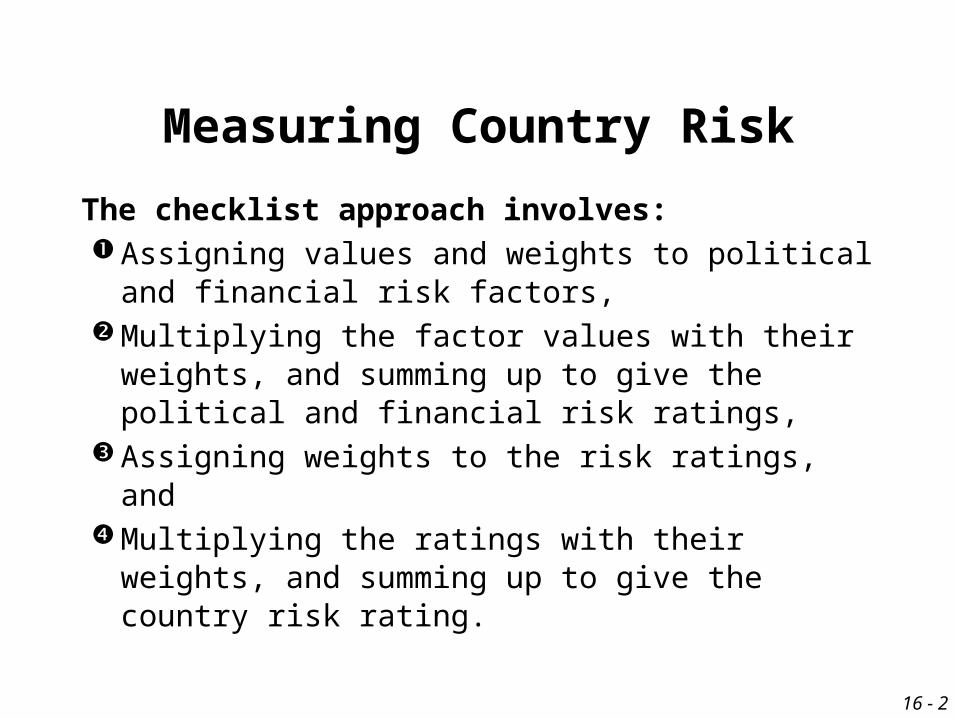

Measuring Country Risk

The checklist approach involves:Assigning values and weights to political and

financial risk factors, Multiplying the factor values with their

weights, and summing up to give the political and financial risk ratings,

Assigning weights to the risk ratings, and Multiplying the ratings with their weights, and

summing up to give the country risk rating.

16 - 3

Cougar Co.:Determining the Overall Country Risk Rating

16 - 4

Cougar Co.:Derivation of the Overall Country Risk Rating

16 - 5

• The procedures for quantifying country risk will vary with the assessor, the country being assessed, as well as the type of operations being planned.

• Firms use country risk ratings when screening potential projects, and when monitoring existing projects.

Measuring Country Risk

16 - 6

Comparing Risk RatingsAmong Countries

• One approach to comparing political and financial ratings among countries is the foreign investment risk matrix (FIRM ).

• The matrix displays financial (or economic) and political risk by intervals ranging from “poor” to “good.”

• Each country can be positioned on the matrix based on its political and financial ratings.

16 - 7

Actual Country Risk Ratings Across Countries

16 - 8

Incorporating Country Risk in Capital Budgeting

• If the risk rating of a country is acceptable, the projects related to that country deserve further consideration.

• Country risk can be incorporated into the capital budgeting analysis of a proposed project either by adjusting the discount rate or by adjusting the estimated cash flows.

16 - 9

• Adjustment of the discount rate¤ The higher the perceived risk, the higher

the discount rate that should be applied to the project’s cash flows.

• Adjustment of the estimated cash flows¤ By estimating how the cash flows could be

affected by each form of risk, the MNC can determine the probability distribution of the net present value of the project.

Incorporating Country Risk in Capital Budgeting

16 - 10

Spartan, Inc.: Summary of Estimated NPVs Across Possible Scenarios

16 - 11

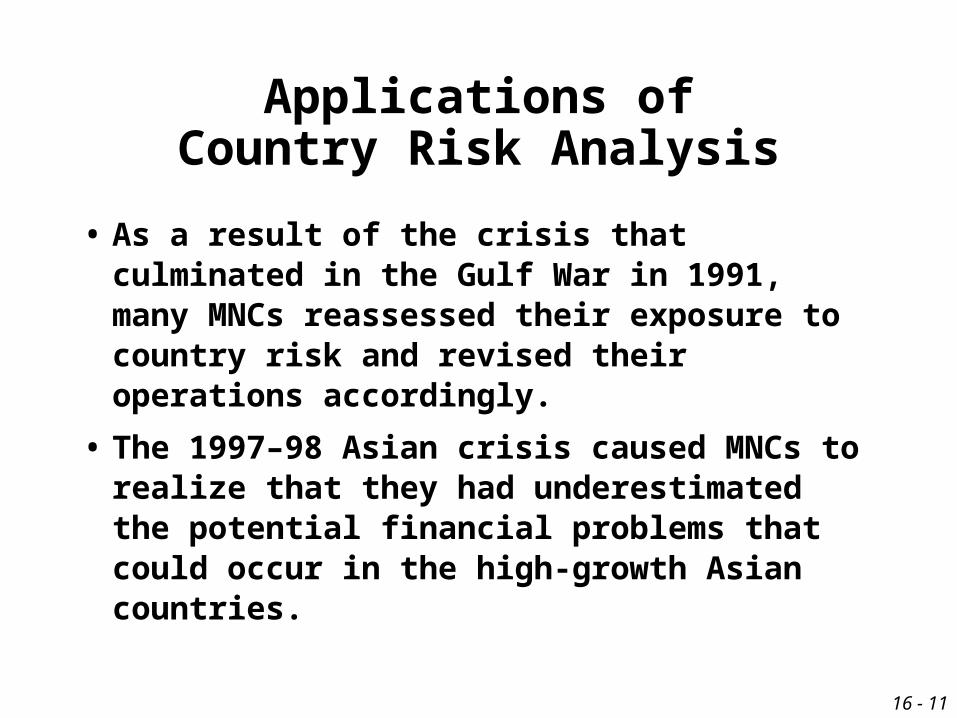

Applications ofCountry Risk Analysis

• As a result of the crisis that culminated in the Gulf War in 1991, many MNCs reassessed their exposure to country risk and revised their operations accordingly.

• The 1997–98 Asian crisis caused MNCs to realize that they had underestimated the potential financial problems that could occur in the high-growth Asian countries.

16 - 12

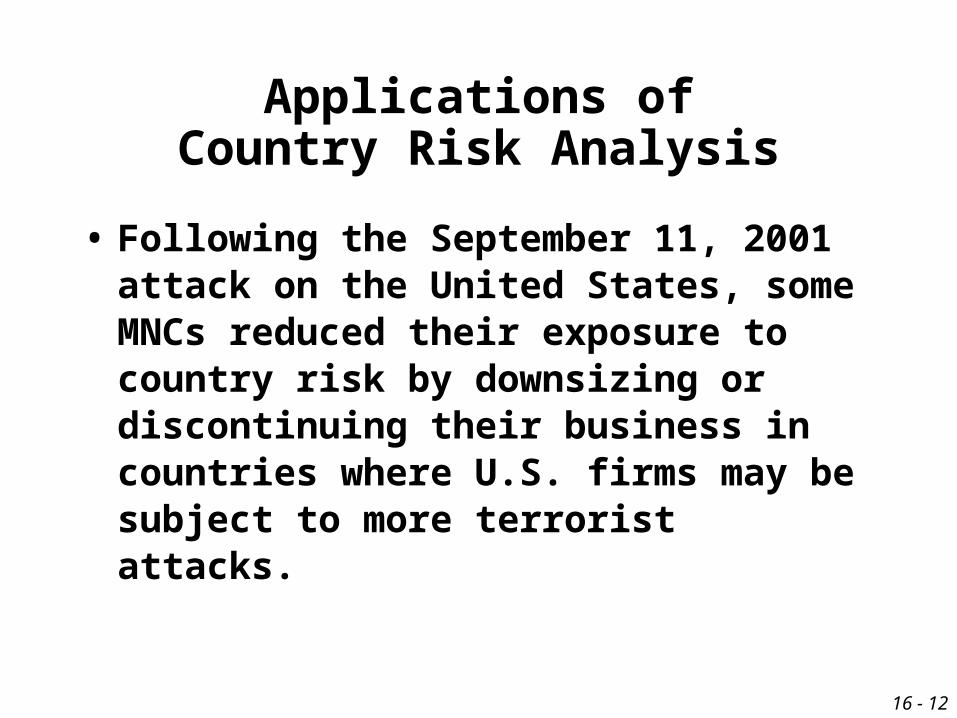

• Following the September 11, 2001 attack on the United States, some MNCs reduced their exposure to country risk by downsizing or discontinuing their business in countries where U.S. firms may be subject to more terrorist attacks.

Applications ofCountry Risk Analysis

16 - 13

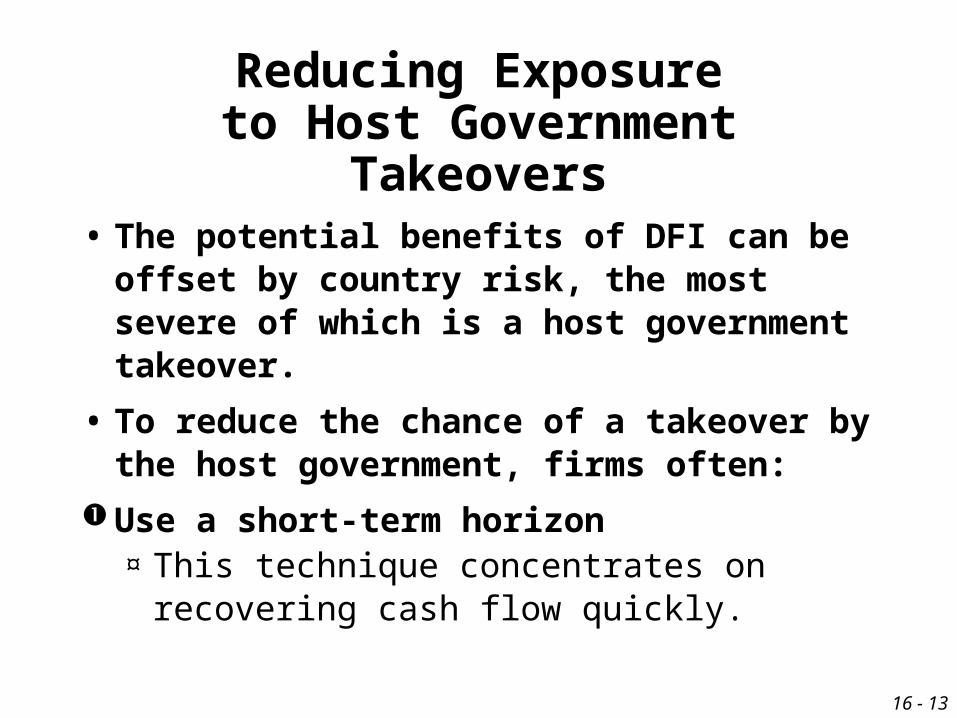

Reducing Exposureto Host Government Takeovers

• The potential benefits of DFI can be offset by country risk, the most severe of which is a host government takeover.

• To reduce the chance of a takeover by the host government, firms often:

Use a short-term horizon¤ This technique concentrates on recovering

cash flow quickly.

16 - 14

Reducing Exposureto Host Government Takeovers

Rely on unique supplies or technology¤ In this way, the host government will not be

able to take over and operate the subsidiary successfully.

Hire local labor¤ The local employees can apply pressure

on their government if they are affected by the takeover.

16 - 15

Borrow local funds¤ The local banks can apply pressure on their

government if they are affected by the takeover.

Purchase insurance¤ Investment guarantee programs offered by

the home country, host country, or an international agency insure to some extent various forms of country risk.

Reducing Exposureto Host Government Takeovers

16 - 16

Use project finance¤ Project finance deals are heavily financed

with credit, thus limiting the MNC’s exposure. The loans are secured by the project’s future revenues and are “nonrecourse.” A bank may guarantee the payments to the MNC.

Reducing Exposureto Host Government Takeovers

16 - 17

• Source: Adopted from South-Western/Thomson Learning © 2006