Cost Based Pricing

for Procurement organizations and Manufacturing companies

Future Procurement

Robert Freeman Procurement Expert

Future Procurement

Cost Based Pricing for Procurement organizations and Manufacturing companies

1. What is price? 2. Why prices are different? 3. Three approaches to price setting 4. Cost Based Pricing principles 5. Getting it all together: Cost Based Pricing example 6. Pro’s and Con’s of Cost Based Pricing 7. Best way to use Cost Based Pricing concept

Future Procurement

1. What is price?

Future Procurement

Monetary equivalent of the product/service. Value of money per 1 unit of product or service. …

Future Procurement

Price is an alternative.

Future Procurement

2. Why prices are different?

Future Procurement

Why prices are different? Future Procurement

Why prices are different?

- Different options (memory, colors… )

-Different added services(network or unlock)

-Delivery terms and conditions

-Different suppliers have different costs

-Profit expectations may vary - …

Why prices are different? Future Procurement

3. Three approaches to price setting

Future Procurement

Future Procurement

Future Procurement

Future Procurement

Future Procurement

Future Procurement

Cost based Market pricing Value based

Future Procurement

• Investigate the competitors

• Position yourself on the market

• Set the price according to market and your position

• Identify the benefits for the customers

• Quantify the benefits in money

• Set the price based on the value for the customer

• Study your costs and volumes

• Set the profit expectations

• Direct cost

+Indirect cost +Overheads

+Mark-up

=Price

Cost based Market pricing Value based

Future Procurement

4. Cost Based Pricing principles

Future Procurement

0

20

40

60

80

100

Price

Mark-up

Cost

What is the mark-up?

What is the base for mark-up?

P.S. Mark-up is not the same thing as Margin or Profit

0

20

40

60

80

100

Price

Mark-up

Cost

Future Procurement

0

20

40

60

80

100

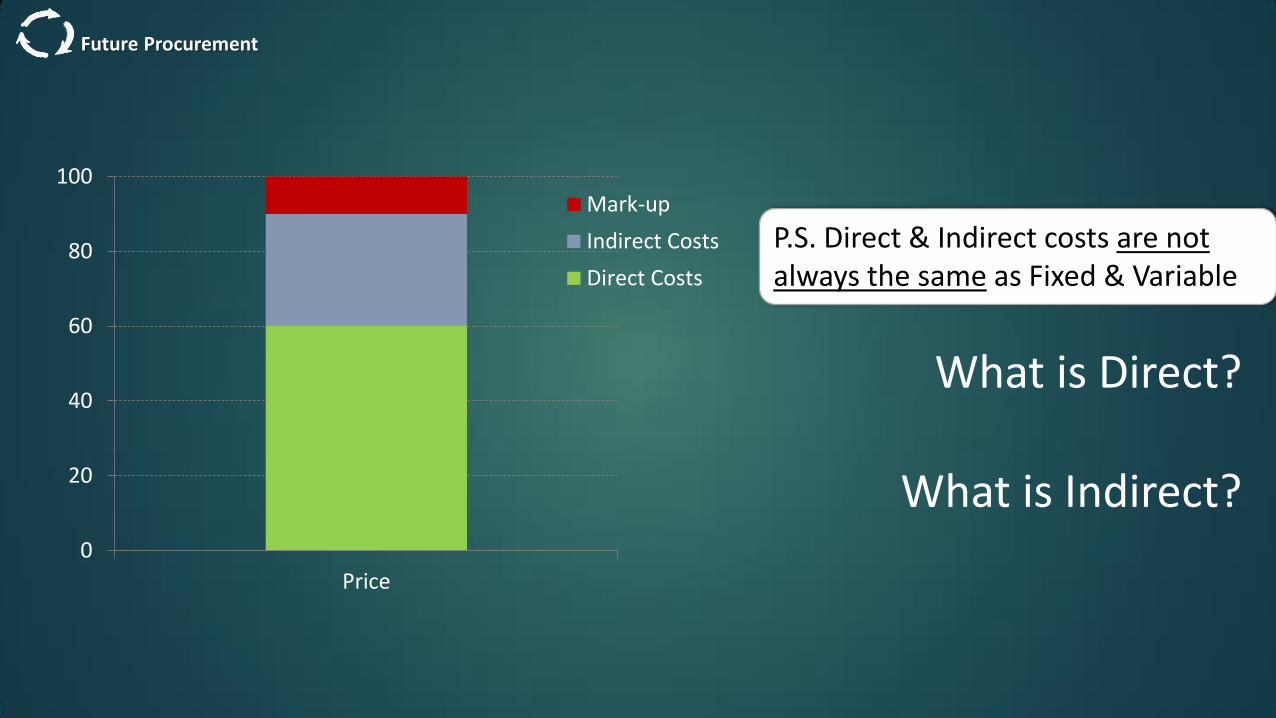

Price

Mark-up

Indirect Costs

Direct Costs

What is Direct?

What is Indirect?

P.S. Direct & Indirect costs are not always the same as Fixed & Variable

Future Procurement

0

20

40

60

80

100

Price

Mark-up

Financial costs

Depreciation

Overheads

Packaging

Energy

Labour

Material C

Material B

Material A

What are the materials involved?

What are the

processes involved?

P.S. use the accountant books to estimate the Indirect costs & Labour

Future Procurement

0

100Mark-up

Financial costs

Depreciation

Overheads

Packaging

Energy

Labour

Material C

Material B

Material A

Future Procurement

5. Getting it all together: Cost Based Pricing example

Future Procurement

Costs

Materials

Direct Indirect

Labour

Direct Indirect

Other expenses

Direct Indirect

Future Procurement

Costs of coffee to go Materials

Direct Indirect

Labour

Direct Indirect

Other expenses

Direct Indirect

Don’t forget about maintenance costs, non-quality costs…

Future Procurement

Fixed costs Variable costs

Semivariable costs

Future Procurement

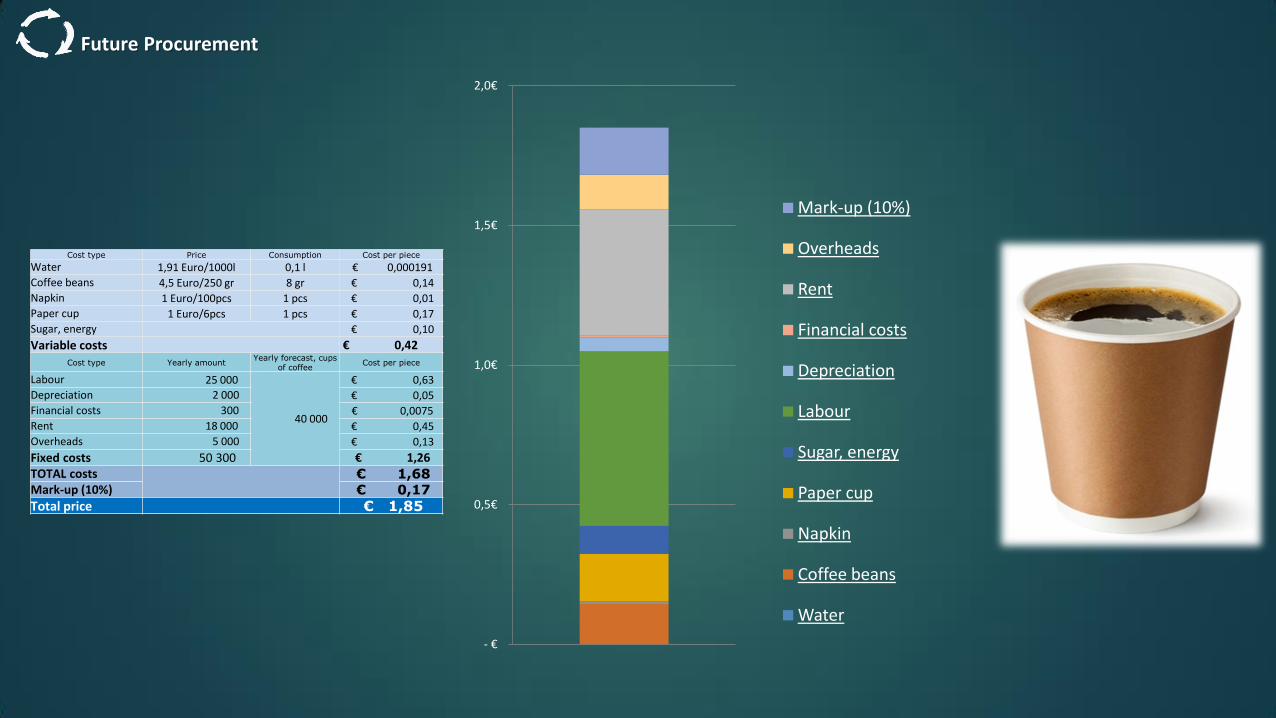

Cost type Price Consumption Cost per piece

Water 1,91 Euro/1000l 0,1 l € 0,000191 Coffee beans 4,5 Euro/250 gr 8 gr € 0,14 Napkin 1 Euro/100pcs 1 pcs € 0,01 Paper cup 1 Euro/6pcs 1 pcs € 0,17 Sugar, energy € 0,10

Variable costs € 0,42

Cost type Yearly amount Yearly forecast, cups

of coffee Cost per piece

Labour 25 000

40 000

€ 0,63 Depreciation 2 000 € 0,05 Financial costs 300 € 0,0075 Rent 18 000 € 0,45 Overheads 5 000 € 0,13

Fixed costs 50 300 € 1,26

TOTAL costs € 1,68

Mark-up (10%) € 0,17

Total price € 1,85

Future Procurement

Cost type Price Consumption Cost per piece

Water 1,91 Euro/1000l 0,1 l € 0,000191 Coffee beans 4,5 Euro/250 gr 8 gr € 0,14 Napkin 1 Euro/100pcs 1 pcs € 0,01 Paper cup 1 Euro/6pcs 1 pcs € 0,17 Sugar, energy € 0,10

Variable costs € 0,42

Cost type Yearly amount Yearly forecast, cups

of coffee Cost per piece

Labour 25 000

40 000

€ 0,63 Depreciation 2 000 € 0,05 Financial costs 300 € 0,0075 Rent 18 000 € 0,45 Overheads 5 000 € 0,13

Fixed costs 50 300 € 1,26

TOTAL costs € 1,68

Mark-up (10%) € 0,17

Total price € 1,85

Cost type Price Consumption Cost per piece

Water 1,91 Euro/1000l 0,1 l € 0,000191 Coffee beans 4,5 Euro/250 gr 8 gr € 0,14 Napkin 1 Euro/100pcs 1 pcs € 0,01 Paper cup 1 Euro/6pcs 1 pcs € 0,17 Sugar, energy € 0,10

Variable costs € 0,42

Cost type Yearly amount Yearly forecast, cups

of coffee Cost per piece

Labour 25 000

55 000

€ 0,45 Depreciation 2 000 € 0,04 Financial costs 300 € 0,0055 Rent 18 000 € 0,33 Overheads 5 000 € 0,09

Fixed costs 50 300 € 0,91

TOTAL costs € 1,34

Mark-up (10%) € 0,13

Total price € 1,47 ECONOMY OF SCALE

Future Procurement

ECONOMY OF SCALE

Cost type Price Consumption Cost per piece

Water 1,91 Euro/1000l 0,1 l € 0,000191 Coffee beans 4,5 Euro/250 gr 8 gr € 0,14 Napkin 1 Euro/100pcs 1 pcs € 0,01 Paper cup 1 Euro/6pcs 1 pcs € 0,17 Sugar, energy € 0,10

Variable costs € 0,42

Cost type Yearly amount Yearly forecast, cups

of coffee Cost per piece

Labour 25 000

40 000

€ 0,63 Depreciation 2 000 € 0,05 Financial costs 300 € 0,0075 Rent 18 000 € 0,45 Overheads 5 000 € 0,13

Fixed costs 50 300 € 1,26

TOTAL costs € 1,68

Mark-up (10%) € 0,17

Total price € 1,85

Cost type Price Consumption Cost per piece

Water 1,91 Euro/1000l 0,1 l € 0,000191 Coffee beans 4,5 Euro/250 gr 8 gr € 0,14 Napkin 1 Euro/100pcs 1 pcs € 0,01 Paper cup 1 Euro/6pcs 1 pcs € 0,17 Sugar, energy € 0,10

Variable costs € 0,42

Cost type Yearly amount Yearly forecast, cups

of coffee Cost per piece

Labour 25 000

30 000

€ 0,83 Depreciation 2 000 € 0,07 Financial costs 300 € 0,0100 Rent 18 000 € 0,60 Overheads 5 000 € 0,17

Fixed costs 50 300 € 1,68

TOTAL costs € 2,10

Mark-up (10%) € 0,21

Total price € 2,31

Future Procurement

- €

0,5€

1,0€

1,5€

2,0€

Mark-up (10%)

Overheads

Rent

Financial costs

Depreciation

Labour

Sugar, energy

Paper cup

Napkin

Coffee beans

Water

Cost type Price Consumption Cost per piece

Water 1,91 Euro/1000l 0,1 l € 0,000191

Coffee beans 4,5 Euro/250 gr 8 gr € 0,14

Napkin 1 Euro/100pcs 1 pcs € 0,01

Paper cup 1 Euro/6pcs 1 pcs € 0,17

Sugar, energy € 0,10

Variable costs € 0,42 Cost type Yearly amount

Yearly forecast, cups of coffee

Cost per piece

Labour 25 000

40 000

€ 0,63

Depreciation 2 000 € 0,05

Financial costs 300 € 0,0075

Rent 18 000 € 0,45

Overheads 5 000 € 0,13

Fixed costs 50 300 € 1,26 TOTAL costs € 1,68 Mark-up (10%) € 0,17

Total price € 1,85

Future Procurement

6. Pro’s and Cons of Cost Based Pricing

Future Procurement

Mark-up

Financial costs

Depreciation

Overheads

Packaging

Energy

Labour

Material C

Material B

Material A

+ Helps you to understand the price from the supplier perspective. + Price negotiations are more effective and fact based + You can make the modeling based on Cost Break Down, when planning the price reduction activities + Good base for building long term partnership on win-win basis

Pro’s

Future Procurement

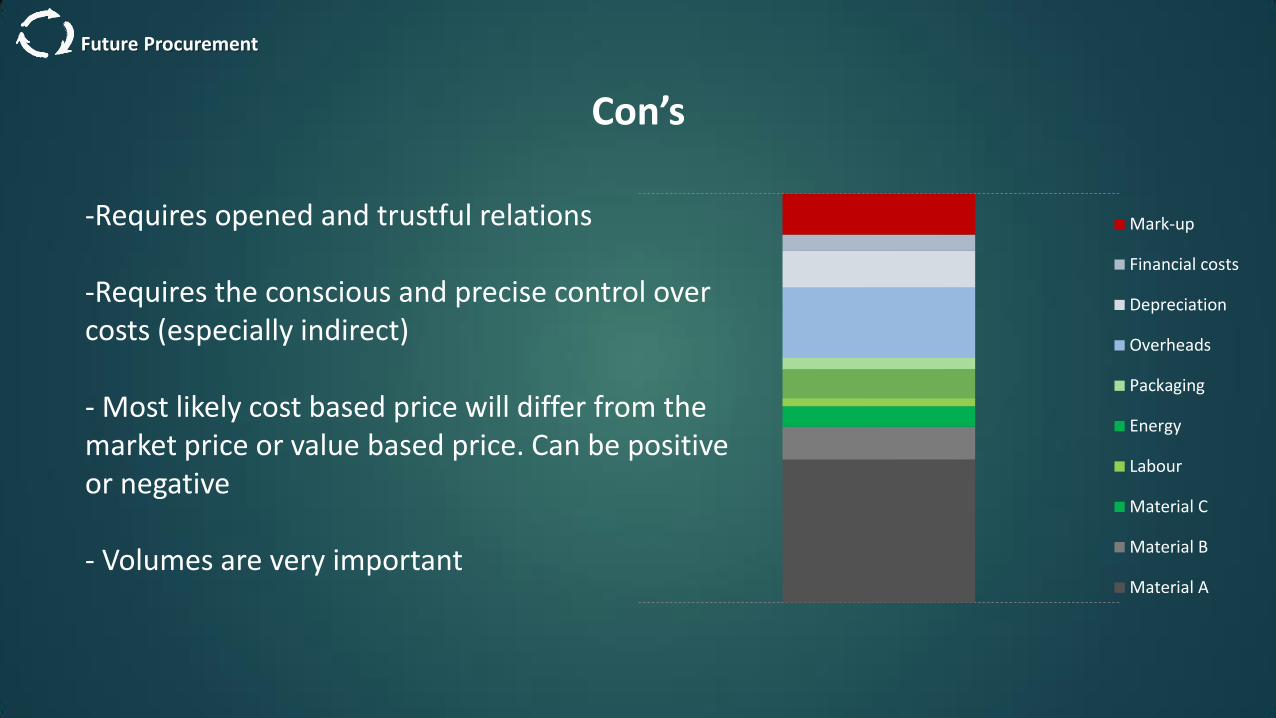

-Requires opened and trustful relations -Requires the conscious and precise control over costs (especially indirect)

- Most likely cost based price will differ from the market price or value based price. Can be positive or negative

- Volumes are very important

Con’s

Mark-up

Financial costs

Depreciation

Overheads

Packaging

Energy

Labour

Material C

Material B

Material A

Future Procurement

7. Best way to use Cost Based Pricing concept

Future Procurement

A good Cost Break Down should:

• Be simple but representative

• Be splitted into fixed and variable costs

• Take in consideration consumptions and prices

• Take in consideration ex-rates (if any)

• Include the volumes/forecasts

- €

0,5€

1,0€

1,5€

2,0€

Mark-up (10%)

Overheads

Rent

Financial costs

Depreciation

Labour

Sugar, energy

Paper cup

Napkin

Coffee beans

Water

Future Procurement

proven practices for procurement professionals

Future Procurement www.FutureProcurement.net Join us

Future Procurement