Costs of financial distress

Costs of leverage

• We have seen that leverage creates value – So why do firms have any equity at all? – Why do some firms have small vs big leverage?

Industry Debt Ratio (%) Electric and Gas 43.2 Food Production 22.9 Paper and Plastic 30.4 Equipment 19.1 Retailers 21.7 Chemicals 17.3 Computer Software 3.5

è because debt has a cost

outline

• Defini=on & clarifica=ons • The debtholder – shareholder conflict • Avoiding conflicts • costs of financial distress & valua=on

Defini=ons & clarifica=ons

• Financial vs economic distress

• Debt restructuring

• Costs of financial distress

2006 balance sheet (in m€)

Assets Liabilities Current = 0.4 ST debt = 9.7 Fixed = 7.1 LT debt = 0.1

Equity = -2.2

Yet, operating profits > 0 à abandonning the tunnel is not a good idea !

example: eurotunnel • a highly levered firm

– Construc=on cost = 13bn€, debt = 9.8bn€ – debt = 24 x EBITDA – never made a (net-‐of-‐interest) profit

• may 2007: debt restructuring – senior debtholders repaid in full, they walk away – junior debt à 210m€ in cash, 1.4bn€ in conv. bonds – subordinated debt à 130m€ cash + 320m€ of CB – equity issue = 240m€

• old shareholders à 13% of new firm – new CB issue: 1.9bn€

2007 balance sheet (in m€)

Assets Liabilities Current = 0.3 ST debt = 0.3 Fixed = 7.0 LT debt = 4.2

Equity =2.8

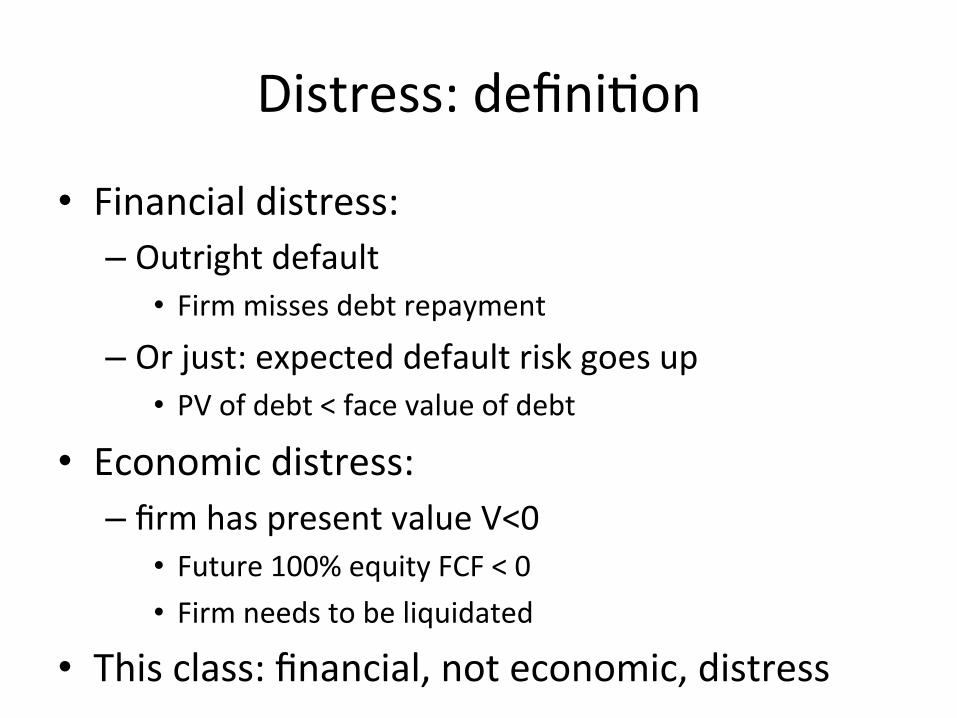

Distress: defini=on

• Financial distress: – Outright default

• Firm misses debt repayment

– Or just: expected default risk goes up • PV of debt < face value of debt

• Economic distress: – firm has present value V<0

• Future 100% equity FCF < 0 • Firm needs to be liquidated

• This class: financial, not economic, distress

defini=on

• This class: Financial distress leads to value destruc0on – In distress, present value V à V-‐F

è Cost of financial distress=p(distress)xF

• « Trade off theory »: Having more debt – Increases tax shield (good) – Increases costs of financial distress (bad)

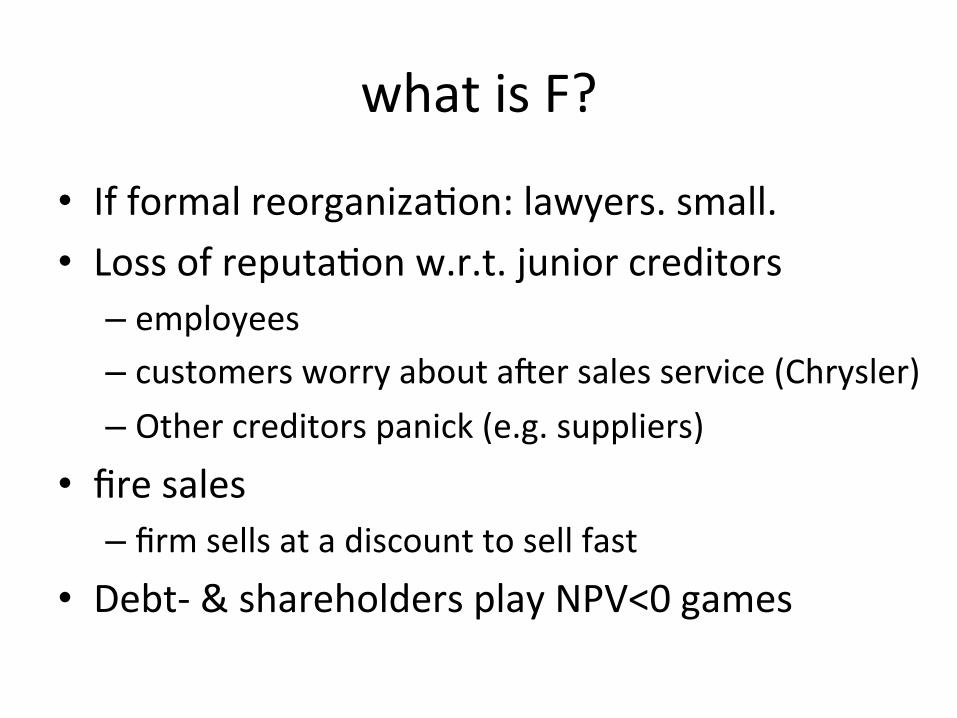

what is F?

• If formal reorganiza=on: lawyers. small. • Loss of reputa=on w.r.t. junior creditors

– employees – customers worry about aher sales service (Chrysler) – Other creditors panick (e.g. suppliers)

• fire sales – firm sells at a discount to sell fast

• Debt-‐ & shareholders play NPV<0 games

Jan

Apr

Jul

Oct

Jan

Apr

Jul

Oct

Jan

Apr

Jul

Oct

Jan

Apr

40000

50000

60000

70000

80000

90000

100000

110000

120000

Jan

Apr

Jul

Oct

Jan

Apr

Jul

Oct

Jan

Apr

Jul

Oct

Jan

Apr

1978 1979 1980

When customers panic: Chrysler New Car Sales 1978-‐1982

Iacocca joins Chrysler aher $248M loss

Treasury is quietly approached

Bailout plan goes public. Controversy.

Bailout chances very dim. Banks won't go along.

Loan guarantees are approved.

Print ads signed by Iacocca build confidence.

aher Chrysler bailout request becomes known.

The shareholder – debtholder conflict

• In financial distress, shareholders and debtholders have diverging goals

• As long as no formal default, shareholders have control. – can use their control rights to directly expropriate debtholders

• Cash in & run – More subtle ways of transfering value from debtholders to shareholders

• Underinvest (debt overhang) • Take more risk (gambling for resurrec=on)

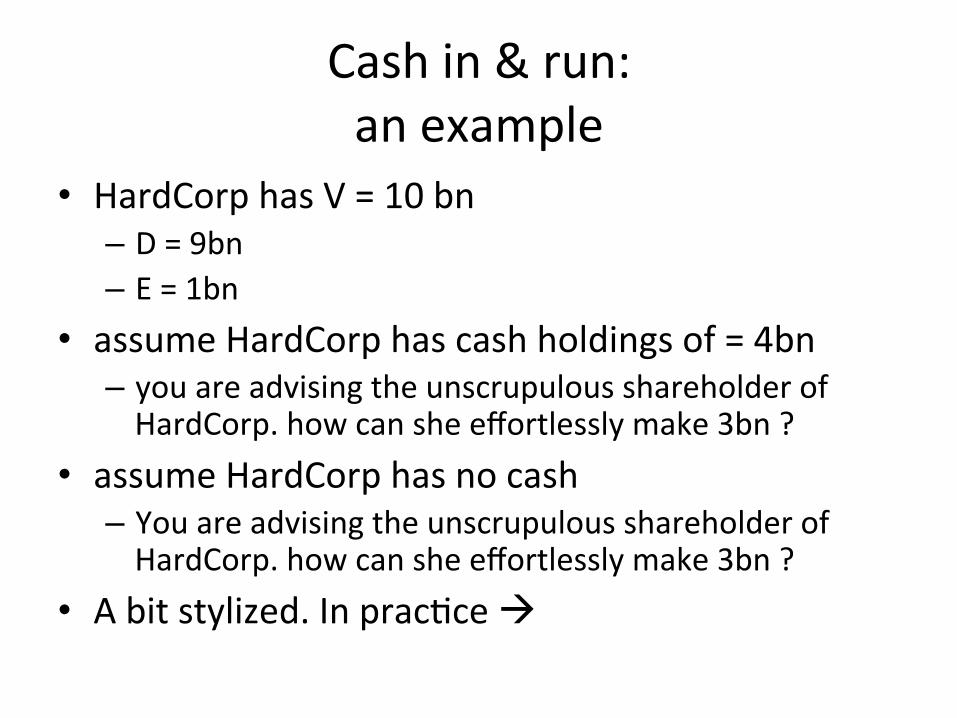

Cash in & run: an example

• HardCorp has V = 10 bn – D = 9bn – E = 1bn

• assume HardCorp has cash holdings of = 4bn – you are advising the unscrupulous shareholder of HardCorp. how can she effortlessly make 3bn ?

• assume HardCorp has no cash – You are advising the unscrupulous shareholder of HardCorp. how can she effortlessly make 3bn ?

• A bit stylized. In prac=ce à

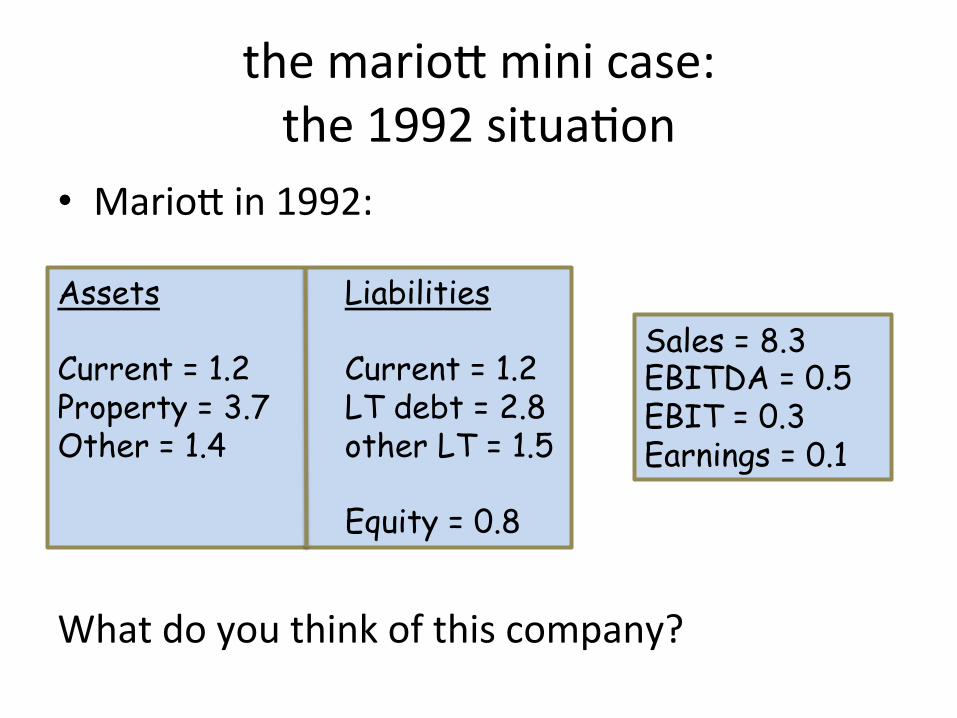

the marioq mini case: the 1992 situa=on

• Marioq in 1992:

What do you think of this company?

Assets Liabilities Current = 1.2 Current = 1.2 Property = 3.7 LT debt = 2.8 Other = 1.4 other LT = 1.5

Equity = 0.8

Sales = 8.3 EBITDA = 0.5 EBIT = 0.3 Earnings = 0.1

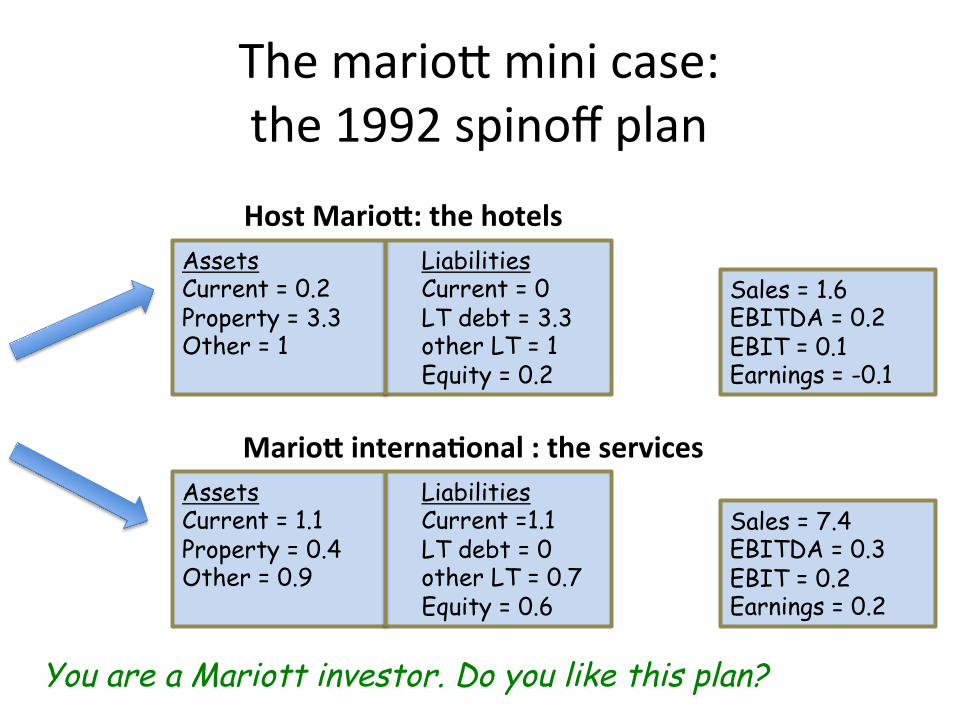

The marioq mini case: the 1992 spinoff plan

Assets Liabilities Current = 0.2 Current = 0 Property = 3.3 LT debt = 3.3 Other = 1 other LT = 1

Equity = 0.2

Sales = 1.6 EBITDA = 0.2 EBIT = 0.1 Earnings = -0.1

Assets Liabilities Current = 1.1 Current =1.1 Property = 0.4 LT debt = 0 Other = 0.9 other LT = 0.7

Equity = 0.6

Sales = 7.4 EBITDA = 0.3 EBIT = 0.2 Earnings = 0.2

Host Mario3: the hotels

Mario3 interna0onal : the services

You are a Mariott investor. Do you like this plan?

Marioq mini case value crea=on

• Assume that before spinoff – market value of debt = book (face) value – market value of equity = 2bn

• Assume that aher spinoff – value of debt of host decreases by 8%

• When spinoff is announced, what is the stock price reac=on?

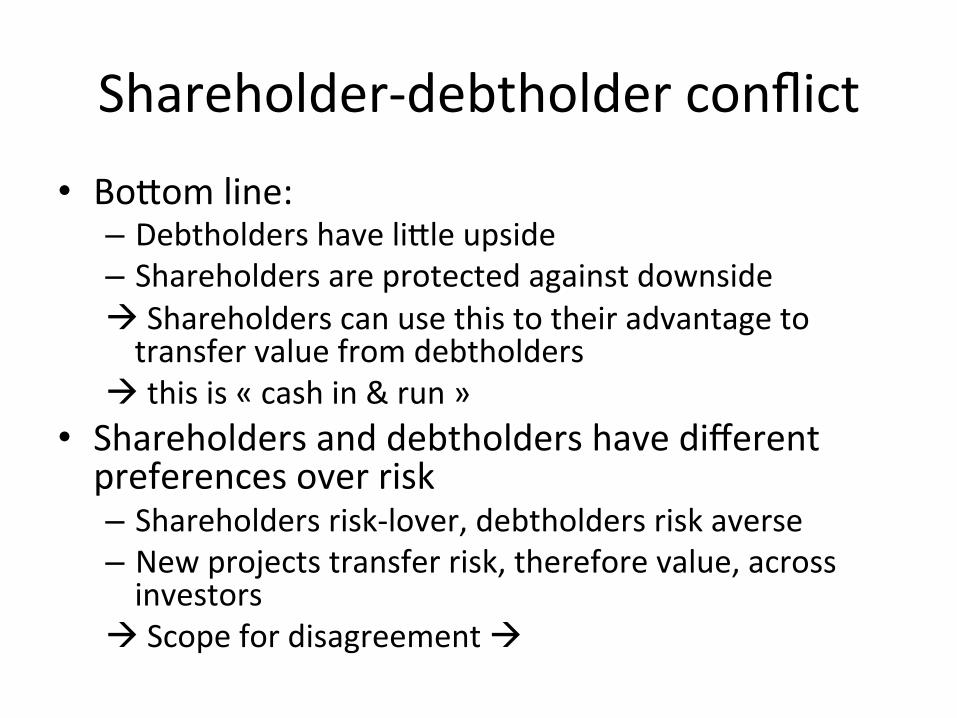

Shareholder-‐debtholder conflict • Boqom line:

– Debtholders have liqle upside – Shareholders are protected against downside à Shareholders can use this to their advantage to transfer value from debtholders

à this is « cash in & run » • Shareholders and debtholders have different preferences over risk – Shareholders risk-‐lover, debtholders risk averse – New projects transfer risk, therefore value, across investors

à Scope for disagreement à

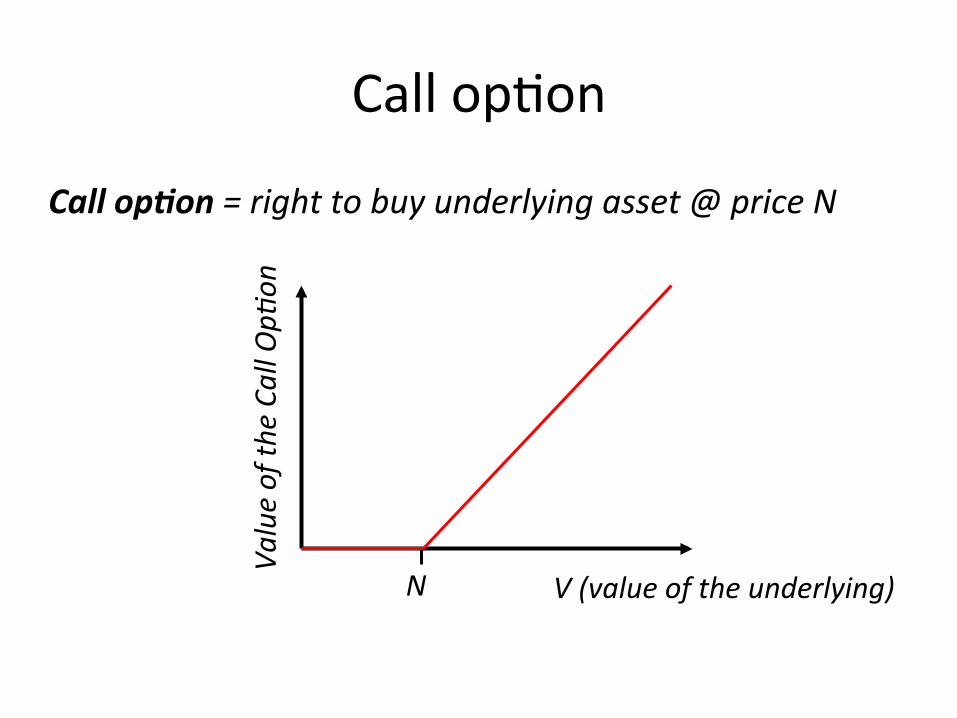

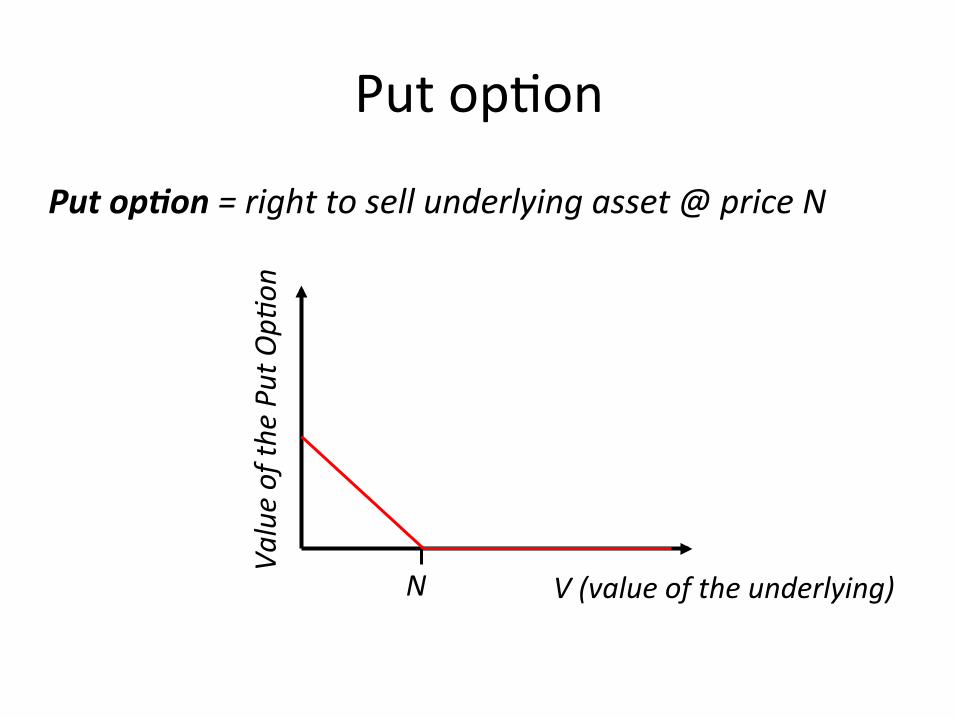

Call op=on

Call op'on = right to buy underlying asset @ price N

N V (value of the underlying)

Value of th

e Ca

ll Op=

on

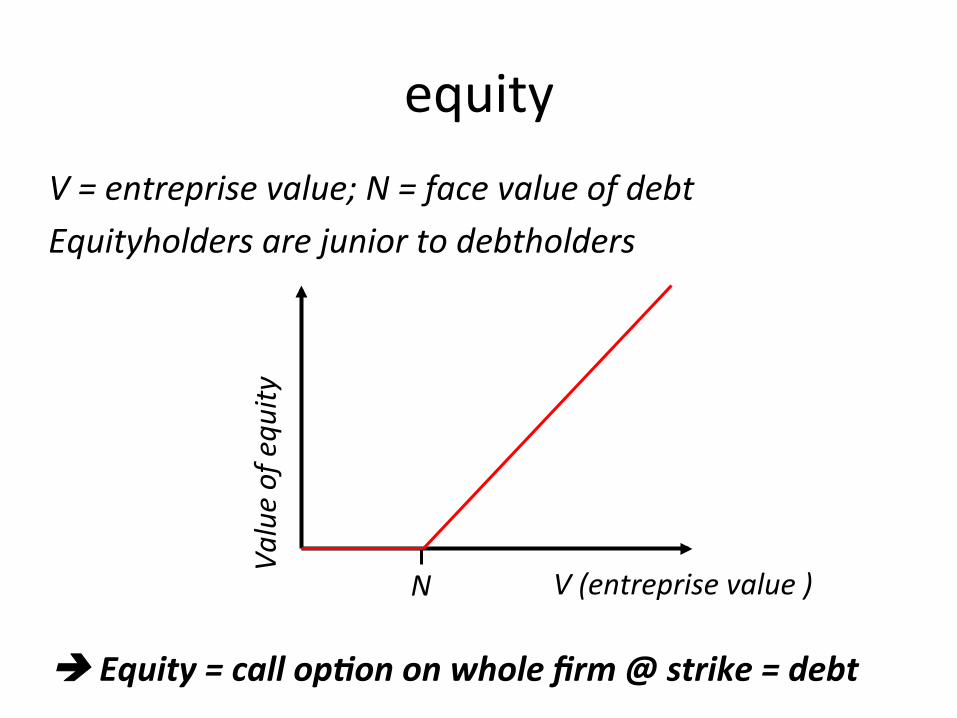

equity V = entreprise value; N = face value of debt Equityholders are junior to debtholders

N V (entreprise value )

Value of equ

ity

è Equity = call op'on on whole firm @ strike = debt

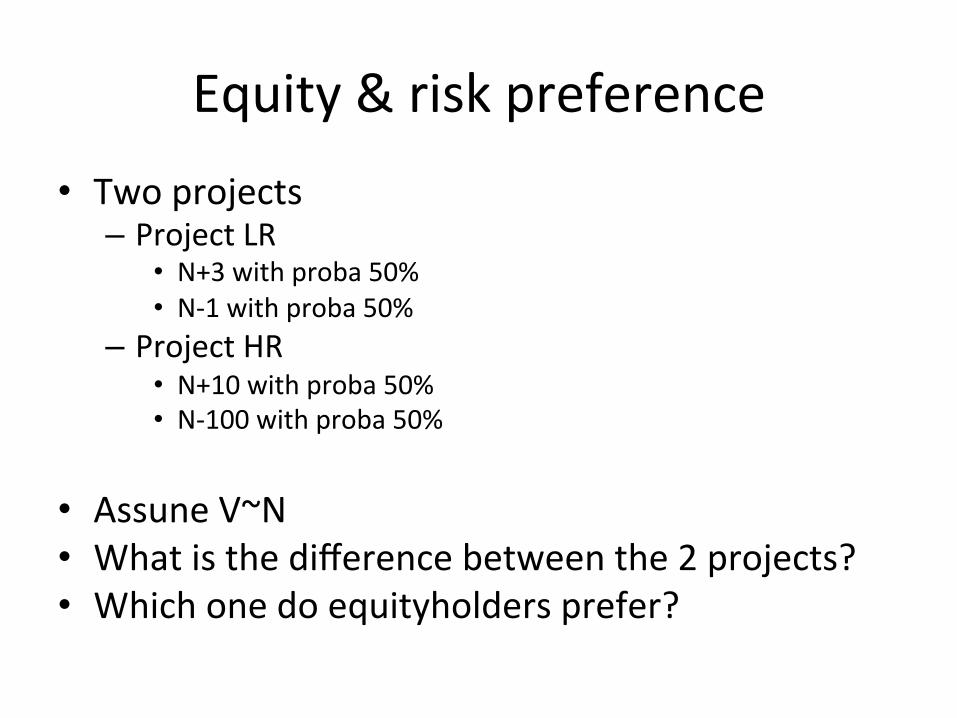

Equity & risk preference • Two projects

– Project LR • N+3 with proba 50% • N-‐1 with proba 50%

– Project HR • N+10 with proba 50% • N-‐100 with proba 50%

• Assune V~N • What is the difference between the 2 projects? • Which one do equityholders prefer?

Put op=on

Put op'on = right to sell underlying asset @ price N

N V (value of the underlying)

Value of th

e Pu

t Op=

on

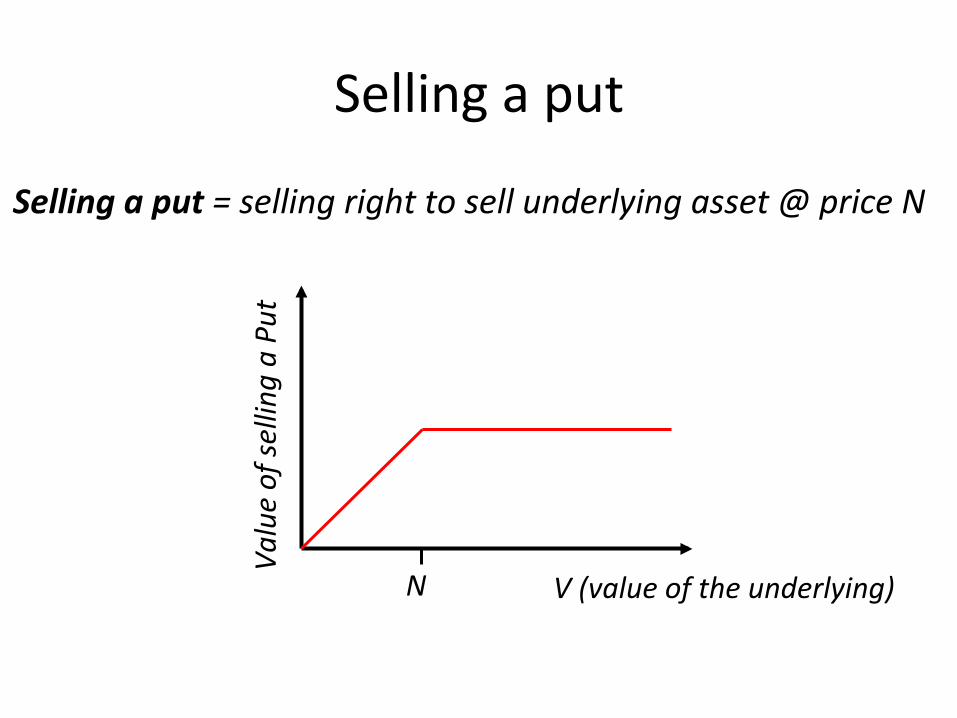

Selling a put

Selling a put = selling right to sell underlying asset @ price N

N V (value of the underlying)

Value of se

lling

a Put

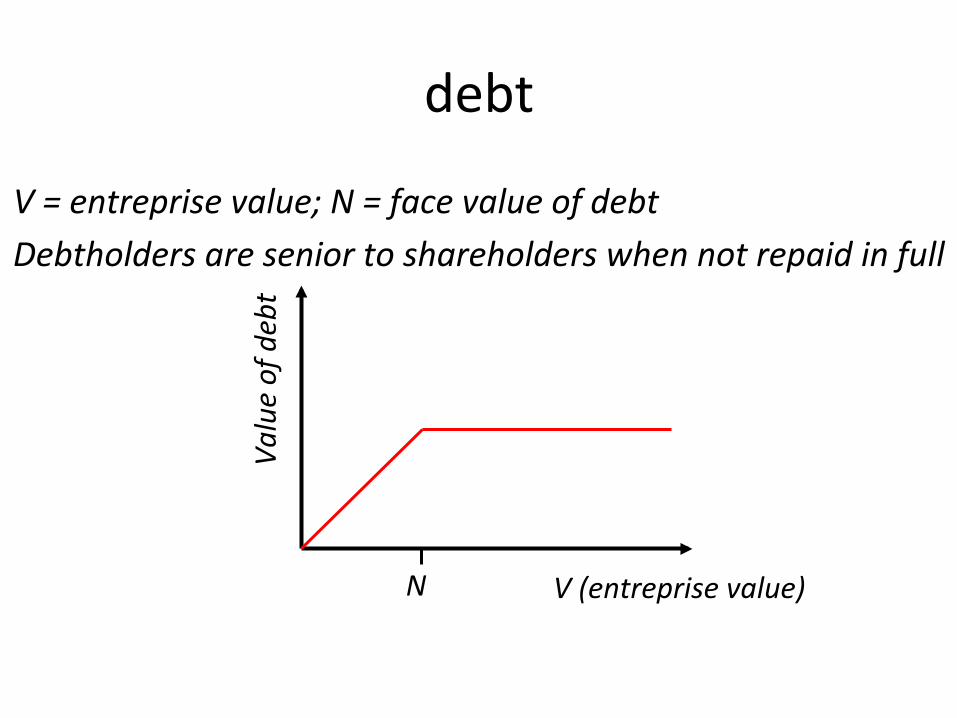

debt

V = entreprise value; N = face value of debt Debtholders are senior to shareholders when not repaid in full

N V (entreprise value)

Value of debt

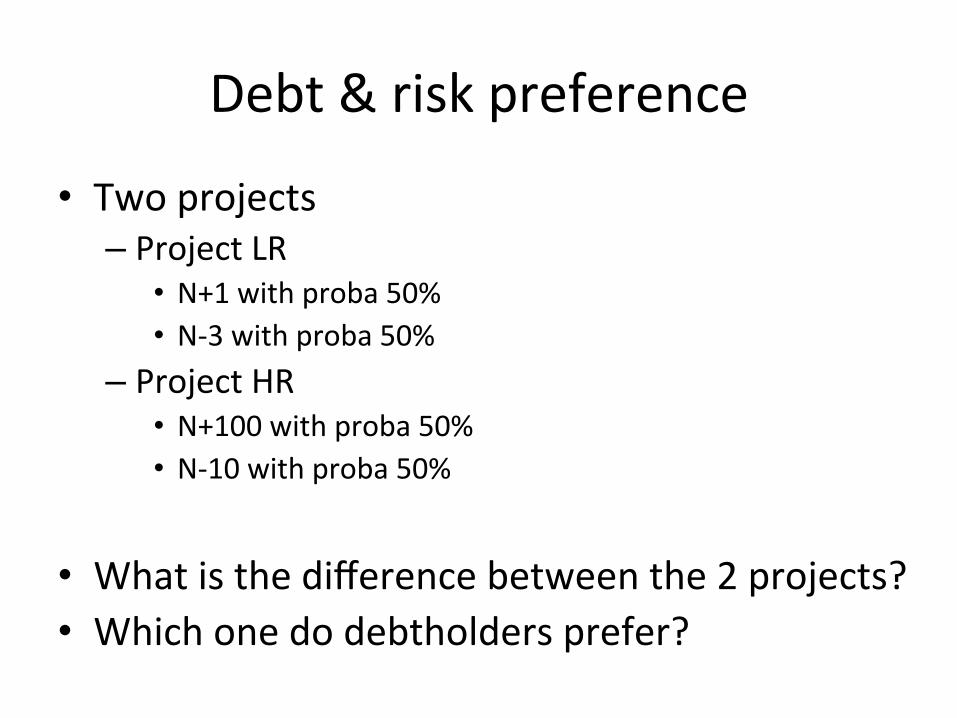

Debt & risk preference

• Two projects – Project LR

• N+1 with proba 50% • N-‐3 with proba 50%

– Project HR • N+100 with proba 50% • N-‐10 with proba 50%

• What is the difference between the 2 projects? • Which one do debtholders prefer?

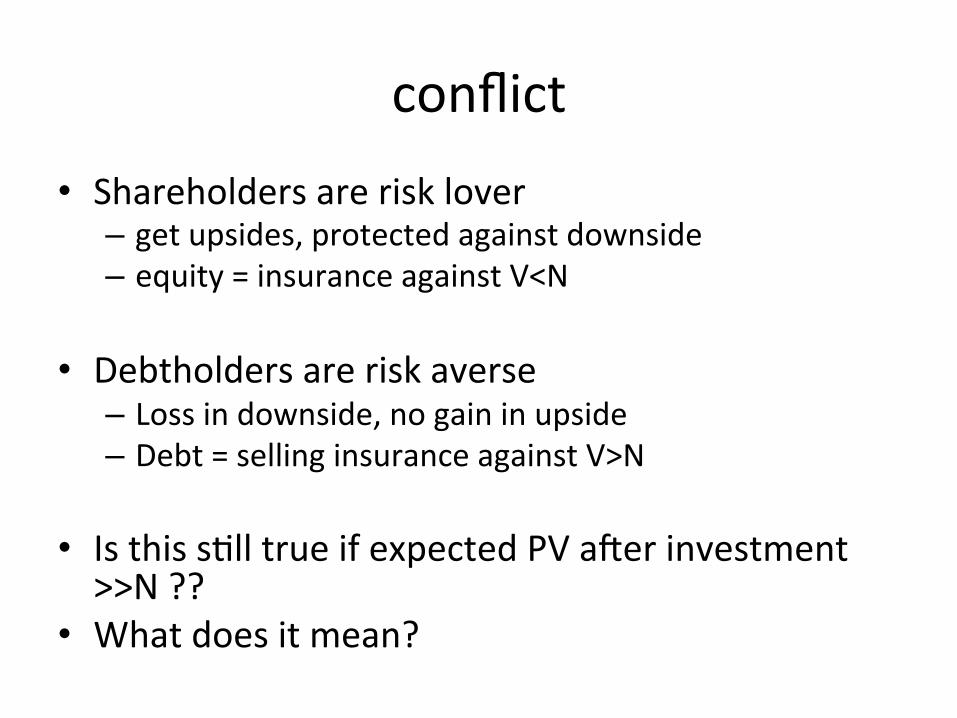

conflict • Shareholders are risk lover

– get upsides, protected against downside – equity = insurance against V<N

• Debtholders are risk averse – Loss in downside, no gain in upside – Debt = selling insurance against V>N

• Is this s=ll true if expected PV aher investment >>N ??

• What does it mean?

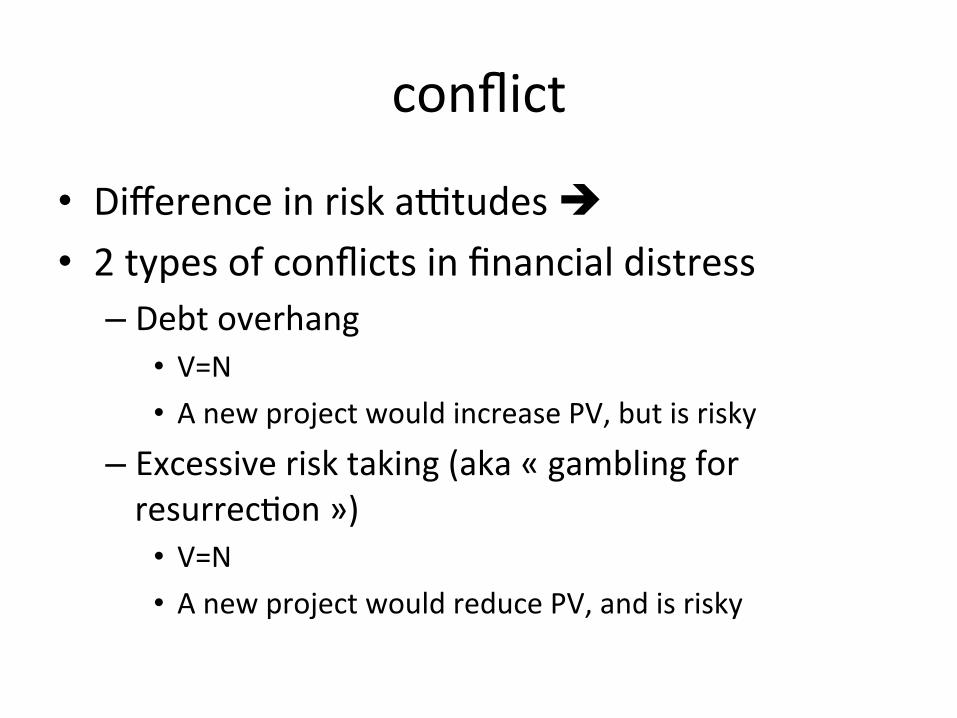

conflict

• Difference in risk autudes è • 2 types of conflicts in financial distress

– Debt overhang • V=N • A new project would increase PV, but is risky

– Excessive risk taking (aka « gambling for resurrec=on »)

• V=N • A new project would reduce PV, and is risky

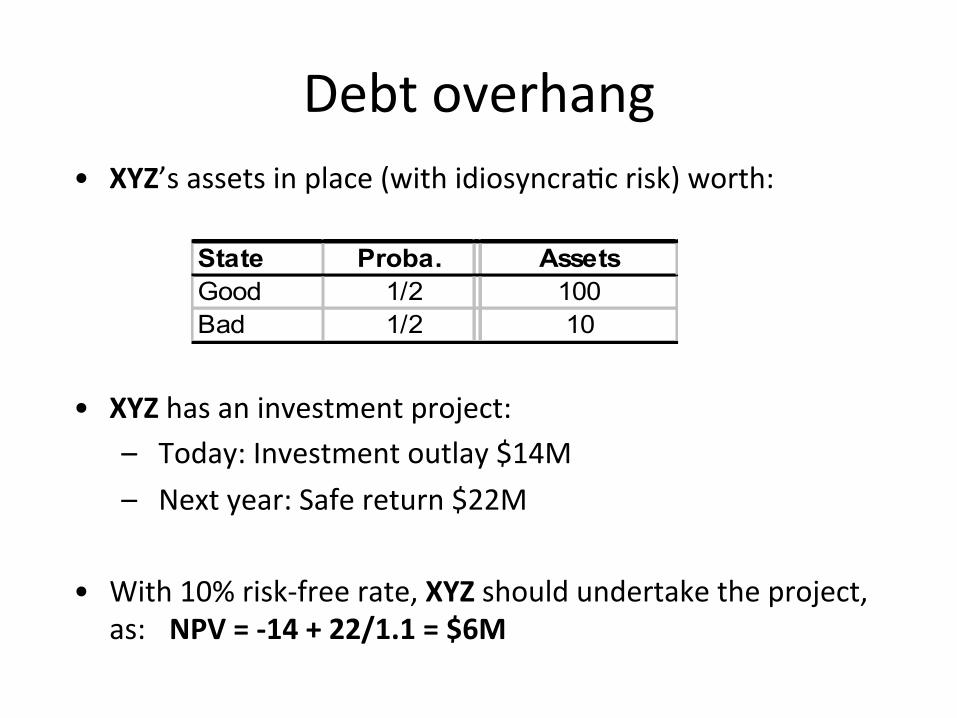

• XYZ’s assets in place (with idiosyncra=c risk) worth:

• XYZ has an investment project: – Today: Investment outlay $14M – Next year: Safe return $22M

• With 10% risk-‐free rate, XYZ should undertake the project,

as: NPV = -‐14 + 22/1.1 = $6M

State Proba. AssetsGood 1/2 100Bad 1/2 10

Debt overhang

• XYZ has debt with face value $35M due next year

• XYZ’s shareholders will not fund the project (e.g. by cuung today’s dividend payment) because: NPV = -‐14 + [(1/2)*22 + (1/2)*0]/1.1 = -‐$4M

State Proba. Assets Creditors ShareholdersGood 1/2 100 35 65Bad 1/2 10 10 0

Without the Project

State Proba. Assets Creditors ShareholdersGood 1/2 100+22=122 35 65+22=87Bad 1/2 10+22=32 10+22=32 0

With the Project

Debt overhang

• Shareholders would: – Incur the full investment cost: -‐ $14M – Receive part of the return (22 in good state only)

• Exis=ng creditors would: – Incur none of the investment cost – S=ll receive part of the return (22 in the bad state)

è Creditors always get a frac0on of returns è Exis0ng debt acts as a “tax on investment”

This is “debt overhang”: NPV>0 projects are not undertaken

Debt overhang

• Assume now the probability of the bad state is 1/4 instead of ½

• is XYZ taking up the project? • how do you interpret this?

Debt overhang

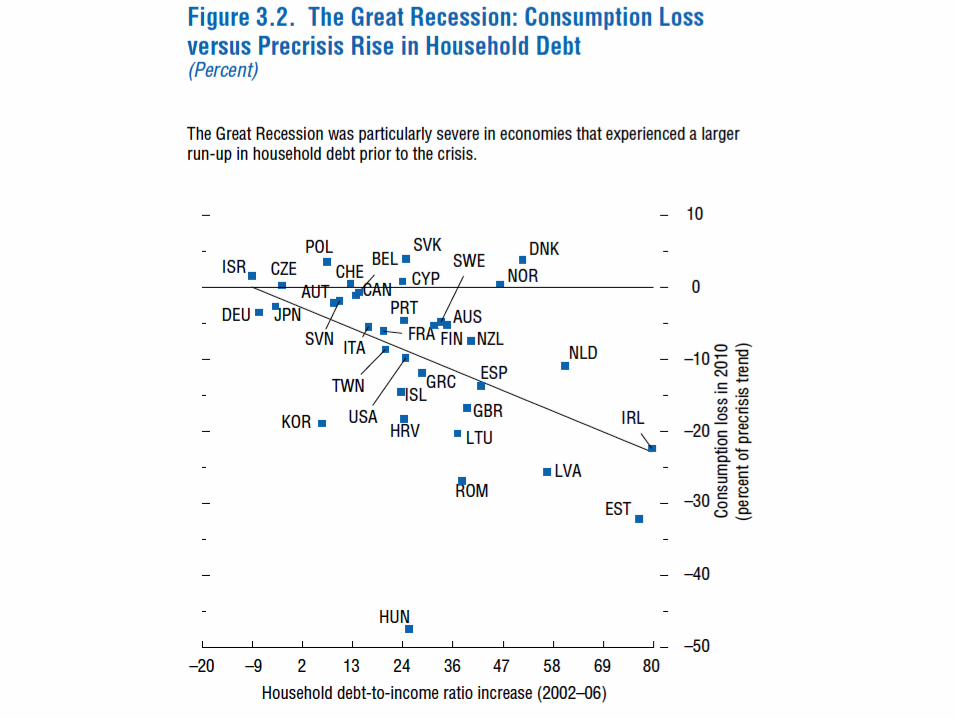

debt overhang at the country level

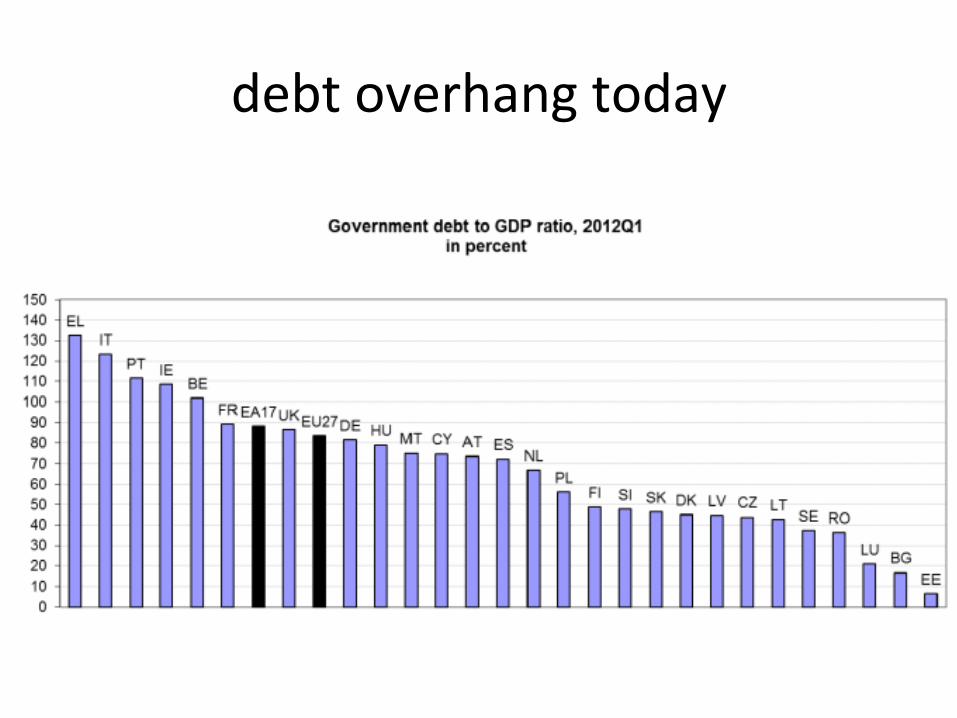

debt overhang today

(back to case where p(success)=1/2) • New equity issue New shareholders would have to break even à Dividend D such that: -‐14 + [(1/2)*D + (1/2)*0]/1.1 = 0 à NPV of this decision to exis=ng shareholders: NPV = [(1/2)*(22-‐D) + (1/2)*0]/1.1 = -‐$4M, again

è exis0ng shareholders do not vote for new equity issue ! • New debt issue, junior to exis'ng debt ? à exactly the same calcula0on !

è Issuing junior debt does not solve the problem

Debt overhang: What can be done?

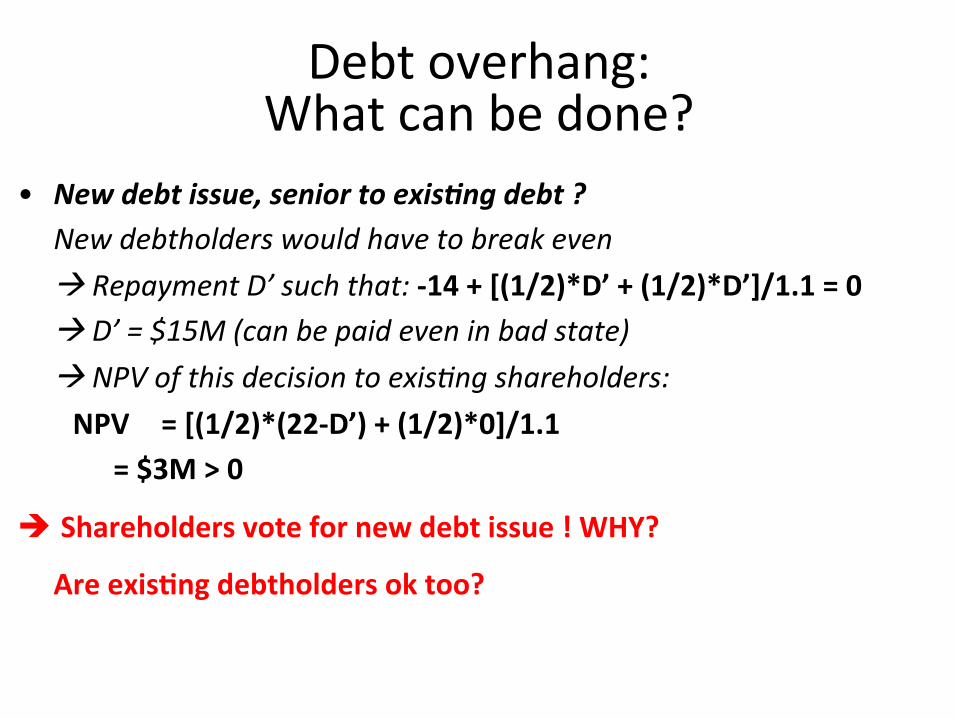

• New debt issue, senior to exis'ng debt ? New debtholders would have to break even à Repayment D’ such that: -‐14 + [(1/2)*D’ + (1/2)*D’]/1.1 = 0 à D’ = $15M (can be paid even in bad state) à NPV of this decision to exis=ng shareholders: NPV = [(1/2)*(22-‐D’) + (1/2)*0]/1.1 = $3M > 0

è Shareholders vote for new debt issue ! WHY?

Are exis0ng debtholders ok too?

Debt overhang: What can be done?

• Exis'ng debt holders • s=ll get 35 in good state • get 32 – 15 = $17M in bad state, instead of just $10M

è value of exis0ng debt increases by (7/2)/1.1 = $3M

Everyone agrees to this issue (even debt holders). Why?

Debt overhang: What can be done?

• More general issue:

here, inves'ng = the pie becomes larger à you can make everyone be3er off

• Assume creditors reduce the face value to $24M, if and only if the project is done. What happens? • This is restructuring

Debt overhang: What can be done?

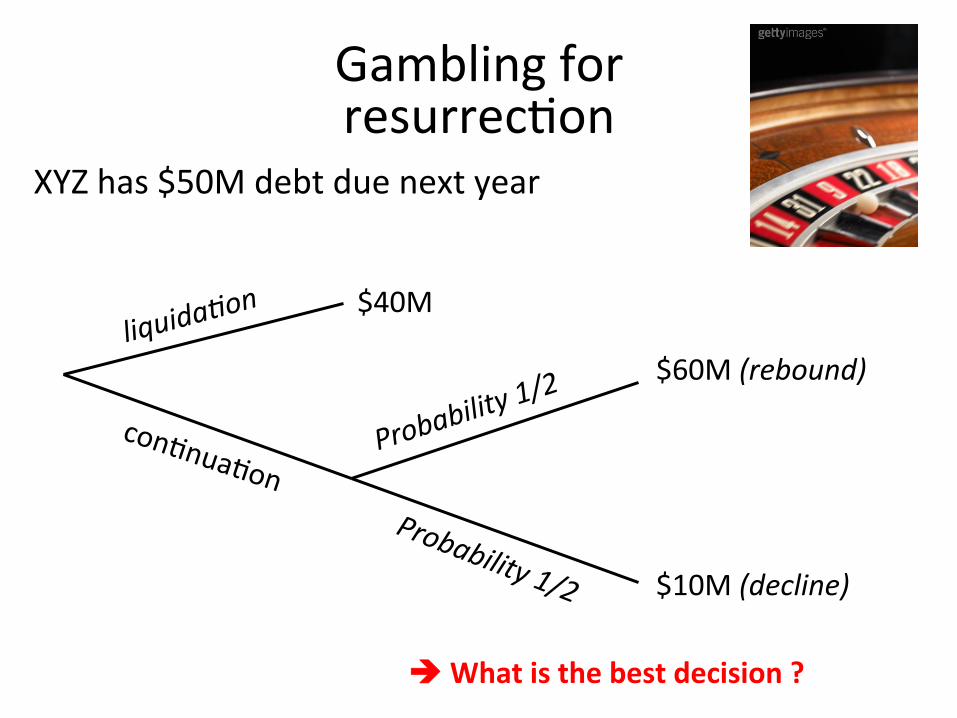

XYZ has $50M debt due next year

$40M liquida

=on

con=nua=on Proba

bility 1/2

$60M (rebound)

$10M (decline)

è What is the best decision ?

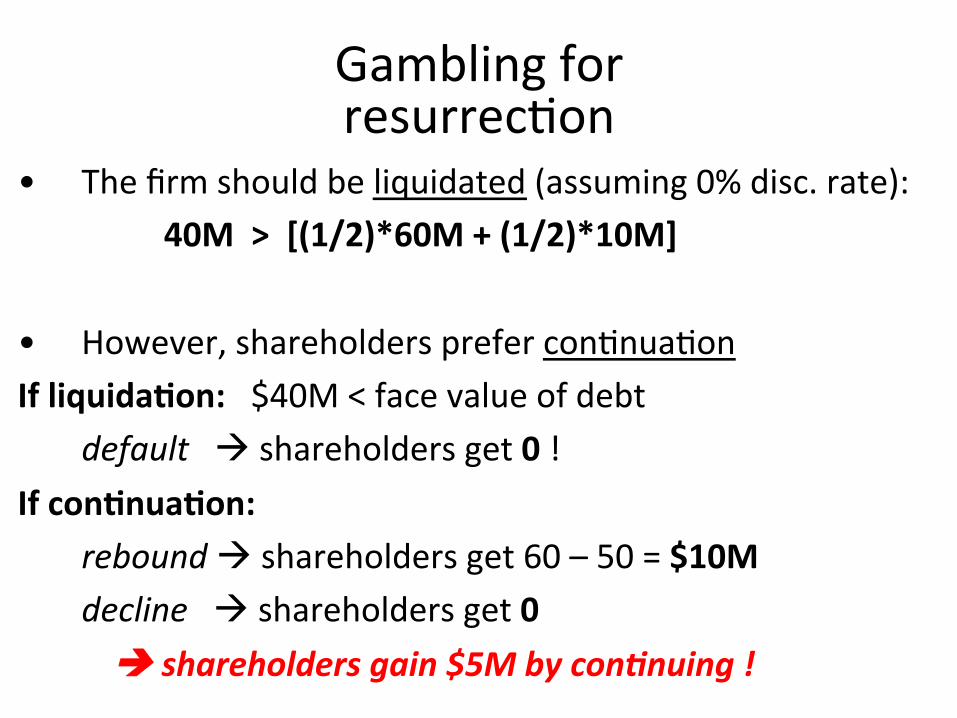

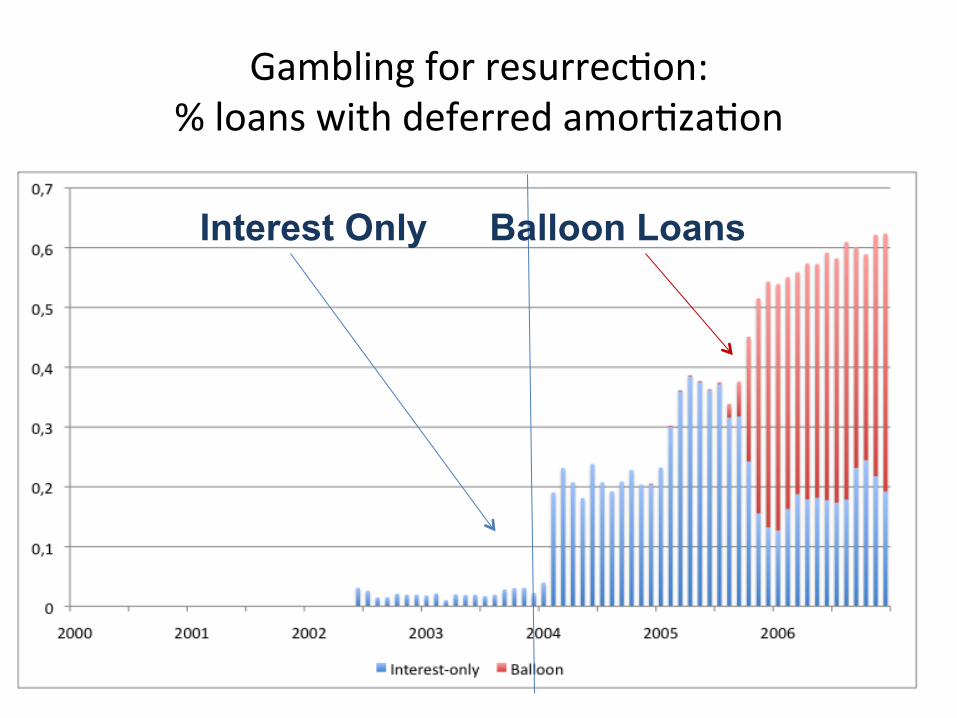

Gambling for resurrec=on

• The firm should be liquidated (assuming 0% disc. rate): 40M > [(1/2)*60M + (1/2)*10M]

• However, shareholders prefer con=nua=on If liquida0on: $40M < face value of debt

default à shareholders get 0 ! If con0nua0on:

rebound à shareholders get 60 – 50 = $10M decline à shareholders get 0 è shareholders gain $5M by con'nuing !

Gambling for resurrec=on

• who gains, who loses?

• NPV of gambling: to the firm = -‐5 to shareholders = 5 to debtholders = -‐10 !

è Gambling = transfer PV from creditors to shareholders

Gambling for resurrec=on

• Imagine the shareholder is in control • Can decide alone to gamble or not

• What are debtholders’ op=ons to get out of this?

Gambling for resurrec=on

gambling for resurrec=on in real life

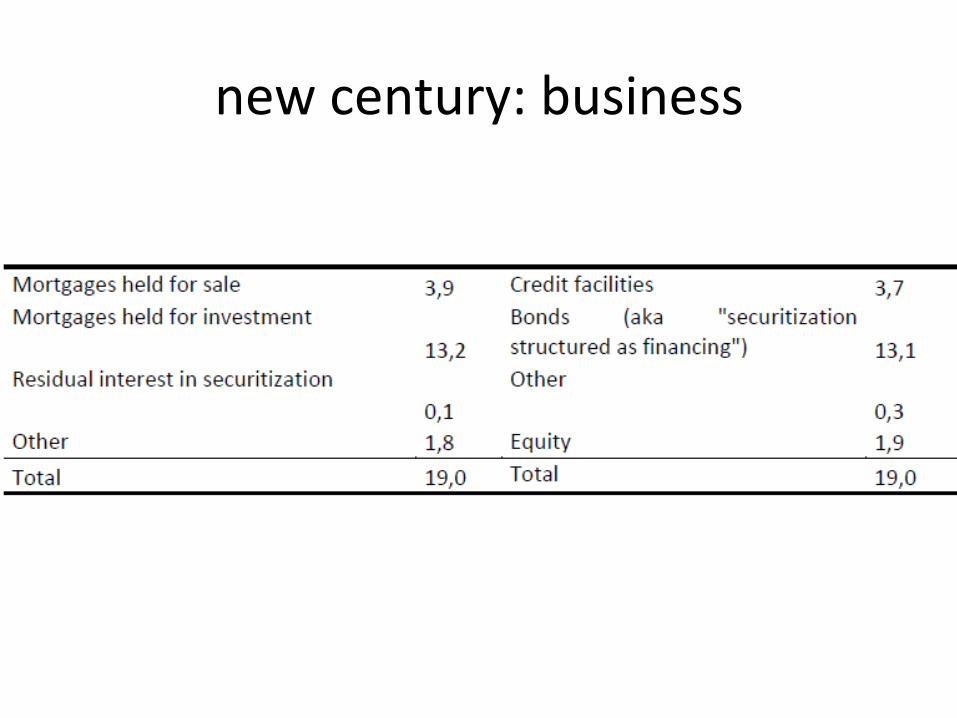

new century: business

NEW CENTURY

Inventory

BROKERS RETAIL

Whole Loan Sale

Securi=za=on as Financing

Securi=za=on as Sale

30Bn

38Bn 4Bn

10Bn

≈0Bn Kept as long term investment !

new century: business

Monetary =ghtening

¨ LIBOR 1m

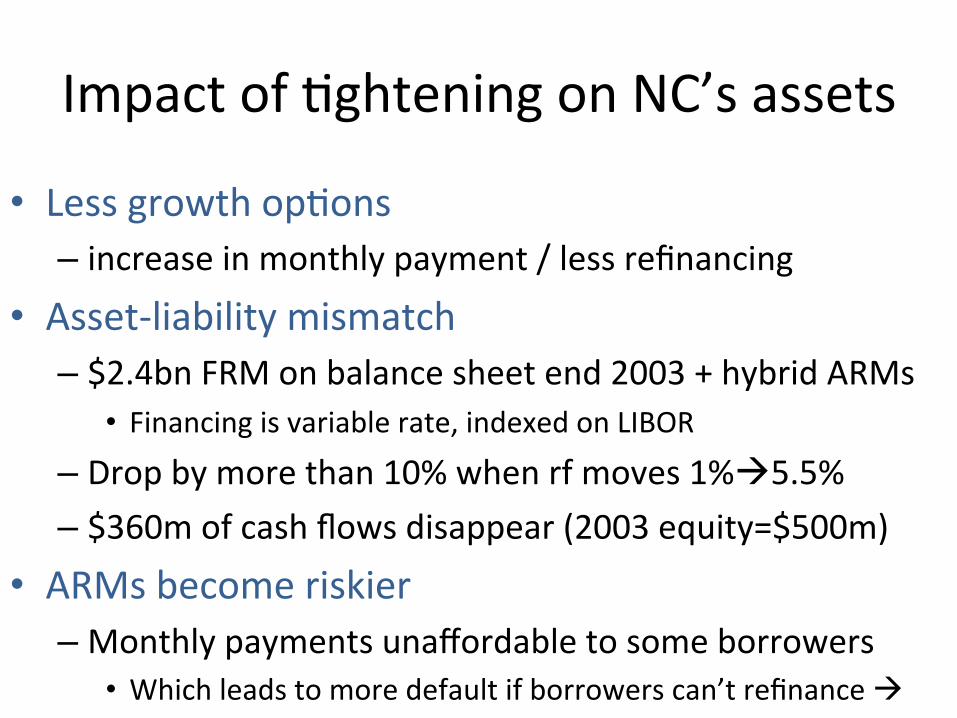

Impact of =ghtening on NC’s assets

• Less growth op=ons – increase in monthly payment / less refinancing

• Asset-‐liability mismatch – $2.4bn FRM on balance sheet end 2003 + hybrid ARMs

• Financing is variable rate, indexed on LIBOR – Drop by more than 10% when rf moves 1%à5.5% – $360m of cash flows disappear (2003 equity=$500m)

• ARMs become riskier – Monthly payments unaffordable to some borrowers

• Which leads to more default if borrowers can’t refinance à

ARMs become riskier The reset =cking bomb (>60 days delinquent)

Gambling for resurrec=on: % loans with deferred amor=za=on

Interest Only Balloon Loans

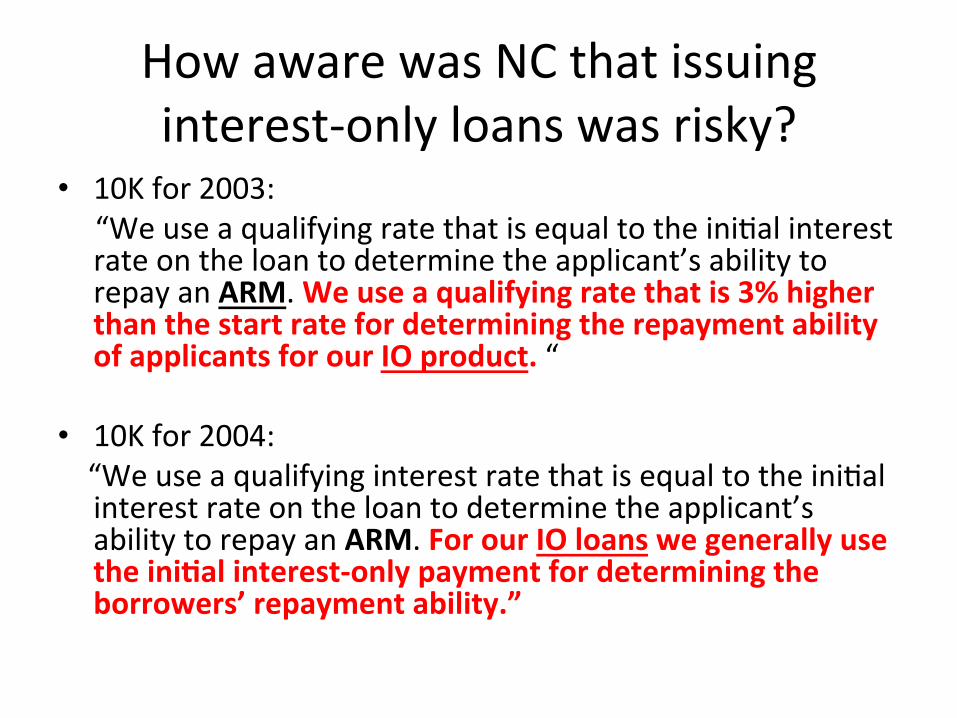

How aware was NC that issuing interest-‐only loans was risky?

• 10K for 2003: “We use a qualifying rate that is equal to the ini=al interest

rate on the loan to determine the applicant’s ability to repay an ARM. We use a qualifying rate that is 3% higher than the start rate for determining the repayment ability of applicants for our IO product. “

• 10K for 2004: “We use a qualifying interest rate that is equal to the ini=al

interest rate on the loan to determine the applicant’s ability to repay an ARM. For our IO loans we generally use the ini0al interest-‐only payment for determining the borrowers’ repayment ability.”

• Renego=ate • Commit • Issue the right security

Avoiding conflicts

Avoiding conflicts • Renego=a=on is useful ex post

– It prevents PV from being destroyed – This is « debt restructuring »

• What makes renego=a=on easy? – Take few creditors

• One bank is beqer than bondholders – Issue homogenous debt securi=es

• Subordinated debtholders have different objec=ves than secured debtholders (they are like shareholders, they can « hold out »)

– bankruptcy law maqers

Avoiding conflicts bankruptcy law around the world

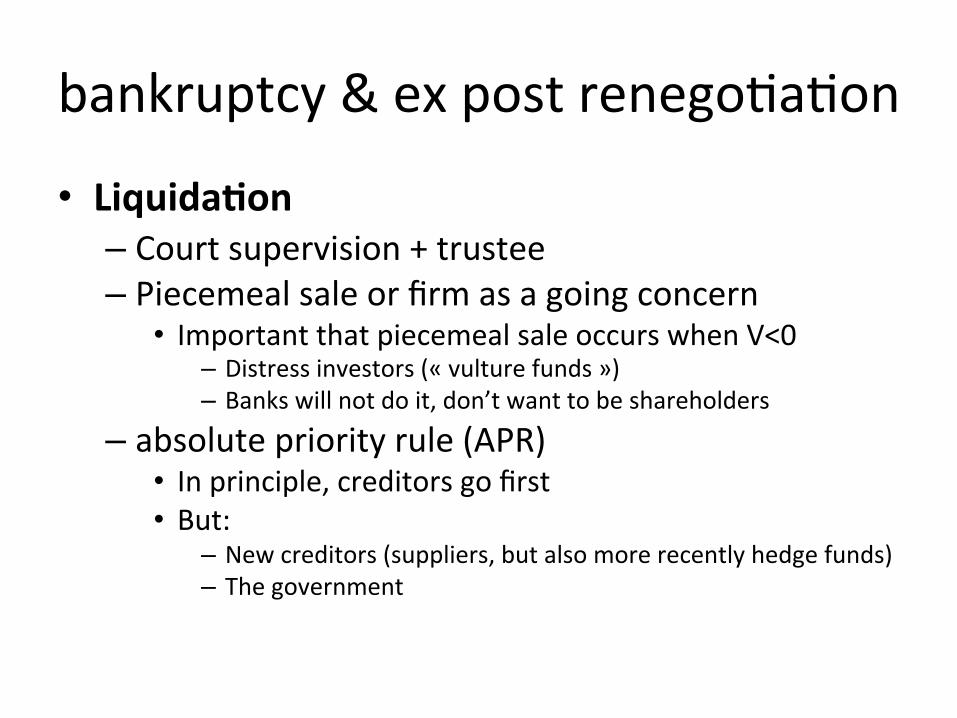

• Three procedures

– Straight liquida=on

– Reorganiza=on

– Foreclosure

• Liquida0on – Court supervision + trustee – Piecemeal sale or firm as a going concern

• Important that piecemeal sale occurs when V<0 – Distress investors (« vulture funds ») – Banks will not do it, don’t want to be shareholders

– absolute priority rule (APR) • In principle, creditors go first • But:

– New creditors (suppliers, but also more recently hedge funds) – The government

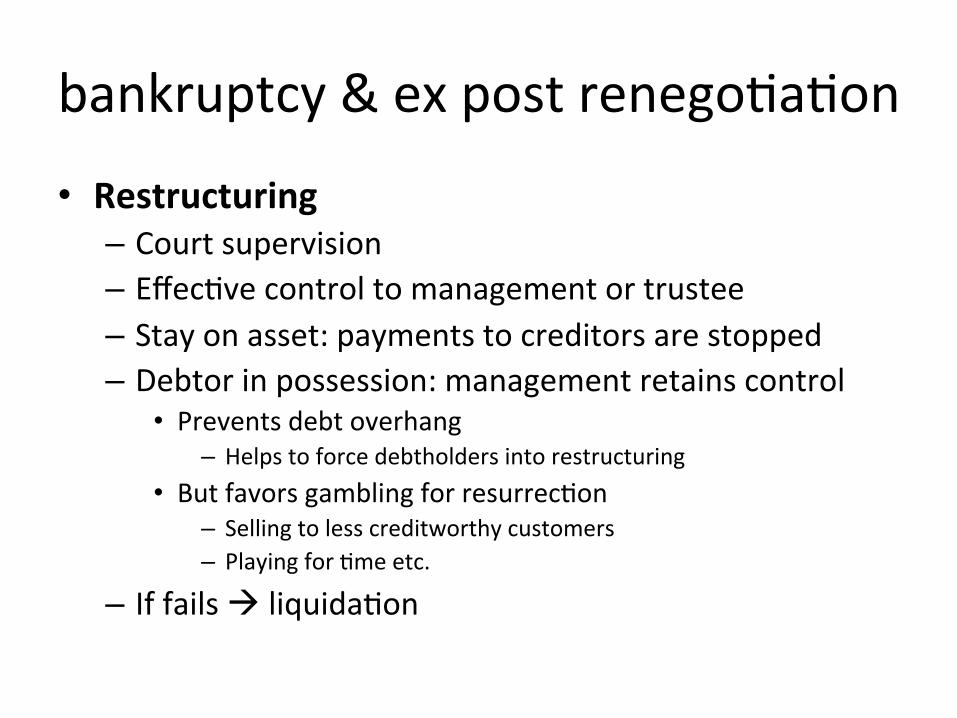

bankruptcy & ex post renego=a=on

• Restructuring – Court supervision – Effec=ve control to management or trustee – Stay on asset: payments to creditors are stopped – Debtor in possession: management retains control

• Prevents debt overhang – Helps to force debtholders into restructuring

• But favors gambling for resurrec=on – Selling to less creditworthy customers – Playing for =me etc.

– If fails à liquida=on

bankruptcy & ex post renego=a=on

bankruptcy & ex post renego=a=on

• Outright foreclosure – NO COURT SUPERVISION – When floa=ng charge security:

• En=re firm serves as collateral to debt • gives 100% ownership IF default, no court • Firm cannot issue more than 1 FCS

– Holder becomes sole owner • Very quick (2 months) • no complex nego=a=on • no shareholder – debtholder conflict ex post

– No gambling for resurrec=on / no overhang

Avoiding conflicts

• Renego=a=on can be costly, however • Intui=on:

– In distress, debtholders « bribe » shareholders to prevent them from destroying value

– Shareholders are not punished « enough » in distress. They can blackmail debtholders

– This destroys incen=ves to avoid distress – Value is destroyed, ex ante

• Commitment not to gamble can be beqer!

$40M liquida

=on

con=nua=on Proba

bility 1/2

$60M

$10M

$100M

Shareholder can influence proba of success

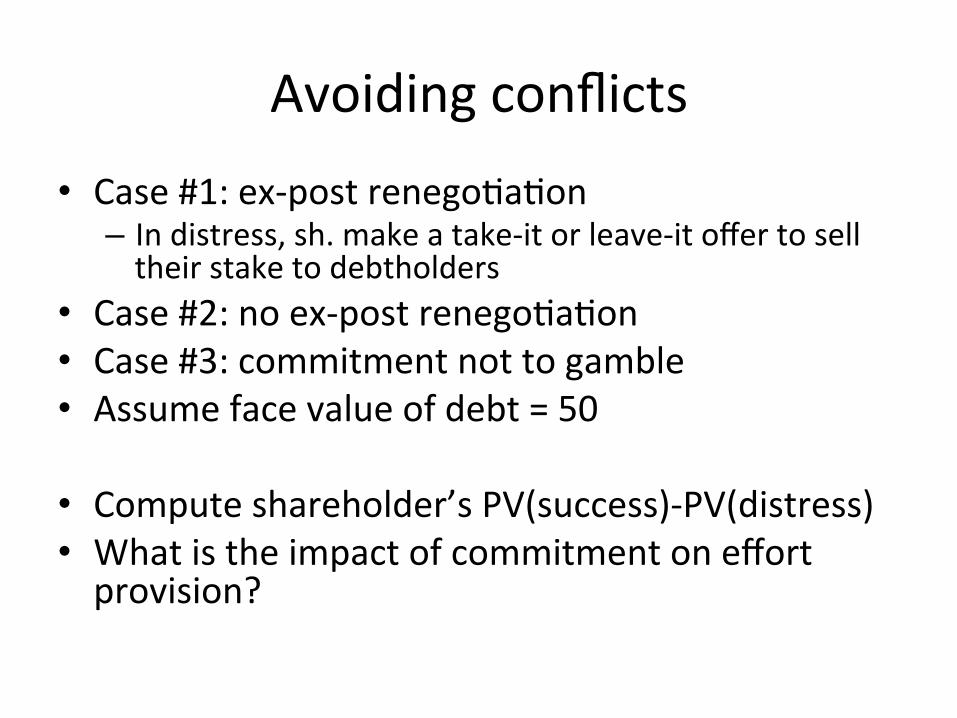

Avoiding conflicts • Case #1: ex-‐post renego=a=on

– In distress, sh. make a take-‐it or leave-‐it offer to sell their stake to debtholders

• Case #2: no ex-‐post renego=a=on • Case #3: commitment not to gamble • Assume face value of debt = 50

• Compute shareholder’s PV(success)-‐PV(distress) • What is the impact of commitment on effort provision?

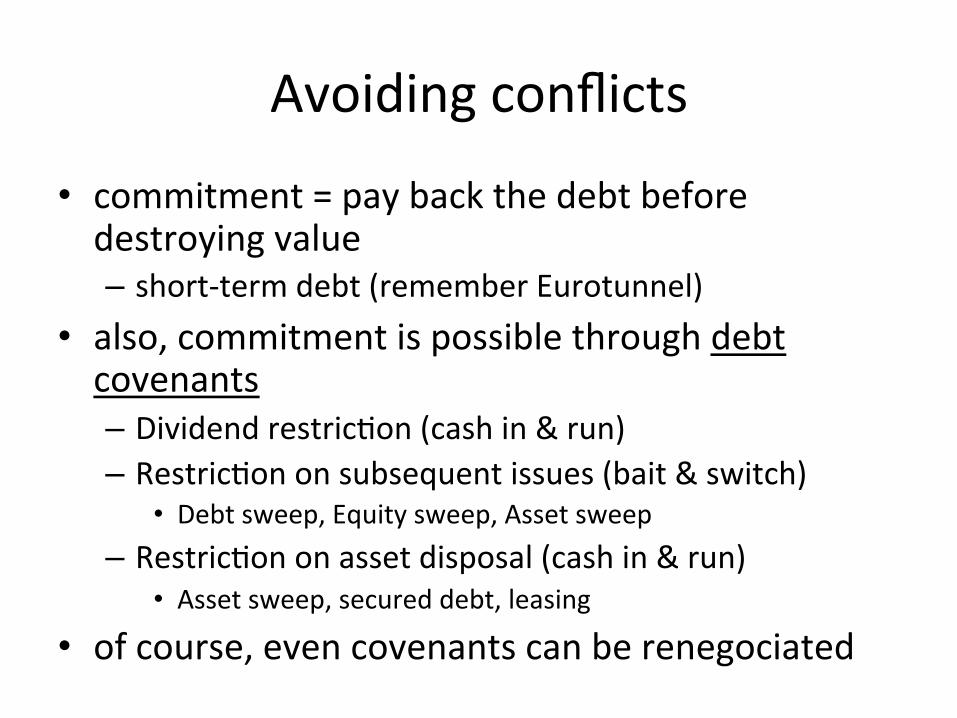

Avoiding conflicts

• commitment = pay back the debt before destroying value – short-‐term debt (remember Eurotunnel)

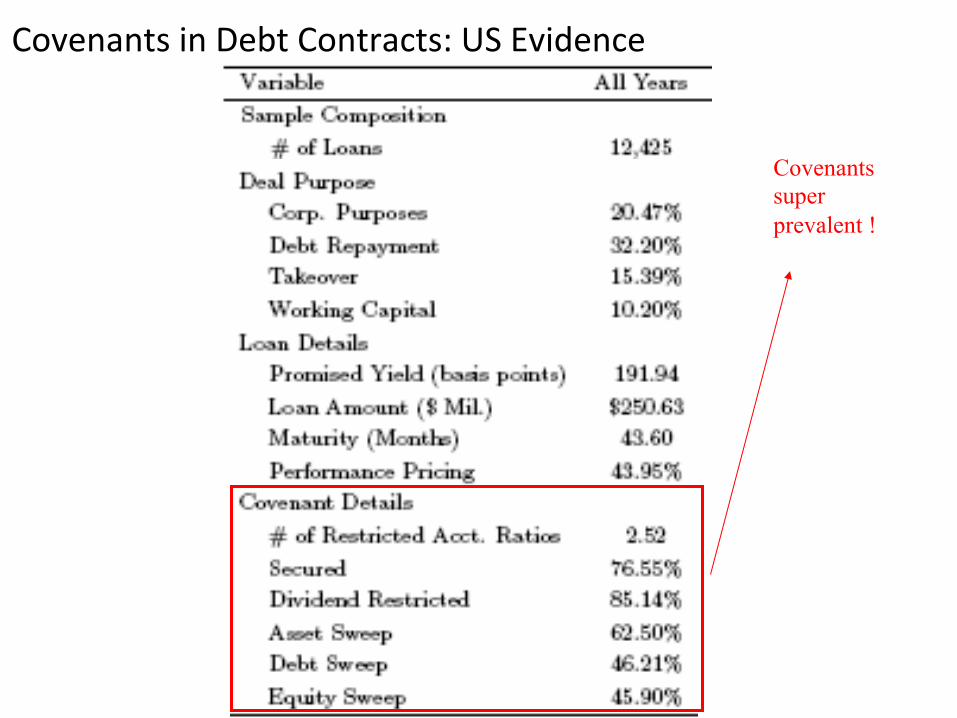

• also, commitment is possible through debt covenants – Dividend restric=on (cash in & run) – Restric=on on subsequent issues (bait & switch)

• Debt sweep, Equity sweep, Asset sweep – Restric=on on asset disposal (cash in & run)

• Asset sweep, secured debt, leasing • of course, even covenants can be renegociated

Covenants super prevalent !

Covenants in Debt Contracts: US Evidence

© David THESMAR

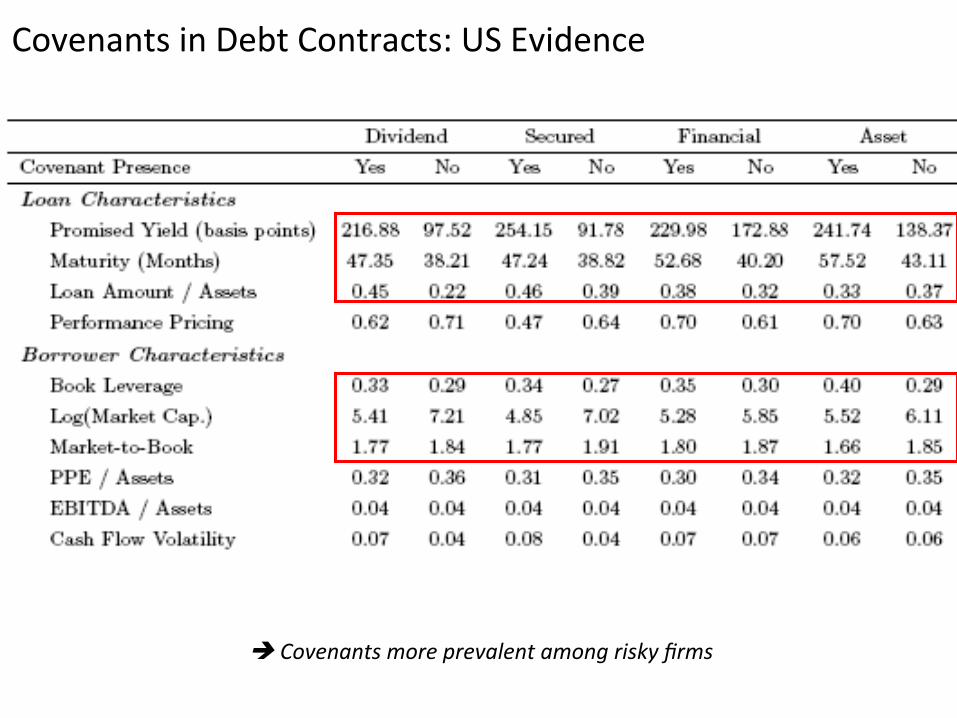

Covenants in Debt Contracts: US Evidence

è Covenants more prevalent among risky firms

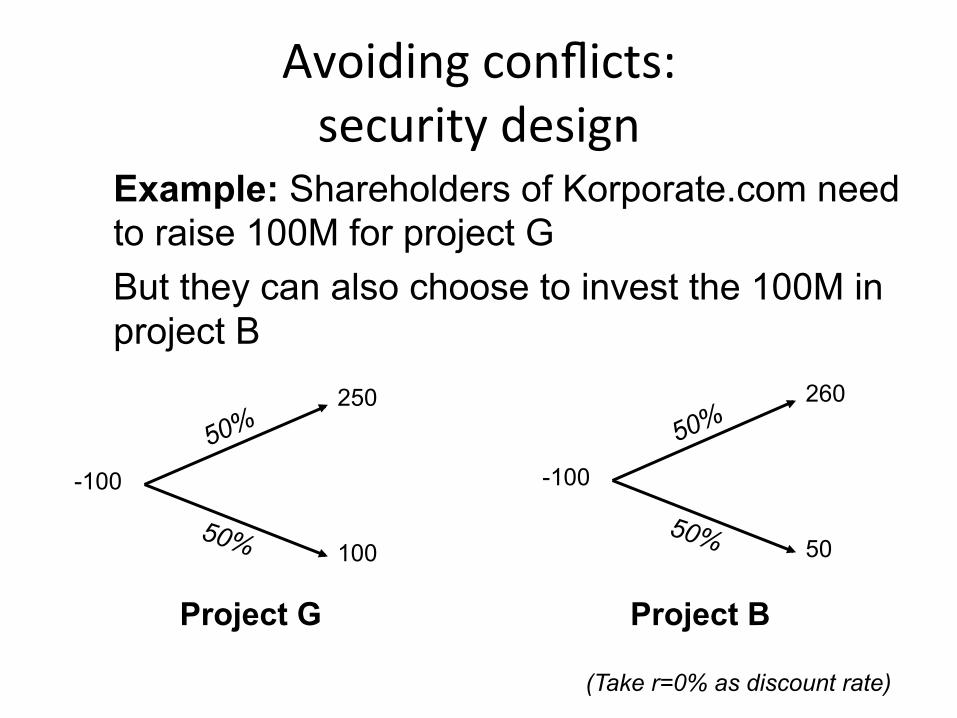

Avoiding conflicts: security design

Example: Shareholders of Korporate.com need to raise 100M for project G But they can also choose to invest the 100M in project B

250

100

-100

50%

260

50

-100

50%

Project G Project B

(Take r=0% as discount rate)

Avoiding conflicts

• Assume shareholders of Korporate.com want to issue debt – Debtholders want NPV=0 (compe==ve but ra=onal)

– Debtholders expect project choice ra=onally • What is the face value of debt. What is the value of equity? Are shareholders happy?

Avoiding conflicts

• Assume Korporate.com issues conver=ble debt – FV = 75 – Debtholders can convert if they want – Conver=on ra=o = 5 (= « conver=ble into 5 shares ») – Shareholders already own 5 shares

• Does this solve the problem? How?

Avoiding conflict

• Who issues conver=ble bonds? – distressed firms. remember Eurotunnel (why?) – Small firms, with liqle collateral – But also:

• Banks (for regulatory reasons) • market =mers (what is the mispricing?)

• Who buys conver=ble bonds?

– Venture capitalists – Hedge funds

Valua=on

• The WACC formula is not affected by costs of financial distress. Why?

• Hint: Go back to the gambling for resurrec=on example – Assume you need to raise $30M ini=ally

• What is the implict interest rate? – assume full commitment to liquidate – assume no commitment, no renego=a=on

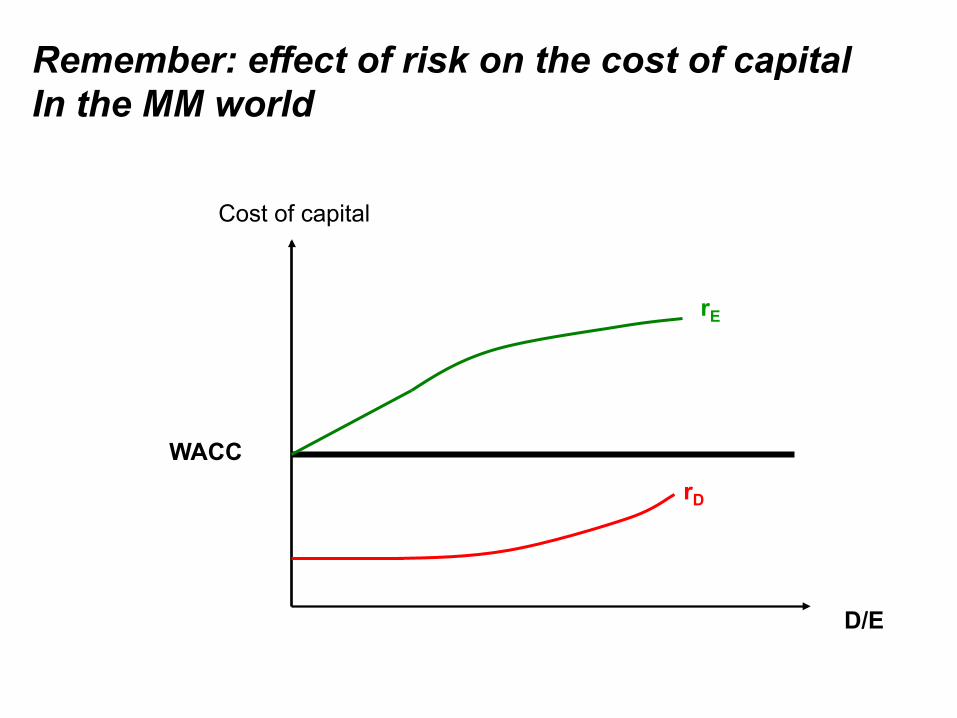

D/E

Cost of capital

WACC

rE

rD

Remember: effect of risk on the cost of capital In the MM world

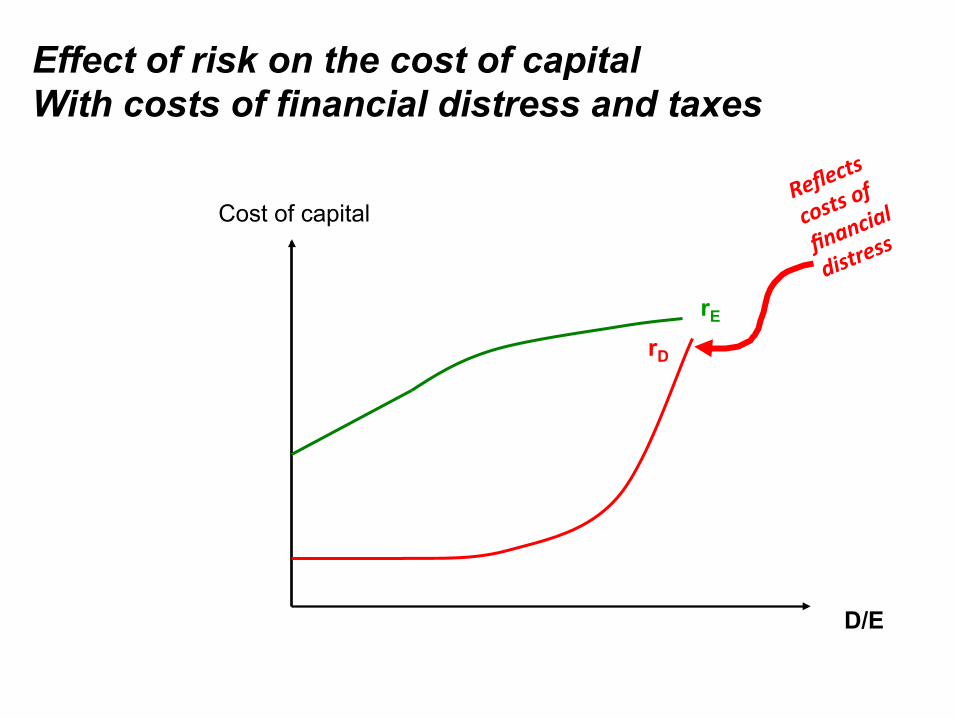

D/E

Cost of capital

rE

Effect of risk on the cost of capital With costs of financial distress and taxes

rD

D/E

Cost of capital

rE

rD

WACC =

e.rE + d.rD.

(1-‐t)

Op'mal capital structure = minimal WACC

Maximum value means minimum WACC: The WACC perspective on tradeoff theory

valua=on

• APV users should incorporate costs of financial distress

APV=PV(unlevered) + PV(tax shield)

- PV(costs of fin. distress) PV (cFD) = expected loss in distress / rFD

valua=on

• Is rFD big or small?

Take aways • Financial distress destroys value

– In distress, most of the loss is borne by debtholders – Debtholders are not stupid – Shareholders utlimately pay for it

• Shareholders can reduce these costs through commitment – Covenants, short term debt, conver=ble debt

• Capital structure trades off tax shield & costs of financial distress – Firms that are vola=le, have no collateral to pledge, whose stakeholders panick easily, should stay away from debt